22

The New World Order’s Perspective and Impact on the Global Market 1 September 2017 Anita Yadav Head of Fixed Income Research Emirates NBD

| Date post: | 01-Jul-2018 |

| Category: |

Documents |

| Upload: | hoangduong |

| View: | 222 times |

| Download: | 0 times |

The New World Order’s Perspective

and Impact on the Global Market

1September 2017

Anita YadavHead of Fixed Income Research

Emirates NBD

2

•An estimated four billion people live in cities, which is up by 23% on a decade

ago. In most of the global cities, supply is not keeping pace with demand for

both commercial and residential properties.

•Also continued technology innovation has increased the demand for business

hubs.

•As at 1Q this year, 490 million people reside in countries with negative interest

rates.

•Investment landscape has become volatile and therefore safe haven assets

are well bid.

•Beside oil prices, the factor that weighs on ME investor is the risk of the Trump

administration intervening in Syria, North Korea and Iran.

•Global real estate market peaked in 2015 and many cities now look over

valued.

Property Landscape

Emirates NBD, Global property guide

3

Flashback

Risks and uncertainty in 1H 2017….

Conservatives lose ground after snap election backfires….

Globally, the threat of a trade war becomes more real…

…. Weakening Brexit negotiating position.

• President Trump continued to accuse multiple countries of currency manipulation and unfair trade practices.

• FED raised interest rates twice (50 bps total), while BOC performed one hike (25bps).

• Despite market expectations, rhetoric from other central banks remains accommodating.

• Despite being regarded as a foregone conclusion, Prime Minister May’s snap election ended up in failure with the conservatives losing ground.

• This had a counter productive effect and weakened the UK’s Brexit negotiating position.

Emirates NBD, Bloomberg

The geopolitical environment remains unstable

4

5

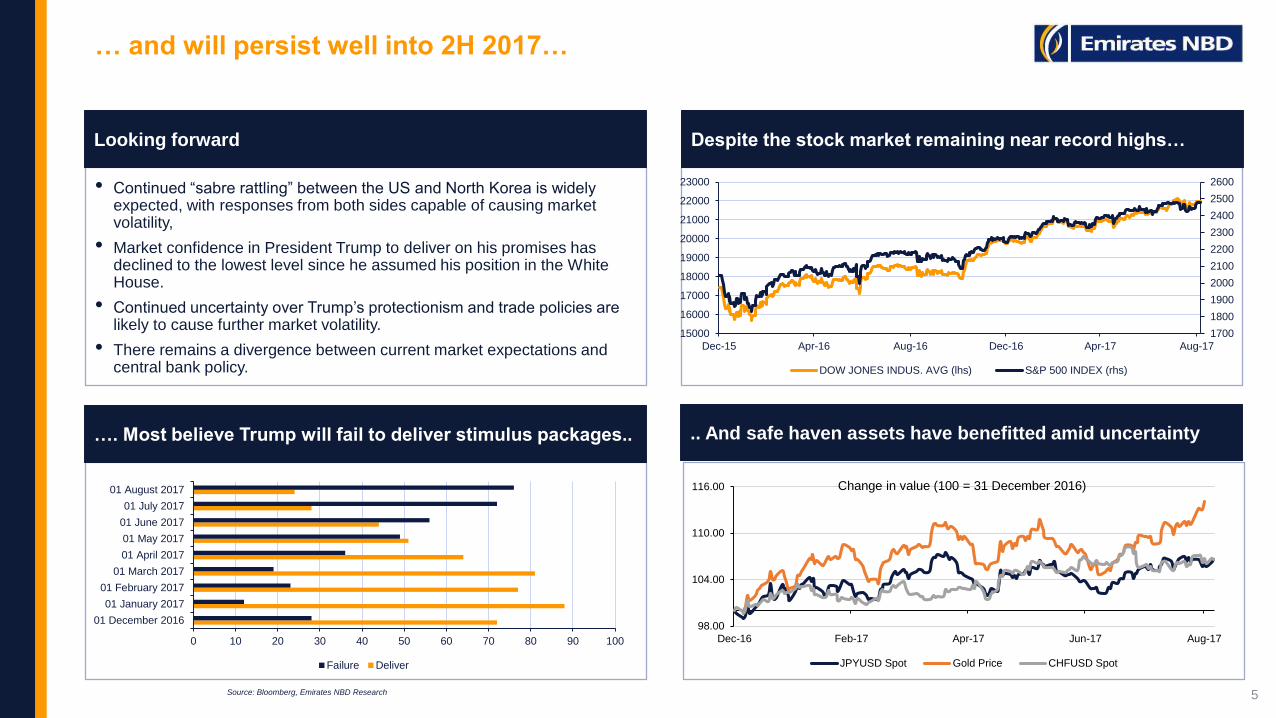

Looking forward

… and will persist well into 2H 2017…

• Continued “sabre rattling” between the US and North Korea is widely expected, with responses from both sides capable of causing market volatility,

