24

1 SIA ANALYST/MEDIA BRIEFING 1H FY2014/15 Results 07 November 2014 THE PARENT AIRLINE 1H FY2014/15 RESULTS

1

SIA ANALYST/MEDIA BRIEFING 1H FY2014/15 Results

07 November 2014

THE PARENT AIRLINE1H FY2014/15

RESULTS

2

THE PARENT AIRLINE COMPANY OPERATING PERFORMANCE – 2Q & 1H FY14/15

Slide 3

25,016Revenue Pax-KM(million)

2Q/14

-0.2

% Change

81.9Passenger Load Factor (%)

+0.8 pt

30,562Available Seat-KM (million)

-1.1 -0.260,825

+0.2 pt79.8

+0.148,516

1H/14%

Change

Slide 4

Passenger Yield(¢/pkm)

Passenger Unit Cost(¢/ask)

Passenger Breakeven Load Factor (%)

10.9 -0.9

9.0 -1.1

82.6 -0.1 pt

THE PARENT AIRLINE COMPANY OPERATING PERFORMANCE – 2Q & 1H FY14/15

2Q/14%

Change

Passenger Unit Ex-Fuel Cost (¢/ask)

5.1 -

-3.38.8

-0.910.9

-2.0 pts80.7

1H/14%

Change

-3.94.9

3

THE PARENT AIRLINE COMPANY RESULTS – 2Q & 1H FY14/15

Slide 5

4.3Operating Profit Margin (%)

1.3 pts

41138Operating Profit 42

3,084

(62)

Total Expenditure

1,175- Fuel Cost18- Fuel Hedging

Loss/(Gain)1,891- Ex-fuel Cost

41

105

(2)

1.3

8.3n.m.

(0.1)

3,222Total Revenue

2Q/14$million

-

Better/(Worse)

$million %

-

(3)183

1486,048

(151)6,231

1H/14$million

982,3531(10)

493,705

Better/(Worse)

$million %

-2.9

(1.6)

2.4

4.07.9

1.3

(2.4)

THE PARENT AIRLINE COMPANY OPERATING PERFORMANCE

0

68

72

76

80

84

88

1H 10/11 1H 11/12 1H 12/13 1H 13/14

Passenger Load FactorBreakeven Load Factor

(%)

79.4

Slide 6

77.579.6

1H 14/15

79.6 79.8

4

THE PARENT AIRLINE COMPANY OPERATING PERFORMANCE

75.4

78.079.8

0

68

72

76

80

84

88

1H 10/11 1H 11/12 1H 12/13 1H 13/14

Passenger Load FactorBreakeven Load Factor

(%)

79.4

Slide 7

77.579.6

1H 14/15

79.6

82.7

79.8

80.7

THE PARENT AIRLINE COMPANY OPERATING PERFORMANCE

75.4

78.079.8

0

68

72

76

80

84

88

1H 10/11 1H 11/12 1H 12/13 1H 13/14

Passenger Load FactorBreakeven Load Factor

(%)

79.4

4.0 -0.5-0.2

Slide 8

77.579.6

1H 14/15

79.6

82.7-3.1

79.8

80.7-0.9

5

THE PARENT AIRLINE COMPANY MONTHLY PASSENGER YIELD

Slide 9

10.8

11.1

11.2

11.411.6

11.311.3

11.611.5

11.411.2

11.0

11.4

10.9

11.2

10.8

11.3

11.1

10.9

11.1 11.311.311.1

10

11

12

Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar

2012-13 2013-14 2014-15

¢/pkm

11.1

10.810.7 10.910.7

11.2

THE PARENT AIRLINE COMPANY COST COMPOSITION – 1H FY14/15

Slide 10

LPO* Charges 5.1% (+0.2% pt)

Others 10.1% (-0.3% pt)

Fuel Cost Post Hedging

38.7% (-0.7% pt)AMO Costs 5.4% (-)

Passenger Costs5.7% (+0.3% pt)

Handling Charges 7.3% (+0.2% pt)

Staff12.9% (-0.1% pt)

Aircraft Depreciation & Lease Rentals

14.8% (+0.4% pt)*Landing, Parking and Overflying

6

THE PARENT AIRLINE COMPANY TOP EXPENDITURE ITEMS – 1H FY14/15

Slide 11

6,195.7

0

6,000

6,100

6,150

6,200

H1 FY13/14

-99.1 (-4.1%)

