38

| Date post: | 19-Dec-2015 |

| Category: |

Documents |

| View: | 226 times |

| Download: | 1 times |

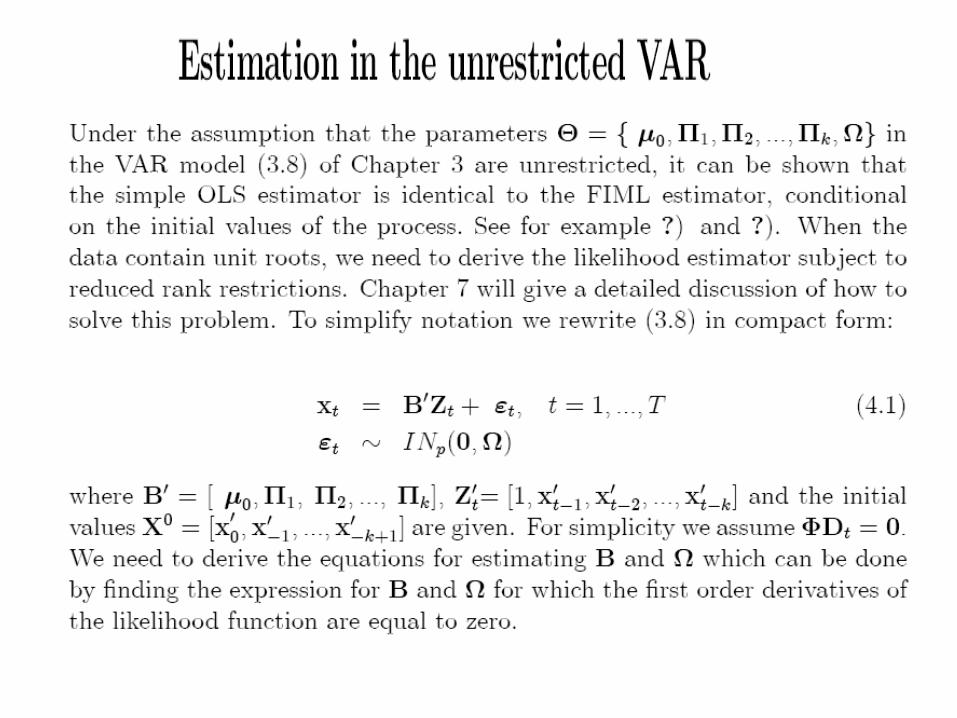

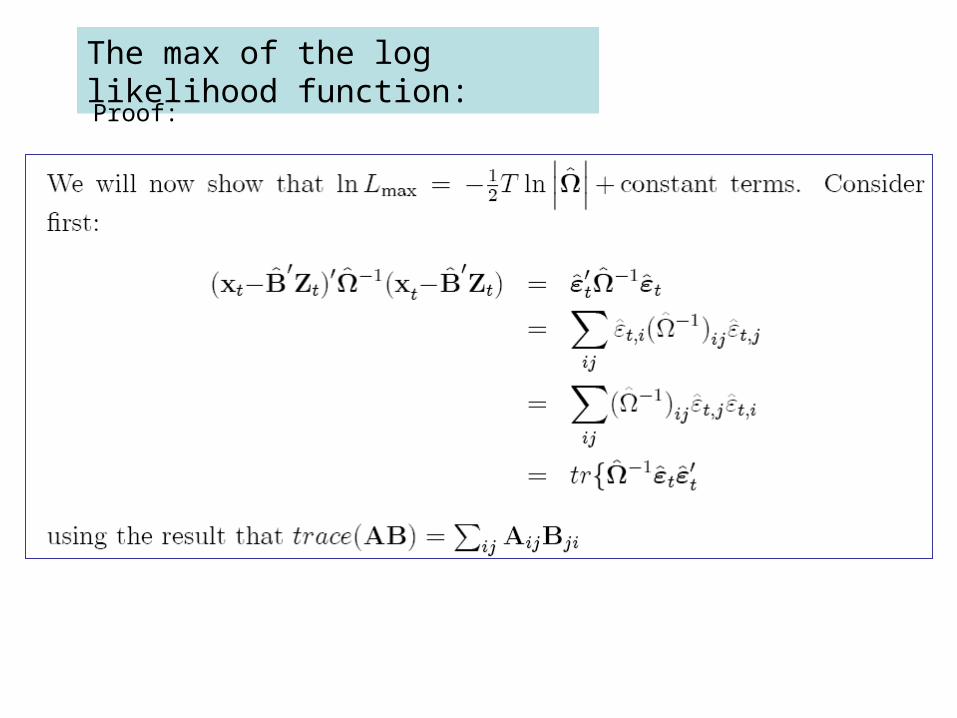

The max log likellihood function is simply a function of the error covariance matrix+ constant terms!

The max of the log likelihood function:

Proof:

