110

New (South Wales Law Deform Commission The Legal Profession BACKGDOUND PAPED ~ II 1980

New (South WalesLaw Deform Commission

The Legal Profession

BACKGDOUNDPAPED ~ II

1980

- 2 -

The Law Reform Commission is constituted by theLaw Reform Commission Act 1967. The Commissioners are -

Chairman: The Honourable Mr. Justice J.H. Wootten

DeputyChairman: Mr. R.D. Conacher

Mr. J.H.P. Disney

Mr. D. Gressier

His Honour Judge T.J. Martin, Q.C.

Mr. John Bennett is Executive Member of theC omm i s s i on.

The Secretary of the Commission is Mr. BruceBuchanan, and its offices are at 16th Level, GoodsellBuilding, 8-12 Chifley Square, Sydney, N.S.W. 2001.

- 3 -

PREFACEThe Commission has a reference from the Attorney

General and Minister for Justice, the Honourable F.J.Walker, LL.M., M.P., to inquire into and review the lawand practice relating to the legal profession. The termsof reference are set out in Appendix I to our Legal Profes-sion Inquiry Discussion Paper No. 1 - General Regulation.

This Paper is intended to complement the DiscussionPaper No.3 on Professional Indemnity Insurance, which wehave issued in the course of our Legal Profession Inquiry.It contains material which we consider particularly usefulto a consideration of the issues raised in that Paper butwhich would not otherwise be readily accessible to mostreaders. It is not intended to be an exhaustive or compre-hensive compilation of material used in the preparation ofthe Discussion Paper.

Several current indemnity insurance policies forlawyers were reproduced in Appendices to the DiscussionPaper. In this Background Paper we include several poli-cies from other jurisdictions, the terms of which differsignificantly from those in the Appendices.

This Paper also includes statistical informationobtained by the Commission from bodies responsible for themanagement of indemnity insurance schemes for lawyers inNew South Wales, Victoria and England. In some instanceswe have compiled tables based on these statistics, in orderto illustrate specific aspects of claims experience.

The Commission's bibliographical files contain aconsiderable amount of material relating to professionalindemnity insurance. Much of this material, and othermaterial relating to our Legal Profession Inquiry, is read-ily available for perusal in the Commission's publicreading room.

Correspondence concerning our Legal ProfessionInquiry should be addressed to Mr. Bruce Buchanan,Secretary, New South Wales Law Reform Commission, Box 6,G.P.O., Sydney, 2001. Telephone 238-7213.

- 4 -

LEGAL PROFESSION INQUIRY

PUBLICATIONS

Discussion Papers

1. General Regulation.

2. Complaints, Discipline and Professional StandardsPart I.

3. Professional Indemnity Insurance.

Background Papers

1. Background Paper - I.

2. Background Paper - II.

ERRATA

CONTENTS (page 5) should read:-

"B. Victoria 93

C. England 94

PART 3. WAIVERS 104."

- 5 -

CONTENTS

PAGE

PREFACE 3

LEGAL PROFESSION INQUIRY PUBLICATIONS 4

PART 1. SELECTED INDEMNITY INSURANCE POLICIESFOR LAWYERS 6

A. England 7

B. Scotland 17

C. Ontario 32

D. Victorian Legal Advice Centres 44

PART 2. STATISTICAL INFORMATION ON SELECTEDSCHEMES 50

List of Tables in Part 2 51

A. New South Wales (Voluntary) 53

B. Victoria 104

C. England 105

PART 3. WAIVERS 115

Part 1

Indemnity InsurancePolicies

forLawyers

- 7 -

A. EnglandThe compulsory indemnity insurance scheme for

English solicitors commenced on 1st September, 1976. Itprovided the model for the schemes now operating inVictoria and Queensland, and for other proposed schemeselsewhere in Australia. The English scheme is therefore animportant point of reference in considering the type ofcompulsory indemnity insurance which should be introducedin New South Wales. The English Master Policy and Certifi-cate of insurance are broadly similar to their Victoriancounterparts which appear in Appendix III to our DiscussionPaper, Professional Indemnity Insurance. They do howeverdiffer in points of detail. Furthermore, some importantadditions have been made to the English Master Policy sincethe commencement of the scheme, in the light of actualclaims experience. These concern the variation of individ-ual premiums to reflect the claims history of each prac-tice, and the imposition of a premium loading on InnerLondon Practices. No comparable provisions have yet beenincorporated into Australian schemes.

The wording of the 1979-80 Master Policy andCertificate of Insurance for English solicitors is as fol-lows .

1. Master Policy

1. The Insurers agree with The Law Society on behalf ofall solicitors from time to time required to be insured byIndemnity Rules made under s.37 of the Solicitors' Act1974, and on behalf of former solicitors, to provide suchinsurance in accordance with the terms of the Certificateattached hereto. Subject as hereinafter appears in respectof former solicitors, such Certificate will be issued annu-ally on request on receipt of the premium payable inaccordance with Clauses 2 and 3 hereof.

2. This Policy commences on the 1st day of September1979. This Policy can be extended for successive periodsof one year on each 1st day of September subject to therates of premium for each renewal being agreed by the In-surers and The Law Society at least six months before suchrenewal. In the event of any failure so to agree suchrates of renewal premium all cover under this Policy shallcease on the 31st August 1980 or (if later) on the expiryof the period for which the Policy was last extended.

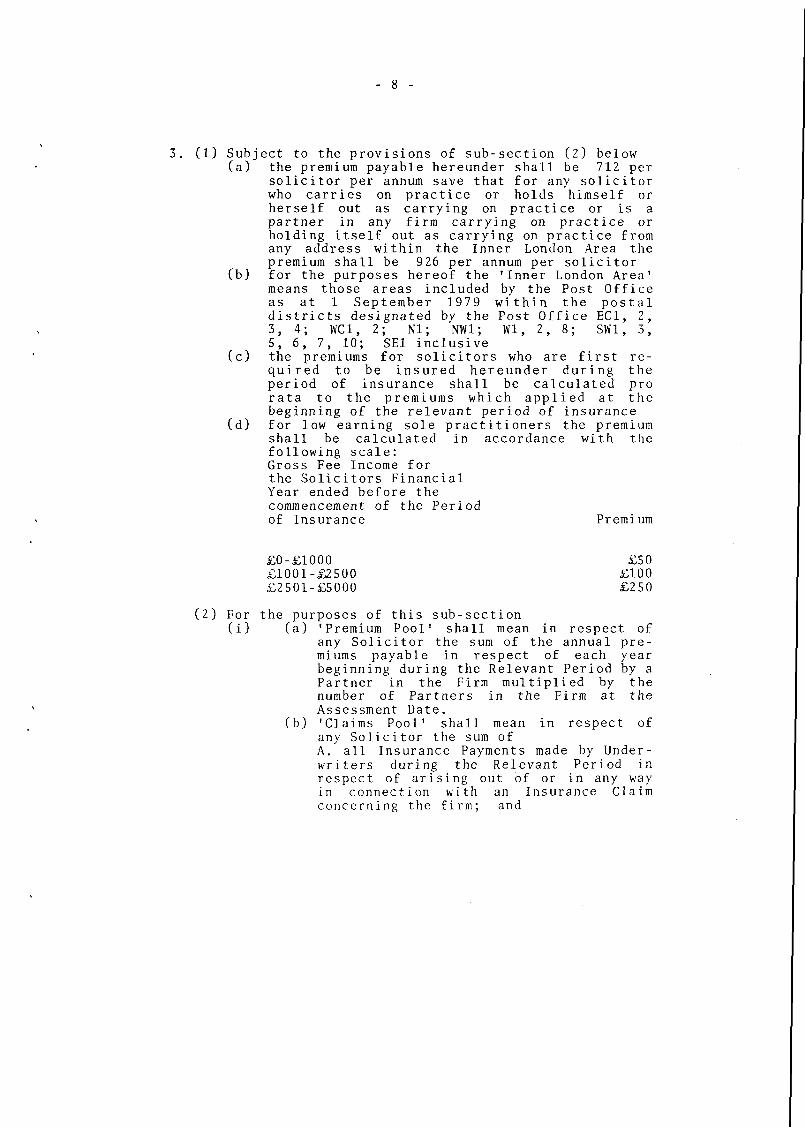

(1) Subject to the provisions of sub-section (2) below(a) the premium payable hereunder shall be 712 per

solicitor per annum save that for any solicitorwho carries on practice or holds himself orherself out as carrying on practice or is apartner in any firm carrying on practice orholding itself out as carrying on practice fromany address within the Inner London Area thepremium shall be 926 per annum per solicitor

(b) for the purposes hereof the 'Inner London Area'means those areas included by the Post Officeas at 1 September 1979 within the postaldistricts designated by the Post Office EC1, 2,3, 4; WC1, 2; Ml; NW1; Wl, 2, 8; SW1, 3,5, 6, 7, 10; SE1 inclusive

(c) the premiums for solicitors who are first re-quired to be insured hereunder during theperiod of insurance shall be calculated prorata to the premiums which applied at thebeginning of the relevant period of insurance

(d) for low earning sole practitioners the premiumshall be calculated in accordance with thefollowing scale:Gross Fee Income forthe Solicitors FinancialYear ended before thecommencement of the Periodof Insurance Premium

£0-£1000 £50£1001-£2500 £100£2501-£5000 £250

(2) For the purposes of this sub-section(i) (a) 'Premium Pool' shall mean in respect of

any Solicitor the sum of the annual pre-miums payable in respect of each yearbeginning during the Relevant Period by aPartner in the Firm multiplied by thenumber of Partners in the Firm at theAssessment Date.

(b) 'Claims Pool' shall mean in respect ofany Solicitor the sum ofA. all Insurance Payments made by Under-writers during the Relevant Period inrespect of arising out of or in any wayin connection with an Insurance Claimconcerning the firm; and

- 9 -

B. the Due Proportion of all InsurancePayments made by Underwriters during theRelevant Period in respect of arising outof or in any way in connection with anInsurance Claim concerning any FormerFirm.

(c) The 'Relevant Period' shall mean theperiod of 3 years ending on the Assess-ment Date.

(d) The 'Assessment Date' shall mean the 31stMarch 1979 or (in the case of any renewalof this Master Policy) the 31st Marchimmediately preceding the Renewal Date.

(e) 'Insurance Payments' shall include allpayments of whatsoever sort made byUnderwriters including but not limited topayments made in respect of claimantsdamages and costs save and except that noaccount shall be taken of sums paid byUnderwriters n respect of the costs ofinvestigating or defending an InsuranceClaim.

(f) 'Insurance Claim1 shall include anyclaims of whatsoever sort whether madethreatened intimated apprehended formu-lated or not in respect of which (ifproved) Underwriters would be liable togrant indemnity under the Certificate.

(g) 'Firm' shall include in the case of anyamalgamation between or merger of two ormore firms previously carrying on thepractice of practising as a solicitoreach such firm.