• Market confidence in President Trump to deliver on his promises has declined to the lowest level since he assumed his position in the White House.

• Continued uncertainty over Trump’s protectionism and trade policies are likely to cause further market volatility.

• There remains a divergence between current market expectations and central bank policy.

…. Most believe Trump will fail to deliver stimulus packages..

Despite the stock market remaining near record highs…

.. And safe haven assets have benefitted amid uncertainty

Source: Bloomberg, Emirates NBD Research

0 10 20 30 40 50 60 70 80 90 100

01 December 2016

01 January 2017

01 February 2017

01 March 2017

01 April 2017

01 May 2017

01 June 2017

01 July 2017

01 August 2017

Failure Deliver

98.00

104.00

110.00

116.00

Dec-16 Feb-17 Apr-17 Jun-17 Aug-17

Change in value (100 = 31 December 2016)

JPYUSD Spot Gold Price CHFUSD Spot

1700

1800

1900

2000

2100

2200

2300

2400

2500

2600

15000

16000

17000

18000

19000

20000

21000

22000

23000

Dec-15 Apr-16 Aug-16 Dec-16 Apr-17 Aug-17

DOW JONES INDUS. AVG (lhs) S&P 500 INDEX (rhs)

6

• North Korean standoff continues to escalate

– Provocative rhetoric from all sides involved.

– Missile development and nuclear weapon tests continuing at unprecedented rate.

– Trump declaring “fire and fury” await further provocation.

• Brexit outcome continues to fog the horizon

– Snap UK general election backfired with the incumbent Conservative Party losing ground .

– Lack of progress with Brexit negotiations leaves much uncertainty.

– Labour party MPs likely to vote against the Repeal Bill at its second reading next week.

• Europe braces for populism

– 24 September: Germany election. Chancellor Angela Merkel’s CDU/CSU drops 0.5 pp to 36.5% with SPD also losing 0.5 pp to 23.5%, according to latest

poll commissioned by Bild newspaper (4th September 2017).

– 1 October: Catalan independence referendum.

– 20-21 October: Czech Republic election. Centre-left social democrats lagging in polls.

…as 2017 still has many risk events ahead.

