60

Blueprint for the future The London Insurance Market Operational drivers in the London Market – a survey of insurers

Blueprint for the future

The London Insurance Market

Operational drivers in the London Market – a survey of insurers

Blueprint for the futureThe London Insurance Market

Operational drivers in the London Market – a survey of insurers

Contents

Introduction

Executive summary

Surer footing

1-2

The value of claims

Rethinking reinsurance

A people business

Capital management

True, fair and transparent

The purse-strings

Counting the costs

The London Insurance Market

3-6

7-12

13-18

19-22

29-32

33-36

37-40

41-44

45-48

51-52

Fingers on the button

Within limits

23-28

49-50

Contacts53-54

Introduction

Pressure to perform

Operational improvements are fuelling the drive to enhance valueand sharpen the competitive edge.

The London Insurance Market hastraditionally been seen as theworld’s leading centre for insuringspeciality risk. However, recentyears have been marked by poorresults and criticism about theefficiency of conducting businessin London. These concerns havebeen cast in sharper focus by theWorld Trade Center losses and thegrowing threat from Bermuda tothe London Market’s global pre-eminence.

The latest market reforms, thoughwelcome, can only go so far inbolstering London’s reputation.Unless market participants are ableto price risks more accurately,control exposures more effectivelyand generate higher and moreconsistent returns, the next fewyears could see a withdrawal ofcapital from London. As one chiefexecutive told us, ‘by 2005 therewill be no margin for error’.Improving operational performancewill be key to survival and success.

In the summer of 2002,PricewaterhouseCoopers surveyeda cross-section of insurers(encompassing a substantialproportion of the market’s 2002capacity) to provide a uniqueinsight into how they areaddressing key operationalchallenges including underwritingperformance, claims costmanagement and optimising theuse of reinsurance. The resultsreveal a high degree of consensusabout what needs to be done, with most respondents listing suchfactors as attracting quality people,closer control of risk aggregationand more appropriate reinsuranceprogrammes among their toppriorities. However, some appear to be finding it harder than othersto turn words into action.

Admittedly, few of the issues arestraightforward. Many organisationsface the dilemma of how to instiltighter underwriting disciplinewithout stifling the flexibility andentrepreneurial flair that are centralto the London Market. Looking to the future, there is the vexedquestion of how to manage thebusiness through the next downturn.

Drivers for success

Our research has enabled us toidentify key attributes that webelieve will be crucial for successin the long-term:

• Clear focus on shareholder value creation, which is

measurable and understoodthroughout the organisation;

• Decisive leadership and a strongpositive culture;

• Clarity of decision-making basedon quality information;

• Strong understanding of capital provider and keystakeholder expectations;

• Capability of attracting, retainingand rewarding quality people;

• Organisational structure thatreflects the corporate cultureand strategic goals;

• Receptiveness to change; and

• Willingness to innovate.

These attributes manifestthemselves in different ways acrossthe organisations we surveyed and almost all ‘talk the talk’.However, to outperform in thelong-term they also need to ‘walkthe walk’. The cushion of thecurrent strong rating increases mayhave abated the sense of urgencyand purpose needed to transformthe modus operandi.

Harder markets tend to maskweaknesses and flatter results. The acid test will come with thecycle downturn. This survey seeksto identify what constitutesoperational best practice, and howit is being implemented to helporganisations outperform theircompetitors across the cycle.

‘Too many capital

providers have been

prepared to back poor

underwriters’Survey respondent

Blueprint for the future • PricewaterhouseCoopers • p2

Executive summary

The PricewaterhouseCoopers study focuses on the operational ratherthan strategic drivers for organisations within the London Market.The analysis is based on 22 in-depth questionnaires and 19 face-to-face interviews with executives from both Lloyd’s and Companymarket businesses. The respondents were selected to reflect a broadspectrum of entity sizes, product classes, independent businessesand subsidiary organisations.

Underwriting

The last five years have producedlargely unsatisfactory results.Poorly controlled exposures haveforced many London Marketorganisations to re-examine theoperational basis of risk, rewardand value management. WTC wasthe final wake-up call for manybusinesses, clearing away anyremaining complacency andhastening change.

Nearly two-thirds of those surveyedare modifying the type of risks to be underwritten over the next 12 months. In addition, over a thirdof respondents in our survey saidthat WTC had led them to changethe classes of business in which theyoperate. Most have now imposedstricter underwriting guidelines,including lower line size limits andmore curbs on delegated authoritybusiness, backed up by morestringent peer review of underwritingdecisions. Many organisations arealso looking to develop moresophisticated scenario modellingand systems-based monitoring.

However, survey respondentsacknowledged that more could be done:

• Many do not appear to fullyunderstand all of the componentsof their ‘cost of sales’;

• Return on economic capitalremains an alien concept formany underwriters; and

• Performance measures are not consistent and are sometimes arbitrary.

How can organisations improveperformance and create value ifthey are not properly evaluating theprospective profitability of thebusiness they are writing?

With notable exceptions,preparations for a future softeningof the market are limited. Manyrespondents accept that they willface hard choices in cuttingvolumes and exiting markets,though forward planning generallylacks detail.

Claims management

Claims represent the bulk of aninsurers’ post-commission costs. Yet, respondents indicated a limitedfocus on reducing expenditure,improving service or the effectivemonitoring of performance. Some organisations are embarkingon limited claims leakage reviews,concentrating mainly on areas suchas direct claims handling costs.There are also moves to enhancethe quality of case reserving andalign it more closely to the pricingof new risks.

‘Anyone can write

profitable business in a

hard market, but you

still need to sort the

wheat from the chaff’Survey respondent

Blueprint for the future • PricewaterhouseCoopers • p4

Executive summary continued

Overall, we believe the opportunitiesfor improvement are significant.

Reinsurance

WTC has forced many organisations torethink their approach to reinsurance.Almost two-thirds of respondents havemoved to higher quality reinsurersover the past year, despite the highercosts and numerous downgradings.Nearly three-quarters would like to reduce the emphasis on lossesoccurring during (‘LOD’) reinsuranceand move to risks attaching cover,though most accept that this is oftenunavailable or too expensive.

To offset the higher costs and improvereturns, many organisations arelooking to reduce their reinsurancerequirements through lower line sizelimits, better risk assessment andhigher deductibles. Such moves arealigned to concerns, especially on theLloyd’s side, that reinsurance is toooften used to mask poor underwriting.Our research has also raised questionsabout the effectiveness of in-houseteams in identifying and collectingpotential recoveries, with a third ofrespondents continuing to rely onmanual-only systems.

People

The pre-eminence of the LondonMarket is underpinned by itsunparalleled concentration ofexperience and specialist expertise.However, around a half of respondentsbelieve that the London Market doesnot actually offer the requisite level ofquality staff, which means paying wellover the odds for suitable personnel.

Quite a number of respondents,especially on the Lloyd’s side, alsoexpressed misgivings about the salaries and status enjoyed by manyunderwriters. In contrast, IT, claims andother key personnel can seem like thepoor relations. Most recognise that thisdisparity needs attention, especially ifthey are to attract talented staff fromoutside the London Market.

Some organisations are looking to tie underwriters and other staff intobroader corporate goals by basing theirbonuses on return on equity and othercapital-based measures. However, aperceived general lack of transparencyand objectivity means that many staffremain sceptical about such moves.

Our interviews have highlighted thattraining and staff retention in manyorganisations also leave room for improvement.

Issues coming to the fore

Respondents gave surprisingly lowrankings to the importance ofregulation and terms of trade. Manyorganisations clearly feel that despitetheir levels of dissatisfaction withinthese areas, such issues are beyondtheir control. However, a brave few aretaking the lead in pressing for moresensible terms of trade and morerealistic compliance requirements.

Cost control seems to have slippeddown the list of priorities for mostorganisations. This lack of importanceis perhaps understandable at a time ofsubstantial rating increases and thedistraction of so many moreimmediate concerns.

‘Recruiting seasoned

underwriters is a

problem’Survey respondent

p5 • Blueprint for the future • PricewaterhouseCoopers

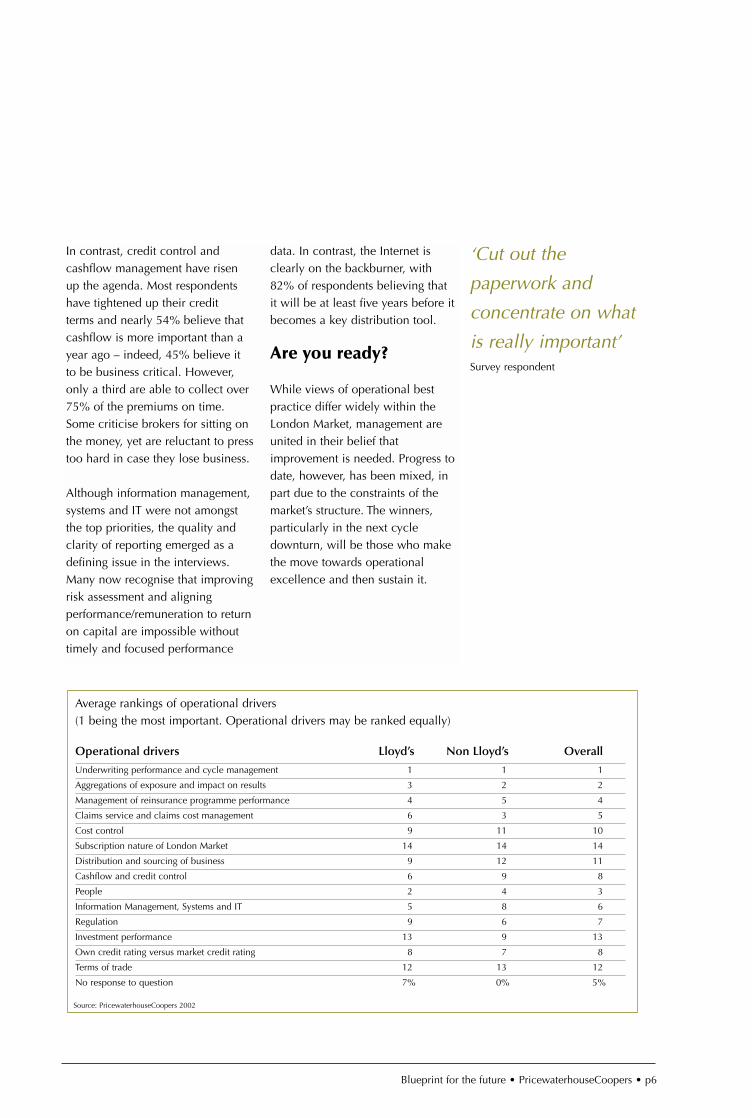

In contrast, credit control andcashflow management have risenup the agenda. Most respondentshave tightened up their credit terms and nearly 54% believe thatcashflow is more important than ayear ago – indeed, 45% believe it to be business critical. However,only a third are able to collect over75% of the premiums on time.Some criticise brokers for sitting onthe money, yet are reluctant to presstoo hard in case they lose business.

Although information management,systems and IT were not amongstthe top priorities, the quality andclarity of reporting emerged as adefining issue in the interviews.Many now recognise that improvingrisk assessment and aligningperformance/remuneration to returnon capital are impossible withouttimely and focused performance

data. In contrast, the Internet isclearly on the backburner, with82% of respondents believing that it will be at least five years before itbecomes a key distribution tool.

Are you ready?

While views of operational bestpractice differ widely within theLondon Market, management areunited in their belief thatimprovement is needed. Progress todate, however, has been mixed, inpart due to the constraints of themarket’s structure. The winners,particularly in the next cycledownturn, will be those who makethe move towards operationalexcellence and then sustain it.

‘Cut out the

paperwork and

concentrate on what

is really important’Survey respondent

Blueprint for the future • PricewaterhouseCoopers • p6

Average rankings of operational drivers(1 being the most important. Operational drivers may be ranked equally)

Operational drivers Lloyd’s Non Lloyd’s Overall

Underwriting performance and cycle management 1 1 1

Aggregations of exposure and impact on results 3 2 2

Management of reinsurance programme performance 4 5 4

Claims service and claims cost management 6 3 5

Cost control 9 11 10

Subscription nature of London Market 14 14 14

Distribution and sourcing of business 9 12 11

Cashflow and credit control 6 9 8

People 2 4 3

Information Management, Systems and IT 5 8 6

Regulation 9 6 7

Investment performance 13 9 13

Own credit rating versus market credit rating 8 7 8

Terms of trade 12 13 12

No response to question 7% 0% 5%

Source: PricewaterhouseCoopers 2002

Surer footing

Underwriting performance and cycle management

Everyone recognises that underwriting risk and performance need tobe more carefully managed. The real question is how?