(h) 'Former Firm' shall mean a firm whichduring the Relevant Period carried on thepractice of practising as a solicitor andwhich prior to the Assessment Date ceasedso to practise otherwise than by amalga-mation or merger with another firm and inwhich at the Cessation Date there was aCessation Partner.

(i) 'Cessation Date' shall mean the date whena Former Firm ceases to practise.

(j) 'Cessation Partner' shall mean a Partnerin the Firm at the Assessment Date whowas a partner in the Former Firm at theCessation Date.

- 10 -

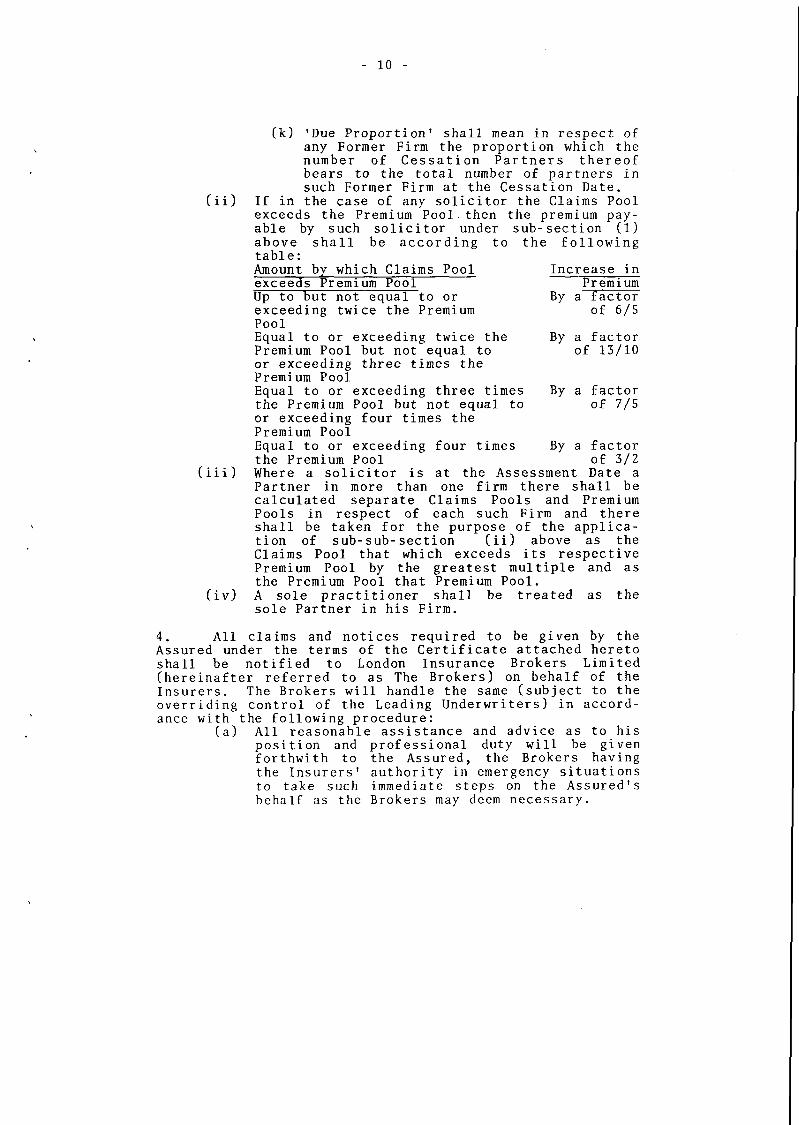

(k) 'Due Proportion' shall mean in respect ofany Former Firm the proportion which thenumber of Cessation Partners thereofbears to the total number of partners insuch Former Firm at the Cessation Date,

(ii) If in the case of any solicitor the Claims Poolexceeds the Premium Pool then the premium pay-able by such solicitor under sub-section (1)above shall be according to the followingtable:Amount by which Claims Pool Increase inexceeds Premium P o o l P r e m i u mUp to but not equal to or By a factorexceeding twice the Premium of 6/5PoolEqual to or exceeding twice the By a factorPremium Pool but not equal to of 13/10or exceeding three times thePremium PoolEqual to or exceeding three times By a factorthe Premium Pool but not equal to of 7/5or exceeding four times thePremium PoolEqual to or exceeding four times By a factorthe Premium Pool of 3/2

(iii) Where a solicitor is at the Assessment Date aPartner in more than one firm there shall becalculated separate Claims Pools and PremiumPools in respect of each such Firm and thereshall be taken for the purpose of the applica-tion of sub-sub-section (ii) above as theClaims Pool that which exceeds its respectivePremium Pool by the greatest multiple and asthe Premium Pool that Premium Pool.

(iv) A sole practitioner shall be treated as thesole Partner in his Firm.

4. All claims and notices required to be given by theAssured under the terms of the Certificate attached heretoshall be notified to London Insurance Brokers Limited(hereinafter referred to as The Brokers) on behalf of theInsurers. The Brokers will handle the same (subject to theoverriding control of the Leading Underwriters) in accord-ance with the following procedure:

(a) All reasonable assistance and advice as to hisposition and professional duty will be givenforthwith to the Assured, the Brokers havingthe Insurers' authority in emergency situationsto take such immediate steps on the Assured'sbehalf as the Brokers may deem necessary.

- 11 -

(b) As soon as practicable brief details (in a formto be agreed with the Leading Underwriters)shall be reported to the Leading Underwritersand further reports will be submitted as andwhen required by the Insurers.

(c) Except in case of urgency the Brokers will notinstruct solicitors or other expert adviserswithout first obtaining the Leading Under-writers ' authority, it being understood that theInsurers will not unreasonably withhold suchapproval in any case where the Assured or theBrokers consider this step to be advisable.Where solicitors are so employed their fees andexpenses will be for the account of the Insur-ers who may require the solicitors' reports tobe submitted directly to them.

(d) A Panel of solicitors to handle claims shall beagreed between The Law Society and theInsurers.

(e) In handing claims and potential claims againstthe Assured, the Brokers shall act as agentsfor the Assured and, subject to such disclosureas may be necessary to the Insurers or asrequired by them in accordance with the termsof this Policy and the attached Certificate,shall be under a duty of confidence to theAssured; and in particular neither the Brokersnor the Insurers shall disclose informationabout any individual or firm to The Law Societywithout his or their consent.

5. In respect of former solicitors (which expression inthis Policy and in the Certificate attached hereto shallinclude solicitors who have ceased by reason of death,retirement or otherwise, to practise as principals in pri-vate practice, and their personal representatives) certifi-cates need not be issued and no premium shall be payable.A former solicitor who has at any time been insured under(or whose successors in practice have at any time beeninsured under) this Master Policy or a previous MasterPolicy issued pursuant to the Solicitors Indemnity Rules1975 or 1978 shall be entitled to be indemnified by theInsurers in respect of any claim or claims first madeagainst him during the currency of this Policy, as if aCertificate in the terms attached hereto had been issuedto him hereunder and as if there were specified in theSchedule to such Certificate (a) as the Period of Insurancethe period during which this Policy shall be in force, and(b) as the Sum Insured the sum of £50,000, if he was prac-tising alone immediately before he ceased so to practise,

- 12 -

and, in any other case, the sum of £30,000 multiplied bythe number of partners immediately before he ceased so topractise in the partnership in which he last so practised.

6. Authority is hereby given by the Insurers to theBrokers to issue on behalf of the Insurers to solicitorsseeking insurance in accordance with Clause 1 hereofcertificates in the form attached hereto.

7. Expressions used in this Policy have the meaningsgiven to them by the Certificate attached hereto.

8. For the payment of an additional premium to bedetermined by the Leading Underwriters the terms of anyCertificate issued hereunder may be extended by endorse-ment .

2. Certificate of InsuranceThis is to certify that in accordance with the

authorisation granted to the undersigned under the MasterPolicy referred to in the Schedule by the Insurers sub-scribing such Master Policy (hereinafter called 'TheInsurers') insurance is granted by the Insurers in accord-ance with the terms and conditions following, and in con-ideration of the payment of the premium stated in the

Schedule.

1. INTERPRETATION

(a) 'The Solicitor1 means the person named as such inthe Schedule.

(b) 'The Assured' means the Solicitor, any personemployed in connection with the Practice (includingany articled clerk, and any solicitor who is aConsultant or Associate in the Firm), and the estateand/or the legal representatives of any of the fore-going, to the intent that each of the foregoingshall be severally insured hereunder.

(c) 'The Practice' means the practice of practising as asolicitor (including the acceptance of obligationsas trustee) undertaken by the Solicitor or hispredecessors in private practice alone or withothers, provided always that wherever any fees orother income accrue therefrom they inure to thebenefit of that practice.

- 13 -

(d) Private practice does not include practice by theSolicitor in the course of or in connection with orin relation to his employment under a contract ofservice by an employer not also a solicitor in pri-vate practice.

(e) 'The Period of Insurance' means the period specifiedin the Schedule.

(f) 'The Firm' means the firm as from time to time con-stituted carrying on the Practice.

(g) 'Partner' includes any solicitor held out by theFirm as a partner in the Firm.

2. INSURING CLAUSES

(a) On the terms and conditions herein contained theInsurers shall indemnify the Assured against allloss to the Assured whensoever occurring arisingfrom any claim or claims first made against theAssured or the Firm during the Period of insurancein respect of any description of civil liabilitywhatsoever incurred in connection with the Practice.Such indemnity as aforesaid shall not extend toindemnify the solicitor in respect of any undertak-ing given by or on behalf of the solicitor to anyperson in connection with the provision of financeproperty assistance or other advantage whatsoever toor for the benefit of the solicitor or any partnerthe solicitor's or any partner's spouse or childrenor any business firm company enterprise associationor venture owned or controlled by the solicitor orany partner whether alone or in concert with others.

(b) The liability of the Insurers under this Certificateand any other Certificate issued under the MasterPolicy shall not exceed in respect of each suchclaim and claimants' costs the sum insured specifiedin the Schedule and in addition all costs and ex-penses incurred with the Insurers' consent (suchconsent not to be unreasonably withheld) in thedefence or settlement of any such claim, providedthat if a payment in excess of the said sum insuredis made to dispose of any such claim the Insurers'liability for any such costs and expenses so incur-red shall be limited to such proportion thereof asthe said sum insured bears to the amount of the pay-ment so made.

(c) For the purposes hereof all claims against theAssured or the Firm arising from the same act oromission shall be regarded as one claim.

- 14 -

3. SPECIAL CONDITIONS.

(a) Subject to General condition (f) the Insurers willnot seek to avoid, repudiate or rescind this insur-ance upon any ground whatsoever, including inparticular non-disclosure or misrepresentation.

