34

The New Health Insurance Marketplace Amy Hudson Director of Business Development

| Date post: | 18-Dec-2015 |

| Category: |

Documents |

| Upload: | curtis-warner |

| View: | 213 times |

| Download: | 0 times |

The New Health Insurance Marketplace

Amy HudsonDirector of Business Development

Topics for Today’s Discussion

Individuals & Families• New Insurance Marketplace starts Oct 1 • Who is Impacted• Getting Ready for Big Changes

Small Businesses• New Market Rules & Requirements • Group Size Matters• Preparing for the Changes

Questions

CoOportunity Health | 4/15/2013 | 2

New Insurance Marketplace

Impacts to Individual Market

CoOportunity Health | 4/15/2013 | 3

3 Big Changes

ACA requires that no one can be denied coverage because of pre-existing conditions

No Pre-Existing Conditions

ACA prohibits health plans from imposing annual or lifetime limits on the amount of coverage an individual receive

No Lifetime or Annual Limits

ACA will not allow insurance companies to charge higher rates based on gender

No Gender Discrimination

CoOportunity Health | 4/15/2013 | 4

INDIVIDUAL MARKET Changes coming in 2014

Exchange Guarantee Issue

Cost Sharing Help

Medicaid Expansion

Individual Mandate

Tobacco Usage

Rates higher for tobacco users

Tax penalties start at $285 for family of 4

Tax credits and subsidies for those who need it most

No one can be denied coverage for medical reasons

New Health Insurance Marketplace opens Oct. 1

Many states are expanding to 138% of FPL

$

CoOportunity Health | 4/15/2013 | 5

Health Insurance Marketplace

Exchange

Individual market restricted to open enrollment periods

The First Year

October 1, 2013 Open Enrollment Period Begins

Health Insurance Marketplace ReadyOnline Shopping Experience at www.healthcare.gov (or state URL)

Determine subsidies; enroll in health plan

March 31, 2014 Open Enrollment Ends

Mar-Sept, 2014 You can enroll if you have a qualifying event

Every Year After…

Oct 15-Dec 7 Open Enrollment Season

CoOportunity Health | 4/15/2013 | 6

Product Standardization

Exchange

All Health Insurance Carriers must offer “Metal” Plan Levels

Bronze Must pay for 60% of actuarial value

Silver Must pay for 70% of actuarial value

Gold Must pay for 80% of actuarial value

Platinum Must pay for 90% of actuarial value

Catastrophic Up to age 30 or exempt from mandate

All limit out-of-pocket expenses

All plans offered must be certified by the Exchange as a Qualified Health Plan and include Essential Health Benefits (10 categories of care that must be covered).

All health plans must include coverage for preventive care like annual physicals, pediatric care, maternity and newborn care

CoOportunity Health | 4/15/2013 | 7

Cannot be turned down for coverage

Guarantee Issue

Issuers in the individual and group markets

must accept every employer

and individual applying for coverage, or

renewing

Issuers may only use 4 Rating Factors to determine premiums

Rating Area (geography)

Age (3:1 bands)

