Actuaries, Consultants, Administrators and Other Benefits Professionals Pension Actuary THE A publication of the American Society of Pension Actuaries Vol.XXX, Number 5 September-October 2000 Continued on page 6 IN THIS ISSUE WASHINGTON UPDATE Must the Investment Options in a 401(k) Plan be Tailored to the Workforce? 3 • Farewell to Section 415(e) 4 • Leased Employees, the Plot Thickens 5 • Welcome New Members 7 New BNA Subscription Discount Program 10 • 2000 Educator's Award Recipient 10 • ABC Events 15 • Wrap-up on ASPA Summer Academy 16 • Call For Papers 17 • American College of Employee Benefits Council Welcomes Six ASPA Members 18 • 2000 Eidson Award Recipient 18 • Martin Rosenberg Academic Achievement Award Winners 19 • 2000 ASPA Annual Conference Highlights 20 • Letter to Annual Conference Attendees 21 • Focus on Government Affairs 22 Focus on ABCs 23 • Focus on E&E 24 • Focus on ASPA 25 • Focus on CE 26 • PIX Digest 27 • Bulletin Board 28 • Calendar of Events 28 Taylor Named as ASPA President George J. Taylor, MSPA, EA, has been named ASPA’s President for the 2000-2001 term, which begins at the close of the 2000 Annual Conference. Mr. Taylor is Senior Vice President of ARIS Pension Services (APS), a division of ARIS Corporation of America. He has over 30 years of experience in the administrative, ac- tuarial, and technical aspects of maintaining qualified retirement plans and provides technical exper- tise and training to APS’s staff, as well as consulting and actuarial ser- vices to APS clients. Mr. Taylor was elected to ASPA’s Board of Directors in 1994, served as Vice President in 1996, 1997, and 1999, and as President-Elect in 2000. He has been active on the Confer- ences Committee and co-chaired the ASPA Annual Conference in 1999. Mr. Taylor has been very active on ASPA’s Government Affairs Com- mittee since 1992, serving as a co- chair for five years (1995-1999). In that capacity, he has had numerous meetings with the IRS, Treasury, the U.S. Department of Labor, the Pen- sion and Welfare Benefits Adminis- tration, and the executive committee of the Pension Benefits Guarantee Corporation. He has also met with legislators and their staffers to present positions that would enhance the private pension sector. Mr. Taylor chaired a committee that drafted ASPA’s Pension Reform Pro- posals. Part of this proposal, the Se- cure Assets for Employees (SAFE) Defined Benefit Plan, has been intro- duced in the House and the Senate. Cash Balance Debate Heats Up by Brian H. Graff, Esq. In the midst of the effort to en- act the most significant pension legislation since ERISA, the de- bate over the future of cash bal- ance plans has intensified and potentially may threaten the bi- partisan atmosphere surrounding pension reform. Along the way, traditional defined benefit plans may be forced to accept addi- tional regulatory burdens due to the brouhaha surrounding their controversial cousins. The debate over cash balance plans has been simmering for al- most two years since the Wall Street Journal began its not-so- subtle assault on the plan design. Since then, most of the legiti- mate legislative discussion has centered on enhanced disclosure and addressing the so-called “wearaway” problem. However, behind the scenes, a fairly brutal debate over the very future of the plan design is focused mainly on whether cash balance plans inher- ently violate the Age Discrimina- tion and Employment Act. The actors in this play include trial lawyers representing participants in several lawsuits against cash balance plan sponsors throughout

Transcript

Actuaries, Consultants, Administrators and Other Benefits Professionals

PensionActuaryTH

E

A publication of the American Society of Pension Actuaries Vol.XXX, Number 5 September-October 2000

Continued on page 6

IN THIS ISSUE

WASHINGTON UPDATE

Must the Investment Opt ions in a 401(k ) P lan be Ta i lo redto the Workforce? 3 • Farewel l to Sect ion 415(e ) 4 • LeasedEmployees, the P lot Th ickens 5 • Welcome New Members 7

New BNA Subscr ip t ion D iscount Program 10 • 2000 Educator 's AwardRec ip ient 10 • ABC Events 15 • Wrap-up on ASPA Summer Academy

16 • Cal l For Papers 17 • Amer ican Co l lege of Employee Benef i tsCounc i l Welcomes S ix ASPA Members 18 • 2000 E idson AwardRec ip ient 18 • Mart in Rosenberg Academic Ach ievement Award

Winners 19 • 2000 ASPA Annua l Conference H igh l ights 20 • Let ter toAnnua l Conference At tendees 21 • Focus on Government Af fa i rs 22

Focus on ABCs 23 • Focus on E&E 24 • Focus on ASPA 25 • Focus onCE 26 • P IX D igest 27 • Bul le t in Board 28 • Ca lendar o f Events 28

