The medical schemes The medical schemes industry: regulatory industry: regulatory approach, trends, approach, trends, challenges & challenges & opportunities opportunities Briefing to the Portfolio Committee Briefing to the Portfolio Committee of Health of Health COUNCIL FOR MEDICAL SCHEMES COUNCIL FOR MEDICAL SCHEMES 20 May 2003 20 May 2003

Transcript

The medical schemes The medical schemes industry: regulatory industry: regulatory approach, trends, approach, trends,

Briefing to the Portfolio Committee of Briefing to the Portfolio Committee of HealthHealth

COUNCIL FOR MEDICAL SCHEMESCOUNCIL FOR MEDICAL SCHEMES

20 May 200320 May 2003

Presentation OutlinePresentation Outline

• Overview of the Council for Medical Overview of the Council for Medical SchemesSchemes

• Our regulatory approachOur regulatory approach

• Trends in the environmentTrends in the environment

• Update on key legislative issuesUpdate on key legislative issues

• Emerging opportunitiesEmerging opportunities

Presentation Outline

An Overview of the An Overview of the Council for Medical Council for Medical

SchemesSchemes

•Objectives of the Act

•Our Vision

•The Industry

•Accountability Structures

•Composition of the Council

•Office Organogram

•Divisions of the Office

•Staffing

Overview of the CMS

Medical Schemes Act, 131 of 1998:Medical Schemes Act, 131 of 1998:the enabling Actthe enabling Act

The Council for Medical Schemes was established in terms The Council for Medical Schemes was established in terms of the Medical Schemes Act, key policy objectives of which of the Medical Schemes Act, key policy objectives of which include to:include to:

Promote non-discriminatory access to privately funded Promote non-discriminatory access to privately funded health carehealth care

Reduce unnecessary financial burden on the public sectorReduce unnecessary financial burden on the public sector

Improve governance of medical schemes in the interests of Improve governance of medical schemes in the interests of membersmembers

Promote greater financial stability in the industryPromote greater financial stability in the industry

Improve consumer protection through enhanced Improve consumer protection through enhanced governmental oversightgovernmental oversight

Overview of the CMS

Our VisionOur Vision

A medical schemes industry which is regulated A medical schemes industry which is regulated

to protect the interests of members to protect the interests of members

and to promote and to promote

fair and equitable access to private health fair and equitable access to private health financing financing

in order to in order to

maximize the health of South Africansmaximize the health of South Africans

Overview of the CMS

Our 7 Strategic AimsOur 7 Strategic Aims Secure an appropriate level of protection for beneficiaries of Secure an appropriate level of protection for beneficiaries of

medical schemes and the public by authorizing the conduct of medical schemes and the public by authorizing the conduct of medical schemes business and monitoring the financial medical schemes business and monitoring the financial performance and soundness of schemesperformance and soundness of schemes

Provide support and guidance to trustees and promote Provide support and guidance to trustees and promote understanding of the medical schemes environment by trustees, understanding of the medical schemes environment by trustees, beneficiaries and the publicbeneficiaries and the public

Foster compliance with the Act by medical schemes, administrators Foster compliance with the Act by medical schemes, administrators and brokers and initiate enforcement action where requiredand brokers and initiate enforcement action where required

Investigate and resolve complaints raised by beneficiaries and the Investigate and resolve complaints raised by beneficiaries and the publicpublic

Monitor the impact of the Act, research developments and Monitor the impact of the Act, research developments and recommend policy options to improve the regulatory environmentrecommend policy options to improve the regulatory environment

Foster the continued development of the CMS as an employer of Foster the continued development of the CMS as an employer of choicechoice

Develop strategic alliances nationally, regionally and internationallyDevelop strategic alliances nationally, regionally and internationally

Overview of the CMS

The Industry The Industry (as at end 2001)(as at end 2001)

• 146 not-for-profit registered medical schemes146 not-for-profit registered medical schemes

• Numerous for-profit intermediariesNumerous for-profit intermediaries– AdministratorsAdministrators– BrokersBrokers– Managed care companiesManaged care companies– Reinsurance companiesReinsurance companies

• 7.02 million covered lives7.02 million covered lives

Composition of the Composition of the CouncilCouncil

• Consists of executive Chairman, Deputy Consists of executive Chairman, Deputy Chairman and 13 members, appointed by the Chairman and 13 members, appointed by the Minister of HealthMinister of Health

• Deputy Chair – Ms Nomgando MatyumzaDeputy Chair – Ms Nomgando Matyumza

• The Council comprises a broad spectrum of The Council comprises a broad spectrum of highly skilled senior people which include the highly skilled senior people which include the Director-General of Health, actuaries, lawyers, Director-General of Health, actuaries, lawyers, medical specialists and general practitionersmedical specialists and general practitioners

Overview of the CMS

Committees of CouncilCommittees of Council

• Council comprises of the following committees:Council comprises of the following committees:– EXCOEXCO– CouncilCouncil

• The following specialist sub-committees have The following specialist sub-committees have been established to aid Council in the been established to aid Council in the fulfillment of its complex mandate:fulfillment of its complex mandate:

• AppealsAppeals• Human ResourcesHuman Resources• Audit Audit • Research & Monitoring Research & Monitoring • Registration and AccreditationRegistration and Accreditation• Internal FinanceInternal Finance• LegalLegal• Financial SupervisionFinancial Supervision

Overview of the CMS

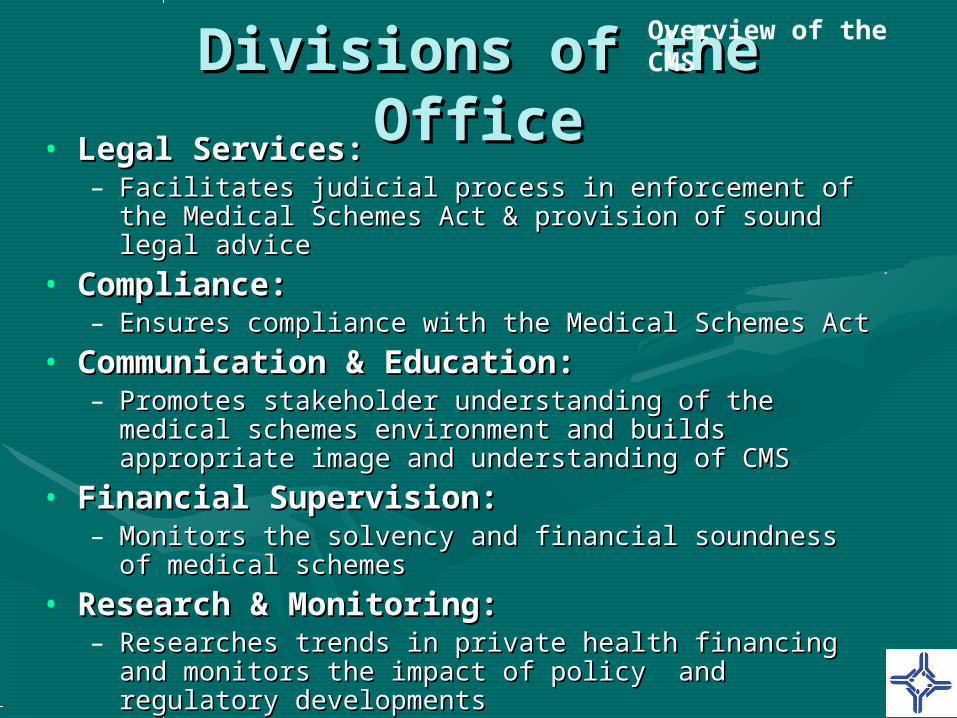

Divisions of the OfficeDivisions of the Office• Legal Services:Legal Services:

