120 R. Dixon et al. / Accounting Forum 28 (2004) 119–138

1. Introduction

The 1990s have witnessed growth in, green consumerism, green ethical investment trustsand general environmental concerns that have lead to specific changes in business practiceand its environment and it can be expected that these changes will affect the accountingprofession (Gray, 1990, p. 65). The Institute of Chartered Accountants in England andWales (ICAEW, 1992, p. 3) points out that “ where environmental factors will impact on acompany’s policy and activities, and will impose costs on the company, or affect its assetvalues or liabilities, actual or contingent, the financial consequences need to be accountedfor or reported in accordance with existing accounting requirements”.

In the past, consumers have demanded traditional information to make their economicchoice in areas such as, value, price, quality, and service. Now consumers have new valuessuch as, the impact of products on the environment, environmental protection,. . . , etc. andthey need information about those values to express their choice and make the market workeffectively (Adams, 1990, pp. 81–83).Herremans, Akathaporn, & Mecinnes (1993)arguethat investors prefer not to deal with companies, which have a bad reputation or do not havea socially responsible attitude towards the environment.

The McFarlane report (Auditing Practices Board (APB), 1992, paragraph 5.24) states that“auditors are already involved in assessing environmental issues when auditing financialstatements”.ICAEW (2000, p. 1) points out that “the importance of environmental issues isincreasingly recognised. They often have implications for business and cannot be ignoredby auditors”.Collison, Gray, and Innes (1996)point out that accountants are becoming moreinvolved in various aspects of the environmental agenda and the notion of auditing is gaininga wider currency on the environmental agenda than as applied to only attestation of financialstatements.Collison and Slomp (2000)suggest that every accountant and auditor shouldbe able to evaluate the consequences of environmental issues in relation to accounting andauditing practices in the financial statements audit. Achieving this will require changes in theeducation and training of accountants, including such areas as the treatment of environmentalcosts and risks in financial statements.ICAEW (2000)points out that environmental matterswill be important for some entities and auditors should have a general awareness of theimpact that such matters may have on financial statements.

Accountants and auditors are now involved in reporting on corporate environmental is-sues, particularly evaluating contingent liabilities, determining the incentive effects of theenvironmental movement on environmental management, and providing decision-makerswith quantitative information on environmental performance (Collison et al., 1996; Elkington& Jennings, 1991; Gray, 1990; Shields & Boer, 1997). Accountants and auditors will in-creasingly find themselves involved in areas such as: dealing with new types of taxes, havingto take new factors into consideration in investment appraisal, helping cost out new pollu-tion control methods, examining the feasibility of replacing materials used with sustainableresources and exploring recycling opportunities, and helping estimate the impact of greenconsumer preference in existing new markets (Gray, 1990, pp. 65–69). A number of argu-ments have addressed the need for widening the scope of the financial auditing professionto encapsulate environmental issues. The question is whether the auditing profession is ableto cope with this new responsibilities for environmental issues and to contribute to meetingthe need for environmental accountability. The central proposal here is that the financial

R. Dixon et al. / Accounting Forum 28 (2004) 119–138 121

audit profession can make a significant contribution to the area of environmental auditing.This proposal leads to asking about the ability of financial auditors to accept environmentalchallenges and participate in environmental auditing.

2. The financial audit profession and the area of environmental auditing

The relationship and overlap between financial and environmental audits has been widelydiscussed (International Federation of Accountants Committee (IFAC), 1995, p. 11). Anumber of studies have addressed the relevance of accountants and financial auditors incarrying out environmental audits (Bebbington, Gray, Thomson, & Walterws, 1994; Black,1998; Canadian Institute of Chartered Accountants (CICA), 1992 and 1997; Collison, 1996;Collison & Gray, 1997; Collison & Slomp, 2000; Collison et al., 1996; Federation desExperts Comptables Europeans (FEE), 1993; Gray & Symon, 1992; Greeno, Hedestrom, &Diberto, 1989; Huizing & Dekker, 1992; ICAEW, 1992, 2000; IFAC, 1995; Power, 1997).ICAEW (1992)addresses the question of the competence of the financial auditor in theenvironmental area. It suggests that the financial auditors should apply scientific expertise,according to their professional qualifications, as would any specialist, in order to achievecredibility in an environmental audit.FEE (1993)points out that the financial auditor hasa long standing tradition of investigating and evaluating systems as well as reporting thefindings.Collison et al. (1996)argue that on the basis of evidence from European countriesthe potential role for financial auditing, related to environmental audits, clearly exists.ICAEW (1992, p. 3) points out that “independent audit can provide important assurance onthe reliability of environmental disclosure.

The work required to give an opinion on published environmental reports will dependon the particular circumstances but will be similar in nature to that performed in auditingfinancial statements and in verifying information contained in.CICA (1992)seeks to deter-mine the relationship between financial and environmental audits and evaluate the expertiseof accountants, which might be relevant.Power (1997)argues that accountants have begunto compete for work in the environmental auditing field, such as the verification and de-velopment of Eco-Management and Audit Scheme (EMAS) and British Standard (BS7750).In doing so they have to establish a competing claim with experts in other fields.Collisonet al. (1996)conducted a survey concerning financial auditors’ responses to environmentalissues. The results indicate that there is a majority desire for guidance from professionalaccountancy bodies related to environmental matters and also a majority view that manyauditors have a potentially useful role to play in attesting environmental reports. Further-more,CICA (1997)points out that accountants and auditors need to expand their knowledgeof environmental issues.The ICAEW Environmental Research Group (1992, 2000, p. 4)noted that the auditor’s responsibilities already extend to consideration of the impact ofenvironmental issues on financial statements in relation to:

• provisions, e.g. for site restoration costs;• contingent liabilities, e.g. arising from pending legal action;• asset values, e.g. where stocks of goods, or the fixed assets used in producing them, are

subject to environmental concern;

122 R. Dixon et al. / Accounting Forum 28 (2004) 119–138

• accounting for capital or revenue expenditure on cleaning up the production process orto meet legal and other standards;

• product redesign costs;• product viability/going concern considerations, e.g. where new regulations impose more

stringent criteria for emissions.

