The Organization of Innovation Across Countries and Industries Sharon Belenzon y Patrick Bolton z Ulya Tsolmon x January 11, 2013 Abstract This paper examines the relationship between ownership, corporate form, and innovation for a cross-section of private and publicly traded innovating rms in the US and 15 European countries. A novel observation emerges from our analysis: while most innovating rms in the US are publicly traded conglomerates, a substantial fraction of innovation is concentrated in private rms and in corporate group a¢ liates in conti- nental European countries. We nd virtually no variation across US industries in the organizational form of innovating rms, but substantial variation across industries in continental European countries, where corporate groups tend to be concentrated in industries with a slower and more fundamental innovation cycle. Our ndings are consistent with the Coasian view of rm organization where rms choose the corpo- rate form most conducive to innovation. This is especially true in Europe, where there are fewer regulatory hurdles to the formation of hybrid organizational forms. Keywords: innovation, patents, conglomerates, corporate groups JEL Classication: O31, O32, O16 1. Introduction While large conglomerates, such as GE, IBM, and DuPont, are often viewed as the leaders among innovative rms, venture capitalbacked startups such as Facebook and Google are also strong models of cohesive and focused structures of entrepreneurial standalones. Venture capital plays a less prominent role in Europe than in the United States; however, innovative activity in diversied corporate groups such as Ericsson, Zeiss, Alstom and Novartis is still highly notable. While there are many extremely innovative, diversely organized rms, and various organizational theories highlight di/erent structural factors critical to innovation, there is no systematic study of how the structure of innovating rms varies across industries and countries. This paper argues that the organization structure most conducive to innovation varies with the characteristics of technology, which dictates the relative advantages and costs of di/erent corporate forms. We present new Acknowledgement: We thank Ashish Arora, Tomer Berkovitz, Luca Enriques, Daniel Ferreira, Ronald Gilson, Hideshi Itoh, Joshua Lerner, Marvin Lieberman, Randall Morck, Joanne Oxley, Daniel Paravisini, Katharina Pistor, Luis Rios, and Daniel Wolfenzon for helpful comments. All remaining errors are our own. y Fuqua School of Business, Duke University. z Graduate School of Business, Columbia University. x Fuqua School of Business, Duke University.

Transcript

The Organization of Innovation Across Countries and Industries∗

Sharon Belenzon† Patrick Bolton‡ Ulya Tsolmon§

January 11, 2013

Abstract

This paper examines the relationship between ownership, corporate form, and innovation for a cross-sectionof private and publicly traded innovating firms in the US and 15 European countries. A novel observationemerges from our analysis: while most innovating firms in the US are publicly traded conglomerates, asubstantial fraction of innovation is concentrated in private firms and in corporate group affi liates in conti-nental European countries. We find virtually no variation across US industries in the organizational formof innovating firms, but substantial variation across industries in continental European countries, wherecorporate groups tend to be concentrated in industries with a slower and more fundamental innovationcycle. Our findings are consistent with the Coasian view of firm organization where firms choose the corpo-rate form most conducive to innovation. This is especially true in Europe, where there are fewer regulatoryhurdles to the formation of hybrid organizational forms.

Keywords: innovation, patents, conglomerates, corporate groups

JEL Classification: O31, O32, O16

1. Introduction

While large conglomerates, such as GE, IBM, and DuPont, are often viewed as the leaders among innovative

firms, venture capital—backed startups such as Facebook and Google are also strong models of cohesive and

focused structures of entrepreneurial standalones. Venture capital plays a less prominent role in Europe than

in the United States; however, innovative activity in diversified corporate groups such as Ericsson, Zeiss,

Alstom and Novartis is still highly notable. While there are many extremely innovative, diversely organized

firms, and various organizational theories highlight different structural factors critical to innovation, there

is no systematic study of how the structure of innovating firms varies across industries and countries. This

paper argues that the organization structure most conducive to innovation varies with the characteristics of

technology, which dictates the relative advantages and costs of different corporate forms. We present new

∗Acknowledgement: We thank Ashish Arora, Tomer Berkovitz, Luca Enriques, Daniel Ferreira, Ronald Gilson, HideshiItoh, Joshua Lerner, Marvin Lieberman, Randall Morck, Joanne Oxley, Daniel Paravisini, Katharina Pistor, Luis Rios, andDaniel Wolfenzon for helpful comments. All remaining errors are our own.†Fuqua School of Business, Duke University.‡Graduate School of Business, Columbia University.§Fuqua School of Business, Duke University.

empirical patterns of innovation and organizational structure across countries and industries using compre-

hensive firm-level data on firms in 15 European countries and the United States. By drawing upon existing

theories on innovation and organization, we show that the patterns are largely consistent with a Coasian

perspective of firm organization. We find that the organization of inventive activity in Europe systematically

varies with underlying technological features of the industry, but not in the United States or Great Britain.

Differences in the pursuit of innovation almost surely underlie the huge variations in productivity across

establishments, firms, and countries. In the US, with the same input, manufacturing plants at the 90th

percentile of the productivity distribution produce on average almost twice as much output as plants at the

10th percentile (Syverson, 2004). Only recently have scholars been able to rely on high-quality, firm-level data

to systematically analyze the factors behind these differences in productivity. These data-rich studies point

to several general factors, such as capital and labor unobserved heterogeneity, trade openness, and managerial

practices (see Syverson, 2010, for an excellent survey). Large and persistent disparities in productivity across

countries have also been attributed to differences in corporate governance and corporate law (Jones and

Romer, 2009). However, these studies have not been linked directly to differences in innovation. The goal of

this paper is to take one further step toward understanding the relationship between institutional differences,

organizational forms, and corporate performance across countries by exploring a comprehensive cross-country,

firm-level data set linking innovation and corporate structure.

Following Williamson (1975) and Chandler (1962, 1977, 1990), economists and business scholars have

pointed to the advantages of centrally managed organizations in managing and funding R&D and in marketing

and distributing new products, while corporate finance scholars have pointed to the benefits of internal

capital markets in lowering the cost of capital for R&D (Gertner, Scharfstein and Stein, 1994; Stein, 1997;

Belenzon and Berkovitz, 2010). These studies suggest that integrated and coordinated internal markets can

be superior for innovation. Research on emerging markets adds to the "bright-side" of internal markets by

emphasizing institutional benefits for firm performance in general (Khanna and Palepu, 1997; Khanna and

Rivkin, 2001) and for innovation in particular (Mahmood and Mitchell, 2004; Chang, Chung and Mahmood,

2006). Conversely, other studies emphasize the "dark side" of internal markets and suggesting the importance

of control and incentives in effective allocation of resources and employee motivation. Explanations for internal

market liabilities include reduced financial discipline for mediocre investments (Scharfstein and Stein, 2000;

Meyer, Milgrom, and Roberts, 1992; Rajan, Servaes, and Zingales, 2000) and less promising R&D projects

(Guedj and Scharfstein, 2004; Seru, 2012), organizational limitations including the reluctance to cannibalize

existing competencies in periods of disruptive innovations (Tushman and Anderson, 1986; Tripsas, 1997),

the over-reliance on existing knowledge (Rosenkopf and Almeida, 2003; Song, Almeida and Wu, 2003) that

results in an unwillingness to integrate new knowledge ("not-invented-here" syndrome), and an inability to

recognize and exploit external knowledge due to a lack of absorptive capacity (Cohen and Levinthal, 1990).

Such mixed evidence on which organizational form is optimal for the effi cient functioning of internal markets

calls for a closer examination of patterns of organizational structure. In this paper, we show that the nature

of technology, as well as the country institutional context, largely dictate the balance of trade-offs between

centrally managed coordination and distributed control.

2

We use a descriptive "just-the-facts" approach motivated by theory. We examine three distinctive organi-

zational forms– standalone firms, conglomerates, and corporate groups– each exhibiting specific governance

characteristics, and focus on the degree of centralization within each structure. The autonomy of standalone

firms offers the highest level of intellectual property rights protection– the ability of inventors to control and

appropriate the returns to their innovations (Teece, 1986; Cohen et al., 2000), resulting in robust incentives–

but standalone firms suffer the most from external financing constraints. Conglomerate divisions have access

to the conglomerate’s resources through internal markets, but intellectual property created by divisions is con-

trolled by headquarters and can be mobilized at the headquarters’discretion. Thus, centralized control and

the resulting weak property-rights regime create a relatively low-incentive environment in conglomerates. In

contrast, sharper boundaries between affi liates of corporate groups allow individual affi liates to retain greater

control of their resources, especially when external parties own equity in the affi liate (a common practice in

continental Europe). This results in both stronger incentives in affi liates through better intellectual property

rights protections, and access to the group’s resources. However, the greater decentralization of corporate

groups comes at the cost of more rigid internal markets because involvement of external parties in affi liates

(through equity, debt, or other contractual relations) imposes constraints and costs on resource mobilization.

Our basic argument therefore is that corporate groups should have a more decentralized structure than

conglomerates, because corporate group affi liates are incorporated as separate legal entities and often have

outside owners. These outside owners impose substantial constraints on headquarters’resource-mobilization

discretion, as well as guarantee credible measures of performance at the affi liate level on the basis of which

high-powered incentives can be established. Using variation across technologies, we aim to tease out benefits

and costs associated with decentralization. Consistent with Coasian logic, we expect a greater share of

innovation in decentralized structures, such as partly owned affi liates of corporate groups, in industries where

the benefits from decentralization are more significant. This should be especially true in countries where

barriers to forming corporate groups are low.