7

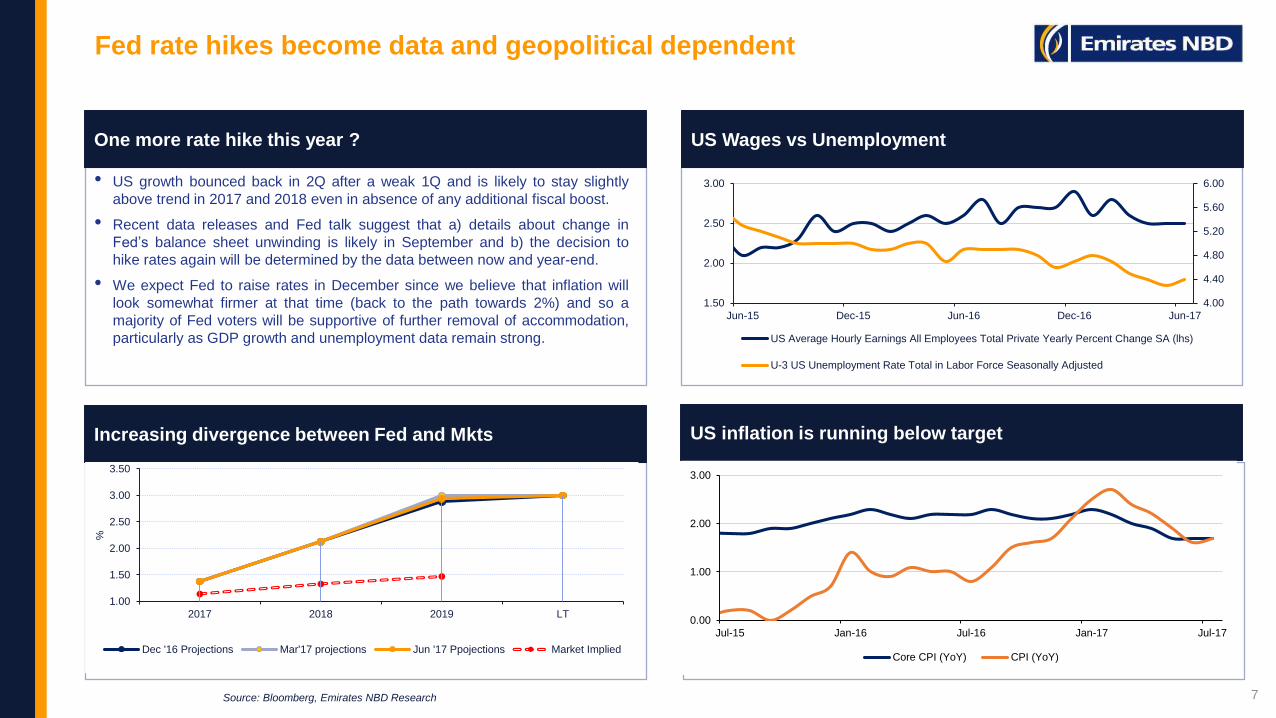

One more rate hike this year ?

Fed rate hikes become data and geopolitical dependent

• US growth bounced back in 2Q after a weak 1Q and is likely to stay slightly

above trend in 2017 and 2018 even in absence of any additional fiscal boost.

• Recent data releases and Fed talk suggest that a) details about change in

Fed’s balance sheet unwinding is likely in September and b) the decision to

hike rates again will be determined by the data between now and year-end.

• We expect Fed to raise rates in December since we believe that inflation will

look somewhat firmer at that time (back to the path towards 2%) and so a

majority of Fed voters will be supportive of further removal of accommodation,

particularly as GDP growth and unemployment data remain strong.

Increasing divergence between Fed and Mkts

US Wages vs Unemployment

US inflation is running below target

Source: Bloomberg, Emirates NBD Research

0.00

1.00

2.00

3.00

Jul-15 Jan-16 Jul-16 Jan-17 Jul-17

Core CPI (YoY) CPI (YoY)

4.00

4.40

4.80

5.20

5.60

6.00

1.50

2.00

2.50

3.00

Jun-15 Dec-15 Jun-16 Dec-16 Jun-17

US Average Hourly Earnings All Employees Total Private Yearly Percent Change SA (lhs)

U-3 US Unemployment Rate Total in Labor Force Seasonally Adjusted

1.00

1.50

2.00

2.50

3.00

3.50

2017 2018 2019 LT

%

Dec '16 Projections Mar'17 projections Jun '17 Ppojections Market Implied

8

Highlights

BoE and ECB stand unchanged

• In the UK, the currency-related inflation spike appears to have passed its peak

with July data showing drop in core inflation to 2.4% from 2.6% in May. GDP

growth also moderated from 2.0% in 1Q to 1.7% in 2Q. Softer data has given

breathing room to BoE and focus is now on Brexit process.

• The Eurozone’s economic growth is synchronised across the region with not

only the core doing well but also previously-struggling countries like Italy and

Portugal growing again. This in turn increases the likelihood that the ECB will

taper its asset purchases next year assuming no material negative impact on

growth from stronger currency. It is most likely to make this announcement in

October.

EUR appreciation lowers investor confidence

Eurozone inflation eases

UK real wages squeezed by higher prices

Source: Bloomberg, Emirates NBD Research Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

-0.30

0.20

0.70

1.20

1.70

2.20

Jul-16 Oct-16 Jan-17 Apr-17 Jul-17

Eurozone CPI (YoY)

-1.0

0.0

1.0

2.0

3.0

4.0

Jun-13 Dec-13 Jun-14 Dec-14 Jun-15 Dec-15 Jun-16 Dec-16 Jun-17

UK CPI (y/y) Avg Weekly Earnings (3m, y/y)

1.00

1.05

1.10

1.15

1.20

0

20

40

60

80

100

Aug-16 Nov-16 Feb-17 May-17 Aug-17

ZEW Germany Assessment of Current Situation ZEW Germany Expectation of Economic Growth