Fuel after

hedging

Lower net fuel

cost

-6.9 (-2.1%)

AMO Cost

+11.5 (+44.1%)

Exchange

Higher revaluation

and hedging

loss

-34.6 (-1.5%)

Others

+8.1 (+2.4%)

Passenger Cost

6,048.0

H1 FY14/15

-147.7(-2.4%)

Composition of decrease in Operating Expenditure

$M

-26.7 (-3.3%)

Staff Cost

THE PARENT AIRLINE COMPANY FUEL PRICE AND EXPENDITURE - TREND

Slide 12

9690 90

10094

135

134124

121 123 124 121

123

80

93 90

136

132120

126 127 126 124

122

8885

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

0102030405060708090100110120130140150160

Fuel Cost after hedging

Fuel Price before hedging

Fuel Price after hedging

2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q

2009-10 2010-11 2011-12 2012-13 2013-14 2014-15

($ million)

1,26

8

851

85996

0

939

899

1,15

0

1,15

6

1,17

4

1,23

6

1,20

6

1,19

4

7

THE PARENT AIRLINE COMPANY FUEL EXPENDITURE – 1H FY14/15

Slide 13

2,442

2300

2400

2500

1HFY13/14

$M

2,343

1HFY14/15

-99(-4.1%)

-75

Volume

Lowervolume uplifted

-1

Hedging

Higher hedging gain vs

last year-9

Price

Lower weighted average

fuel price-14

Exchange

WeakerUS Dollar

THE GROUP1H FY2014/15

RESULTS

8

($ million)2013/14 2014/15

GROUP REVENUE – 1H FY2014/15

3,840

3,682

0

2,750

3,000

3,250

3,500

3,750

4,000

Q1 Q2

Year-on-Year$154M-2.0%

Half Year Revenue$7,587M-$158m

-4.1%

Slide 15

3,901 3,905 +$4m+0.1%

2013/14 2014/15

GROUP EXPENDITURE– 1H FY2014/15

3,7583,643

Q1 Q2

($ million)

0

2,750

3,000

3,250

3,500

3,750

4,000

-$115m-3.1%

Slide 16

3,814 3,773 -$41m-1.1%

Year-on-Year$156M-2.1%

Half Year Expenditure

$7,416M

9

2013/14 2014/15

GROUP OPERATING PROFIT– 1H FY2014/15

82

39

0

25

50

75

100

125

150

Q1 Q2

Half Year Op Profit$171M

Year-on-Year$2M

+1.2%

($ million)

-$43m-52.4%

Slide 17

87

132+$45m+51.7%

CONTRIBUTION TO GROUP OPERATING PROFIT – 1H FY14/15 ($ million)

5

183

1H 1415

(34)

37

SilkAir

Singapore Airlines

SIA Cargo

SIA Engineering

22

186

(71)

56

1H 13/14

17-

3-

37+

19-

Change

Slide 18

77.3-

1.6-

52.1+

33.9-

% Change

10

($ million)2013/14 2014/15

GROUP NET PROFIT– 1H FY2014/15

122

35

0

50

100

150

200

Q1 Q2

-$87M-71.3%

Half Year Net Profit

$126M

Year-on-Year$157M -55.5%

Slide 19

161

91

-$70M-43.5%

($ million)

GROUP NET PROFIT – 1H FY2014/15

0

50

100

150

200

250

300

1H FY13/14

Associates Operating Profit

Interestand

Others

283

1H FY14/15

126

-157-55.5%

Slide 20

AircraftDisposal

ExceptionalItems

-154

Share of losses from associates

against profits last

year

-32

Exceptional items

+2

Higher operating

profit

+31

Higher gain on

disposal of aircraft

-4.0

Others

11

Slide 21

10.05.0Interim Dividend Per Share (¢)

1.251.09EBITDAR Per Share ($)

1H 13141H 1415

11.2610.96Net Asset Value Per Share ($)

At 31 Mar 14At 30 Sep 14

24.010.7Earnings Per Share (¢)