(b) Where the Assured1s breach of or non-compliance withany condition of this insurance has resulted insubstantial prejudice to the handling or settlementof any claim against the Assured or the Firm inrespect of which the Assured is insured hereunderthe Assured shall reimburse to the Insurers the dif-ference between the sum payable by the Insurers inrespect of that claim and the sum which would havebeen payable in the absence of such prejudice.Provided always that it shall be a condition prece-dent of the right of the Insurers to seek suchreimbursement that they shall have fully indemnifiedthe Assured in accordance with the terms hereof.

(c) (i) For the purposes of this paragraph 'the rele-vant date' means the date when a claim thesubject of the Insuring Clauses hereof is firstmade against the Assured or the date, if earli-er, when circumstances which may give risethereto first come to the notice of the Solici-tor or of any solicitor or former solicitor(including the personal representatives of anysuch solicitor or former solicitor) liable withthe Solicitor in respect of thereof.

(ii) If on the relevant date the Solicitor is prac-tising as a solicitor in partnership with oneor more solicitors, or is a partner in morethan one such partnership, the Schedule shall,subject to (iii) below, be deemed to specify asthe Sum Insured in respect of that claim, anamount of £30,000 multiplied by the number inpartnerhip or in the largest such partnership(measured by the number of partners who aremembers thereof) on the relevant date or on the1st September preceding that date, whichevernumber is greatest.

(iii) If on the relevant date one or more solicitorswho are liable to the claimant are practisingas solicitors in partnership but there is nosuch partnership of which all of them are mem-bers the Schedule shall be deemed to specify asthe Sum Insured in respect of that claim anamount of £30,000 multiplied by the number ofpartners in the largest partnership (measuredas aforesaid) in which any such solicitor is

- 15 -

practising on that date or on the 1st Septemberpreceding that date, whichever number isgreater.

(iv) The number by which the amount of £30,000 fallsto be multiplied under (ii) or (iii) above isherein called 'the multiplier'.

(d) This insurance shall extend to indemnify the Assuredup to the Sum Insured calculated as above in respectof any loss arising from any claim or claims firstmade against the Assured or the Firm during thePeriod of Insurance arising out of any dishonest orfraudulent act or omission of any past or presentPartner in the Firm (not being the Solicitor him-self). Provided always that:(i) at the request of the Insurers the Assured

shall take or procure to be taken by the Firmat the Insurers' expense all reasonable stepsto obtain reimbursement from any partner orformer partner concerned in such dishonesty orfraud, or from the legal representatives of anysuch partner or former partner, and

(ii) the Assured shall procure that any reimburse-ment so obtained together with any monies whichbut for such fraud or dishonesty would be dueto such partner or former partner from the Firmshall be paid to the Insurers up to but notexceeding the amounts paid by the Insurers inrespect of such claim together with any expend-iture reasonably incurred by the Insurers inobtaining such reimbursement.

4. GENERAL CONDITIONS.

(a) (i) Neither the Assured nor the Firm shall admitliability for, or settle, any claim fallingwithin the Insuring Clauses hereof or incur anycosts or expenses in connection therewith with-out the consent of the Insurers (such consentnot to be unreasonably withheld) and subject to(ii) below the Assured shall procure that theInsurers shall be entitled at their own expenseat any time to take over the conduct in thename of the Assured or the Firm of the defenceor settlement of any such claim.

(ii) Neither the Assured nor the Firm nor the insur-ers shall be required to contest any legalproceedings unless a Queen's Counsel (to bemutually agreed upon by the Assured and theInsurers or failing agreement to be appointed

- 16 -

by the President of The Law Society for thetime being) shall advise that such proceedingsshould be contested.

(b) The Assured shall procure that notice to the Insur-ers shall be given in writing as soon as practicableof any claims the subject of the Insuring Clauseshereof made during the Period of Insurance againstthe Assured or the firm or of the receipt by eitherof them of notice from any person of any intentionto make a claim against them. The Assured may alsogive notice in writing to the Insurers of any cir-cumstances of which the Assured shall become awareduring the period of Insurance which may give riseto such a claim. If notice is given to the Insurersunder this paragraph any claim subsequently made(whether before or after the expiration of thePeriod of Insurance) pursuant to such an intentionto claim or arising from circumstances so notifiedshall be deemed to have been made at the date whensuch notice was given.

(c) The Insurers waive any rights of subrogation againstany employee of the Assured save where those rightsarise in connection with a dishonest or criminal actby that employee.

(d) Notices to the Insurers to be given hereunder shallbe deemed to be properly made if given to LondonInsurance Brokers Limited.

(e) Save as provided in General Condition (a)(ii) aboveany dispute or disagreement between the Assured andthe Insurers arising out of or in connection withthis insurance shall at the request of either ofthem be referred to the sole arbitrament of a personto be appointed (failing agreement between them) bythe President of The Law Society for the time beingwhose decision shall be final and binding upon bothparties.

(f) If the Assured shall prefer any claim hereunderknowing the same to be false or fraudulent asregards amount or otherwise this insurance shallbecome void and all claims hereunder shall beforfeited.

5. GENERAL EXCLUSIONS.

(a) This insurance shall not indemnify the Assured inrespect of the first £400 of any one claim or (inthe case of any claim to which Special Condition (c)applies) the first £400 multiplied by the Multipli-er .

- 17 -

(b) This insurance shall not indemnify the Assured inrespect of any loss arising out of any claim:(i) for death, bodily injury, physical loss or

physical damage to property of any kind whatso-ever (other than property in the care, custodyand control of the Assured or the Firm in con-nection with the Practice for which they areresponsible, not being property occupied orused by them for the purposes of the Practice);

(ii) for the payment of a trading debt incurred bythe Assured or the Firm;

(iii) in respect of any circumstances or occurrencewhich has been notified under any other insur-ance attaching prior to the inception of thisCertificate;

(iv) in respect of his own dishonest or fraudulentact or omission;

(v) directly or indirectly caused by or contributedto by or arising from ionising radiations orcontamination by radioactivity from any nuclearfuel or from any nuclear waste from combustionof nuclear fuel, the radioactive toxic explo-sive or other hazardous properties of anyexplosive nuclear assembly or nuclear componenttherof; directly occasioned by pressure wavescaused by aircraft or other aerial devicestravelling at sonic or supersonic speeds, orfrom war, invasion, acts of foreign enemies,hostilities (whether war be declared or not),civil war, rebellion, revolution, insurrection,military or usurped power.

(vi) in respect of any liability incurred in connec-tion with a practice wholly outside England andWales.

B. ScotlandScotland is the only comparable jurisdiction to New

South Wales, with a separate Bar, which has compulsoryschemes in force for each branch of the profession. Someof the features of the barristers' scheme operated by theFaculty of Advocates are referred to in our DiscussionPaper, Professional Indemnity Insurance. However, theFaculty has indicated to the Commission that it could notapprove publication of the terms of the Advocates' polic yin this Background Paper.

- 18 -

The compulsory Master Policy scheme for Scottishsolicitors, operated by the Law Society of Scotland, com-menced on 1st February 1978. The Scottish scheme differsfrom the existing English and Australian schemes in severalrespects, including the amount of cover, definition of thescope of cover, and premium setting (including the imposi-tion of premium loadings).

The wording of the current Master Policy andCertificate of Insurance is as follows.

1. Master Policy

1. INTERPRETATION

In this Policy unless the context otherwise re-quires : -

"Brokers" shall mean the Brokers fromtime to time appointed by theCouncil of the Society to acton behalf of the Society andits members in relation tothis Policy.

"Insured" shall mean the Insured as de-fined in the Certificates tobe issued in terms of thisPolicy.

"Insurers" shall mean the Insurers whofrom time to time are provid-ing cover under this Policy.

"Leading Insurer" shall mean the Insurer firstnamed in the said Certifi-cates .

"Practice Unit" means where the practice iscarried on by a sole practi-tioner that practitioner andwhere the practice is carriedon in partnership that part-nership.

"the Society" means the Law Society ofScotland established under theSolicitors (Scotland) Act1949.

- 19 -

2. INSURANCE

The Insurers agree with the Society on behalf of allsolicitors from time to time required to be insured by theSolicitors' (Scotland) professional Indemnity InsuranceRules 1977 and on behalf of former solicitors hereinafterreferred to to provide insurance in accordance with theterms of the Certificate attached hereto. Subject as here-inafter appears in respect of former solicitors the Certif-icate will be issued to each Practice Unit in respect ofeach practice year or part thereof (as the case may be) onrequest on payment of the appropriate premium.

3. DURATION

This Policy commences on 1st February 1978 for theperiod from that date to 31st October 1979 and shall con-tinue yearly thereafter from 1st November each year untilterminated in terms hereof.

4. PREMIUMS

(a) The premiums payable hereunder by each Practice Unitshall be in accordance with the Schedules of annualpremiums agreed for the period concerned between theSociety and the Insurers, copies of the Schedulesrelative to the period from the date of commencementof this Policy to 31st October 1979 having beensigned by the Society and the Leading Insurer anddeposited with the Society, the premiums thereinbeing based on the number of principals and em-ployees (as defined in the Certificate) in eachPractice Unit as at the date of the relevant propos-al.

(b) Notwithstanding (a) above the Insurers in consulta-tion with the Brokers shall be entitled in appropri-ate cases to load the premium for any Practice Unitbut so that any such loading shall not exceed 1501of the premium which would have been otherwise pay-able. Any Practice Unit whose premium is loaded interms hereof shall have the right to appeal againstsuch loading.