ZEW Eurozone Expectation of Economic Growth EURUSD Spot (rhs)

9

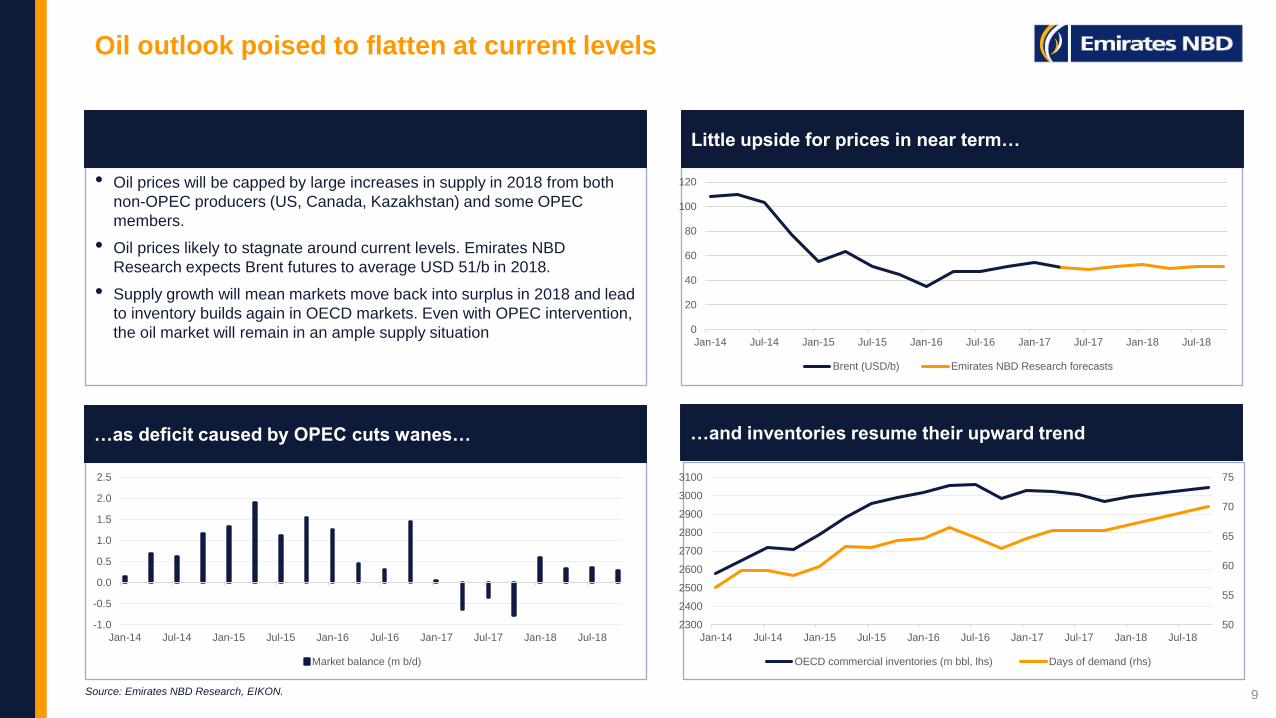

Oil outlook poised to flatten at current levels

• Oil prices will be capped by large increases in supply in 2018 from both

non-OPEC producers (US, Canada, Kazakhstan) and some OPEC

members.

• Oil prices likely to stagnate around current levels. Emirates NBD

Research expects Brent futures to average USD 51/b in 2018.

• Supply growth will mean markets move back into surplus in 2018 and lead

to inventory builds again in OECD markets. Even with OPEC intervention,

the oil market will remain in an ample supply situation

…as deficit caused by OPEC cuts wanes…

Little upside for prices in near term…

…and inventories resume their upward trend

Source: Emirates NBD Research, EIKON.