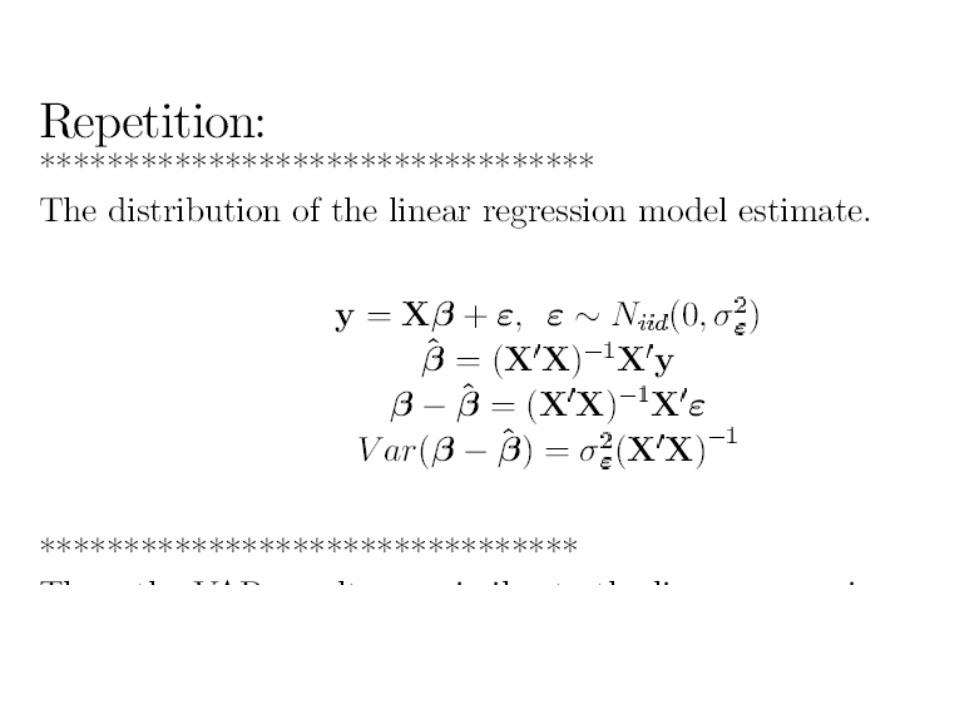

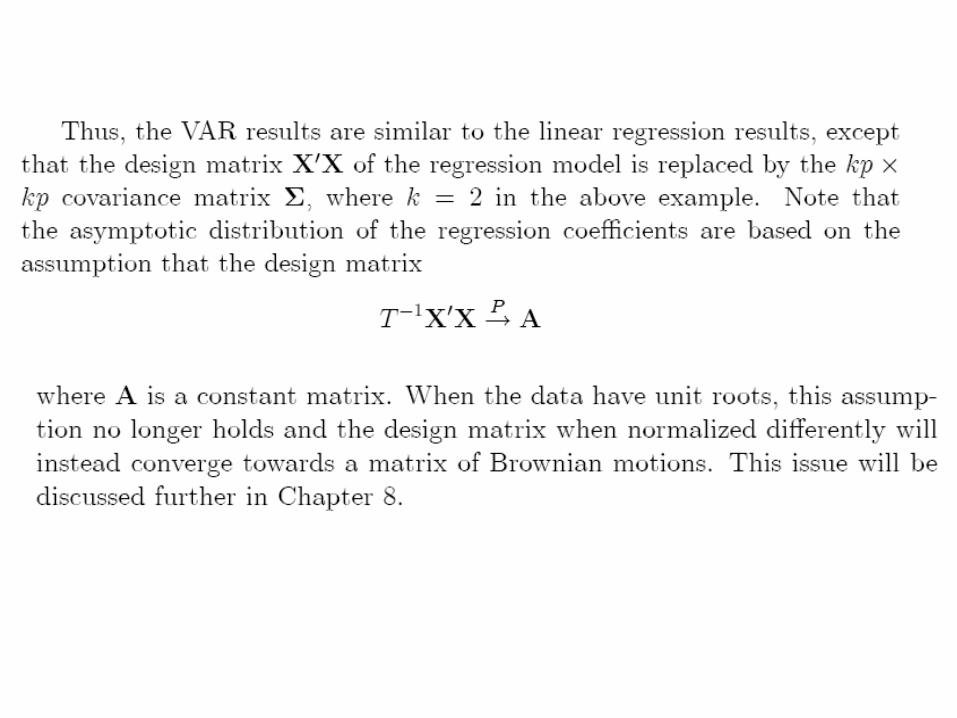

The distribution of the