38

The New Mexico Economy: Recent Developments and Outlook 18 th Annual Data Users Conference Jeffrey Mitchell, BBER Director

The New Mexico Economy: Recent Developments and Outlook

18th Annual Data Users Conference Jeffrey Mitchell, BBER Director

Rapid Post-election Analysis o Short and medium term tradeoff between heightened uncertainty

for businesses and consumers and likely fiscal stimulus (infrastructure, tax cuts).

o Greater concern for longer-term outlook as many analysts expect increased federal deficits and higher interest rates.

o Specific measures – some suggested in outline of President-elect’s 100 Day plan. Impacts will likely be highly uneven – winners & losers.

o Roll back of Obamacare – shake up in insurance and healthcare markets. Most think changes will not be overnight.

o Tax reform: lower marginal rates for individuals and corporations; however, without changes in spending policy, deficits will grow rapidly.

Rapid Post-election Analysis o Likely rollback of various business regulations, including

environmental regulations, which will impact the energy sector (and others).

o Changes to US immigration policy may impact undocumented workers, including and individuals with HB-1 visas. Impact on labor markets likely.

o Re-working of international trade agreements (such as NAFTA and others) including possible initiation of import quotas or taxation with countries such as China. Likely higher inflation.

o In short – uncertainty. Cabinet selections may be early signal.

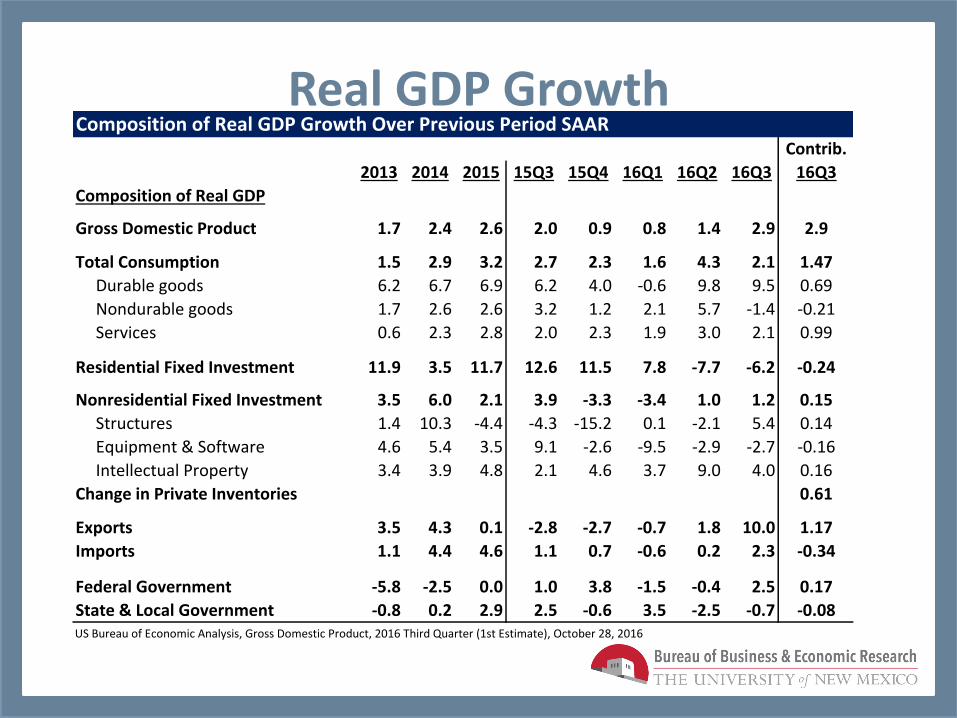

Real GDP Growth

Contrib.

2013 2014 2015 15Q3 15Q4 16Q1 16Q2 16Q3 16Q3

Composition of Real GDP

Gross Domestic Product 1.7 2.4 2.6 2.0 0.9 0.8 1.4 2.9 2.9

Total Consumption 1.5 2.9 3.2 2.7 2.3 1.6 4.3 2.1 1.47

Durable goods 6.2 6.7 6.9 6.2 4.0 -0.6 9.8 9.5 0.69

Nondurable goods 1.7 2.6 2.6 3.2 1.2 2.1 5.7 -1.4 -0.21

Services 0.6 2.3 2.8 2.0 2.3 1.9 3.0 2.1 0.99

Residential Fixed Investment 11.9 3.5 11.7 12.6 11.5 7.8 -7.7 -6.2 -0.24

Nonresidential Fixed Investment 3.5 6.0 2.1 3.9 -3.3 -3.4 1.0 1.2 0.15

Structures 1.4 10.3 -4.4 -4.3 -15.2 0.1 -2.1 5.4 0.14

Equipment & Software 4.6 5.4 3.5 9.1 -2.6 -9.5 -2.9 -2.7 -0.16

Intellectual Property 3.4 3.9 4.8 2.1 4.6 3.7 9.0 4.0 0.16

Change in Private Inventories 0.61

Exports 3.5 4.3 0.1 -2.8 -2.7 -0.7 1.8 10.0 1.17

Imports 1.1 4.4 4.6 1.1 0.7 -0.6 0.2 2.3 -0.34

Federal Government -5.8 -2.5 0.0 1.0 3.8 -1.5 -0.4 2.5 0.17

State & Local Government -0.8 0.2 2.9 2.5 -0.6 3.5 -2.5 -0.7 -0.08US Bureau of Economic Analysis, Gross Domestic Product, 2016 Third Quarter (1st Estimate), October 28, 2016

Composition of Real GDP Growth Over Previous Period SAAR

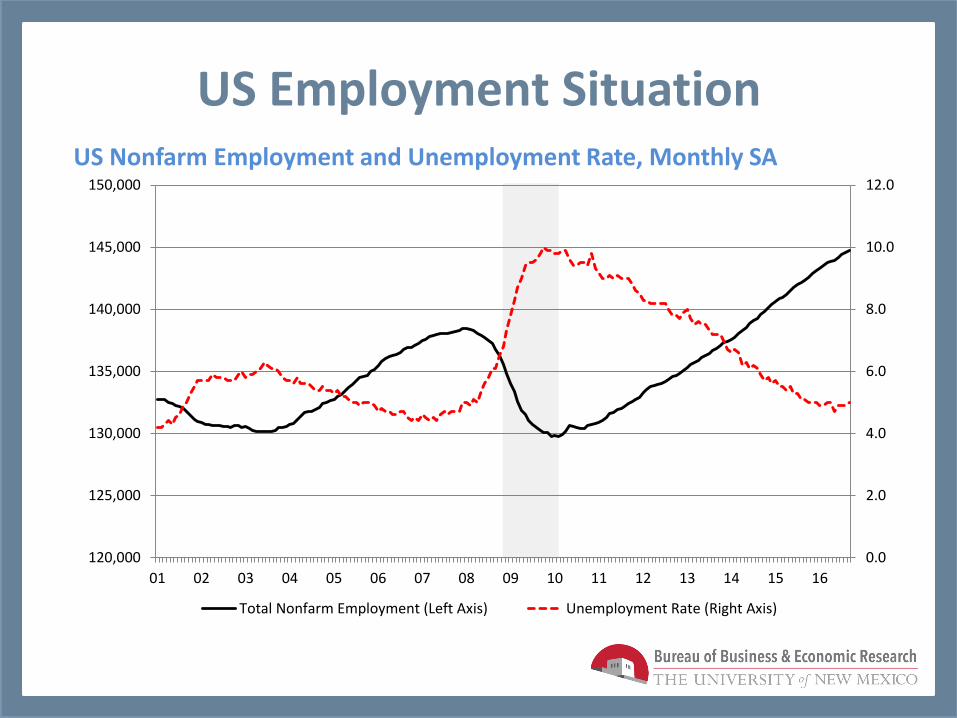

US Nonfarm Employment and Unemployment Rate, Monthly SA

US Employment Situation

0.0

2.0

4.0

6.0

8.0

10.0

12.0

120,000

125,000

130,000

135,000

140,000

145,000

150,000

01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16

Total Nonfarm Employment (Left Axis) Unemployment Rate (Right Axis)