We base our analysis on a comprehensive data set of both private and publicly traded American and

European firms and match all corporate patents granted by the United States Patent and Trademark Offi ce

(USPTO) and the European Patent Offi ce (EPO) to these firms. We have identified about 64,000 firms (legal

entities) that hold at least one patent from the EPO or USPTO. Of these firms, about 60% are American,

11% German, 8% British, 4% French, and 5% Italian. We matched 776,030 USPTO and 532,894 EPO

patents. 73% of USPTO patents and 33% of EPO patents are held by American corporations. Germany

appears to be the most innovative European country, holding 12% and 28% of USPTO and EPO patents,

respectively. We sort the firms in our sample into four organizational categories using detailed ownership-

structure data: standalones, headquarters, and wholly owned and partly owned affi liates, listed by degree

of decentralization. Our empirical operationalization of organizational forms is more continuous along the

decentralization dimension: standalones directly correspond to the conceptual category of most centralized

standalone firm structure, headquarters and wholly owned affi liates capture the diverse semi-autonomy of

conglomerates, and partly owned affi liates represent the most decentralized structure of corporate groups.

Several novel findings emerge from our analysis. First, while the overall distribution of citations-weighted

3

USPTO patents by ownership structure in the whole sample is 18% standalones, 61% headquarters, and 21%

affi liates, in the United States this distribution is skewed toward standalones and headquarters, with 20%

and 66% respectively of patents falling in these categories, and only 14% of patents being held by affi liates.

In Europe, meanwhile, 50% of the patents are held by affi liates, and 10% and 40% respectively are held by

standalones and headquarters. There is also wide variation in organizational form across European countries.

While Germany resembles the United States in terms of concentration of innovation in headquarters (58%),

French and Italian firms are clearly skewed toward affi liates, with only 13% and 8% of their respective patents

being held by headquarters.

Second, we distinguish between affi liates that are wholly owned by their parent company and those with

minority shareholders. The presence of minority shareholders in an affi liate company establishes a separation

between the affi liate and its parent company in terms of retained profits, patent holdings, and resource

reallocation. In the United States less than one percent of patents are held by partly owned affi liates, while

in France and Italy about 20% of innovation takes place in affi liates with minority shareholders. Great Britain

has a unique structure, with 55% of British patents held by affi liates (as compared to only 14% of American

patents), but effectively all of these affi liates are wholly owned subsidiaries.

Third, we find substantial variation in organization structure across industries in continental Europe, but

not in the United States and Great Britain. In continental Europe, affi liates, especially partly owned, tend to

be concentrated in industries where innovation takes longer to complete and is less certain but has a higher

potential payoff. These innovative activities may be more vulnerable to hold-up problems and require greater

intellectual property rights protection for the innovator. In contrast, conglomerates are more prevalent

in industries with rapid, complex innovations, where the ability of conglomerates to identify the relevant

innovation and quickly redeploy assets may give this organizational form an edge over corporate groups.

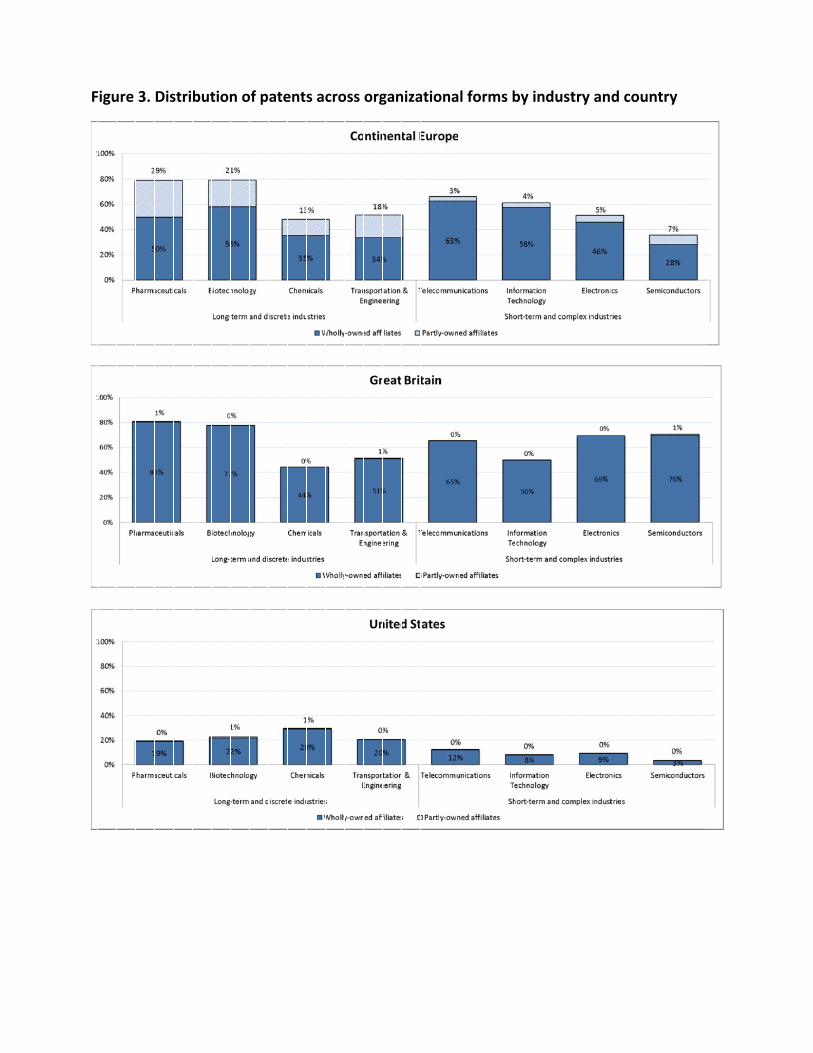

For example, in Pharmaceuticals, partly owned affi liates hold close to 30% of the patents in continental

Europe but only 1% of patents in the United States and Great Britain. In the Telecommunications sector,

however, partly owned affi liates are rare, holding only 3% of continental European patents and less than 1%

of American and British patents. Thus, in more dynamic industries we do not observe substantial differences

in the way innovation is organized between continental Europe and the United States and Great Britain.

There may, of course, be reasons besides governance why we see this cross-industry pattern in organi-

zational form. For example, organizational capabilities in marketing new products and adapting quickly to

new economic conditions may also explain this cross-industry variation. Thus, our findings of high central-

ization of inventive activity in industries with a rapidly changing economic environments are consistent with

and reinforce organization flexibility theories (Daft, 1998). Governance and flexibility are inherently related,

as stronger governance builds upon decentralized decision-making and greater autonomy of corporate unit

managers (Aghion and Tirole, 1997). Similarly, flexibility in terms of frequent resource reallocation may

affect ex-ante incentives by inducing divisional managers to invest in more short-term projects (Seru, 2012;

Lerner and Wulf, 2007). Intellectual property rights and organizational form are also complements with

respect to the commercialization of inventions. In industries where commercialization is achieved at a more

aggregate level, by combining several interrelated inventions, the owner of a patent to a single invention may

4

be more vulnerable to hold-up problems by the organization. Put differently, high-powered incentives in the

form of equity stakes in a partly owned subsidiary is likely to be less effective in such industries. We would

then expect the centralized conglomerate organizational form to emerge in these industries and to see other

incentive mechanisms to induce R&D than intellectual property rights.

It is important to emphasize the limitations of our empirical approach. While theory clearly distinguishes

between discrete organizational forms, empirically, such sharp distinctions are diffi cult to make in a systematic

manner. We measure innovation using patents and then track how these are assigned to firms. We infer

organizational structure using inter-firm ownership ties, although we acknowledge that other dimensions,

such as social ties, are also likely to characterize links between firms. Developing more fine-grained measures

of internal structures of large organizations by harnessing new comprehensive data on ownership structures

and innovation indicators (which are becoming more rapidly available) is clearly a challenge for future work.

We note finally that our findings are broadly consistent with a Coasian view of firm organization– firms

choose the organizational form best suited to fostering innovative activities. The alternative, dominant view

in the literature on groups, especially when discussing complex partly owned structures with significant

separation between ownership and control, is that organizational form is chosen by entrenched managers or

controlling shareholders to suit their best interests at the expense of minority shareholders and overall firm

effi ciency (Bertrand et al., 2002; Morck et al., 2005). By this latter view it is not obvious that one should see

any systematic difference in organization form in a given country across industries.

2. Governance and Innovation

Organizational structure "involves how a firm is organized and governed, and how decisions actually are

made and carried out" (Nelson, 1991). The organizational form could be effi ciency-based, which means a

firm chooses the organizational form best suited to its goals and strategy (Coase, 1937; Williamson, 1975;

Chandler, 1962), or institutionally-driven, a view that holds external influences, such as legal, resource, and

social factors, shape firm structure (DiMaggio and Powell, 1983; Haunschild and Miner, 1997). We integrate

these two broad views and show that the interaction of the institutional environment and firm strategy

explains the patterns of innovation across industries and countries.

We distinguish between standalone firms, conglomerates, and corporate groups, and discuss unique fea-

tures and relative advantages and disadvantages of each form for innovative processes. While previous studies

on centralized and decentralized organizational forms typically contrast unified functional structures with mul-

tidivisional forms (e.g., Williamson, 1975; Nickerson and Zenger, 2002; Siggelkow and Levinthal, 2003), we

primarily compare the degree of centralization of conglomerates and corporate groups, focusing on relative

levels of flexibility and incentives for innovation in each form of governance. Due to the voluminous nature

of research in the separate fields of organization and innovation, we do not intend to provide a complete

review of the literature, and thus we purposefully keep our discussion concise and focus only on the most

important points specific to the context of this paper. Importantly, while we recognize the empirical diversity

of organizational structures, our theoretical framework distinguishing organizational forms into three distinct

5

categories deliberately keeps these distinctions sharp and parsimonious in order to highlight the effects of

key dimensions associated with different forms of innovative activities. In our empirical analysis, however,

we utilize more continuous measures of centralization.