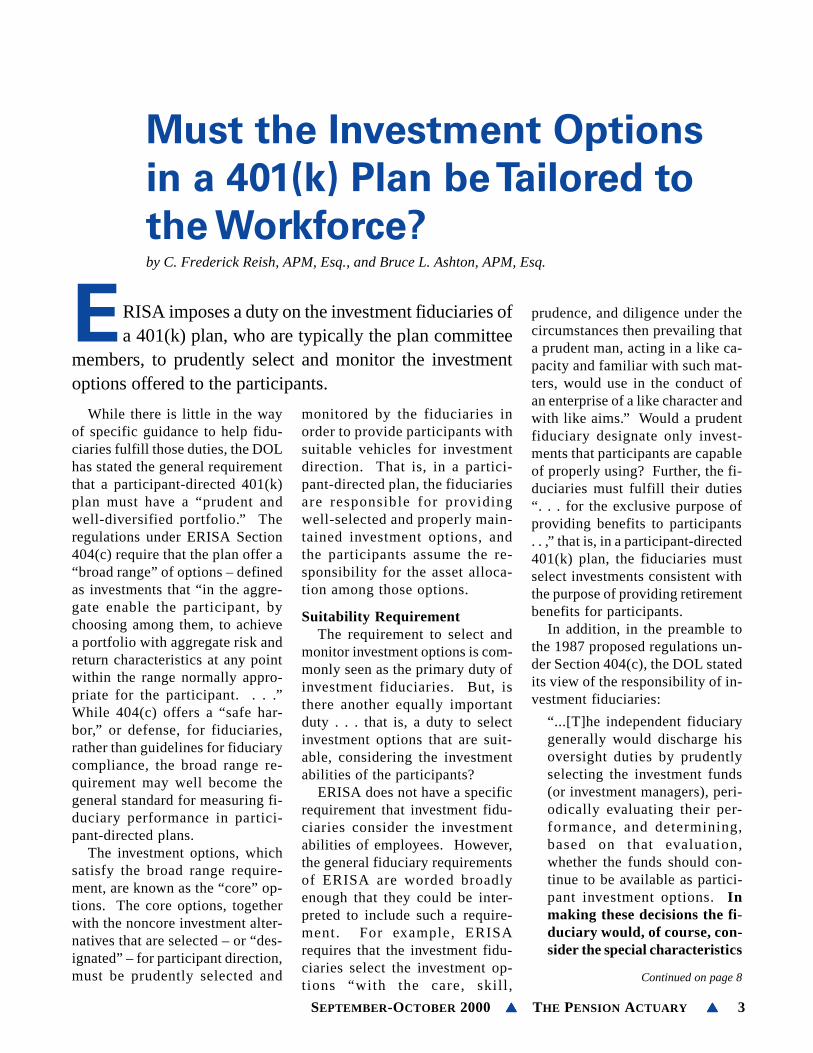

Taylor

Named as

ASPA PresidentGeorge J. Taylor, MSPA, EA, has

been named ASPA’s President for the2000-2001 term, which begins at theclose of the 2000 Annual Conference.Mr. Taylor is Senior Vice Presidentof ARIS Pension Services (APS), adivision of ARIS Corporation ofAmerica. He has over 30 years ofexperience in the administrative, ac-tuarial, and technical aspects ofmaintaining qualified retirementplans and provides technical exper-tise and training to APS’s staff, aswell as consulting and actuarial ser-vices to APS clients.

Mr. Taylor was elected to ASPA’sBoard of Directors in 1994, servedas Vice President in 1996, 1997, and1999, and as President-Elect in 2000.He has been active on the Confer-ences Committee and co-chaired the

ASPA Annual Conference in 1999.Mr. Taylor has been very active onASPA’s Government Affairs Com-mittee since 1992, serving as a co-chair for five years (1995-1999). Inthat capacity, he has had numerousmeetings with the IRS, Treasury, theU.S. Department of Labor, the Pen-sion and Welfare Benefits Adminis-tration, and the executive committeeof the Pension Benefits GuaranteeCorporation. He has also met withlegislators and their staffers topresent positions that would enhancethe private pension sector.

Mr. Taylor chaired a committee thatdrafted ASPA’s Pension Reform Pro-posals. Part of this proposal, the Se-cure Assets for Employees (SAFE)Defined Benefit Plan, has been intro-duced in the House and the Senate.

Cash BalanceDebate Heats Upby Brian H. Graff, Esq.

In the midst of the effort to en-act the most significant pensionlegislation since ERISA, the de-bate over the future of cash bal-ance plans has intensified andpotentially may threaten the bi-partisan atmosphere surroundingpension reform. Along the way,traditional defined benefit plansmay be forced to accept addi-tional regulatory burdens due tothe brouhaha surrounding theircontroversial cousins.

