The Market Outlook of Display Industry Eric Chiou Senior Research Director [email protected]Oct,2015 8 October 2015 | Page 2 ALL RIGHTS RESERVED. REPRODUCTION PROHIBITED WITHOUT WRITTEN PERMISSION. D Outline o wnstream Demand Status S upply and Demand Overview C onclusion P anel Industry Update

8 October 2015 | Page 2ALL RIGHTS RESERVED. REPRODUCTION PROHIBITED WITHOUT WRITTEN PERMISSION.

D

Outline

ownstream Demand Status

Supply and Demand Overview

Conclusion

Panel Industry Update

8 October 2015 | Page 3ALL RIGHTS RESERVED. REPRODUCTION PROHIBITED WITHOUT WRITTEN PERMISSION.

D

Outline

ownstream Demand Status

Supply and Demand Overview

Conclusion

Panel Industry Update

8 October 2015 | Page 4ALL RIGHTS RESERVED. REPRODUCTION PROHIBITED WITHOUT WRITTEN PERMISSION.

In 1H15, panel makers shipped out TV panel proactively. It was the first time that shipment proportion from 1H vs. 2H towere 50.9% vs. 49.1%. Moreover, Chinese makers' three G8.5 fabs capacities were entering mass production. Hence, thisyear's TV panel shipments prediction was modified upwards to 259.9M units. As for end-market sales, different regions'sales had different directions of momentum. In Q3, to increase negotiation power, brands' procurement momentum wasvery strong. Hence, shipments only declined 0.4% QoQ.

In 4Q15, the traditional off season, because capacities entered mass production and panel prices dropped rapidly, brandswill want to postpone procurement. Panel shipments are predicted to decline 9.6% QoQ.

2015 LCD TV Panel Shipment Projection

8 October 2015 | Page 5ALL RIGHTS RESERVED. REPRODUCTION PROHIBITED WITHOUT WRITTEN PERMISSION.

Because 2015's end market demand has continued to be weak, the annual shipment will be modified downwardly from151.6M units to 140.5M units.

For the first time ever, LCD monitor's panel shipments are close to set shipments. It means brands are more careful forprocurement quantities when end-market demand is weak. Also, monitors' days sales of inventory are usually shorter thanother applications'. This means such products and market are approaching maturity.

2015 Monitor Panel Shipment Projection

8 October 2015 | Page 6ALL RIGHTS RESERVED. REPRODUCTION PROHIBITED WITHOUT WRITTEN PERMISSION.

Due to soft demand, in 2015, NB panels lack of procurement momentum. NB's annual estimation is down from 189M units(predicted in Q2) to 174.6M units.

Weak demand for NB has caused accumulated inventories since Q1, and led to slow procurement momentum in Q2.Without releasing new models of NB, in Q3, shipments are predicted to decrease 3.1%. A traditional NB peak season willnot be seen in 3Q15.

2015 NB Panel Shipment Projection

8 October 2015 | Page 7ALL RIGHTS RESERVED. REPRODUCTION PROHIBITED WITHOUT WRITTEN PERMISSION.

In 2015, demand for Tablet brands and non-branded are both soft. Annual Tablet shipments are adjusted downwards from208M units (estimation from Q2) to 202.3M units.

In Q2, some new models stocked up, so Tablet demand grew 2.5%.