2.1. Conglomerates

Perhaps the most studied organizational form is the American conglomerate, which consists of large multi-

unit firms operating in several industries (Amihud and Lev, 1981; Porter, 1987; Teece, 1982; Peteraf, 1993;

Chatterjee and Wernerfelt, 1991; Robins and Wiersema, 1995). A classic model of a conglomerate is an

"M-form" organization, where headquarters formulates and coordinates strategic direction for specialized

divisions (Chandler, 1962; Berle and Means, 1932). The larger size of conglomerates offers greater and more

diverse resources than otherwise would be available within a single division. These resources are redistributed

through conglomerate’s internal markets, guided by company headquarters, which ensure timely deployment

of critical resources to any part of the organization. An internal market allows organizations to mobilize

internal resources from one unit to another. Internal markets can operate similarly to external markets, where

prices regulate transactions, or they can be coordinated without prices by authority within the hierarchy. In

the following theoretical discussion we single out two main features of divisions that should strongly affect

the way in which internal markets operate: legal independence and the measurement of performance. We

also emphasize two characteristics that distinguish conglomerates from corporate groups.

The first distinguishing feature of conglomerates is the legal integration of their divisions. Unlike stand-

alone firms or business units of a corporate group, divisions of a conglomerate are not registered as legal

entities apart from their parent company. Legal independence may have important implications for decen-

tralization of control and overall resource mobilization, especially if that independence is associated with

greater direct interaction between divisions and external parties. Legally incorporated divisions can form

direct contracts with other firms, independently issue debt, and even sell equity. For non-incorporated divi-

sions, these activities are performed centrally by headquarters. To the extent that forming direct contractual

or ownership relations with external parties introduces friction to the process of resource mobilization, legal

status should have important implications for how internal markets operate. For instance, the presence of

minority owners in a legally independent unit should strongly affect the ability of headquarters to mobilize

resources to and from this affi liate. Because the rights of minority owners are protected, especially in the

developed countries we focus on in this paper, any internal transaction involving a partly owned unit has to be

contractual. Contractibility adds direct costs of negotiation and drafting contracts, but it can also decrease

incentives by headquarters to mobilize resources to and from partly owned units (Grossman and Hart, 1986;

Aghion and Tirole, 1994; Belenzon et al., 2012). Conversely, tight legal integration which eliminates potential

frictions to resource mobilization caused by outside stockholders allows for the quick and timely distribution

of resources to any part of the organization.

The second distinguishing feature of conglomerates is the measurement of division performance. Accurate

measurement of output in team production is critical to avoiding free-rider problems, and according to trans-

action cost economics logic it is a central mechanism driving firm boundaries (Alchian and Demsetz, 1972;

6

Jensen and Meckling, 1976; Jensen, 1986). Although divisional structure allows top management to reward

managers based on business unit performance relative to functional units in standalone firms (Williamson,

1991), individual divisions do not disclose independent financial reports, especially when they are not incor-

porated. Even for conglomerates that utilize internal accounting systems aimed at disaggregating earnings to

the level of each profit center, such systems are likely to be vulnerable to opportunism and not be externally

enforceable (Williamson, 1991; Rajan, Servaes, and Zingales, 2000; Galunic and Eisenhardt, 2001). Thus, a

lack of disaggregated performance measures (combined with costly monitoring) results in a weakened link be-

tween performance and rewards and reduction in incentive intensity facing divisional managers (Williamson,

1975; Holmstrom, 1999). Additionally, greater intervention by headquarters in resource mobilization can

further distort incentives for individual divisions to innovate, as in the absence of a reliable accounting sys-

tem, profits generated by own innovations may be reallocated elsewhere, and other critical resources (such as

intellectual property and human capital) could be redeployed (Seru, 2012).

Incentives are especially important for innovation in the context of long-term investments with highly

uncertain payoffs. Several studies emphasize how low-powered incentives in conglomerates may affect inno-

vation. The evidence is mixed. The general conclusion coming from the strategy field is that centralization

is associated with stronger incentives for long-term risky innovation, and decentralization is better suited

for more applied research. For example, Cockburn et al. (1999) find that intensity of incentives for applied

research is lower in organizations where decision-making authority is centralized, due to differing monitoring

systems in centralized and decentralized structures. Lerner and Wulf (2007) find similar evidence emphasizing

the superiority of centralized structures for setting up incentives for longer-term risky projects. While not

addressing incentives directly, Arora et al. (2012) use data on patent assignment to systematically infer the

internal structure of R&D for large American corporations and present strong evidence of a negative rela-

tionship between basic research and decentralization. Using survey data, Argyres and Silverman (2004) find

a similar relationship– centralized R&D is less applied and generates innovations that build on a wider range

of technologies and are of higher impact. On the other hand, finance scholarship emphasizes the "dark side"

of centralization, where agency problems and "corporate socialism" are seen as major sources of ineffi ciency.

For example, Seru (2012) finds that publicly traded American conglomerates with above-average realloca-

tion of funds across divisions are less productive innovators than comparable standalone firms. Guedj and

Scharfstein (2004) compare clinical trials in the biopharmaceutical industry and find that big pharmaceutical

firms engaged in cancer research tend to initiate too many studies but are quicker to terminate unpromising

research than smaller (standalone) biotech firms.

To summarize, conglomerates have two distinct features, which are central to our analysis: lack of legal

status for divisions and profit consolidation, both of which allow conglomerates to develop and utilize internal

markets. These internal markets play a central role in shaping incentives for innovative activities and the

degree of coordination among units. Centralized structures with low-powered incentives can contribute to

effective interdivisional coordination but can be costly in terms of controls on division-level decision-making

and performance. Legal integration and the diffi culty in measuring division-level performance may make

hierarchy-based internal markets more effi cient than price-based internal markets, especially in industries

7

where fast mobilization of resources is necessary. Since establishing performance evaluation metrics for

each price-based exchange requires significant time and effort on the part of headquarters compared to

discretionary allocations, lack of prices can contribute to more flexible and responsive internal markets in

centralized structures. Thus, they can prove to be advantageous for firms where fast reallocation of resources

is important.

2.2. Corporate Groups

Accounts of business groups in emerging markets (Caves and Uesaka, 1976; Strachan, 1976; Leff, 1978;

Ghemawat and Khanna, 1998) and corporate groups in developed markets (Faccio and Lang, 2002; Faccio, et

al., 2010; Belenzon and Berkovitz, 2010; Belenzon et al., 2012) have highlighted the prevalence and economic

significance of collections of legally independent firms linked by social and ownership ties and controlled by an

ultimate owner. Corporate groups feature firm-like centralized coordinated control by the ultimate owner and

varying degrees of market-like transactions between the affi liates (Khanna and Palepu, 1997; Granovetter,

2005; Khanna and Yafeh, 2007), and thus have blurred the traditionally sharp boundaries between markets

and hierarchies described by transaction cost economics (Coase, 1937; Williamson, 1975).

The study of corporate groups highlights the firm-like feature of mutual ties, which facilitate effi cient

reallocation of resources within the group (Guillén, 2000; Khanna and Palepu, 1999; Belenzon and Berkovitz,

2010), provide cross-subsidies to distressed affi liates, and utilize internal markets to substitute missing or

dysfunctional external institutions (Leff, 1978; Khanna and Palepu, 1997; Khanna and Rivkin, 2001), with

positive effects on innovation in particular (Mahmood and Mitchell, 2004; Chang, Chung and Mahmood,

2006). Another stream of research, primarily in the context of developing economies and family-controlled

groups, highlights the negative features of corporate groups, such as utilization of group structure for diverting

cash flows from affi liates with minority owners– "tunneling" (La Porta et al., 1997, 1999; Johnson et al., 2000;

Bertrand et al., 2002; Bae et al., 2002; Morck et al., 2005), and building indirect ownership arrangements

to control more affi liates– "pyramiding" (Almeida and Wolfenzon, 2006; Barca and Becht, 2001; Claessens

et al., 2000, 2002; Chang, 2003). Recent debates suggest that the findings of these studies highlighting

the "negative" side of corporate groups may be subject to reinterpretation, and remain largely inconclusive

(Bebchuk et al., 2000; Khanna and Yafeh, 2007).

In this paper we single out unique features of corporate groups that make them more decentralized than

conglomerates. We focus on the relative independence of group affi liates and explain how it may be related

to the organization of inventive activity. Following the preceding discussion on conglomerates, we emphasize

legal independence and credible division performance as the main distinguishing features of decentralization

of corporate groups relative to conglomerates.

Perhaps the most important difference between a group affi liate and a division of a conglomerate is the

legal status of affi liates. As discussed above, while divisions of conglomerates do not usually have a separate

legal identity, corporate group affi liates are incorporated as distinct legal entities. This allows an affi liate to

behave much like a standalone firm: it can sell equity to outside investors (as well as issue debt and form

independent contracts), form its own board of directors, and file separate unconsolidated financial reports–

8

actions that are not available to conglomerate units. The legal independence of affi liates generates a functional

and organizational separation between affi liates and the rest of the group. Of course, this separation is not

discrete and is likely to vary substantially along many dimensions (Belenzon et al., 2012, present a detailed

analysis of this issue). However, compared to conglomerates, corporate groups should be more decentralized

as indicated by the degree of functional separation and relative autonomy of decision-making.

This decentralization within corporate groups results in their internal markets functioning more like

external markets, which are primarily coordinated by prices rather than hierarchy. The separation between

ownership and control is especially pronounced in groups that have affi liates with outside stockholders.

Unlike division managers of conglomerates, minority owners are highly protected by country legal institutions.

Thus, disputes involving group affi liates can be taken to courts, unlike internal disputes of a conglomerate

(Williamson, 1991). As a result, shared ownership reduces the flexibility of internal markets in groups, so

moving resources between affi liates is typically associated with more friction than moving resources between

conglomerate divisions.