GROUP RESULTS – 1H FY2014/15

- 4

- 1

OUT: Decommissioned B777-200

OUT: Decommissioned A330-300

FLEET DEVELOPMENT - SIA

Slide 22

105Operating Fleet at 30 September 14

No. of Aircraft

105Operating Fleet at 31 March 15

+ 2IN: Delivery of A330-300+ 3Delivery of B777-300ER

12

- 1

- 1

OUT: Decommissioned A320-200

Decommissioned A319-100

FLEET DEVELOPMENT - SLK

Slide 23

26Operating Fleet at 30 September 14

No. of Aircraft

27Operating Fleet at 31 March 15

+ 3IN: Delivery of B737-800

FLEET DEVELOPMENT - SCOOT

Slide 24

6Operating Fleet at 30 September 14

No. of Aircraft

+ 2IN: Delivery of B787-9

- 2OUT: Decommissioned B777-200

6Operating Fleet at 31 March 15

13

GROUP CAPITAL EXPENDITURE

FY15/16 FY16/17 FY17/18 FY18/19 FY19/20

Aircraft 2,750 2,900 4,150 4,200 3,800

Other Assets 200 200 150 100 100

Total 2,950 3,100 4,300 4,300 3,900

Slide 25

GROUP FUEL HEDGING POSITION

Slide 26

For the period Oct 14 to Mar 15

Jet Fuel Brent

Percentage hedged (%)

65.3 0.8

Average hedged price (USD/BBL - Jet Fuel)