(c) For the purpose of dealing with appeals under para-graph (b) above there shall be formed a committeewhich shall meet in Scotland and comprise two mem-bers nominated by the Leading Insurers, two membersnominated by the Society, and one member nominatedby the Brokers. The members nominated shall not be

- 20 -

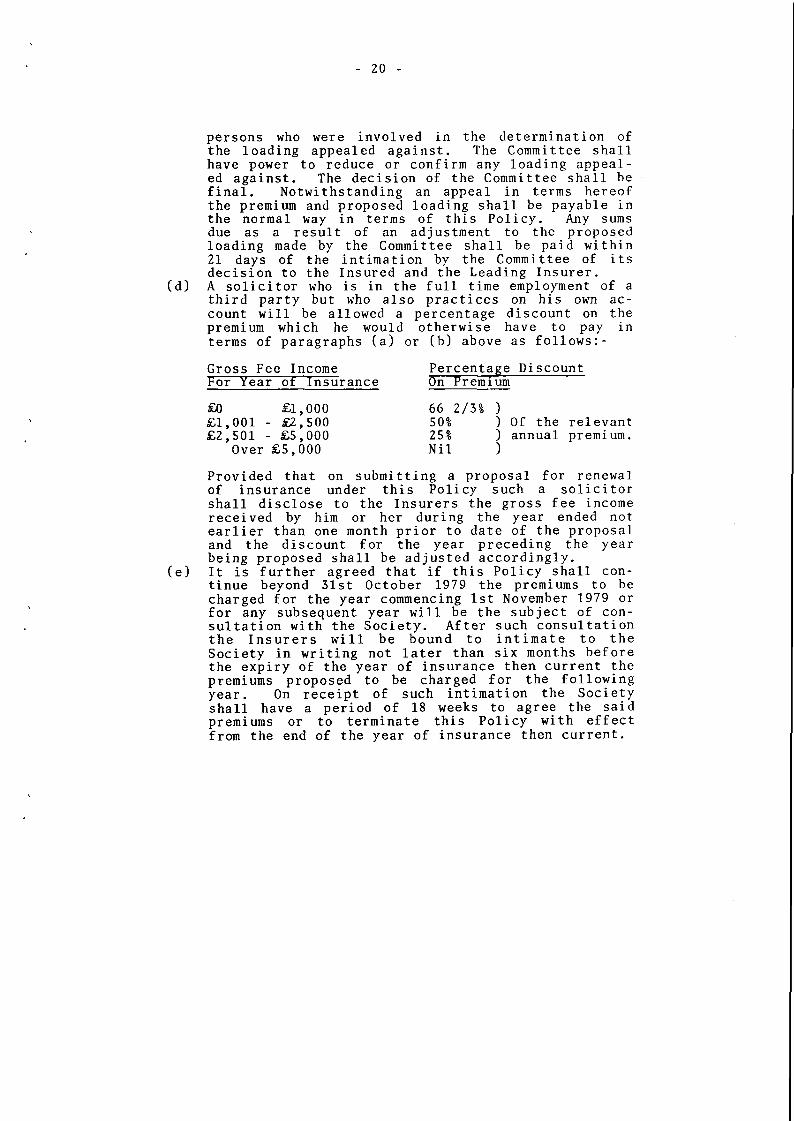

persons who were involved in the determination ofthe loading appealed against. The Committee shallhave power to reduce or confirm any loading appeal-ed against. The decision of the Committee shall befinal. Notwithstanding an appeal in terms hereofthe premium and proposed loading shall be payable inthe normal way in terms of this Policy. Any sumsdue as a result of an adjustment to the proposedloading made by the Committee shall be paid within21 days of the intimation by the Committee of itsdecision to the Insured and the Leading Insurer.

(d) A solicitor who is in the full time employment of athird party but who also practices on his own ac-count will be allowed a percentage discount on thepremium which he would otherwise have to pay interms of paragraphs (a) or (b) above as follows:-

Gross Fee Income Percentage DiscountFor Year of Insurance On Premium

£0 £1,000 66 2/3% )£1,001 - £2,500 501 ) Of the relevant£2,501 - £5,000 25% ) annual premium.

Over £5,000 Nil )

Provided that on submitting a proposal for renewalof insurance under this Policy such a solicitorshall disclose to the Insurers the gross fee incomereceived by him or her during the year ended notearlier than one month prior to date of the proposaland the discount for the year preceding the yearbeing proposed shall be adjusted accordingly.

(e) It is further agreed that if this Policy shall con-tinue beyond 31st October 1979 the premiums to becharged for the year commencing 1st November 1979 orfor any subsequent year will be the subject of con-sultation with the Society. After such consultationthe Insurers will be bound to intimate to theSociety in writing not later than six months beforethe expiry of the year of insurance then current thepremiums proposed to be charged for the followingyear. On receipt of such intimation the Societyshall have a period of 18 weeks to agree the saidpremiums or to terminate this Policy with effectfrom the end of the year of insurance then current.

- 21 -

5. LIMITS OF INDEMNITY AND SELF-INSURED AMOUNTS

Unless otherwise agreed the premiums shall relate tothe following limits of indemnity and self-insured amounts,namely

(A) Limits of Indemnity

Sole Practitioner £75,000 each and every claim.

Solicitors in For each partnership £50,000Partnership each and every claim multi-

plied by the number of part-ners as at the date of com-mencement of cover or at 1stNovember in each year ofinsurance as the case may bewith an upper limit in respectof any partnership of

£500,000.(B) Self-Insured Amount

Sole Practitioner £500 each and every claim.

Solicitors in For each partnership £500 eachPartnership and every claim multiplied by

the number of partners as atthe date of commencement ofcover or as at 1st November ineach year of insurance as thecase may be with an upperlimit in respect of any part-nership of £5,000.

6. ALTERATIONS IN PRACTICE UNITS

(i) In the event of any change in a Practice Unit duringany period of insurance by reason of the death, re-tiral (from practice as a solicitor or for thepurpose of becoming a consultant to that PracticeUnit) or suspension of a partner or partners, or,the assumption of a partner or partners (being asolicitor of solicitors not previously insured underthis Policy) there shall be no alteration in premi-um, current limits of indemnity or self-insuredamount relating to the partnership in question butany new partner or partners will nevertheless beinsured under this Policy and the Certificate thencurrent. The foregoing shall not however, precludethe limit of indemnity and self-insured amounts be-

- 22 -

ing increased to the limits prescribed in thibPolicy on the assumption of a partner or partners onpayment of the appropriate premium and completion ofa new proposal form.

(ii) In the event of any change in a Practice Unit duringany period of insurance by reason of: -(a) The withdrawal from the partnership of a part-

ner who remains in practice other than as aconsultant.

(b) The assumption into a Practice Unit of, or theformation of a new Practice Unit or Units byany solicitor or solicitors who is/are at thattime insured hereunder.

the limit or limits of indemnity and self-insured amount oramounts as from the date of the change or changes shallwithout adjustment of premium be held to be those whichwould have been applicable had the change or changes takenplace immediately prior to the commencement of the periodof insurance and a Certificate or Certificates to thateffect issued; Provided always that where the new PracticeUnit or Units comprise a sole practitioner the limit ofindemnity until the next renewal date shall be £50,000.

7. TERMINATION

In addition to their right to terminate this Policyin terms of Clause 4 (e) hereof the Society shall be enti-tled to terminate this Policy on 31 October 1979 or on theexpiry of any period of insurance thereafter on giving tothe Leading Insurer not less than six months prior writtennotice of their intention to do so. The Insurers shall beentitled to terminate this Policy at any time on or afterthe said 31st October 1979 on giving to the Society notless than nine months prior written notice of their inten-tion to do so.

8. Before taking out insurance under this Policy priorto 1st November 1978 or taking out or renewing cover on orafter that date each practice Unit shall be bound to submitto the Brokers a proposal in terms of the form thereof at-tached hereto or in such other form as may from time totime be agreed between the Leading Insurer and the Societyand that no later than 30 days before the insurance isrequired and to provide the Insurers with such other in-formation as they may require.

- 23 -

9. CLAIMS

All claims and notices required to be given by theInsured under the terms of the Certificate attached heretoshall be notified to the Brokers who will in turn advisethe Insurers.

(a) A panel of solicitors to handle claims as requiredby the Leading Insurer shall be agreed between theSociety and the Insurers.

(b) The Brokers and the Insurers shall be under a dutyof confidence to the Insured; and in particularneither the Brokers nor the Insurers shall discloseinformation which would enable the Society to iden-tify any individual or Practice Unit without his ortheir consent.

10. FORMER SOLICITORS

In respect of former solicitors as described below(which expression in this Policy shall mean solicitors whohave ceased to practise as principals in private practice,and their personal representatives) Certificates need notbe issued and no premium shall be payable. A former solic-itor who has at any time been insured hereunder or whosesuccessors in business have at any time been insured here-under shall be entitled to be indemnified by the Insurersin respect of any claim or claims made against him or heras if a Certificate in the terms attached hereto had beenissued to him or her hereunder and as if there were speci-fied in the Schedule to such Certificate (a) as the periodof insurance the period during which this Policy shall bein force, and (b) as the limit of indemnity £75,000 foreach and every claim if the former solicitor was practis-ing alone immediately before he or she ceased so to prac-tise, and in any other case the sum of £50,000 for each andevery claim multiplied by the number of members in thepartnership in which the former solicitor practised immedi-ately before he or she ceased so to practise with an upperlimit in respect of any partnership of £500,000.

11. CERTIFICATES

Authority is hereby given by the Insurers to theBrokers to issue on behalf of the Insurers Certificates inthe form attached hereto.

- 24 -

12. EXTENSION OF COVER

For the payment of an additional premium to bedetermined by the Insurers the cover under any Certificateissued hereunder may be extended by endorsement.

13. TRANSITIONAL PROVISIONS

In the event of the cover and/or Limit of indemnityprovided by an existing policy of a solicitor which willexpire between 1st November 1978 and 31st January 1979(hereinafter called the "Existing Policy") being less thanthat provided by this Policy this Policy (subject to theappropriate self-insured amount) shall (without payment ofpremium) apply to the risks in addition to and amount ofindemnity in excess of the cover provided by the ExistingPolicy. Provided that no claim shall be payable under thisclause unless the insurers of the Existing Policy areliable to pay the full amounts available under their policyor policies. For the purpose of this clause the expression"Existing Policy" shall mean not only the primary policyheld by a member of the Society but also any excess layerpolicy or policies.

14. This Policy shall be governed and interpretedaccording to Scots Law.

2. Certificate of InsuranceThis is to certify that in accordance with the

authorisation granted to the Brokers (named in the Schedulehereto) under the Master Policy being Policy Number947Y031750 of Sun Alliance and London Insurance Limited(the Leading Insurer) in consideration of the Premiumspecified in the Schedule insurance is granted by theInsurers (named in the Schedule annexed hereto) to theInsured in accordance with the terms and conditions con-tained in the Master Policy and on the following terms andconditions.

The Master Policy this Certificate the Schedule andany Memoranda thereon shall be considered one document andany word or expression to which a specific meaning has beenattached in any of them shall bear such meaning throughoutand where appropriate the singular shall include the pluraland vice versa.

- 25 -

Interpretations

For the purposes of this Certificate.

1. Documents shall mean and include deeds wills agree-ments maps plans records books letters certificates formstapes discs microfilm microfiche and documents of anynature whatsoever written printed prepared or reproduced byany other method (other than bearer bonds coupons banknotes currency notes and negotiable instruments).

2. Employee shall mean any person (including anyapprentice) at any time employed by or who is a consultantto the Principal Insured or his predecessors in the Prac-tice .

3. the Insured shall mean(a) the Principal Insured.(b) any other person who may during the Period of

Insurance become a partner in the firm of thePrincipal Insured.

(c) any former partner of the Principal Insured or hispredecessors.

(d) any Employee.(e) in the event of the death of an Insured the personal

representatives of such Insured,or any of them.

4. the Practice shall mean the business of practisingas a solicitor undertaken by the Principal Insured or hispredecessors in business while acting as a solicitor andbusiness shall cover all manner of business carried on ortransacted by the Principal Insured which is customarily(but not necessarily exclusively) carried on or transactedby Solicitors in Scotland.