On the other hand, unconsolidated financial reports and the presence of minority owners ensure that

resources and profits generated by the affi liate would not be shifted to another unit without proper com-

pensation. Measurement of performance at the affi liate level is therefore separable and credible, particularly

where misrepresentation of actual performance in a partly owned affi liate is a violation of minority shareholder

rights. This allows affi liate managers to be compensated directly on the basis of unit-level performance– very

similar to the high-powered incentives managers in venture capitalist—backed standalone firms face. More-

over, as an independent legal entity, an affi liate can assign the patents it generates to itself, and the presence

of minority owners ensures that intellectual property rights are assigned to the inventing unit. Thus, control

over own resources and greater transparency of measured outcomes in affi liates contribute to high-powered

incentives for innovation and lower free-riding tendencies in corporate groups.

The corporate group structure, especially in partly owned affi liates, introduces an interesting trade-off

that to the best of our knowledge has not been systematically addressed in previous research. On one hand,

prices can drive imperfect coordination and exchange in the internal markets of corporate groups– especially

when partly owned affi liates are involved. On the other hand, these rigidities in the internal markets provide

stronger incentives for innovation. In the next section we argue that this trade-off relies on the nature of

innovation: faster-paced, more complex innovation would benefit more from the flexibility and coordination

inherent in conglomerate internal markets, and slower, more discrete innovation would benefit more from the

constrained but incentive-intensive internal markets of corporate groups.

It is important to emphasize that in our empirical analysis, partial ownership represents one of the highest

forms of decentralization, where external regulations protecting minority owners necessitate price-mediated

transactions closely resembling the exchanges in external markets. While we focus the theoretical discussion

and empirical analysis on partly owned affi liates to illuminate the decentralized organizational form, we also

recognize that wholly owned affi liates display a wide variation in the degree of their independence, and that

other factors can contribute to organizational cohesion and centralization. However, data constraints do not

allow us to systematically observe and measure such independence in wholly owned affi liates. Thus, our

9

analysis is limited to variations in ownership structure. Alternative and more subtle ways to discriminate the

degree of organizational decentralization are left for future research.

2.3. Standalone Firms

Standalone firms are independent entities with no controlling equity ties to other firms. They are the most

autonomous form of organization in terms of both legal status and performance measurement, as their

interaction with other firms is entirely market-based rather than mediated through centralized coordination.

This ownership structure provides the strongest incentives to innovate, as the owners have direct and large

stakes in the future profits the firm generates. This is especially true when managers hold equity stakes in

their firms. As such, the incentives among different owners are largely aligned, and agency problems are

likely to be mitigated due to strong governance in the form of tight monitoring and high-powered incentives

(Holmstrom, 1989).

On the other hand, standalone firms do not have access to extensive internal markets. They rely primarily

on external markets for resources, and therefore are more vulnerable to fluctuations and frictions in their

environments compared to conglomerates and corporate group affi liates (Himmelberg and Peterson, 1994;

Stein, 1997). Standalone firms may have diffi culty raising capital for risky and uncertain R&D, sourcing

human capital and technologies for innovative activities, and developing timely commercialization of innova-

tions. These constraints would be magnified if external capital and labor markets are ineffi cient and the legal

environment provides weak enforcement of intellectual property protection.

In the proceeding analysis, a standalone structure is contrasted with the more complex structures of

conglomerates and corporate groups mainly on its relative prevalence across countries and industries. Due

to the lack of extensive internal markets in standalones, the primary structural trade-offs we are interested

in are between conglomerate and corporate group forms, which is the focus of the next section.

3. The Nature of Innovation

We consider two industry dimensions which we identify as key drivers of the trade-offs discussed in the

previous section. These dimensions are how discrete or complex innovations are in the industry, and how

fast or slow the innovation cycle is in the industry. We consider how these characteristics affect the relative

advantage of each organizational form.

3.1. Complex vs. Discrete

We classify industries as complex or discrete from a commercialization standpoint and determine how internal

markets interact with the nature of technology. Products in industries with complex innovations comprise a

set of multiple components integrated into a coherent whole, while products in discrete industries require fewer

elements. Product complexity in this categorization is a matter of degree, and closely aligns with the concept

of architectural innovation, which distinguishes between core technological knowledge within each component

and architectural knowledge about the relationship between the individual components (Henderson and Clark,

10

1990). Complex products require both core knowledge within each technology and integrative knowledge of

how technologies fit together, but discrete products rely less on integrative knowledge due to fewer components

that make up the final product.

Each type of innovation introduces tradeoffs in organizational form along two main dimensions: cost of

coordination and incentives. We contend that firms producing complex products are likely to benefit from

centralized structures, because they can economize on coordination costs through centralized management

and design alternative incentive structures to mitigate weakened unit-level incentives. On the other hand, co-

ordination between units is less critical for discrete products, and linking effort directly to unit-level outcomes

is more feasible, thus decentralized structures are better suited for commercializing discrete products.

Costs of coordination can increase with product complexity. Commercializing complex innovations en-

tails a larger degree of integrative knowledge and greater communication and coordination between various

organizational units. Since firms can economize on information processing by specializing in particular types

of information within each internal unit, it becomes more costly for firms producing complex products to

delegate both component-specific and integrative functions to individual units (Arrow, 1974; Bolton and

Dewatripont, 1994). In order to allow individual units to focus on their own knowledge domains, centralized

governance can take on the coordination role and utilize internal markets to facilitate effi cient transfer and

combination of knowledge and resources (Amit and Schoemaker, 1993; Dierickx and Cool, 1989; Mahoney

and Pandian, 1992; Peteraf, 1993; Teece, Pisano, and Shuen, 1997). Thus, centralized coordination can better

foster knowledge spillovers across divisional boundaries (Teece, 1982). Consistent with these notions, Argyres

and Silverman (2004) confirm that firms with centralized coordination of innovative activities typically pursue

research encompassing a broader range of technological areas than firms with more decentralized structures.

Since complex product innovation combines inputs from several distinct technological and functional areas,

the process can blur the link between effort and performance, and therefore result in weaker incentives, reduced

individual effort, and increased free-riding (Williamson, 1975; Holmstrom and Milgrom, 1994). Thus, typical

unit-level incentive structures are not as effective in commercializing complex products. Instead, centrally

coordinated research efforts can mitigate measurement problems by taking on the responsibility for initiatives

and outcomes and using promotion-based incentives to encourage collaboration (Cockburn, Henderson and

Stern, 1999). Consistent with this notion, from a licensing standpoint, Arora et al. (2012) show that

for narrower and focused technologies, licensing decisions will be decentralized and delegated to business

units, while licensing authority of more general-purpose technologies will be centralized at headquarters

level, because business unit-level incentives are insuffi cient for licensing such technologies. Therefore, a high

degree of legal integration combined with centralized decision-making and resource allocation processes make

conglomerate structures more advantageous than other organizational forms in industries where significant

internal recombination and coordination are important to commercialize a product.

On the other hand, when innovation is discrete, there are fewer distinct components to combine for a

final product, thus internal coordination across units is not as critical. Firms can economize on information

processing by delegating product-specific knowledge management to individual units. At the same time,

low interdependency of inputs across units creates a tighter link between inputs and outcomes within units,

11

making stronger incentive regimes more valuable for discrete products than integrated internal markets.

Thus, decentralized structure of corporate groups is more conducive to development of discrete innovations,

because it allows unit-level specialization without high degree of integration across units and offers an overall

stronger unit-based incentives environment than conglomerates, especially where minority owners are present.

Stronger incentives within group affi liates stem from two main factors. First, the greater independence of

affi liates offers a stronger link between effort and outcomes, resulting in an incentive regime appropriate for

discrete technology. Second, affi liates are further incentivized to exert effort because relative immobility of

their resources, such as intellectual property assigned to the inventing affi liate, allows them to appropriate

the returns from their own innovations.

Overall, our discussion points to a clear advantage of integration and aggregation when innovation is

complex, and strong advantages to decentralization and disaggregation when innovation is more discrete.

3.2. Long vs. Short Innovation Cycles

The length of an innovation cycle can have important consequences for the types of innovations pursued by

different organizational forms. Some technologies take much longer to develop than others, requiring greater

and prolonged commitment of resources. Products with lengthy development phases do not generate imme-

diate cash flows, and the outcomes of long-term projects are typically highly uncertain, making investments

into these types of innovations highly risky. Standalone firms that depend primarily on external markets

for resources would face greater diffi culties obtaining commitment of external funding for long-term risky

projects. In contrast, organizational forms with active internal markets have an advantage in industries

with longer innovation cycles, as they can invest internal funds in these types of projects and commit their

resources for an extended period of time.

We argue that corporate groups should be better positioned to support innovations with longer develop-

ment cycles than conglomerates. This is for two reasons. First, better measurability of affi liate performance

in corporate groups allows for the effective evaluation of the long-term performance of a unit, because transi-

tory shocks are less confounding over extended milestones of a project than for innovations that are assessed

more frequently and therefore can be subject to random shocks in demand and technology. Second, legal

independence of affi liates results in more rigid internal markets in corporate groups than in conglomerates,

which can be advantageous when the need to redeploy resources is infrequent but greater control and stability

of resources is critical, as when the innovation cycle is long.

When the innovation cycle is short, the need for readjustment of resources is likely to be more frequent,

in which case having a frictionless internal market would be more valuable (Teece and Pisano, 1994; Teece

et al., 1997). Highly integrated and flexible internal markets of conglomerates allow fast recombination and

transfer of resources in response to investment opportunities (Aghion and Tirole, 1997). When uncertainty

arises from frequent disturbances, gains from effective internal market coordination can offset incentive losses

associated with highly integrated and consolidated internal markets (Williamson, 1991; 1995). The winner-

picking advantage of conglomerates would be especially strong in industries with a faster pace of technology

change (Stein, 1997). Thus, the centralized conglomerate form may provide an advantage in industries with

12

short innovation cycles.