– Facilitates judicial process in enforcement of the Facilitates judicial process in enforcement of the Medical Schemes Act & provision of sound legal adviceMedical Schemes Act & provision of sound legal advice

• Compliance: Compliance: – Ensures compliance with the Medical Schemes ActEnsures compliance with the Medical Schemes Act

• Communication & Education:Communication & Education: – Promotes stakeholder understanding of the medical Promotes stakeholder understanding of the medical

schemes environment and builds appropriate image schemes environment and builds appropriate image and understanding of CMSand understanding of CMS

• Financial Supervision: Financial Supervision: – Monitors the solvency and financial soundness of Monitors the solvency and financial soundness of

medical schemesmedical schemes

• Research & Monitoring: Research & Monitoring: – Researches trends in private health financing and Researches trends in private health financing and

monitors the impact of policy and regulatory monitors the impact of policy and regulatory developmentsdevelopments

Overview of the CMS

• Registration and Accreditation:Registration and Accreditation: – Ensures proper registration of medical Ensures proper registration of medical

schemes, approval of scheme rules, and schemes, approval of scheme rules, and accreditation of healthcare brokers, brokerage accreditation of healthcare brokers, brokerage houses, managed care organizations and houses, managed care organizations and administratorsadministrators

• Complaints:Complaints:– Investigates and resolves complaints lodged by Investigates and resolves complaints lodged by

members, providers and other stakeholdersmembers, providers and other stakeholders• Internal Finance: Internal Finance:

– Maintains an effective system of internal Maintains an effective system of internal financial managementfinancial management

• Information Technology: Information Technology: – Implements IT initiatives that improve cost Implements IT initiatives that improve cost

effectiveness, service quality and business effectiveness, service quality and business development.development.

Staffing of the OfficeStaffing of the Office

• CEO & Registrar: Patrick MasobeCEO & Registrar: Patrick Masobe

• Head of Financial Supervision and CFO: Fikile Head of Financial Supervision and CFO: Fikile MothobiMothobi

• The Council for Medical Schemes comprises a The Council for Medical Schemes comprises a highly specialized team of multidisciplinary highly specialized team of multidisciplinary professionals. Together the members of the team professionals. Together the members of the team of 55 combine expertise in medical and nursing of 55 combine expertise in medical and nursing care, law, epidemiology, public health, care, law, epidemiology, public health, accounting, economics, information management accounting, economics, information management and administration.and administration.

Overview of the CMS

Our Regulatory ApproachOur Regulatory Approach• For the first couple of years of operation of the For the first couple of years of operation of the

Council for Medical Schemes and office of the Council for Medical Schemes and office of the Registrar, in terms of the Medical Schemes Act, Registrar, in terms of the Medical Schemes Act, 1998, our focus was largely on understanding the 1998, our focus was largely on understanding the environment, identifying and curbing blatant environment, identifying and curbing blatant abuses, and further developing the legislative abuses, and further developing the legislative framework to deal with emerging deficienciesframework to deal with emerging deficiencies

• Our focus has now evolved to one less reliant on Our focus has now evolved to one less reliant on “fire-fighting” and more focused on prioritising “fire-fighting” and more focused on prioritising strategic interventions with greatest impact on strategic interventions with greatest impact on the stability and sustainability of the environmentthe stability and sustainability of the environment

• This approach is based upon 7 key tenetsThis approach is based upon 7 key tenets

EnforcementBased

Regulation

Develop-mental

Regulation

ParticipativeRegulation

ResearchBased

Regulation

Risk BasedRegulation

ThematicRegulation

AnticipativeRegulation

7 Tenets of Our Regulatory

Approach

Our Regulatory Approach

Anticipative RegulationAnticipative Regulation• A proactive approach to regulating as opposed to a passive A proactive approach to regulating as opposed to a passive

approach leaving the industry to vagaries of the market, approach leaving the industry to vagaries of the market, economy, and disease patternseconomy, and disease patterns

• It involves imagining a medical schemes industry which accords It involves imagining a medical schemes industry which accords with a shared vision, and anticipating what will be needed to with a shared vision, and anticipating what will be needed to bridge the gap from that visionary future to the present. It bridge the gap from that visionary future to the present. It entails:entails:

– Visioning the future of the industry and the regulator, and generating Visioning the future of the industry and the regulator, and generating strategic dialogue within government and industry around that visionstrategic dialogue within government and industry around that vision

– Developing a shared understanding of strategic regulatory priorities Developing a shared understanding of strategic regulatory priorities for the short, medium and long term that will underpin that futurefor the short, medium and long term that will underpin that future

– Reviewing our broad strategic goals in light of that visionReviewing our broad strategic goals in light of that vision– Selecting strategic factors and assessing their impact Selecting strategic factors and assessing their impact – Focusing on strategic themes and factors with highest impact in the Focusing on strategic themes and factors with highest impact in the

short, medium and long term toward closing the gap between what short, medium and long term toward closing the gap between what we aspire for and current reality of the organizationwe aspire for and current reality of the organization

– Developing action plans that capture identified strategic priorities, Developing action plans that capture identified strategic priorities, and and moving to implementationmoving to implementation

