43

THE LITHUANIAN PROPERTY MARKET REPORTResearch, 2004

Lithuania

2

Kaunas City

Vilnius City

4

Klaipëda City

Contents

Chapter 1. Introduction.....................................................................................................................................7

Chapter 2. Executive Summary......................................................................................................................8

Chapter 3. Lithuania: Main Factors.............................................................................................................93.1. Geography and Population........................................................................................................93.2. Politics..........................................................................................................................................93.3. Economic Figures........................................................................................................................10

Chapter 4. Major Cities of Lithuania.........................................................................................................14

Chapter 5. Introduction to the Commercial Property Market................................................155.1. General Remarks....................................................................................................................155.2. Commercial Property Market Segments........................................................................16

5.2.1 Office Market......................................................................................................................165.2.2. Retail Market ..................................................................................................................185.2.3. Industrial Market .......................................................................................................21

Chapter 6. The Lithuanian Investment Market.........................................................................22

Chapter 7. SWOT Analysis............................................................................................................................25

Chapter 8. KOBA�s Expectations of the Market .............................................................................26

Chapter 9. Legal Facts about the Commercial Property Market .............................................28

Chapter 10. Taxation..............................................................................................................................33

Appendices ................................................................................................................................................................37

6

The purpose of this Report is to give an introduction to the commercial property market inLithuania and an actual approach to potential investment opportunities.

The Report is based on external material from official institutions of Lithuania, leading commercialbanks and internal information and data from KOFOD-JENSEN & BACH-NIELSEN Lithuania(KOBA), Cushman & Wakefield Healey & Baker, and the Law Firm Jurevièius, Balèiûnas & Partners,EY Law.

The information provided in the Report is correct to the best of our knowledge, however, givenwith no responsibility.

The Report is divided into ten chapters. Each chapter can be read independently of the Report assuch.

Chapter 2 gives an executive summary of the aspects of the market report.

Chapter 3 is a brief survey of Lithuania�s geography, politics and economic data.

Chapter 4 briefly introduces the major cities of Lithuania and their peculiarities.

Chapter 5 focuses on the commercial property market segments in Lithuania.

Chapter 6 provides an insight into the investment market tendencies � rents and yields.

Chapter 7 gives a SWOT analysis of the market.

Chapter 8 summarises the property market analysis and gives KOBA�s expectations of the market.

Chapters 9 and 10 give descriptions of practical aspects of investing in properties in Lithuania suchas taxation and the legal environment.

The editing of this market Report ended on 10 February 2004. �The Lithuanian Property MarketReport� has been prepared by KOFOD-JENSEN & BACH-NIELSEN Lithuania (KOBA)together with the Law Firm Jurevièius, Balèiûnas & Partners, EY Law, primarily for professionalinvestors, leaseholders and developers taking an interest in Lithuanian property markets.

NB! Please notice that any distribution, reprints (total or partly), etc. is only allowed with written permission from KOBA and the Law Firm Jurevièius, Balèiûnas & Partners, EY Law.

IntroductionChapter 1

Chapter 2

�The Lithuanian Property Market Report 2004� describes an upcoming property market in an economicallypromising area with old democratic traditions although often in history overruled by aggressive neighbouringcountries.

After independence Lithuania introduced radical economic reforms which brought it successfully along theroad from a planned economy controlled by the Soviet Union to a friendly place, where a market economyprospers within a proper and well-regulated framework.

The development of the Lithuanian property market started in 1990 when the planned economy of the countrystarted to transform into a free market economy and influenced the growth and maturing of its real estatemarket.

During more than ten years the growing domestic demand supported the local economy, and the market becamedeveloped and mature. Private consumption growth is having a more important role, investments have alsostarted to grow strongly thus supporting long-term developments. Economic growth was accompanied by thedevelopment of business, which stimulated the demand for office, retail and warehouse-logistic premises.

In the office market the demand first of all arose among representative offices of foreign companies, foundationsand other financial institutions. Compared with the other Baltic States, Tallinn was a pioneer in the office market,mainly due to close ties with the Nordic countries and active investment in the Estonian economy. Investmentsin Riga were focussed on the reconstruction of old buildings and adaptation to office needs. Vilnius was the lastto experience growth in new office construction but this helped to avoid mistakes leading to low occupancy anddecline in rent levels. Other cities of Lithuania are still far behind developments in Vilnius, as due to the limitedsize of the Lithuanian market in general, there is no demand for representative offices in several towns, and themajority of business is located in the capital.

The retail space market was determined both by economic development and geographical features. Vilnius has acentral retail street � Gedimino Avenue. The concentration of shops and the location make this street mostconvenient for retail. Kaunas, the second largest city of Lithuania, has a unique pedestrian area, Laisvës Alëja,where all major brands are located too. Other cities traditionally are developing retail space in the central part ofthe city. In respect of shopping centres, Lithuanian retail chains, and not developers, are the main builders andinitiators of construction. They are quite successful in these activities, and are ahead of other builders in termsof the size of a shopping centre compared with the other Baltic countries.

The development of industrial/warehousing space is in an early stage compared with other segments of the propertymarket. Many new non-speculative industrial and warehousing facilities appeared, which produced a shrinkingeffect upon the market of potential lessees and resulted in a stagnation of prices in this segment. The demandfor new premises remains, encouraging developers to engage in construction/reconstruction of this type ofproperty.

The future membership of the EU has already boosted the local market with regard to international interest, butas long as the local market is opaque and has a limited liquidity, we are not going to see significant drops in realinvestment yields.

Executive Summary

8

Chapter 3 Lithuania: Main Factors

3.1. Geography and Population

Lithuania is the largest country among the Baltic States. With an area of 65,300 sq.km, Lithuaniais even larger than Belgium, Denmark, the Netherlands and Switzerland. It borders Latvia in theNorth, Belarus in the southeast, Poland and the Kaliningrad region of the Russian Federation inthe southwest.

Arable land accounts for 70% of the country�s lowlands, plains and hilly uplands, and 28% isforested. Lithuania�s 722 rivers, more than 2,800 lakes and 99 km of the Baltic Sea coastline aremostly devoted to recreation and preservation of nature.

The climate is transitional between maritime and continental.

The population of Lithuania is 3,475 million. The major cities are Vilnius (542,300 inhabitants),Kaunas (373,700), Klaipëda (194,400), Ðiauliai (133,800) and Panevëþys (134,000).

About 67% of Lithuania�s 3.5 million people live in urban areas, giving the country a populationdensity of 53.5 people per sq.km.

The majority of the population � 83.5% � is Lithuanian, 6.3% Russian, 6.7% Polish, and 3.5%other (Belarusians, Ukrainians, Latvians, etc.).

The official state language is Lithuanian, which is closely related to Sanskrit and belongs to theBaltic family of the Indo-European languages. Most of the population also speak Russian; Englishis common among young people.

3.2. Politics

The parliament of Lithuania officially declared independence in March 1990.

The Lithuania�s Constitution was adopted in October 1992. The Constitution established theRepublic of Lithuania with a President as the head of state. The highest legislative authority is theSeimas (parliament), a unicameral body. The President is elected by direct general election for aterm of five years and may be elected for a maximum of two consecutive terms. The PrimeMinister is appointed or dismissed by the Government with the approval of the Seimas. Lithuania�stype of government is parliamentary democracy.

On 13 December 2002, Lithuania finished negotiations with the EU and from 1 May 2004 willbecome a member of the European Union. It is forecast that Lithuania will introduce the Eurobetween 2005 and 2007.

On 21 November 2002, NATO formally invited seven countries to accession talks with theAlliance: Bulgaria, Estonia, Latvia, Lithuania, Romania, Slovakia and Slovenia.

Country

Population

Lithuania andInternationalMembership

3.3. Economic Figures

A strong domestic demand has supported the economic development of Lithuania in the previous years. Privateconsumption growth is having a more important role than in previous years also investments have started togrow strongly thus supporting long-term developments.

The balance of the economy has significantly improved, interest rates are at a low level, budget deficits havebeen reduced, and the government policy has become more reliable being clear and successful in fulfilling itsplans.