The marketenvironment

The market environment is provingever more challenging as Londonsquares up to its global competitorsin what is an increasingly fiercecontest for investment. The majorcapital providers, upon which thefuture of the London Marketdepends, are not prepared toaccept the volatility and poorreturns that have dogged themarket. WTC has intensified thispressure, forcing insurers andreinsurers to re-examine thenature, pricing and aggregation of the risks they underwrite.

14% of respondents are planningsignificant changes in the type ofrisks underwritten over the next 12months. A further 59% expect somemodification. WTC has specificallyled 54% of respondents to changethe classes of business in whichthey operate. Many are withdrawingfrom US casualty business, withsome also considering reductions in

aviation, US property andprofessional indemnity exposures.Almost 80% of respondents haveincreased year-on-year grosspremium rates by at least 20%, with 14% recording rises of 50% or more. Rates for some lines havemore than doubled.

Blueprint for the future • PricewaterhouseCoopers • p8

YesOnly to a limited extentNo

46%36%

18%

Has September 11 led to youchanging the classes of business inwhich you operate?

100%75-100%50-75%

20-50%Less than 20%No response to question

13% 14%

9%

64%

What is the overall percentage grossrating increase in 2002 renewals?

YesOnly to a limited extentNo

Lloyd‘s

Non-Lloyd‘s

0 100%

43% 21% 36%

25% 12% 63%

Has September 11 led to you changing the classes of business in whichyou operate?

Lloyd‘s

Non-Lloyd‘s

0 100%100%75-100%50-75%

20-50%Less than 20%No response to question

79% 21%

37% 38% 25%

What is the overall percentage gross rating increase in 2002 renewals over2001 business?

Source: PricewaterhouseCoopers 2002 Source: PricewaterhouseCoopers 2002

Source: PricewaterhouseCoopers 2002

Source: PricewaterhouseCoopers 2002

Surer footing continued

However, all believe that these ratelevels are not sustainable. Once thecycle turns, almost all intervieweesstressed the need to then cut back onvolume and be more selective in therisks they accept to enable them tomaintain margins and profitability.Some are developing early warningsystems to enable them to anticipateand promptly respond to decliningrates. However, there seemed to be ageneral lack of clarity and detail abouthow the necessary reorientation was tobe achieved.

Many appreciate that it may bedifficult to convince underwriters torein in their writings when many havetraditionally ranked themselves onvolume, especially if they still haveaccess to ‘hard market’ levels ofcapital. Subsidiaries of larger globalgroups may also face difficulties insquaring the contraction in incomewith their capital providers, who demand ever increasing returns to satisfy the capital market.Nevertheless, it is generally recognisedthat sustainable profitability is the keyto safeguarding the confidence andsupport of investors.

Distribution

The need for greater selectivity andvigilance about the risks underwrittenhas intensified concerns about the safety of delegated authorityarrangements, which still account for at least 10% of business for nearlyhalf of respondents. Most respondentswere keen to curtail the use of‘binders’, though it was generallyaccepted that this is still often the bestway to manage certain businessclasses such as US direct property.Many felt that adequate control ofsuch arrangements is feasible as longas there is an effective infrastructure togovern relationships and performance.

‘Underwriters are

moving away from

being traders to

becoming risk

assessors’Survey respondent

p9 • Blueprint for the future • PricewaterhouseCoopers

0-10%10-20%20-30%

30%+No response to question

5%

50%

9%

18%

18%

What percentage of your business iswritten through delegated authorities,including binders and lineslips, where theunderwriting pen has been given away?

0-10%10-20%20-30%

30%+No response to question

Lloyd‘s

Non-Lloyd‘s

0 100%

21% 29% 7%14%29%

100%

What percentage of your business is written through delegated authorities,including binders and lineslips, where the underwriting pen has beengiven away?

Source: PricewaterhouseCoopers 2002

Source: PricewaterhouseCoopers 2002

Closer to home, the subscriptionnature of the market is still animportant foundation for mostorganisations. Only a third ofrespondents lead more than 50% of the business they write. However, many now recognise theneed to build closer relationshipswith clients through regular face-to-face communication.

Although brokers are still powerful,direct contact with policyholderscould act as a catalyst in theevolving relationship betweeninsurer and broker. Two-fifths ofrespondents would support directsettlement with policyholders. As one interviewee commented,‘brokers have got to accept thatthey’re under pressure, becausedirect sales are coming through’.Many respondents believe thatcutting out the broker throughdirect settlement would improvecredit control and allow brokers to offer a fee-driven professionalservice, which could even be basedon the perceived level of added

value. While others agree that therole of brokers needs to evolve,most are reluctant to take on theextra administrative burden ofdealing directly with policyholders.

Most respondents remain cautiousabout trading over the Internet. 82% do believe that web-enabledtechnology should be used toreduce distribution and businessacquisition costs. Nevertheless, only 18% anticipate any significantincrease in their Internet tradingcapability over the next 12 months.82% reckon that it will be at leastfive years before the web is a keydistribution tool in the LondonMarket, with only 9% feeling that itis already important. 9% feel thatlloyds.com is currently useful. Itseems that, for some time at least,people will remain the maindistribution channel.

Blueprint for the future • PricewaterhouseCoopers • p10

‘At the moment Lloyd’s

is a subscription

market which works in

certain classes, but

you need to get closer

to the client and also

closer to the brokers’Survey respondent

0-10%10-25%25-50%

50-75%75%+

9% 14%

50%

27%

What percentage of the businessthat you write, by premium volume,do you lead?

0-10%10-25%25-50%

50-75%75%+

Lloyd‘s

Non-Lloyd‘s

0 100%

7% 57% 7%29%

25% 37% 13%25%

What percentage of the business that you write, by premium volume,do you lead?

YesNoNo response to question

9%18%

73%

Do you anticipate significantlyincreasing your Internet tradingcapability in the coming 12 months?

Source: PricewaterhouseCoopers 2002

Source: PricewaterhouseCoopers 2002

Source: PricewaterhouseCoopers 2002

‘People are still the main

distribution channel’Survey respondent

Surer footing continued

Control

Concerns over their ability to controland monitor aggregations have forcedmost respondents to review theirformal underwriting process andguidelines. Such controls are oftenbacked up by increasinglysophisticated realistic disaster scenario(‘RDS’) and probable maximum loss(‘PML’) modelling, capable ofidentifying and capping aggregations.As one respondent noted, ‘the oldRDS technique is no longer aneffective benchmark after WTC; you’re now looking beyond that toother possibilities’.

Ultimately, controls depend onunderwriter integrity and the capabilityand commitment to enforce it. Whilemost respondents still value theimportance of ‘at the box’ peer review, most have stepped up thescope and frequency of more formalscrutiny. Some larger and morecomplex risks are subject to pre-acceptance review, though most otherrisks are analysed after they have beenbound. In many organisations,compliance and internal auditpersonnel contribute to the reviews. It would clearly be impractical toexamine every slip, so most tend tobase their selections on the size andexceptional nature of the risk.

The survey found that the quality ofenforcement often tends to depend onthe organisational structure. Clear linesof command are far harder to maintainin some of the more diffuse businessentities. Wisely, some have now

streamlined their operations. Many interviewees also stressed theimportance of a strong culture. For some this is reflected in anuncompromising insistence that ‘breakthe rules and you’re out’, though suchdictates may not be so appropriatewithin the more collegiate atmospherewe observed in some organisations.One interviewee insisted that layingdown the letter of the law can inhibitinitiative and that ‘trust and teamworkare far better than a book’.

A more subtle middle way that couldequally apply to either kind of entity isto augment detailed rules with morebroad-based principles, through whichsmall-print compliance gives way to amore proactive and all-encompassingenvironment of risk control.

Performancemeasurement

Independent research (from McKinsey& Co) suggests that between 25% and50% of under-pricing is due to poorunderwriting execution. Only arounda third of respondents actively involveactuaries or statisticians in the pricingof individual risks or treaties.

Historically much of the business hasbeen underwritten without a trueunderstanding of whether that businessis actually making money. In response,many underwriting Key PerformanceIndicators (‘KPIs’) now take fullaccount of reinsurance, investmentincome and directly attributableexpenses to create a more realisticassessment of whether business isgenuinely profitable. The challenge

‘WTC has

accelerated best

practice on

aggregation’Survey respondent

p11 • Blueprint for the future • PricewaterhouseCoopers

‘The key challenge

is how to balance

underwriting control,

autonomy and

entrepreneurship’Survey respondent

here is to maintain responsibilityand accountability, while ensuringthat underwriters concentrate onmaximising shareholder value. Forexample, some organisations do notbelieve that underwriters should bemeasured on their post investmentincome results, and that their focusshould be on the combined ratio.

It is essential to ensure thatmanagement information systemsare geared to creating timely andcredible analysis of the KPIs used.However, only a quarter ofrespondents are fully satisfied with the quality of their internalmanagement reporting and theeffectiveness of the KPIs theyemploy. Most believe that ‘it is timeto stop bombarding directors withbewildering streams of extraneousdetail and concentrate on what isreally important’. Where and howto streamline the managementinformation depends on the

organisation. The key factor iswhether people trust andunderstand the numbers and areable to take decisions quickly.

The level of benchmarking againstpeer syndicates and companies isminimal. Most respondents did notconsider it important in spite ofoperating in an environment wherecompetition for capital is so intense.

‘Successful

underwriting relies on

quality information’Survey respondent

Blueprint for the future • PricewaterhouseCoopers • p12

SatisfiedPartially satisfied

Not satisfiedNo response to question

Overall

Lloyd’s

Non-Lloyd‘s

0 100%

38%

23% 54% 18% 5%

12%50%

14% 57% 7%22%

How satisfied are you with the quality of your internal management reportingand the effectiveness of Key Performance Indicators employed?

Lloyd’s/fundedaccounting

underwritinginformation

Annualaccounting

underwritinginformation

Balance sheet Cashflowstatement

Claimsdevelopment

(including largelosses)

Actuarialestimates

Return onequity/capital

measures

Non-financialmeasures

(eg employee& customersatisfaction)

0

20

40

60

80

100%

Lloyd’sNon-Lloyd’sOverall

100

13

6871

75 73

57

75

64

86

7582

100

8895

79

8882

43

25

36

21

38

27

Do your regular management accounts/Board packs include any of the following?

Source: PricewaterhouseCoopers 2002

Source: PricewaterhouseCoopers 2002

The value of claims

Claims service and claims cost management

Claims are by far insurers’ biggest expense. How can they ensurethat this money isn’t going down the drain?

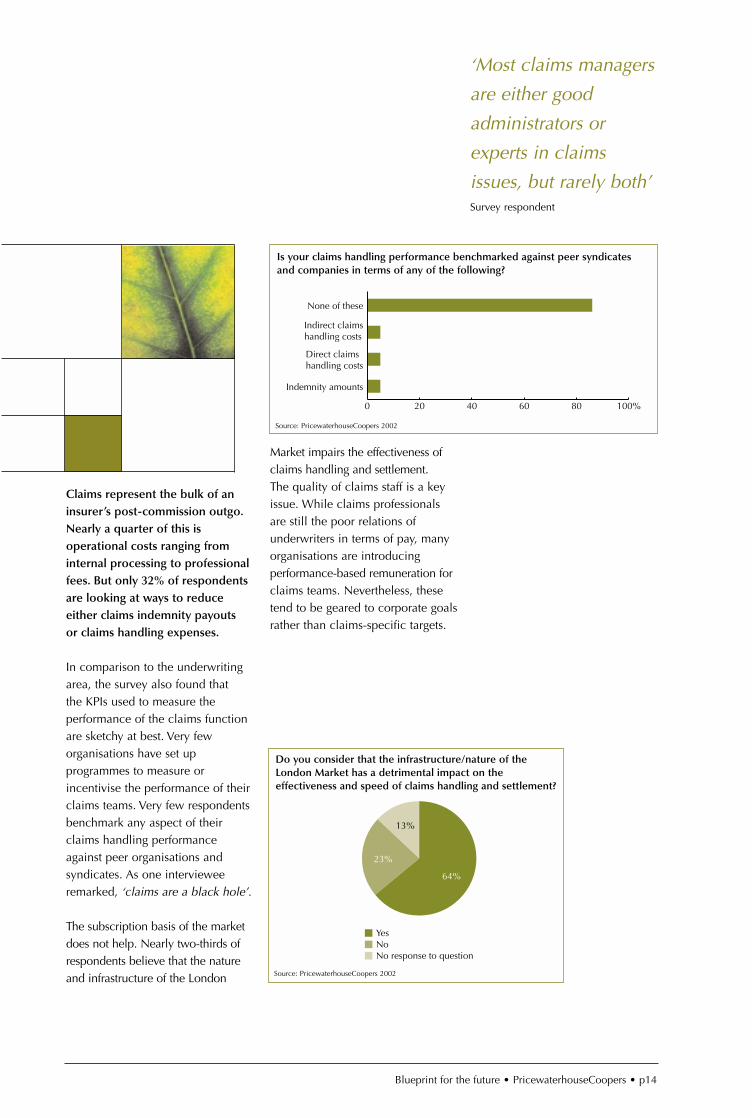

Claims represent the bulk of aninsurer’s post-commission outgo.Nearly a quarter of this isoperational costs ranging frominternal processing to professionalfees. But only 32% of respondentsare looking at ways to reduceeither claims indemnity payouts or claims handling expenses.