Our Regulatory Approach

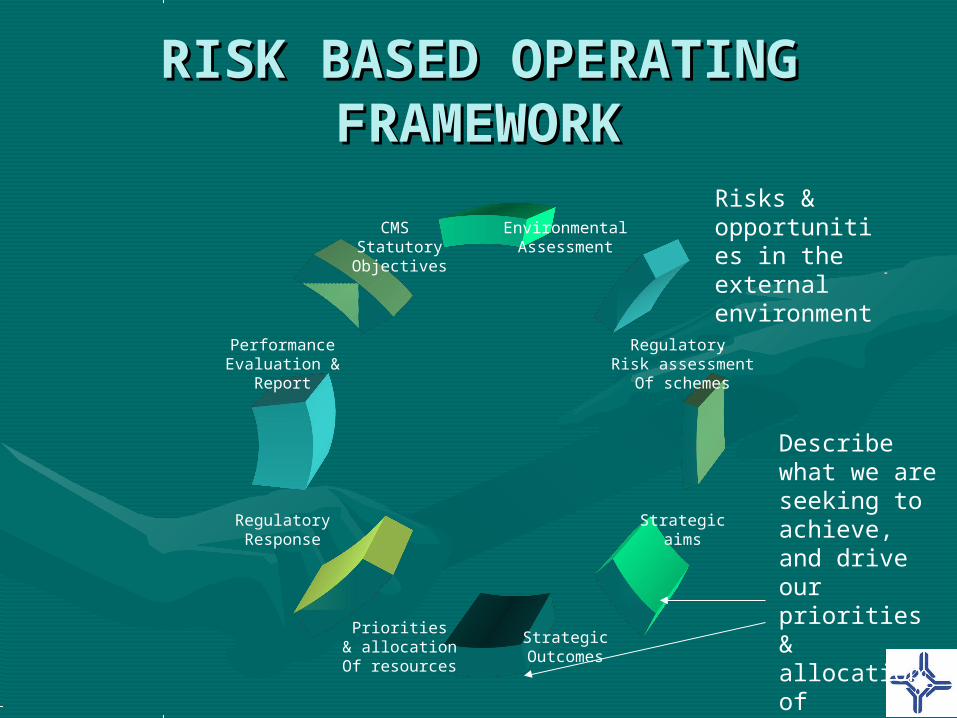

Risk Based RegulationRisk Based Regulation

• Focuses on identifying risks and solving associated problems Focuses on identifying risks and solving associated problems which are most critical to achieving our statutory objectiveswhich are most critical to achieving our statutory objectives

• Schemes are categorized into high, medium and low impact Schemes are categorized into high, medium and low impact schemes in terms of the extent to which their operation, and schemes in terms of the extent to which their operation, and potential failure, may impact on the medical schemes potential failure, may impact on the medical schemes environmentenvironment

• Risk assessments will be conducted for each high impact Risk assessments will be conducted for each high impact scheme, and individualized risk mitigation plans developed for scheme, and individualized risk mitigation plans developed for each such schemeeach such scheme

• Compliance with risk mitigation plans will be carefully Compliance with risk mitigation plans will be carefully monitored through frequent reporting, market intelligence and monitored through frequent reporting, market intelligence and on-site visitson-site visits

• This enables proactive management of risks before problems This enables proactive management of risks before problems materialize, and allows for effective prioritization of resourcesmaterialize, and allows for effective prioritization of resources

Our Regulatory Approach

RISK BASED OPERATING RISK BASED OPERATING FRAMEWORKFRAMEWORK

EnvironmentalAssessment

StrategicOutcomes

CMS StatutoryObjectives

Strategicaims

Regulatory Risk assessment

Of schemes

Priorities& allocationOf resources

RegulatoryResponse

PerformanceEvaluation &

Report

Risks & opportunities in the external environment.

Describe what we are seeking to achieve, and drive our priorities & allocation of resources

Thematic RegulationThematic Regulation• Activities of Council are increasingly integrated in “theme Activities of Council are increasingly integrated in “theme

projects” whose results have greatest impact on our regulatory projects” whose results have greatest impact on our regulatory objectivesobjectives

• For 2003/4, the theme projects are:For 2003/4, the theme projects are:

– Fair Treatment of Beneficiaries and the Public, which involves:Fair Treatment of Beneficiaries and the Public, which involves:• Developing an understanding of practices of medical schemes and Developing an understanding of practices of medical schemes and

intermediaries which might cause unfairnessintermediaries which might cause unfairness• Assessing the extent to which this unfairness is already satisfactorily Assessing the extent to which this unfairness is already satisfactorily

addressedaddressed• Developing strategies to improve protection of consumers where Developing strategies to improve protection of consumers where

safeguards are inadequatesafeguards are inadequate

– Developing the Risk-Based Regulatory approach, focusing on:Developing the Risk-Based Regulatory approach, focusing on:• Criteria for allocating schemes to impact bandsCriteria for allocating schemes to impact bands• Risk assessment plans and risk mitigation plans for high impact Risk assessment plans and risk mitigation plans for high impact

schemesschemes• Regulatory tools as part of the risk mitigation planRegulatory tools as part of the risk mitigation plan

– Managed Health Care and Risk Transfer, to:Managed Health Care and Risk Transfer, to:• Review current capitation contractsReview current capitation contracts• Assess the appropriateness of forms of risk transferAssess the appropriateness of forms of risk transfer• Propose mechanisms to ensure the appropriateness of risk transferPropose mechanisms to ensure the appropriateness of risk transfer

Our Regulatory Approach

Research Based Research Based RegulationRegulation

• Regulatory approaches are based, as far as possible, on sound Regulatory approaches are based, as far as possible, on sound research into trends in private health financing and the impact of research into trends in private health financing and the impact of policy and regulatory developmentspolicy and regulatory developments

• Research activities include a combination of literature reviews, Research activities include a combination of literature reviews, consultative processes, surveys, statistical methods, and data consultative processes, surveys, statistical methods, and data analysisanalysis

• Recent research outputs have included: Annual Reports of the Recent research outputs have included: Annual Reports of the Registrar, a stakeholder analysis, a study of governance structures Registrar, a stakeholder analysis, a study of governance structures in medical schemes, an assessment of contribution increases, and in medical schemes, an assessment of contribution increases, and a study on the costing of prescribed minimum benefitsa study on the costing of prescribed minimum benefits

• Endeavours are made to promote international best practice Endeavours are made to promote international best practice through study visits and hosting of counterpart regulators. through study visits and hosting of counterpart regulators. Consideration is also being given to a staff exchange programme Consideration is also being given to a staff exchange programme with comparable regulators internationallywith comparable regulators internationally

Our Regulatory Approach

Participative RegulationParticipative Regulation• We are committed to optimal transparency in regulatory approachesWe are committed to optimal transparency in regulatory approaches

• We strive to inform our activities as far as possible with stakeholder We strive to inform our activities as far as possible with stakeholder input and opinion, without succumbing to regulatory capture by input and opinion, without succumbing to regulatory capture by entities with vested interestentities with vested interest

• Consultative processes include: establishment of advisory Consultative processes include: establishment of advisory committees; invitations for comment on discussion documents; road committees; invitations for comment on discussion documents; road shows and consultative workshops; and focus group discussionsshows and consultative workshops; and focus group discussions

• Major consultative processes currently underway include:Major consultative processes currently underway include:– Invitation for comment on a financial soundness discussion paper, Invitation for comment on a financial soundness discussion paper,

outlining alternative regulatory approaches to prudential regulationoutlining alternative regulatory approaches to prudential regulation– An industry representative advisory committee on treatment algorithms An industry representative advisory committee on treatment algorithms

for the Chronic Disease List in the prescribed minimum benefits, plus for the Chronic Disease List in the prescribed minimum benefits, plus distribution of draft algorithms for commentdistribution of draft algorithms for comment