On 29 January 2004, with a 10.6% GDP growth rate in the last quarter of 2003 and 8.9% in the whole year 2003,Lithuania is one of the fastest growing economies in the world, according to preliminary data of the Departmentof Statistics.

The biggest input into GDP growth came from the industry, trade and construction, and increasing domesticconsumption stimulated it.

According to the Ministry of Finance, GDP growth rate for 2004 is forecast at 7.5%�8%.

The EU accession will have a positive impact on the economic development: in 2002�2003 the pre-accession aidwas employed in Lithuania, in 2004�2006 the EU Structural Funds and other EU financial assistance will acceleratethe pace of GDP growth.

In 2002 deflation resulted in a steady decline of the rate of monthly prices, in comparison with the previousmonth. The disinflation in the second half of the year 2002 (except that in July) manifested itself as a monthly-annual deflation. It was intensified by an enhanced competition in sale of meat, fish and vegetables; therefore,the annual deflation of a month occurred more frequently. Due to the same reasons the monthly-annual deflationsustained in 2003.

Gross DomesticProduct

Inflation

10

Due to low inflation and increased non-tax revenue rate the real salary is likely to grow at a moreaccelerated pace than the nominal one. The average monthly salary in Lithuania is forecast togrow to 1,333 LTL in 2006.

In 2002, the average gross salary in Vilnius was 1,241 LTL per month and exceeded the overallaverage of Lithuania (1,014 LTL) by 22.3%.

According to experts� evaluations, in 2002 about 21.9% of Lithuania�s industrial labour, 22.3% ofthe construction sector labour and 21.4% of the service sector are employed in Vilnius. In thelast decade, the service sector has been the most rapidly developing sector of the city�s economy.Currently the service sector employs more than 69% of people employed in Vilnius.

The central bank of the Republic of Lithuania is the Bank of Lithuania. The main objective ofthe Bank of Lithuania is to maintain the currency stability in the Republic of Lithuania, ensuresound functioning of the money market, credit and the settlements system.

Lithuanian banks offer a wide range of banking services: foreign exchange transactions and theissue and receipt of cheques, letters of credit, international payments, etc. Citizens of the Republicof Lithuania and foreign states may have current accounts and term deposits in foreign currencies.There are no foreign exchange restrictions. Lithuania offers unrestricted movement of capitaland dividends.

Currently, ten commercial banks holding a license from the Bank of Lithuania, three foreignbank branches, three foreign banks representative offices, the central credit union of Lithuaniaand 57 credit unions are operating in the country.

Labour market

Financial sector

The Lithuanian currency, the Litas, was initially pegged to the US Dollar at a fixed rate of 1 USD = 4 LTL , thenit was re-pegged to the Euro at a rate of 1 EUR = 3, 4528 LTL.

In 2004 Standard & Poor�s Lithuania�s long-term borrowing rating on foreign currency increased from BBB+ to A-.

Over the past few years, Lithuania has become a leading location for foreign investors and a competitive centrefor product sourcing in the region. The main reasons are a high-skilled, low cost alternative to production in theWest, along with a stable and strong production springboard to the huge markets to the East. In addition, theimpressive economic growth, the stable currency and great business environment all combine to make Lithuaniathe premier investment location in the region, experts of the Lithuanian Development Agency state.

CumulativeForeign Direct

Investment

Currency

FDI(Foreign

DirectInvestment)

Cumulative FDI in Lithuania as of 1 October 2003 (EUR billion)

Cumulative FDI by Country as of 1 October 2003 (EUR million)

12

Chapter 4 Major Cities of Lithuania

There are three major cities in Lithuania � Vilnius, the capital of Lithuania, Kaunas and Klaipëda. We supposethat it is worth describing the peculiarities for foreign investors of each briefly.

Being the capital of Lithuania, Vilnius is basically the most attractive city for foreign investors. All the mainpublic and educational institutions are located in Vilnius. As most investors are trying to be as close as possibleto the decision makers � governmental institutions � they want to have their main offices or at least branches incapitals. Vilnius is progressing rapidly and the companies from other country regions are seeking for job offershere. The unemployment rate in Vilnius at 6.1% is one of the lowest in the country. The creation of additionalworkplaces, especially in the construction sector, also reduces the unemployment in neighbouring regions.

The city of Vilnius has become the major engine of the economic development in Lithuania, having the highestGDP level per capita and the fastest speed of growth. The potential of Vilnius is basically determined by thespecific climate of the capital city, which has made it the largest administrative centre in Lithuania with all majorpolitical, economic, social and cultural institutions.

Vilnius is famous not only as the capital of Lithuania, but also as a cultural and historical centre of the country.The Old Town is on the UNESCO World Cultural Heritage list. With its beautiful Old Town and nice surroundings,Vilnius is becoming more and more attractive for tourists. Vilnius Airport serves as a convenient connection tovarious cities of the world.

Situated in the central part of Lithuania, on the highway Via Baltica, between Vilnius and Klaipëda, Kaunas (theformer capital of Lithuania) is the second largest city of our country. With almost 374,000 inhabitants, Kaunasis famous as an educational and innovation centre, where a lot of universities and high schools are located.

The beautiful Old Town and the unique pedestrian Laisvës Alëja attract a lot of visitors to various cafes, restaurantsand shops.

Kaunas has the largest cargo airport in Lithuania making it a natural terminal for distribution. Also consideringthat Kaunas Free Economic Zone is starting its operations this might increase investors interest in the region.

The geographical location of Klaipëda, the third largest city of Lithuania, has defined its historical role asintermediary in the economic relations between East and West for 750 years. It has the northernmost ice-freeport on the Eastern coast of the Baltic Sea and good land routes into the continent. Klaipëda is a large, multi-modal transport junction of sea, land and railway routes, connecting Eastern and Western industries and marketsin the shortest possible ways. Klaipëda Seaport is a centre of shipping, cargo and other related services. There are regular ferry, ro-ro and cargoservices to Germany, Sweden, Denmark, the Netherlands, Belgium, Russia, Poland, Great Britain and othercountries worldwide.

With almost 195,000 inhabitants and being an important economical, historical and cultural centre of Westernpart of Lithuania, Klaipëda attracts a lot of visitors.

Klaipëda Free Economic Zone is actively operating, which also makes the area attractive to various foreign investors.

Vilnius

Kaunas

Klaipëda

14

Chapter 5

5.1. General Remarks

The development of the Lithuanian property market started in 1990 when the Seimas of Lithuaniaofficially declared its independence and laws related to land and real estate issues were among thefirst to be discussed.

Economic growth was accompanied by the development of business, which stimulated the demandfor both retail and office space.

Historically, prestige has been related to the location of business in the city centre, therefore,changes including reconstruction works, investments etc. started in the central parts and oldtowns of the capitals. In the initial stage of market development, the processes were quite similar:old-town apartments were reconstructed into office premises, shops were privatised, and roomson the first floor were transformed into retail areas. Such a development scenario could meet theinitial needs of growing markets, however, further development required new solutions, ideasand investments.

In the office market, the demand first of all arose among representative offices of foreign companies,foundations, and other financial institutions. The growing demand for premises and for the qualityof the construction increased the rent levels, which, in its turn, stimulated the development ofnew office premises.

Compared with other capitals of the Baltic States, Vilnius was the last to experience growth innew office construction but this helped to avoid mistakes leading to low occupancy and decline inrent levels as it happened in the capitals of the other Baltic States. Other cities of Lithuania arestill far behind development in Vilnius, as due to the limited size of the Lithuanian market ingeneral, there is no demand for representative offices in several towns, and the majority ofbusinesses is located in the capital. However, in Kaunas and Klaipëda, demand for the new premisesexceeds supply, what encourages developers to consider new projects in these cities. It is alsoworth mentioning that in Vilnius demand is mainly related to the premises for rent, while inKaunas and Klaipëda the majority of the demanded premises is for acquisition.

