1 The Outlook for Energy includes Exxon Mobil Corporation’s internal estimates and forecasts of energy demand, supply, and trends through 2040 based upon internal data and analyses as well as publicly available information from external sources including the International Energy Agency. Work on the report was conducted throughout 2015. This presentation includes forward looking statements. Actual future conditions and results (including energy demand, energy supply, the relative mix of energy across sources, economic sectors and geographic regions, imports and exports of energy) could differ materially due to changes in economic conditions, technology, the development of new supply sources, political events, demographic changes, and other factors discussed herein and under the heading “Factors Affecting Future Results” in the Investors section of our website at www.exxonmobil.com. This material is not to be used or reproduced without the permission of Exxon Mobil Corporation. All rights reserved. The Outlook for Energy: A View to 2040 Tahmid Mizan June 27, 2016

Transcript

1

The Outlook for Energy includes Exxon Mobil Corporation’s internal estimates and forecasts of energy demand, supply, and trends through 2040 based upon internal data and analyses as well as publicly available information from external sources including the International Energy Agency. Work on the report was conducted throughout 2015. This presentation includes forward looking statements. Actual future conditions and results (including energy demand, energy supply, the relative mix of energy across sources, economic sectors and geographic regions, imports and exports of energy) could differ materially due to changes in economic conditions, technology, the development of new supply sources, political events, demographic changes, and other factors discussed herein and under the heading “Factors Affecting Future Results” in the Investors section of our website at www.exxonmobil.com. This material is not to be used or reproduced without the permission of Exxon Mobil Corporation. All rights reserved.

The Outlook for Energy: A View to 2040 Tahmid Mizan June 27, 2016

2

Global fundamentals

3

ExxonMobil 2016 Outlook for Energy

0%

25%

50%

75%

100%

125%

2014 20400%

25%

50%

75%

100%

125%

2014 20400%

25%

50%

75%

100%

125%

2014 20400%

25%

50%

75%

100%

125%

2014 2040

Global Trends Continue to Evolve

GDP

Population Demand

Carbon Emissions

Percent

Growth from 2014 Level

4

ExxonMobil 2016 Outlook for Energy

Energy Fuels Human Development

0.00

0.25

0.50

0.75

1.00

10 100 1000 10000

U.N. Human Development Index 2013 Index

Source: United Nations, ExxonMobil estimates Energy Use per Capita (Thousand BTU/person/day)