In comparison to the underwritingarea, the survey also found that the KPIs used to measure theperformance of the claims functionare sketchy at best. Very feworganisations have set upprogrammes to measure orincentivise the performance of theirclaims teams. Very few respondentsbenchmark any aspect of theirclaims handling performanceagainst peer organisations andsyndicates. As one intervieweeremarked, ‘claims are a black hole’.

The subscription basis of the marketdoes not help. Nearly two-thirds ofrespondents believe that the natureand infrastructure of the London

Market impairs the effectiveness ofclaims handling and settlement. The quality of claims staff is a keyissue. While claims professionalsare still the poor relations ofunderwriters in terms of pay, manyorganisations are introducingperformance-based remuneration forclaims teams. Nevertheless, thesetend to be geared to corporate goalsrather than claims-specific targets.

‘Most claims managers

are either good

administrators or

experts in claims

issues, but rarely both’Survey respondent

Blueprint for the future • PricewaterhouseCoopers • p14

None of these

Indirect claimshandling costs

Direct claimshandling costs

Indemnity amounts

0 20 40 60 80 100%

Is your claims handling performance benchmarked against peer syndicatesand companies in terms of any of the following?

YesNoNo response to question

13%

64%

23%

Do you consider that the infrastructure/nature of theLondon Market has a detrimental impact on theeffectiveness and speed of claims handling and settlement?

Source: PricewaterhouseCoopers 2002

Source: PricewaterhouseCoopers 2002

The value of claims continued

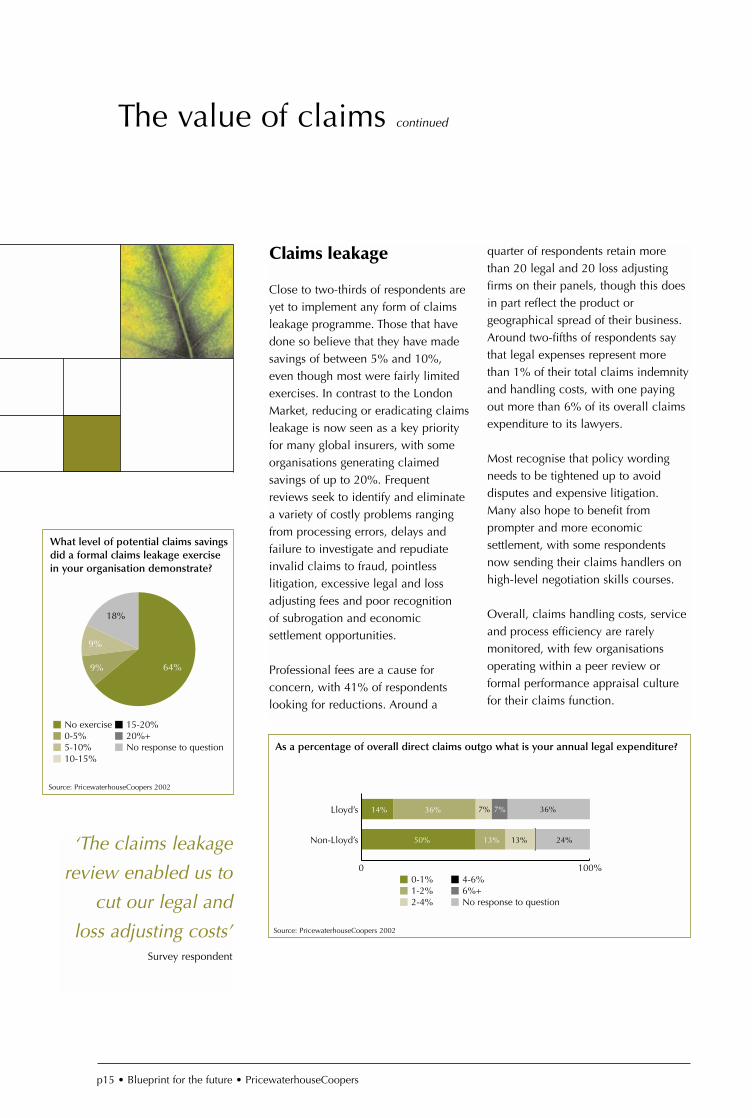

Claims leakage

Close to two-thirds of respondents areyet to implement any form of claimsleakage programme. Those that havedone so believe that they have madesavings of between 5% and 10%, even though most were fairly limitedexercises. In contrast to the LondonMarket, reducing or eradicating claimsleakage is now seen as a key priorityfor many global insurers, with someorganisations generating claimedsavings of up to 20%. Frequentreviews seek to identify and eliminatea variety of costly problems rangingfrom processing errors, delays andfailure to investigate and repudiateinvalid claims to fraud, pointlesslitigation, excessive legal and lossadjusting fees and poor recognition of subrogation and economicsettlement opportunities.

Professional fees are a cause forconcern, with 41% of respondentslooking for reductions. Around a

quarter of respondents retain morethan 20 legal and 20 loss adjustingfirms on their panels, though this doesin part reflect the product orgeographical spread of their business.Around two-fifths of respondents saythat legal expenses represent morethan 1% of their total claims indemnityand handling costs, with one payingout more than 6% of its overall claimsexpenditure to its lawyers.

Most recognise that policy wordingneeds to be tightened up to avoiddisputes and expensive litigation.Many also hope to benefit fromprompter and more economicsettlement, with some respondentsnow sending their claims handlers onhigh-level negotiation skills courses.

Overall, claims handling costs, serviceand process efficiency are rarelymonitored, with few organisationsoperating within a peer review orformal performance appraisal culturefor their claims function.

‘The claims leakage

review enabled us to

cut our legal and

loss adjusting costs’Survey respondent

p15 • Blueprint for the future • PricewaterhouseCoopers

9%

18%

64%9%

No exercise0-5%5-10%10-15%

15-20%20%+No response to question

What level of potential claims savingsdid a formal claims leakage exercisein your organisation demonstrate?

Lloyd’s

Non-Lloyd’s

0 100%0-1%1-2%2-4%

4-6%6%+No response to question

14% 36% 7% 7% 36%

50% 13% 13% 24%

As a percentage of overall direct claims outgo what is your annual legal expenditure?

Source: PricewaterhouseCoopers 2002

Source: PricewaterhouseCoopers 2002

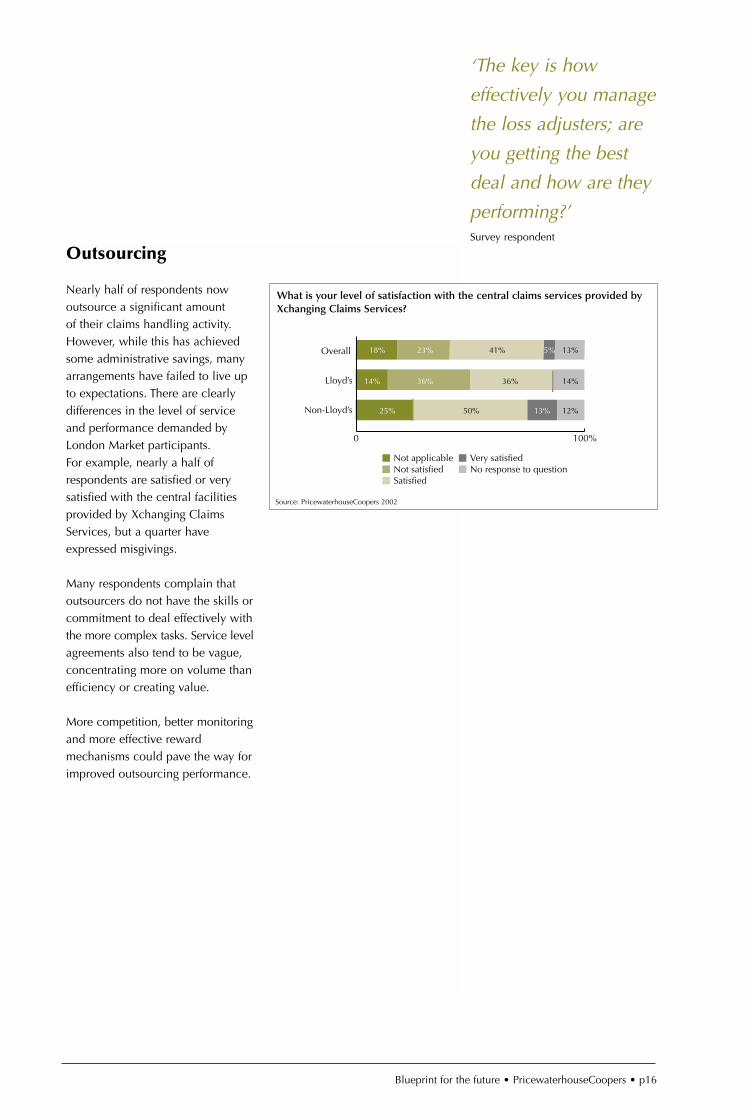

Outsourcing

Nearly half of respondents nowoutsource a significant amount of their claims handling activity.However, while this has achievedsome administrative savings, manyarrangements have failed to live upto expectations. There are clearlydifferences in the level of serviceand performance demanded byLondon Market participants. For example, nearly a half ofrespondents are satisfied or verysatisfied with the central facilitiesprovided by Xchanging ClaimsServices, but a quarter haveexpressed misgivings.

Many respondents complain thatoutsourcers do not have the skills orcommitment to deal effectively withthe more complex tasks. Service levelagreements also tend to be vague,concentrating more on volume thanefficiency or creating value.

More competition, better monitoringand more effective rewardmechanisms could pave the way forimproved outsourcing performance.

‘The key is how

effectively you manage

the loss adjusters; are

you getting the best

deal and how are they

performing?’Survey respondent

Blueprint for the future • PricewaterhouseCoopers • p16

Overall

Lloyd’s

Non-Lloyd’s

0 100%

18% 23% 41% 5% 13%

14% 36% 36% 14%

25% 50% 13% 12%

Not applicableNot satisfiedSatisfied

Very satisfiedNo response to question

What is your level of satisfaction with the central claims services provided byXchanging Claims Services?

Source: PricewaterhouseCoopers 2002

The value of claims continued

Forecasting

Although Lloyd’s in particular hasstruggled historically to shake off itspoor reputation for forecasting, manyorganisations appear satisfied with theircurrent procedures. Over one-third ofLloyd’s respondents believe their caseestimating is ‘very good’. Although theCompany market participants did notshare such a high level of confidence,half described their case estimating as‘good’. No respondents admitted thatit was ‘poor’.

To ensure that the reserving process is robust, nearly three-quarters ofrespondents now have a committeeresponsible for setting reserves, whichmeets regularly. In addition, most useactuaries and some two-thirdsregularly use external actuarialconsultants to support the process.Nearly three-fifths look at ranges andexplicit margins or loadings in settingtheir reserve levels. About halfincorporate these evaluations into theirrisk pricing, at least for some classes,though only one in five use them incashflow management.

‘The quality of

reserving is

undermined by

rogue contracts,

rogue underwriters

and poor

underwriting

controls’Survey respondent

p17 • Blueprint for the future • PricewaterhouseCoopers

Overall

Non-Lloyd’s

Lloyd’s

0 100%

59% 32% 9%

50% 43% 7%

75% 12%13%

YesNoNo response to question

Do you include explicit margins or loadings anywhere in your reservesetting process?