2015 Tablet Panel Shipment Forecast

8 October 2015 | Page 8ALL RIGHTS RESERVED. REPRODUCTION PROHIBITED WITHOUT WRITTEN PERMISSION.

7.5%

-2.0%

4.9%

-1.5%

4.9%

-12.0%-8.9%

-11.9%-15%

TV Monitor NB Tablet2014 2015E

248

160

192

230

26.6%

7.2%

11.4%

4.3% 2.4%

-6.2%

Mn -units

LCD TV LCD Monitor Notebook

Netbook Tablet YoY %

2015 Large-sized Panel Demand 777.3M, YoY -6.2%

8 October 2015 | Page 9ALL RIGHTS RESERVED. REPRODUCTION PROHIBITED WITHOUT WRITTEN PERMISSION.

18.3%

0.1%

6.7%

1.3%5.6%

-8.3%-11.2% -9.0%

-20%TV Monitor NB Tablet

YoY%2014 2015E

31.6%

2.5%

13.4%

5.0%

13.8%

1.9%

Mn m²

Tablet Netbook Notebook

LCD Monitor LCD TV YoY %

2015 Large-sized Panel Demand by Area 161 M m², YoY1.9%

8 October 2015 | Page 10ALL RIGHTS RESERVED. REPRODUCTION PROHIBITED WITHOUT WRITTEN PERMISSION.

D

Outline

ownstream Demand Status

Supply and Demand Overview

Conclusion

Panel Industry Update

8 October 2015 | Page 11ALL RIGHTS RESERVED. REPRODUCTION PROHIBITED WITHOUT WRITTEN PERMISSION.

In 2015, LCD TV brands' annual shipments growth rate have been modified downwards due to weak sales of China's LaborDay and Dragon Boat Festival, and because of currencies depreciation of Europe and emerging markets. Brands' annualshipments were modified from 223.4M units (estimated early this year) to 220M units, and annual growth rate was modifieddownwards from 3.3% to 1.7%.

TV 2015 Shipment Growth Rate Was Modified to 1.7% YoY

8 October 2015 | Page 12ALL RIGHTS RESERVED. REPRODUCTION PROHIBITED WITHOUT WRITTEN PERMISSION.

In 2015, UD penetration rate are modified downwards from 15.4% (predicted in previous quarter) to 14.1% mostly becauseFHD and UD panels' prices gaps are apparently shrinking recently. However, it is too late for this year's sales.

2015 UHD TV Penetration Rate Is 14.1%

8 October 2015 | Page 13ALL RIGHTS RESERVED. REPRODUCTION PROHIBITED WITHOUT WRITTEN PERMISSION.

WitsView revised the YoY growth rate of LCD monitor shipment in 2015, from -4.9% to -6.6%. Since this year, only the USAmarket's demand has been strong, but the demand of Europe, China or emerging countries hasn't been ideal. Hence,WitsView adjusts 2015's annual shipment downwards.

LCD monitors' product life cycles are very long. Moreover, in a weak global economy, consumers' budgets are limited. LCDmonitors are not their top priority to shop, so the declining trend of shipments year by year is unavoidable.

2015 MNT/AIO Market Outlook

8 October 2015 | Page 14ALL RIGHTS RESERVED. REPRODUCTION PROHIBITED WITHOUT WRITTEN PERMISSION.

The wide viewing angle monitor penetration rate reached 41% in Q2.wide viewing angle monitor penetration rate continued to rise and was ranked #1. LGE came

very close to Dell, and its penetration rate reached nearly 60%.AOC/Philips launched many new wide viewing angle models. Due to the new model distribution effect,

wide viewing angle penetration rate reached 44% and it was ranked #3 brand vendor interms of penetration rate.

Penetration Rate of Wide-Viewing-Angle LCD Monitors

8 October 2015 | Page 15ALL RIGHTS RESERVED. REPRODUCTION PROHIBITED WITHOUT WRITTEN PERMISSION.

Given disappointing shipments in the first half of the year, inventory levels have risen, while new Skylake CPU hashad some poor yields. As a result, TrendForce forecasts total 2015 notebook shipments will drop to 160.8 Million units, anannual rate of decline of 8.4%.

Regarding the 2016 notebook outlook, WitsView forecasts that those vendors using Skylake CPU may experienceshipment delays, so shipments should increase slightly next year.

2015 NB Market Outlook

8 October 2015 | Page 16ALL RIGHTS RESERVED. REPRODUCTION PROHIBITED WITHOUT WRITTEN PERMISSION.

In 2015, Chromebook shipments are forecast to fall from 9.88 million units to 8.11 million units due to underperformanceby Acer, Samsung and Asus.