The retail space market development was determined both by economic development andgeographical features. Just as in other countries of the world, boutiques selling clothes and othergoods opened in the Old Town. As regards prestigious shops, the trends differ from country tocountry. This is determined by location and peculiarities of individual streets. Vilnius has a centralretail street � Gedimino Avenue. The concentration of shops and the location make this streetthe most convenient for retail. The number of retail outlets should increase after municipal andother public institutions move out to other locations. Kaunas, the second largest city of Lithuania,has a unique pedestrian area Laisvës Alëja, where all major brands are located. Other cities havetraditionally developed retail space in their central parts. In respect of shopping centres, Lithuanianretail chains are main builders and initiators of construction. While the biggest development ofshopping centres is in Vilnius, Kaunas and Klaipëda are also of interest for major retail chains.

The supply of industrial/warehousing space was determined by warehouses, factories etc. remainingfrom Soviet times. As the market developed, companies required higher-quality buildings andsuch premises were lacking. In this way many new non-speculative industrial and warehousingfacilities appeared, which, in its turn, produced a shrinking effect upon the market of potentiallessees and resulted in a stagnation of prices in this segment. Anyway, the demand for new premisesremains, encouraging developers to engage in construction of this type.

As regards the investment market, with the increased international demand for attractive investmentopportunities we now see some interest from strong international investors in the Lithuanian real

Introduction to the CommercialProperty Market

estate market. Lithuania is, however, still seen as a small local market with small liquidity and transparency, whichfor international investors leads to higher yield expectations.

The future membership of the EU has already boosted the local market with regard to international interest, butas long as the local market is non-transparent and has a limited liquidity, we are not going to see significant dropsin real investment yields. Investors trade yield for risk and as the Lithuanian real estate market in general offerslittle liquidity, investors are afraid of the possibilities of reselling their property investments with a real growth inproperty value.

With the present yields, some increase in the international interest for investing in real estate in Lithuania is,however, experienced.

5.2. Commercial Property Market Segments

In general commercial property market segments can be split as follows:- Office space market;- Retail space market;- Industrial/warehouse/logistic space market.

We will describe every segment of the Lithuanian commercial market below.

5.2.1. Office Market

Active office development processes have been taking place in Lithuania since 1999. The new buildings completed at theend of 2002 and in the beginning of 2003 are 90% occupied, with several new projects launched at business centres andin peripheral areas.

Usually the office space market is the largest in the capital cities, because the country is relatively small and it is notexpedient for a company to have offices in several cities; sometimes it is worth having only one office in the Baltic States.

Both the previous and the upcoming year is a period of active office construction as the office market is growingdynamically in Lithuania, mainly concentrating in Vilnius. Recently developed new office buildings and significantgrowth of the Lithuanian economy are having an impact on future office development projects.

Major developments in Vilnius are expanding into two districts: the business centre on A. Goðtauto, GeleþinioVilko, and J. Jasinskio streets that form the �Business Triangle� and the right side of the River Neris onKonstitucijos Avenue. Developments in Konstitucijos Avenue have high potential since the Municipality buildingproject and the Europa business centre building aim at making this street a new modern business area.

The development of both areas will be successful because of a convenient location, accessibility, sufficientparking space and concentration of properties for the same purpose.

There are some new office building projects planned, however, most of them depend on pre-leases. As developershave successfully rented almost all of their new premises, they started looking for potential possibilities to go forfurther developments, taking into account pre-lease conditions. The present market in Vilnius is to some extentfilled up and it will take some time for it to match demand for new premises with supply, therefore the developersstart constructions having at least 60%�70% pre-leased premises.

Estimated vacancy of the modern office premises is approximately 10% in Vilnius, however, with new projectsentering the market in 2004 and 2005 (the Europa office building and others), vacancy will increase, as there isa high competition to attract tenants. By the end of 2004 approximately 70,000 sq.m of new office space isplanned to be built in Vilnius.

Total stock of new modern premises in Vilnius in the beginning of 2004 was approximately 80,000 sq.m.

Supply

16

In other Lithuanian cities the markets are in a development stage, as the majority of the premisesare being used and owned by local companies themselves. There are a few projects of new premisesto be built in Kaunas, Klaipëda, Alytus and other cities. However, the main tenants are the samecompanies in every city � major telecommunication companies, insurance companies or banks.

There are two types of supply on the secondary market: old vacant premises that appeared as aresult of companies moving to newly-built offices and new constructions built to match therequirements of retail and warehousing. It is mostly located outside the central part of the city,and it depends on the operating business of the company.

Initially the prime office space demand in Lithuania was defined by the needs of internationalcompanies and representative offices. The greatest demand came from the pharmaceutical, insurance,information technology, and banking sectors. At the moment, however, more and more localcompanies realize the importance of high representation of their office premises, improved workingconditions for the employees, as well as the importance of the services provided by the landlord andthe state-of-the-art communications. Parking facilities, which are now becoming more and moreimportant, define one of the most important aspects of the demand for new premises.

On the other hand, leasing instead of owning the premises is becoming a new tendency for localcompanies as well, as parking facilities become more and more important in making decisionregarding the rent for certain premises.

According to KOBA research, small and medium size companies that normally require from100 sq.m to 300 sq.m account for over 70% of the demand for high-standard office space fromVilnius. Banks, major telecommunications, consulting companies, software companies, andconsumer product companies require larger spaces, however, most of them have already establishedthemselves in the new premises.

The majority of companies are moving to new premises, which meet high standard requirements.According to KOBA research, companies require ventilation, air conditioning and humidificationsystems. High computer and telecommunication technologies are compulsory as it is the core ofmodern business.

However, parking does not reflect the quality of premises, it is definitely one of the primaryvalues of an office building. Offices located in business districts should allocate a parking placeper 25 sq.m of the rented office space.

In addition to the net rental of office space, the aspects usually valued by lessees are as follows:- Location;- Quality of management services;- Utility costs level;- Design of rooms;- Parking options and cost of parking;- Convenient access;- Catering options for the employees;- Reputation of the building.

In other Lithuanian cities, demand for new premises is relatively stable. However, demand to alarge extent depends on the rent level. As the cost of a new office building is almost the same inVilnius and in other cities, the rent should attract local tenants.

Demand

Demand forQuality, Parking

and Prestige

Due to an increased supply of high-quality standard premises, in Vilnius the rent has lowered slightly from 65 to60�55 LTL/sq.m/month on average and remains relatively stable. No significant fluctuations are expected in thenear future, although this situation could change after the relocation of existing companies compared to newentries to the commercial market. Lithuania can still expect a major influx of some projects that are now in designstages and will achieve pre-leases. The rental charge for high-quality standard office premises in the �BusinessTriangle� varies between 50 and 60 LTL/sq.m/month. It will remain stable until further developments come to themarket. Rent in non-business locations, city centre, and downtown varies from 40 to 45 LTL/sq.m/month.

We anticipate that the rent in high-quality buildings will remain stable at least until new developments enter themarket, although affordable rent in low-quality buildings will continue to decline.

In other Lithuanian cities rent is significantly lower, however, the level of the quality premises also differs fromthe newly built modern premises.

5.2.2. Retail Market

Generally, the retail market could be characterised as a market actively developing in Lithuania, which is, on theother hand, far behind the other Baltic countries and has a great potential to develop.

Between 1998 and 2001, there was a significant increase in supply of supermarkets, hypermarkets and shoppingcentres in Lithuania as a result of the growth in the economy and consumer spending power. Consumers gotused to shopping centres rather than to retail streets of the city centre.

As shopping centres are convenient for consumers and are attracting more and more shoppers, this factor can have aside effect on retail on high streets. Though shopping centres are numerous in European countries, high streets are stillleading in rent, sales turnover, and the number of consumers. It varies from country to country, from city to city, buthigh streets always remain as the starting point of clothing retail chains, so almost every retailer seeks to establish aflagship store there. Only then did they expand into other streets, shopping centres or other cities. The number ofsmall shop units is decreasing and this is a natural phenomenon, as shopping centres have taken the biggest share ofthe retail market. On the other hand, cosy and convenient shopping in small shops will remain popular. As a rule allmajor brands establish their first shop in the capital of the country. The main concentration of shops is in Vilnius.Kaunas has a unique shopping street, Laisvës Alëja, where all major brands have also established their shops. InKlaipëda, as in other Lithuanian cities, major shops are also located in the central part of the town.