Overall

Lloyd’s

Non-Lloyd’s

0 100%

23% 32% 32%

50% 38%

36% 21% 29%

13%

12%

14%

Very goodGoodAcceptable

PoorNo response to question

What is the quality of case reserving?

Source: PricewaterhouseCoopers 2002

Source: PricewaterhouseCoopers 2002

Closing the book

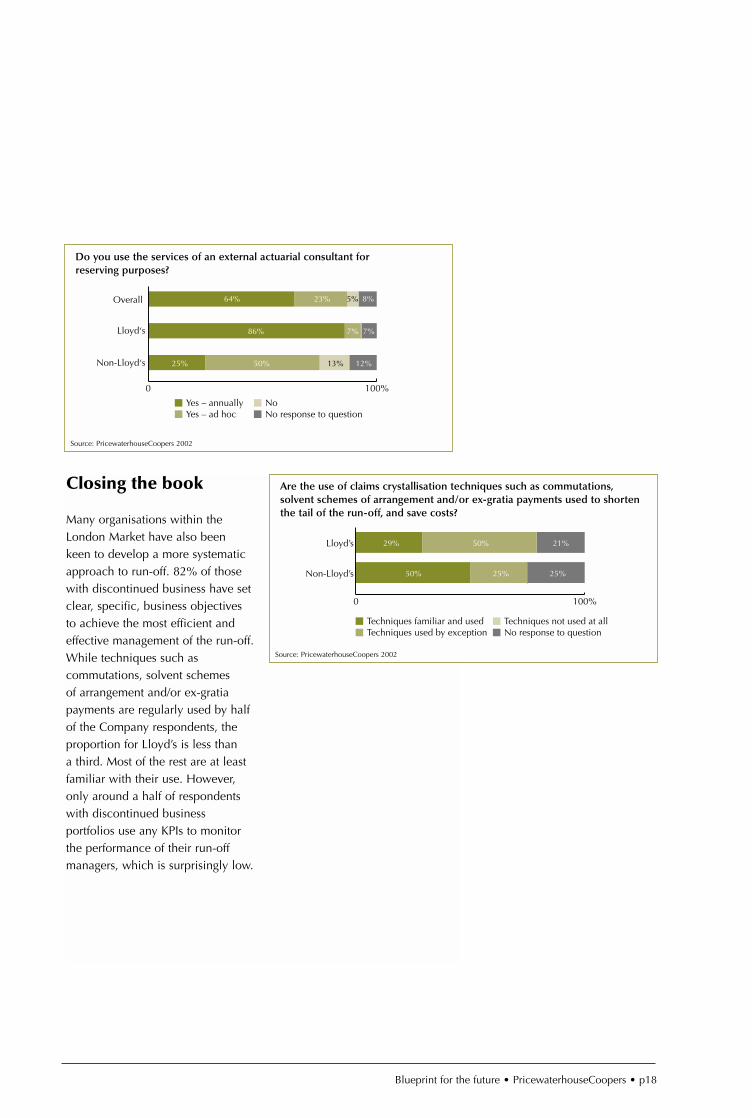

Many organisations within theLondon Market have also been keen to develop a more systematicapproach to run-off. 82% of thosewith discontinued business have setclear, specific, business objectivesto achieve the most efficient andeffective management of the run-off.While techniques such ascommutations, solvent schemes of arrangement and/or ex-gratiapayments are regularly used by halfof the Company respondents, theproportion for Lloyd’s is less than a third. Most of the rest are at leastfamiliar with their use. However,only around a half of respondentswith discontinued businessportfolios use any KPIs to monitorthe performance of their run-offmanagers, which is surprisingly low.

Blueprint for the future • PricewaterhouseCoopers • p18

Lloyd’s

Non-Lloyd’s

0 100%

29% 50% 21%

50% 25% 25%

Techniques familiar and usedTechniques used by exception

Techniques not used at allNo response to question

Are the use of claims crystallisation techniques such as commutations,solvent schemes of arrangement and/or ex-gratia payments used to shortenthe tail of the run-off, and save costs?

Overall

Lloyd‘s

Non-Lloyd‘s

0 100%

64% 23% 8%5%

86% 7% 7%

25% 12%50% 13%

Yes – annuallyYes – ad hoc

NoNo response to question

Do you use the services of an external actuarial consultant forreserving purposes?

Source: PricewaterhouseCoopers 2002

Source: PricewaterhouseCoopers 2002

Rethinking reinsurance

Management of reinsurance programme performance

Higher costs and concerns about reinsurer security and programmeperformance have spurred many insurers to rethink their approachto reinsurance.

‘WTC was a big turning point forreinsurance,’ said one interviewee.‘A lot of people came unstuckbecause they didn’t reallyunderstand their exposures,they didn’t have a reinsuranceprogramme that worked and thereinsurance didn’t cover the tail.’

Others maintained that theirprogrammes had performedreasonably satisfactorily, thoughthey accepted that WTC hadunderlined the need for a morerobust approach. Close to two-thirds of respondents have upgradedthe quality of their reinsurer panel,despite the higher costs andwidespread credit downgradings. An S&P credit rating of ‘A’ or itsequivalent now appears to be theminimum threshold, with one in ten now insisting on ‘AA’ or itsequivalent and above. Almost all of those surveyed now have areinsurance security committee, with78% of Lloyd’s respondents makinguse of reinsurance security experts.

32% of respondents reportedsignificant changes to the cost ofreinsurance, 27% substantialchanges to the terms and limits and 9% noted changes to both overthe past year. However, to thesurprise of some, securing sufficientcover has not been a problem. This may stem from reduceddemand as organisations writesmaller gross or larger net lines.Higher insurance premiums andexpected improvements inprofitability, combined with betterrisk assessment and aggregationmonitoring, have certainlyencouraged greater retention.

‘Every pound spent on

reinsurance is a pound

wasted...we need to

cut the line sizes’Survey respondent

Blueprint for the future • PricewaterhouseCoopers • p20

Lloyd’sAA

ABBB

BBB

Other – please specifyNo response to question

Overall

Lloyd’s

Non-Lloyd’s

0 100%

9% 32% 5% 27% 27%

13% 63% 13% 11%

7% 14% 7% 36% 36%

What is your minimum criterion for a reinsurer’s S&P credit rating?

Overall

Lloyd’s

Non-Lloyd’s

0 100%

23% 32% 27% 9% 9%

38% 13% 25% 13% 11%

14% 43% 29% 7% 7%

Broadly the sameBroadly the same terms and limits but at significantly higher costSignificant change in the terms and limits but broadly the same costSignificant changes in structure and costNo response to question

How would you describe your 2002 outwards programme in comparison tothe 2001 programme?

Source: PricewaterhouseCoopers 2002

Source: PricewaterhouseCoopers 2002

Rethinking reinsurance continued

Nevertheless, this continues to be aheavily geared market, with manybelieving that reinsurance is too oftenused to mitigate sloppy underwriting.Partly as a result, more and morereinsurance is now bought centrally,albeit with strong input from senior underwriters to ensure thatprogrammes purchased match theprofile of the business written.

Cover

The survey also highlighted morespecific concerns about the structureand matching of reinsuranceprotections with inwards writings.

Some respondents are now switchingfrom whole account programmes todiscrete product-orientated cover,which they believe is more suited todealing with catastrophic events suchas WTC.

Others are looking at how to ensurethat reinsurance protection is properlyaligned to the periods covered in thepolicies underwritten. Here, the mostserious misgivings centre on thereliance on LOD covers, particularlyin respect of the lack of protection forunexpired risks. Nearly three-quartersof respondents would like to reducetheir use of LOD reinsurance andmove to a wholly risks attachingprogramme. Most believe that thelatter is either too expensive or notreadily available, but as the quotesopposite show, views vary.

Several interviewees insisted that theuse of LOD covers can be effective if properly managed. In particular,users need to ensure that the pricing ofthe underlying policies protected byLOD covers takes full account of theadditional costs of purchasingreinsurance to cover unexpired risks atthe end of the underwriting year. It isalso possible to stagger the purchaseof LOD protection over the course of the underwriting year.

Although such procedures may beeffective, it is pertinent to ask whetherorganisations are sacrificing theeffective matching of risks by buyinglower-cost LOD cover, rather thanaccepting the expense of a moresuitable risks attaching programme.

p21 • Blueprint for the future • PricewaterhouseCoopers

Overall

Lloyd’s

Non-Lloyd’s

0 100%

64% 23% 13%

25% 63% 12%

86% 14%

YesNoNo response to question

Do you purchase a significant amount (more than 20% of total reinsurancepremiums) of ‘losses occurring during’ (LOD) reinsurance?

Overall

Lloyd’s

Non-Lloyd’s

0 100%

73% 18% 9%

63% 25% 12%

79% 7%14%

YesNoNo response to question

Would you like to reduce the amount of LOD reinsurance purchased and move to awholly risks attaching programme?

Source: PricewaterhouseCoopers 2002

Source: PricewaterhouseCoopers 2002

New horizons

Alternative risk transfer productscontinue to make little headway,though it has attracted a small butenthusiastic band of converts. One respondent believes thatcatastrophe bonds can work outcheaper to buy than comparablereinsurance cover. Electronicreinsurance exchanges have alsofailed to set the market alight,largely reflecting concerns aboutthe ability to specify and placecomplex reinsurance requirementsover such platforms and the relativesimplicity of the products currentlyavailable. However, there isgrowing interest in purchasingfacultative and specific coversthrough such exchanges.

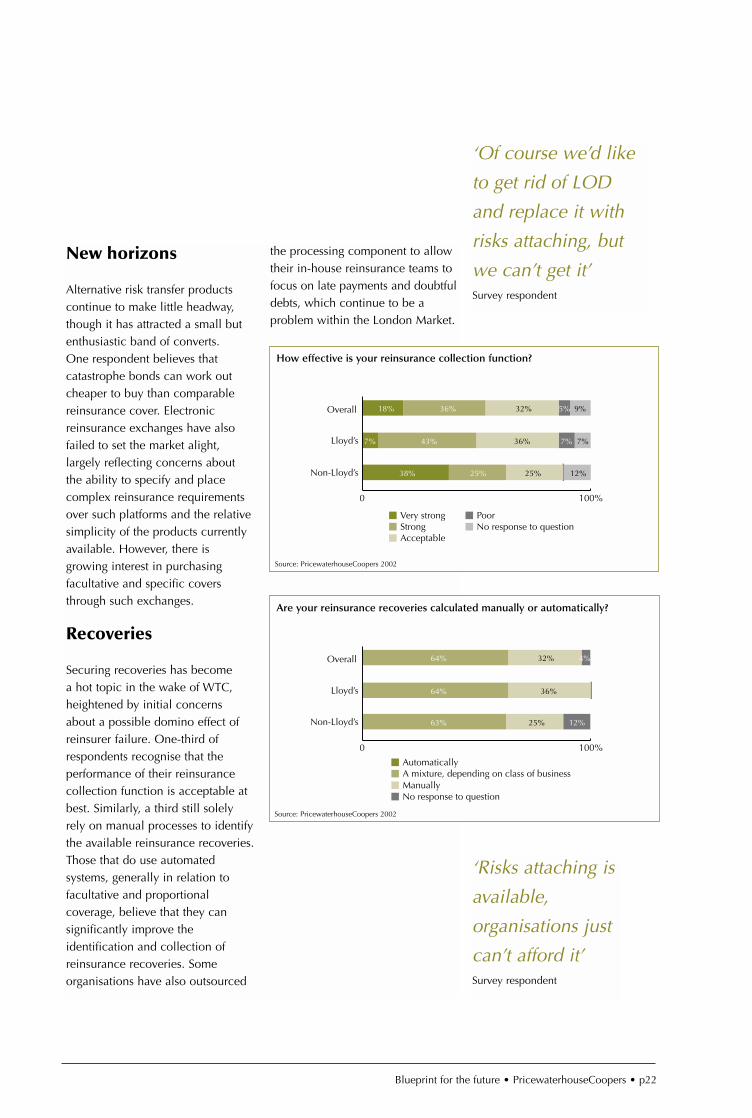

Recoveries

Securing recoveries has become a hot topic in the wake of WTC,heightened by initial concernsabout a possible domino effect ofreinsurer failure. One-third ofrespondents recognise that theperformance of their reinsurancecollection function is acceptable atbest. Similarly, a third still solelyrely on manual processes to identifythe available reinsurance recoveries.Those that do use automatedsystems, generally in relation tofacultative and proportionalcoverage, believe that they cansignificantly improve theidentification and collection ofreinsurance recoveries. Someorganisations have also outsourced

the processing component to allowtheir in-house reinsurance teams tofocus on late payments and doubtfuldebts, which continue to be aproblem within the London Market.