– Invitation for comment on the criteria for allocation of schemes into high, Invitation for comment on the criteria for allocation of schemes into high, medium and low impact bandsmedium and low impact bands

– Invitation for industry responses on the Treatment Action Campaign’s Invitation for industry responses on the Treatment Action Campaign’s complaint of alleged coverage of substandard treatment of HIV benefitscomplaint of alleged coverage of substandard treatment of HIV benefits

Our Regulatory Approach

Developmental Developmental RegulationRegulation

• This entails developing knowledge, skills and This entails developing knowledge, skills and abilities of key decision makers in relation to abilities of key decision makers in relation to scheme governance and enhancing consumer scheme governance and enhancing consumer awareness of rights and responsibilities. This is awareness of rights and responsibilities. This is done through done through inter aliainter alia: :

• trustee training programmes with basic curriculae on trustee training programmes with basic curriculae on issues of governance and administration, and more issues of governance and administration, and more advanced modules on issues of financial management, advanced modules on issues of financial management, clinical governance and health policy reformclinical governance and health policy reform

• workshops with consumer organizations and trade unions workshops with consumer organizations and trade unions in respect of responsible consumer behavior and rights in respect of responsible consumer behavior and rights and responsibilities in terms of the Medical Schemes Actand responsibilities in terms of the Medical Schemes Act

Our Regulatory Approach

Compliance Based Compliance Based RegulationRegulation

• Persistent non-compliance with regulatory requirements Persistent non-compliance with regulatory requirements demands, on occasion, tough enforcement actions, which we demands, on occasion, tough enforcement actions, which we do through:do through:

– Conducting scheduled and unscheduled inspectionsConducting scheduled and unscheduled inspections– Investigating, warning and prosecuting offendersInvestigating, warning and prosecuting offenders– Instituting disciplinary proceedingsInstituting disciplinary proceedings– Collaborating with specialized law enforcement agencies, such Collaborating with specialized law enforcement agencies, such

as the Office for Serious Economic Offences and the Specialized as the Office for Serious Economic Offences and the Specialized Commercial crimes CourtCommercial crimes Court

• Recent enforcement actions have included:Recent enforcement actions have included:

– Curatorships of KwaZulu-Natal Medical Scheme, Medicover 2000 Curatorships of KwaZulu-Natal Medical Scheme, Medicover 2000 and Telemed relating to problems with scheme governanceand Telemed relating to problems with scheme governance

– Suspension of 11 of the 15 trustees of ProSano medical scheme, Suspension of 11 of the 15 trustees of ProSano medical scheme, for alleged financial irregularities in the use of scheme fundsfor alleged financial irregularities in the use of scheme funds

– Collaboration with criminal authorities on the institution of Collaboration with criminal authorities on the institution of criminal proceedings against an unregistered operation, Africa criminal proceedings against an unregistered operation, Africa HealthHealth

Our Regulatory Approach

Underlying PrinciplesUnderlying Principles

• In executing the above Regulatory Approaches we In executing the above Regulatory Approaches we adopt the following principles of good regulation:adopt the following principles of good regulation:

• Acting in an administratively fair and transparent manner, Acting in an administratively fair and transparent manner, with integrity, professionalism and respectwith integrity, professionalism and respect

• Being conscious of the need to be cost-effective in the use Being conscious of the need to be cost-effective in the use of resources of the Council and those of the regulated of resources of the Council and those of the regulated entities;entities;

• Proportionate regulation, recognizing the responsibilities of Proportionate regulation, recognizing the responsibilities of members of Boards of Trustees of Medical Schemesmembers of Boards of Trustees of Medical Schemes

• Not unduly impeding innovation, while facilitating fair Not unduly impeding innovation, while facilitating fair competitioncompetition

Our Regulatory Approach

Trends in the Trends in the EnvironmentEnvironment

• Since the mid-1990’s there has been little overall Since the mid-1990’s there has been little overall growth in number of covered lives, although there growth in number of covered lives, although there has been significant member movement between has been significant member movement between medical schemesmedical schemes

• Unaudited figures suggest that this trend has Unaudited figures suggest that this trend has continued during 2002continued during 2002

• This can be attributed This can be attributed inter alia inter alia to:to:– cost escalation cost escalation – indirect discouragement of unhealthy lives from joining or indirect discouragement of unhealthy lives from joining or

remaining on schemesremaining on schemes– limited innovation in the creation of low cost medical limited innovation in the creation of low cost medical

schemes schemes – insufficient incentives for brokers to target the emerging insufficient incentives for brokers to target the emerging

market as opposed to existing membersmarket as opposed to existing members

Trends in the Environment

Membership 2000/2001Membership 2000/2001

Distribution of Beneficiaries in Medical SchemesDistribution of Beneficiaries in Medical Schemes

Financial TrendsFinancial Trends– Average solvency industry-wide has remained relatively Average solvency industry-wide has remained relatively

stable since 2000, with unaudited results showing some stable since 2000, with unaudited results showing some overall improvement during 2002overall improvement during 2002

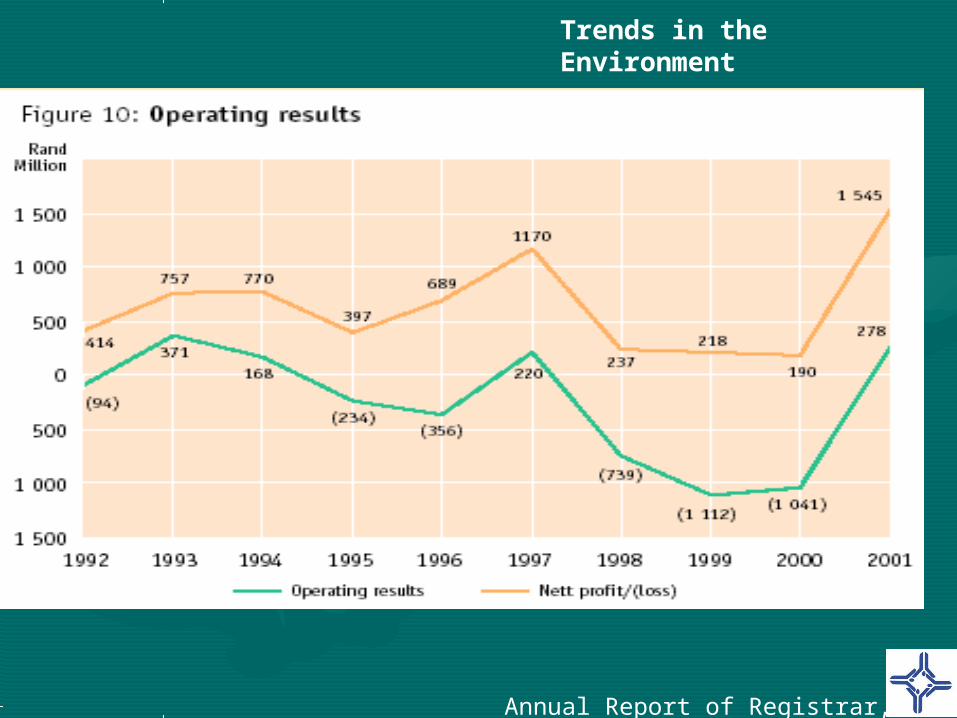

– Operating results have improved dramatically since 2000 Operating results have improved dramatically since 2000