# People on Plan

Tobacco Usage CoOportunity Health | 4/15/2013 | 8

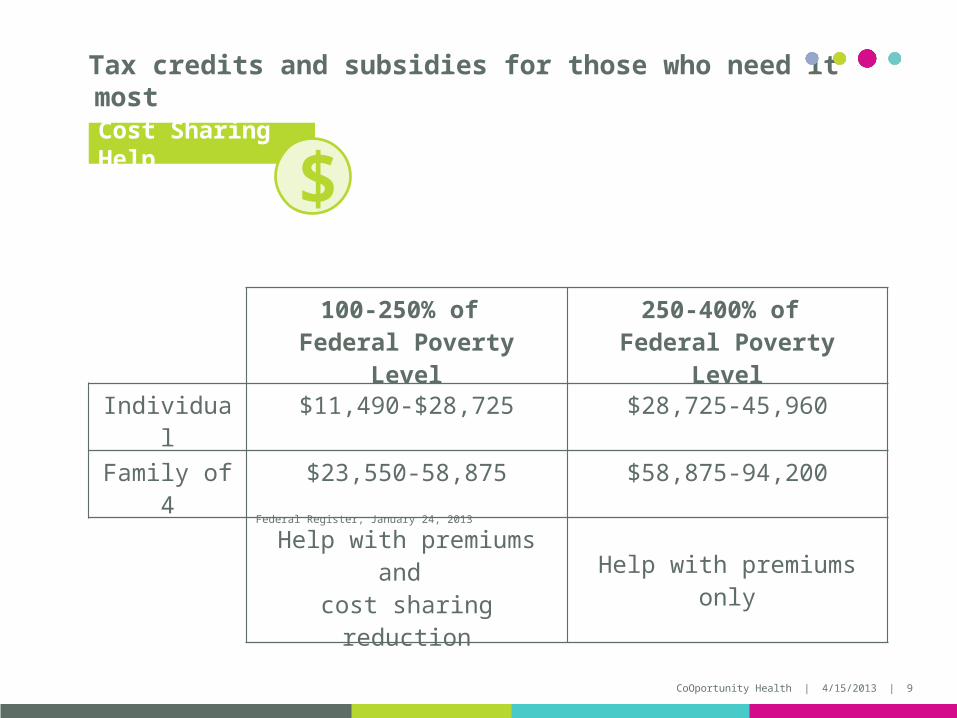

Tax credits and subsidies for those who need it most

Cost Sharing Help

$100-250% of

Federal Poverty Level250-400% of

Federal Poverty Level

Individual $11,490-$28,725 $28,725-45,960

Family of 4 $23,550-58,875 $58,875-94,200

Help with premiums and cost sharing reduction Help with premiums only

Federal Register, January 24, 2013

CoOportunity Health | 4/15/2013 | 9

Of those,Will likely be eligible for Federal Premium Assistance tax credit

Individuals/families with incomes between 100% and 400% of the Federal Poverty Level

Subsidy: Individuals pay premiums equal to: 2% of income for those at 100% of FPL rising to 9.5% of income for those at 400% of FPL

19 Million Nationwide

Cost Sharing Help

$

Uninsured

Unemployed

Self employed in individual market now

25 Million 19 Million

CoOportunity Health | 4/15/2013 | 10

States may expand from 100 to 133% of FPL

Medicaid Expansion

States that expand receive 100% of federal funding for the first 3 years, phasing to 90% in subsequent years.

Gov. Branstad is leaning toward not expanding Medicaid in Iowa.

CoOportunity Health | 4/15/2013 | 11

Tax penalties

Mandate to Buy

All individuals must maintain “minimum essential coverage” through an employer-sponsored plan or an individual plan.

2014 $95 per uninsured adult, or1% of household income

2015 $325 per uninsured adult, or2% of household income

2016 $695 per uninsured adult, or2.5 % of household income

Total household penalty may not exceed 300% of the adult penalty

CoOportunity Health | 4/15/2013 | 12

Exceptions

Mandate to Buy

Proposed 10 categories of individuals who are exempt from penalties

1 Individuals not lawfully present in the U.S. (undocumented immigrants)

2 Taxpayers with income below the filing threshold

3Individuals who cannot afford coverage; contributions toward coverage exceed 8% of household income

4 Taxpayers with income under 100% of poverty level (qualify for Medicaid)

5 Individuals who experience short coverage gaps

6 Members of Indian tribes

7 Hardship

8 Religious conscience

9 Incarcerated individuals

10 Members of health care sharing ministry

CoOportunity Health | 4/15/2013 | 13

Encouraging a Tobacco-free U.S.