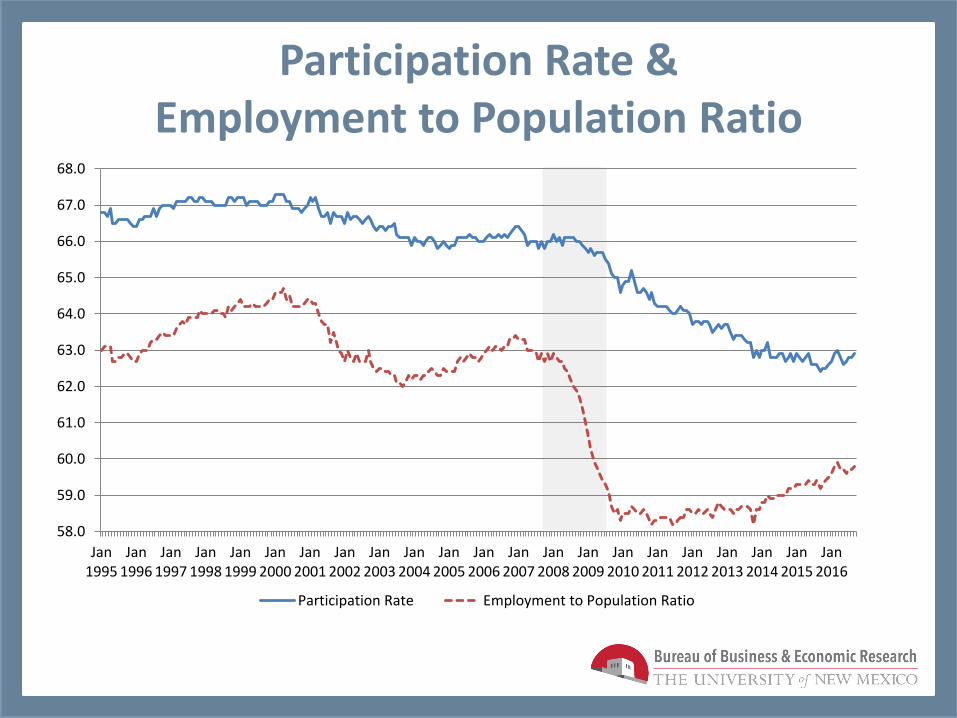

Participation Rate & Employment to Population Ratio

58.0

59.0

60.0

61.0

62.0

63.0

64.0

65.0

66.0

67.0

68.0

Jan1995

Jan1996

Jan1997

Jan1998

Jan1999

Jan2000

Jan2001

Jan2002

Jan2003

Jan2004

Jan2005

Jan2006

Jan2007

Jan2008

Jan2009

Jan2010

Jan2011

Jan2012

Jan2013

Jan2014

Jan2015

Jan2016

Participation Rate Employment to Population Ratio

IHS Pessimistic Scenario All Forecasts completed in October & do not reflect election results.

o Global and political risks trigger uncertainty and damage business confidence.

o US economy suffers brief recession in second half of 2017 as productivity and business investment suffer.

o Dollar strengthens as it becomes even more of a safe haven – US exports are negatively impacted thereby worsening the trade deficit.

o Modest demand-side pressure put upward pressure on wage and price inflation prompting the Fed to raise rates aggressively in the near-term.

o Oil markets tighten quickly pushing oil prices up in the near-term.

o Consumer & business confidence falls, causing both consumer spending and equity markets to fall sharply.

o The Fed is forced to return to rock-bottom interest rates and oil markets again retreat.