In sum, it is clear that different organizational forms present complex trade-offs regarding innovative

activities. The Coasian perspective of firm organization predicts clear advantages of decentralized organi-

zational forms, such as corporate groups, in industries where technologies are more discrete and that have

longer development cycles. On the other hand, more centralized organizational forms, such as conglomerates,

should have an advantage in industries where technologies are more complex and innovation has shorter

development cycles– making resource recombination more frequent.

3.3. Country Institutions

While we argue that the choice of organizing innovative activity depends largely on industry characteristics,

such as the degree of product complexity and pace of technology development, institutional context can

shape and limit the flexibility of firms’choice (Milgrom and Roberts, 1992; Hall and Soskice, 2001). In some

cases, strong traditions of industrial and university research determine national or regional technological

specialization, which can influence the types of innovation firms engage in and consequently dictate the

predominance of certain organizational forms (Freeman, 1995). In other cases, the legal environment can

provide a safe haven for or severely limit some governance structures (La Porta et al., 1999). In this section

we briefly discuss how variations in institutional contexts across our sample countries are likely to mediate

or obscure industry effects on organizational form, despite similarities including the countries’ degrees of

economic and regulatory development.

Three institutional factors are particularly relevant: development of external factor markets, the degree

of legal protection of minority owners, and tax regulations favoring or discriminating against certain organi-

zational forms. First, where factor markets are lacking, internal markets become more important (Gertner,

Scharfstein and Stein, 1994; Himmelberg and Peterson, 1994; Stein, 1997). Thus, conglomerates and affi liates

of corporate groups gain advantage over standalone firms where access to external capital and specialized

labor, for example, is more challenging. Second, legal protection of minority owners against expropriation

strengthens the autonomy of partly owned affi liates of corporate groups and thereby contributes to greater

decentralization within groups (La Porta et al., 1999). Greater independence of affi liates in corporate groups

becomes an advantage in industries where decentralization and the resulting stronger incentives at the unit

level are more important for innovation. However, the independence and unit-based incentives can become a

liability in industries where flexibility and greater coordination among units are necessary. Third, in countries

with additional taxes on intercompany dividends– income transfers among group affi liates– organizing as a

corporate group becomes more costly. For example, in the United States, dividend income transferred from

a subsidiary to the parent company is subject to an additional 7.5 percent tax (Morck, 2005). A similar tax

does not apply to conglomerates who are allowed to consolidate their earnings, and these taxes on intra-group

transactions do not exist in Europe. As illustrated, variations in institutional factors can significantly affect

organizational choices, distorting the effects of the nature of technology on organizational form.

13

4. Data

Our paper combines data from several sources: (1) firm and ownership data from Amadeus for European

firms and from Icarus for American firms (both are provided by Bureau van Dijk), (2) information on patents

from the United States Patent and Trademark Offi ce (USPTO), and (3) the European Patent Offi ce (EPO).

The Bureau van Dijk data, which has comprehensive cross-sectional coverage, is collected from various

government sources in Europe. We have name and address information for practically all firms in Europe

and the United States, which we use in matching patents. However, these data have several limitations.

First, in some European countries, reporting of financial information is not mandatory for very small firms.

For example, in Great Britain, companies with fewer than 10 employees do not have to report financial

information, such as sales and number of employees, in their annual reports. In France, on the other hand, all

firms are obligated to report financial information. To mitigate this selection issue, we make no restrictions

on the availability of financial items when including firms in our sample. Moreover, as our goal is to map

inventive activity across organization forms, it is unlikely that the observed pattern would be driven by

very small firms, as the vast majority of patents are generated by large corporations. Second, ownership

information is central to our analysis. Should ownership coverage vary systematically across countries, then

our findings may be biased.

A priori there is no reason to suspect that the ownership data is systematically biased. The ownership

data is collected by a large international team of researchers and analysts that track company reports, news,

and other public sources that provide ownership information. There are about 4 million firms in our data

for which ownership information is available (these firms are included in the ownership algorithm described

below). However, there still may be some noise in our ownership data, especially for smaller firms, that

may potentially bias our findings. To mitigate the potential measurement bias, we hand-collect ownership

information on the top 20 companies for the major countries in our sample from financial reports and various

public sources. We confirm that the data for these firms as reported by Bureau van Dijk is accurate, and that

the same patterns we observe for the whole sample also holds for the restricted sample of large corporations.

We also randomly check the information provided by Bureau van Dijk for numerous firms by directly accessing

company houses in different countries as well as firm websites. Again, we find very few discrepancies between

the Bureau van Dijk data and the information from public sources.

4.1. Ownership

While our theoretical discussion clearly distinguishes between organizational forms, empirically, such sharp

distinctions are diffi cult to make in a systematic manner. Since we do not observe various types of innovations

and internal divisions, we measure innovation using patents and track how these patents are assigned to

firms. We infer organizational structure using inter-firm ownership ties. We utilize these ties to systematically

measure the degree of centralization in various organizational structures. Specifically, in the empirical analysis

we emphasize the continuum of centralization measured by ownership structure and examine the pattern of

independence and inventive activity across industries and countries.

14

The Amadeus and Icarus data sets contain detailed information on direct ownership links between firms.

We sort firms into four different categories based on their ownership structure: (i) standalones, (ii) headquar-

A firm is categorized as a standalone if it has no equity ties to any other firm, as a headquarters if it is at

the apex of a group of firms, as a wholly owned affi liate if a parent company owns 100% of its shares, and as

a partly owned affi liate if it has both a parent-company controlling-shareholder and minority shareholders.

The diversity of organizational forms complicates sorting of firms into conceptual categories. Conglom-

erates that operate solely internal, legally integrated divisions are empirically indistinguishable from unitary

functionally organized standalone firms, and conglomerates with external, legally independent divisions re-

semble corporate groups with wholly owned affi liates. Since making clear distinctions between standalone,

conglomerate, and corporate group structures is very diffi cult to do systematically in the data, we utilize

variation in ownership structure to create a more continuous measure of firm-level centralization that allows

us to examine patterns of innovative activity across industries and countries along this dimension.

The operationalization of standalone firms corresponds directly with the theory, but it is important

to reiterate that this empirical categorization does not distinguish between unitary functionally organized

standalone firms and multidivisional firms, in which all divisions are internal and are not separate legal entities.

Thus, the standalone category represents the most centralized structure. Headquarters represents the next

most centralized structure and is conceptually equivalent to conglomerates with legally independent divisions.

Wholly owned affi liates represent a form between centralized and decentralized structures, since they are

entirely owned and controlled by their ultimate owner, but they are more independent, as they are legally

separate from their ultimate owner. In the context of our analysis there is little difference between a division

of a conglomerate and a wholly owned subsidiary1,2, with each representing a semi-decentralized structure.

Partly owned affi liates are the most decentralized form in our analysis, as they are legally independent from

their ultimate owner and also have minority owners. The presence of minority shareholders in an affi liate

company establishes a sharper separation between the affi liate and its parent company in terms of retained

profits, patent holdings, and resource reallocation. Thus, partly owned affi liates are most representative of

the corporate group structure discussed in the theory section. Exploiting variation in the ownership structure

allows us to operationalize conceptually distinct yet empirically murky organizational forms in a much more

systematic and continuous manner than has otherwise been possible in the literature.

To fully characterize the ownership structure of firms in our sample, we use ownership link information

for private and public American and European firms from the ownership section of the 2008 version of Icarus

and Amadeus. To ensure that all ownership links represent control, we take the following steps: i) for private

1The case of wholly owned affi liates can be potentially studied in the context of delegated authority, lying somewhere betweenno control (the employee case) and full control (the owner case). Quoting Oliver Hart (1995): “If firm A buys firm B andconverts it into a wholly owned subsidiary, then it is often argued that the managers of firm B have more control and authority(‘independence’) than if firm A merges with firm B.”

2Future research should extend our model to allow for informal delegation. Examples include: (i) Centralized personnelmanagement and its career-oriented administration make it diffi cult for the HQs to differentiate and isolate internal divisionsin terms of pay, status, transfers, etc. (ii) Subsidiaries are apparently treated differently from internal divisions. There aredifferences in terms of pay, status, and future career prospects between internal divisions and subsidiaries. (iii) Both employeesand communities tend to accept differential treatments across legal boundaries.

15

subsidiaries, we keep only links where the shareholder has at least 50% of the voting rights, and ii) for public

firms we keep only links where the shareholder has at least 20% of the voting rights. This leaves us with close

to one million ownership links.3 To infer group structure from these links, we use the algorithm developed

and described in Belenzon and Berkovitz (2010). This algorithm constructs corporate ownership chains and

groups together firms controlled by the same ultimate owner.4

Some of the affi liated firms in our sample, especially those that are wholly owned, have no substantial

economic activity and exist only for tax or accounting reasons. To avoid including economically insignificant

firms that may influence the classification of firms as standalones and headquarters, we classify a firm as

headquarters only if it has affi liates with real economic activity (in determining whether a firm controls other

firms, we include both innovating and non-innovating firms); we do so by excluding affi liates that generate less

than $1 million in annual sales and employ fewer than 20 employees. Moreover, as the goal of this paper is to

explore stable organizational forms, we exclude groups that are held by private equity and other investment

institutions, as well as joint ventures. The sample we end up with has 63 percent standalones, 11 percent

To create a firm-level measure of innovation, we examine patent-based indicators of technological advances by

firms. We use patent data to measure innovative activity because we do not have direct information on R&D

expenditures for private firms. Our patent data builds upon Belenzon and Berkovitz (2010), who matched

EPO and USPTO patents to the complete set of Amadeus firms. We extend their data to include American

firms by matching patents to Icarus, and update the European matching to include patents granted up to

2007. For the USPTO, our source of information is an updated version of the NBER file which covers the

period 1975—2007.