Norway United States

Brazil

Germany

Niger

India China

Nigeria

Bangladesh

5

ExxonMobil 2016 Outlook for Energy

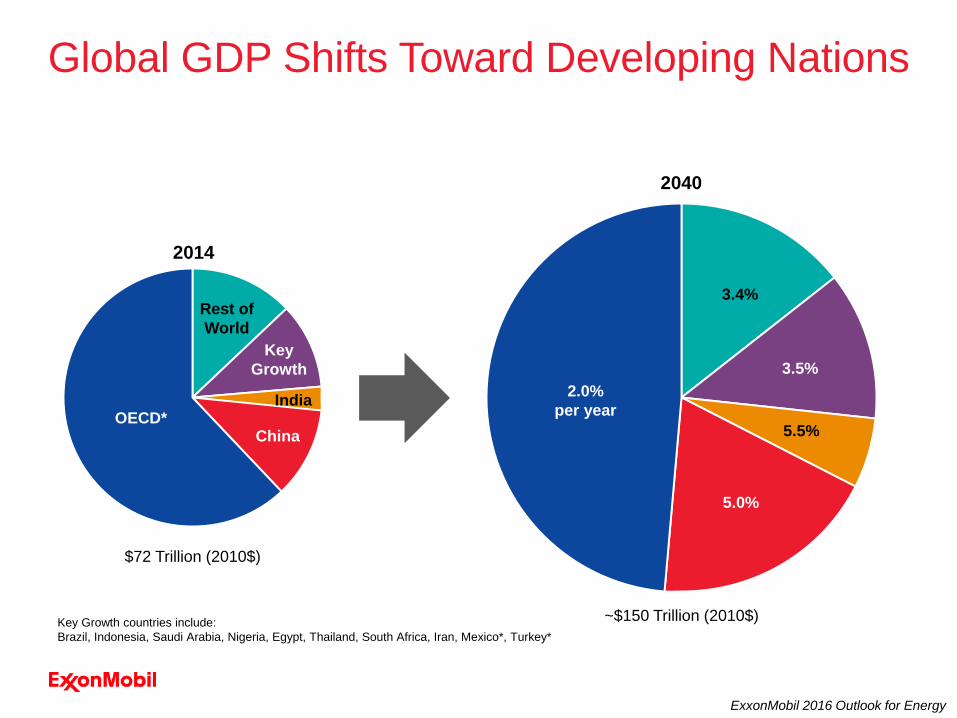

Global GDP Shifts Toward Developing Nations

2014

2040

$72 Trillion (2010$)

~$150 Trillion (2010$) Key Growth countries include: Brazil, Indonesia, Saudi Arabia, Nigeria, Egypt, Thailand, South Africa, Iran, Mexico*, Turkey*

2.0% per year

5.0%

5.5%

3.5%

3.4%

OECD* China

India

Key Growth

Rest of World

6

ExxonMobil 2016 Outlook for Energy

0

200

400

600

800

1000

1200

1400

2000 2020 20400

40

80

120

160

2000 2020 20400

3

6

9

12

15

18

21

2000 2020 2040

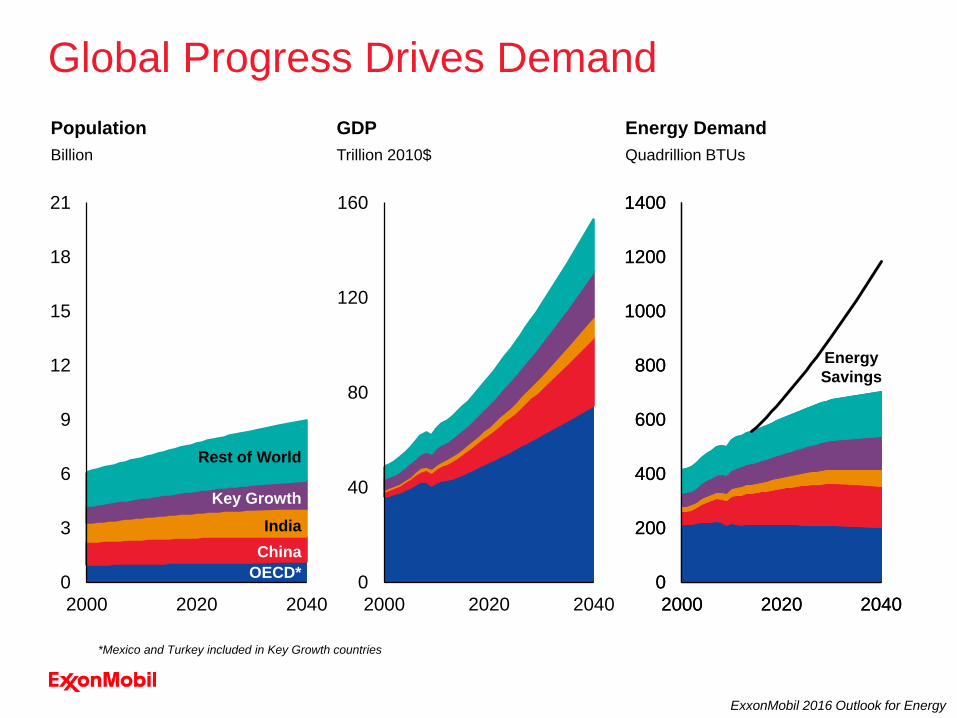

Global Progress Drives Demand Population Billion

GDP Trillion 2010$

Energy Demand Quadrillion BTUs

OECD*

Key Growth

China India

Rest of World

Energy Savings

0

200

400

600

800

1000

1200

1400

2000 2020 2040

*Mexico and Turkey included in Key Growth countries

7

ExxonMobil 2016 Outlook for Energy

0

5

10

15

1970 1980 1990 2000 2010 2020 2030 2040

Technology Helps Us Do More With Less Global Average Energy Intensity Thousand BTUs per dollar GDP (2010$)