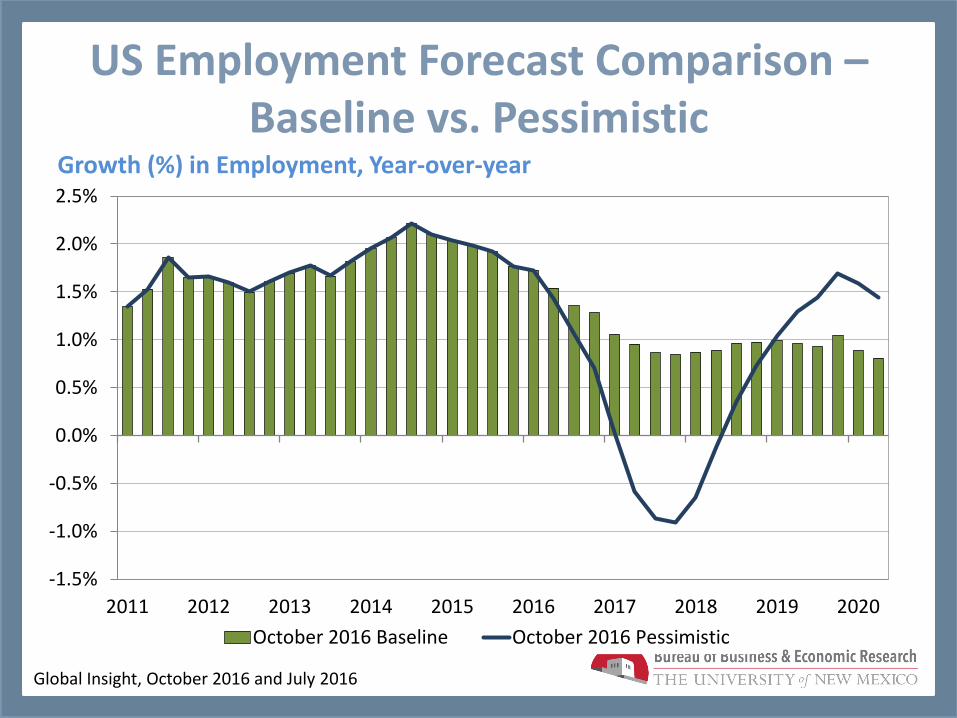

Growth (%) in Employment, Year-over-year

Global Insight, October 2016 and July 2016

US Employment Forecast Comparison – Baseline vs. Pessimistic

-1.5%

-1.0%

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

October 2016 Baseline October 2016 Pessimistic

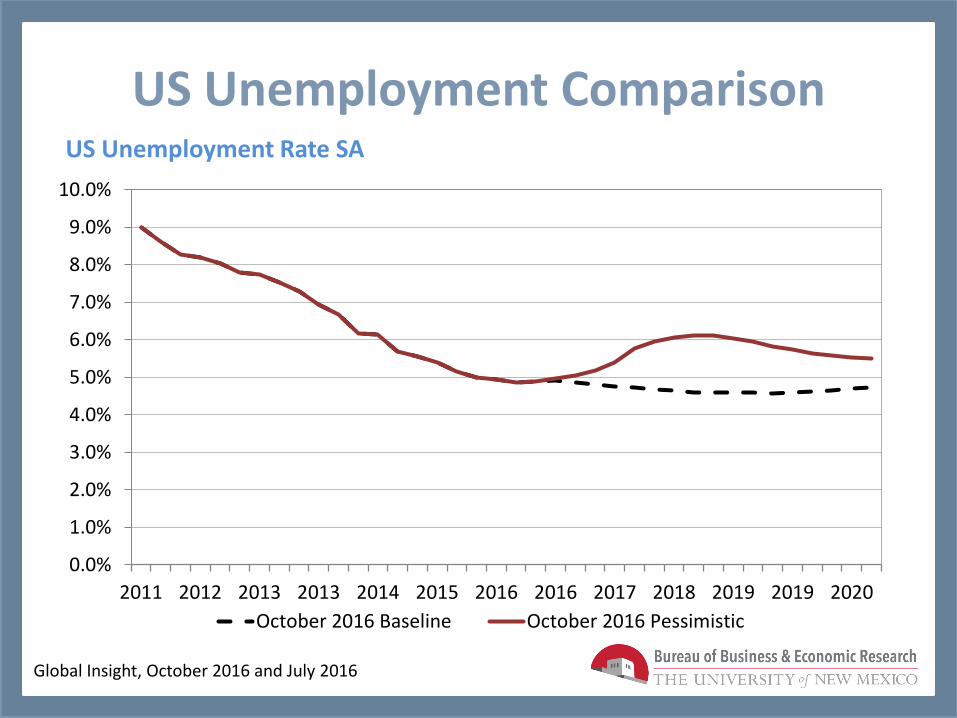

US Unemployment Rate SA

Global Insight, October 2016 and July 2016

US Unemployment Comparison

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

2011 2012 2013 2013 2014 2015 2016 2016 2017 2018 2019 2019 2020

October 2016 Baseline October 2016 Pessimistic

Global Insight, October 2016

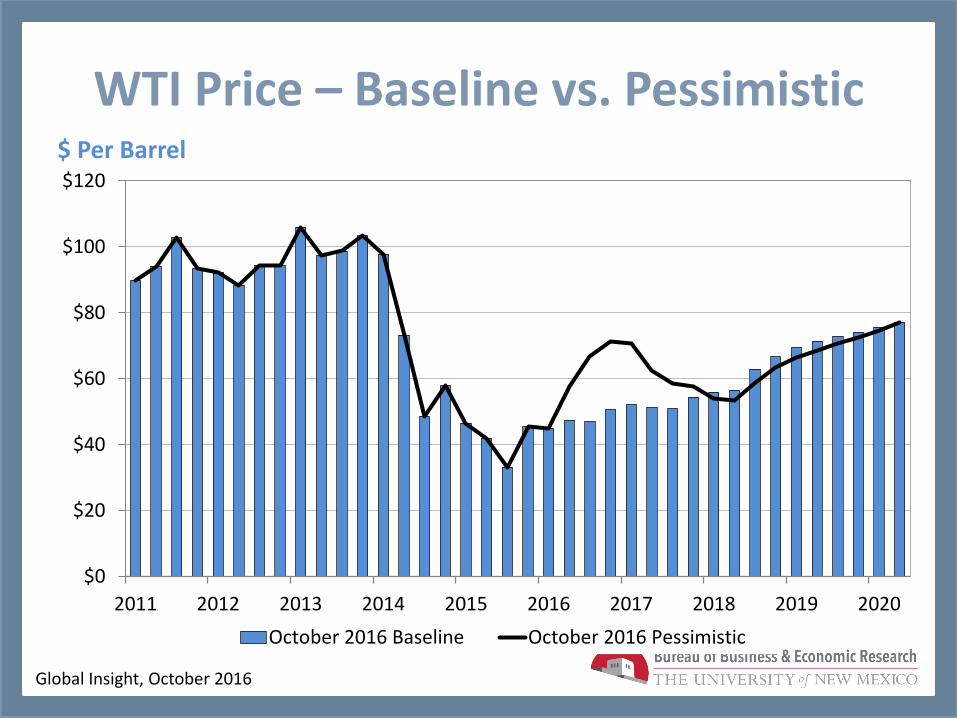

$ Per Barrel

WTI Price – Baseline vs. Pessimistic

$0

$20

$40

$60

$80

$100

$120

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

October 2016 Baseline October 2016 Pessimistic

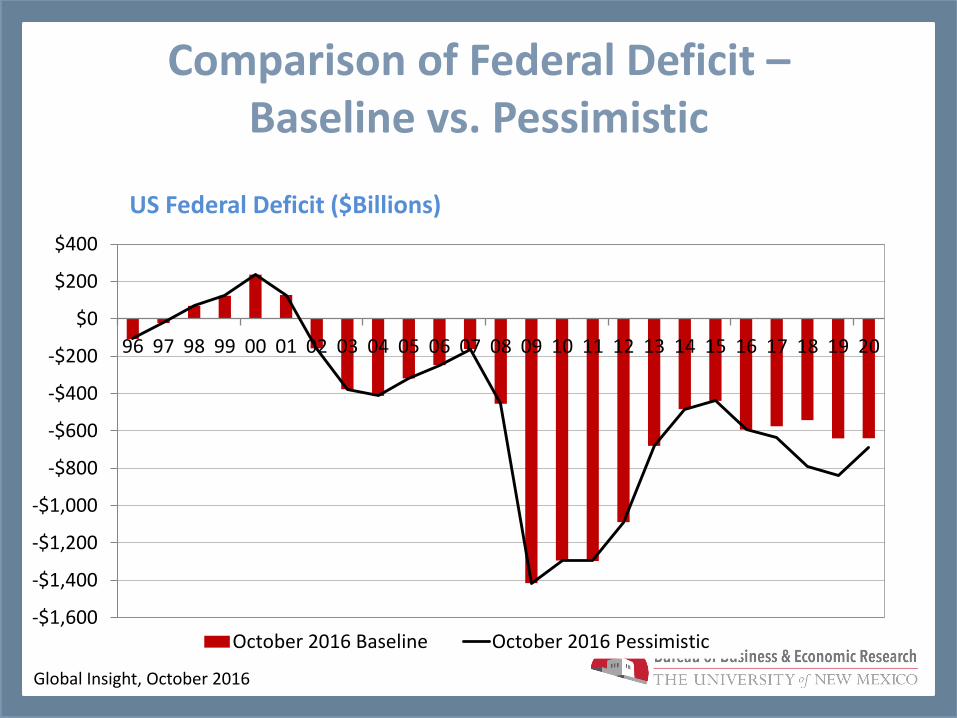

US Federal Deficit ($Billions)

Global Insight, October 2016

Comparison of Federal Deficit – Baseline vs. Pessimistic

-$1,600

-$1,400

-$1,200

-$1,000

-$800

-$600

-$400

-$200

$0

$200

$400

96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18 19 20

October 2016 Baseline October 2016 Pessimistic

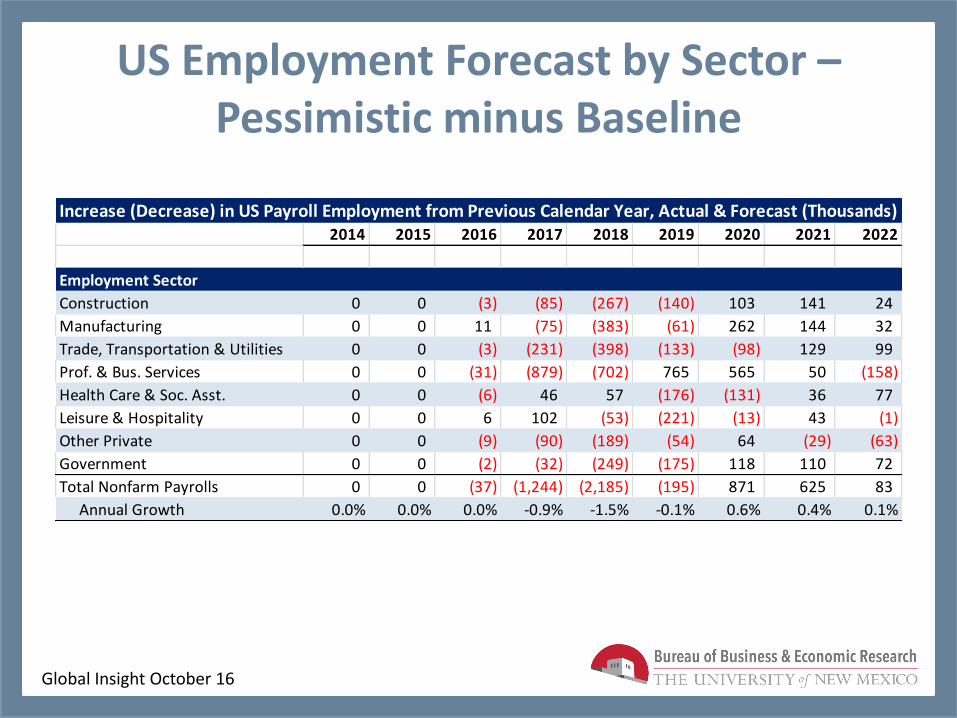

US Employment Forecast by Sector –Pessimistic minus Baseline

Global Insight October 16

2014 2015 2016 2017 2018 2019 2020 2021 2022

Employment Sector

Construction 0 0 (3) (85) (267) (140) 103 141 24

Manufacturing 0 0 11 (75) (383) (61) 262 144 32

Trade, Transportation & Utilities 0 0 (3) (231) (398) (133) (98) 129 99

Prof. & Bus. Services 0 0 (31) (879) (702) 765 565 50 (158)

Health Care & Soc. Asst. 0 0 (6) 46 57 (176) (131) 36 77

Leisure & Hospitality 0 0 6 102 (53) (221) (13) 43 (1)

Other Private 0 0 (9) (90) (189) (54) 64 (29) (63)

Government 0 0 (2) (32) (249) (175) 118 110 72

Total Nonfarm Payrolls 0 0 (37) (1,244) (2,185) (195) 871 625 83

Annual Growth 0.0% 0.0% 0.0% -0.9% -1.5% -0.1% 0.6% 0.4% 0.1%

Increase (Decrease) in US Payroll Employment from Previous Calendar Year, Actual & Forecast (Thousands)

New Mexico Review

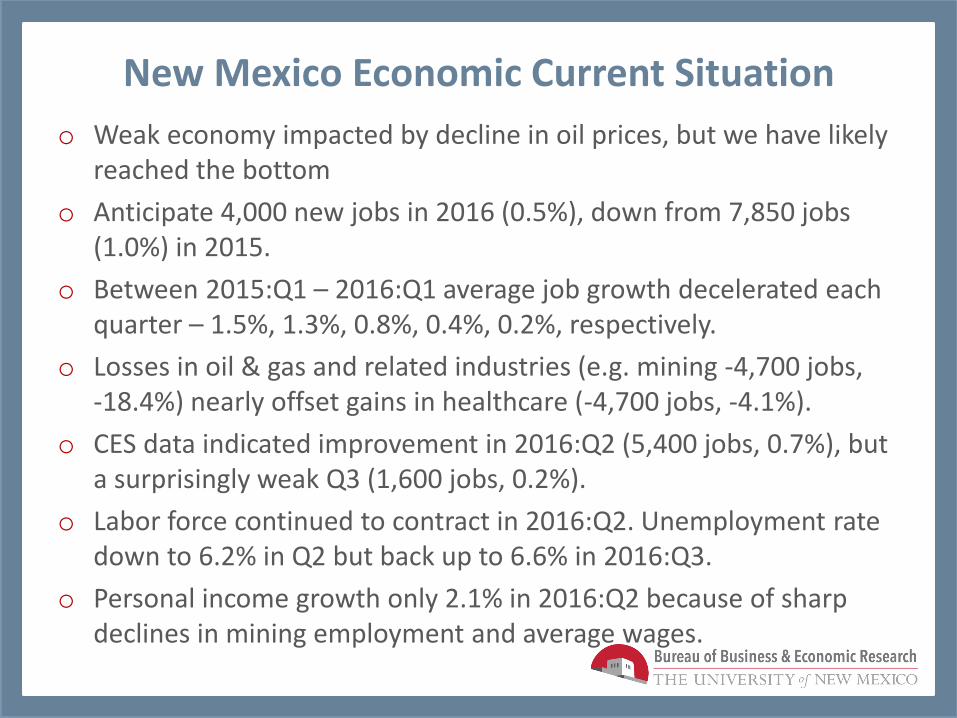

New Mexico Economic Current Situation

o Weak economy impacted by decline in oil prices, but we have likely reached the bottom

o Anticipate 4,000 new jobs in 2016 (0.5%), down from 7,850 jobs (1.0%) in 2015.

o Between 2015:Q1 – 2016:Q1 average job growth decelerated each quarter – 1.5%, 1.3%, 0.8%, 0.4%, 0.2%, respectively.

o Losses in oil & gas and related industries (e.g. mining -4,700 jobs, -18.4%) nearly offset gains in healthcare (-4,700 jobs, -4.1%).

o CES data indicated improvement in 2016:Q2 (5,400 jobs, 0.7%), but a surprisingly weak Q3 (1,600 jobs, 0.2%).

o Labor force continued to contract in 2016:Q2. Unemployment rate down to 6.2% in Q2 but back up to 6.6% in 2016:Q3.

o Personal income growth only 2.1% in 2016:Q2 because of sharp declines in mining employment and average wages.