For Dell, 2015 shipments are better than expected in terms of Chromebooks and overall about the same as in thatcategory.

Chromebook Annual Shipment Estimates

8 October 2015 | Page 17ALL RIGHTS RESERVED. REPRODUCTION PROHIBITED WITHOUT WRITTEN PERMISSION.

In recent years, TVs and smartphones start a trend of FHD and super-narrow bezel. Will it apply to NB?

Currently the mainstream resolution of NB is still HD, with annual shipment proportion more than 80%. Recently HDmodels' panel prices continue to drop, panel makers almost make no profits from it. Hence, panel makers gradually focuson more profitable FHD or higher resolution models. In the past, panel price gap between HD and FHD's is at least US$10,but currently the top 5 panel makers all proactively promote FHD models. If they can effectively stimulate demand, theprice gap between HD and FHD will be able to be reduced effectively.

Because all makers proactively promote high resolution products, WitsView predicts that FHD-and-above shipments mightcome to 25% of annual shipments in 2016.

NB Era of High-end Visual Enjoyment Has Come

8 October 2015 | Page 18ALL RIGHTS RESERVED. REPRODUCTION PROHIBITED WITHOUT WRITTEN PERMISSION.

As IPS penetration rate gradually increases in monitor markets, IPS penetration rate also increases in NB panels. Korean,Taiwanese or Chinese panel makers (BOE and CEC Panda) all join the wide viewing angle market, and IPS becomes thestandard spec of 2-in-1 products.

However, IPS still cannot become popular in NB market. Because not only is the high prices, but also IPS does notspecially attract Clamshell NB users. Nevertheless, high color gamut panel's visual effect are more attractive to users.Hence, WCG technology gradually stands out in NB panels.

For clamshell users, IPS is not essential, but higher color gamut can provide more beautiful screens. Hence, INX focuseson high color gamut TN panels, so that brands can increasingly use them on clamshell NB.

No matter IPS that are mostly sold to the 2-in-1 market, or WCG panels that mostly focus on clamshell NB, prices are stillthe key to control market share.

Scales of prices increase are similar to brands' "TNand WCG combination" or to "TN transforming intoIPS".

Choose compatible panels according to differentproducts features.