0

20

40

60

80

100

120

Jan-14 Jul-14 Jan-15 Jul-15 Jan-16 Jul-16 Jan-17 Jul-17 Jan-18 Jul-18

Brent (USD/b) Emirates NBD Research forecasts

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

Jan-14 Jul-14 Jan-15 Jul-15 Jan-16 Jul-16 Jan-17 Jul-17 Jan-18 Jul-18

Market balance (m b/d)

50

55

60

65

70

75

2300

2400

2500

2600

2700

2800

2900

3000

3100

Jan-14 Jul-14 Jan-15 Jul-15 Jan-16 Jul-16 Jan-17 Jul-17 Jan-18 Jul-18

OECD commercial inventories (m bbl, lhs) Days of demand (rhs)

10

Highlights

GCC Outlook: Growth to accelerate in 2018 on oil, infrastructure

GCC infrastructure projects by country, % of USD 1tn as of

August 2017

GCC real GDP growth (average)

Top 10 GCC projects (in execution), % of total

Source: MEED Projects, Emirates NBD Research Source : MEED Projects, Emirates NBD Research

• Headline GDP growth across the GCC is expected to slow in 2017,

largely on the back of OPEC production cuts. These are have been

extended through Q1 2018. However, from Q2 2018 we expect oil

production to recover in the GCC oil exporting countries, supporting

faster overall GDP growth

• Non-oil sector growth is also likely to accelerate in 2018, supported by

infrastructure and other investment.

• The total value of GCC projects (either in planning, execution and on

hold) reached USD 2tn in H1 2017. More than 50% of this is channeled in

infrastructure with UAE accounting for roughly half of total GCC spending

in the sector. Source: Bloomberg, Emirates NBD Research

3.2

3.8

2.3

1.1

2.8

1.0

1.5

2.0

2.5

3.0

3.5

4.0

2014 2015 2016e 2017f 2018f

% y

/y

Dubailand18.9%

King Abdullah Economic City (KAEC) - SA

17.7%Housing Project - SA

16.7%

Capital District11.1%

Jeddah Economic City -SA8.3%

Mohammed Bin Rashid (MBR) City7.5%

Lusail Development -Qatar5.3%

Duqm New Town -Oman5.0%

Yas Island Development

4.8%

Mecca Gate - SA4.7%

UAE46.7%

Saudi Arabia31.8%

Qatar6.7%

Kuwait6.6%

Oman5.1%

Bahrain3.1%

11

Highlights

Saudi Arabia: Extended OPEC cuts mean lower growth

Saudi PMI signals faster non oil growth

Oil output to remain lower in H2 2017

Monthly change in SAMA’s net foreign assets

Source: Haver Analytics, Emirates NBD Research

• We have revised our 2017 GDP growth forecast down to 0.5% as OPEC cuts have been

extended through Q1 2018. Growth is expected to accelerate to 2.5% in 2018 as oil output

rises next year.

• PMI data shows the non-oil sector has expanded at a faster rate ytd 2017 compared with the

same period in 2016.

• SAMAs net foreign assets have declined by nearly -USD 42bn in the year to July, signaling a

deficit in the Balance of Payments, despite higher oil prices and a successful sukuk issue.

BoP data for Q1 2017 shows a large negative ‘net errors and omissions’ figure, pointing to

capital flight.

• The Finance Ministry resumed domestic debt issuance from July.

Source: Bloomberg, Emirates NBD Research

-16.0

-14.0

-12.0

-10.0

-8.0

-6.0

-4.0

-2.0

0.0

2.0

4.0

Jan-16 Apr-16 Jul-16 Oct-16 Jan-17 Apr-17 Jul-17

US

D b

n

47

49

51

53

55

57

59

61

63

65

Jan-16 Apr-16 Jul-16 Oct-16 Jan-17 Apr-17 Jul-17

Headline KSA PMI New Orders Employment

9.4

9.6

9.8

10.0

10.2

10.4

10.6

10.8

Jan-16 Apr-16 Jul-16 Oct-16 Jan-17 Apr-17 Jul-17

mn b

/d

Saudi Arabia oil output KSA production target

12

Highlights

UAE: Growth should rebound in 2018

UAE bank loan and deposit growth

Oil output still a touch above agreed limit

UAE PMI shows faster non-oil growth

Source : Haver Analytics, Emirates NBD Research Source : Bloomberg, Emirates NBD Research

• GDP growth of 3% in 2016 exactly in line with our forecast. Key drivers

were oil & gas (3.8% y/y), transport & storage (7.4% y/y), manufacturing

(6.0% y/y) and construction (3.0% y/y).

• Oil production finally fell to the target agreed with OPEC in May but has

increased slightly since then. We have assumed full compliance in H2

2017 and Q1 2018, but expect oil production to rise through the rest of

2018. We forecast 2.0% GDP growth in 2017, rising to 3.4% in 2018.

• Non-oil sector growth remains robust, with PMI averaging 55.9 in Jan-

Aug, up from 53.8 in the same period 2016. However, employment

growth remains weak as firms’ margins remain under pressure.