The expansion of food retail chains has slowed down as the market absorbed a big amount of retail space between2000 and 2002, and now developers are looking for the possibility to build new shopping centres. On the otherhand, supply of food retail space has no influence on general retail market rent, as most of the projects werebuilt to suit. Keen competition among large food chains is observed at present. For the time being, VP Marketremains the leader; the second largest food retail chain RIMI Lietuva is restructuring its strategy, and a moreaggressive strategy is to be expexted. The IKI chain has targeted its special segment and has a stable position inthe market at the moment. The NORFA chain is becoming more and more popular as a cheap goods retailer.

VP Market has opened the first shopping centre Akropolis in 2002 and the great success of the project showedthat at the moment there is a significant lack of such developments in the market. There are several plans ofdifferent developers to open new shopping centres in Vilnius (Europa centre, G&C centre, Vilnius Dairy shoppingcentre), Kaunas (Akropolis) and in Klaipëda. The existing stock for retail is estimated at 250,000 sq.m. It isplanned to build 120,000 sq.m of modern retail space between 2004 and 2005.

There are also numerous developments in the DIY (Do It Yourself) segment. A few shopping centres have beenopened in the capital and other cities. Senukai remains the leader; some other companies such as Jysk and

Rent

18

Rubikon should also be mentioned. There is a new developed area in the northern part of Vilnius,called North Town where DIY shops are concentrated.

Capital cities are particularly attractive for foreign retailers� activity expansion in the Baltic Statesas their plans for the retail location are usually directed toward the capital of the country. If thecities of a country are considered too small for business expansion, the entire Baltic region maybe considered as a single area.

Currently, the demand for retail market space comes mostly from local retailers. There are veryfew well-known foreign retailers active in the market at the moment. Often retailers from a BalticState are expanding into other Baltic countries, though there is a strong interest and markettesting from foreign retailers.

High Streets Retail Market

There is not sufficient supply of retail space on high streets in all Lithuanian cities. The majority ofnew shops are opened due to change of tenants. Since there is a scarce supply of land plots land in thispart of the city, new developments are rarely made there. In the future, a supply of this kind of spacemay appear because high streets still have big gaps of retail premises where government and municipalityinstitutions are located, and we think that those premises will be sold or rented to retailers.

The demand for this kind of space will remain stable, with some changes depending on the local market.In Vilnius, for instance, the regeneration of the city centre and transport/parking improvements willincrease the attractiveness of it as a shopping destination; there will undoubtedly be an increase in the levelof demand and developments of this type of space. Although the main high streets will be under pressuredue to strong competition with shopping centres located in the centre, it is doubtful whether this willaffect their attractiveness in the long run. However, international retailers and growth of the retail marketare factors indicating the presence of demand for retail premises in the country.

In Vilnius the development and concentration of shops is the highest compared with other Lithuaniantowns. It is not only due to the status of the capital, as we have stated above, but also to a relatively biggerpurchasing power of the inhabitants and a larger number of buyers in general.

However, Kaunas is also a very attractive area for retailers due to its geographical location and theunique pedestrian area in the centre of the city.

The rent in Vilnius high streets remains stable and varies between 100 and 200 LTL/sq.m/month. There is a difference in rent between Gedimino Avenue and other Vilnius streets. Theinterest in Gedimino Avenue after its reconstruction and the construction of underground parkingunder the street has increased the interest of foreign retailers. This might lead to increased rentsin the future.

Supply

Demand

Rent

Supply

Demand

Rent

ConsumerBehaviour

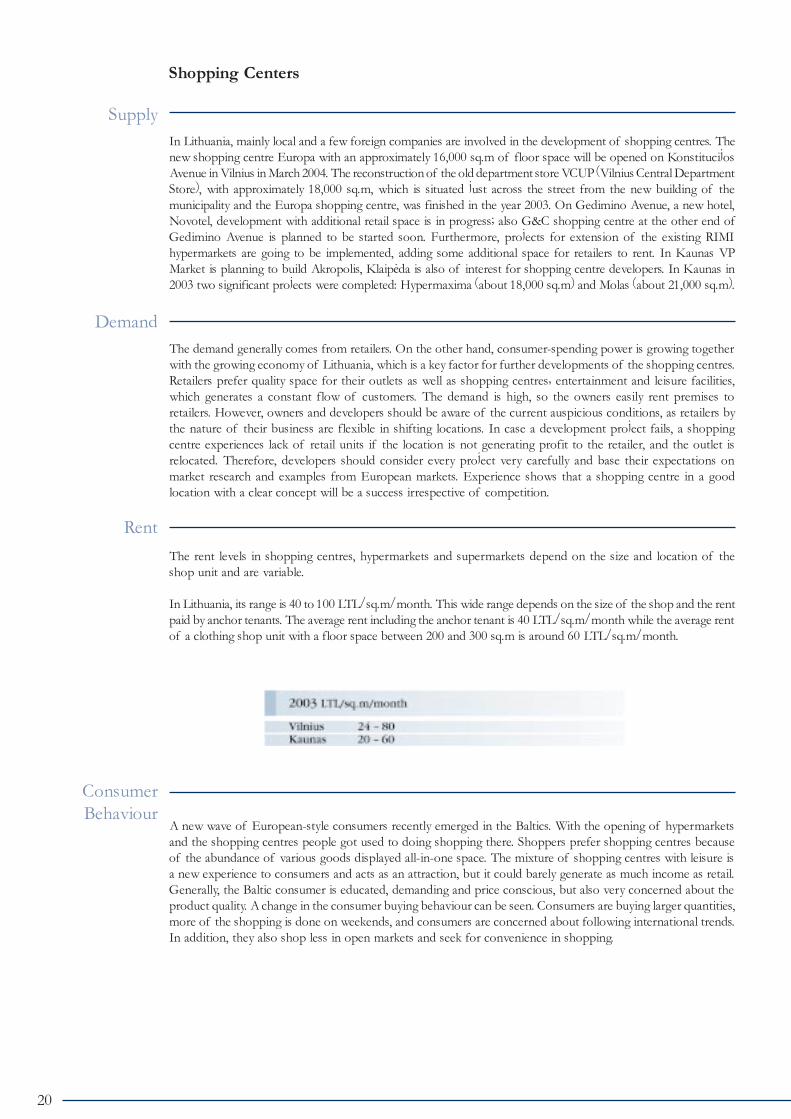

Shopping Centers

In Lithuania, mainly local and a few foreign companies are involved in the development of shopping centres. Thenew shopping centre Europa with an approximately 16,000 sq.m of floor space will be opened on KonstitucijosAvenue in Vilnius in March 2004. The reconstruction of the old department store VCUP (Vilnius Central DepartmentStore), with approximately 18,000 sq.m, which is situated just across the street from the new building of themunicipality and the Europa shopping centre, was finished in the year 2003. On Gedimino Avenue, a new hotel,Novotel, development with additional retail space is in progress; also G&C shopping centre at the other end ofGedimino Avenue is planned to be started soon. Furthermore, projects for extension of the existing RIMIhypermarkets are going to be implemented, adding some additional space for retailers to rent. In Kaunas VPMarket is planning to build Akropolis, Klaipëda is also of interest for shopping centre developers. In Kaunas in2003 two significant projects were completed: Hypermaxima (about 18,000 sq.m) and Molas (about 21,000 sq.m).

The demand generally comes from retailers. On the other hand, consumer-spending power is growing togetherwith the growing economy of Lithuania, which is a key factor for further developments of the shopping centres.Retailers prefer quality space for their outlets as well as shopping centres� entertainment and leisure facilities,which generates a constant flow of customers. The demand is high, so the owners easily rent premises toretailers. However, owners and developers should be aware of the current auspicious conditions, as retailers bythe nature of their business are flexible in shifting locations. In case a development project fails, a shoppingcentre experiences lack of retail units if the location is not generating profit to the retailer, and the outlet isrelocated. Therefore, developers should consider every project very carefully and base their expectations onmarket research and examples from European markets. Experience shows that a shopping centre in a goodlocation with a clear concept will be a success irrespective of competition.

The rent levels in shopping centres, hypermarkets and supermarkets depend on the size and location of theshop unit and are variable.