5. Principal Insured shall mean the Principal Insurednamed in the Schedule or any of them.

6. Proposal shall mean any signed proposal form anddeclaration and any information supplied by or on behalf ofthe Principal Insured in addition thereto or in substitu-tion therefor.

- 26 -

7. Self-Insured Amount shall mean the total amount pay-able by the Insured in respect of each and every claim madeagainst the Insured for all damages and claimant's costsand expenses the appropriate amount being stated in theSchedule.

The Proposal

The Proposal shall be incorporated in and be thebasis of the contract and the truth of the Proposal shallbe a condition precedent to any liability of the Insurerssubject to the provisions of special Condition 1 herein-after contained.

Insurance

The Insurers will indemnify the Insured

1. against liability at law for damages and claimant'scosts and expenses in respect of claims or alleged claimsmade against the Insured and notified to the Brokers duringthe period of Insurance specified in the Schedule by reasonof any negligent act neglect error or omission on the partof

(a) the Insured or the predecessors in the Practice.(b) any agent or correspondent of the Insured or of the

predecessors in the Practice.occurring or committed or alleged to have occurred or tohave been committed in good faith in connection with thePractice.

2. against liability at law for loss or damages andclaimant's costs and expenses in respect of claims oralleged claims made against the Insured and notified to theBrokers during the Period of Insurance by reason of anydishonest fraudulent criminal or malicious act or omissionoccurring or committed or alleged to have occurred or tohave been committed in connection with the Practice on thepart of the Insured.Provided that

(a) no individual committing or condoning such act oromission shall be entitled to indemnity underInsurance 2.

(b) if the Insurers request it the Insured shall takeall reasonable steps to recover the loss from theperson committing or condoning such dishonest fraud-

- 27 -

ulent criminal or malicious act or omission or fromthe personal representatives of such person and theamount recovered (up to but not exceeding the amountpaid by the Insurers) shall be paid to the Insurers.

3. against liability at law in respect of claims andclaimant's costs and expenses made against the Insured orthe predecessors in the Practice and notified to theBrokers during the Period of Insurance.

(a) by reason of any negligent act neglect error oromission committed by the Insured or the predeces-sors in the Practice while acting as an ExecutorTrustee Judicial Factor Curator or as a DirectorSecretary Treasurer or Auditor of any body (whetherincorporated or unincorporated) or as a Liquidatoror Receiver but only so far as.(i) fees paid or which would have been payable are

part of or would have formed part of thereceipts of the Practice or taken into accountin allocating the profits earned by thePrincipal Insured or.

(ii) if honorary the appointment is undertaken withthe knowledge and approval of the PrincipalInsured.

(b) for failure or alleged failure in good faith toaccount to clients for monies had and received inconnection with the Practice.

(c) for breach of warranty of authority committed oralleged to have been committed in connection withthe Practice in the belief that appropriateauthority was held.

(d) for breach committed or alleged to have been commit-ted in connection with the Practice of any duty asdescribed in the speech of Lord Morris reported inMedley Byrne and Co. Ltd. v. Heller and PartnersLtd. 1964 A.C. 465.

4. against loss notified to the Brokers during thePeriod of Insurance and claimant's costs and expensesarising from honouring any personal undertaking or letteror obligation given in good faith by the Insured in theInsured's professional capacity in the Practice.

5. against liability at law for damages and claimant'scosts and expenses in respect of claims made against theInsured and notifed to the Brokers during the Period ofInsurance for libel or slander committed or alleged to havebeen committed in good faith by reason of words written or

- 28 -

spoken by the Insured in the course of the Practiceprovided that the Self-Insured Amount shall not apply tosuch indemnity.

6. notwithstanding Exception 2 in the event of loss ofor damage to Documents occurring in connection with thePractice and discovered during any Period of Insurance inrespect of

(a) all sums which the Insured shall become legallyliable to pay in consequence of such loss or damageand

(b) all costs and expenses reasonably incurred by theInsured in replacing or restoring such DocumentsProvided that(i) such loss or damage is sustained while the

Documents are either anywhere in transit or arein the custody of the Insured or of any personto whom the Insured has entrusted them in thecourse of the normal conduct of the Practice.

Cii) the amount of any claim for such costs andexpenses shall be supported by bills and ac-counts which shall be subject to approval by acompetent person to be nominated by the Insur-ers with the consent of the Insured.

(iii) the Insurers shall not be liable in respect ofloss or damage caused by riot or civil commo-tion outside Scotland England and Wales theChannel Islands or the Isle of Man.

(iv) the Self-Insured Amount shall not apply toparagraph (b) above.

Limit of Indemnity

The liability of the Insurers for loss damages andclaimant's costs and expenses arising out of any one claimshall not exceed the Limit of Indemnity specified in theSchedule. All claims made against the Insured and atttrib-utable to the same act neglect error or omission shall beregarded as one claim.

Other Costs

The Insurers will in addition to the Limit ofIndemnity pay all other costs and expenses incurred withtheir written consent. Provided that the amount of damagesand claimant's costs and expenses in respect of any oneclaim exceeds the Limit of Indemnity the liability of the

- 29 -

Insurers for such other costs and expenses shall be onlythat proportion which the Limit of Indemnity bears to thetotal amount of damages and claimant's costs and expensespayable to dispose of the claim.

Exceptions

The Insurers shall not be liable in respect of

1. the Self-Insured Amount except as provided underInsurance 5 and 6(b).

2. death bodily injury or damage to property unlessarising out of advice given or negligent act or omission inconnection with the Practice.

3. (a) loss or destruction of or damage to any propertywhatsoever or any loss or expense whatsoever result-ing or arising therefrom or any consequential lossor any legal liability of whatsoever nature directlyor indirectly caused by or contributed to by orarising from(i) ionising radiations or contamination by

radioactivity from any nuclear fuel or fromany nuclear waste from the combustion ofnuclear fuel.

(ii) the radioactive toxic explosive or otherhazardous properties of any explosive nuclearassembly or nuclear component thereof.

(b) loss destruction or damage directy occasioned bypressure waves caused by aircraft and other aerialdevices travelling at sonic or supersonic speeds.

4. the consequences of any circumstance notified underany insurance which was in force prior to the inceptiondate of this Certificate.

5. claims made upon the Insured prior to the inceptiondate of this Certificate.

6. any consequence of war invasion act of foreign enemyhostilities (whether war be declared or not) civil warrebellion revolution insurrection or military or usurpedpower.

Partners' Previous Business

The Practice shall include any Solicitors' practicein which any of the persons described under (a), and (b) ofthe definition of the Insured in Interpretation 3 has been

- 30 -

previously engaged provided that such person is not enti-tled to an indemnity under any other insurance. Subjectalways to General Condition 6.

Special Conditions

1.(a) In the event of non-disclosure or misrepresentationat inception or at any subsequent renewal the Insur-ers will waive their rights to avoid this Certifi-cate subject to the premium for the Certificatebeing adjusted to that which would have applied ifthe circumstances which gave rise to the right hadbeen disclosed at inception or the appropriaterenewal as the case may be.

(b) The Insurers shall not avoid any claim on thegrounds of the breach of any General Condition ofthis Certificate other than General Condition 5.

Provided that where the Insured's non-disclosure ormisrepresentation at inception or renewal or breach or non-compliance with any condition of this Certificate hasprejudiced the handling or settlement of any claim theamount payable in respect of such claim (including costsand expenses) shall be reduced to such sum as would havebeen payable in the absence of such prejudice.

2. In the event of any dispute or disagreement betweenthe Insured and the Insurers (except for the matters refer-red to a Queen's Counsel in General Condition 3) as to theapplication meaning or effect of this insurance or any ofthe terms exclusions and conditions thereof or any endorsa-tions made or to be made hereon the same shall be referredto the decision of an arbiter to be appointed failing agre-ement by the Dean of the Faculty of Advocates for the timebeing and the decision of such arbiter whether interim orfinal shall be binding on the parties. The terms ofSection 3(1) of the Administration of Justice (Scotland)Act 1972 shall not apply to any such reference to arbitra-tion.

General Conditions

1. The Insured shall give written notice to the Brokers(regardless of any Self-Insured Amount) as soon as possibleafter becoming aware of circumstances which might reason-ably be expected to produce a claim irrespective of theInsured's views as to the validity of the claim or onreceiving information of a claim for which there may be

- 31 -

liability under this Certificate. Any claim arising fromsuch circumstances shall be deemed to have been made in thePeriod of Insurance in which such notice has been given.

2. Every letter claim writ summons and process shall beforwarded to the Brokers immediately on receipt. No admis-sion offer promise payment or indemnity shall be made orgiven by or on behalf of the Insured without the writtenconsent of the Insurers who shall be entitled to take overand conduct in the name of the Insured the defence orsettlement of any claim or to pursue in the name of theInsured for their own benefit any right of relief and shallhave full discretion in the conduct of any proceedings andin the settlement of any claim.

3. The Insured shall give all such assistance as theInsurers may require but the Insured shall not be requiredto contest or pursue any legal proceedings unless a Queen'sCounsel or similar authority (to be mutually agreed upon bythe Insured and the Insurers) shall advise that such proce-edings could be contested or pursued with the probabilityof success.

4. In connection with any claim against the Insured theInsurers may at any time pay to the Insured the Limit ofIndemnity (after deduction of any sums already paid asdamages or claimant's costs and expenses in respect of suchclaim) or any less amount for which such claim can be set-tled and thereupon the Insurers shall relinquish the con-trol of such claim and be under no further liability inconnection therewith except for costs and expenses forwhich the Insurers may be responsible under this Certifi-cate in respect of matters prior to the date of suchpayment.

5. If any claim be in any respect fraudulent or if anyfraudulent means or devices be used by the Insured or any-one acting on the Insured's behalf to obtain benefit underthis Certificate all benefit hereunder in respect of theindividual or individuals committing or condoning the fraudshall be forfeited.

6. If at the time any claim arises under this Certifi-cate there be any other insurance covering the same l i a b i l -ity the Insurers shall not be liable except in respect ofany excess beyond the amount which would have been payableunder such other insurance.