Source: Bloomberg, Emirates NBD Research

2.4

2.6

2.8

3.0

3.2

Jan-16 Apr-16 Jul-16 Oct-16 Jan-17 Apr-17 Jul-17

mn b

/d

UAE oil output UAE production target

50

52

54

56

58

60

62

64

66

68

70

Jan-15 Jun-15 Nov-15 Apr-16 Sep-16 Feb-17 Jul-17

Output New Orders Employment

0

2

4

6

8

10

12

Jan-15 Jul-15 Jan-16 Jul-16 Jan-17 Jul-17

% y

/y

Loans and Advances Bank deposits

13

Highlights

Qatar: Downside risks while sanctions remain in place

Food inflation accelerates on sanctions

GDP growth

Growth in commercial bank deposits (by source)

Source : Haver Analytics, Emirates NBD Research Source : Bloomberg, Emirates NBD Research

• We have already downgraded our forecasts for Qatar’s GDP growth to

2.5% in 2017 and 3.5% in 2018. While the Qatari’s have found alternative

sources for food and materials from outside the GCC, the costs of these

imports have increased. The longer the sanctions remain in place, the

bigger the risk around Qatar’s readiness for FIFA World Cup in 2022.

• Qatari banks have seen an outflow of non-resident and resident private

sector deposits from the banking system. These have been offset by

increased deposits from the government/ public sector. Qatari banks have

reportedly been encouraged to source longer-term funding from outside the

GCC (ie Asia/ Europe). The cost of this funding is likely to be higher.

Source: Bloomberg, Emirates NBD Research

4.0

3.53.3

2.0

2.5

3.5

0

1

2

3

4

5

2013 2014 2015 2016e 2017f 2018f

% y

/y

-4.0

-2.0

0.0

2.0

4.0

6.0

Jan-16 Jun-16 Nov-16 Apr-17

% y

/y

CPI Food & beverages

-30

10

50

90

130

170

Jan-16 Apr-16 Jul-16 Oct-16 Jan-17 Apr-17 Jul-17

% y

/y

Private public non-residents

14

Highlights

Egypt

Egyptian Pound

FX Reserves

Source : IHS Markit, Emirates NBD Research Source : Haver Analytics, Emirates NBD Research

• IMF has disbursement a total of USD 4bn to date. IMF program has underpinned

fiscal and other reforms including subsidy cuts, VAT, fx devaluation. This,

together with high interest rates have attracted significant foreign portfolio

inflows.

• Headline PMI rose to 48.9 in August, its highest reading in over a year. While the

index still shows deteriorating conditions in the non-oil economy, the severity of

the contraction has eased significantly since Q4 2016.

• Inflation remains high at 33% y/y in July on weaker EGP and higher energy,

utility costs, but should ease in 2018 off a high base. .