Job Growth by Sector, 2016

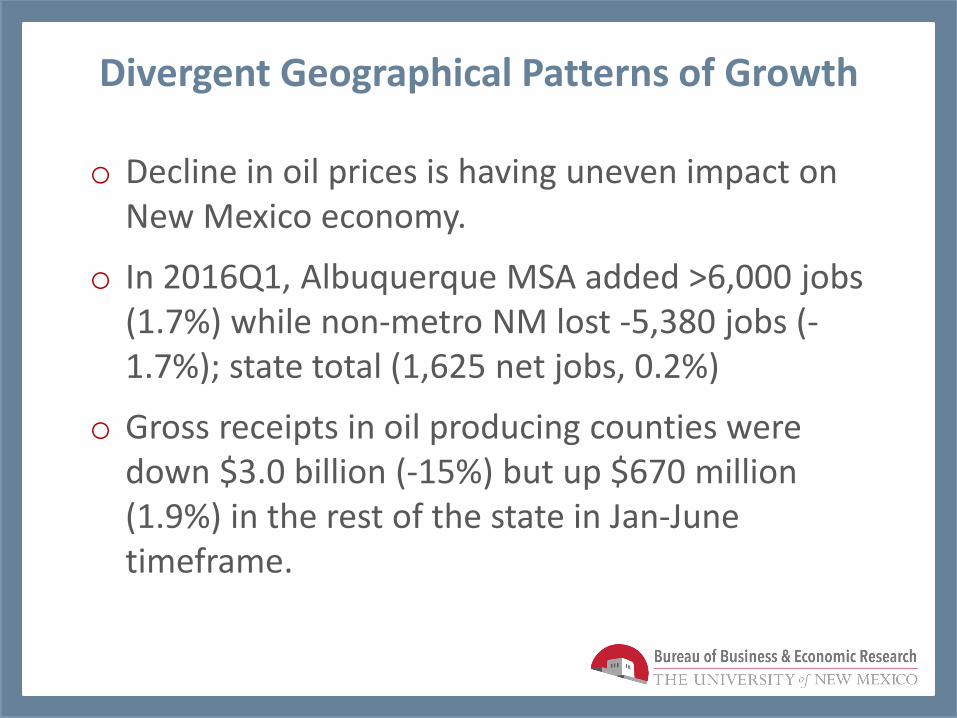

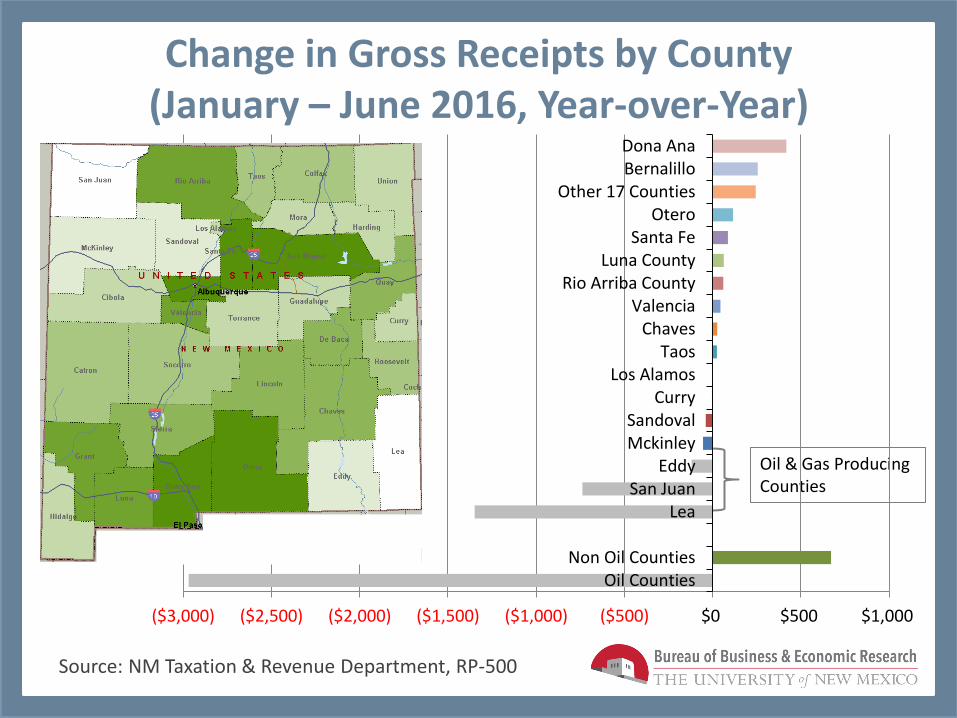

Divergent Geographical Patterns of Growth

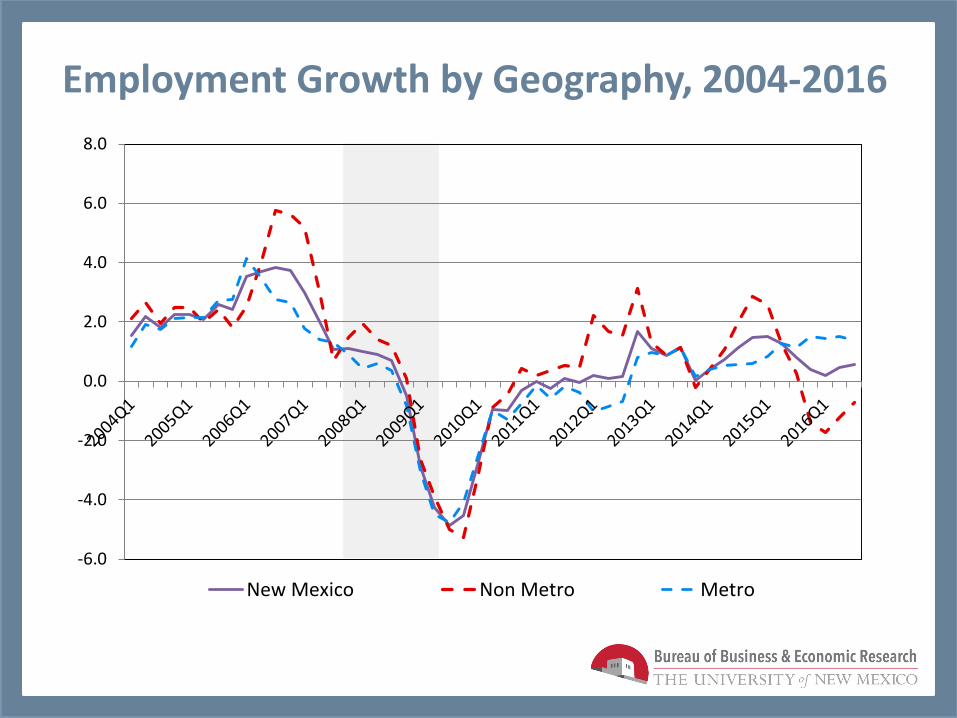

o Decline in oil prices is having uneven impact on New Mexico economy.

o In 2016Q1, Albuquerque MSA added >6,000 jobs (1.7%) while non-metro NM lost -5,380 jobs (-1.7%); state total (1,625 net jobs, 0.2%)

o Gross receipts in oil producing counties were down $3.0 billion (-15%) but up $670 million (1.9%) in the rest of the state in Jan-June timeframe.