WCG and IPS Lead Differentiation of NB Products

8 October 2015 | Page 19ALL RIGHTS RESERVED. REPRODUCTION PROHIBITED WITHOUT WRITTEN PERMISSION.

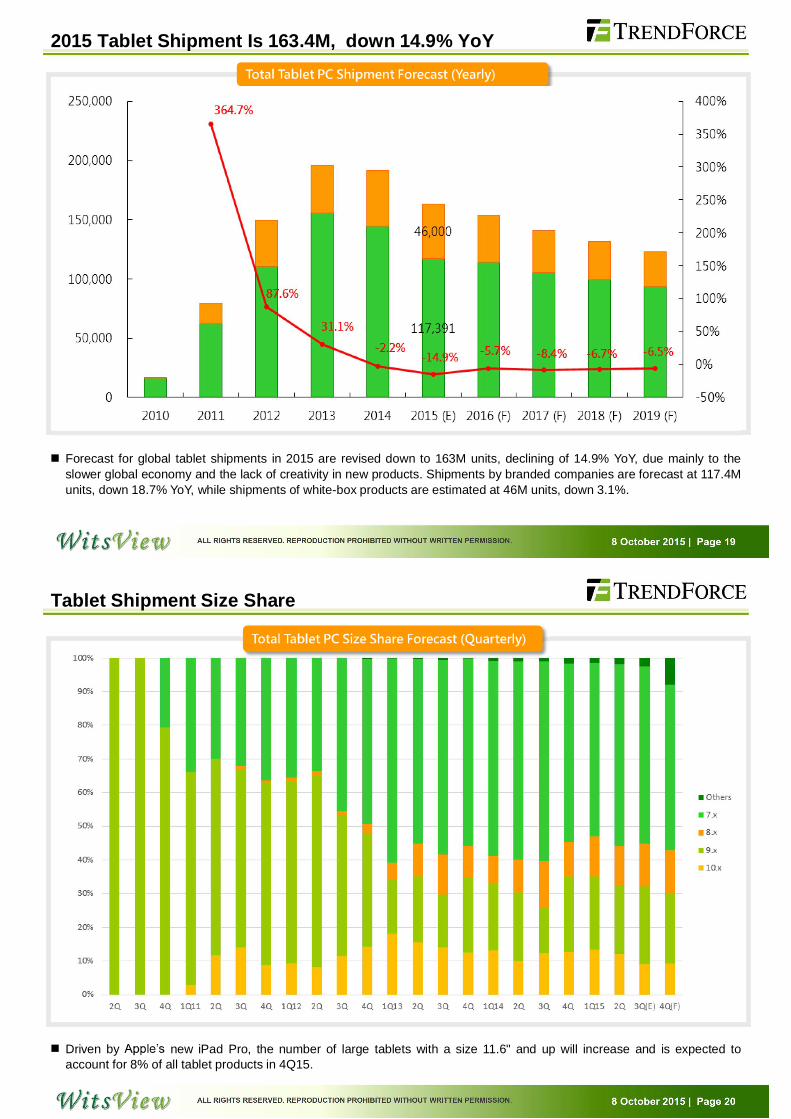

Forecast for global tablet shipments in 2015 are revised down to 163M units, declining of 14.9% YoY, due mainly to theslower global economy and the lack of creativity in new products. Shipments by branded companies are forecast at 117.4Munits, down 18.7% YoY, while shipments of white-box products are estimated at 46M units, down 3.1%.

2015 Tablet Shipment Is 163.4M, down 14.9% YoY

8 October 2015 | Page 20ALL RIGHTS RESERVED. REPRODUCTION PROHIBITED WITHOUT WRITTEN PERMISSION.

Driven by new iPad Pro, the number of large tablets with a size 11.6" and up will increase and is expected toaccount for 8% of all tablet products in 4Q15.

Tablet Shipment Size Share

8 October 2015 | Page 21ALL RIGHTS RESERVED. REPRODUCTION PROHIBITED WITHOUT WRITTEN PERMISSION.

Before 2014, smartphone market had been growing explosively. However, since 2015, due to saturation of the market, entiregrowth momentum has slowed down with annual growth rate maintaining below 10%.

Worldwide Smartphone Market Size Forecast

8 October 2015 | Page 22ALL RIGHTS RESERVED. REPRODUCTION PROHIBITED WITHOUT WRITTEN PERMISSION.

Since 2015, due to the trend of enlarging smartphone sizes and lowering prices of smartphones, the 5.x" has officiallyoccupied market share for over 50% of smartphones and become the mainstream size category.

2014-2019 Size Trend of Smartphone

8 October 2015 | Page 23ALL RIGHTS RESERVED. REPRODUCTION PROHIBITED WITHOUT WRITTEN PERMISSION.

Because prices of HD and FHD product are dropping, HD's and FHD's share continue to increase in global smartphonemarket. Shares for HD and FHD are 40.1% and 17.5% respectively.

For the resolution QHD-and-above, the prices are still high, and the speed of QHD-and-above to raise share is limited.

2014-2019 Resolution Trend of Smartphone

8 October 2015 | Page 24ALL RIGHTS RESERVED. REPRODUCTION PROHIBITED WITHOUT WRITTEN PERMISSION.

D

Outline

ownstream Demand Status

Supply and Demand Overview

Conclusion

Panel Industry Update

8 October 2015 | Page 25ALL RIGHTS RESERVED. REPRODUCTION PROHIBITED WITHOUT WRITTEN PERMISSION.

Large Size TFT-LCD Glass Input Area

8 October 2015 | Page 26ALL RIGHTS RESERVED. REPRODUCTION PROHIBITED WITHOUT WRITTEN PERMISSION.

New Capacity Update

8 October 2015 | Page 27ALL RIGHTS RESERVED. REPRODUCTION PROHIBITED WITHOUT WRITTEN PERMISSION.

Due to weakening demand of smartphone, some new LTPS fabs' timing of mass production is postponed, or plants plan toreduce capacities. Hence, the oversupply pressure is eased slightly.