For the EPO, our main information source is the 2007 publication of the PATSTAT database, which is

the standard source for European patent data and is published by the OECD. This database contains all

European patent applications and granted patents from the beginning of the EPO system in 1978 to 2007.

For each USPTO and EPO patent document we have information on the name of the firm to which the

patent is assigned as well as the firm’s address. We match the name and the address fields from the patent

3Erring on the side of caution, we define control of a private firm as ownership at least 50% of the firm’s voting rights (excludingnon-voting shares). Following previous literature on public firms (La Porta et al., 1999; Faccio and Lang, 2002; and others),which have a more dispersed ownership, we set the threshold for control of a public firm at 20%. All our results are robust todifferent numbers for these thresholds.

4We conduct several robustness tests to check the sensitivity of our findings to ownership assumptions. For control assumptions,the same pattern of results continues to hold for ownership thresholds of 40% and 25% for private firms, and 10% for public firms.Furthermore, we construct corporate group structures using the algorithm developed by Almeida, Yong Park, Subrahmanyam,and Wolfenzon (2007) (AYPSW). The advantage of AYPSW over our algorithm is that it better deals with cases of cross-holdings(e.g., firm A owns 50% of firm B, and firm B owns 50% of firm A); however, our algorithm better handles very large ownershipdata sets and is more robust to missing ownership links. For reasons of computational power we are not able to run the AYPSWalgorithm on our full set of firms. Although restricting the sample is problematic, the general pattern that emerges highlyresembles the one generated by our algorithm. While cross-holdings are prevalent in East Asian countries, where the AYPSWalgorithm was first implemented, we find that cross-holdings are very rare in Europe. Only 0.01% of the ownership chains ouralgorithm generates are associated with some form of cross-holdings. In the vast majority of cases with cross-holdings, they donot involve the ultimate owner; thus, the classification of firms to the different organizational form categories is not affected.

16

document to the name and address fields in Amadeus and Icarus. To control for patent quality, we weight

patents by the number of citations they receive, excluding self-citations (that is, a citation from one patent

to a predecessor patent that is held by the same citing firm), in a period of five years after they are granted.

Using a short citation lag allows us to avoid truncation problems that are associated with comparing patents

of different ages. However, we examine the sensitivity of our results to longer citation lags, and find practically

the same pattern of results when using citation lags of five, ten, and twenty years. We control for cohort

and technology area effects using the weighting scheme proposed by Trajtenberg (1990). For each patent, we

divide the number of citations it receives by the average number of citations received by all patents granted

at the same year and classified under the same three-digit technology class.

It is important to note that we make no restrictions on the availability of accounting information for our

sample firms. That is, every firm that was matched to the patent data sets is included in our analysis. While

the coverage of accounting information is likely to vary across countries, especially for very small firms, the

coverage of names and addresses is constant across countries regardless of firm size. The general pattern of

results continues to hold when we exclude firms for which we have no accounting information, or firms with

less than 20 employees (this threshold tends to reduce differences in coverage across countries).5,6

Figure 1 demonstrates the variation we aim to capture with our data. The top portion of Figure 1

illustrates the corporate structure and the assignment of patents for IBM. It is clear from this figure that

almost all patents that IBM generates are assigned to headquarters (the apex firm). IBM appears to be highly

integrated, with most of its units held internally, while the most economically significant of its 195 legally

independent subsidiaries are wholly owned by the headquarters. The wholly owned incorporated units are

assigned a negligible fraction of IBM’s patents. In contrast, the second figure illustrates the Nestle corporate

group, which exhibits a much more decentralized structure. The Nestle group includes 431 legally independent

units, many of which are partly owned and demonstrate significant economic activity, as indicated by sales

and patenting. Unlike IBM, the apex firm Nestle does not own many of the group patents, but instead the

partly owned affi liate L’Oreal holds the majority of patents in the group.

5Although we do not exclude firms from our sample if they do not report financial information, some interesting observationsemerge from examining only firms for which financial information is available. Standalone firms tend to be substantially smallerthan conglomerates and partly owned affi liates, which do not differ much in size. The average standalone firm has 177 employees(a median of 20), and about $100 million in annual sales (a median of $8.3 million). The average conglomerate has 3,650 employees(a median of 136), and $918 million in annual sales (a median of $14.3 million). The average partly owned affi liate has 2,400employees (a median of 214), and about $1 billion (a median of $65 million). Comparing conglomerates to partly owned affi liates,the different in mean size (annual sales) is not significant (a t-stat of -0.482).

6On average, firms in our sample hold 15 USPTO patents and 10 EPO patents. Groups also hold on average more USPTOpatents than EPO patents: 686 and 609, respectively. The US firms hold more than 3 times more USPTO patents than EPOpatents (20 versus 6), but the patents assigned to US groups are spread more evenly between USPTO (686 patents) and EPO(523 patents). While firms in Great Britain hold more EPO patents (7 versus 5), groups in Great Britain hold more USPTOpatents than EPO patents (741 and 730, respectively). Firms and groups in other European countries hold more EPO patentsthan from USPTO, as expected. German firms are most innovative and hold on average 15 USPTO and 26 EPO patents. Thenumber of USPTO patents among French firms is much lower at around 8 patents compared to average of 21 EPO patents. TheItalian firms hold about 2 patents from USPTO and 4 patents from EPO.

17

5. Findings

5.1. Comparison Across Countries

Our analysis shows that technology affects within-country variation of organizational forms in Europe, but

the effect is not evident in the United States or Great Britain. We show that the mediating role of technology

in driving the organizational form depends not only on the nature of technology itself, but also on the

institutional context the firms operate in. To accomplish this, we first explore cross-country variations

independent of technology and then examine how these cross-country differences vary by key technology

dimensions. The methodology is evocative of difference-in-difference approach, as we examine how differences

in organizational form between countries are driven by technology characteristics. We provide descriptive

statistics to outline the overall pattern and then use regression analysis to rule out effects of various covariates

and establish the significance of observed differences.