Change in Gross Receipts by County (January – June 2016, Year-over-Year)

Source: NM Taxation & Revenue Department, RP-500

Oil & Gas Producing Counties

($3,000) ($2,500) ($2,000) ($1,500) ($1,000) ($500) $0 $500 $1,000

Oil CountiesNon Oil Counties

LeaSan Juan

EddyMckinleySandoval

CurryLos Alamos

TaosChaves

ValenciaRio Arriba County

Luna CountySanta Fe

OteroOther 17 Counties

BernalilloDona Ana

Employment Growth by Geography, 2004-2016

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

New Mexico Non Metro Metro

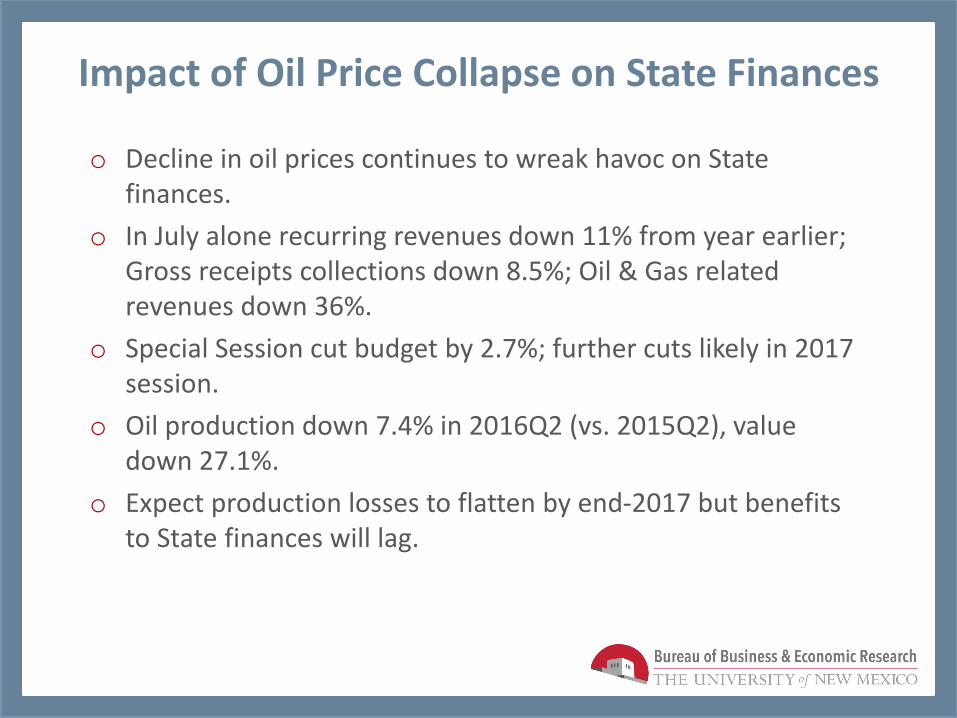

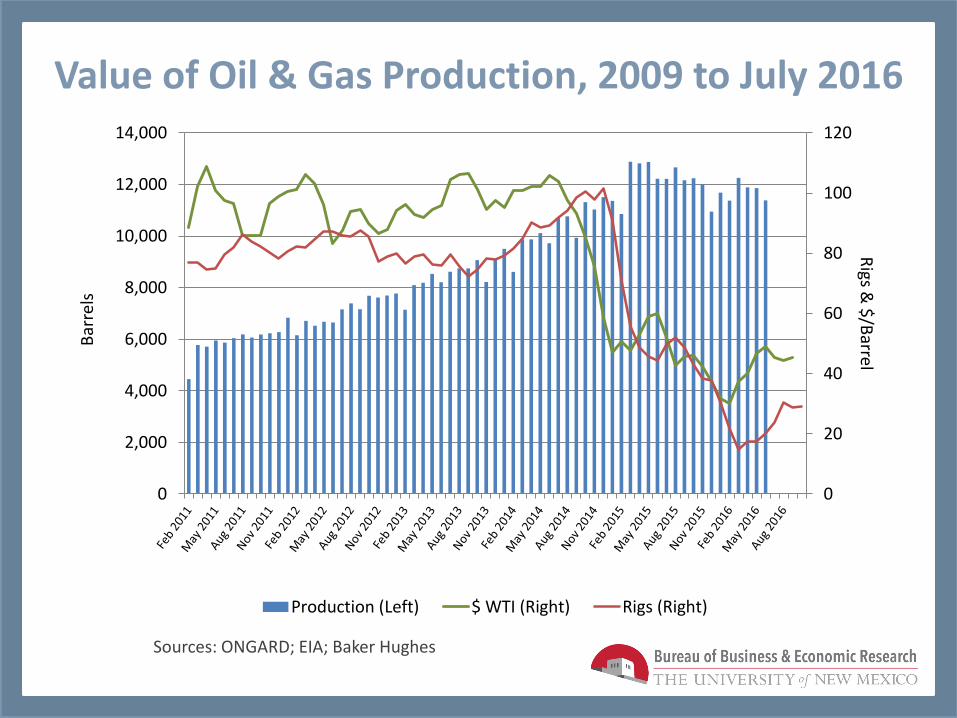

Impact of Oil Price Collapse on State Finances

o Decline in oil prices continues to wreak havoc on State finances.

o In July alone recurring revenues down 11% from year earlier; Gross receipts collections down 8.5%; Oil & Gas related revenues down 36%.

o Special Session cut budget by 2.7%; further cuts likely in 2017 session.

o Oil production down 7.4% in 2016Q2 (vs. 2015Q2), value down 27.1%.

o Expect production losses to flatten by end-2017 but benefits to State finances will lag.

New Mexico State General Fund Revenues, by Source

Source: NMTRI

Oil & Gas (Direct & Indirect) = 31%

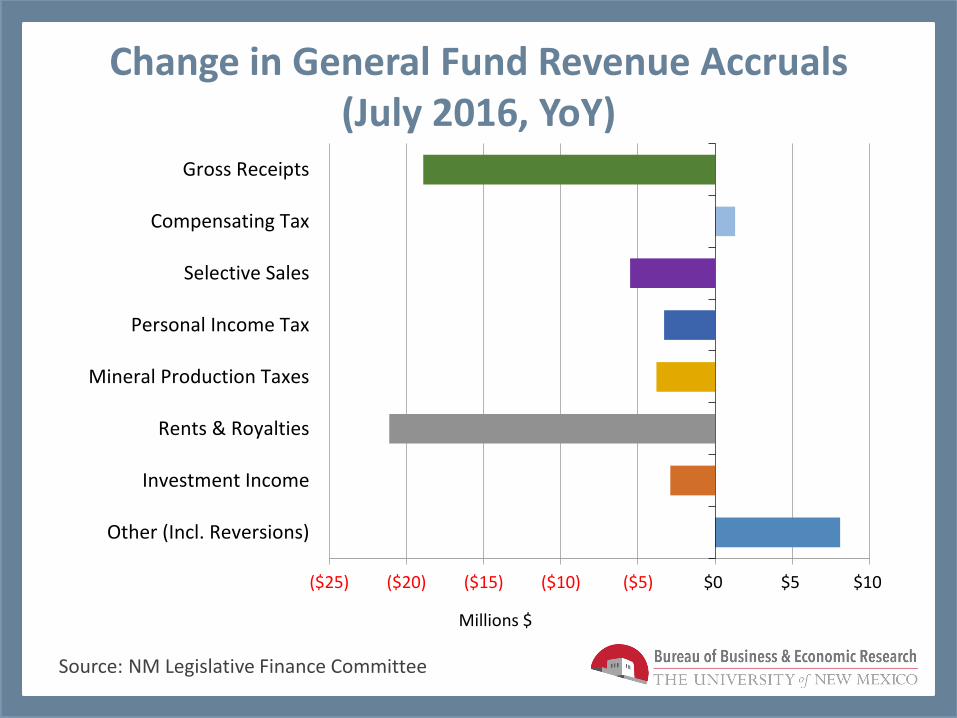

Change in General Fund Revenue Accruals (July 2016, YoY)

Source: NM Legislative Finance Committee

($25) ($20) ($15) ($10) ($5) $0 $5 $10

Other (Incl. Reversions)

Investment Income

Rents & Royalties

Mineral Production Taxes

Personal Income Tax

Selective Sales

Compensating Tax

Gross Receipts

Millions $

Value of Oil & Gas Production, 2009 to July 2016

Sources: ONGARD; EIA; Baker Hughes

0

20

40

60

80

100

120

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

Rigs &

$/B

arrel B

arre

ls

Production (Left) $ WTI (Right) Rigs (Right)

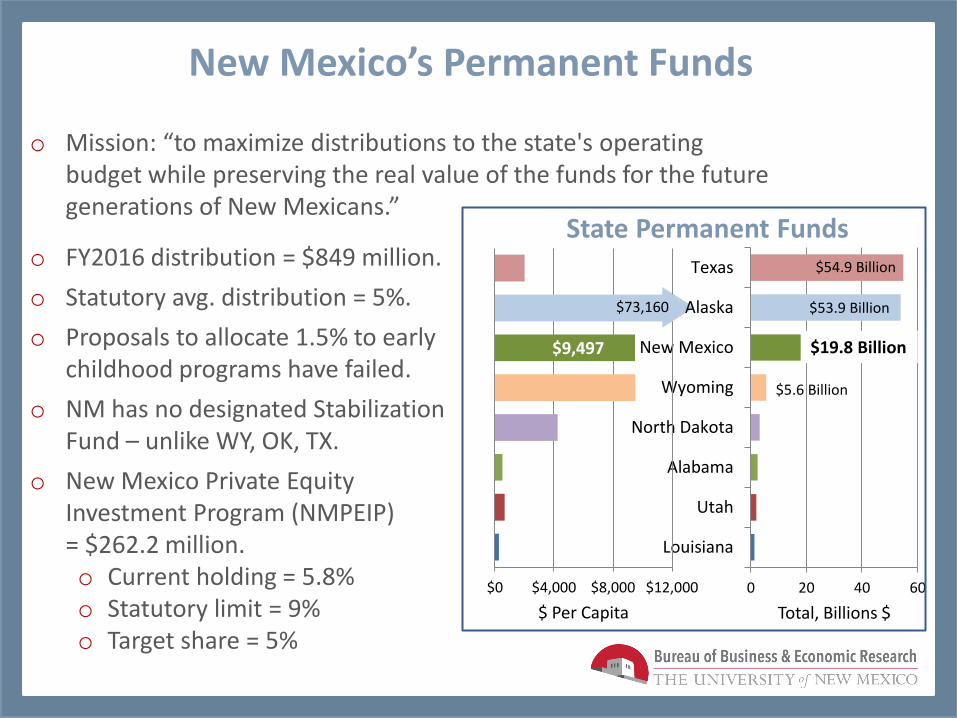

New Mexico’s Permanent Funds

o FY2016 distribution = $849 million.

o Statutory avg. distribution = 5%.

o Proposals to allocate 1.5% to early childhood programs have failed.

o NM has no designated Stabilization Fund – unlike WY, OK, TX.

o New Mexico Private Equity Investment Program (NMPEIP) = $262.2 million. o Current holding = 5.8% o Statutory limit = 9% o Target share = 5%

o Mission: “to maximize distributions to the state's operating budget while preserving the real value of the funds for the future generations of New Mexicans.”