Blueprint for the future • PricewaterhouseCoopers • p22

‘Of course we’d like

to get rid of LOD

and replace it with

risks attaching, but

we can’t get it’Survey respondent

‘Risks attaching is

available,

organisations just

can’t afford it’Survey respondent

Overall

Lloyd’s

Non-Lloyd’s

0 100%

18% 36% 32% 9%5%

38% 25% 25% 12%

7% 43% 7%7%36%

Very strongStrongAcceptable

PoorNo response to question

How effective is your reinsurance collection function?

Overall

Lloyd’s

Non-Lloyd’s

0 100%

64% 32% 4%

63% 25% 12%

64% 36%

AutomaticallyA mixture, depending on class of businessManuallyNo response to question

Are your reinsurance recoveries calculated manually or automatically?

Source: PricewaterhouseCoopers 2002

Source: PricewaterhouseCoopers 2002

A people business

Recruiting, retaining and nurturing quality staff

Everyone recognises that performance depends on the quality of thepeople. Aligning KPIs with remuneration and reward is increasinglyseen as the key.

One of the key findings of thesurvey was respondents’ emphasison the importance of people.As one interviewee commented,‘success relies on having the rightpeople covering the right issues,and keeping them driven to movethe business forward’.

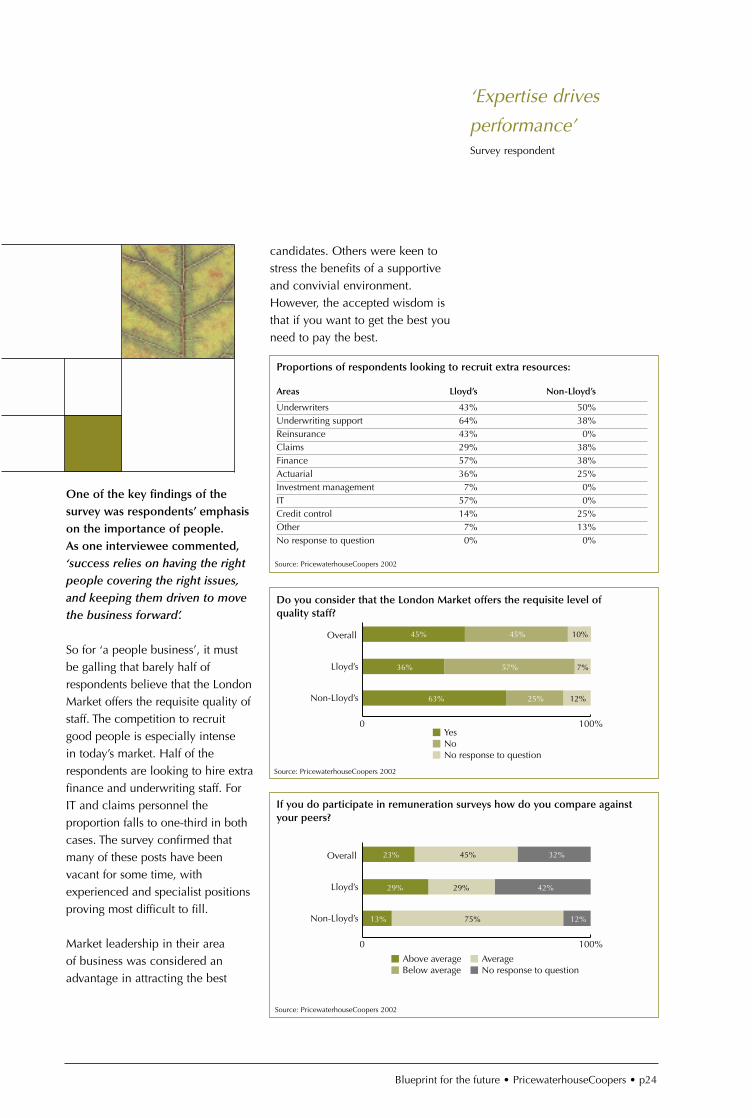

So for ‘a people business’, it mustbe galling that barely half ofrespondents believe that the LondonMarket offers the requisite quality ofstaff. The competition to recruitgood people is especially intense in today’s market. Half of therespondents are looking to hire extrafinance and underwriting staff. ForIT and claims personnel theproportion falls to one-third in bothcases. The survey confirmed thatmany of these posts have beenvacant for some time, withexperienced and specialist positionsproving most difficult to fill.

Market leadership in their area of business was considered anadvantage in attracting the best

candidates. Others were keen tostress the benefits of a supportiveand convivial environment.However, the accepted wisdom isthat if you want to get the best youneed to pay the best.

‘Expertise drives

performance’Survey respondent

Blueprint for the future • PricewaterhouseCoopers • p24

Overall

Lloyd’s

Non-Lloyd’s

0 100%

23% 45% 32%

13% 75% 12%

29%29% 42%

Above averageBelow average

AverageNo response to question

If you do participate in remuneration surveys how do you compare againstyour peers?

Source: PricewaterhouseCoopers 2002

Overall

Lloyd’s

Non-Lloyd’s

0 100%

45% 45% 10%

63% 25% 12%

36% 7%57%

YesNoNo response to question

Do you consider that the London Market offers the requisite level ofquality staff?

Source: PricewaterhouseCoopers 2002

Proportions of respondents looking to recruit extra resources:

Areas Lloyd’s Non-Lloyd’s

Underwriters 43% 50%Underwriting support 64% 38%Reinsurance 43% 0%Claims 29% 38%Finance 57% 38%Actuarial 36% 25%Investment management 7% 0%IT 57% 0%Credit control 14% 25%Other 7% 13%No response to question 0% 0%

Source: PricewaterhouseCoopers 2002

A people business continued

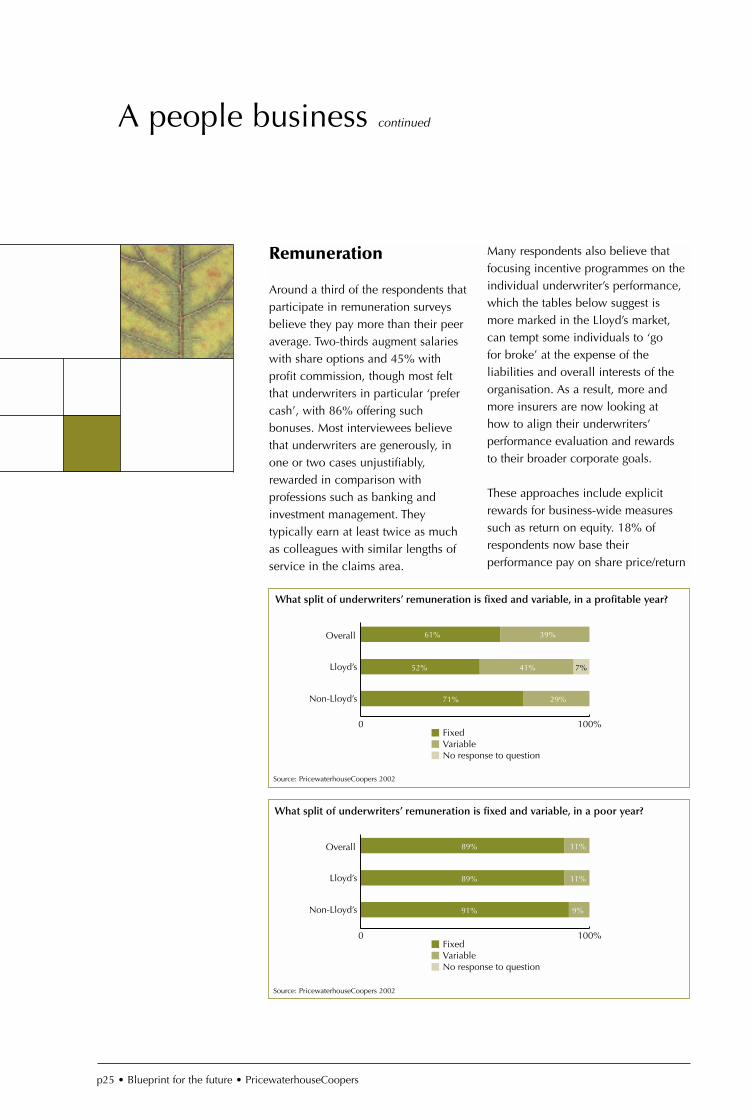

Remuneration

Around a third of the respondents thatparticipate in remuneration surveysbelieve they pay more than their peeraverage. Two-thirds augment salarieswith share options and 45% withprofit commission, though most feltthat underwriters in particular ‘prefercash’, with 86% offering suchbonuses. Most interviewees believethat underwriters are generously, inone or two cases unjustifiably,rewarded in comparison withprofessions such as banking andinvestment management. Theytypically earn at least twice as muchas colleagues with similar lengths ofservice in the claims area.

Many respondents also believe thatfocusing incentive programmes on theindividual underwriter’s performance,which the tables below suggest ismore marked in the Lloyd’s market,can tempt some individuals to ‘go for broke’ at the expense of theliabilities and overall interests of theorganisation. As a result, more andmore insurers are now looking at how to align their underwriters’performance evaluation and rewards to their broader corporate goals.

These approaches include explicitrewards for business-wide measuressuch as return on equity. 18% ofrespondents now base theirperformance pay on share price/return

p25 • Blueprint for the future • PricewaterhouseCoopers

Overall

Lloyd’s

Non-Lloyd’s

0 100%

61% 39%

71% 29%

52% 7%41%

FixedVariableNo response to question

What split of underwriters’ remuneration is fixed and variable, in a profitable year?

Overall

Lloyd’s

Non-Lloyd’s

0 100%

91% 9%

89% 11%

89% 11%

FixedVariableNo response to question

What split of underwriters’ remuneration is fixed and variable, in a poor year?

Source: PricewaterhouseCoopers 2002

Source: PricewaterhouseCoopers 2002

on capital measures. The keyquestion is what criteria are mostsuitable for the organisation andhow to ensure that underwritersunderstand and endorse them. It can sometimes be difficult to getunderwriters to appreciate theimportance of capital measures,though as one interviewee noted,‘the best way to get them tounderstand return on equity is tobuild it into their bonuses’.

The survey revealed no single orsimple answer as to how suchremuneration programmes shouldbe structured, especially as manytend to incorporate a variety ofdifferent elements to reflect the nature and organisation of thebusiness. However, thoserespondents that have proved most successful have been able todevelop transparent and clearlydefined criteria covering capitalallocation and incentivisation,preferably with feedback and ‘buy-in’ from their underwriters.

Stars

On the Lloyd’s side, reservationsabout underwriter remuneration arematched by misgivings about theirvaulted status. Clearly, underwritersare the linchpin of the business andthe very best will become ‘stars’.However, the new breed of corporatecapital providers are much less likelyto trust their investment to peoplewho have traditionally been allowedto operate as virtually independententrepreneurs. In the words of onerespondent, ‘superstar underwriterscan rapidly become unmanageable’.

Particular concerns centre on the‘personal franchise’ built up bymany top underwriters, much ofwhich they can take with themwhen they leave. A variety oftechniques are used to retain the business or ‘lock in’ seniorunderwriters, ranging fromcontractual restraints to equity anddeferred bonuses, albeit with mixedresults. As the Company market hasdemonstrated with some success, it is ultimately up to seniormanagement to ensure that evenstars recognise their responsibilityto the cohesion and objectives ofthe group as a whole.

Lagging behind

Nurturing talent from within wouldseem preferable to buying it.However, training and staffretention within the London Marketare generally poor in comparisonwith other financial sectors. The survey found that although82% of respondents do have aformal training budget, theprogrammes can often be arbitraryand on average account for only0.7% of net earned premiums.While around 40% of respondents

‘A lot of business has

a personal franchise

attached to it’Survey respondent

Blueprint for the future • PricewaterhouseCoopers • p26

Overall

Lloyd’s

Non-Lloyd’s

0 100%

82% 4% 14%

100%

71% 21%8%

YesNoNo response to question

Do you have a formal training budget?

Source: PricewaterhouseCoopers 2002

Overall Lloyd’s

0.5

0.8

0.7

Non-Lloyd’s0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8%

If you have a formal trainingbudget, what percentage is it ofnet earned premium?