Gray and Symon (1992, p. 11) argue that accountants trained as statutory auditors shouldbe in a position to assess the extent to which environmental information systems providesufficient evidence to come to conclusions about the reliability of reported data.Black(1998, p. 24) states that “the attention of environmental auditors should now shift to theaudit of fully integrated environmental management systems, which are designed to sustainand promote environmental advances while utilising fewer resources than a compliance ap-proach requires”. While,Power (1997, p. 134) argues that the potential role for accountantsto act as environmental verifiers and certifiers has become an increasingly prominent themein the UK and elsewhere. Furthermore,Blokdijk and Drieenhuizen (1992)pointed out thatthe Limperg Institute in the Netherlands published a discussion document, its title is Milieuen Accountant (the Environment and the Audit Profession). It concluded that the financialauditing profession could make an important contribution to the training of environmentalauditors and to the implementation of environmental audits. It also suggested that a speciallytrained environmental auditor rather than a financial auditor should make the verificationof environmental reports. The Limperg Institute’s study group has drawn up a profile ofa member of this new profession. An environmental auditor should be well versed in thedesign of accounting systems and internal controls, including the methods and techniquesused to measure and verify variables (the basic principles of financial auditing). The finan-cial audit profession can make a meaningful contribution to the training of environmentalauditors. The working relationship between the financial and environmental auditor wouldbe similar to that between the auditor and the actuary of an insurance company’s pensionfund. In the UK, Standard Auditing Statement no. 600 (SAS600) Auditors’ reports on finan-cial statements (APB, 1993) uses an alleged breach of an environmental regulation in itsfirst example of a paragraph within the audit report describing a fundamental uncertainty.Standard Auditing Statement no. 160 (SAS160) “Other Information in Documents Con-taining Audited Financial Statements”, requires that in some circumstances, for examplewhen auditing the financial statements of limited companies in the UK, auditors have astatutory responsibility to consider whether the information (financial and non-financial in-formation) given in the directors’ report is consistent with the financial statements in whichit is issued. If they are of the opinion that it is not, they are required to make referenceto the inconsistencies in their report. Also International Standards on Auditing (ISA720)“Other Information in Documents Containing Audited Financial Statements” addresses theissues which auditors should consider in auditing this information (APB, 1999). Collisonand Gray (1997, p. 140) point out that there are two factors related to financial auditor’sawareness and involvement with environmental issues. The first is related to direct guidancefrom the professional accountancy bodies on matters related to the environmental aspectsof the statutory financial audit. The second factor is related to the environmental audit andthe attestation of environmental reports.Power (1997)argues that the financial auditor’spotential role in environmental auditing is normalised by analogy with other areas where

R. Dixon et al. / Accounting Forum 28 (2004) 119–138 123

they have worked with non-accounting specialists. Furthermore,ICAEW (1992, p. 108)states that “it is more likely that a relevant physical scientist or engineer would be the ap-propriate person to provide such verification because of the technical and narrow focus ofsuch disclosure”. The auditors in this situation have a broad field in which to work, whilethey use the specialist to cover technical problems. Also, it indicates that the environmentis no different from any other specialist areas such as property valuation or interpreta-tion of legal agreements. The environment is one area among others, which can be inte-grated into the audit process, which will involve discussion with specialists (ICAEW, 1992,p. 106).

It can be argued that some companies may trust the auditors or certified public accoun-tants (CPAs) more than any other specialists to ask them advice in business situations. Forexample, in the US a recent survey found that small business owners consider certified pub-lic accountants as the primary source of external advice concerning a variety of businesssituations. CPAs were chosen by 44.5% of the respondents as the most trusted external advi-sor far ahead of other, types of business consultants (20%) and attorneys (18%) (Steadman,Green, & Zimmerer, 1995).

There are in fact many different disciplines and many specialists such as, engineers,chemists, lawyers and others who compete with accountants and auditors in performingenvironmental audits.Sittle (1992, p. 21) states that “if accountants fail to grasp this op-portunity (i.e. performing environmental audits) there are many other types of organisationthat will take up the challenge.Maltby (1995, p. 19) points out that accounting firms arenot the only organisation offering an environmental auditing service, for example the con-sultants listed in the UKEnvironmental Data Service (ENDS) Directory (1991)exhibit awide variety of specialists.

An investigation into the attestation of environmental reports (on 26 companies from FEEmember countries) published in Europe has been undertaken by Kamp-Roelands (1995) (asquoted inCollison et al., 1996, p. 14), the results indicated that the majority of audits werecarried out by non-accounting firms, the proportion involving accounting firms is 25% of thetotal. However, this is not static and there are reasons for thinking that the role of financialauditors in environmental audits is increasing in importance, such as:

• The US Environmental Protection Agency (EPA) endorsed the concept of environmentalauditing in its policy statement issued in July 1986. This policy statement emphasises theimportance of auditing to ensure that corporations comply with environmental rules andregulations (Rezaee, Szendi, & Aggarwal, 1995, p. 28).

• Companies have commissioned environmental audit reports. In the UK, Norsk Hydropublished a 28-page environmental report on its operations, within the report was areview carried out by Independent environmental consultants (Lloyd’s Register). CairdGroup has commissioned two environmental audits in 1989 and 1991. A summary ofauditor’s findings on these reports was published (Maltby, 1995, p. 15). Also, BritishAirways provided experimental forms of independent attestation in advance of EMASand BS7750 schemes (Gray, 1993, p. 252).

• The Australian Society of Certified Practising Accountants (ASCPA) has established anEthics Centre of Excellence, from which practitioners are encouraged to obtain adviceand consultation on ethical issues (Leung & Coopers, 1994).

124 R. Dixon et al. / Accounting Forum 28 (2004) 119–138

The previous arguments lead to a question about the type of relationship between financialauditors and environmental specialists, if auditors participate in environmental auditing whatis their responsibility towards environmental disclosure?.

3. Financial auditors and environmental specialists

The education and experience of auditors enable them to be knowledgeable about ac-counting and auditing. Auditing standards recognise that auditors are not expected to haveexpertise in other fields. There are instances in which they consult with specialists in otherareas, e.g., in an audit of a client with possible environmental violations, auditors may utilisethe work of an environmental specialist or consultant (Colbert & Scarbrough, 1993, p. 28).

The auditor’s use of a specialist is the topic of Standard Auditing Statement no. 11(SAS11), “using the work of a specialist” (AICPA, 1989). SAS11 provides guidance to theauditor who utilizes the work of a specialist in performing an audit of financial statementsin accordance with generally accepted auditing standards. SAS11 defines a specialist as“a person (or firm) possessing special skill or knowledge in a particular field other thanaccounting or auditing. For example, appraisers, attorneys, engineers (American Instituteof Certified Public Accountants (AICPA), 1989, p. 157).” It is widely accepted that envi-ronmental auditing requires a multidisciplinary team (FEE, 1993; Hillary, 1993; Huizing& Dekker, 1992; ICAEW, 1992, 2000; Salter, 1992; Sanehi & Waire, 1991). Salter (1992),Hillary (1993), Sanehi and Waire (1991)andHuizing and Dekker (1992)all indicate thatan environmental auditing team should consist of external auditors and other scientists whohave technical and environmental legislative skills. On the other hand,Gray and Symon(1992)argue that there are many different disciplines that could be involved in environmen-tal audits such as, specialist biologists, chemists, engineers, etc. All of these may have littleunderstanding of the economic, financial or management implications of their conclusions.However, in performing an audit of financial statements, auditors may find matters poten-tially material to the fair presentation of financial statements in conformity with generallyaccepted accounting principles that require special knowledge and that in their judgementrequire using the work of a specialist. Furthermore, the auditors and the specialists shouldreach an agreement as to the work to be performed. The agreement, preferably in writing,should include the objectives and the scope of the consultant’s work, the methods and as-sumptions to be used, the planned form and content of the consultant’s report, and the useof the report (AICPA, 1989, p. 158;Colbert & Scarbrough, 1993, p. 29).

However, the specialist’s work may impact on the auditors’ report as SAS11 points out,“if auditors determine that the specialist’s findings support the related representations inthe financial statements, they may reasonably conclude that sufficient competent evidentialmatter has been obtained. If, there is a material difference between the specialist’s findingsand the representations in the financial statements, or if auditors believe that the determi-nations made by the specialist are unreasonable, they should apply additional procedures.If after applying any additional procedures that might be appropriate, they are unable toresolve the matter, auditors should obtain the opinion of another specialist, unless it ap-pears to the auditors that the matter cannot be resolved. A matter that has not been resolvedwill ordinarily cause them to conclude that they should qualify their opinion or disclaim

R. Dixon et al. / Accounting Forum 28 (2004) 119–138 125

an opinion because the inability to obtain sufficient competent evidential matter as to anassertion of material significance in the financial statements constitutes a scope limitation”(AICPA, 1989, p. 159).