ML estimates:

The covariance matrix

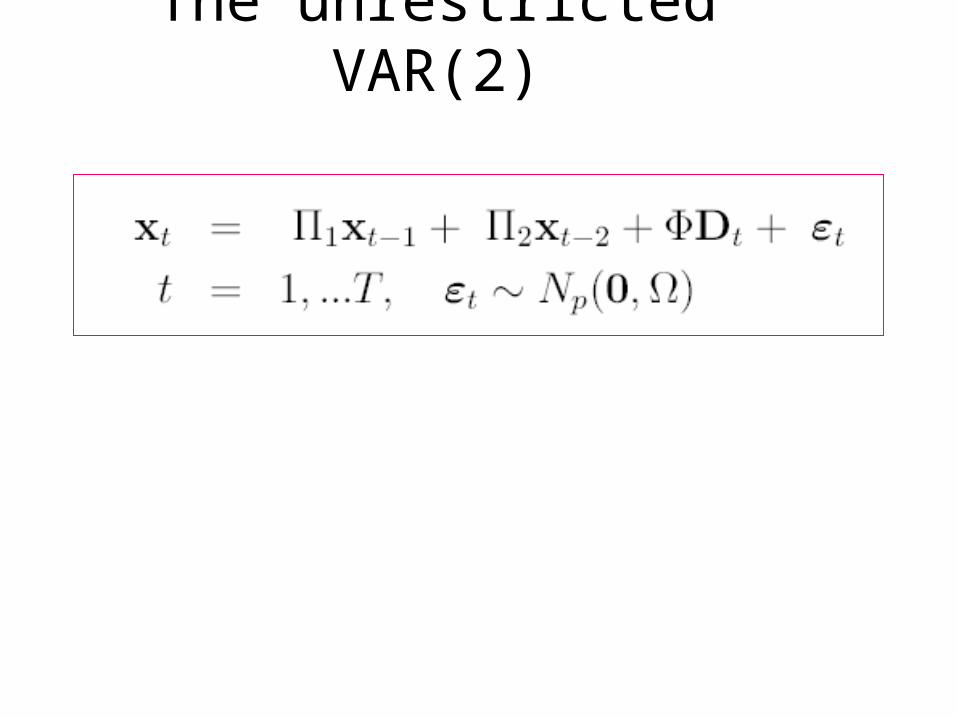

The unrestricted VAR(2)