In Lithuania, its range is 40 to 100 LTL/sq.m/month. This wide range depends on the size of the shop and the rentpaid by anchor tenants. The average rent including the anchor tenant is 40 LTL/sq.m/month while the average rentof a clothing shop unit with a floor space between 200 and 300 sq.m is around 60 LTL/sq.m/month.

A new wave of European-style consumers recently emerged in the Baltics. With the opening of hypermarketsand the shopping centres people got used to doing shopping there. Shoppers prefer shopping centres becauseof the abundance of various goods displayed all-in-one space. The mixture of shopping centres with leisure isa new experience to consumers and acts as an attraction, but it could barely generate as much income as retail.Generally, the Baltic consumer is educated, demanding and price conscious, but also very concerned about theproduct quality. A change in the consumer buying behaviour can be seen. Consumers are buying larger quantities,more of the shopping is done on weekends, and consumers are concerned about following international trends.In addition, they also shop less in open markets and seek for convenience in shopping.

20

5.2.3. The Industrial Market

As the level of automation is increasing, production is becoming increasingly capital-intensive.Expansion of new products and new markets require a strong capital base. This has made manycompanies outsource some of the distribution to external companies and generally, as it hasbecome possible, they are increasingly outsourcing the ownership of buildings. The old traditionof owner-occupied distribution space is changing.

In Lithuania, the trend of modern warehouse space has just emerged and currently very fewmodern warehouse buildings are built for rent to other companies.

Thus KOBA concludes that the focus on warehouse/distribution space and locations is going toincrease in the near future, which will give new opportunities to developers and investors togetherwith many distribution companies that are expected to grow.

The demand in the industrial/warehouse market is growing, but there is still the lack of newspeculative industrial space. Up to now all new developments have been completed for their ownuse or at the request of potential tenants. The conversion of former industrial premises in thecentral parts of the cities continues to grow. The premises on the main streets are reconvertedinto commercial premises and lower-class office premises. The remaining part is used forwarehousing or adapted to small-scale industry and service purposes. The lack of logistic centresforces seekers of the premises to develop their own centres. The first priority for developmentsof the projects is location and accessibility from the logistic point of view represent top prioritiesfor development of projects.

It is worth mentioning that rents for premises in Vilnius conforming with new quality standardsand conveniently located (in the city) amount up to 20 LTL/sq.m/month, new modern premisesoutside the city centre, from 12 to 18 LTL/sq.m/month. The remaining premises are rented in arange of 5 to 15 LTL/sq.m/month. In Kaunas the rent for premises varies from 8 to 20 LTL/sq.m/month, in Klaipëda, from 6 to 12 LTL/sq.m/month.

As the majority of new premises are built for their own needs and/or as a result of the expansionof companies they will not increase the rented premises market considerably:

- The volume of vacant premises may increase due to moving out of former lesseesto premises built specifically to meet their needs;

- New production premises or storage areas increase the value of the nearby unusedland and create preconditions for the origination of new districts favourable froma logistical standpoint.

Distribution

Industrial Space inLithuania

Rent

Chapter 6 The Lithuanian Investment Market

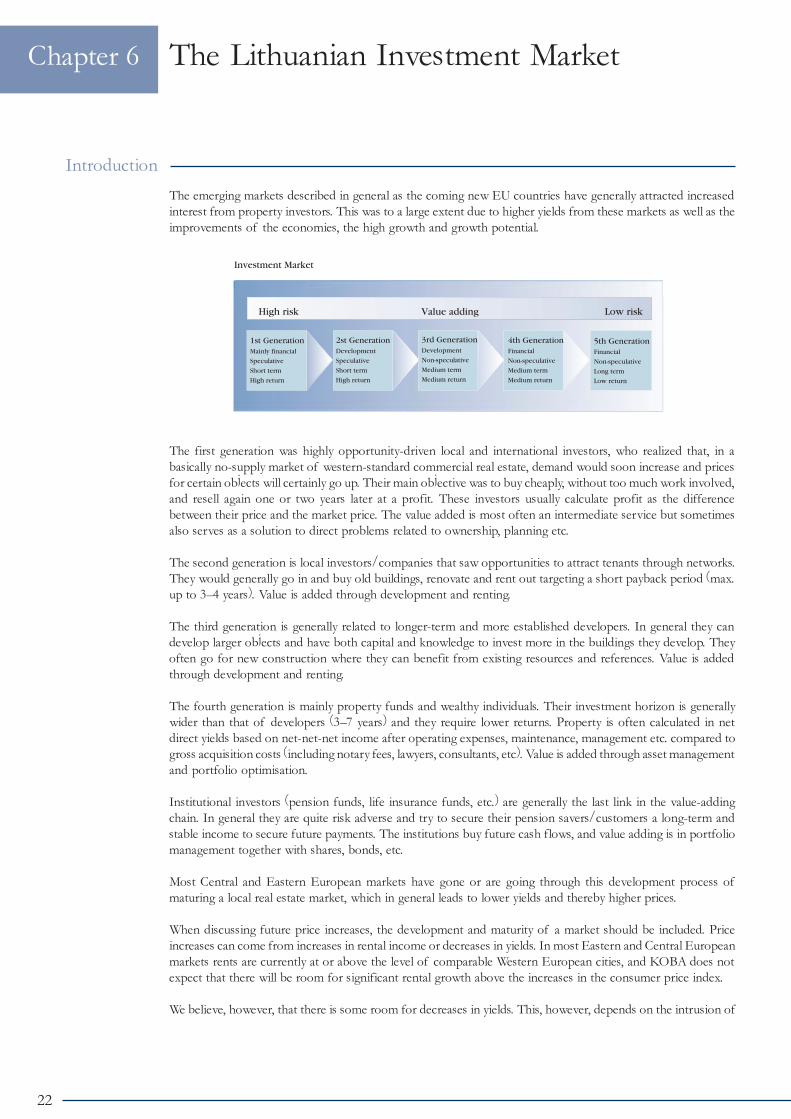

The emerging markets described in general as the coming new EU countries have generally attracted increasedinterest from property investors. This was to a large extent due to higher yields from these markets as well as theimprovements of the economies, the high growth and growth potential.

The first generation was highly opportunity-driven local and international investors, who realized that, in abasically no-supply market of western-standard commercial real estate, demand would soon increase and pricesfor certain objects will certainly go up. Their main objective was to buy cheaply, without too much work involved,and resell again one or two years later at a profit. These investors usually calculate profit as the differencebetween their price and the market price. The value added is most often an intermediate service but sometimesalso serves as a solution to direct problems related to ownership, planning etc.

The second generation is local investors/companies that saw opportunities to attract tenants through networks.They would generally go in and buy old buildings, renovate and rent out targeting a short payback period (max.up to 3�4 years). Value is added through development and renting.

The third generation is generally related to longer-term and more established developers. In general they candevelop larger objects and have both capital and knowledge to invest more in the buildings they develop. Theyoften go for new construction where they can benefit from existing resources and references. Value is addedthrough development and renting.

The fourth generation is mainly property funds and wealthy individuals. Their investment horizon is generallywider than that of developers (3�7 years) and they require lower returns. Property is often calculated in netdirect yields based on net-net-net income after operating expenses, maintenance, management etc. compared togross acquisition costs (including notary fees, lawyers, consultants, etc). Value is added through asset managementand portfolio optimisation.

Institutional investors (pension funds, life insurance funds, etc.) are generally the last link in the value-addingchain. In general they are quite risk adverse and try to secure their pension savers/customers a long-term andstable income to secure future payments. The institutions buy future cash flows, and value adding is in portfoliomanagement together with shares, bonds, etc.

Most Central and Eastern European markets have gone or are going through this development process ofmaturing a local real estate market, which in general leads to lower yields and thereby higher prices.

When discussing future price increases, the development and maturity of a market should be included. Priceincreases can come from increases in rental income or decreases in yields. In most Eastern and Central Europeanmarkets rents are currently at or above the level of comparable Western European cities, and KOBA does notexpect that there will be room for significant rental growth above the increases in the consumer price index.

We believe, however, that there is some room for decreases in yields. This, however, depends on the intrusion of

Introduction

22

General

Offices

both fourth and fifth generation investors. In general these investors require an established,transparent and liquid market, as they have to be able to adjust their portfolios regularly.