Source: PricewaterhouseCoopers 2002

‘We need to recognise

that the market is not

just about underwriters

and reward others

such as IT and claims

people appropriately’Survey respondent

A people business continued

have reduced the level of staff turnoverover the past year, it remains at over15% for around a quarter of thosesurveyed. Apart from mergers andrestructuring, it is unclear what isdriving this high staff turnover, as lessthan a third of respondents conductregular employee satisfaction surveys.The level of turnover appears to belower in the Company market, wherearound 50% of organisations carry outsuch surveys, compared to Lloyd’swhere only 14% of respondents havegone down that route.

In many other industries, training andstaff retention are increasingly seen asintangible assets capable ofunderpinning sustainable valuecreation. Within the London Market,

their status does at last appear to be improving. Most businesses nowinsist, or at least encourage, theiryounger underwriters to pursue ACIIqualifications. Some organisationsbase pay rises and promotion on ACIIexams passed. This is supported bycontinuous professional developmentin areas such as negotiation andpresentation skills.

Such moves are likely to be givenadded impetus by the FSA’s directiveon ‘training and competence’ for‘approved persons’. One intervieweehas effectively given up trying to hireseasoned underwriters, reasoning thatmost of those that are available areeither unsuitable or too expensive.Instead, the organisation prefers to

p27 • Blueprint for the future • PricewaterhouseCoopers

Overall

Lloyd’s

Non-Lloyd’s

0 100%

27% 64% 9%

50% 50%

14% 15%71%

YesNoNo response to question

Do you conduct formal employee satisfaction surveys at least annually?

Overall

Lloyd’s

Non-Lloyd’s

0 100%

23% 36% 9% 5%27%

13% 49% 13% 25%

29% 29% 6%29%7%

0-5%5-10%10-15%

15%+No response to question

What was your level of employee turnover in the last financial year?‘Training in the market

is awful’Survey respondent

Source: PricewaterhouseCoopers 2002

Source: PricewaterhouseCoopers 2002

recruit people in their late twentiesand then mould them for seniorpositions. Such candidates canoften be ‘more loyal, motivated andreceptive to change’ than many oftheir older counterparts.

New blood

Many interviewees have also cometo recognise that ‘the market is notjust about underwriters’ and that itis time to value and reward otherequally important members of theteam. Most recognise that culturecan be just as much of a problem as money, with many intervieweescommenting that the LondonMarket faces a tough challenge if it is to attract the best support andprofessional staff within thefinancial services sector.

Many respondents now includeback office staff in their bonus and profit sharing programmes,explicitly linking such rewards tothe organisation’s overall results orthe extent to which they have met individual objectives. Othersare stepping up efforts to draw stafffrom outside the London Market,with many of the peopleinterviewed in this survey havingthemselves come from othersectors. Their fresh experience andexpertise can prove a valuablecatalyst for change.

Blueprint for the future • PricewaterhouseCoopers • p28

Capital management

Turning capital into shareholder value

Securing and sustaining investment is crucial to the long-term futureof the London Market. Yet surprisingly few organisations make useof return on capital measures.

Optimising return on capitalemployed (‘ROCE’) is especiallycrucial at a time of considerablecompetition for investment.Over a quarter of respondentsneed to attract a capital injectionover the next 12 months.Inter-company funding or loanswere seen as the most readilyavailable source of capital, closelyfollowed by LOC, bank loans and,in the case of Lloyd’s businesses,a cash call from Names.

Capital management tools alloworganisations to allocate capital and measure added value by eachpolicy, unit or class of business,

enabling them to optimise returns,understand the dynamics of theirenterprise and manage theirunderwriting and reinsurancestrategy more effectively. However, the survey revealed thatthe use of even the most basicROCE measures is still notwidespread in the London Market.Only two-thirds of respondents nowtake into account a return oncapital target in the pricing ofparticular classes of business, andonly 41% consider such a return forindividual risks.

‘Capital management

is about keeping the

capital provider happy’Survey respondent

‘If the business is

profitable we’ll get the

capital. The problem

is proving that it’s

profitable’Survey respondent

Blueprint for the future • PricewaterhouseCoopers • p30

Have adequate fundingWill require a capital injection

0 100 %

Lloyd’s

Non-Lloyd’s

75%

43% 21%

12%

36%

75% 13%

No response to question

Based on current forecasts do you have adequate funding for the next twelvemonths or will you require a capital injection?

Source: PricewaterhouseCoopers 2002

YesNo

0 100 %

Lloyd’s

Non-Lloyd’s

64% 7%

24%

29%

63% 13%

No response to question

Do you actively consider a return on capital target in the pricing ofindividual classes?

Source: PricewaterhouseCoopers 2002

Capital management continued

Some forward-thinking organisationsare looking to develop moresophisticated asset/liability modellingand capital management tools. Others have gone further by insistingthat underwriting teams include return on equity evaluations in theirbusiness plans.

Only one respondent makes extensiveuse of Lloyd’s risk based capital(‘RBC’) measures for internal capitalmanagement. A further 9% of thosesurveyed use them to some extent,supplemented by other tools ormeasures, and 23% of respondents

employ RBC criteria as no more than abroad benchmark. The RBC criteria arenot used by any of the non-Lloyd’srespondents. The majority of therespondents agreed that a clear focuson shareholder value creation, whichis measurable and cascaded throughthe organisation, is essential for long-term success. The survey results andour interviews suggest that capitalmanagement within manyorganisations has some way to go toachieve this.

‘Underwriters do not

have enough

appreciation of

return on capital’Survey respondent

p31 • Blueprint for the future • PricewaterhouseCoopers

To a large extentTo some extent, supplemented by other tools/measures

0 100 %

Lloyd’s

Non-Lloyd’s

7% 14% 36% 29%14%

88% 12%

Only as a benchmarkNot at allNo response to question

To what extent do you utilise Lloyd’s Risk Based Capital measures for internalcapital management?

YesNo

0 100 %

Lloyd’s

Non-Lloyd’s

36% 28%

12%

36%

50% 38%

No response to question

Do you actively consider a return on capital target in the pricing of individual risks?

Source: PricewaterhouseCoopers 2002

Source: PricewaterhouseCoopers 2002

True, fair and transparent

Effective financial reporting

A fog of reporting is creating confusion. It’s time to clear the air.

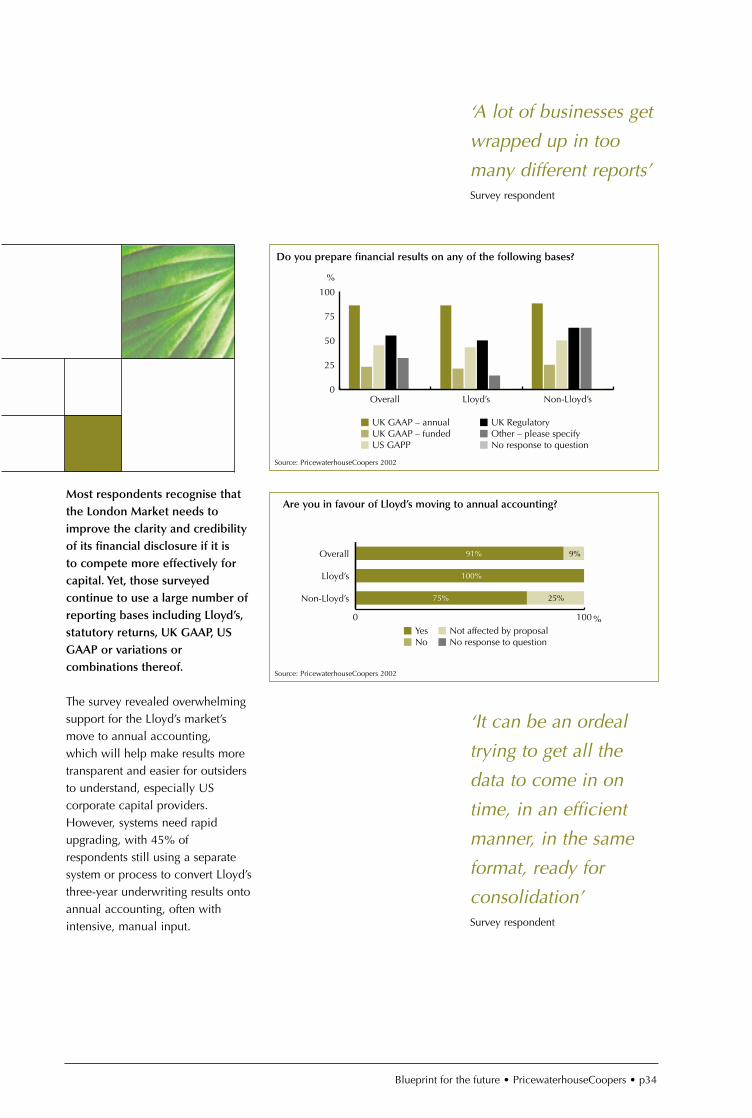

Most respondents recognise thatthe London Market needs toimprove the clarity and credibilityof its financial disclosure if it is to compete more effectively forcapital. Yet, those surveyedcontinue to use a large number ofreporting bases including Lloyd’s,statutory returns, UK GAAP, USGAAP or variations orcombinations thereof.

The survey revealed overwhelmingsupport for the Lloyd’s market’smove to annual accounting, which will help make results moretransparent and easier for outsidersto understand, especially UScorporate capital providers.However, systems need rapidupgrading, with 45% ofrespondents still using a separatesystem or process to convert Lloyd’sthree-year underwriting results ontoannual accounting, often withintensive, manual input.

‘A lot of businesses get

wrapped up in too

many different reports’Survey respondent

‘It can be an ordeal

trying to get all the

data to come in on

time, in an efficient

manner, in the same

format, ready for

consolidation’Survey respondent

Blueprint for the future • PricewaterhouseCoopers • p34

0

25

50

75

100

Non-Lloyd’sLloyd’sOverall

UK GAAP – annualUK GAAP – fundedUS GAPP

UK RegulatoryOther – please specifyNo response to question

%

Do you prepare financial results on any of the following bases?

YesNo

Not affected by proposalNo response to question

0 100 %

Overall

Lloyd’s

Non-Lloyd’s 75%

91% 9%

25%

100%

Are you in favour of Lloyd’s moving to annual accounting?

Source: PricewaterhouseCoopers 2002

Source: PricewaterhouseCoopers 2002

True, fair and transparent continued

Such a multitude of reporting cancreate a damaging lack of cohesionand transparency within theorganisation. In our experience, the board tends to manage thebusiness on a GAAP basis, whereasunderwriters often think and act on anunderwriting year basis. While in the final analysis the results should bethe same, variations in timing andmeasurement can influence thebehaviour and mindset. We believethat within the most efficientorganisations, key staff recognise

the importance of focusing onperformance as measured by GAAP accounting. The impendingintroduction of InternationalAccounting Standards will also havean impact on this.

Our discussions also highlighted atendency to ignore non-financialmeasures such as businessrelationships, reputation andinnovation, which are increasinglybeing used in other financial sectors.

p35 • Blueprint for the future • PricewaterhouseCoopers

0

10

20

30

40

50

Lloyd’sUK GAAP - annualUK GAAP - funded

US GAAPUK RegulatoryOther - please specify

%

What would you describe as the basis on which the Board/Management runs thebusiness for capital management purposes?

0

10

20

30

40

50

Lloyd’sUK GAAP - annualUK GAAP - fundedUS GAAP

UK RegulatoryOther - please specifyNo response to question

%

What would you describe as the basis on which the Board/Management runs thebusiness from shareholders’ perspective, if applicable?

Source: PricewaterhouseCoopers 2002

Source: PricewaterhouseCoopers 2002

The purse-strings

Credit control and cashflow management

The credit control and cashflow problems within the London Markethave generally been viewed as an occupational hazard. Could therenow be a will to overcome them?