A number of studies address the use of specialists in the teams used for environmentalauditing (Buckley, 1991; Salter, 1992; Sanehi & Waire, 1991). While, Patrick (1990)dis-cusses the use of environmental consultants in the audit team for investigating the physicalconditions and regulatory issues involved.

Dezalay (1995)addresses the role of a lawyer in environmental audit team. It can beargued that, during the auditor’s work, if environmental issues arise, there will be manyquestions which the auditor needs to have answered to assess the materiality of contingentliabilities. A specialist can aid the auditor in some matters such as, identifying applicablelaws, determining possible environmental violations, measuring the physical conditions andrectifying the situation. Many users of environmental information may be less interested inthe level of polluted emissions, but are more interested in the implications of these emissionson a company’s financial statements in the situation where this company is fined or penalisedby governmental agencies because of its environmental violations.

4. The auditors’ responsibility towards environmental disclosures

It is widely accepted that financial auditors can participate in environmental audits withother specialists or in multidisciplinary teams (Collison & Gray, 1997; FEE, 1993; Gray &Symon, 1992; Hillary, 1993; Huizing & Dekker, 1992; Hunt, 1993; ICAEW, 1992, 2000;IFAC, 1995; Maltby, 1995; Sanehi & Waire, 1991). IFAC (1995)andAICPA (1989)discussthe auditor’s responsibility for using the work of an expert. The application of InternationalAuditing Atandards involves the auditor assuming responsibility for the quality of the workperformed by the expert. SAS57 points out that management is responsible for accountingestimates included in the financial statement. The auditor is responsible for evaluating thereasonableness of these accounting estimates.IFAC (1995, p. 41) states that “management isresponsible for ensuring that the entity complies with the environmental regulatory require-ments and its own environmental policies, and for establishing and maintaining an effectiveenvironmental management system”.ICAEW (2000, p. 2) points out that where manage-ment engages an expert to provide technical advice to assist in developing estimates anddisclosures in the financial statements relating to environmental matters, the auditor shouldconsider the adequacy of such work, as well as the expert’s competence and objectivity.

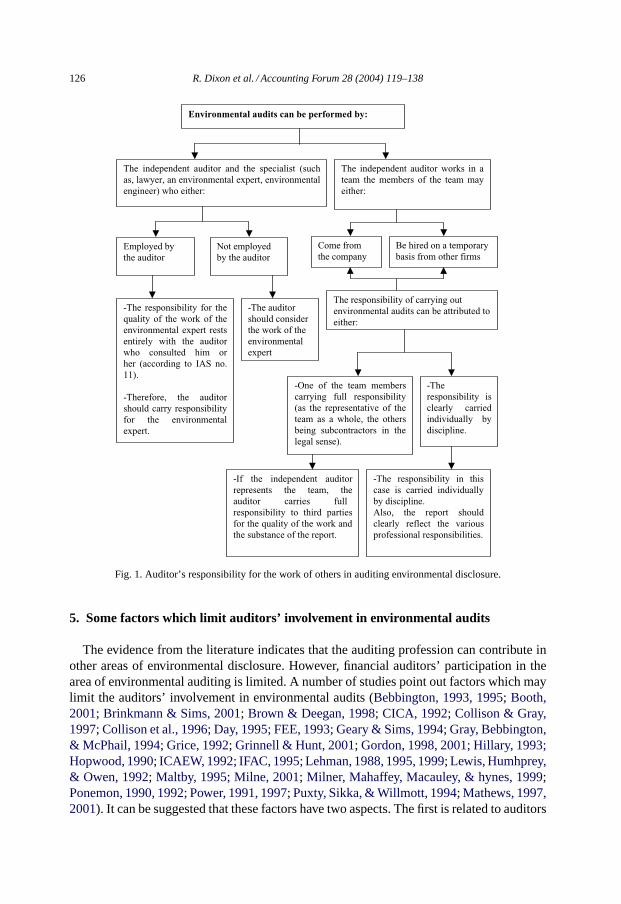

AICPA (1989), International Federation of Accountants (IFA) (1995) andInternationalAuditing Practice Committee (IAPC) (1995, pp. 38–44 and 2000) discuss how environ-mental audits should be performed in an attempt to specify auditors’ responsibility towardsenvironmental disclosure. This discussion is presented in the followingFig. 1.

Moreover,AICPA (1989)andAuditing Practice Committee (APC) (1991)address theimpacts of illegal acts on the auditors’ report. In accordance with generally accepted auditingprinciples (GAAP) an auditor should express an opinion when auditing financial statements.This opinion may be qualified, unqualified, adverse or disclaimer in nature (Kell, Boynton, &Ziegler, 1986). The auditor’s opinion when auditing financial statements and environmentalmatters can be summarised and is shown in the followingTable 1.

126 R. Dixon et al. / Accounting Forum 28 (2004) 119–138

Environmental audits can be performed by:

The independent auditor and the specialist (such

as, lawyer, an environmental expert, environmental

engineer) who either:

The independent auditor works in a

team the members of the team may

either:

Employed by

the auditor

Not employed

by the auditor

Come from

the company

Be hired on a temporary

basis from other firms

-The responsibility for the

quality of the work of the

environmental expert rests

entirely with the auditor

who consulted him or

her (according to IAS no.

11).

-Therefore, the auditor

should carry responsibility

for the environmental

expert.

-The auditor

should consider

the work of the

environmental

expert

The responsibility of carrying out

environmental audits can be attributed to

either:

-One of the team members

carrying full responsibility

(as the representative of the

team as a whole, the others

being subcontractors in the

legal sense).

-The

responsibility is

clearly carried

individually by

discipline.

-The responsibility in this

case is carried individually

by discipline.

Also, the report should

clearly reflect the various

professional responsibilities.

-If the independent auditor

represents the team, the

auditor carries full

responsibility to third parties

for the quality of the work and

the substance of the report.

Fig. 1. Auditor’s responsibility for the work of others in auditing environmental disclosure.

5. Some factors which limit auditors’ involvement in environmental audits

The evidence from the literature indicates that the auditing profession can contribute inother areas of environmental disclosure. However, financial auditors’ participation in thearea of environmental auditing is limited. A number of studies point out factors which maylimit the auditors’ involvement in environmental audits (Bebbington, 1993, 1995; Booth,2001; Brinkmann & Sims, 2001; Brown & Deegan, 1998; CICA, 1992; Collison & Gray,1997; Collison et al., 1996; Day, 1995; FEE, 1993; Geary & Sims, 1994; Gray, Bebbington,& McPhail, 1994; Grice, 1992; Grinnell & Hunt, 2001; Gordon, 1998, 2001; Hillary, 1993;Hopwood, 1990; ICAEW, 1992; IFAC, 1995; Lehman, 1988, 1995, 1999; Lewis, Humhprey,& Owen, 1992; Maltby, 1995; Milne, 2001; Milner, Mahaffey, Macauley, & hynes, 1999;Ponemon, 1990, 1992; Power, 1991, 1997; Puxty, Sikka, & Willmott, 1994; Mathews, 1997,2001). It can be suggested that these factors have two aspects. The first is related to auditors