We believe that for the most serious investors the current yields together with the currently verylow interest are providing very attractive opportunities for high returns, with prime yields currentlyin a range between 10.5% and 11% and interest rates in a range of 4.6%�6%.

Generally the Lithuanian real estate investment market is concentrated in and around Vilniuswhich is still considered the main place of interest for particularly international investors.

In the last two years, we have seen the first real investment transactions described as the investmentin fully developed and rented property based on present and future net income streams contraryto investments based on development potential.

These investments have mainly been driven by international investors of which the largest currentlyis the Baltic Property Trust.

Within the last 12 months we have, however, seen interest from other investors increase dramatically.This is of course to some extent driven by the international increased interest in real estateinvestments, but also to a large extent by the strengthened trust in the emerging markets.

The local investment climate is quite differentiated and tends to be very speculative in specialareas and segments. The local valuation methodology is often dominated by comparable salesapproach and thereby sometimes without relation to the real income and outgoings.

As previously mentioned, mainly due to the limited liquidity in the market it is difficult to havereliable empirical evidence on the market yields. However, there is a clear trend in the transactionsthat have been carried out over the last 24 months.

There is some demand for office properties, but generally only for A-class property in the bestlocations. Generally the investment markets focus on newly built office buildings but also oldercentral properties with a strong tenant base are interesting.

In Lithuania, we have seen within the last two years four office investment transactions withinternational investors. Several other transactions have been clinched but they have all been basedon buyer occupancy or development potential.

Yields have developed significantly and are currently considered at 10.5% prime net yield comparedto 12.5%�13% just a few years ago. Before then it made little sense to discuss yields as there wasno real investment market however the calculated yield/return on investment in renovated propertydropped from approx. 20%�25% just after independence in 1990.

Offices are often sold to the local companies and investors as individual apartments in largerbuildings. This is partly due to the low interest level where real estate can be financed directly viamortgage or bank financing or via leasing. Interest rates are considerably lower than the currentproperty investment yields. Also the great local optimism and faith in future price increases forreal estate play a significant role in this market.

Prices for office apartments generally range from 3,200 to 4,800 LTL/sq.m in prime locations;prices in newly constructed buildings close to the city centre range between 2,400 and 3,200LTL/sq.m and in locations away from the city centre, 1,600�2,400 LTL/sq.m.

Retail

Industrial/Warehouses

Hotels

Generally we see a great demand for buying independent retail units on the major retail locations in Vilnius likeGedimino Avenue, Vokieèiø and Didþioji streets and others, mostly driven by local retailers occupying the spacethemselves. There is currently little willingness to sell these units as financing is cheap and expectations to futureprice increases are high. There is a high preference by local retailers to buy instead of renting in high streetlocations.

Shopping centres have traditionally as previously mentioned been developed and built by the major food retailerssuch as Rimi, Maxima (VP Market) and IKI. As the local financing has been cheap these have so far beenreluctant to sell based on the same reasons as in the high streets. We expect, however, that more developers willenter this area in the near future and new shopping centres will become available for investments in the comingyears.

As basically no transactions have been clinched in this area in Lithuania, there is no empirical evidence on themarket yield. However, comparable transactions in other Baltic countries have been carried out with yield levelsranging between 10.5% and 11.5% for prime city locations including larger regional shopping centres and up to12.5%�13.5% for secondary locations.

The industrial property is exclusively dominated by owner/occupiers and there is basically no real investmentmarket. Market prices for new premises vary from 1,200 LTL/sq.m and up to 1,800 LTL for the basic buildingsdepending on specific requirements. Old Russian-style buildings in the same areas can, however, be acquireddown to 200�600 LTL/sq.m. In secondary cities like �iauliai, Alytus and others, the cost can go even lower, butthen the premises would generally require major renovation.

The warehouse/logistic market was earlier also dominated by owner occupancy, but there is a trend to anincreased demand for rented premises. This segment is, however, currently not supplied, meaning that basicallyall new warehouse properties are built to suit. Although one would expect that this market would provide a goodbalance between owner and occupier requirements for longer lease contracts we have still seen very few transactionsin this segment � mainly due to a large gap between the lending rate and the yield.

Currently the yield on modern buildings ranges between 11.5% and 14% depending on the tenant, the length ofthe lease and the specifics of the building.

There is currently some oversupply of hotel rooms in Vilnius, which has reduced general occupancy figures.Almost all hotels in Lithuania are either owner operated or owner managed with an operating agreement.

There have until now been no independent hotel investment transactions but we expect that the yields forestablished hotels with a proven track record would range between 12% and 13% based on an operating agreementwith an international, well recognized operator but owner managed. For a leased hotel with a major hoteloperator and a 7�10 year lease contract, we expect the yields to come down to 10.5%�11%.

24

Chapter 7

A SWOT analysis is the most common tool in analysing the expected performance of equities. Itdescribes in verbal terms strong and weak sides of an investment together with opportunities andthreats. It does not pretend to give an exact answer to invest or not to invest, but illustratesexpected yields and risks.

- Demand for high quality properties in attractive locations;- Favourable investment environment;- EU membership;- High yield level;- Well-educated and cheap labour force;- Attractive financing;- Market space for big retail centres.

- Limited possibility to exit the property market;- High competition among developers might have an impact on vacancy or rental levels

(in office segment).

- Fast growing economy and consumer spending;- A stable political climate with a democratic spirit;- Development in consumer habits towards the western style;- A low-cost market compared with West and Central Europe;- A higher level of productivity caused by a well-motivated population.

- The so-called �shadow economy�;- Political instability in neighbouring countries;- Overestimated expectations of property owners regarding values of the property after

joining the EU;- Excessive development.

SWOT analysis

Strengths

Opportunities

Weaknesses

Threats

Like other new markets the Lithuanian property market is characterised by little transparency and thereforedifficulties in verifying market data. A low turnover and only a few qualified consultants are other barriers toobtaining valid information.

The Lithuanian cities except Vilnius generally have a look of decay and many buildings suffer from a lack ofinternal and external maintenance. In many situations, where restrictions on historical sites are not imposed, therational solution will be to tear the old buildings down and build new modern properties. The geographicallocation of many official buildings, e.g., government buildings, and the space used is chosen with little regard tomarket economic elements. Therefore they are often placed in the best locations and prime addresses seen froma commercial standpoint.

This compared with potential building possibilities within a short distance from the centre means that a growingdemand for office space, where a prime city address is not a must, can be satisfied in a shorter run.

While speaking about yield dynamics from the investors� point of view, the yield has more than only compensatedthe drop in commercial space rent prices. This picture was seen in other major Eastern and Central European(CEE) cities just a few years ago, where investors, who have allocated their capital in property investments have,in general, succeeded in making very profitable deals.

We believe that by entering the Lithuanian property market now a similar investment design is possible, especiallywithin retail and investments in high-street locations in the largest cities.

Stiff competition in the local borrowing market is expected within the forthcoming years due to the increasingnumber of foreign financing sources. It will make the yield fall, as it was also observed in other major EastEuropean cities some years ago.

Nowadays there are also some very attractive possibilities in the Lithuanian property market for investors withlow-risk strategies. While struggling for market shares, companies are focusing on their core businesses byestablishing branch offices and retail shops all over the country and thus employing their own capital. Since thelocal financing market does not function properly, the blue chip companies are forced to look for other financingsources for further expansion. This situation is favourable for foreign investors, who gain excellent opportunitiesto acquire new modern well-located shopping centres by applying the sale and lease-back models and excepting amaster lease.

The initial shortage of western quality office space � both in the very centre of Vilnius and in urban areas � hasattracted real estate developers to build some new modern commercial centres. As experience shows, not all ofthem have succeeded to rent out at the initially budgeted price though. These cases illustrate that the market isnot yet ready to pay above an average for a higher quality facilities.

Moreover, the commercial structure and size and a relatively small international influence of Lithuania do notindicate a bigger demand for administration and representative offices in the very centre of Vilnius in the shortrun. The allocation of capital in relation to the country�s extent seems not to underline any need for big prestigeoffice or business centres at prestigious addresses for the moment.