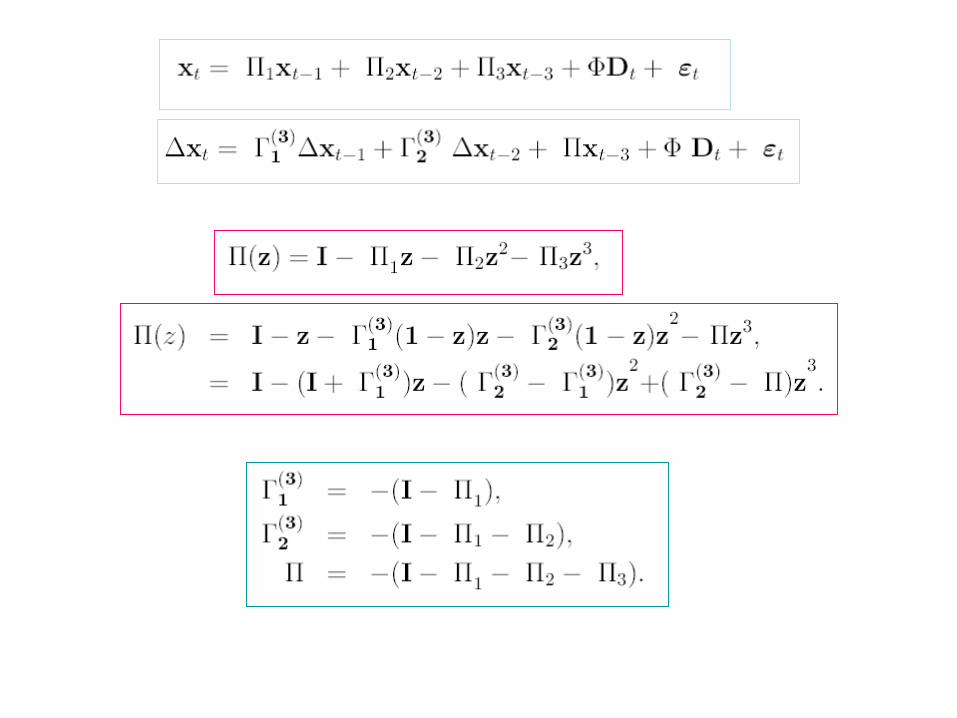

ECM representations

Ecm with m=1

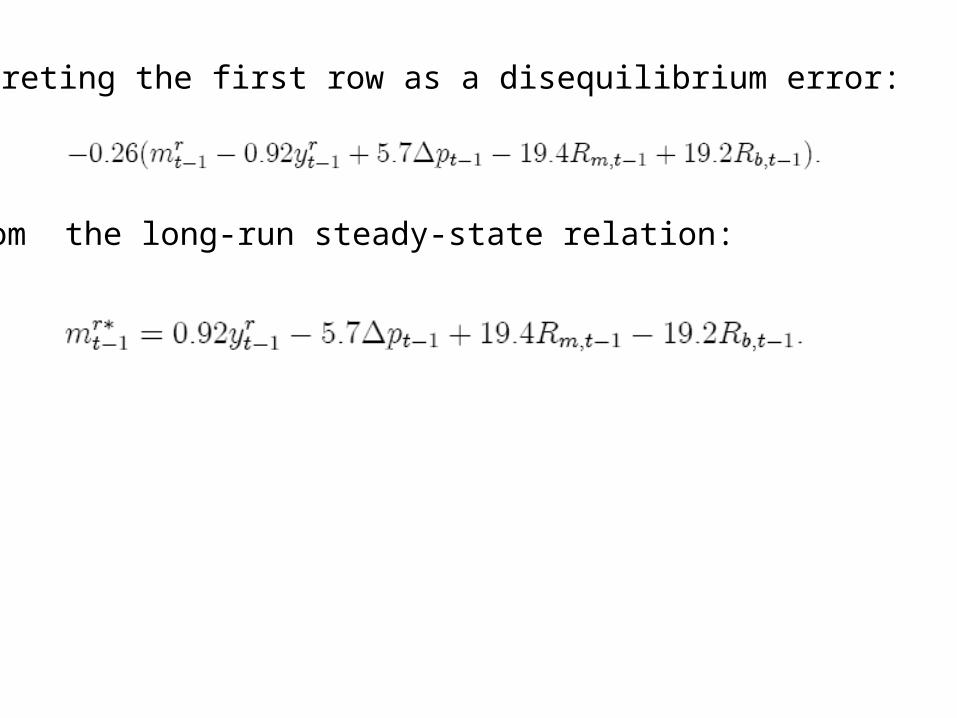

Interpreting the first row as a disequilibrium error:

from the long-run steady-state relation:

Ecm with m=2

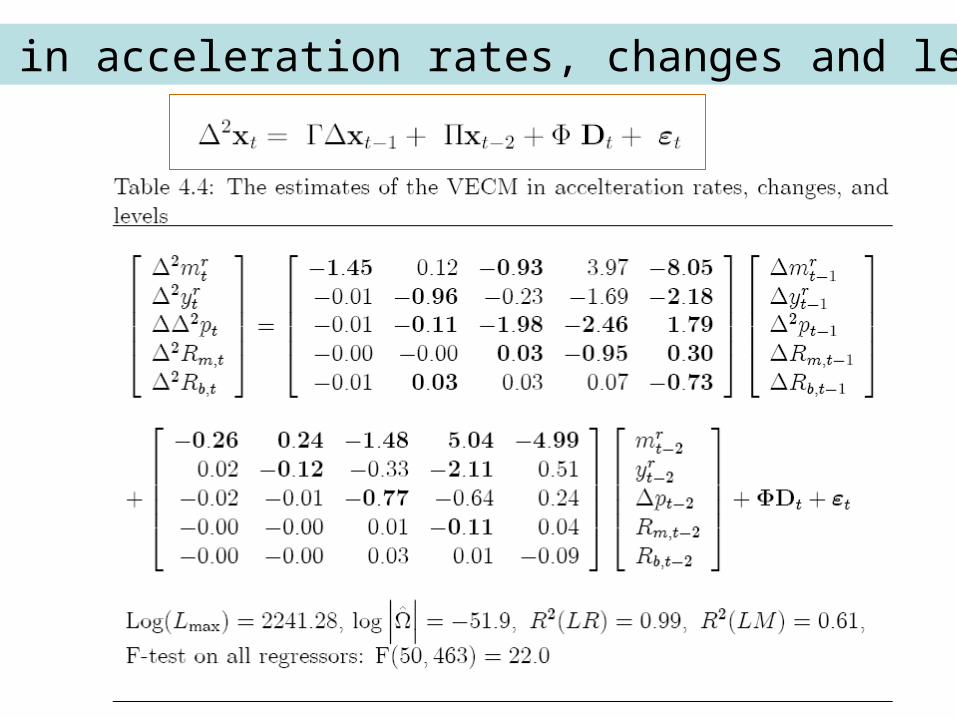

Ecm in acceleration rates, changes and levels

Invariant and variant testsF-tests of ind. Regressors:

m=1

Acceler. Rates:

Log likelihood value identical in all cases!