R. Dixon et al. / Accounting Forum 28 (2004) 119–138 127

Table 1Auditor’s opinion concerning environmental issues in the audit of financial statements

Unqualified opinion If the auditor thinks that the financial statements presented fairly. The statements arenot affected by a major uncertainty (such as, environmental liabilities, law suits)In other words there are no impacts from environmental issues on financial statementsor the company’s continuity

Qualified opinion If the auditor concludes that environmental issues have a material effect on thefinancial statements and the company has not properly accounted for or disclosed thisIf the auditor is unable to obtain sufficient evidence concerning items in the statementsIf financial statements contain a material departure from GAAP

Adverse opinion If the auditor concludes that environmental issues have a material effect on thefinancial statements and the company has not properly accounted for or disclosed thisIf financial statements are not presented fairly in conformity with GAAP and aqualified opinion is not appropriate

Disclaimer opinion If the auditor is precluded by the company from obtaining sufficient competentevidential matter to evaluate whether environmental issues could be material to thefinancial statementsIf there are significant uncertainties (such as, contingent environmental liabilities)affecting the financial statements as a whole and qualified opinion is therefore notappropriate

and the auditing profession. The second is related to lack of the demand for environmentalreporting from companies.

The first aspect is developed as follows.

5.1. Accounting education

Education is the key to changing long-establis patterns of social behaviour. It can helpcombat the unsustainable production and consumption patterns that are responsible forenvironmental degradation, loss of biodiversity, population growth beyond the capacity ofsystems, and unplanned urbanisation (Atchia & Tropps, 1995).

Lehman (1988, p. 77) points out that the contemporary notions of accounting educationrest on a commitment to training in a technical sense, teche from the Greek, or technique:skilful production expert mastery of objectified tasks.

It can be argued that the role of accounting education in qualifying business studentsand the impact of accounting education on the profession has recently attracted many re-searchers attention (Albrecht & Sack, 2000; Bebbington, 1995; Booth, 2001; Gray et al.,1994; Grinnell & Hunt, 2001; Hopwood, 1990; Lehman, 1988; Leung & Coopers, 1994;Lewis et al., 1992; Lockhart & Mathews, 2000; Mathews, 1997; Ponemon, 1990, 1992;Power, 1991, 1997). Puxty et al. (1994, p. 85) observe that practising accountants are them-selves a product of the socialisation that arises from the educational and training process.Leung and Coopers (1994)discuss that business schools aim to produce academically quali-fied graduates. They educate their students in the theory and practice of financial accounting,marketing, finance, taxation and many other areas. However, it is not often, that businessschools look beyond these immediate concerns. It can be argued that other matters may bemore important for the curriculum in business schools.

128 R. Dixon et al. / Accounting Forum 28 (2004) 119–138

Lehman (1988)argues that business educators are responsible for teaching students tobe conscious of the sides they are choosing and to be critical thinkers in decisions havingethical consequences.Mathews (1997)argues that the teaching or educational aspect hasnot reached a satisfactory level of activity and is needed if the next generation of academicaccountants are to carry on the work, and if the professional arm is to be reformed. Asatisfactory educational programme would be one where accounting theory and alternativeforms of accounting received a level of emphasis equivalent to that given to conventionalcorporate accounting.Gray and Bebbington (1994)argue that the existence of a univer-sity education dominated by technique acquisition, generates neither practically trainedindividuals who can be immediately useful in the office nor educationally developed indi-viduals with a sophisticated capacity to enquire, reason, conceptualise and evaluate. Otherauthors (Hopwood, 1990; Laughlin, Lowe, & Puxty, 1986; Puxty, 1991) discuss the samearguments, and conclude neither the training nor the education of accounting students issatisfactory. This failure, at least of the educational component of university accountingteaching, has been widely remarked upon.McPhail and Gray (1996)argue that studentsdisplay different levels of ethical awareness in fields outside accounting and they suggestthat something unusual is occurring in accounting education, which may connect studentsof ethical awareness only the sphere of accountancy. The authors suggest that the way inwhich accounting is conceived, constructed and taught make it inevitable that accountingstudents will experience intellectual and moral atrophy.

Geary and Sims (1994, p. 9) argue that the weakness of accounting pedagogy is illustratedby such issues as ethical problems which often do not have specific correct solutions likethose problems on the Certified of Public Accountant (CPA) examination. An emphasison factual rules important to success in professional examinations can create a classroomexpectation that is especially un-welcoming to the unstructured and ill-defined ethical prob-lems that students will actually face. TheAmerican Accounting Association (AAA) FutureCommittee (1986, p. 177) made the following observation:

“Fifty years ago, the method of lecture together with routine-problem-solving was gen-erally used. Today, that same method tends to dominate accounting teaching methods,although class discussion in the form of teacher-question and student-answer is given moreemphasis. The current pedagogy also emphasises problems with specific solutions. As thenumber of authoritative pronouncements has expanded, textbooks and faculty have requiredstudents to learn more factual rules and procedures to be applied in rather rigid fashion.A primary focus in many cases has been on the acquisition of knowledge needed to passprofessional examinations”.

On the other hand,Geary and Sims (1994, p. 16) suggest that if accounting facultyreach consensus on the goals of ethics education, make wise pedagogical choices em-phasising active rather than passive learning strategies, incorporate a well-structured andwell-implemented debriefing phase, and provide for feedback through an effective assess-ment process, ethics education will mature as an integral and vital component of an account-ing curriculum. Attempts have been recently made to argue the case for a limited social andenvironmental accounting education programme as a part of other conventional accountingcourses (Booth, 2001; Gordon, 1998, 2001; Lockhart & Mathews, 2000; Mathews, 2001;Milne, 2001). These studies point out that the need for widening and developing accountingeducation to encapsulate environmental issues.

R. Dixon et al. / Accounting Forum 28 (2004) 119–138 129

5.2. The ethical and social aspects in accounting education

The integrity of ethical and social aspects in accounting education is very important to thequalification of accountants and auditors who should be able to deal with new professionalchallenges, such as environmental matters. The importance of an ethical component in busi-ness and accounting education has been addressed in many studies (Adams, Tashchian, &Shore, 1999; Bebbington, 1993; Brinkmann & Sims, 2001; CICA, 1992; ICAEW, 1992;Lehman, 1988, 1995, 1999; Lewis et al., 1992; Loeb, 1988, 1991; Ponemon, 1990, 1992;Puxty et al., 1994; Welton, Lagrone, & Davis, 1994). The goals of ethics education in ac-counting are to develop a sense of moral obligation or responsibility, to develop the abilitiesneeded to deal with ethical conflicts, and to learn how to deal with the uncertainties of theaccounting profession (Loeb, 1988, p. 322).CICA (1992)points out that ethical character-istics similar to those of financial auditors would be needed in the environmental field.