116 100

14

BUSINESS OUTLOOK FOR

FY2014/15

OUTLOOK

Intense competition

Geopolitical factors

Economic risks

Slide 28

15

MEETING THECHALLENGES

CHALLENGES

Geography Additional Hubs

LCC Competition

Group Portfolio

FSC Competition

NetworkServiceProduct

Slide 30

16

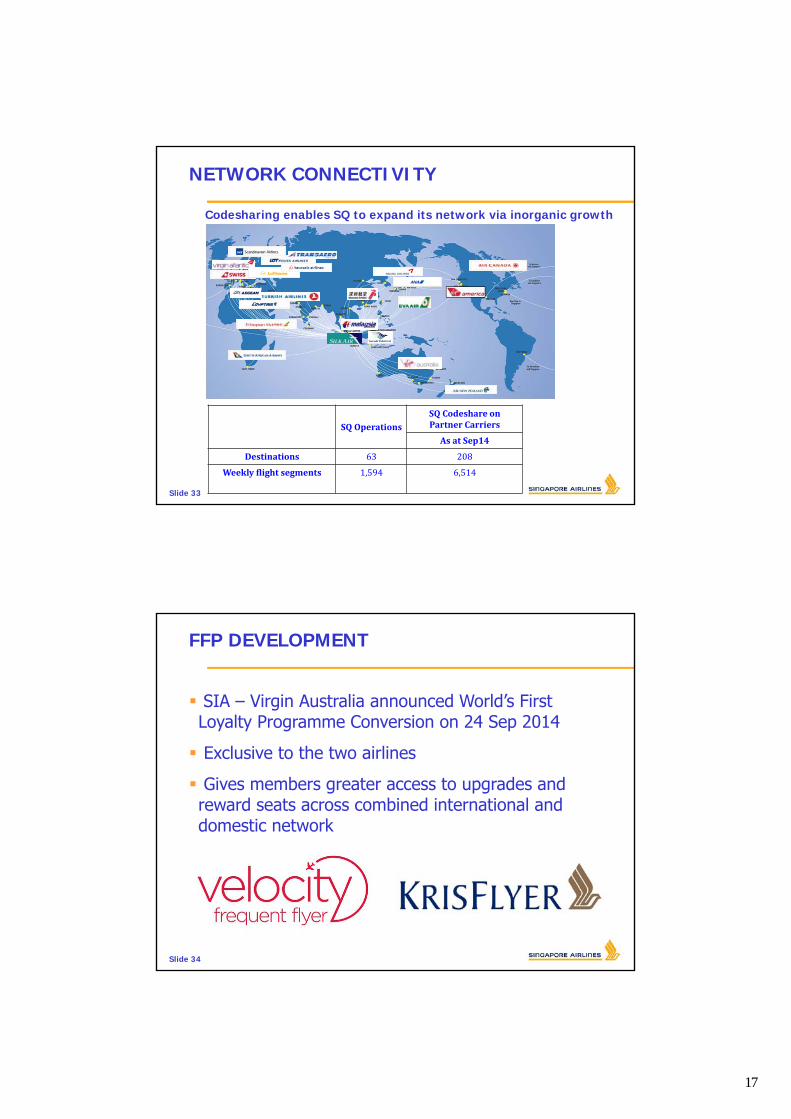

NETWORK CONNECTIVITY

Slide 31

SilkAir Projected capacity growth of 7% for FY14-15 over FY13-14

New destinations & frequency increase for existing destinations

4 new destinations: Kalibo, Mandalay, Hangzhou, Bali

NETWORK CONNECTIVITY

Air New Zealand SQ – NZ alliance to launch on 6 Jan 2015

NZ to operate daily AKL-SIN vv on B772

SQ to operate daily SIN-AKL vv on A380 and daily SIN-CHC vv on B772

20% capacity increase between Singapore and New Zealand

Turkish Airlines Major expansion of codeshare ties commencing May 14

Connecting passengers between SQ and TK increased more than 13,000 in the period Jun 14 – Sep 14, year-on-year

Slide 32

17

NETWORK CONNECTIVITY

Slide 33

SQOperationsSQCodeshareonPartnerCarriers

AsatSep14

Destinations 63 208

Weeklyflightsegments 1,594 6,514

Codesharing enables SQ to expand its network via inorganic growth

SIA – Virgin Australia announced World’s First Loyalty Programme Conversion on 24 Sep 2014

Exclusive to the two airlines

Gives members greater access to upgrades and reward seats across combined international and domestic network

FFP DEVELOPMENT

Slide 34

18

KrisFlyer Spree− Launched 19 Jun 2014

− Online platform where memberscan earn miles when they shop

− Attract new KF members and increase engagement and benefits to existing ones

Pay with KrisFlyer Miles− Members are able to use miles

to pay for all or part of theircommercial airfares, fuel surcharge, and fees.

− Effective Aug 2014, miles can be used to pay for preferred seats

− Minimum miles level reduced from 5,000 to 3,000Slide 35

FFP DEVELOPMENT

BRANDING INITIATIVES

Slide 36

Projecting the SIA Brand to a global audience through sponsorships 2014 Formula 1 Singapore Airlines Singapore Grand Prix

2014 WTA Finals Singapore

19

Full Service

LCC

Regional

The Group’s portfolio of brands extends its market reach

Long-HaulMarkets

Po

siti

on

ing

Extend

Market

Reach

SIA GROUP PORTFOLIO

Slide 37

Gaining Travellers' Mindshare

Slide 38

SIA GROUP PORTFOLIO

20

Strong LCC growth in Asia Pacific

Further growth potential

LCC participation as an engine of growth

Asia Pacific 5-year CAGR*(2009 – 2013)

Full Service Carriers +6%

Low Cost Carriers +18%

Region Market Share* of LCCs(January –August 2014)

Europe 42%

United States 31%

Asia Pacific 26%

Singapore 30%

*Source: Diio Mi, CAPASlide 39

SIA GROUP PORTFOLIO

FSC platform SQ/MI synergy 50% increase in SQ/MI connecting traffic in

last three years 60% of MI traffic is connecting SQ

A short-haul LCC platform is essential

SilkAir SIA

Traffic growth in Singapore has been driven by transfer traffic

From/To Singapore YoY Growth*

Point to Point Traffic 3.4%

Transfer Traffic 6.1%

Slide 40

SIA GROUP PORTFOLIO

Tiger

LCC platform Scoot-Tiger ATI Mutually beneficial cooperation between a

short haul LCC and Scoot Tiger Airways remains the most viable

short-haul LCC platform for the Group

ScootTigerTiger

21

Unprofitable overseas subsidiaries have been disposed of

Capacity overhang has been addressed

Refocus on Singapore operations

Commercial cooperation with Scoot - with ATI - will bring clear benefits to both Tiger Airways and Scoot

Tiger Airways is entering a rebuilding phase

Slide 41

TIGER AIRWAYS

Tiger Airways needs to repair balance sheet SIA providing support

To support the increased investment in Tiger Airways, SIA will require Greater influence over Tiger Airways’ development Greater alignment of interests Therefore, stepping up to controlling stake

For Tiger Airways to grow, it would need capabilities of SIA Group Economies of scale Network connectivity and distribution