– There has been significant improvement in accumulated There has been significant improvement in accumulated funds, continuing in 2002funds, continuing in 2002

– Exponential increases have been seen in non-health care Exponential increases have been seen in non-health care expenditure since the mid 1990s, although unaudited expenditure since the mid 1990s, although unaudited results for 2002 suggest that the rate of increase may be results for 2002 suggest that the rate of increase may be slowing downslowing down

– Expenditure on health care benefits continues to rise Expenditure on health care benefits continues to rise above the rate of normal inflation above the rate of normal inflation

Trends in the Environment

Please Note: Please Note:

All financial results for 2002 are All financial results for 2002 are based on unaudited based on unaudited

management accounts, and are management accounts, and are therefore subject to change in therefore subject to change in

the analysis of the audited the analysis of the audited annual 2002 statutory returns annual 2002 statutory returns

Accumulated Funds and Operating Accumulated Funds and Operating ResultsResults

• Minimum accumulated funds grew by 21,3% to R7,4 Minimum accumulated funds grew by 21,3% to R7,4 bn in 2001, and to R8.9 bn in 2002 (a further growth bn in 2001, and to R8.9 bn in 2002 (a further growth of 19.58%)***of 19.58%)***

• Net assets increased by 27.5% to R8,3bn in 2001, Net assets increased by 27.5% to R8,3bn in 2001, and to R10 bn in 2002 (a further growth of 21.3%)***and to R10 bn in 2002 (a further growth of 21.3%)***

• Compared to a loss of R1 bn in 2000, schemes Compared to a loss of R1 bn in 2000, schemes showed profits from operations of R 278m in 2001, showed profits from operations of R 278m in 2001, increasing to R1,5bn when investment income is increasing to R1,5bn when investment income is taken into account, and R2.25 bn in 2002 (a further taken into account, and R2.25 bn in 2002 (a further growth of 46.5%)***growth of 46.5%)***

***2002 figures are based on unaudited results

Trends in the Environment

Annual Report of Registrar, 2001

Trends in the Environment

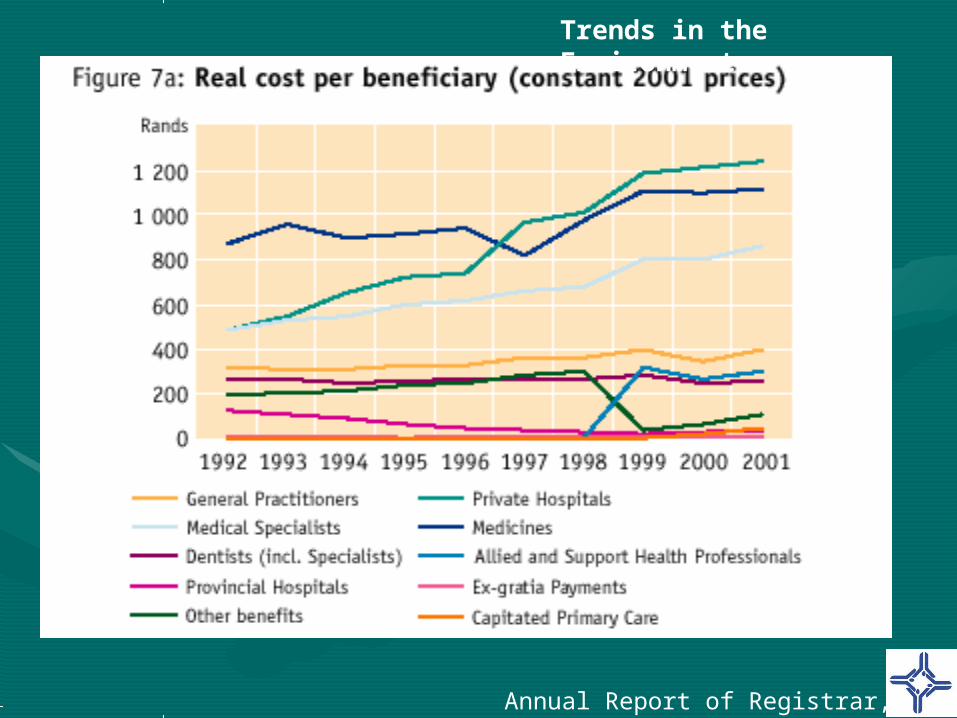

Expenditure TrendsExpenditure Trends

• Increase in expenditure on health care benefits has Increase in expenditure on health care benefits has continued to outstrip normal inflation since implementation continued to outstrip normal inflation since implementation of the Medical Schemes Act, with the major contributors of the Medical Schemes Act, with the major contributors being private hospitals, medicines and specialists being private hospitals, medicines and specialists

• Dramatic increases in non-healthcare expenditure have Dramatic increases in non-healthcare expenditure have been seen in recent years, including been seen in recent years, including inter alia inter alia administration expenditure, managed care fees, administration expenditure, managed care fees, reinsurance losses, and broker fees reinsurance losses, and broker fees

• This is illustrated in a decrease in claims ratios (% of This is illustrated in a decrease in claims ratios (% of contributions spent on health care benefits) from 89.3% in contributions spent on health care benefits) from 89.3% in 2000 to 83.1% in 20012000 to 83.1% in 2001

Trends in the Environment

Annual Report of Registrar, 2001

Trends in the Environment

Annual Report of Registrar, 2001

Trends in the Environment

Annual Report of Registrar, 2001

Trends in the Environment

• Unaudited results for 2002 suggest –Unaudited results for 2002 suggest –

– total benefits paid increased by 10.59% in 2002 (as total benefits paid increased by 10.59% in 2002 (as opposed to an increase of 13.7% in 2001)opposed to an increase of 13.7% in 2001)

– overall gross administration costs increased by 11.58% (as overall gross administration costs increased by 11.58% (as opposed to an increase of 41.7% in 2001):opposed to an increase of 41.7% in 2001):

• in open schemes the increase was 9.18% (as opposed to an in open schemes the increase was 9.18% (as opposed to an increase of 52.7% in 2001)increase of 52.7% in 2001)

– expenditure on managed care administration decreased expenditure on managed care administration decreased by 7.14% (as opposed to an increase of 11.4% in 2001)by 7.14% (as opposed to an increase of 11.4% in 2001)

– reinsurance losses in open schemes decreased by 7.14% reinsurance losses in open schemes decreased by 7.14% (as opposed to an increase of 61% in 2001)(as opposed to an increase of 61% in 2001)

– broker fees paid by medical schemes increased by 45.06% broker fees paid by medical schemes increased by 45.06% (as opposed to an increase of 26.09% in 2001)(as opposed to an increase of 26.09% in 2001)

– overall non-health expenditure increased by 8.70% in overall non-health expenditure increased by 8.70% in 2002.2002.