State Permanent Funds

0 20 40 60

Louisiana

Utah

Alabama

North Dakota

Wyoming

New Mexico

Alaska

Texas

Total, Billions $

$0 $4,000 $8,000 $12,000

$ Per Capita

$73,160

$9,497

$53.9 Billion

$19.8 Billion

$5.6 Billion

$54.9 Billion

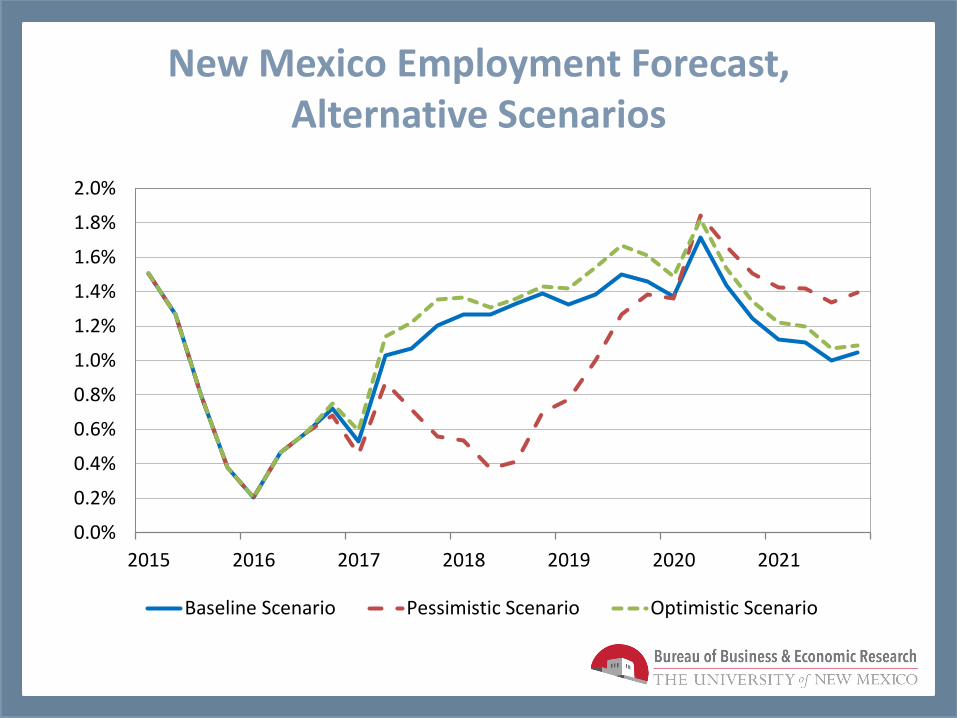

New Mexico Economic Outlook

New Mexico Economic Outlook: 2016-2022 o Economic impacts of oil collapse will lessen in second half of 2016, and reach

the bottom by mid-2017 – though fiscal impacts will linger.

o Employment growth: 5,300 jobs (0.7%) in second half of 2016, and 7,800 jobs (1.0%) in 2017 and 1.2% thereafter.

o Short-term job growth is in Metro areas, esp. Albuquerque, but slightly negative in non-metro areas. Stronger statewide mid- and longer-term growth occur when non-Metro moves positive.

o Composition of new jobs:

o 55% (2017)/38% (2018-2022) in education and healthcare & social assistance

o 36% (2017)/26% (2018-2022) in low-wage service sectors

o 12% (2017)/19% (2018-2022) in mining, utilities, construction, manufacturing, transportation

o 12% (2017)/9% (2018-2022) in financial and P&BS

o Outlook for government employment weak (-0.9% in 2017, 0.3% thereafter).

o Income outlook slow: 2.4% in 2016, rising to 3.6% in 2017, and 4.6% through 2022. Wage growth to private sector workers key variable.

New Mexico Employment Forecast, Alternative Scenarios

0.0%

0.2%

0.4%

0.6%

0.8%

1.0%

1.2%

1.4%

1.6%

1.8%

2.0%

2015 2016 2017 2018 2019 2020 2021

Baseline Scenario Pessimistic Scenario Optimistic Scenario

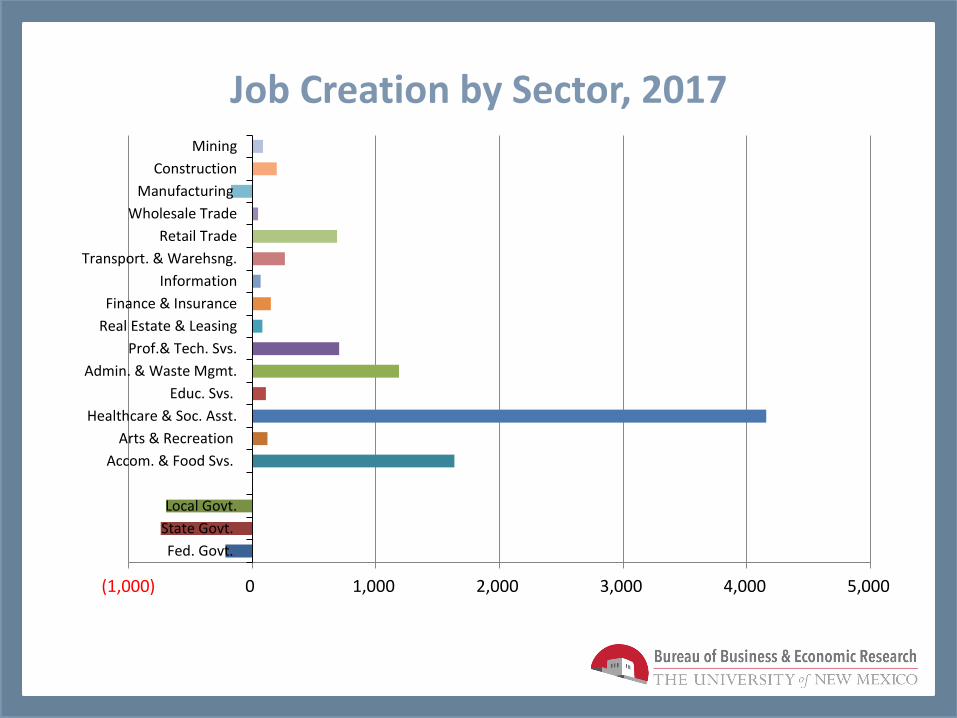

Job Creation by Sector, 2017

(1,000) 0 1,000 2,000 3,000 4,000 5,000

Fed. Govt.

State Govt.

Local Govt.

Accom. & Food Svs.

Arts & Recreation

Healthcare & Soc. Asst.

Educ. Svs.

Admin. & Waste Mgmt.

Prof.& Tech. Svs.

Real Estate & Leasing

Finance & Insurance

Information

Transport. & Warehsng.