Source: Bloomberg, Emirates NBD Research

Egypt Purchasing Managers’ Index

35.0

40.0

45.0

50.0

55.0

60.0

Jan-16 Apr-16 Jul-16 Oct-16 Jan-17 Apr-17 Jul-17

PMI Index New Export Orders

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

Jan-16 Apr-16 Jul-16 Oct-16 Jan-17 Apr-17 Jul-17

5

10

15

20

25

30

35

Jan-11 Jul-12 Jan-14 Jul-15 Jan-17

US

D b

n

15

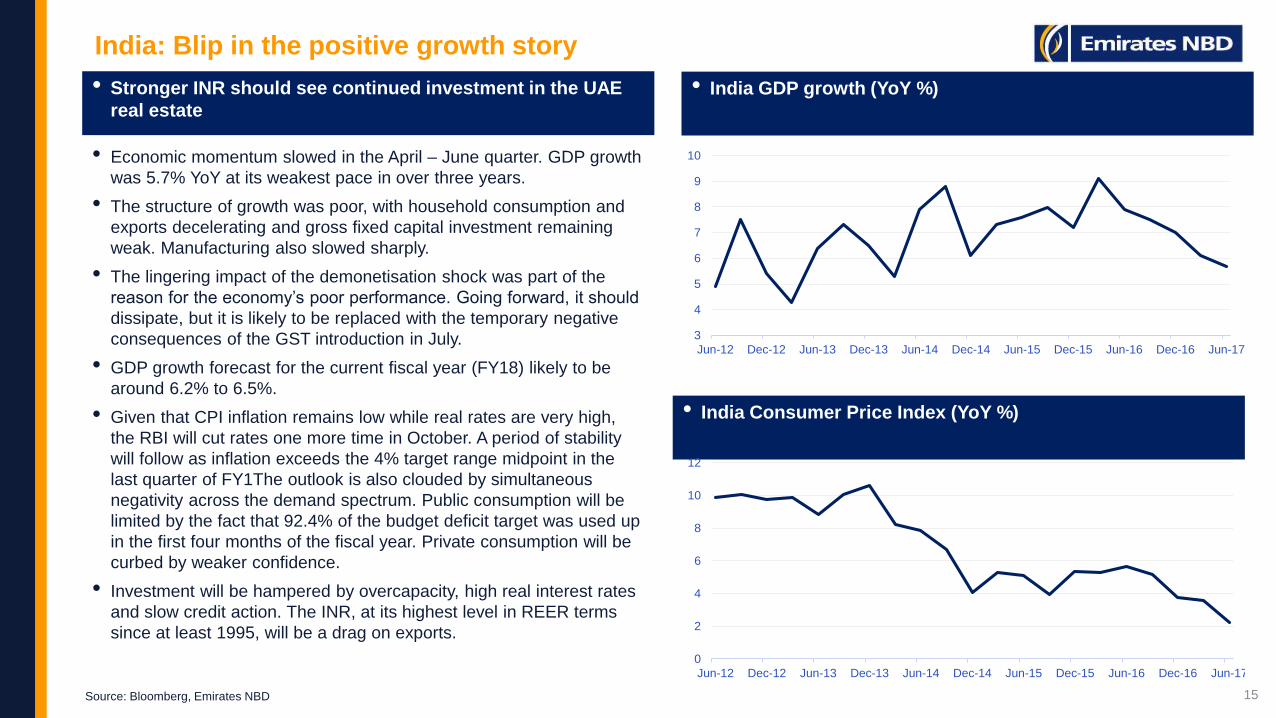

• Economic momentum slowed in the April – June quarter. GDP growth

was 5.7% YoY at its weakest pace in over three years.

• The structure of growth was poor, with household consumption and

exports decelerating and gross fixed capital investment remaining

weak. Manufacturing also slowed sharply.

• The lingering impact of the demonetisation shock was part of the

reason for the economy’s poor performance. Going forward, it should

dissipate, but it is likely to be replaced with the temporary negative

consequences of the GST introduction in July.

• GDP growth forecast for the current fiscal year (FY18) likely to be

around 6.2% to 6.5%.

• Given that CPI inflation remains low while real rates are very high,

the RBI will cut rates one more time in October. A period of stability

will follow as inflation exceeds the 4% target range midpoint in the

last quarter of FY1The outlook is also clouded by simultaneous

negativity across the demand spectrum. Public consumption will be

limited by the fact that 92.4% of the budget deficit target was used up

in the first four months of the fiscal year. Private consumption will be

curbed by weaker confidence.

• Investment will be hampered by overcapacity, high real interest rates

and slow credit action. The INR, at its highest level in REER terms

since at least 1995, will be a drag on exports.

India: Blip in the positive growth story

Source: Bloomberg, Emirates NBD

• India GDP growth (YoY %)

• India Consumer Price Index (YoY %)

3

4

5

6

7

8

9

10

Jun-12 Dec-12 Jun-13 Dec-13 Jun-14 Dec-14 Jun-15 Dec-15 Jun-16 Dec-16 Jun-17

0

2

4

6

8

10

12

Jun-12 Dec-12 Jun-13 Dec-13 Jun-14 Dec-14 Jun-15 Dec-15 Jun-16 Dec-16 Jun-17

• Stronger INR should see continued investment in the UAE

real estate

16

Interest Rates impact Real estate

Bloomberg

0

1

2

3

4

5

6

7

0

50

100

150

200

250

300

350

400

DJUSRE Index (R1) FDTRMID Index (L1)

17

UAE: Lending to Construction and Real Estate

Source: Phidar Advisory, UAECB

204.4

212.6

235.0

264.7 267.0

-40

-20

0

20

40

60

80

50

100

150

200

250

300

2013 2014 2015 2016 Q1 2017

Construction and Real Estate, AED bn (LHS) Construction and Real Estate, y/y growth (RHS)

y/y growthAED bn

18

Dubai apt prices (per sqft)