We can see that the office space rent prices have dropped about 10%�15% during the last two years. However,we do not think the reasons for this decrease in rent price is the same for Vilnius as for Warsaw, Budapest orPrague. In Vilnius only relatively few square meters of commercial space, both office and retail, have been builtthe last years, in comparison with hundreds of thousands built in major cities of CEE. The latter have experienceda sudden decrease in office space rent prices, because in this market the supply has exceeded the demand. Theretail space prices were affected much less as the demand created by increasing inflow of retailers has followedthe supply.

Chapter 8 KOBA�s Expectations of the Market

Offices

26

Neither demand nor the situation in the financing market or office rental levels motivate realestate developers to speculate erecting new office buildings without finding tenants (minimum50%) before starting constructions. We foresee this situation to be favourable for the furtherdevelopment of the Lithuanian property market.

Almost the same conclusions can be made speaking about investments in industrial properties.Lithuania has an infrastructure, which gives many alternatives for location of new industries. Italso gains attractiveness for industries with its cheap labour force, a suitable geographical location,free economic zones, etc. The focus for many industrial developments is, however, often in largersecondary cities like Alytus, Ðiauliai or Paneveþys as these cities are very competitive on costs oflabour and real estate. Others tend to look for the advantages of locating in the Free EconomicalZones in Klaipëda and Kaunas as some tax and other incentives are attached to these locations.Besides to some extent in Kaunas and Klaipëda no real investment market can be foreseen.

For warehouses the distribution areas and corridors in Lithuania remain in focus. Locations onthe Vilnius � Kaunas � Klaipëda highway currently have a main priority among distributors andavailability of land on the corridor primarily near Vilnius is currently very scarce. With a futuredevelopment of the Via Baltica road from Warsaw to Helsinki and St. Petersburg via the Balticcountries this corridor may receive further attention in the future.

The port of Klaipëda can gain some advantages in the form of a regular transit service betweenEastern and Western Europe.

We believe that the investment market for warehouse/logistics buildings will increase significantlyin the near future.

Industrial

The harmonisation of legal acts with those of the European Union and the reform of the administrative systemin Lithuania has contributed to the protection of ownership, legal occupancy and investments. The real estatemarket in Lithuania is regulated following generally accepted principles of ownership immunity and protectionof rights of a just acquirer (possessor). Also, the principles of equal treatment and equal protection are the mainprinciples of the investment law, meaning that both Lithuanian and foreign investors are subject to equal businessconditions and their rights and lawful interests are equally protected by law.

Lithuania is eagerly awaiting its forthcoming accession to the EU. Numerous changes in important areas forcommercial real estate investment such as tax framework, accounting or real estate laws have to some extentalready been made or are planned for the near future. Now is the time to plan investment structures and modelsin the light of the new regulations, and to determine strategies for the future. However, your attorney and taxadvisor should always be consulted about the risks and effects of whatever steps you decide on.

General Provisions

Principally, there are no severe limitations to the acquisition of land and buildings for development by foreigners.Foreign investors have the right to buy or lease buildings for their commercial activities as well as lease orpurchase land plots for the construction of buildings.

For the protection of owner interests, real estate sale�purchase agreements have to be certified by a notary.Following the general principles of law, the Lithuanian law is always applied to international transactions concerningreal estate located in Lithuania. The transfer of real estate has to be documented by a statement of transfer-acceptance that is signed by the buyer and the seller.

A notarised real estate sale�purchase agreement is binding for the seller and the buyer. However, the sale andpurchase of real estate may be invoked on third parties only upon proper registration of such agreements withthe Real Property Register.

Acquisition of Land

Rights of foreigners to acquire land in Lithuania are established in the Constitution of Lithuania and regulatedby the special Constitutional Law on Implementation of Part 3 of Article 47 of the Constitution. With certainexceptions of the entrails of earth (underground) and nationally significant land areas exclusively belonging tothe State, other land, inland waters and forests may be acquired into ownership by foreigners as explained below.

The main requirement for foreigners who wish to acquire land in Lithuania is meeting the criteria of origin, i.e.the criteria of the European and transatlantic integration, which means that only those foreigners may acquireownership of land in Lithuania who are citizens or permanent residents of, or legal persons or other legalorganisations established in, one of the below listed foreign states:

1. A Member State of the European Union or a State that entered into the Europe Agreement(Association Agreement) with the European Communities and their Member States;

2. A Member State of the Organisation for Economic Cooperation and Development (OECD), aMember State of the North Atlantic Treaty Organisation (NATO), or a State which is party to theEuropean Economic Area (EEA) Agreement (all EU Member States and Iceland, Liechtensteinand Norway are parties to the EEA Agreement).

Permanent residents of Lithuania without Lithuanian citizenship are also deemed corresponding to the criteria of origin.

Following the Constitutional Law there are two different procedures established for acquisition of land byforeigners.

Legal Facts about the CommercialProperty Market

Chapter 9

Real Estate Acquisition

28

Until Lithuania joins the EU, foreigners complying with the criteria of origin may acquire intoownership only non-agricultural land in Lithuania designated and required for:

- Operation of the buildings designated for the business activities of a foreign personthat are indicated in the incorporation documents of that foreign person;

- Construction and operation of new buildings to be designated for the mentionedbusiness activities.

Foreigners intending to acquire land plots for their business activities as described above have toobtain a permit of the respective County�s Governor for land acquisition.

After Lithuania joins the EU, foreigners complying with the criteria of origin will be entitled toacquire land, inland waters and forests following the same conditions and procedure as applied tothe citizens and legal persons of Lithuania, with certain limitations for acquisition of agriculturaland forestry land during the seven-year transitional period. During the transitional period onlyforeign individuals who have been permanently residing and engaged in agricultural activities forat least three years as well as foreign legal persons and other organizations that have established inLithuania their representative offices or branches will be allowed to acquire agricultural and forestryland.

Foreigners that do not comply with the established criteria may lease the land plots or use themon some other basis established by law except for ownership. Also, land may be acquired indirectlyas described in the section Indirect Real Estate Acquisition below.

Acquisition of Buildings

As for buildings, premises or other constructions, there are no substantial restrictions imposed bythe Lithuanian law related to the acquisition of these types of real estate by Lithuanians orforeigners.

It is noteworthy that for the sake of the acquirer the Lithuanian law establishes the connectionbetween the land and buildings. Pursuant to the Civil Code of Lithuania, if a land plot is subjectto acquisition, it is presumed that the buyer also obtains the ownership right to the buildings,constructions and facilities on this plot of land, unless the sale�purchase agreement specifiesotherwise. On the other hand, by an agreement on sale-purchase of a building or other real estatethe seller has to transfer to the buyer the rights to the plot of land, on which the building islocated. In case the seller of the building is also the owner of the land plot, the seller has totransfer to the buyer either the ownership right to that land plot of land or the right of the landlease or development. If the seller does not own the land on which the sold building is located,the buyer acquires the right to use a respective part of the plot of land under the same conditionsas the seller.

Indirect Real Estate Acquisition

There are no restrictions for foreigners on the acquisition and sale of interest in enterprises forthe purpose of acquiring real estate indirectly. Enterprises established in Lithuania notwithstandingwho has their effective control are entitled to acquire land plots and buildings without anyrestrictions.

Companies of limited liability are the common legal form in Lithuania. �Closed� stock companieswith a minimum capital of 10,000 LTL (approx. 2,900 EUR) and up to 250 stockholders and theso- called �open� stock companies with a minimum capital of 150,000 LTL (approx. 43,443 EUR)are the two alternatives for companies. A special kind of companies is controlling investmentcompanies investing mainly in securities. The Lithuanian law, designated to satisfy private interests,has established a number of other legal forms that may be chosen for private ownership and the useof real estate: a personal enterprise, a general partnership, a limited partnership as well as acooperative company, an agricultural company and other. With the exception of limited partnersin a limited partnership, personal enterprises and partnerships are regarded as enterprises withunlimited responsibility. Other mentioned enterprises are with limited liability.