Trends in the Environment

Contribution IncreasesContribution Increases• The overall average increase in contributions from January 2002 to The overall average increase in contributions from January 2002 to

January 2003 was 14.1% for members, 15.9% for adult dependants January 2003 was 14.1% for members, 15.9% for adult dependants and 15.1% for child dependantsand 15.1% for child dependants

• Increases were slightly higher in open schemes than in restricted Increases were slightly higher in open schemes than in restricted schemesschemes

• Overall the rate of contribution increases were lower than in the Overall the rate of contribution increases were lower than in the previous yearprevious year

• Nevertheless, although lower, contribution increases were still high Nevertheless, although lower, contribution increases were still high in relation to both medical inflation and the consumer price indexin relation to both medical inflation and the consumer price index

• Contribution increases are driven, Contribution increases are driven, inter aliainter alia, by consumer , by consumer preference, supplier induced demand, the fee for service model of preference, supplier induced demand, the fee for service model of reimbursement, new technology and increasing non-health costsreimbursement, new technology and increasing non-health costs

Trends in the Environment

Contribution increases by type Contribution increases by type of medical schemeof medical scheme 2002/2003 2002/2003

0

5

10

15

20

25

Members Dependants Members Dependants Members Dependants

Open Restricted Registered

Per

cen

t

2002 2003

Trends in the Environment

An Update on Key An Update on Key Regulatory IssuesRegulatory Issues

• IntermediariesIntermediaries• Reinsurance contractsReinsurance contracts• BrokersBrokers• Managed health care organisationsManaged health care organisations• AdministratorsAdministrators

• Tariff settingTariff setting

Key Regulatory Issues

GovernanceGovernance• To a large extent, boards of trustees are exercising To a large extent, boards of trustees are exercising

independent decision-making in the interests of independent decision-making in the interests of beneficiaries, and compare well to international beneficiaries, and compare well to international experience on a number of key indicatorsexperience on a number of key indicators

• A study conducted for Council showed, however, A study conducted for Council showed, however, that while many boards are stable and strategically that while many boards are stable and strategically focused, others are still geared toward crisis focused, others are still geared toward crisis managementmanagement

• Repetition of serious alleged irregularities, as with Repetition of serious alleged irregularities, as with the recent example of ProSano medical scheme, will the recent example of ProSano medical scheme, will compel a critical review of aspects of the compel a critical review of aspects of the governance model enshrined in the Medical governance model enshrined in the Medical Schemes ActSchemes Act

Key Regulatory Issues

Financial SoundnessFinancial Soundness• Experience in regulating has convinced us that the approach to Experience in regulating has convinced us that the approach to

prudential regulation in the Medical Schemes Act is prudential regulation in the Medical Schemes Act is fundamentally sound, but that improvements can be made over fundamentally sound, but that improvements can be made over timetime

• Where problems have been encountered in relation to financial Where problems have been encountered in relation to financial soundness of schemes, these have typically been caused by: soundness of schemes, these have typically been caused by: inappropriate contracts with third parties; inadequate inappropriate contracts with third parties; inadequate contribution setting and lack of professional guidance; contribution setting and lack of professional guidance; inaccurate estimation of incurred but not recorded claims inaccurate estimation of incurred but not recorded claims (IBNR); and unwise investments(IBNR); and unwise investments

• Consultation is currently underway on a discussion document, Consultation is currently underway on a discussion document, inviting comments on a range of issues, including:inviting comments on a range of issues, including:– Requirements for professional supervision of contribution-settingRequirements for professional supervision of contribution-setting– Calculation of IBNRCalculation of IBNR– Inclusion of considerations of risk transfer in solvency assessmentInclusion of considerations of risk transfer in solvency assessment– Risk-based capital approaches to solvency regulationRisk-based capital approaches to solvency regulation

Key Regulatory Issues

Benefits: Benefits: Delivery of Prescribed Minimum Delivery of Prescribed Minimum

BenefitsBenefits• Medical schemes responded to implementation of PMBs by Medical schemes responded to implementation of PMBs by

amending rules to say PMBs would be covered only in public amending rules to say PMBs would be covered only in public hospitalshospitals

• In general –In general –– administrative systems were not configured to identify PMBs, administrative systems were not configured to identify PMBs,

with the result that there was little impact on benefit protectionwith the result that there was little impact on benefit protection– additionally, no arrangements were made with public hospitals additionally, no arrangements were made with public hospitals

to accommodate patientsto accommodate patients– in some cases where members relied on PMB protection, in some cases where members relied on PMB protection,

medical schemes denied coverage where public hospitals could medical schemes denied coverage where public hospitals could not accommodate themnot accommodate them

• As of 1 January 2004, medical schemes will be incentivised As of 1 January 2004, medical schemes will be incentivised to specifically contract with the public sector or other low to specifically contract with the public sector or other low cost providers to deliver PMBs, because they will be liable cost providers to deliver PMBs, because they will be liable through regulation to cover the benefits in an alternative through regulation to cover the benefits in an alternative provider if the provider of the scheme’s choice is not provider if the provider of the scheme’s choice is not reasonably availablereasonably available

Key Regulatory Issues

Benefits:Benefits:PMB Chronic Disease ListPMB Chronic Disease List

• Since implementation of the Medical Schemes Since implementation of the Medical Schemes Act, there has been an industry-wide trend to Act, there has been an industry-wide trend to reduce coverage for chronic disease conditions, reduce coverage for chronic disease conditions, with the effect that continued membership of with the effect that continued membership of chronically ill persons was discouragedchronically ill persons was discouraged

• As of 1 January 2004, a set of 25 chronic As of 1 January 2004, a set of 25 chronic conditions will be included in the prescribed conditions will be included in the prescribed minimum benefits – requiring full coverage for at minimum benefits – requiring full coverage for at least basic defined treatment of these conditionsleast basic defined treatment of these conditions

• This should significantly reduce opportunity for This should significantly reduce opportunity for indirect discrimination against sufferers of chronic indirect discrimination against sufferers of chronic diseasesdiseases