Tobacco Usage

Insurance Reforms

Rating factor for tobacco use 1.5:1 (or 50% higher)

Health insurance plans (individual and group) must provide coverage for treatments to help smokers and other tobacco users quit with no out-of-pocket cost

Must provide counseling for pregnant women who smoke with no out-of-pocket cost

CoOportunity Health | 4/15/2013 | 14

I BUY PRIVATE

INSURANCETODAY

I DON’T HAVE

INSURANCE

I HAVE INSURANCE THROUGH

MY EMPLOYER

Who is impacted by the changes?

CoOportunity Health | 4/15/2013 | 15

I DON’T HAVE

INSURANCE

Who is impacted by the changes?

UNINSURED POPULATION

YOUNG & INVINCIBLES

LOST EMPLOYER COVERAGE

• In Iowa, 250,000 people are uninsured

• May stay on parent’s plan to age 26

• Looking for affordable options

GO SHOPPING

• May qualify for premium and/or cost-sharing subsidies• Go to Exchange beginning October 1, 2013 to apply• Subject to tax penalties if don’t have coverage

CoOportunity Health | 4/15/2013 | 16

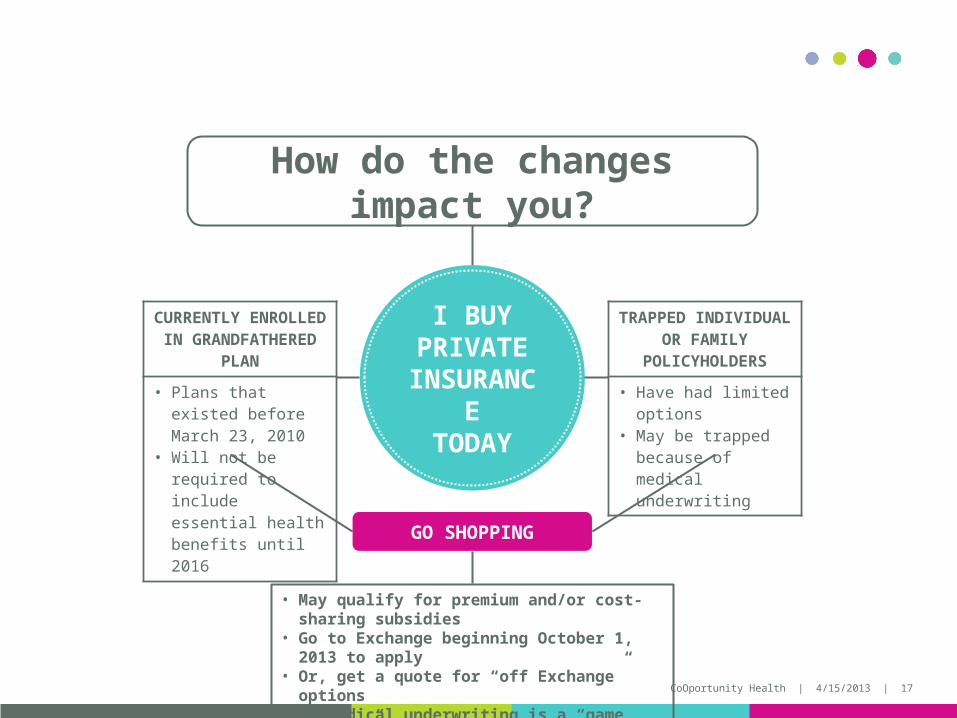

I BUY PRIVATE

INSURANCETODAY

How do the changes impact you?

TRAPPED INDIVIDUAL OR FAMILY POLICYHOLDERS

• Have had limited options

• May be trapped because of medical underwriting

CURRENTLY ENROLLED IN GRANDFATHERED PLAN

• Plans that existed before March 23, 2010

• Will not be required to include essential health benefits until 2016

GO SHOPPING

• May qualify for premium and/or cost-sharing subsidies• Go to Exchange beginning October 1, 2013 to apply• Or, get a quote for “off Exchange” options• No medical underwriting is a “game changer”

CoOportunity Health | 4/15/2013 | 17

I HAVE INSURANCE THROUGH

MY EMPLOYER

How do the changes impact you?