Gray et al. (1994)argue that accounting education fails to develop students’ intellectualand related ethical maturity. The authors suggest that there are many possible solutionsto this problem. One possible solution may lie with social and environmental accounting,which challenges much of the traditional approach to accounting education in universi-ties, offers a vehicle within which many of the implicit assumptions of accounting andaccounting education can be explored and provides a potential opportunity to enhance theethical and intellectual development of accounting students. Moreover, in the US, the reportof National Commission on Fraudulent Financial Reporting, the“Treadway Commission”(1987)recommends that business and accounting curricula should emphasise ethical val-ues, that professional certification examinations should test students on ethical values, andthat continuing professional education and continuing management education should focuson ethical values. Also, theAAA (1986) argues that students in business schools should beexposed to the ethical dimensions of their business studies. Although many studies advo-cate teaching ethical applications in accounting, this subject is still not receiving adequateattention in accounting education (Loeb, 1991). Furthermore,Lewis et al. (1992, p. 221)observe that there is a reluctance to explore the ethical dimension of the current economicand political structures underpinning accounting practice. An important task of a businessschool is to sensitise its students to the ethical issues they will have to cope with during theirprofessional lives (Leung & Coopers, 1994). Therefore, accounting courses must considertraditional business and society issues as well as the resolution of moral dilemmas (Geary &Sims, 1994, p. 5). A significant number of business schools do not systematically integrateor incorporate ethics issues into business disciplines (Milton-Smith, 1991). Also,Mathews(1987, p. 12) states that “the use of social in conjunction with accounting does not seemto work as well as the addition of financial, management or tax, these words add a largemeasure of explanation and precision to accounting, which social does not, perhaps onedifficulty is the range of total activity included under social accounting”.Puxty et al. (1994,p. 79) argue that professional accountants are induced to act ethically through two aspectsof their socialisation: the educational process preparing them for qualifying examinationsand the influence of work experience and role models who show what it means to be ethical.It can be argued that there is a crucial need to encapsulate ethical and social dimensionsin accounting education to raise the abilities of financial auditors to be able to cope withenvironmental issues and the uncertainties of the auditing profession.

130 R. Dixon et al. / Accounting Forum 28 (2004) 119–138

5.3. Research in accounting and auditing profession

The ability of research to support the development of practice has attracted a varietyof studies (Bebbington et al., 1994; Day, 1995; Kaplan, 1984; Lee, 1989; Lehman, 1988;Lewis et al., 1992; Power, 1991, 1997; Sterling, 1973). Academics do not offer solutions forproblems, which face practitioners in their work (Bebbington, 1997; Gray, 1996). While,Sterling (1973, pp. 44–52) argues that research is isolated from education and practice.Education and practice are complementary in that educators teach accepted practices andpractitioners practice what they are taught. It difficult to assert that there is congruencebetween research and actual education and professional practice. A state of affairs thatis usually viewed as being detrimental to both research and practice (Lee, 1989, p. 415).Kaplan (1984)suspects that researchers will not learn about the production and organisationproblems of contemporary industrial corporations by reading economics and managementscience journals. Researchers will need to leave their offices and study the practices ofinnovating organisations.

Day (1995, p. 104) argues that the possibilities of changing accounting practices dependjust as much on transforming current generations of accounting student’s understandings,as on transforming current practitioners, and their understanding.Lee (1989, p. 237) ex-amined the relationship between accounting’s research, practice and education functions.In summary much of the material in the area has led a number of commentators to expressconcern that research appears to exist in increasing isolation from education and practice. Itcan be argued that there is a need to link research with teaching or education, and teachingwith practice, through the development of the curriculum.Bebbington (1995)has provideda review of the lack of connection between curricula and the services, which accountantsprovide. Research is needed to investigate the extent to which, curricula are determinedby the profession, the academic institution, individuals teaching the programme or variouscombinations of these groups. It can be argued that research should play an effective rolein solving problems, which face practitioners. Financial auditor’s knowledge about envi-ronmental matters can be increased by research, which should be integrated with educationand practice.

5.4. The experience, skills and training of financial auditors

The financial auditors can play a role in environmental auditing but they possess onlyone element of the required knowledge, skills and experience needed to carry out envi-ronmental audits (FEE, 1993, p. 13).Hillary (1993, p. 36) states that “defining auditors’skills is difficult because there are no recognised standards. While,Huizing and Dekker(1992, p. 444) argue that if there really is to be a new environmental audit “Profession”,its personnel and skills are as yet indeterminate and vague.Lehman (1988, p. 77) pointsout that accounting students are trained in how to do (how to apply a present formulaor model) but the underlying implications of why are either unarticulated or not scru-tinised.Burchell, Clubb, Hopwood, and Naphapiet (1980)point out that formalised ac-counting knowledge can be seen as a condition for the possibility of the professionalisa-tion of accounting and that professionalisation in turn changes the conditions underlyingthe elaboration and development of accounting knowledge. The claim to expertise plays

R. Dixon et al. / Accounting Forum 28 (2004) 119–138 131

a central but complex role in sustaining professional communities. The complexity re-lates both to and between the external legitimising function of such claims and the inter-nal specification of the content of expert knowledge itself (Power, 1991, p. 336).Grice(1992) argues that students in the accounting profession should be trained not only inareas such as communications and ethics but also in a broad range of human relation-ship skills. There is a requirement for auditors to have adequate environmental experi-ence as well as auditing experience (Mathews & Reynolds, 2001). Auditors need manyskills to effectively conduct successfully an environmental audit. For example,Neebes,Guy, and Whittington (1991)argue that the auditors’ ability to evaluate the contingenteffect of an illegal act (environmental violation) on the financial statements are limited.They generally do not have the legal training or experience. Also, auditors need manytechniques to effectively and efficiently gather and analyse information while maintain-ing the necessary level of objectivity (Greeno et al., 1989). Langford (1995)points outthat every accountant and auditor should be able to evaluate the consequences of environ-mental issues in relation to accounting and auditing practices in the financial statementaudit. This will require changes to the education and training of accountants. It can beargued that educational systems consider one of the essential processes by which expertiseis transmitted, developed and regulated. The financial auditors need to learn more aboutthe impact of environmental matters on business and the implications of these matters onfinancial statements. Auditors also need new experience, training and the opportunity to de-velop skills to deal with environmental challenges. Auditors’ skills concerning some issuesneed to be improved, these issues such as; the use and analysis of environmental informa-tion, the evaluation and estimation of uncertainty and those which relate to environmentalissues.

5.5. Professional guidance for environmental matters

The accounting professional bodies do not provide adequate and specific guidance forthe determination, estimation, measurement and disclosure of environmental issues.Ilintch,Soderstrom, and Thomas (1998)point out that the accounting profession has been slow totake on the role of measuring and controlling environmental matters.Welton et al. (1994)argue that the accounting profession needs to develop the ability to consider ethical issues.Bebbington et al. (1994)concludes accountants and auditors will make little progress un-til there are rules.Brown and Deegan (1998)point out that the professional accountingbodies in various countries should dedicate both effort and financial resources towards thedevelopment of environmental disclosure guidelines. Many empirical studies (Collison,1996; Collison & Gray, 1997; Collison & Slomp, 2000; Collison et al., 1996; Huizing& Dekker, 1992; Maltby, 1995; Pong & Whittington, 1994; Rezaee et al., 1995) providestrong evidence that the absence of professional guidance limits auditors’ involvement inenvironmental audits.

5.6. Auditors’ views towards performing environmental audits

Empirical studies of financial auditors’ views on environmental matters have producedmixed evidence (CICA, 1994; Collison, 1996; Collison & Gray, 1997; Collison et al., 1996;

132 R. Dixon et al. / Accounting Forum 28 (2004) 119–138

Coopers & Lybrand, 1990; FEE, 1993; Maltby, 1995; The Limperg Institute, 1992). Theevidence suggests some auditors perceive a risk of litigation because of legal responsibilitiesin the area of environmental disclosure.