SIA’s stake in Tiger Airways

Slide 42

TIGER AIRWAYS

22

Passed 3 million passenger milestone in Jul 2014

Commence renewal of fleet from end of 2014 with first delivery of B787

13 destinations in eight countries or territories

Slide 43

SCOOT

LCC based in Don Mueang International Airport, Bangkok

Second home market for Scoot

Fleet of B777s

Milestones:

−Brand Launch on 8 Sep 2014

−Air Transport Service License granted on 8 Sep 2014

−Air Operator Certificate received on 30 Oct 2014

NOKSCOOT JOINT VENTURE

Slide 44

23

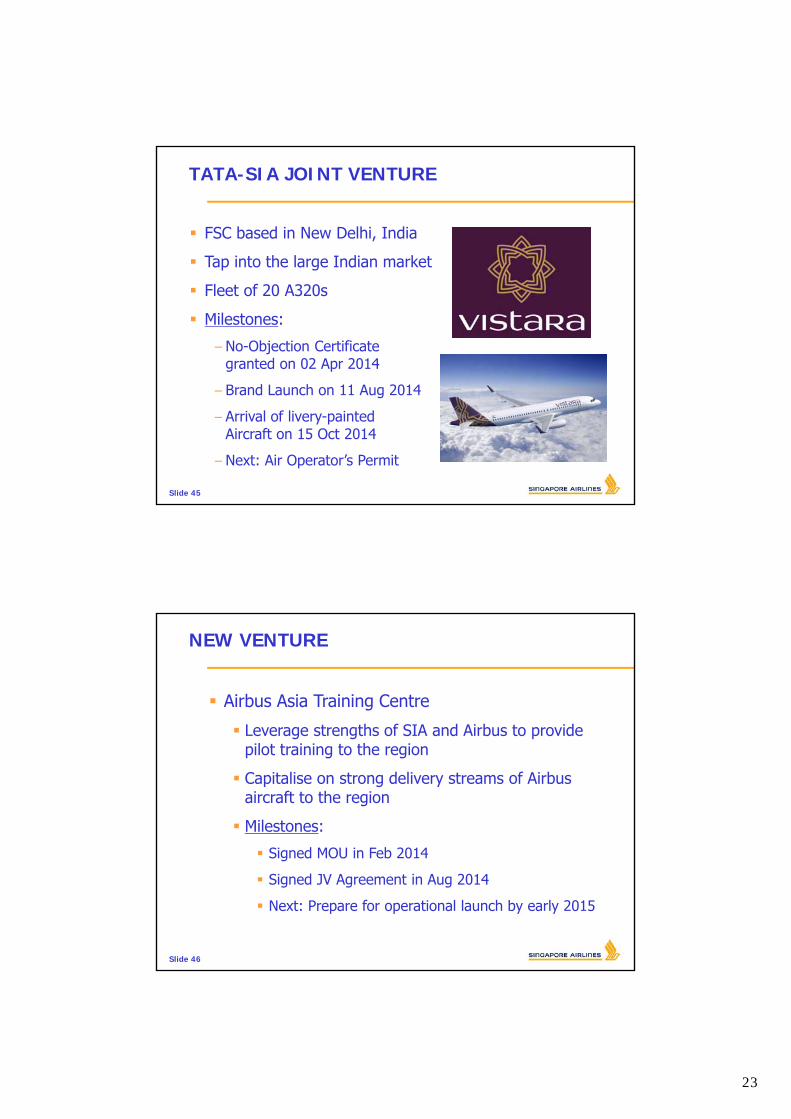

FSC based in New Delhi, India

Tap into the large Indian market

Fleet of 20 A320s

Milestones:

−No-Objection Certificategranted on 02 Apr 2014

−Brand Launch on 11 Aug 2014

−Arrival of livery-painted Aircraft on 15 Oct 2014

−Next: Air Operator’s Permit

TATA-SIA JOINT VENTURE

Slide 45

NEW VENTURE

Slide 46

Airbus Asia Training Centre

Leverage strengths of SIA and Airbus to provide pilot training to the region

Capitalise on strong delivery streams of Airbus aircraft to the region

Milestones:

Signed MOU in Feb 2014

Signed JV Agreement in Aug 2014

Next: Prepare for operational launch by early 2015

24

Thank You

![[REVISI] PiO Syndicate 3 Singapore Airlines](https://static.documents.pub/doc/80x56/55cf8d2d5503462b1392bd46/revisi-pio-syndicate-3-singapore-airlines.jpg)