The Manipulation of Basel Risk-Weights Mike Mariathasan University of Oxford Ouarda Merrouche Graduate Institute, Geneva CONSOB-BOCCONI Conference on Banks, Markets and Financial Innovation; presented by: Charlotte Werger, EUI May 22, 2013

Transcript

The Manipulation of Basel Risk-Weights

Mike Mariathasan

University of Oxford

Ouarda Merrouche

Graduate Institute, Geneva

CONSOB-BOCCONI Conference on Banks, Markets and Financial Innovation;presented by: Charlotte Werger, EUI

May 22, 2013

Introduction

Bank capital regulation

� core of (microprudential) bank regulation� global standards continuously revised: Basel I, Basel II, Basel III, ...

� dual objective:� enhances shareholder monitoring ex ante� protects depositors (tax payer) ex post

� Basel III:� “more of the same, but better” (Haldane, 2011)� internal models still used

� literature: incentives for banks to misreport risk (Blum, 2008)

Contribution

This paper

� does the data support Blum (2008)’s hypotheses?

Contribution

This paper

� does the data support Blum (2008)’s hypotheses?

� average reported riskiness (RWATA ) declined upon IRB adoption

� specifically for weakly capitalised banks

Contribution

This paper

� does the data support Blum (2008)’s hypotheses?

� average reported riskiness (RWATA ) declined upon IRB adoption

� specifically for weakly capitalised banks

� competing explanations� IRB induced re-allocation of resources towards safer assets� Risk-weights implied by Basel I were fundamentally too high� IRB weights are too low (by accident)� IRB weights are too low (intentionally)

Contribution

This paper

� does the data support Blum (2008)’s hypotheses?

� average reported riskiness (RWATA ) declined upon IRB adoption

� specifically for weakly capitalised banks

� competing explanations� IRB induced re-allocation of resources towards safer assets� Risk-weights implied by Basel I were fundamentally too high� IRB weights are too low (by accident)� IRB weights are too low (intentionally)

� corresponding empirical predictions

Contribution

This paper

� does the data support Blum (2008)’s hypotheses?

� average reported riskiness (RWATA ) declined upon IRB adoption

� specifically for weakly capitalised banks

� competing explanations� IRB induced re-allocation of resources towards safer assets� Risk-weights implied by Basel I were fundamentally too high� IRB weights are too low (by accident)� IRB weights are too low (intentionally)

� corresponding empirical predictions� no effect when controlling for loan categories

Contribution

This paper

� does the data support Blum (2008)’s hypotheses?

� average reported riskiness (RWATA ) declined upon IRB adoption

� specifically for weakly capitalised banks

� competing explanations� IRB induced re-allocation of resources towards safer assets� Risk-weights implied by Basel I were fundamentally too high� IRB weights are too low (by accident)� IRB weights are too low (intentionally)

� corresponding empirical predictions� effect should disappear when controlling for loan categories� banks should be able to reduce capital and remain stable

Contribution

This paper

� does the data support Blum (2008)’s hypotheses?

� average reported riskiness (RWATA ) declined upon IRB adoption

� specifically for weakly capitalised banks

� competing explanations� IRB induced re-allocation of resources towards safer assets� Risk-weights implied by Basel I were fundamentally too high� IRB weights are too low (by accident)� IRB weights are too low (intentionally)

� corresponding empirical predictions� effect should disappear when controlling for loan categories� banks should be able to reduce capital and remain stable� very hard to distinguish

Contribution

This paper

� does the data support Blum (2008)’s hypotheses?

� average reported riskiness (RWATA ) declined upon IRB adoption

� specifically for weakly capitalised banks

� competing explanations� IRB induced re-allocation of resources towards safer assets� Risk-weights implied by Basel I were fundamentally too high� IRB weights are too low (by accident)� IRB weights are too low (intentionally)

� corresponding empirical predictions� effect should disappear when controlling for loan categories� banks should be able to reduce capital and remain stable� supervisory scrutiny should matter more in case of intention

Contribution

This paper

� does the data support Blum (2008)’s hypotheses?