Huizing and Dekker (1992)surveyed Dutch practitioners’ views concerning their in-volvement in environmental audits. A proportion felt that they lacked the necessary techni-cal, ecological, administrative, and organisational expertise. Whilst others believed thatthey could make judgements about the integrity of systems, which generate green re-ports.

Companies that wish to engage in environmental disclosure may face a lack of reliable andcredible methodologies to measure, monitor and communicate environmental information.There is no general acceptance of the format of environmental reports and their contents,how verification should be carried out, what should be included in a verification statementor opinion, and who should carry out verification. Companies may therefore face a numberof obstacles in engaging in environmental disclosure because of the perceived lack ofrequirements or frameworks for environmental reports, which can consequently impact onthe level of demand for environmental auditing (CC, 1999; CICA, 1994; FEE, 2000; GRI,2000; IAPC, 1995; ICAEW, 2000; IFAC, 1995; KPMG, 1996, 1997, 1999; Langford, 1995;Lloyd, 2001; Maltby, 1995). Some of the complications in this area can be summarised asfollows:

• Environmental data and information. The existing information systems in companiesmay not address environmental issues and have inadequate resources (technical, fi-nancial, or qualified resources) in order to produce environmental informa-tion.

• Environmental indicators. They are essential for credibility in environmental reporting.There are barriers to development of environmental indicators, such as, how to choosesuitable scientific and technical methods to calculate the indicators, and what is the ap-propriate benchmark for environmental performance.

• The contents of environmental reporting. There is no generally accepted framework forthe contents of environmental reports. Unlike financial reporting, environmental report-ing has not been guided by a set of widely accepted standards and principles that can beused in reporting environmental information.

• Independent verification. Although there is no consensus on what should be included ina verification statement or opinion, there is a wide acceptance concerning the importanceof the verification of environmental reports by a third party.

• Limited public demand for environmental reports. The level of the public demand forenvironmental information is limited because environmental awareness is still develop-ing.

• Voluntary reporting. Because environmental reports are voluntary, a number of com-panies may prefer not to engage in environmental disclosure. Developing environmen-tal reports may eventually require legal requirements to make reports manda-tory.

In order to pull the analysis within the review of literature together within the literature,a general framework of the necessary characteristics of environmental auditors has beensuggested as inFig. 2.

R. Dixon et al. / Accounting Forum 28 (2004) 119–138 133

A general framework of the necessary characteristics of environmental auditors

Guidance Practice Training Skills Research Ethical and SocialAspects

Education

Professional

guidance is

required to

address

environmental

issues, such

as:-

Should

depend

on:

-Practical

examples

Auditors need

different skills

to perform

environmental

audits such as:-

The profession

should be:

- Integrated with

education and

practice

Should

develop in

auditors

potential

to:-

There is a

need to make

changes in

accounting

education in

universities

Should

create:

-New

ways to

think

and act

by the

auditor

Audit and

review of

financial

statements

involving

environmental

matters

-New skills

and

technical

approaches

-New

techniques

and skills

Analytical

skills

-Analyzes and

measures the

environmental

implications on

business

-Ability to

deal with

moral

situations

Education

should focus

on teaching

ethical and

social aspects

Estimate

environmental

costs and

liabilities

-Case

study

approaches

Technical

skills

-Suggests

solutions to

environmental

problems

-Develop

awareness of

environmental

issues

Develop

new skills

and

techniques

Environmental

disclosures

Environmental

reporting

-Develop,

act and

think

Decision

making

skills-Ability to

deal with

uncertainties Teaching real

problems,

which face

auditors in

practice

Standards for

independent

verification

Teaching

environmental

sciences

Raising auditors’ ability:-

-to think logically

-to collect, use and analyze

environmental information

-to estimate and evaluate

environmental liabilities

-to deal with uncertainties in

the area of environmental

issues

-to make decisions

-to communicate effectively

Financial auditors

Some auditors prefer not to engage in environmental audits, because of:

Some auditors are enthusiastic to perform environmental audits

Legal responsibility An increase in the cost

of the audit process

May think they are not qualified

to perform environmental audits

-Auditors

should

co-operate

with

academics

to solve

professional

problems

-Addresses

the real

problems

which face

practitioners

Fig. 2. A general framework of the necessary characteristics of environmental auditors.

134 R. Dixon et al. / Accounting Forum 28 (2004) 119–138

6. Conclusions

It can be argued that environmental issues are having a variety of impacts on business. Thespeed with which these changes have occurred has made it difficult for auditors to keep upto date. Environmental issues can still be considered a relatively new challenge for auditors,whether environmental responsibilities are voluntary or through regulation. A number ofarguments have emerged concerning the relevance of the auditing profession in playing aneffective role in environmental issues. Some of these arguments advocate that auditors canparticipate in environmental audits with other specialists, such as environmental specialists,engineers and lawyers. However, the auditors’ participation in environmental auditing isstill limited. There are a number of obstacles, which impact on this contribution. Theseobstacles can be summarised inFig. 3.

There is a crucial need to make a number of changes in accounting education to qualifyauditors to deal with environmental matters. Ethical and social dimensions need to beencapsulated in accounting education to raise the abilities of financial auditors to cope withenvironmental issues and the uncertainties of the auditing profession. Auditors need a wide

Obstacles, which limit auditors’ participation in environmental

auditing

Factors related to auditors and the

auditing profession

Accounting education

Ethical and social aspects

in accounting education

Research in accounting

and auditing profession

The experience, skills and

training of the financial

auditor

Professional guidance on

environmental matters

Auditors’ view towards

involving in environmental

auditing

Factors related to the companies’ lack

of demand for environmental

reporting

Environmental data and

information

Environmental indicators

The contents of

environmental reporting

The need for independent

verification

Professional standards and

principles of

environmental reports

Limited public demand for

environmental reports

The current voluntary

nature of the demand for

environmental reporting

Fig. 3. Obstacles, which limit auditors’ participation in environmental auditing.

R. Dixon et al. / Accounting Forum 28 (2004) 119–138 135

variety of skills to cope with environmental matters, e.g., analytical, technical and decisionmaking skills. There is a need for professional guidance, which should address items suchas environmental costs and liabilities, environmental disclosures, environmental reportingand standards for independent verification. Without this guidance auditors may not be ableto cope with the demands of environmental auditing. Companies’ perception of the lack ofthe demand for environmental reports makes them prefer to avoid environmental disclosure,which in turn reduces the demand for environmental auditing.

In summary, this paper argues that the contribution of the auditing profession remainslimited due to the lack of important characteristics of its membership and its failure to tacklethe issues by the development of principles and guidelines.

References

Adams, R. (1990). The greening of consumerism.Accountancy, (June), 81–83.Adams, J., Tashchian, A., & Shore, T. H. (1999). Frequency, recall, and usefulness of undergraduate ethics

education.Teaching Business Ethics, 3(3), 241–253.Albrecht, W., & Sack, R. (2000).Accounting education: Charting the course through a perilous future. Sarasota,

FL: American Accounting Association.American Accounting Association (AAA) (1986). Committee on the Future Structure, Content, and Scope of

Accounting Education (The Bedford Committee).Future accounting education: Preparing for the expandingprofession(pp. 68–95). Issues in Accounting Education, Spring.