COVERED EMPLOYEE & DEPENDENTS

• Can opt out of employer’s coverage if it is unaffordable: more than 9.5% of household income to cover the employee’s share of premium costs

GO SHOPPING

• May qualify for premium and/or cost-sharing subsidies• Go to Exchange beginning October 1, 2013 to

understand available options

TRAPPED EARLY RETIREE

• May have felt unable to retire for fear of having no health insurance

CoOportunity Health | 4/15/2013 | 18

7 Things Individuals Can Do Now

1 Learn about different types of health insurance

2 Make a list of questions you have before it’s time to choose your health plan

3 Make sure you understand how insurance works, including deductibles, out-of-pocket maximums, copayments, etc.

4 Start gathering basic information about your household income

5 Set your budget

6 Find out from your employer whether they plan to offer health insurance

7 Explore current options; healthcare.gov is a good place to start

CoOportunity Health | 4/15/2013 | 19

Huge Market Changes for Groups

Small Group (1-50) ImpactsLarge Group (>51) Impacts

CoOportunity Health | 4/15/2013 | 20

What concerns you most about Healthcare Reform?

?What will it cost?

?How much time will this take to manage?

?When will my employees see a benefit?

?Where can I get information I can trust?

?Who can help make sure we’re prepared?

CoOportunity Health | 4/15/2013 | 21

GROUP MARKET Changes coming in 2014

Expanded Benefits New Rules SHOP

Exchange

Tax Credits Employer Mandate

New Taxes & Fees

Employer and insurer fees to support new marketplace

Requirements for groups with >50 employees

Expanded tax credits for small groups with 1-25 FTEs

Required coverage categories, levels and amounts

SHOP Exchange for Small Group (1-50)

Rating and market rule changes for small group

$

CoOportunity Health | 4/15/2013 | 22

Small Group Market (1-50) Plan Requirements

Expanded Benefits

Essential Health Benefits

Out-of-Pocket Maximum

Small Group Deductible Ceiling

Limited to Metal Plans

10 required coverage categories

New accumulation rules and ceiling

$2,000 single/$4,000 family

BronzeSilverGoldPlatinum

CoOportunity Health | 4/15/2013 | 23

Essential Health Benefits

Expanded Benefits

Essential Health Benefits

Emergency Services Hospitalization Maternity and

Newborn Care

Mental Health and Substance Use Disorder

Services

Prescription Drugs

Rehabilitative & Habilitative Services &

Devices

Laboratory Services

Preventive & Wellness

Services, Chronic Disease

Management

Pediatric Dental & Vision Care

Ambulatory Patient Services

• 10 categories of care must be included in all small group plans• No lifetime limits• No annual dollar limits

CoOportunity Health | 4/15/2013 | 24

Small Group Market Plans (1-50)

Expanded Benefits

Plans Limited to Metal Plans

Bronze Must pay for 60% of actuarial value

Silver Must pay for 70% of actuarial value

Gold Must pay for 80% of actuarial value

Platinum Must pay for 90% of actuarial value

CoOportunity Health | 4/15/2013 | 25

▶ Big Changes for Small Groups• Small Groups (1-50) – move to adjusted community rating where ALL

policyholders’ premiums only vary by location, small age bands, and tobacco use

▶ All Group Plans• Removal of pre-existing conditions• Guaranteed issue and renewal coverage• No medical underwriting

Rating and Market Rule Changes

New Rules

CoOportunity Health | 4/15/2013 | 26

Employer Requirements, SHOP & Tax Credits

1-25 FTEs 26-50 FTEs >51 FTEsInsurance

RequirementNot required to provide health insurance

Not required to provide health insurance

Required to provide health insurance

Penalties Exempt from penalties Exempt from penalties May be penalized whether or not they provide health coverage