� average reported riskiness (RWATA ) declined upon IRB adoption

� specifically for weakly capitalised banks

� competing explanations� IRB induced re-allocation of resources towards safer assets� Risk-weights implied by Basel I were fundamentally too high� IRB weights are too low (by accident)� IRB weights are too low (intentionally)

� corresponding empirical predictions� effect should disappear when controlling for loan categories� banks should be able to reduce capital and remain stable� supervisory scrutiny should matter more in case of intention� would expect faulty models to imply more impaired loans

MotivationRWATA (%) before & after IRB adoption

Full implementation of the advanced approach

Resolved

Not resolved

5055

6065

7075

-10 -5 0 5 10Quarters before and after implementation

� strong decline and leveling with non-resolved banks afterwards

� harder to disentangle stable from fragile banks

Setup

Sample

� 115 banks that have been approved for IRB adoption� A-IRB & F-IRB� mostly for corporate & retail loans� 77% of assets covered on average

� annual balance sheet data, 2004-10 (Bankscope)

� 21 OECD countries

Setup

Model�

RWATA

�

i ,t= α0 + α1 · 1IRB

i ,t + β�Xi ,t + ui ,t

� 1IRBi,t : IRB adoption dummy (= 1, for t ≥ implementation date)

� Xi,t : control variables� Ln(TA), GDP growth, year dummies, bank FE� Bank level: gross loans, corporate loans, residential loans, liquid assets� Country level: short-term rate, public debt/ GDP

� interaction effects� variations of the LHS variable

Explanation 2: Risk-weights implied by Basel I werefundamentally too high

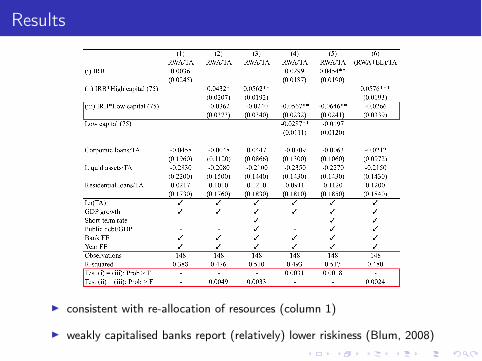

Results

� well capitalised banks increase capital after IRB adoption

� not weakly capitalised banks

� consistent with justified adjustment, but ...

Results

� ex post capital was fundamentally too low

Results

Explanations 3 & 4: Models implied too little capital. Byaccident, or intentionally?

Results

� more supervisory scrutiny associated with higher reported riskiness

Results

� more supervisory scrutiny associated with higher reported riskiness

Results

� results robust at the country level

Results

� consistent with misconduct

Results

� consistent with misconduct

� but:

Results

� consistent with misconduct

� but: closer supervision could also enhance model quality

Results

� consistent with misconduct

� but: closer supervision could also enhance model quality

� additional evidence: prudence more generally & loan quality

Results

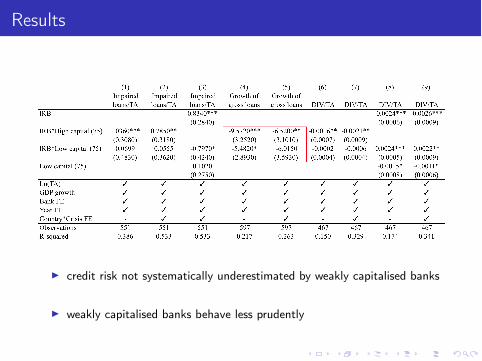

� credit risk not systematically underestimated by weakly capitalised banks

� weakly capitalised banks behave less prudently

Results

� credit risk not systematically underestimated by weakly capitalised banks

� weakly capitalised banks behave less prudently

Results

� credit risk not systematically underestimated by weakly capitalised banks

� weakly capitalised banks behave less prudently

Results

� credit risk not systematically underestimated by weakly capitalised banks

� weakly capitalised banks behave less prudently

Conclusions

Internal risk-models under Basel II� have lead to a reduction in reported riskiness� less if banks are better capitalised & more if supervision is weak

Lessons for regulation� value of simple & transparent rules� tight auditing rules could complement regulation� leverage-dependent scaling factor?� Basel III goes in the right direction (leverage ratio constraint)