- 32 -

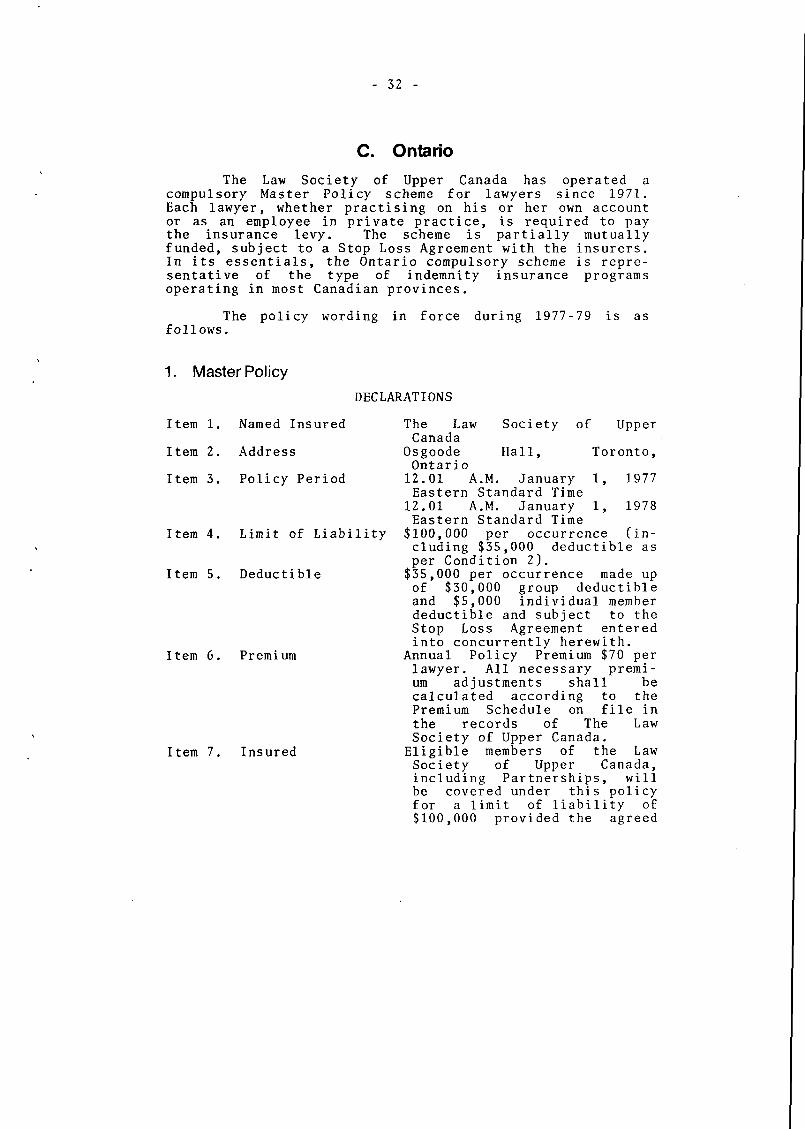

C. OntarioThe Law Society of Upper Canada has operated a

compulsory Master Policy scheme for lawyers since 1971.Each lawyer, whether practising on his or her own accountor as an employee in private practice, is required to paythe insurance levy. The scheme is partially mutuallyfunded, subject to a Stop Loss Agreement with the insurers.In its essentials, the Ontario compulsory scheme is repre-sentative of the type of indemnity insurance programsoperating in most Canadian provinces.

The policy wording in force during 1977-79 is asfollows.

1. Master PolicyDECLARATIONS

Item 1. Named Insured The Law Society of UpperCanada

Item 2. Address Osgoode Hall, Toronto,Ontario

Item 3. Policy Period 12.01 A.M. January 1, 1977Eastern Standard Time12.01 A.M. January 1, 1978Eastern Standard Time

Item 4. Limit of Liability $100,000 per occurrence (in-cluding $35,000 deductible asper Condition 2).

Item 5. Deductible $35,000 per occurrence made upof $30,000 group deductibleand $5,000 individual memberdeductible and subject to theStop Loss Agreement enteredinto concurrently herewith.

Item 6. Premium Annual Policy Premium $70 perlawyer. All necessary premi-um adjustments shall becalculated according to thePremium Schedule on file inthe records of The LawSociety of Upper Canada.

Item 7. Insured Eligible members of the LawSociety of Upper Canada,including Partnerships, willbe covered under this policyfor a limit of liability of$100,000 provided the agreed

- 33 -

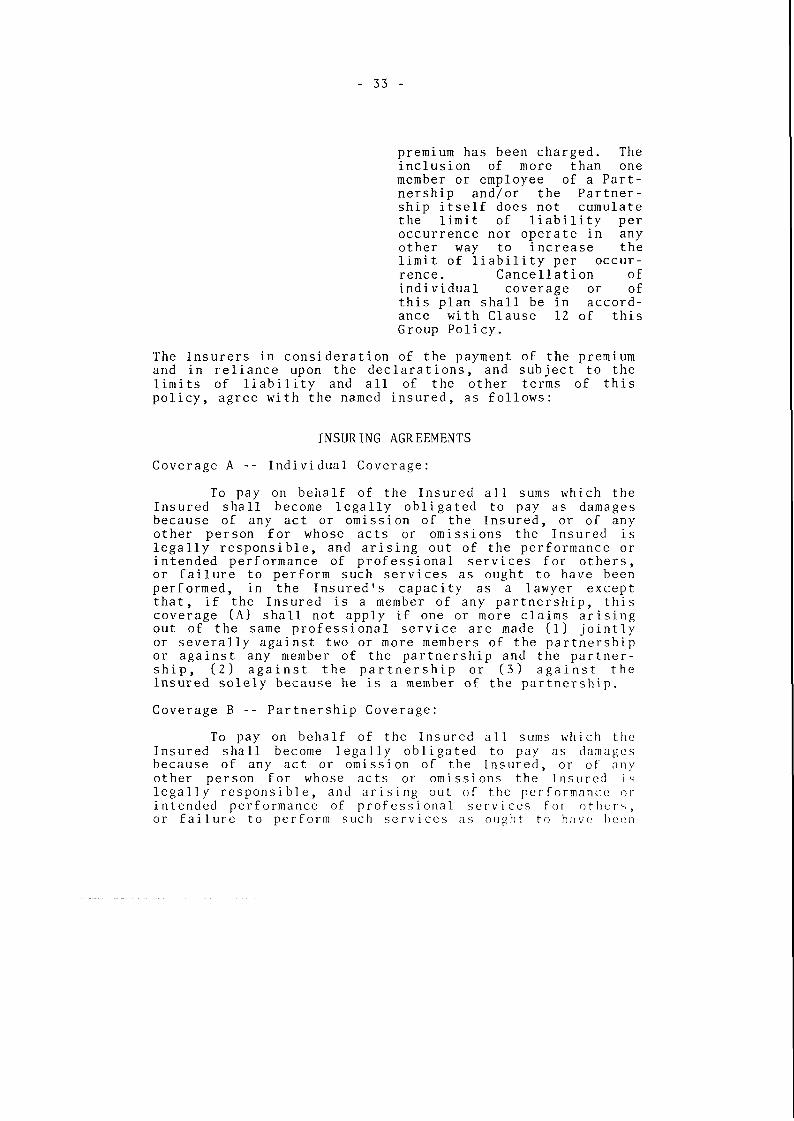

premium has been charged. Theinclusion of more than onemember or employee of a Part-nership and/or the Partner-ship itself does not cumulatethe limit of liability peroccurrence nor operate in anyother way to increase thelimit of liability per occur-rence. Cancellation ofindividual coverage or ofthis plan shall be in accord-ance with Clause 12 of thisGroup Policy.

The Insurers in consideration of the payment of the premiumand in reliance upon the declarations, and subject to thelimits of liability and all of the other terms of thispolicy, agree with the named insured, as follows:

INSURING AGREEMENTS

Coverage A -- Individual Coverage:

To pay on behalf of the Insured all sums which theInsured shall become legally obligated to pay as damagesbecause of any act or omission of the Insured, or of anyother person for whose acts or omissions the Insured islegally responsible, and arising out of the performance orintended performance of professional services for others,or failure to perform such services as ought to have beenperformed, in the Insured's capacity as a lawyer exceptthat, if the Insured is a member of any partnership, thiscoverage (A) shall not apply if one or more claims arisingout of the same professional service are made (1) jointlyor severally against two or more members of the partnershipor against any member of the partnership and the partner-ship, (2) against the partnership or (3) against theInsured solely because he is a member of the partnership.

Coverage B -- Partnership Coverage:

To pay on behalf of the Insured all sums which theInsured shall become legally obligated to pay as damagesbecause of any act or omission of the Insured, or of anyother person for whose acts or omissions the Insured islegally responsible, and arising out of the performance orintended performance of professional services for others,or failure to perform such services as ought to have been

- 34 -

performed, in the Insured's capacity as a lawyer providedone or more claims arising out of the same professionalservice are made (1) jointly or severally against two ormore members of the partnership insured hereunder oragainst any member and such partnership, (2) against thepartnership or (3) against the Insured solely because he isa member of the partnership insured hereunder.

Coverage C -- Defense, Settlement, Supplementary Payments:With respect to such insurance as is afforded by thisPolicy, the Insurers shall--

(a) Defend any suit against the Insured alleging suchact or omission and seeking damages which are or maybe payable under the terms of this Policy, even ifany of the allegations of the suit are groundless,false or fraudulent; but the Insurers may make suchinvestigation and, with the consent of the Insured,such settlement of any claim or suit as they deemexpedient; if the Insured and Insurers fail toagree on whether settlement shall be made then suchissue shall be decided by reference to an arbitratorappointed by the Claims Committee whose decisionshall be binding on the Insurers and the Insured andNamed Insured.

(b) Pay, in addition to the applicable limit of liabili-ty:(i) all costs taxed against the Insured in any suit

defended by the Insurers and all interest onthe amount of any judgment therein which ac-crues after entry of the judgment and beforethe Insurers have paid or tendered or depositedin Court that part of the judgment which doesnot exceed the limit of the Insurers' liabilitythereon; where the judgment exceeds the policylimit the Insurers will only be liable fortheir pro rata proportion of such cost andinterest;

(ii) premiums on appeal bonds required in any suchsuit, premiums on bonds to release attachmentsfor an amount not in excess of the applicablelimit of liability of this policy but withoutany obligation to apply for or furnish any suchbonds;

Subsections (a) and (b) of Coverage C above, aresubject to the deductible.

(c) Pay all reasonable expenses, other than loss ofearnings, incurred by the Insured at the Insurers'request.

- 35 -

EXCLUSIONS

This Policy Does Not Apply:

(a) to any dishonest, fraudulent, criminal or maliciousact or omission of any Insured;

(b) to any claim made by an employer who is not insuredhereunder against an Insured who is a salariedemployee of such employer. In the event of a claimcovered by the policy being made by an employer whois an Insured hereunder against another Insured whois a salaried employee of such employer, this policywill indemnify the insured employee only to theextent of the employer's vicarious liability for thenegligence of the insured employee and within thelimits of this policy. This policy shall notindemnify the insured employee in respect of anyclaim by the insured employer for any alleged con-sequential damage to the goodwill or reputation ofthe employer;

(c) to bodily injury to, or sickness, disease or deathof any person, or to injury to or destruction of anytangible property, including the loss of use there-of; unless arising out of the performance of pro-fessional services, which is covered hereunder;

(d) with respect to acts or omissions committed prior tothe policy period of the Insured on the effectivedate of this policy had knowledge that such acts oromissions might be expected to be the basis of aclaim or suit.