m=2

VAR

The relationship between the ECM parameters

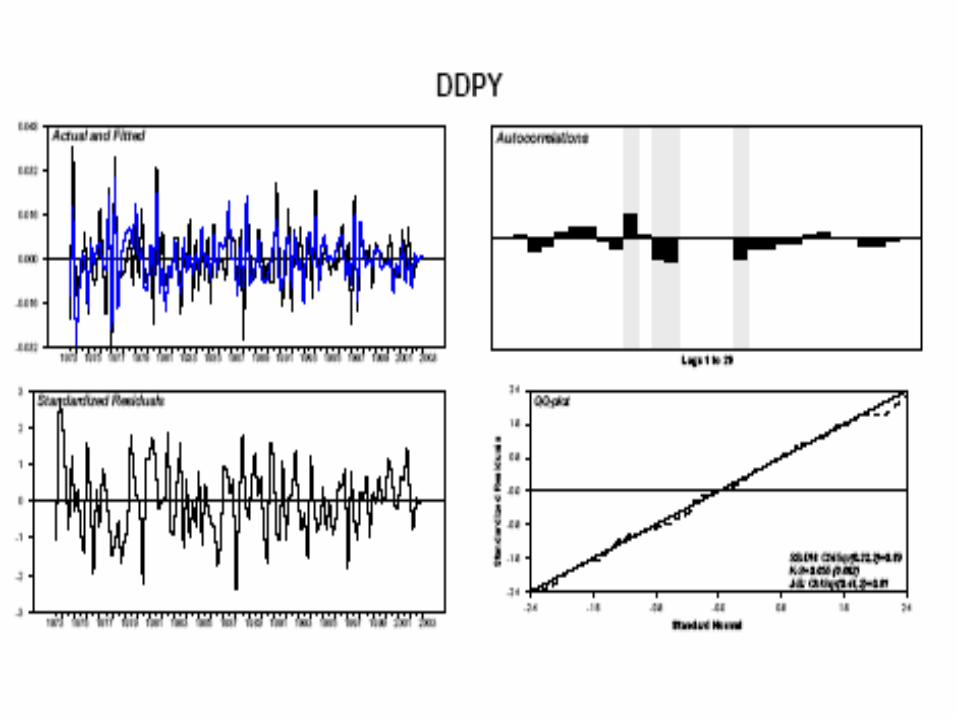

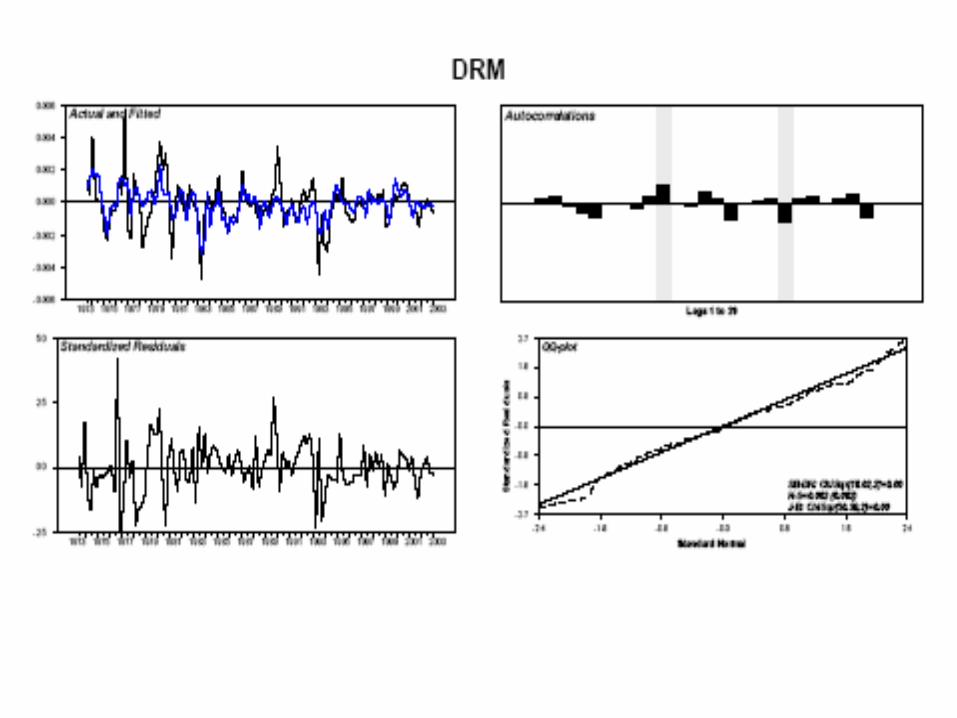

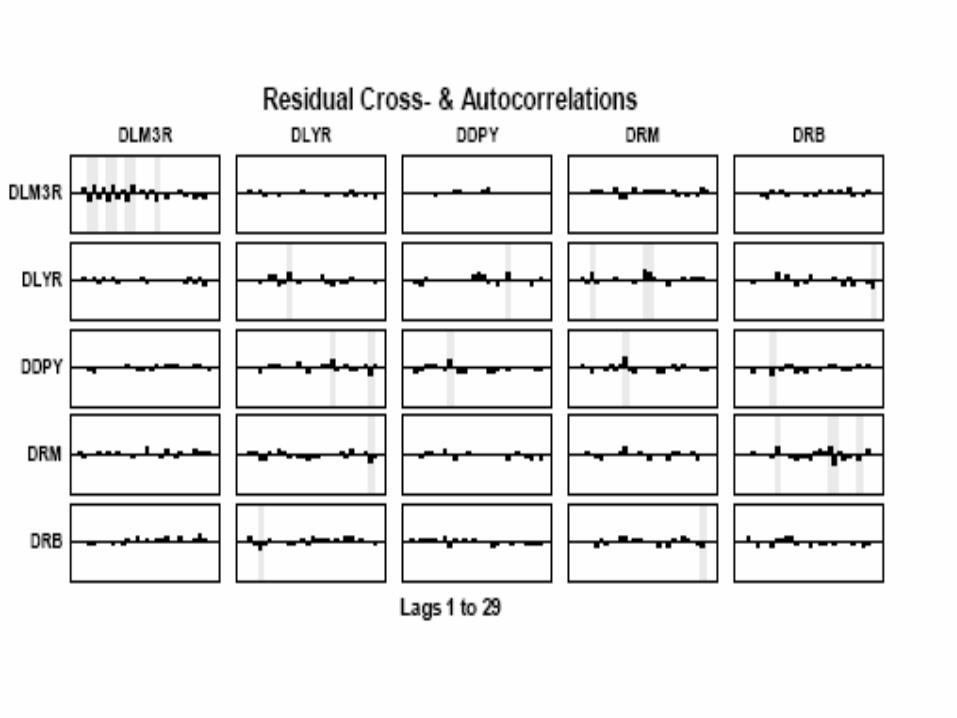

Misspecification tests

Information criteria

Choice of lag length

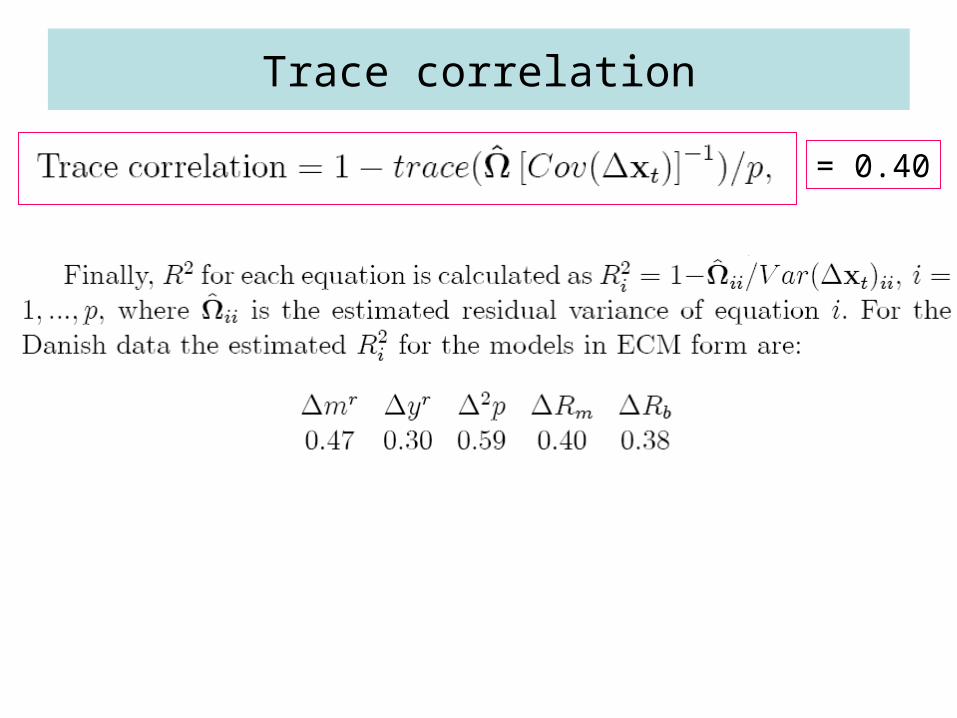

Trace correlation

= 0.40

Tests of residual autocorrelation

Tests of residual heteroscedasticity

Normality

• Skewness and excess kurtosis

• Univariate normality tests (Jarque-Bera)

• Mulivariate normallity test (Doornik-Hansen)

Univariate Normality tests

Asymptotic normality tests

Univariate Jarque-Bera type of test:

Multivariate Jarque-Bera type of test:

Approximate normality tests

Multivariate Bowman-Shenton normality test

What about the other tests?

The univariate normality tests