Retail Trade

Wholesale Trade

Manufacturing

Construction

Mining

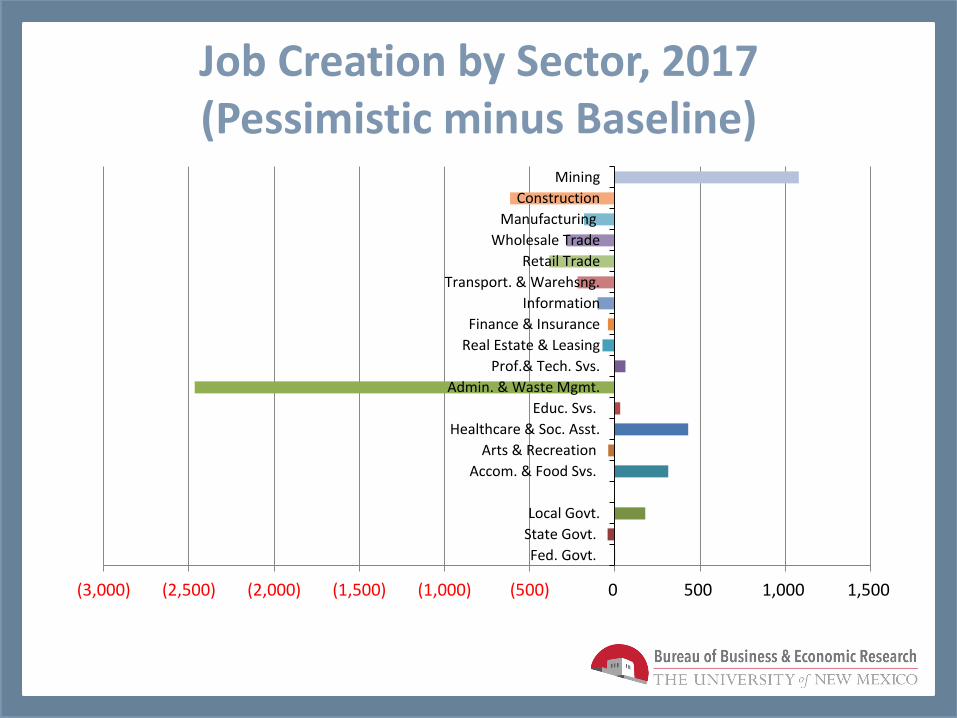

Job Creation by Sector, 2017 (Pessimistic minus Baseline)

(3,000) (2,500) (2,000) (1,500) (1,000) (500) 0 500 1,000 1,500

Fed. Govt.

State Govt.

Local Govt.

Accom. & Food Svs.

Arts & Recreation

Healthcare & Soc. Asst.

Educ. Svs.

Admin. & Waste Mgmt.

Prof.& Tech. Svs.

Real Estate & Leasing

Finance & Insurance

Information

Transport. & Warehsng.

Retail Trade

Wholesale Trade

Manufacturing

Construction

Mining

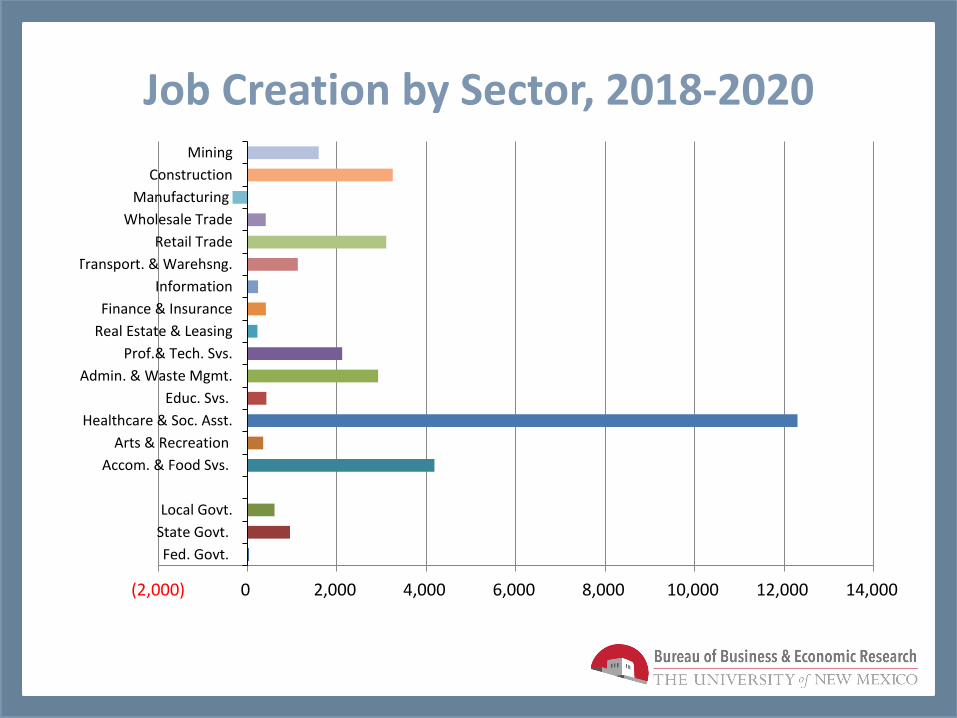

Job Creation by Sector, 2018-2020

(2,000) 0 2,000 4,000 6,000 8,000 10,000 12,000 14,000

Fed. Govt.

State Govt.

Local Govt.

Accom. & Food Svs.

Arts & Recreation

Healthcare & Soc. Asst.

Educ. Svs.

Admin. & Waste Mgmt.

Prof.& Tech. Svs.

Real Estate & Leasing

Finance & Insurance

Information

Transport. & Warehsng.

Retail Trade

Wholesale Trade

Manufacturing

Construction

Mining

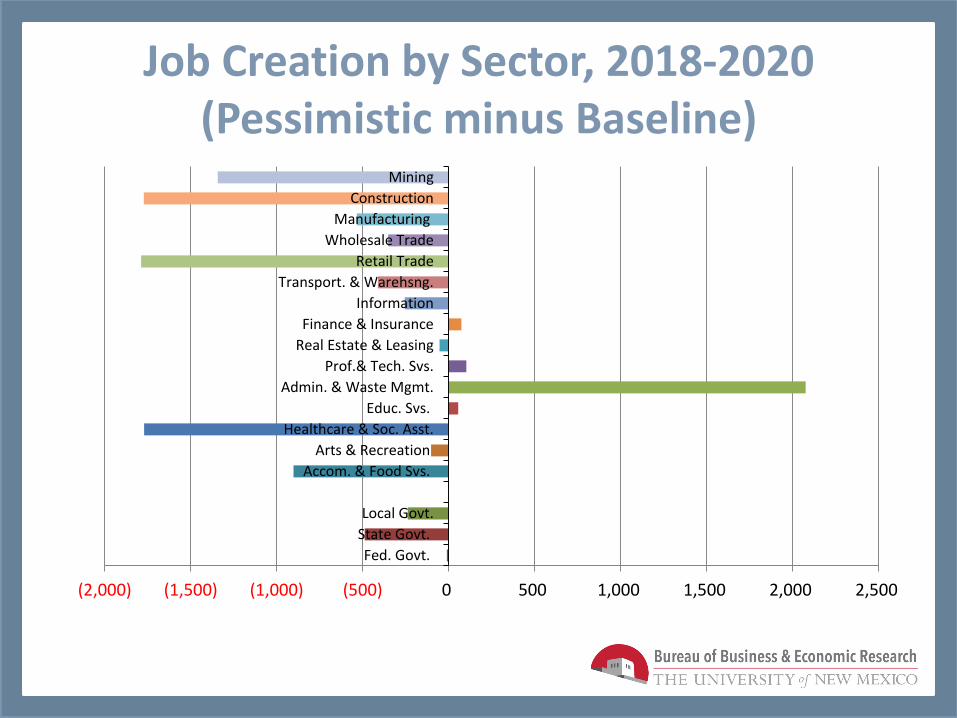

Job Creation by Sector, 2018-2020 (Pessimistic minus Baseline)

(2,000) (1,500) (1,000) (500) 0 500 1,000 1,500 2,000 2,500

Fed. Govt.

State Govt.

Local Govt.

Accom. & Food Svs.

Arts & Recreation

Healthcare & Soc. Asst.

Educ. Svs.

Admin. & Waste Mgmt.

Prof.& Tech. Svs.

Real Estate & Leasing

Finance & Insurance

Information

Transport. & Warehsng.

Retail Trade

Wholesale Trade

Manufacturing

Construction

Mining

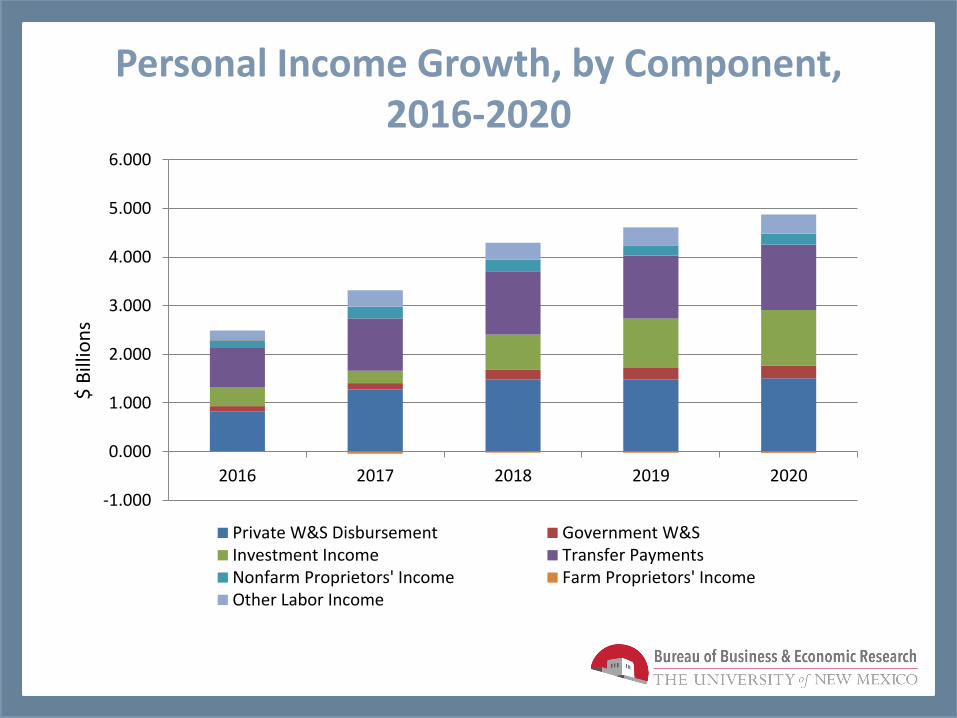

Personal Income Growth, by Component, 2016-2020

-1.000

0.000

1.000

2.000

3.000

4.000

5.000

6.000

2016 2017 2018 2019 2020

Private W&S Disbursement Government W&SInvestment Income Transfer PaymentsNonfarm Proprietors' Income Farm Proprietors' IncomeOther Labor Income