2014

8

Emissions

9

ExxonMobil 2016 Outlook for Energy

~ 35 $/ton

~ 20 $/ton

~ 80 $/ton

< 10 $/ton

2040 CO2 “Proxy” Cost

CO2 Policy Assumptions Vary by Region

10

ExxonMobil 2016 Outlook for Energy

0%

25%

50%

75%

100%

2014 20400

10

20

30

40

2000 2020 2040

Energy-Related CO2 Emissions by Region Billion Tonnes

CO2 Emissions Plateau Energy Mix Shifts to Lower-Carbon Fuels

India

Key Growth

Rest of World

OECD*

China

Global Energy Mix Percent

Oil

Coal

Gas

Biomass Renewables Nuclear

*Mexico and Turkey included in Key Growth countries

11

Transportation

12

ExxonMobil 2016 Outlook for Energy

0

25

50

75

2000 2020 2040

Sector Demand MBDOE

Light Duty

Marine

Rail

Heavy Duty

Aviation

Transportation Demand

Commercial

13

ExxonMobil 2016 Outlook for Energy

0

15

30

45

60

75

2010 2020 2030 20400

15

30

45

60

75

2010 2020 2030 2040

Average Vehicle Efficiency On-Road Miles per Gallon

Average Fleet

Light Duty Vehicle Efficiency

0

200

400

600

800

1000

1200

1400

1600

1800

2010 2015 2020 2025 2030 2035 2040

Elec/Plug-in/Fuel CellHybridNatural Gas & LPGDieselGasoline

Fleet by Type Million

U.S.

Europe

14

Industrial

15

ExxonMobil 2016 Outlook for Energy

0

100

200

300

1980 2010 2040

Industrial Demand By Sector Quadrillion BTUs

Other

Energy Industry

Heavy Industry

Chemical

0

100

200

300

1980 2010 2040

By Fuel Quadrillion BTUs

Oil

Gas

Coal

Biomass

Electricity

16

ExxonMobil 2016 Outlook for Energy

Chemicals Demand Grows Globally

0

10

20

30

40

2000 2020 2040

Asia Pacific

Europe

North America

Middle East

Russia/Caspian Latin America

Africa

MBDOE By Region

MBDOE

By Sector

0

10

20

30

40

2000 2020 2040

Steam Cracking

Fertilizer

Other Chemicals

17

ExxonMobil 2016 Outlook for Energy

0

10

20

30

40

2000 2020 2040

Chemicals Demand Sees Significant Growth

MBDOE

By Sector MTA

Ethylene Production

0

100

200

300

2010 2025 2040

Asia Pacific

Rest of World

North America

Steam Cracking

Fertilizer

Other Chemicals

18

ExxonMobil 2016 Outlook for Energy

North America MBDOE

Chemicals Energy Demand by Region Asia Pacific MBDOE

Naphtha

Electricity/Heat

Gas Liquids

Coal

Gas

Other Oil

0

4

8

12

16

'00 '10 '20 '30 '40

Europe MBDOE

0

4

8

12

16

'00 '10 '20 '30 '400

4

8

12

16

'00 '10 '20 '30 '40

19

Electricity generation

20

ExxonMobil 2016 Outlook for Energy

0

10

20

30

40

2000 2020 2040

Electricity Grows in Developing Economies Electricity Demand by Region Thousand TWh

United States

OECD*

China

India Key Growth

Rest of World

*Mexico and Turkey included in Key Growth countries

0

5

10

15

1980 2010 2040

Per Capita Demand MWh per person

United States

India

Europe China

Key Growth

2014

21

ExxonMobil 2016 Outlook for Energy

0

10

20

30

40

2000 2020 2040

2010

2040

0

500

1000

1500

Nuclear Wind Solar0

500

1000

1500

Nuclear Wind Solar

GW Global Capacity

Global Electricity Generation Mix Evolves

Global Capacity Utilized

2014

2040

Thousand TWh By Generation Type

Wind & Solar

Oil

Coal

Nuclear

Other Renewables

Gas

22

ExxonMobil 2016 Outlook for Energy

Oil

A Shift in Electricity Generation

-2 0 2 4 6

OECD*ChinaIndiaKey GrowthRest of World

Thousand TWh Change in Electricity Net Delivered 2014-2040

Gas

Wind/Solar

Nuclear

Other Renewables

Coal

*Mexico and Turkey included in Key Growth countries