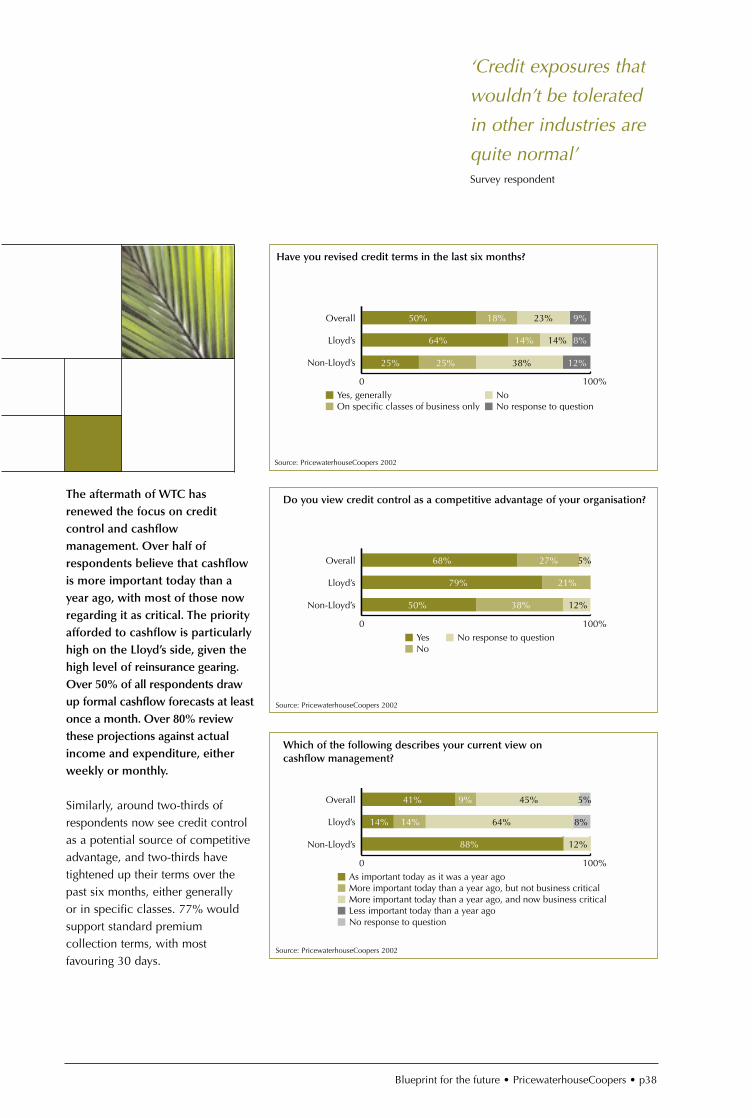

The aftermath of WTC hasrenewed the focus on creditcontrol and cashflowmanagement. Over half ofrespondents believe that cashflowis more important today than ayear ago, with most of those nowregarding it as critical. The priorityafforded to cashflow is particularlyhigh on the Lloyd’s side, given thehigh level of reinsurance gearing.Over 50% of all respondents drawup formal cashflow forecasts at leastonce a month. Over 80% reviewthese projections against actualincome and expenditure, eitherweekly or monthly.

Similarly, around two-thirds ofrespondents now see credit controlas a potential source of competitiveadvantage, and two-thirds havetightened up their terms over thepast six months, either generally or in specific classes. 77% wouldsupport standard premiumcollection terms, with mostfavouring 30 days.

‘Credit exposures that

wouldn’t be tolerated

in other industries are

quite normal’Survey respondent

Blueprint for the future • PricewaterhouseCoopers • p38

As important today as it was a year agoMore important today than a year ago, but not business criticalMore important today than a year ago, and now business criticalLess important today than a year agoNo response to question

0 100%

Overall

Lloyd’s

Non-Lloyd’s

64%14%14%

88%

9%41% 45% 5%

12%

8%

Which of the following describes your current view oncashflow management?

Yes, generallyOn specific classes of business only No response to question

No0 100%

Overall

Lloyd’s

Non-Lloyd’s

64%

25%

50% 23% 9%18%

38% 12%25%

14% 14% 8%

Have you revised credit terms in the last six months?

Source: PricewaterhouseCoopers 2002

Source: PricewaterhouseCoopers 2002

YesNo

No response to question0 100%

Overall

Lloyd’s

Non-Lloyd’s

79%

50%

68% 27% 5%

38% 12%

21%

Do you view credit control as a competitive advantage of your organisation?

Source: PricewaterhouseCoopers 2002

The purse-strings continued

It remains to be seen whether thisrenewed commitment to credit controland cashflow management willeventually bear fruit. Only one in fourrespondents reward credit controllersagainst set performance targets. Onlyjust under a third are able to collectover 75% of the premiums due ontime, despite what are considered to bealready generous credit terms.

‘If you write the

business 10%

quicker than anyone

else, you collect

the premiums 10%

quicker, you collect

the reinsurance

recoveries 10%

quicker, then you

invest your money

and it all multiplies’Survey respondent

p39 • Blueprint for the future • PricewaterhouseCoopers

YesNo

No response to question0 100%

Overall

Lloyd’s

Non-Lloyd’s

29%

13%

23% 73% 4%

75% 12%

71%

Are your credit controllers set collection targets and rewarded on the basisof performance?

0 - 25%25 - 50%

50 - 75%75%+

No response to question0 100%

Overall

Lloyd’s

Non-Lloyd’s

29%14% 36%7%

25%13%

32%14% 32% 17%

24%38%

14%

5%

What percentage of your premiums is collected on time?

Source: PricewaterhouseCoopers 2002

Source: PricewaterhouseCoopers 2002

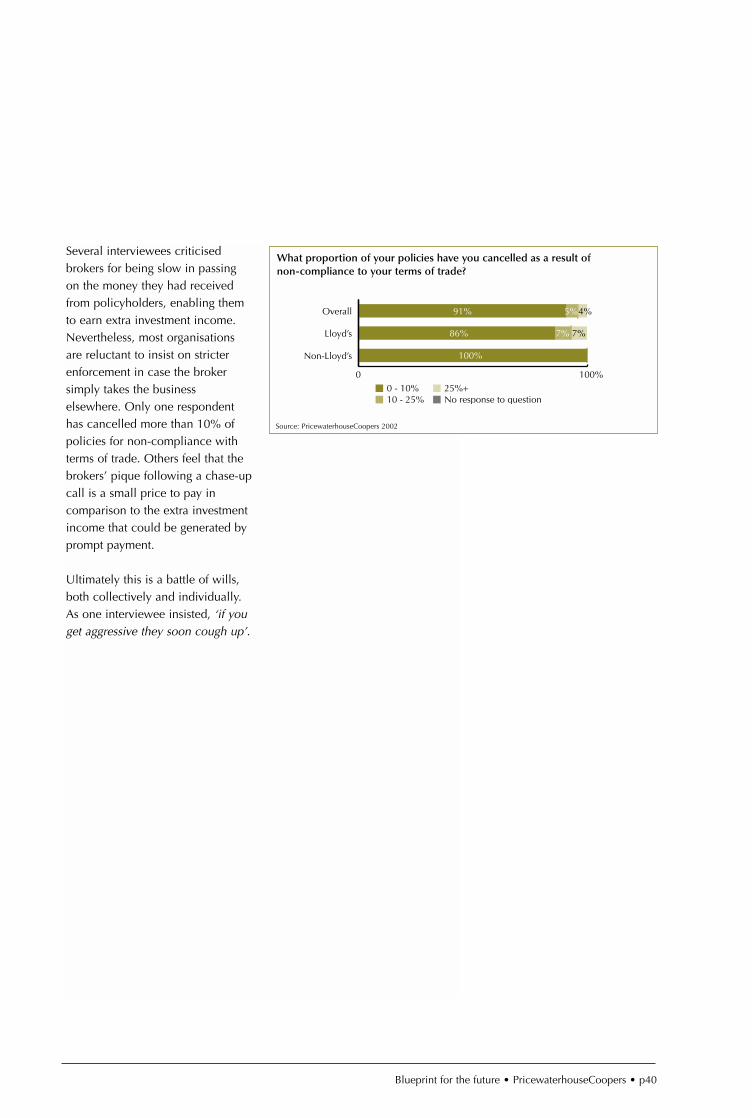

Several interviewees criticisedbrokers for being slow in passing on the money they had receivedfrom policyholders, enabling themto earn extra investment income.Nevertheless, most organisationsare reluctant to insist on stricterenforcement in case the brokersimply takes the businesselsewhere. Only one respondenthas cancelled more than 10% ofpolicies for non-compliance withterms of trade. Others feel that thebrokers’ pique following a chase-upcall is a small price to pay incomparison to the extra investmentincome that could be generated byprompt payment.

Ultimately this is a battle of wills,both collectively and individually.As one interviewee insisted, ‘if youget aggressive they soon cough up’.

Blueprint for the future • PricewaterhouseCoopers • p40

0 - 10%10 - 25%

25%+No response to question

0 100%

Overall

Lloyd’s

Non-Lloyd’s

86% 7%

100%

5%91% 4%

7%

What proportion of your policies have you cancelled as a result ofnon-compliance to your terms of trade?

Source: PricewaterhouseCoopers 2002

Counting the costs

Cost control and procurement management

Surprisingly, the survey showed that most organisations do notregard costs as a key priority in today’s hard market. However, somefeel that this is just the time to press for a better deal.

Cost has slipped down the agenda,with many organisations divertedby more urgent concerns such as risk and performancemanagement. Less than a third ofrespondents plan to reduce theirexpenses over the next year.

Overall, less than a fifth ofrespondents benchmark their expenseratio against their peer group in adetailed manner. A third employ ahead of procurement and, of these,just over half are offeredperformance rewards for savingsagainst set targets.

Some developments are in thepipeline. Around half ofrespondents set expense targets that are cascaded through theorganisation. A significantproportion of respondents areconsidering outsourcing at least partof their IT, finance, investment,accounting & tax, actuarial andunderwriting support functions.Over 80% also feel that web-

‘25% of costs come

from data entry

mistakes’Survey respondent

Blueprint for the future • PricewaterhouseCoopers • p42

What areas of cost do you consider to be outside of your control?

Overall Lloyd’s Non-Lloyd’s

Staff 5% 7% 0%

Broker commissions 14% 7% 25%

Premises 18% 14% 25%

IT and systems 9% 0% 25%

Lloyd’s/central charges 45% 64% 13%

Inter-group charges 27% 21% 38%

Capital raising/borrowing/funding 18% 21% 13%

YesOnly at a broad level

NoNo response

0 100 %

Lloyd’s

Overall

Non-Lloyd’s

21% 57% 14% 8%

5%27%50%18%

13% 37% 50%

Do you benchmark your expense ratios against your peer group andrationalise differences?

YesNoNo response to question

9%

27%

64%

Does your 2002 budget plan toreduce the level of expenses fromthe 2001 total?

Source: PricewaterhouseCoopers 2002

Source: PricewaterhouseCoopers 2002

Source: PricewaterhouseCoopers 2002

‘It’s cheaper to write

the same business in

the Company market’Survey respondent

Counting the costs continued

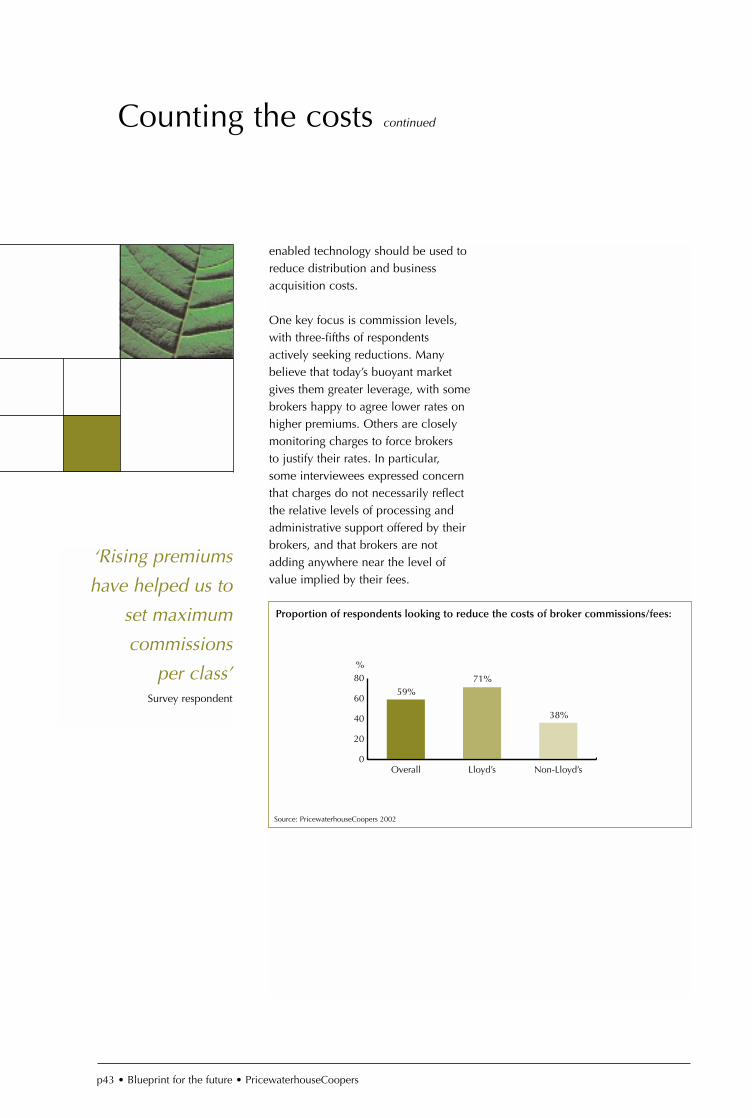

enabled technology should be used toreduce distribution and businessacquisition costs.