Size Requirements

& Programs

Tax Credits• Fewer than 25 FTEs• Pay average annual wages

below $50,000• Contribute 50% or more

toward employee premiums• Up to 50% for “for profit”

firms• Up to 35% for nonprofits

Minimum Value• Insurance plan must provide

“minimum value”• Plan must pay at least 60% of

the cost of services• Plan passes “affordability” test

as long as premium contribution for single coverage does not exceed 9.5% of an employee’s W-2 wages

SHOP Exchange

• Shopping portal for small businesses

• Metal plans offered by private insurance companies

• Increased purchasing power

• Shopping portal for small businesses

• Metal plans offered by private insurance companies

• Increased purchasing power

• Iowa not changing definition yet

• Beginning in 2016, small group definition increases to fewer than 100 FTEs

• SHOP available to employers 1-100 in 2016

Outside Exchange

• May continue to purchase coverage off Exchange

• May continue to purchase coverage off Exchange

• May continue to purchase coverage off Exchange

CoOportunity Health | 4/15/2013 | 27

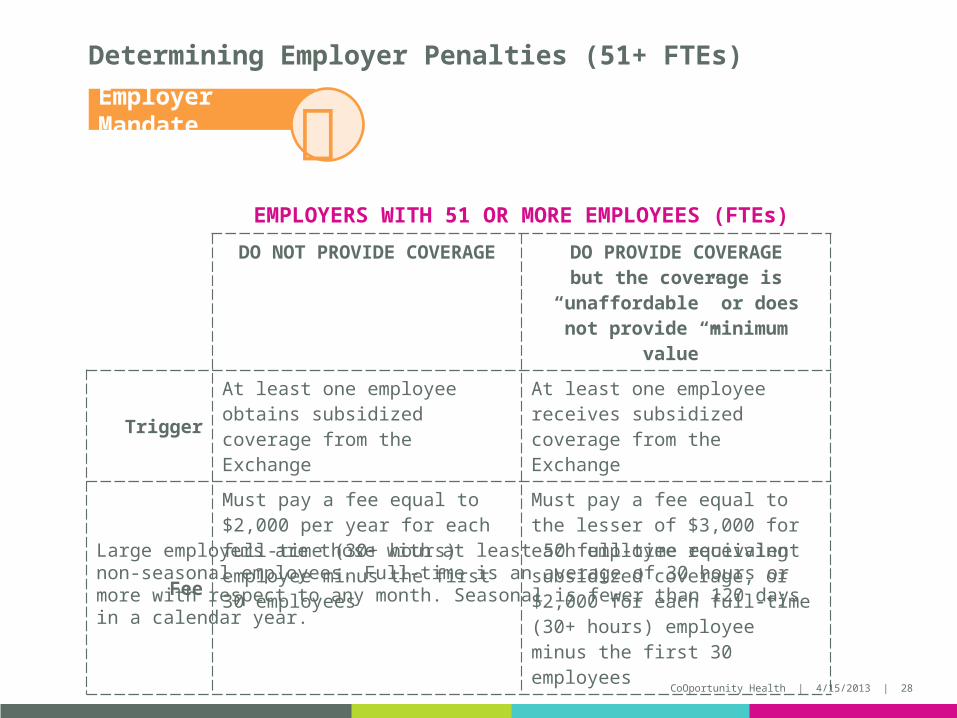

Determining Employer Penalties (51+ FTEs)

EMPLOYERS WITH 51 OR MORE EMPLOYEES (FTEs)

DO NOT PROVIDE COVERAGE DO PROVIDE COVERAGEbut the coverage is “unaffordable” or does not provide “minimum value”

TriggerAt least one employee obtains subsidized coverage from the Exchange

At least one employee receives subsidized coverage from the Exchange

Fee

Must pay a fee equal to $2,000 per year for each full-time (30+ hours) employee minus the first 30 employees

Must pay a fee equal to the lesser of $3,000 for each employee receiving subsidized coverage, or $2,000 for each full-time (30+ hours) employee minus the first 30 employees

Large employers are those with at least 50 full-time equivalent non-seasonal employees. Full-time is an average of 30 hours or more with respect to any month. Seasonal is fewer than 120 days in a calendar year.