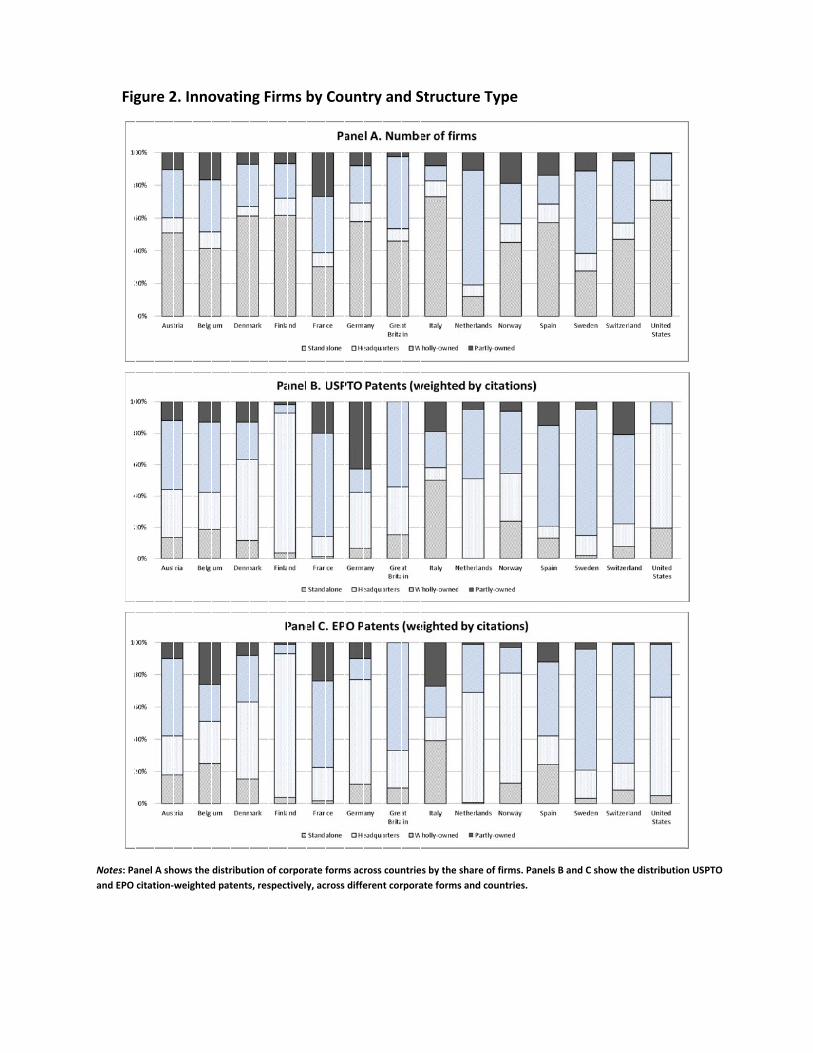

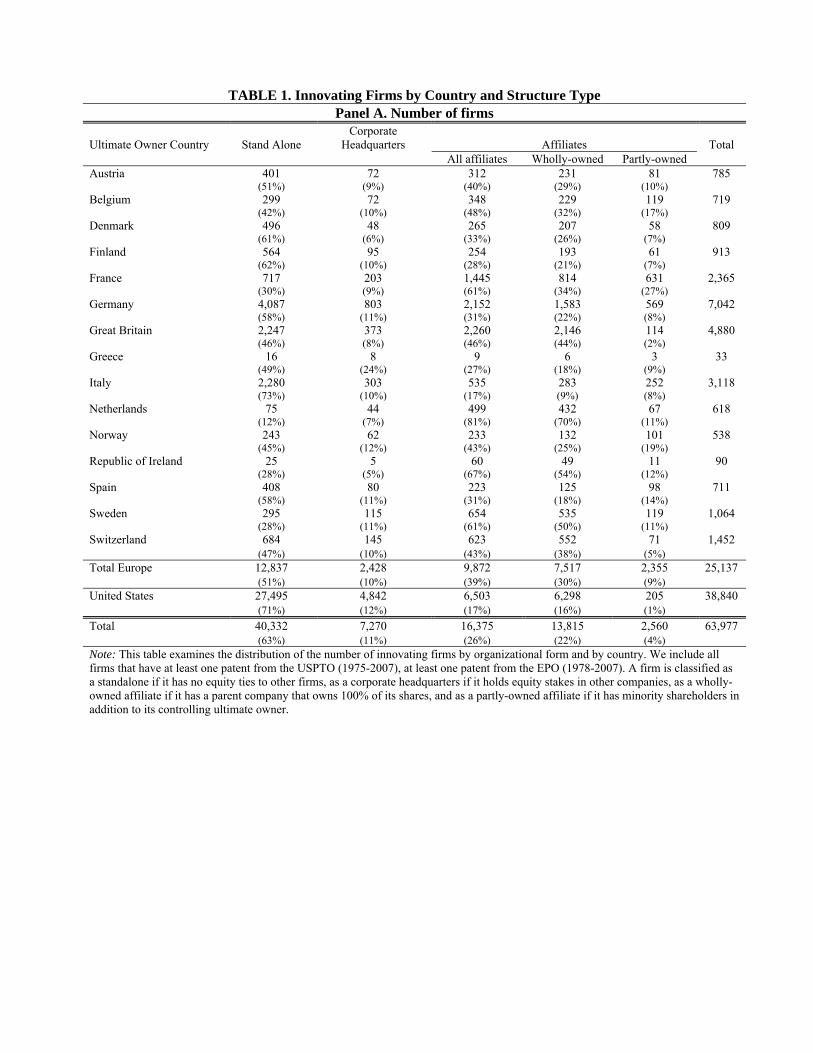

Several notable findings emerge from our cross-country analysis, as summarized in Figure 2 (detailed

distributions are reported in Table 1). First, the overall distribution of organizational form clearly varies by

country (Panel A). In the United States, 71% of all firms are organized in the highly centralized structure of

a standalone, with no equity ties to other firms, while standalones make up about half of all organizational

forms in Europe. Within Europe, the variation is also wide: the share of standalones ranges from 12% in

the Netherlands to 73% in Italy. Corporate headquarters make up about 10% of all organizational forms in

both the United States and Europe. Significant differences exist in the prevalence of both wholly owned and

partly owned affi liates. The affi liate form is not very common in the United States (17%), and almost all

are wholly owned affi liates: only 1% of all affi liates are partly owned, indicating that highly decentralized

structures are rare in the United States. In contrast, affi liates make up almost 40% of firms in Europe, and

decentralized structures with partial ownership are more common at 9% (ranging from 2% in Great Britain

to 27% in France). The overall pattern in the distribution of organizational form indicates greater propensity

toward centralized structures in the United States than in Europe.

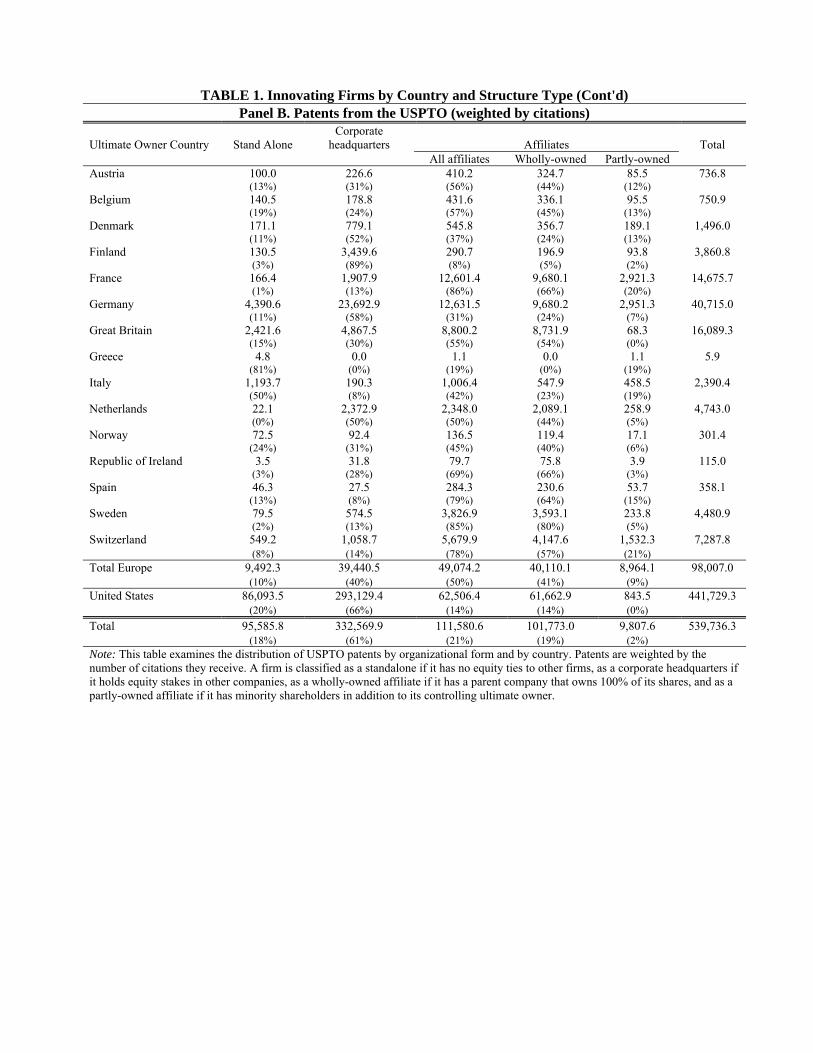

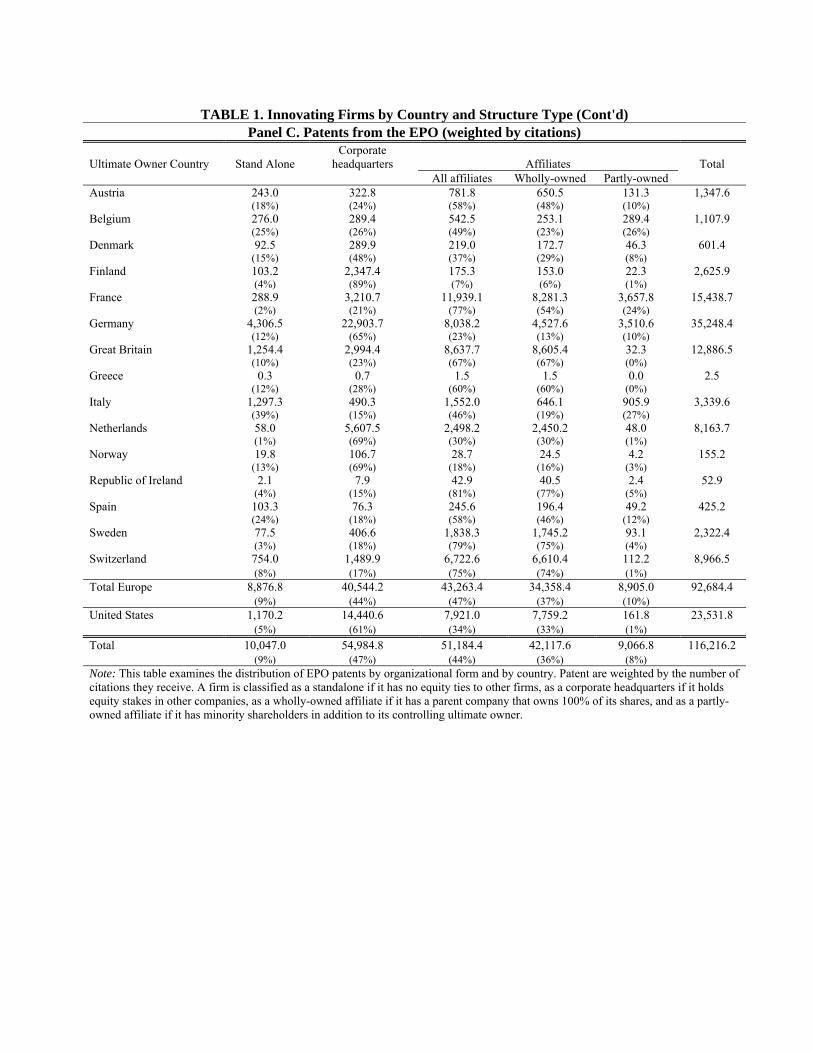

Panels B and C in Figure 2 summarize the distribution of citation-weighted USPTO and EPO patents,

respectively, across different organizational structures and countries. While the overall distribution of citation-

weighted USPTO patents by ownership structure in Europe is slanted toward more decentralized forms– 40%

for corporate headquarters and 50% for affi liates– in the United States this distribution is skewed toward

centralization: standalones and corporate headquarters, with 20% and 66% respectively of patents falling

in these categories, and only 14% of patents held by affi liates. Remarkably, in the United States less than

one percent of patents are held by partly owned affi liates, while in France and Italy about 20% of innovation

takes place in affi liates with minority shareholder ownership. There is also a wide variation in the distribution

of innovation and organizational form across European countries. While Germany appears to resemble the

United States in terms of concentration of innovation in corporate headquarters (58%), French and Italian

firms are clearly skewed toward decentralization, with only 13% and 8% of their respective patents held by

corporate headquarters. Great Britain has a somewhat unique structure, with 55% of British patents held

18

by affi liates, but with nearly all of these affi liates being wholly owned subsidiaries.7 A similar overall pattern

emerges for EPO patents: most patents in the United States belong to more centralized structures; in Europe,

more patents are assigned to decentralized forms, such as affi liates.