$ B

illio

ns

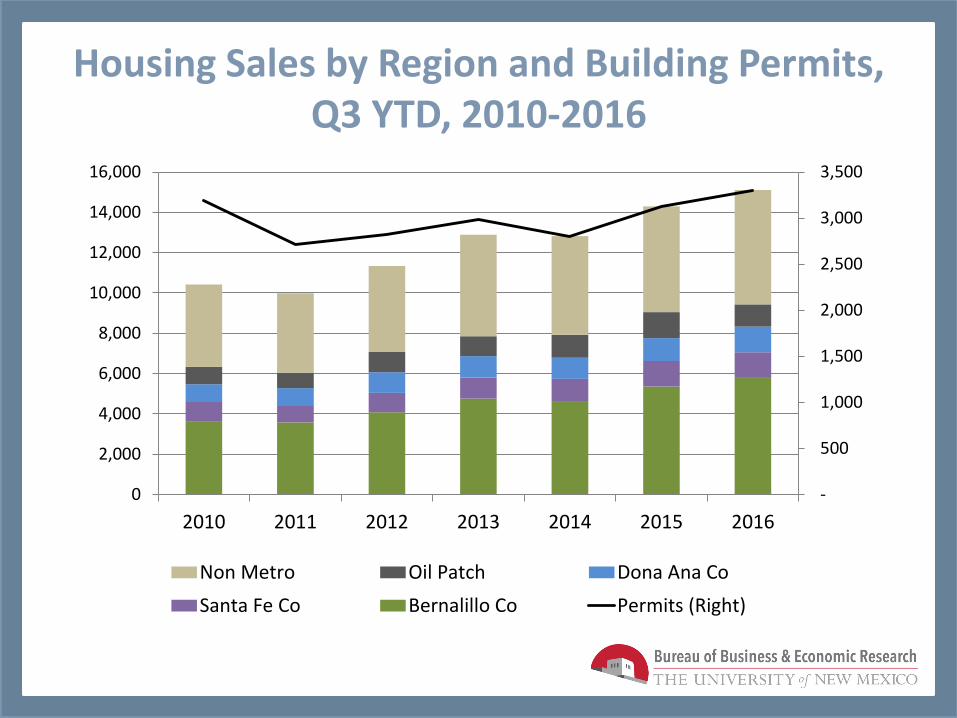

Housing Sales by Region and Building Permits, Q3 YTD, 2010-2016

-

500

1,000

1,500

2,000

2,500

3,000

3,500

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

2010 2011 2012 2013 2014 2015 2016

Non Metro Oil Patch Dona Ana Co

Santa Fe Co Bernalillo Co Permits (Right)

US & NM: Housing Starts & Permits

0.000

0.200

0.400

0.600

0.800

1.000

1.200

1.400

1.600

1.800

2.000

0.000

2.000

4.000

6.000

8.000

10.000

12.000

14.000

16.000

06 07 08 09 10 11 12 13 14 15 16 17 18 19 20

NM Housing Permits (Total) US Housing Start (Total)

Thousands, NM Millions, USA

Metro & Non-metro New Mexico

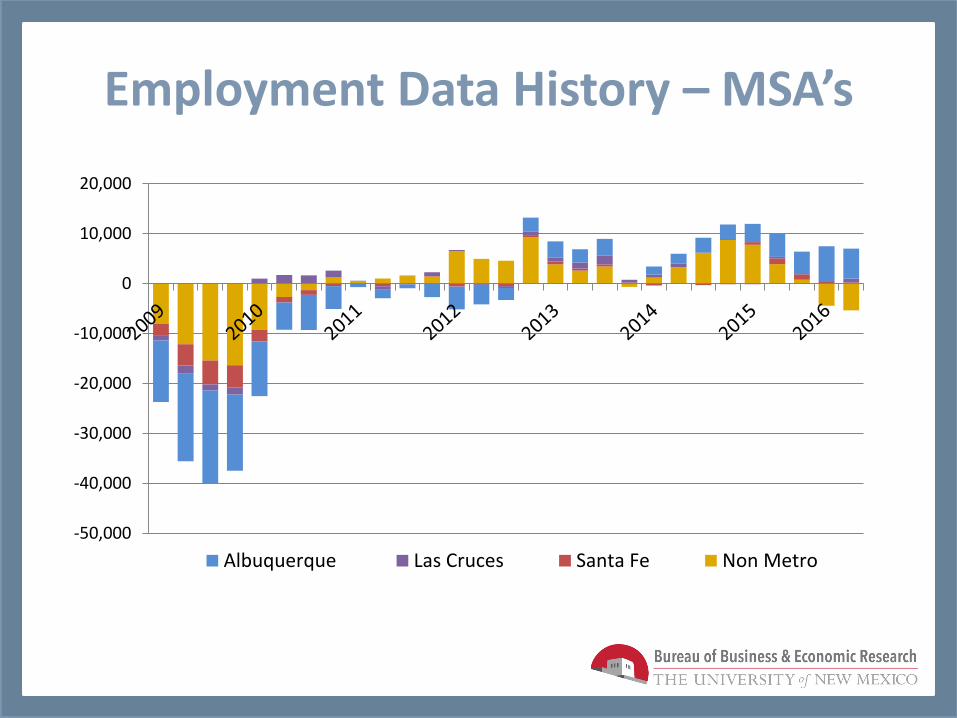

Employment Data History – MSA’s

-50,000

-40,000

-30,000

-20,000

-10,000

0

10,000

20,000

Albuquerque Las Cruces Santa Fe Non Metro

Job Creation by MSA, 2016-2020

-10,000

-5,000

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

Albuquerque Las Cruces Santa Fe Non Metro

Job

s

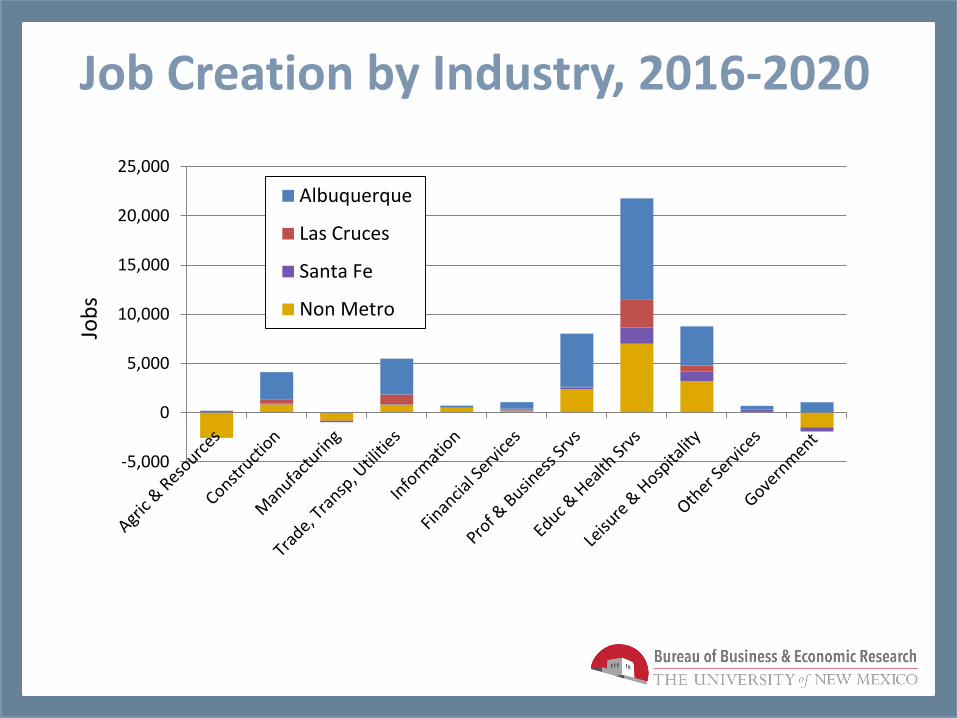

Government

Other Services

Leisure & Hospitality

Educ & Health Srvs

Prof & Business Srvs

Financial Services

Information

Trade, Transp, Utilities

Manufacturing

Construction

Agric & Resources

Job Creation by Industry, 2016-2020

-5,000

0

5,000

10,000

15,000

20,000

25,000

Job

s

Albuquerque

Las Cruces

Santa Fe

Non Metro

Questions / Comments?

18th Annual Data Users Conference Jeffrey Mitchell, BBER Director