One key focus is commission levels,with three-fifths of respondentsactively seeking reductions. Manybelieve that today’s buoyant marketgives them greater leverage, with somebrokers happy to agree lower rates onhigher premiums. Others are closelymonitoring charges to force brokers to justify their rates. In particular, some interviewees expressed concernthat charges do not necessarily reflectthe relative levels of processing andadministrative support offered by theirbrokers, and that brokers are notadding anywhere near the level ofvalue implied by their fees.

‘Rising premiums

have helped us to

set maximum

commissions

per class’Survey respondent

p43 • Blueprint for the future • PricewaterhouseCoopers

0

20

40

60

80

Overall Lloyd’s Non-Lloyd’s

59%71%

38%

%

Proportion of respondents looking to reduce the costs of broker commissions/fees:

Source: PricewaterhouseCoopers 2002

Fingers on the button

IT management

IT and systems development could enhance decision-making. It could also facilitate faster and cheaper processing anddistribution. However, many remain sceptical.

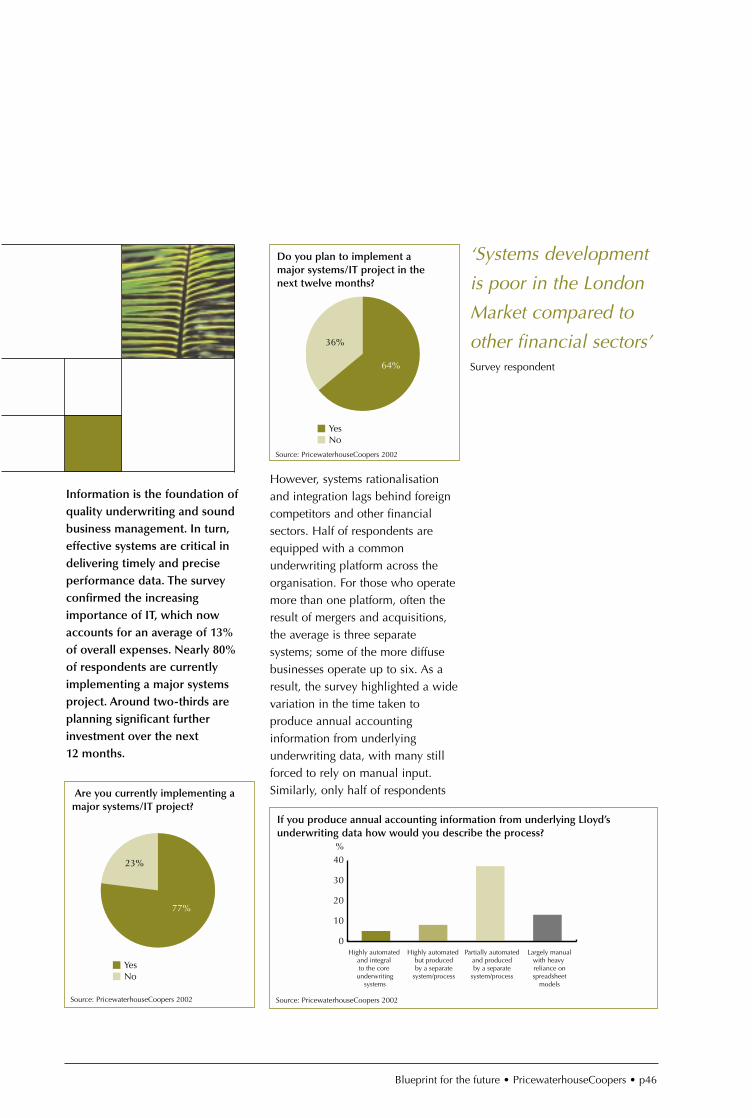

Information is the foundation ofquality underwriting and soundbusiness management. In turn,effective systems are critical indelivering timely and preciseperformance data. The surveyconfirmed the increasingimportance of IT, which nowaccounts for an average of 13% of overall expenses. Nearly 80% of respondents are currentlyimplementing a major systemsproject. Around two-thirds areplanning significant furtherinvestment over the next 12 months.

However, systems rationalisationand integration lags behind foreigncompetitors and other financialsectors. Half of respondents areequipped with a commonunderwriting platform across theorganisation. For those who operatemore than one platform, often theresult of mergers and acquisitions,the average is three separatesystems; some of the more diffusebusinesses operate up to six. As aresult, the survey highlighted a widevariation in the time taken toproduce annual accountinginformation from underlyingunderwriting data, with many stillforced to rely on manual input.Similarly, only half of respondents

‘Systems development

is poor in the London

Market compared to

other financial sectors’Survey respondent

Blueprint for the future • PricewaterhouseCoopers • p46

YesNo

23%

77%

Are you currently implementing amajor systems/IT project?

YesNo

36%

64%

Do you plan to implement amajor systems/IT project in thenext twelve months?

0

10

20

30

40

Highly automated and integral to the core

underwritingsystems

Highly automated but produced by a separate

system/process

Partially automatedand produced by a separate

system/process

Largely manual with heavy reliance onspreadsheet

models

%

If you produce annual accounting information from underlying Lloyd’sunderwriting data how would you describe the process?

Source: PricewaterhouseCoopers 2002

Source: PricewaterhouseCoopers 2002 Source: PricewaterhouseCoopers 2002

Fingers on the button continued

have moved to a common claimshandling platform.

Crystal ball

A key priority for IT investment is thedevelopment of new risk aggregation,risk management and premium ratingmodels. These include the stochasticmodelling capabilities that will berequired under the new IntegratedPrudential Sourcebook regulatoryframework. Aside from meetingregulatory needs, many believe thatsuch systems can help to underpinmore accurate pricing and reserving.

Others believe that online networkswill be able to take care of more andmore routine processing and riskmonitoring. 32% of respondents cannow collect premiums and 27% trackclaims over the Internet within someelements of their business. 50% canreview risks offered and 27% canmonitor the activities of coverholders,though the actual level of functionalitymay be limited. Many believe that

such capabilities can help them tokeep a closer eye on delegatedauthority business.

However, as outlined earlier,confidence in online trading platformsis limited. It could be at least five yearsbefore such electronic marketplacesare firmly established as a viabledistribution channel for most businesseswithin the London Market. Lookingfurther ahead, most feel that greatercommitment and standardisation areessential if the Lloyd’s Blue Mountainproject is to get off the ground. This, they believe, will require more co-operation from brokers.

‘Suppliers can tell

you that their

software can do this,

that and other and it

probably could, but

that’s with about five

years of investment,

tears and heartache,

which just isn’t

realistic’Survey respondent

‘Standardisation is a

prerequisite

for Internet

development...

brokers are blocking

standards’Survey respondent

p47 • Blueprint for the future • PricewaterhouseCoopers

0102030405060

Reviewrisks

offered

36

2732

2723 23

0

36

50

Trackclaims

Issue policies

Monitor theactivities of

coverholders

Collectpremiums

Policymaintenance

Shareinformationwith fellow

underwriters

Purchaseoutwards

reinsurance

Purchaseservices/goods

fromsuppliers

%

Are you currently able to do the following on-line for any or all of your business?

Source: PricewaterhouseCoopers 2002

Within limits

Regulation and governance

Regulation is seen by some as onerous and poorly focused,especially on the Lloyd’s side. Is this holding the market back?

All respondents report that theyrecognise the importance of soundgovernance in sustaining confidencein the market and guarding againstsystemic risk. However, 68% feelthat the volume of work needed tosatisfy the current regulations is toomuch. Frustration was especiallymarked on the Lloyd’s side, whereeach syndicate is required to submit78 separate reports every year.More than half of respondentsbelieve that the current regulatoryframework partially or whollyinhibits their ability to pursue theirstrategy properly.

Two-thirds of respondents on theCompany market side feel that N2has so far made little or no differenceto the activities of the regulator.However, most would like to see moresecondment of market professionalsinto the FSA to ensure that theAuthority has the necessary expertiseto regulate complex businesses.

Looking specifically at Lloyd’s, most organisations welcome theChairman’s Strategy Groupproposals, at least in principle.

In the light of recent events, mostsee accounting integrity as a keypriority. Around three-quarters of respondents have an auditcommittee, which generally meetseither quarterly or half-yearly. Manyare also looking to expand thescrutinising role of their non-executive directors.

‘We are overburdened

by the reporting

regime’Survey respondent

Blueprint for the future • PricewaterhouseCoopers • p50

About rightToo much

Too little0 100%

Overall

Lloyd’s

Non-Lloyd’s

32%

21%

50% 50%

79%

68%

How do you view the volume of work required to satisfy thecurrent regulations?

Source: PricewaterhouseCoopers 2002

YesNo

0 100 %

Overall

38%

77%

100%

62%

23%

Lloyd’s

Non-Lloyd’s

Do you have an Audit Committee or equivalent?

Source: PricewaterhouseCoopers 2002

YesOnly in limited ways

NoNo response to question

0 100 %

Overall

Lloyd’s

Non-Lloyd’s

23%

29%

13% 12% 75%

50% 14% 7%

36% 36% 5%

Does the current regulatory framework inhibit your ability to pursueyour strategy?

Source: PricewaterhouseCoopers 2002

The London Insurance Market

Background

Blueprint for the future • PricewaterhouseCoopers • p52

What is the London Insurance Market?

A subscription market in which various entities participate:

• 87 Lloyd’s syndicates (backed either by individual Names or corporate capital) in 2002;

• UK-domiciled insurers and reinsurers; and

• UK subsidiaries and branches of US, European and internationalinsurers and reinsurers.

Total capacity of around £20 billion in 2002:

• £12 billion capacity within Lloyd’s alone.

Reputation as long-established market:

• Large proportion of major global organisations have policiesplaced within the London Market; and

• Over two-thirds of FTSE 100 organisations and over 80% of theDow Jones Index constituents have policies placed within theLondon Market.

Quality of underwriting expertise, particularly in speciality risks:

• The London Market share of the world’s aviation market is over30%; and

• The London Market also has substantial global market share inmarine and energy risks.

Contacts

If you would like to discuss any of the issues raised in this survey in moredetail please speak with your usual PricewaterhouseCoopers contact, orone of the partners listed below:

Philip CalnanPartnerPhone: 44 20 7212 4419Email: [email protected]

Paul DelbridgePartnerPhone: 44 20 7212 3085Email: [email protected]

Andrew KailPartnerPhone: 44 20 7212 5193Email: [email protected]

Survey Participants

We would like to take this opportunity to thank all those organisations andexecutives who agreed to participate in the development of this survey.We are extremely grateful for the time that they gave us and especially forthe openness with which they discussed the key issues facing their industry.

Production

The development and production of this survey involved a significantnumber of people and we would like to thank those listed for theirvaluable contribution.

John Ashworth

Esmée Robinson

Mark Malone

Mohammad Khan

Sébastien Delfaud

Mark Knowlson

Emma Riza

Áine O’Connor

Alpa Patel

Blueprint for the future • PricewaterhouseCoopers • p54

PricewaterhouseCoopers (www.pwcglobal.com) is the world’s largest professional services organisation. Drawing on the knowledge and skills of more than 150,000people in 150 countries, we help our clients solve complex business problems and measurably enhance their ability to build value, manage risk and improve

performance in an Internet-enabled world.

PricewaterhouseCoopers refers to the member firms of the worldwide PricewaterhouseCoopers organisation.If you would like additional copies of this survey please contact Áine O’Connor, Head of Financial Services Marketing, on email [email protected]

Copyright © 2002 PricewaterhouseCoopers. All rights reserved. Designed and produced by studio ec4 13975.

Your worlds Our people