The new LTPS Gen 6. fabs in Japan, Taiwan and China are estimated to enter mass production one by one in 2016.However, the real influence to the market will take place in 2H16 or 2017.

On-going LTPS Capacity Expansion

8 October 2015 | Page 28ALL RIGHTS RESERVED. REPRODUCTION PROHIBITED WITHOUT WRITTEN PERMISSION.

D

Outline

ownstream Demand Status

Supply and Demand Overview

Conclusion

Panel Industry Update

8 October 2015 | Page 29ALL RIGHTS RESERVED. REPRODUCTION PROHIBITED WITHOUT WRITTEN PERMISSION.

22 September 2015 | Page 1ALL RIGHTS RESERVED. REPRODUCTION PROHIBITED WITHOUT WRITTEN PERMISSION.

22 September 2015 | Page 2ALL RIGHTS RESERVED. REPRODUCTION PROHIBITED WITHOUT WRITTEN PERMISSION.

Established in 2004, TrendForce's LCD display division

consists of a team of panel industry experts. WitsView

research covers upstream components, midstream panels,

and downstream system and retail vendors. We believe

accurate research helps manufacturers avoid risk and

promotes profitability and high industry value. Therefore,

our research covers the industry from top to bottom,

providing analysis of each level of the industry chain,

thereby enabling clients to make informed decisions. Our

client list includes component makers, panel makers,

system integrators, channel vendors, brand manufacturers,

investment firms, and government organizations.

For more about WitsView, please visit www.witsview.com

2015 WitsView Market Intelligence

ID WitsViewMIServiceLineup Frequency

1 QuarterlyKeyComponentMarketUpdate Q PDF

17 QuarterlyKeyComponentPriceTracker Q Excel PDF

26 QuarterlyMonitor&LCDTVPanelCost&Breakdown Q Excel PDF

27 QuarterlyNotebook&TabletPanelCost&Breakdown Q Excel PDF

23 QuarterlyPanelCapacityStatusReport Q Excel PDF

2 QuarterlyPanelIndustryMarketUpdate Q PDF

5 MonthlyPanelPriceBook(5th,20th/M)&MarketStatusUpdate 2/M Excel PDF

7 MonthlyPanelPriceForecast M Excel

10 MonthlyPanelShipmentTracker M Excel PDF

22 QuarterlySufficiencyAnalysisReport Q Excel PDF

3 QuarterlyDownstreamIndustryMarketUpdate Q PDF

8 MonthlyStreetPriceBook M Excel PDF

12 MonthlyMonitorSystemIntegratorShipmentTracker M Excel PDF

13 MonthlyBrandedMonitorShipmentTracker M Excel PDF

14 QuarterlyLCDTVSystemIntegratorShipmentTracker Q Excel PDF

15 QuarterlyBrandedLCDTVShipmentTracker Q Excel PDF

16 MonthlyMobilePCODMShipmentTracker M Excel PDF

T1 QuarterlyTouchModuleCostBreakdownReport Q Excel PDF

T2 QuarterlyTouchModuleandTabletPCMarketUpdateReport Q PDF

T3 MonthlyTabletPanelandTouchModulePriceBook M Excel PDF

T5 QuarterlyBrandedTabletShipmentTracker Q Excel PDF

S1 MonthlyLCDTVPanelSupplyChainTracker M Excel

S2 MonthlyNotebookPanelSupplyChainTracker M Excel

S3 MonthlyPanelSupplierUtilizationOperationTracker M Excel PDF

![Global and US Outlook MABE Outlook 2011[1]](https://static.documents.pub/doc/80x56/577d34871a28ab3a6b8e3de1/global-and-us-outlook-mabe-outlook-20111.jpg)