Global house prices

Euro area House Price Index

US House Price Index

UK House Price Index

Bloomberg, Emirates NBD

300

310

320

330

340

350

360

370

380

390

400

94

96

98

100

102

104

106

Mar-12 Sep-12 Mar-13 Sep-13 Mar-14 Sep-14 Mar-15 Sep-15 Mar-16 Sep-16 Mar-17

300

320

340

360

380

400

420

440

500.0

800.0

1100.0

1400.0

1700.0

2000.0

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

19

Investment in Dubai Real Estate, USD bn.

Bloomberg, Emirates NBD, JLL

7.1

5.4

4.4

2.72.5 2.4

2.2

10.1

5.7

3.3 3.3

1.6

2.2

1.6

1.2

5.9

0

2

4

6

8

10

12

UAE Indian Non-GCC UK Saudi Arabian Other GCCMENA

Pakistani Rest

2015 2016

20

Dubai Real Estate Investment by Nationality

Bloomberg, JLL

UAE24.6%

India13.4%

Saudi Arabia8.2%

UK5.9%Pakistan

4.6%

Jordan2.8%

Egypt2.7%

China2.1%

USA1.9%

Lebanon1.8%

Rest32.0%

Phidar 9/5 House Price index

Dubai: Softness in residential real estate prices continues in Jan-Aug 2017

with apartment prices faring better than villas

Rents declined at a slower rate

With transaction volumes easing (9/5 Index)

While yields remain high in August 2017

Source: Phidar Advisory, Emirates NBD Research

-18

-15

-12

-9

-6

-3

0

3

6

Jan-15 Jun-15 Nov-15 Apr-16 Sep-16 Feb-17 Jul-17

% y

/y

Apartments Villas

-13

-11

-9

-7

-5

-3

-12

-10

-8

-6

-4

-2

0

2

Jan-15 Jun-15 Nov-15 Apr-16 Sep-16 Feb-17 Jul-17

% y

/y

Apartments (LHS) Villas (RHS)

4.0

4.2

4.4

4.6

4.8

5.0

5.2

5.4

6.4

6.8

7.2

7.6

8.0

8.4

Jan-15 Jun-15 Nov-15 Apr-16 Sep-16 Feb-17 Jul-17

Apts Yields (LHS) Villas Yields (RHS)%

0

20

40

60

80

100

120

140

0

100

200

300

400

500

600

Jan-14 Aug-14 Mar-15 Oct-15 May-16 Dec-16 Jul-17

Apartments (LHS) Villas (RHS)

DisclaimerThe material in this presentation is general background information about Emirates NBD's activities current at the date of the presentation. It is information given

in summary form and does not purport to be complete. It is not intended to be relied upon as advice to investors or potential investors and does not take in to

account the investment objectives, financial situation or needs of any particular investor. These should be considered, with or without professional advice when

deciding if an investment is appropriate.

The information contained here in has been prepared by Emirates NBD. Some of the information relied on by Emirates NBD is obtained from sources believed to

be reliable but does not guarantee its accuracy or completeness.

Forward Looking StatementsIt is possible that this presentation could or may contain forward-looking statements that are based on current expectations or beliefs, as well as assumptions

about future events. These forward-looking statements can be identified by the fact that they do not relate only to historical or current facts. Forward-looking

statements often use words such as anticipate, target, expect, estimate, intend, plan, goal, believe, will, may, should, would, could or other words of similar

meaning. Undue reliance should not be placed on any such statements because, by their very nature, they are subject to known and unknown risks and

uncertainties and can be affected by other factors that could cause actual results, and the Group’s plans and objectives, to differ materially from those expressed

or implied in the forward-looking statements.

There are several factors which could cause actual results to differ materially from those expressed or implied in forward looking statements. Among the factors

that could cause actual results to differ materially from those described in the forward-looking statements are changes in the global, political, economic, business,

competitive, market and regulatory forces, future exchange and interest rates, changes in tax rates and future business combinations or dispositions.

Emirates NBD undertakes no obligation to revise or update any forward looking statement contained within this presentation, regardless of whether those

statements are affected as a result of new information, future events or otherwise.

Important Information

22