Key Regulatory Issues

Benefits: PMB CostingBenefits: PMB Costing

• A recent study found the monthly cost of A recent study found the monthly cost of PMBs (including the chronic disease list) in PMBs (including the chronic disease list) in 2001 prices for a low income family of four 2001 prices for a low income family of four to be, on average:to be, on average:– R 640.33 in the private sectorR 640.33 in the private sector– R416.76 in the public sectorR416.76 in the public sector

• The study found that the cost of PMBs The study found that the cost of PMBs does not unduly impact on affordability of does not unduly impact on affordability of low cost medical schemeslow cost medical schemes

Key Regulatory Issues

Benefits: HIV CoverageBenefits: HIV Coverage• PMBs were expanded in 2003 to include,PMBs were expanded in 2003 to include, inter alia inter alia, coverage for , coverage for

voluntary counseling and testing, and post-exposure prophylaxis voluntary counseling and testing, and post-exposure prophylaxis following sexual assault and occupational exposurefollowing sexual assault and occupational exposure

• It stopped short of including coverage for chronic (ongoing) It stopped short of including coverage for chronic (ongoing) provision of anti-retroviral therapy (ART)provision of anti-retroviral therapy (ART)

• A study conducted by the Centre for Actuarial Research in 2001 A study conducted by the Centre for Actuarial Research in 2001 showed nevertheless that while there is reasonably widespread showed nevertheless that while there is reasonably widespread coverage of ART, utilisation of these benefits has been minimalcoverage of ART, utilisation of these benefits has been minimal

• The Treatment Action Campaign (TAC) has alleged coverage of The Treatment Action Campaign (TAC) has alleged coverage of substandard HIV prophylaxis by some medical schemessubstandard HIV prophylaxis by some medical schemes

• In response to the TAC complaint, the Council has launched an In response to the TAC complaint, the Council has launched an extensive investigation into HIV coverage by medical schemes, extensive investigation into HIV coverage by medical schemes, with release of results anticipated in September 2003with release of results anticipated in September 2003

• Various for-profit entities have Various for-profit entities have submitted applications for exemption submitted applications for exemption from the Medical Schemes Act for from the Medical Schemes Act for products that offer HIV-only benefitsproducts that offer HIV-only benefits

• These entities typically do the These entities typically do the business of a medical schemebusiness of a medical scheme

Key Regulatory Issues

Medical Scheme

Traditional Medical Scheme Traditional Medical Scheme ArrangementArrangement

Employer

Managed CareOrganisation

Provider

Employee

Contributions

Contracts

Service (PMB + other)

Key Regulatory Issues

HIV Fund

Proposed HIV Carve-Out Proposed HIV Carve-Out ArrangementArrangement

Employer

Managed CareOrganisation

Provider

Employee

Contributions

Contracts

Service (HIV only)

Key Regulatory Issues

• While recognising the public health crisis presented by the While recognising the public health crisis presented by the HIV epidemic, Council has been unable to grant blanket HIV epidemic, Council has been unable to grant blanket exemptions for applications made thus far, because –exemptions for applications made thus far, because –

– it would result in these products operating in a regulatory it would result in these products operating in a regulatory vacuum, and consumers would therefore lack protection in an vacuum, and consumers would therefore lack protection in an area susceptible to significant abusearea susceptible to significant abuse

– it is Council’s assessment that it would be exceeding its it is Council’s assessment that it would be exceeding its statutory powers to grant these exemptions, and cannot do so statutory powers to grant these exemptions, and cannot do so in the absence of specific legislative provision for thisin the absence of specific legislative provision for this

• Circumstances nevertheless exist in which Council is able to Circumstances nevertheless exist in which Council is able to provide limited exemptions, and guideline principles for provide limited exemptions, and guideline principles for such exemptions are availablesuch exemptions are available

• Council has also given the go-ahead to certain employer-Council has also given the go-ahead to certain employer-based HIV programmes (e.g. De Beers) which entail direct based HIV programmes (e.g. De Beers) which entail direct funding of HIV-related expenses by the employer in the funding of HIV-related expenses by the employer in the absence of contributions to an entity in return for liability absence of contributions to an entity in return for liability being incurred, which in our assessment have not being incurred, which in our assessment have not conducted the business of a medical scheme and therefore conducted the business of a medical scheme and therefore have fallen outside the Medical Schemes Acthave fallen outside the Medical Schemes Act

Key Regulatory Issues

Benefits: DemarcationBenefits: Demarcation

• There are regrettably still certain players in There are regrettably still certain players in the market who seek to circumvent the the market who seek to circumvent the provisions of the Medical Schemes Act, provisions of the Medical Schemes Act, relating to open enrollment, community relating to open enrollment, community rating etc, by doing the business of a medical rating etc, by doing the business of a medical scheme under the guise of health insurancescheme under the guise of health insurance

• Council is working with Senior Counsel and Council is working with Senior Counsel and prosecuting authorities to bring a test prosecuting authorities to bring a test prosecution case to the courts in the near prosecution case to the courts in the near futurefuture

• The Medical Schemes Amendment Act 2001 required The Medical Schemes Amendment Act 2001 required medical schemes to obtain independent evaluations of the medical schemes to obtain independent evaluations of the need for reinsurance, and scrutiny by the Registrar, before need for reinsurance, and scrutiny by the Registrar, before entering into reinsurance contractsentering into reinsurance contracts

• Although full implementation of these changes is still in Although full implementation of these changes is still in progress, preliminary assessment of the impact of these progress, preliminary assessment of the impact of these amendments is favourable:amendments is favourable:– unaudited results show a decline in overall reinsurance losses unaudited results show a decline in overall reinsurance losses

during 2002during 2002– in some cases, dramatic turn-arounds in solvency positions of in some cases, dramatic turn-arounds in solvency positions of

schemes have been seen following intervention by the schemes have been seen following intervention by the Registrar on reinsurance practicesRegistrar on reinsurance practices

– in some cases, large amounts paid in premiums on invalid in some cases, large amounts paid in premiums on invalid contracts have been recovered for memberscontracts have been recovered for members

– healthy interaction has been generated between schemes and healthy interaction has been generated between schemes and the office of the Registrar in relation to issues of sound the office of the Registrar in relation to issues of sound financial governancefinancial governance

Key Regulatory Issues

Intermediaries: BrokersIntermediaries: Brokers• The Medical Schemes Amendment Act, 2002, harmonising The Medical Schemes Amendment Act, 2002, harmonising

the relationship between the Medical Schemes Act and the the relationship between the Medical Schemes Act and the Financial Advisory and Intermediary Services Act, came into Financial Advisory and Intermediary Services Act, came into operation on 1 May 2003operation on 1 May 2003

• A joint working committee has been established between the A joint working committee has been established between the Council for Medical Schemes and the Financial Services Council for Medical Schemes and the Financial Services Board to coordinate effective regulation of health broker Board to coordinate effective regulation of health broker activityactivity