Employer Mandate

CoOportunity Health | 4/15/2013 | 28

Paying to Play in the New Insurance Marketplace

New Taxes & FeesPCORI Fee Insurer Fee Transitional

Reinsurance Fee

Excise Tax Risk Adjustment Program & Fee

Helps fund the “Patient Centered Outcomes Research Institute”

Funds the Health Insurance Marketplace (Exchange)

Stabilizes Individual & Small Group Markets

On Rich Benefit Coverage

Helps fund administrative cost of running the program

Individual MarketSmall Group Market51+ Fully Insured & ASO Groups

Fully Insured Only-Individual Market-Small Group

Individual MarketSmall Group Market51+ Fully Insured & ASO Groups

51+ Fully Insured & ASO Groups

Fully Insured Only-Individual Market-Small Group

CoOportunity Health | 4/15/2013 | 29

Components Driving Pricing Impacts

Rating Rules Changes

Product/Benefit Enhancements

Taxes & Fees

AverageAnnual Rate

Increase+

Individual Market Small Group Market Large Group Market

ACA compliance drives significant price increases

Community Rating causes material price disruption for healthiest groups

Incremental increases to rates beginning in 2013 to cover taxes, fees and benefits

CoOportunity Health | 4/15/2013 | 30

Key Dates & Changes for Group Plans

2013 Notifications

Employers must provide all employees with information about Exchanges in late summer/early fallEmployers with more than 250 employees required to put the cost of health benefits on W-2sFlexible Spending Accounts (FSAs) capped at $2,500 per plan year (indexed with inflation in future years)

October 1, 2013 Open Enrollment Period Begins for the Individual Health Insurance Marketplace (Exchange) and Small Group 1-50 SHOP Exchange

March 31, 2014 Open Enrollment Ends for individual and small group

Mar-Sept, 2014 Individuals can make changes outside of Open Enrollment if they have a HIPAA-qualifying event

2016 Small Group Market (and SHOP) expands to 1-100

2017 Large Groups may be able to participate on SHOP Exchange

CoOportunity Health | 4/15/2013 | 31

7 Things Employers Can Do Now

1 Know the law. Depending on the size of your firm and the composition of your workforce, there are major implications

2 View healthcare reform as a real opportunity to explore new options

3 Model your company’s situation; you may need to re-shape your workforce or capitalize on the law to vault your business forward

4 Determine if you will continue to offer coverage and when the effective date will be; be mindful of individual market Exchange enrollment periods

5 Get organized with required application information if you intend to apply for coverage through the SHOP Exchange

6 Review employer mandates, premium changes and develop strategy

7 This is an unprecedented time to shop; use a trusted advisor to help you evaluate options and make decisions

CoOportunity Health | 4/15/2013 | 32

• New option for Iowans and Nebraskans• Nonprofit CO-OP (consumer operated and

oriented plan); member owned and governed• CO-OPs established in the Affordable Care Act• “Invented” to provide affordable options for

individuals and families• 24 CO-OPs in U.S. so far• Low interest startup loans provided by federal

government• Start marketing health plans October 1• On Exchange plans for individuals and small

businesses• Off Exchange plans for all market segments• Alternative to traditional commercial carriers

CoOportunity Health | 4/15/2013 | 33

Questions?

CoOportunity Health | 4/15/2013 | 34

Register for Next Webinars:- April 23, 1-2 p.m.: https://

cc.readytalk.com/cc/s/registrations/new?cid=u5brugyln8cz - April 30, 1-2 p.m.: https://

cc.readytalk.com/cc/s/registrations/new?cid=czp0k8hd7nkl