DEFINITIONS

A. "Named Insured" means The Law Society of UpperCanada

B. "Insured" means1. with respect to Coverages A and C

(a) each lawyer who is a member of The LawSociety of Upper Canada and is eligiblefor coverage under this Policy, and

(b) each judge, each former member of The LawSociety of Upper Canada, and each lawyerexempted by the Benchers of The LawSociety of Upper Canada from this Law-yers' Professional Liability Policy;provided that at the time such personbecame a judge or ceased to be a memberor was exempted he was a member of The

- 36 -

Law Society of Upper Canada and wouldhave been eligible within the Rules ofThe Law Society of Upper Canada for cov-erage under this Policy, and providedfurther that each such person shall be anInsured only with respect to acts oromissions committed prior to his becominga judge or ceasing to be a member or be-ing exempted, respectively.

2. with respect to Coverages B and C(a) each partnership in which an Insured

under Coverage A is or was a partner, andeach partner and employed lawyer thereof;

(b) if two or more insured persons are orwere held out to the public as partners,they shall be deemed to be partnerswhether or not the partnership in factexists, or existed.

"Claims Committee" means that committee as from timeto time may be constituted between the Named Insuredand the Insurers as provided for in the agreemententered into concurrently herewith."Policy Period" means1. with respect to the Named Insured and each

Insured as defined in Definition B (b) theperiod shown in item 3 of the Declarations ofthis Policy;

2. with respect to each other insured, the periodfrom the time when coverage has been effectedthrough The Law Society of Upper Canada and forwhich a premium has been paid, until either theexpiration date shown in Item 3 of the Declara-tions of this Group Policy, or until cancella-tion of coverage, whichever first occurs.

"Occurrence" shall mean any error or alleged erroror any omission or alleged omission by an Insuredhereunder or by his/her partner and/or employee(s)in the performance of professional services forothers; in the event that more than one error oromission is alleged to have occurred in relation tothe same professional service then all such errorsand omissions shall be deemed to be a single occur-rence and the limit of liability in respect thereofshall be $100,000 except in the event that one ormore claims arising out of the same professionalservices are made jointly or severally against two

- 37 -

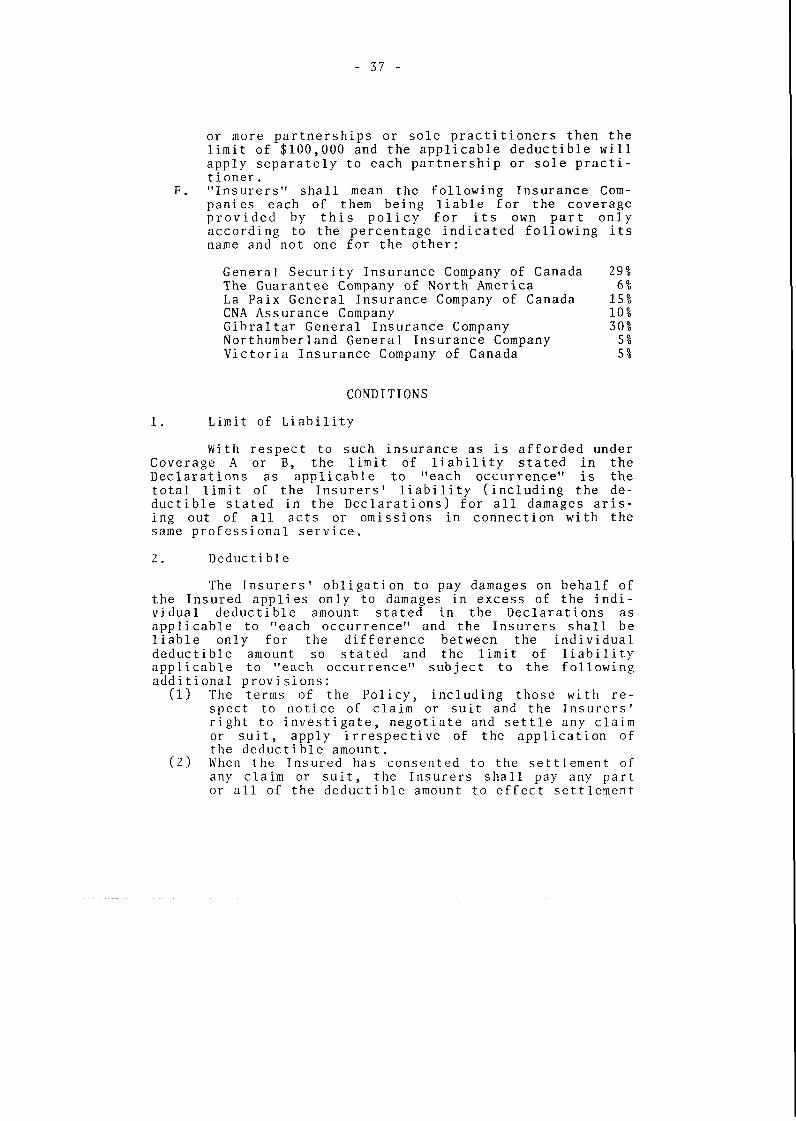

or more partnerships or sole practitioners then thelimit of $100,000 and the applicable deductible willapply separately to each partnership or sole practi-tioner ."Insurers" shall mean the following Insurance Com-panies each of them being liable for the coverageprovided by this policy for its own part onlyaccording to the percentage indicated following itsname and not one for the other:

General Security Insurance Company of Canada 29%The Guarantee Company of North America 6%La Paix General Insurance Company of Canada 15%CNA Assurance Company 10%Gibraltar General Insurance Company 30%Northumberland General Insurance Company 5%Victoria Insurance Company of Canada 5%

CONDITIONS

1. Limit of Liability

With respect to such insurance as is afforded underCoverage A or B, the limit of liability stated in theDeclarations as applicable to "each occurrence" is thetotal limit of the Insurers' liability (including the de-ductible stated in the Declarations) for all damages aris-ing out of all acts or omissions in connection with thesame professional service.

2. Deductible

The Insurers' obligation to pay damages on behalf ofthe Insured applies only to damages in excess of the indi-vidual deductible amount stated in the Declarations asapplicable to "each occurrence" and the Insurers shall beliable only for the difference between the individualdeductible amount so stated and the limit of liabilityapplicable to "each occurrence" subject to the followingadditional provisions:

(1) The terms of the Policy, including those with re-spect to notice of claim or suit and the Insurers'right to investigate, negotiate and settle any claimor suit, apply irrespective of the application ofthe deductible amount.

(2) When the Insured has consented to the settlement ofany claim or suit, the Insurers shall pay any partor all of the deductible amount to effect settlement

- 38 -

of any claim or suit and, upon notification of theaction taken, the Named Insured shall promptly placethe Insurers in funds sufficient to satisfy theclaim subject to the maximum group deductible of$30,000 and shall arrange for prompt payment of theindividual deductible of $5,000, or so much thereofas shall be required to effect the settlement.

3. Coverage, Policy Period, Territory

This insurance applies to acts or omissions commit-ted by an Insured in connection with his practice as amember of The Law Society of Upper Canada provided theoriginal claim or suit for damages is brought during thepolicy period; provided further that if during the policyperiod the Insured shall become aware of any happeningwhich may subsequently give rise to a claim and shall,during the policy period, give notice in accordance withCondition 5, any claim or suit subsequently brought againstthe Insured arising out of that happening shall be deemedfor the purpose of this insurance to have been made duringthe policy period. Upon the expiration of the policyperiod, this policy shall be free of all claims other thanthose mentioned above in this paragraph. If the policyperiod stated in the Declarations is subsequently extended,this Condition shall not apply separately to each suchextended period, except that this shall not operate toincrease the Limit of Liability applicable to any occur-rence .

4. Fiduciary

When the Insured acts as an administrator, executor,guardian, trustee, or in any similar fiduciary capacity,his acts and omissions in such capacity shall be covered(a) only to the extent that such acts or omissions arethose for which he is legally responsible in the usualsolicitor-client relationship, and shall be (b) subject toall Exclusions and other Conditions of this policy.

5. Notice of Claim or Suit

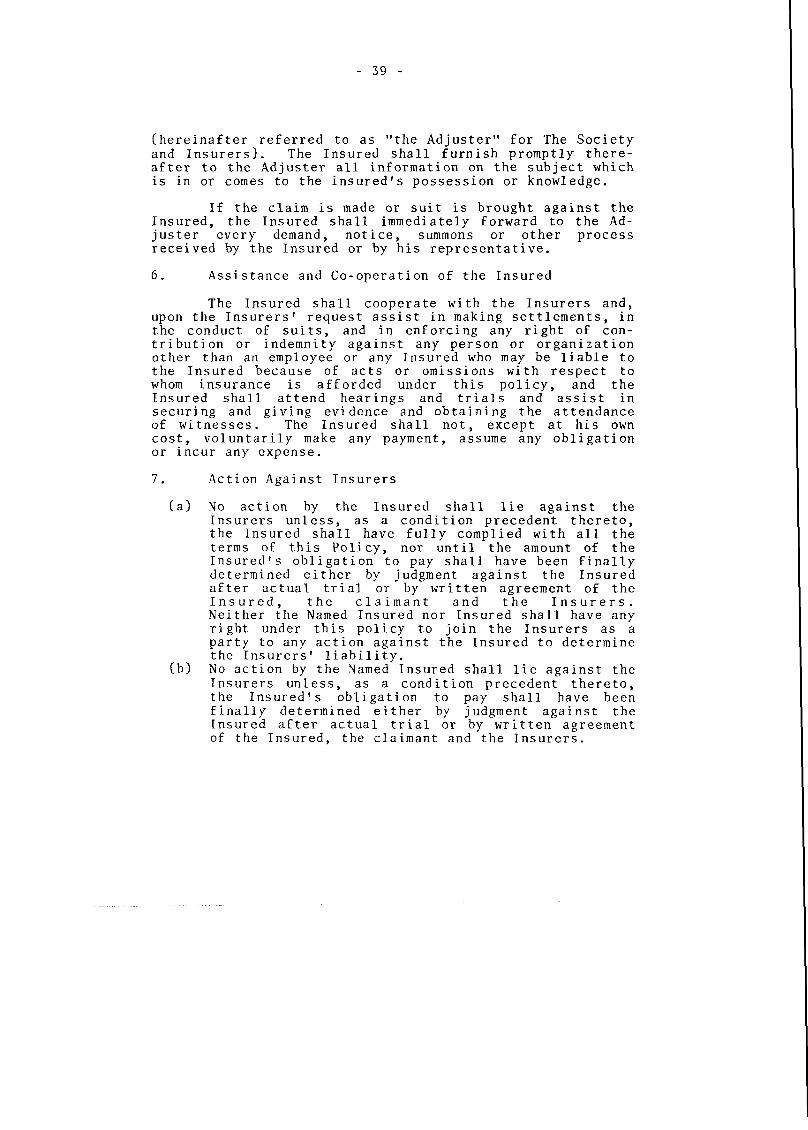

The Insured as soon as practicable after learning ofa happening which may give rise to a claim hereunder shallgive notice or cause notice to be given to:

F.C. Maltman & Co. Ltd.P.O. Box 5, Postal Station QTORONTO, OntarioM4T 2L8

- 39 -

(hereinafter referred to as "the Adjuster" for The Societyand Insurers). The Insured shall furnish promptly there-after to the Adjuster all information on the subject whichis in or comes to the insured's possession or knowledge.