All registration differences of enterprises of so-called �local� capital and of �foreign� capital have been eliminated.A new integrated Register of Legal Persons has been recently established for the purpose of accumulating,protecting and providing information on all Lithuanian legal persons, including all kinds of enterprises. Anenterprise is considered to be established only when this enterprise is registered in the Register of Legal Persons;upon registration with the Register an enterprise is issued a certificate of an established form and given a registernumber (code). Consequently, any changes of incorporation documents and data of the enterprise are effectiveonly after they are registered in the Register of Legal Persons.

Privatisation

Real estate may also be acquired following the special procedures of privatisation of state and municipal property.Usually, investors in state and municipal property are asked to assume certain contractual obligations, which aremainly contributing to preservation and development of such property.

Privatisation may take the form of any of the following: public sale of shares, public auction, public tender, directnegotiations or transfer of control of state or municipality�controlled enterprises. Investors may negotiate settlementfor privatised property in instalments and, depending on the form of privatisation and the privatised property, paymentsmay be allocated during the period of one to five years. Under certain conditions, for instance, major investment in theleased state or municipal buildings or premises, such premises may be later privatised according to an agreement onlease with option to purchase allowing the investor to settle for the real estate during the lease period up to ten years.

The latest information about privatisation objects may be found in the Information Bulletin on Privatisation(Informacinis privatizavimo biuletenis). Privatised property is sold by privatisation institutions such as the State PropertyFund (in case state property is privatised) or municipal administration (in case municipal property is privatised).

Both Lithuanian enterprises and foreigners may lease land and buildings, either from the state or from privateowners. Any agreement for the leasing of real estate is to be concluded in written form. Such agreement may beinvoked in respect to third parties only upon its registration with the Real Property Register.

With the exception of certain lease conditions specified by law, provisions of the lease of real estate are negotiable.Some of the lease conditions regulated by law are 1) terms of state-owned land leases may not exceed 99 yearsand other real estate may not exceed 100 years; 2) terms of state-owned land plot for agricultural purpose maynot be shorter than five years.

Commercial real estate leases typically have terms of three or more years. A lessee that has duly performedunder the terms of a lease agreement shall be entitled to a pre-emptive right to renew the lease agreement and isentitled to restitution if the lessor has failed to comply. A land lease agreement may be terminated with twomonths minimum notice if the land is not for agricultural purpose, or three months notice if the agreement ofthe agricultural land lease is terminated. An agreement of building lease may be terminated under certaincircumstances as established by law and the contract.

Rent fee is often denominated in the Litas by establishing a firm rate with Euro (3.4528 LTL to 1 EUR) or inEuros if a foreigner is a party to the lease agreement. The quoted rent fee generally does not include utilities andservice charges and value added tax (18%) that are added on the rent fee.

There are no particular restrictions imposed on the construction activities of foreign enterprises. According tothe Law on Construction, both Lithuanian and foreign persons can benefit from construction rights to theextent limited by law.

The principal legal requirements include possession of the land on which construction activities are to beundertaken. Land developers thus have to own the land or use the plot on other legal basis. The second step isto obtain planning permission for the building. The developer should also be in the possession of constructionpermit that is issued based on complete architectural plans to comply with general area development plans. Theprocedure for issuance of construction permits has been simplified and is based on a principle that all issueshave to be addressed to one administration centre. A construction permit can be obtained from the local

Real EstateLease

Planning andDevelopment

30

municipality if the developer submits certain documentation. A construction permit is normallygranted for a period of ten years.

The owner is entitled to use the newly constructed or reconstructed building after it has beenaccepted as suitable for usage by a respective commission. The next step is to register the buildingin the Real Property Register.

The Real Property Register contains all actual information on buildings and land plots registeredin the Real Property Register, rights to real estate and their encumbrances. One can receiveinformation from the Real Property Register on changes in real estate, mortgages on buildings orland plots including pledges of land lease rights, imposed seizures, civil cases brought to the courtregarding real estate as well as registered agreements or decisions made regarding the legal statusof real estate, such as concluded lease agreements and equivalent.

As mentioned, all real estate sale-purchase agreements have to be signed in the presence of anotary who verifies the agreement for its legality as well as notifies the Real Property Register onthe concluded sale-purchase agreement of a particular property. Nevertheless, the buyer of hisown sake should apply to the Real Property Register for registration of his ownership right to theproperty after the transfer-acceptance of the property takes place. Even if the registration of theowner change in the Real Property Register is not mandatory, no further real estate transactionswould be possible as long as the registration is not completed.

The notary fee depends on the transaction amount and counts as a percentage of the pricepayable for the purchased property. For example, if the price is over 100,000 LTL (approx. 29,000EUR), the notary fee would be 790 LTL (approx. 230 EUR) plus 0.5% of the price exceeding100,000 LTL.

Real estate owners are free to mortgage their property in order to secure the existing or intendedundertakings and obligations arising with respect to land transactions, commercial loans andother. It is noteworthy that the mortgaged property remains with the owner and does not eliminatethe owner�s rights to use and dispose of the mortgaged property taking into account the rights ofthe creditor.

As other real estate transactions, contractual mortgage has to be certified by a notary and registered.Divisions of Mortgages at the local courts are in charge of the registration of mortgages thatcome into effect upon registration in the Register of Mortgages. Real estate mortgages are commoncollateral on loans issued by Lithuanian banks for the acquisition and development of real estate

The Bank of Lithuania provided the following statistics on average loan interest rates proposedby major Lithuanian banks in January 2004 that were decreasing throughout the year 2003.

Real PropertyRegister

Mortgage

Financing

Notary

The investor rights and lawful interests are secured by the Law on Investments and other regulations. An investorhas the right to manage, use and dispose of the assets he invested in and, upon payment of the taxes prescribedby the laws of Lithuania, to convert the profit into foreign currency and transfer it abroad without any restrictions.Damage inflicted upon the investor by unlawful actions of state or local authorities is compensated according tothe procedure established by law.

The Constitution of Lithuania guaranties inviolability of property. Therefore, investment is protected fromexpropriation following the generally accepted principles, i.e., property may be taken 1) only according to theprocedure prescribed by law; 2) only for public needs; and 3) only for just compensation.

Foreign investors can defend their rights and lawful interests against Lithuania in the courts of Lithuania,international arbitration institutions or other institutions. In case of investment disputes, foreign investors alsohave the right to directly address the International Centre for Settlement of Investment Disputes.

InvestmentProtection and

Guarantees

32

Tax rates in Lithuania are in general similar to those in Latvia and Estonia

The below overview focuses on the taxation aspects relevant for the real estate owners, lessees anddevelopers and is not aimed at providing a thorough coverage of the Lithuanian taxation framework.

With the exception of the fact that the Lithuanian law will continue to be brought in line with theEU directives and the implementation of the EU Parent/Subsidiary Directive, no major changesin tax legislation described below are planned at present.

In terms of taxation, there is no difference between investments in partnerships and companiesbecause Lithuanian partnerships are not transparent for tax purposes and, like companies, areliable for corporate profit tax. Under the Lithuanian tax law, all enterprises registered in Lithuaniaare subject to the corporate profit tax.

Usually, permanent establishments of foreign enterprises in Lithuania are subject to the same taxrequirements as other Lithuanian enterprises with certain exceptions (allowed deduction ofadministrative expenses of the head office, etc.). A foreign enterprise has a permanent establishmentin Lithuania when such enterprise 1) carries on in Lithuania business activity of a permanentnature either itself or via a dependent agent, or 2) uses a construction site, an assembly or installationobject in Lithuania, or 3) operates a natural resource exploration or extraction site. In particular,rent and lease payments (less expenses) to permanent Lithuanian establishments of foreigncompanies are subject to the standard 15% or 13% corporate profit tax as current income. No taxis applied on repatriated profit of branches (permanent establishments).

The standard corporate profit tax rate is 15% and drops to 13% for small enterprises with anannual income of less than 500,000 LTL (approx. 783,000 EUR) and less than ten employees onaverage.

The tax base is the net income in the balance sheet adjusted for tax provisions, e.g., for a rentalproperty it is rental income less tax-deductible operating expenses.

When computing corporate profit tax other taxes (e.g., real estate taxes, social insurancecontributions, etc.) are deducted from taxable income.