• Improved regulations on broker conduct and remuneration, Improved regulations on broker conduct and remuneration, and expanding the enforcement powers of the Registrar of and expanding the enforcement powers of the Registrar of Medical Schemes, took effect on 1 January 2003Medical Schemes, took effect on 1 January 2003

• Overall, these legislative developments have created an Overall, these legislative developments have created an environment in which brokers are more effectively regulated environment in which brokers are more effectively regulated and consumers are better protectedand consumers are better protected

• For the first time, relatively comprehensive For the first time, relatively comprehensive regulations regarding the implementation of regulations regarding the implementation of managed care programmes and the operation of managed care programmes and the operation of managed care organisations came into effect on 1 managed care organisations came into effect on 1 January 2003January 2003

• Regulations focused on promoting greater Regulations focused on promoting greater transparency in managed care interventions and transparency in managed care interventions and improved quality of careimproved quality of care

• Council is currently developing a set of accreditation Council is currently developing a set of accreditation standards for managed care organisations, to be standards for managed care organisations, to be implemented in the second half of this yearimplemented in the second half of this year

• A consortium, led by KPMG, was appointed A consortium, led by KPMG, was appointed to work together with Council in the to work together with Council in the development of accreditation standards development of accreditation standards for third party administrators and to for third party administrators and to conduct evaluations of compliance with conduct evaluations of compliance with those standardsthose standards

• The process is in an advanced stage, and The process is in an advanced stage, and evaluations of administrators will evaluations of administrators will commence in the near futurecommence in the near future

Key Regulatory Issues

Tariff SettingTariff Setting• Agreement on recommended tariffs between funders and Agreement on recommended tariffs between funders and

providers was complicated this year by disputes over providers was complicated this year by disputes over intellectual property of tariff codes and descriptors, intellectual property of tariff codes and descriptors, disagreement on appropriate reimbursement levels, and disagreement on appropriate reimbursement levels, and uncertainty over the implications of competition legislationuncertainty over the implications of competition legislation

• Deadlock in tariff discussions during December 2002 and Deadlock in tariff discussions during December 2002 and January 2003 resulted in severe disruption of payment of January 2003 resulted in severe disruption of payment of member claimsmember claims

• In response, the Minister of Health appointed a committee to In response, the Minister of Health appointed a committee to develop and understanding of the problems and to formulate develop and understanding of the problems and to formulate recommendations to prevent a recurrencerecommendations to prevent a recurrence

• The Council is also in discussions with the Competition The Council is also in discussions with the Competition Commission in relation to its investigations into collusion and Commission in relation to its investigations into collusion and price-setting in the private health sectorprice-setting in the private health sector

Key Regulatory Issues

Emerging OpportunitiesEmerging Opportunities

• Public Servants Medical SchemePublic Servants Medical Scheme

• Social Health InsuranceSocial Health Insurance

• Risk EqualizationRisk Equalization

Emerging Opportunities

Public Servants’ Medical Public Servants’ Medical SchemeScheme

• Open choice of medical scheme for public servants results in:Open choice of medical scheme for public servants results in:– substantial intermediary costssubstantial intermediary costs– administrative inefficienciesadministrative inefficiencies– fragmentation of risk pools, and loss of economies of scale and fragmentation of risk pools, and loss of economies of scale and

purchasing powerpurchasing power– inequities in government subsidies resulting in inadequate inequities in government subsidies resulting in inadequate

coveragecoverage

• The proposed public servants’ medical scheme will reduce or The proposed public servants’ medical scheme will reduce or eliminate many of these problemseliminate many of these problems

• If properly managed, it can have substantial industry wide If properly managed, it can have substantial industry wide benefit , by:benefit , by:– stimulating much needed consolidation of small risk poolsstimulating much needed consolidation of small risk pools– consolidating bargaining power in respect of purchase of health consolidating bargaining power in respect of purchase of health

services and non-health commodities, thereby reducing overall services and non-health commodities, thereby reducing overall costs in the industrycosts in the industry

Emerging Opportunities

Social Health InsuranceSocial Health Insurance

• Social health insurance proposals which are Social health insurance proposals which are currently subject to consultation offer the currently subject to consultation offer the opportunity to achieve considerably greater opportunity to achieve considerably greater equity in access to health care of South equity in access to health care of South AfricansAfricans

• Key proposals around mandatory coverage Key proposals around mandatory coverage for people who can afford it, restructuring of for people who can afford it, restructuring of the tax subsidy, a Central Equity Fund, and the tax subsidy, a Central Equity Fund, and the creation of a low cost State-sponsored the creation of a low cost State-sponsored medical scheme, create the conditions for medical scheme, create the conditions for long-term sustainability of the public and long-term sustainability of the public and private health funding environmentsprivate health funding environments

Emerging Opportunities

Risk EqualisationRisk Equalisation• The Taylor Commission recommended that implementation of The Taylor Commission recommended that implementation of

a risk-equalisation mechanism should be “prioritised for a risk-equalisation mechanism should be “prioritised for immediate development and implementation”immediate development and implementation”

• Internationally, risk equalisation is widely regarded as a Internationally, risk equalisation is widely regarded as a prerequisite for the successful long-term implementation of prerequisite for the successful long-term implementation of open enrolment and community ratingopen enrolment and community rating

• In the absence of risk equalisation, variation in risk profile In the absence of risk equalisation, variation in risk profile implies substantial cost differences for schemes unrelated to implies substantial cost differences for schemes unrelated to their efficiency in managing costs, whereas risk equalisation their efficiency in managing costs, whereas risk equalisation promotes competition based on cost, quality of health service promotes competition based on cost, quality of health service and administrative efficienciesand administrative efficiencies

• Nevertheless, further work needs to be conducted into the Nevertheless, further work needs to be conducted into the feasibility of implementing risk equalisation in the South feasibility of implementing risk equalisation in the South African contextAfrican context

Emerging Opportunities

Concluding quotation Concluding quotation

““[Regulatory bodies need to] acknowledge the need [Regulatory bodies need to] acknowledge the need to make choices. Make them rationally, to make choices. Make them rationally, analytically and democratically. Take analytically and democratically. Take responsibility for the choices you make. Correct, responsibility for the choices you make. Correct, by using your judgment, deficiencies of law. by using your judgment, deficiencies of law. Organize yourself to deliver important results. Organize yourself to deliver important results. Choose specific goals of public value and focus on Choose specific goals of public value and focus on them. Devise methods that are economical with them. Devise methods that are economical with respect to the use of state authority, the respect to the use of state authority, the resources of the regulated community, and the resources of the regulated community, and the resources of the agency. And as you carefully resources of the agency. And as you carefully pick and choose what to do and how to do it, pick and choose what to do and how to do it, reconcile your pursuit of effectiveness with the reconcile your pursuit of effectiveness with the values of justice and equity.”values of justice and equity.”

Malcolm Sparrow, Malcolm Sparrow, The The Regulatory CraftRegulatory Craft