Patent assignment patterns in the largest innovating firms illustrate this trend. American conglomerates

usually assign patents to headquarters or to special central intellectual property management divisions, not

to the division where the patent was generated. For example, IBM assigns almost all patents its divisions

generate to its New York headquarters (as indicated by the assignee name on the patent records). Other

large conglomerates that adopt a central patent management structure include General Electric (21,830 out

of 22,348 of GE’s patents are assigned to its Global Research Center division in New York), and 3M (10,640

out of the 10,806 of 3M’s patents are assigned to its headquarters, and the remaining patents are assigned to

the wholly owned IP management subsidiary 3M Innovative Property).

In contrast, corporate groups have a decentralized patent assignment. We hypothesize that the presence

of minority shareholders makes it diffi cult to simply transfer IP assets from the inventing to the controlling

firm. In France, for example, L’Oreal holds 3,135 USPTO patents out of a total of 4,882 patents assigned

to the whole Nestle group. Assigning L’Oreal’s patents to Nestle would be considered an expropriation of

the rights of minority shareholders of L’Oreal. The transfer of patents to the controlling entity requires some

form of valuation and compensation of shareholders of the originating firm. This is likely to be a diffi cult

transaction, which is why patents mostly remain with the originating firm.

We supplement our cross-sectional analysis by examining ownership changes for a sample of innovating

firms that were acquired by an American or European corporation during the period 1997—2007.8 Consistent

with our previous control assumptions, we include deals where the acquired shares exceed 50% for private

firms and 20% for public firms. The M&A sample includes 2,478 firms (where 1,236 are American, 389 British,

199 French, and 293 German), which hold 25,068 USPTO and 28,399 EPO patents. We distinguish between

wholly owned and partly owned acquisitions. The pattern of results is consistent with the cross-sectional

observations of degree of centralization. While in the United States effectively all acquisitions are wholly

owned, in Europe, about half of the acquired (citation-weighted) patents are by partly owned acquisitions.

We also examine the distribution of organizational form of newly established firms. We observe a very similar

pattern of results for firms that were founded between 1997 and 2007. In the United States and Great Britain,

about 1% of these firms are founded as partly owned affi liates, compared to 11% in continental Europe (in

France, 27% of the firms are incorporated as partly owned affi liates). This additional evidence provides

support for the patterns observed for the centralized assignment of patents in the United States and more

decentralized assignment to affi liates in Europe.

Table 2 further highlights the differences in the distribution of patents by ownership type across countries.

7As discussed in in the paper, data is limited to make a distinction between divisions of a conglomerate and wholly ownedsubsidiaries. A richer framework could make a meaningful distinction by introducing relational contracts (see, e.g., MacLeodand Malcomson, 1989; Levin, 2003; chapter 10 of Bolton and Dewatripont, 2005). By creating legally independent firms withina corporation, an organization may be able to gain flexibility by supporting separate relational contracts for different sets ofemployees. We leave the exploration of this idea to future research.

8Not reported in tables; available from authors upon request.

19

Panel A describes the top 20 American innovating firms. IBM leads the list with more than 43,000 USPTO

patents. All American firms in this table have the same ownership structure: they are all publicly traded

conglomerates. Panel B focuses on British firms, which resemble the American conglomerate structure.9

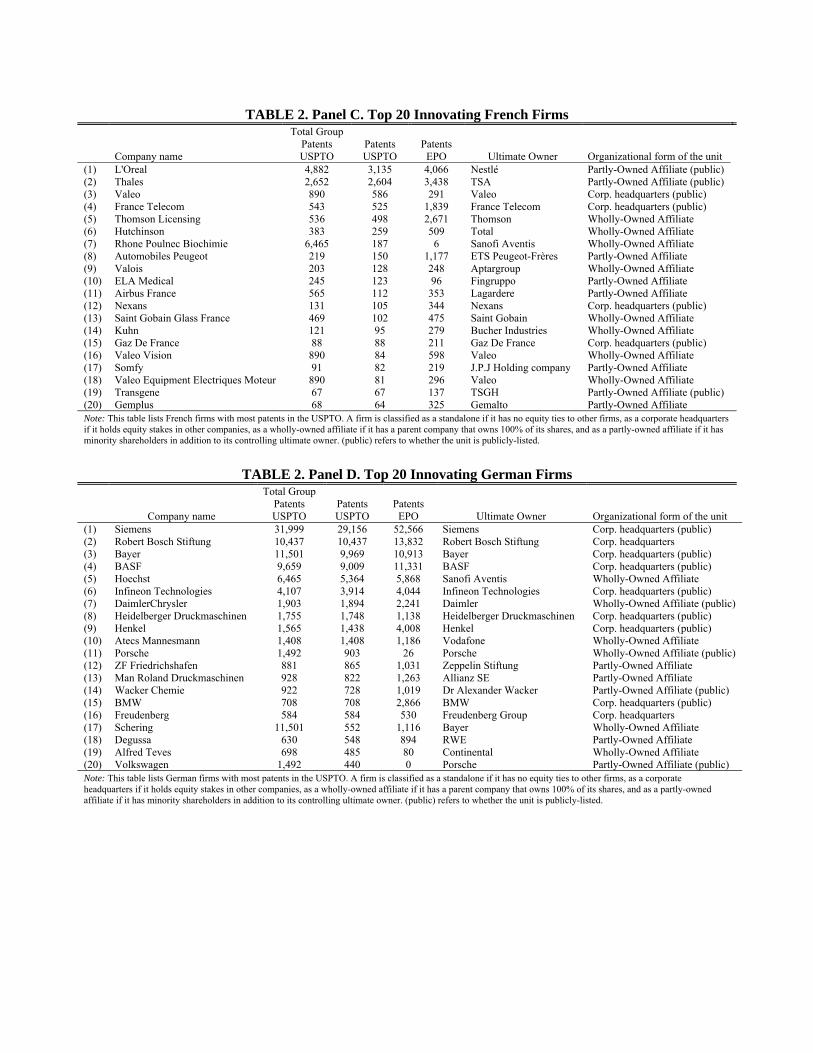

Panel C examines the leading innovating firms in France. More than half are corporate group affi liates,

and 40% with partial ownership. Only 35% of these firms are publicly traded. In Germany (panel D), 20%

of firms are partly owned corporate group affi liates. Lastly, 40% of Italian firms (panel E) are partly owned

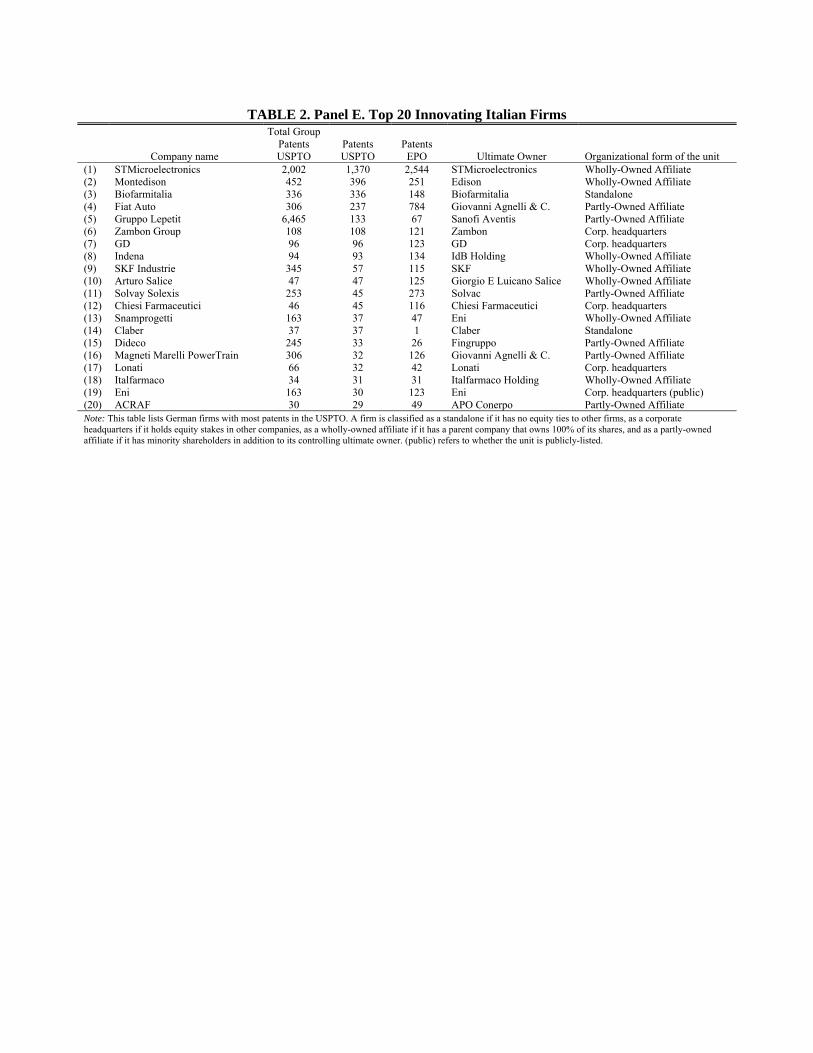

corporate group affi liates, and only one Italian firm is publicly traded.10

Why do we observe a high concentration of more decentralized structures such as corporate groups in

Europe, but not in the United States? Based on the history of corporate groups in the United States, a