American Institute of Certified Public Accountants, (AICPA) (1989).Codification of statements on auditingstandards numbers 1 to 60. New York: Commerce Clearing House Inc.

Atchia, M., & Tropps, S. (1995).Environmental management issues and solutions. London: John Wiley and SonsLtd.

Auditing Practices Board (APB) (1992).The future development of auditing: A paper to promote public debate(The McFarlane Report). London: APB.

Auditing Practices Board (APB) (1993).SAS600 auditors’ report on financial statements. London: APB.Auditing Practices Board (APB) (1999).SAS160, other information in documents containing audited financial

statements. London: APB.Auditing Practices Committee (APC) (1991).Auditing guideline the auditor’s responsibility in relation to illegal

acts, exposure draft. London: Auditing Practice Committee of CCAB Limited.Bebbington, J. (1993). The European community fifth action plan: towards sustainability.Social and Environmental

Accounting, 13(1), 9–11.Bebbington, J. (1995). Teaching social and environmental accounting: A review essay.Accounting Forum, 19(2–3),

263–273.Bebbington, J. (1997). Engagement, education and sustainability: A review essay on environmental accounting.

Accounting, Auditing and Accountability Journal, 10(3), 365–381.Bebbington, J., Gray, R., Thomson, I., & Walterws, D. (1994). Accountants’ attitudes and environmentally-sensitive

accounting.Accounting and Business Research, 24, 109–120.Black, R. (1998). A new leaf in environmental auditing.The Environmental Auditor, 55(3), 24–27.Blokdijk, J., & Drieenhuizen, F. (1992). The Environment and the audit profession.European Accounting Review,

437–443.Booth, P. (2001). Commentary on: Some thoughts on social and environmental accounting education.Accounting

Education, 10(4), 357–359.Brinkmann, J., & Sims, R. R. (2001). Stakeholder-sensitive business ethics teaching.Teaching Business Ethics,

5(2), 171–193.Brown, N., & Deegan, C. (1998). The public disclosure of environmental performance information—A dual test

of media agenda setting theory and legitimacy theory.Accounting and Business Research, 29(1), 21–41.

136 R. Dixon et al. / Accounting Forum 28 (2004) 119–138

Buckley, R. (1991). Environmental audit and legal professional privilege.Environmental and Planning LawJournal, 8(4), 335–345.

Burchell, S., Clubb, C., Hopwood, A., & Naphapiet (1980). The role of accounting in organisations and society.Accounting, Organisations and Society, 5–27.

Canadian Institute of Chartered Accountants (CICA) (1992).Environmental auditing and the role of the accountingprofession. Toronto: CICA.

Canadian Institute of Chartered Accountants (CICA) (1994a).Environmental stewardship managementaccountability and the role of chartered accountants. Toronto: CICA.

Canadian Institute of Chartered Accountants (CICA) (1994b).Reporting on environmental performance. Toronto:CICA.

Canadian Institute of Chartered Accountants (CICA) (1997).Full cost accounting from an environmentalperspective. Toronto: CICA.

Colbert, J., & Scarbrough, C. (1993). Environmental issues in a financial audit which professional standards apply.Managerial Auditing Journal, 8(5), 26–32.

Collison, D. (1996). The response of statutory financial auditors in the UK to environmental issues: A descriptiveand exploratory case study.British Accounting Review, 28(4), 325–349.

Collison, D., & Gray, R. (1997). Auditor’s responses to emerging issues: A UK perspective on the statutoryfinancial auditor and the environment.International Journal of Auditing, 1(2), 135–149.

Collison, D., & Slomp, S. (2000). Environmental Accounting, auditing and reporting in Europe: The role of FEE.The European Accounting Review, 9(1), 111–129.

Collison, D., Gray, R., & Innes, J. (1996). The financial auditor and the environment. London: The Institute ofChartered Accountants in England & Wales.

Coopers, & Lybrand Deloitte (1990). Positive audit for the environment. London: Coopers and Lybrand Deloitte.Copenhagen Charter (CC) (1999).http://www.stakeholder.dk.Day, M. (1995). Ethics of teaching critical: feminism on the wings of desire.Accounting, Auditing and

Accountability Journal, 8(3), 97–112.Dezalay, Y. (1995). Turf battles or class struggles: the internationalisation of the market for expertise in the

professional society.Accounting, Organisations and Society, 20, 331–344.Elkington, J., & Jennings, V. (1991). The rise of the environmental audit.Integrated Environmental Management,

8–12.Environmental Data Services (ENDS) (1991).Directory of environmental consultants. London: ENDS.Federation des Experts Comptables Europeens (FEE) (1993).Environmental accounting and auditing: A survey

of current activities and developments. Brussels: FEE.Fédération des Experts Comptables Européens (FEE), (2000).Towards a generally accepted framework for

environmental reporting. Paper Issued by the Environmental Working Party of the European Federation ofAccountants, Brussels, (FEE), July.

Geary, W., & Sims, R. (1994). Can ethics be learned?Accounting Education—An International Journal, 3(1),3–18.

Global Reporting Initiatives (GRI) (2000).Sustainability reporting guidelines(pp. 22–36). http://www.globalreporting.org, 2001.

Gordon, I. (1998). Enhancing students’ knowledge of social responsibility accounting.Issues in AccountingEducation, 13(1), 31–46.

Gordon, I. (2001). Commentary on: Some thoughts on social and environmental accounting education.AccountingEducation, 10(4), 361–364.

Gray, R. (1990). The accountant’s task as a friend to the earth.Accountancy, (June), 65–69.Gray, R. (1993).Accounting for the environment. London: Paul Chapman Ltd.Gray, R. (1996). The interesting relationship between accounting research and accounting practice: A personal

reply to Professor Whittington.Journal of Applied Accounting Research, 3(1), 5–34.Gray, R., & Bebbington, J. (1994).Sustainable development of accounting: Incentives and disincentives for the

adoption of sustainability by transnational corporations. Dundee Discussion Papers in Accountancy andBusiness Finance, Acc/9414, University of Dundee.

Gray, R., Bebbington, J., & McPhail, K. (1994). Teaching ethics in accounting and the ethics of accountingteaching: Education for immorality and a possible case for social and environmental accounting education.Accounting Education—An International Journal, 3(1), 51–75.

R. Dixon et al. / Accounting Forum 28 (2004) 119–138 137

Gray, R., & Symon, I. (1992). An environmental audit by any other name.Integrated Environmental Management,6, 9–11.

Greeno, J., Hedestrom, G., & Diberto, M., (1989). The environmental health and safety auditor’s handbook.London: Arthur D. Little Inc.