If the claim is made or suit is brought against theInsured, the Insured shall immediately forward to the Ad-juster every demand, notice, summons or other processreceived by the Insured or by his representative.

6. Assistance and Co-operation of the Insured

The Insured shall cooperate with the Insurers and,upon the Insurers' request assist in making settlements, inthe conduct of suits, and in enforcing any right of con-tribution or indemnity against any person or organizationother than an employee or any Insured who may be liable tothe Insured because of acts or omissions with respect towhom insurance is afforded under this policy, and theInsured shall attend hearings and trials and assist insecuring and giving evidence and obtaining the attendanceof witnesses. The Insured shall not, except at his owncost, voluntarily make any payment, assume any obligationor incur any expense.

7. Action Against Insurers

(a) No action by the Insured shall lie against theInsurers unless, as a condition precedent thereto,the Insured shall have fully complied with all theterms of this Policy, nor until the amount of theInsured's obligation to pay shall have been finallydetermined either by judgment against the Insuredafter actual trial or by written agreement of theInsured, the claimant and the Insurers.Neither the Named Insured nor Insured shall have anyright under this policy to join the Insurers as aparty to any action against the Insured to determinethe Insurers' liability.

(b) No action by the Named Insured shall lie against theInsurers unless, as a condition precedent thereto,the Insured's obligation to pay shall have beenfinally determined either by judgment against theInsured after actual trial or by written agreementof the Insured, the claimant and the Insurers.

- 40 -

8. Other Insurance

If the Insured has other insurance against a losscovered by this Policy, except insurance specificallyarranged to apply as excess over the insurance provided bythis Policy, the insurance hereunder shall apply only asexcess insurance over any other valid and collectibleinsurance and shall not be called upon in contribution.

9. Subrogation

In case of payment of loss by the Insurers here-under, the Insurers shall be subrogated to the Insured'sright of recovery against any other person for such lossand the Insured shall execute all papers required and shallco-operate with the Insurers to secure such rights. TheInsured shall do nothing after loss to prejudice suchrights. In the event that the Insured has been required topay part of any settlement or judgement in respect of whichthe Insurers have paid and the net amount recovered pursu-ant to the Insurers' subrogated right, after deducting thecost of recovery, is not sufficient to provide a completeindemnity for both Insurers and Insured, that amount shallbe divided between the Insurers and the Insured in theproportions in which the cost of settlement or of satisfy-ing a judgment has been borne by them respectively. TheInsurers shall not by way of subrogation to the rights ofan Insured, seek to recover from another Insured, except tothe extent that the Insurers have been prejudiced by thefailure of such other Insured to comply with the terms ofthis policy.

10. Changes

Notice to the Broker or knowledge possessed by anyagent or by any other person shall not effect a waiver nora change in any part of this Policy, nor estop the Insurersfrom asserting any right under the terms of this Policy,nor shall the terms of this Policy be waived or changedexcept by an endorsement issued to form a part of thisPolicy, signed by a duly authorized representative of theInsurers and accepted by the Named Insured.

11. Assignment

The interest hereunder of any Insured is not assign-able. If the Insured shall die, be adjudged incapable ofmanaging his affairs or become bankrupt or insolvent, thispolicy shall cover the Insured's legal representative as anInsured with respect to acts or omissions covered by this

- 41 -

policy. Bankruptcy or insolvency of the Insured or of theInsured's estate shall not relieve the Insurers of any oftheir obligations hereunder.

12. Cancellation

Group Policy--

This Group Policy may be cancelled by the NamedInsured or by the Insurers by giving not less than onehundred and eighty (180) days notice in writing the one tothe other. Such notice may be delivered or sent by regis-tered mail to the registered office of the Named Insured atOsgoode Hall, Toronto, or the Gestas Corporation, in itscapacity as manager, at Suite 530, 410 St. Nicholas Street,Montreal as may be required. The effective date of cancel-lation stated in the notice shall become the end of thepolicy period.

If the Named Insured or the Insurers cancel, earnedpremium shall be computed pro rata. Premium adjustment maybe made either at the time cancellation is effected or assoon as practicable after cancellation becomes effective,but payment or tender of unearned premium is not a condi-tion of cancellation.

Upon such cancellation, all coverage under thisPolicy and all coverage afforded to any and all Insuredsshall terminate concurrently with the termination of cover-age under this Group Policy except as provided under thefirst paragraph of Condition 3. In the event of suchcancellation the Named Insured shall advise its members.

Individual Insureds--

Individual coverage provided under this Policy maybe terminated by the Insurers only on agreement from theBenchers of The Law Society of Upper Canada by mailing tothe Insured fifteen (15) days notice of termination byregistered mail or giving five (5) days written noticepersonally delivered. The fifteen (15) days mentionedabove commences to run on the day following the mailing ofthe registered letter. No return of premium will be made.

13. Compromise

The Named Insured and Insurers shall not compromiseany claim nor settle any suit without the consent of theInsured. If the Insured shall refuse to consent to anysettlement recommended by the Named Insured and Insurers

- 42 -

and shall elect to contest or continue legal proceedings inconnection with such claim, the amount payable under thispolicy for such claim shall not exceed the amount for whichsuch claim could have been so settled plus the costs andexpenses incurred with the Claims Committee's consent up tothe date of such refusal, all subject always to the deduct-ible, limits and limitations of this policy.

2. Stop Loss and Management AgreementBETWEEN: The Law Society of Upper Canada (herein-

after called the "Society") of the firstpart.

AND: Gestas Corporation Ltd. (hereinafter cal-led the "Manager") in its capacity asManager for Insurers, as listed below, ofthe second part:-

General Security Insurance Company ofCanadaThe Guarantee Company of Nor th Amer icaLa P a i x G e n e r a l I n s u r a n c e Company ofCanadaCNA Assurance CompanyGibraltar General Insurance CompanyNorthumberland General Insurance CompanyVictoria Insurance Company of Canada

WHEREAS the Manager has agreed to issue on behalf of Insur-ers Policy No. RP 601369 of Group Professional LiabilityInsurance to the Society on behalf of its eligible members;

AND WHEREAS the Manager has agreed to administer the hand-ling and payment of damages under the said Policy, notwith-standing the deductible shown therein;

AND WHEREAS the Society has agreed to place the Manager infunds up to the limits and on the conditions herein con-tained;

AND WHEREAS it is the intent of this agreement that thegroup deductible for which the Society is responsible shallnot exceed the amounts hereinafter set forth;

NOW THEREFORE THIS AGREEMENT WITNESSETH:

1. The Society and the Manager mutually agree -(a) To establish a Claims Committee comprised of a

representative of the Society, a representative

- 43 -

of the Manager, and an arbitrator as required,and;

(b) To establish rules of procedure and conduct asmay be necessary for the operation of theClaims Committee.

No payment of damages or expenses shall be made forany occurrence irrespective of the application ofany deductible, unless such payment has been ap-proved by the Committee.

2. The Society Agrees -

(a) To place the Manager in funds to pay alldamages which the Manager is required to payunder the Policy, provided, however that:(i) Such funds do not exceed $35,000 per

occurrence made up of $30,000 Group De-ductible and $5,000 individual memberdeductible.

(ii) The Society's aggregate payments shall notexceed $2,000,000 or the sum of $225 timesthe number of lawyers eligible for cover-age as at January 1, 1977 (whichever isthe larger amount) for all damages anddefence expenses for all occurrences re-ported during the policy period January 1,1977 to January 1, 1978, calculated exclu-sive of individual Insureds' deductibles.

(b) In any succeeding year the Society's aggregatepayments shall not exceed the sum of $225 timesthe number of lawyers eligible at the begin-ning of each such year, calculated exclusive ofindividual Insureds' deductibles.

(c) To provide an Adjuster at the expense of theSociety who shall investigate on behalf of theManager and the Society all reported occur-rences, and who shall adjust all claims fordamages regardless of amount, and obtain at thedirection of the Manager, all necessary re-leases with respect to settlements made.

The Manager has the right to employ at its ownexpense such other adjusting assistance as itdeems necessary. If the Claims Committee ob-tains expert assistance in addition to theSociety's Adjuster, the expense of such a d d i -tional assistance shall be borne by the Society

- 44 -

and be included in calculating the limit of itsliability as set forth in Clauses 2(a)(ii) and2(b).

(d) To pay all counselling expenses necessarilyincurred by the Adjuster in carrying out hisresponsibilities.

(e) If the aggregate paid to the Manager as re-spects occurrences reported during any periodstated in 2(a)(ii) and 2(b) above reaches theaggregate amount applicable to such period, toarrange for payment by the Insured to pay alldamages and defence expenses which the Manageris required to pay by Coverages A and B of thepolicy not exceeding the sum of $5,000 for eachfurther occurrence.

(f) In the event of cancellation of the policy dur-ing any annual period, Clauses 2(a)(ii) and 2(bj shall apply pro rata.

3. The Manager Agrees -(a) To issue its cheque in payment of damages or

defence costs in accordance with the terms ofthe Policy and this Agreement.

(b) That the termination of the policy or of thecoverage of any Insured does not terminate thisAgreement either in whole or in part.

(c) That it shall from time to time after January1, 1977 advise the Society, promptly throughits Broker of any changes in the Schedule ofsubscribing Insurers.

(d) That no change in the Schedule of Insurers ortheir percentages shall modify the terms orconditions of the policy.

D. Victorian Legal Advice CentresIn late 1979 the Law Institute of Victoria negoti-

ated a group scheme for voluntary legal advice centres inMelbourne. The scheme requires adoption by at least tencentres before it can commence. The Commission was advisedin December 1979 that this target was expected to beachieved.

The wording of the proposed group policy is as fol-lows .

- 45 -

PolicyWhereas the Assured, as stated in the Schedule, has

made to Underwriters a written Proposal/Declaration bearingthe date stated in the Schedule containing particulars andstatements which it is hereby agreed are the basis of thisPolicy and are to be considered as incorporated herein, andhave paid the premium stated in the Schedule.

Now, We, the Insurers, to the extent and in the man-ner hereinafter provided, hereby agree to indemnify theAssured against all sums which the Assured shall becomelegally liable to pay as damages as a result of a claim orclaims made against the Assured during the period specifiedin the Policy arising out of any negligent act error oromission on the part of the Assured or any employee orother person working under the control, direction or super-vision of the Assured in or about the conduct of theAssured's occupation as a legal advice centre.