Grice, B. (1992). Pushing a degree of ethics and history.Business Review Weekly(13 November, Australia).Grinnell, D. J., & Hunt, H. G. (2001). Commentary on: Some thoughts on social and environmental accounting

education.Accounting Education, 10(4), 365–368.Herremans, I., Akathaporn, P., & Mecinnes, M. (1993). An investigation of corporate social responsibility

reputation and economic performance.Accounting, Organisations and Society, 18(7–8), 587–604.Hillary, R. (1993). The eco-management and audit scheme: a practical guide. Letchworth, UK: Technical

Communications Publishing Ltd.Hopwood, A. (1990). Ambiguity, knowledge and territorial claims: Some observations on the doctrine of substance

over form. A review essay.British Accounting Review, 22(1), 79–88.Huizing, A., & Dekker, H. (1992). The environmental issue on the Dutch political market.Accounting,

Organisations and Society, 17, 427–448.Hunt, D. (1993). Expertise of environmental auditors—The EARA scheme. East Kirly Linces UK: Environmental

Auditors Registration Association.Ilintch, A., Soderstrom, N., & Thomas, T. (1998). Measuring corporate environmental performance.Journal of

Accounting and Public Policy, 17, 383–408.Institute of Chartered Accountants in England and Wales (ICAEW) (1992).Business accountancy and the

environment: A policy and research agenda. London: ICAEW.Institute of Chartered Accountants in England and Wales (ICAEW) (2000).Environmental issues in the audit of

financial statements. London: ICAEW.International Auditing Practices Committee (IAPC) (1995).The audit profession and the environment. Discussion

Paper Issued by the International Federation of Accountants. New York: IFA.International Auditing Practices Committee (IAPC) (1995).The audit profession and the environment. Discussion

Paper Issued by the International Federation of Accountants. New York: IFAC.International Federation of Accountants Committee (IFAC) (1995).Discussion paper: The audit profession and

the environment. New York: IFAC.Kaplan, R. S. (1984). The evaluation of management accounting.The Accounting Review, LIX(3), 405–417.Kell, W., Boynton, W., & Ziegler, R. (1986).Modern auditing(third ed.). Chichester, England: John Wiley & Sons

Inc.KPMG (1996).International survey of environmental reporting. London: KPMG.KPMG (1997).UK Survey of Environmental Reporting. London: KPMG.KPMG (1999).International survey of environmental reporting.http://www.wimm.nl/publications/kpmg1999.pdf.Langford, R. (1995). Accountants and the environment.Accountancy, (June), 128–129.Laughlin, R., Lowe, A., & Puxty, A. (1986). Designing and operating a course in accounting methodology:

Philosophy, experience and some preliminary empirical tests.The British Accounting Review, 18(1), 17–42.Lee, T. (1989). education, practice and research in accounting: Gaps, closed loops, bridges and magic accounting.

Accounting and Business Research, 19(5), 237–253.Lehman, C. (1988). Accounting ethics: surviving survival of the fittest.Advances in Public Interest Accounting,

2, 71–82.Lehman, G. (1995). A legitimate concern for environmental accounting.Critical Perspectives on Accounting, 6,

393–412.Lehman, G. (1999). Disclosing new worlds: A role for social and environmental accounting and auditing.

Accounting, Organisations and Society, 24, 217–241.Leung, P., & Coopers, B. (1994). Ethics in accounting: A classroom experience.Accounting Education, 3(1),

19–33.Lewis, L., Humhprey, C., & Owen, D. (1992). Accounting and the social: A pedagogical perspective.British

Accounting Review, 24(2), 219–234.Lloyd, K. (2001). The role of corporate environmental reporting in a Canada information system for the

environment final report. Straton Inc.,http://www.stratos-sts.com.Lockhart, J. A., & Mathews, M. (2000). Teaching environmental accounting: A four-part framework.Advances

138 R. Dixon et al. / Accounting Forum 28 (2004) 119–138

Loeb, S. (1988). Teaching students accounting ethics: Some crucial issues.Issues in Accounting Education, (3),316–329.

Loeb, S. (1991). The evaluation of outcomes of accounting ethics education.Journal of Business Ethics, (10),71–84.

Maltby, J. (1995). Environmental audit: Theory and practices.Managerial Auditing Journal, 10(8), 15–26.Mathews, M. (1987). “Social Accounting and the Development of Accounting Education”, Accounting and Finance

Discussion Paper, No. 68, Massey University.Mathews, M. (1997). Twenty-five years of social and environmental accounting research—Is there a silver jubilee

to celebrate?Accounting, Auditing and Accountability Journal, 10(4), 381–531.Mathews, M. (2001). Some thoughts on social and environmental accounting education.Accounting

Education—An international Journal, 10(4), 335–352.Mathews, M., & Reynolds, M. (2001). Structures for Non-Traditional Accounting Disclosures in the 21st Century,

Massey University, New Zealand, Unpublished Paper Presented at Northumbria University, UK.McPhail, K., & Gray, R. (1996).Not developing ethical maturity in accounting education: Hegemony, dissonance

and homogeneity in accounting student’s world views. Discussion Papers in Accountancy and Business FinanceACC/9605, University of Dundee.

Milne, M. (2001). Commentary on: Some thoughts on social and environmental accounting education.AccountingEducation, 10(4), 369–374.

Milner, D., Mahaffey, T., Macauley, K., & hynes, T. (1999). The effect of business education on the ethics ofstudents: An empirical assessment controlling for maturation.Teaching Business Ethics, 3(3), 255–267.

Milton-Smith, J. (1991). Australian Business Ethics Project, Phase 1: Business Schools and Business Educators,Curtin University.

Neebes, D., Guy, D., & Whittington, G. (1991). Illegal acts: What are the auditor’s responsibilities?Journal ofAccountancy, (January), 82–93.

Patrick, D. (1990). The environmental consultants’ opinion letter: A step beyond an environmental audit.Environmental Law Reporter, VXX(5).

Ponemon, L. (1990). Ethical judgements in accounting: A cognitive-developmental perspective.CriticalPerspectives on Accounting, 1, 191–215.

Ponemon, L. (1992). Ethical reasoning selection—Socialisation in accounting.Accounting, Organisations andSociety, 17(3–4), 239–258.

Pong, C., & Whittington, G. (1994). The working of the auditing practices committee—Three case studies.Accounting and Business Research, 24(94), 157–175.

Power, M. (1991). Auditing and environmental expertise: Between protest and professionalisation.Accounting,Auditing and Accountability Journal, 4(3), 30–42.

Power, M. (1997). Expertise and the construction of relevance: Accountants and environmental audit.Accounting,Organisation and Society, 22(2), 123–146.

Puxty, A. (1991). Social accountability and universal pragmatics.Advances in Public Interest Accounting, (4),35–46.

Puxty, A., Sikka, P., & Willmott, H. (1994). Reforming the circle: Education, ethics and accountancy practices.Accounting Education—An International Journal, 3(1), 77–92.

Rezaee, Z., Szendi, J., & Aggarwal, R. (1995). Corporate governance and accountability for environmentalconcerns.Managerial Auditing Journal, 10(8), 27–33.

Salter, J. (1992). Corporate environmental responsibility: Law and practice. London: Butterworth.Sanehi, A., & Waire, A. (1991). Audit to test green credentials.Financial Times, 8 August.Shields, D., & Boer, G. (1997). Research in environmental accounting.Journal of Accounting and Public Policy,

16(2), 117–125.Steadman, M., Green, R., & Zimmerer, T. (1995). Advising your clients about environmental accounting issues.

Managerial Auditing Journal, 10(8), 52–55.Sittle, J. (1992), A sound way to move into a greener world.Accountancy Age, (10), 20.Sterling, R. (1973). Accounting research, education and practice.The Journal of Accountancy, (September), 44–52.Treadway Commission (1987). Report on the National Commission on Fraudulent Financial Reporting, James

Treadway, Chairperson, National Commission on Fraudulent Financial Reporting, United States of America.Welton, R., Lagrone, M., & Davis, J. (1994). Promoting the moral development of accounting graduate students:

An instructional design and assessment.Accounting Education—An International Journal, 3(1), 35–50.