The debate over cash balanceplans has been simmering for al-most two years since the WallStreet Journal began its not-so-subtle assault on the plan design.Since then, most of the legiti-mate legislative discussion hascentered on enhanced disclosureand addressing the so-called“wearaway” problem. However,behind the scenes, a fairly brutaldebate over the very future of theplan design is focused mainly onwhether cash balance plans inher-ently violate the Age Discrimina-tion and Employment Act. Theactors in this play include triallawyers representing participantsin several lawsuits against cashbalance plan sponsors throughout

The Pension Actuary is produced by the executive director and Pension Actuary Committee.Statements of fact and opinion in this publication, including editorials and letters to the editor,are the sole responsibility of the authors and do not necessarily represent the position of ASPAor the editors of The Pension Actuary.

The purpose of ASPA is to educate pension actuaries, consultants, administrators, and otherbenefits professionals, and to preserve and enhance the private pension system as part of thedevelopment of a cohesive and coherent national retirement income policy.

ASPA members are retirement plan professionals in a highly diversified, technical, andregulated industry. ASPA is made up of individuals who have chosen to be among the mostdedicated practicing in the profession, and who view retirement plan work as a career.

Editor in Chief

Brian H. Graff, Esq.

Pension Actuary Committee

Chris Stroud, MSPA, ChairAmy L. Cavanaugh, QPAConstance E. King, CPC, QPARobert M. Richter, APMDaphne M. Weitzel, QPA

Managing Editor

Chris Stroud, MSPA

ASPA Officers

President

John P. Parks, MSPA

President-Elect

George J. Taylor, MSPA

Vice Presidents

Joan A. Gucciardi, MSPA, CPCCraig P. Hoffman, APMScott D. Miller, FSPA, CPC

Secretary

Gwen S. O’Connell, CPC, QPA

Treasurer

Cynthia A. Groszkiewicz, MSPA, QPA

Immediate Past President

Carol R. Sears, FSPA, CPC

Ex Officio Member of the ExecutiveCommittee

Sarah E. Simoneaux, CPC

American Society of Pension Actuaries, 4245 North Fairfax Drive, Suite 750, Arlington, Virginia 22203Phone: (703) 516-9300, Fax: (703) 516-9308, E-mail: [email protected], World-Wide Web: www.aspa.org

Lawrence Deutsch, MSPAKevin J. Donovan, MSPADavid R. Levin, APMMargorie R. Martin, MSPADuane L. Mayer, MSPANicholas L. Saakvitne, APM, Esq.

Layout and Design

Chip Chabot and Alicia Hood

He also chaired a committee that de-veloped ASPA’s Pension Expansionand Simplification Amendments(PESAS). Many of these amend-ments were included in the SmallBusiness Job Protection Act of 1994.

Mr. Taylor is a graduate ofWilliam Patterson College and hascompleted post-graduate studies inactuarial science, corporate and in-dividual taxation, and health and in-dividual insurance. Mr. Taylor liveswith his wife, Betty, in Muncy, Penn-sylvania, on property that has beenin the family for generations. Manyfamily members, including hisgrandson, live nearby.

Mr. Taylor is part owner in araquetball and fitness club, playsraquetball as much as possible, andalso jogs three times a week. Inthe fall, he keeps fit by refereeingfootball games for area high schoolstudents.

The other members of the 2001Executive Committee include:

President-ElectCraig P. Hoffman, APMJacksonville, FL

Vice PresidentsStephen Dobrow, CPC, QPABurlingame, CA

Joan Gucciardi, MSPA, CPCWauwatosa, Wisconsin

Stephen H. Rosen, MSPA, CPCHaddonfield, NJ

SecretaryGwen S. O’Connell, CPC, QPAEugene, Oregon

TreasurerScott D. Miller, FSPA, CPCSouth Salem, New York

Immediate Past PresidentJohn P. Parks, MSPAPittsburgh, Pennsylvania

Ex-Officio Member of theExecutive CommitteeBruce Ashton, APMLos Angeles, CA ▲

Notice of AnnualBusinessMeeting

ASPA’s Annual Meeting will beheld during the 2000 ASPA An-nual Conference on Monday,October 30 from 7:30 a.m. to8:00 a.m. We invite all ASPAmembers to attend and partici-pate in the discussion of mem-bership business. Credentialedmembers of ASPA are encour-aged to attend the meeting andvote for new members of ASPA’s2001 Board of Directors.

SEPTEMBER-OCTOBER 2000 ▲▲▲▲▲ THE PENSION ACTUARY ▲▲▲▲▲ 3

Continued on page 8

Must the Investment Options

in a 401(k) Plan be Tailored to

the Workforce?by C. Frederick Reish, APM, Esq., and Bruce L. Ashton, APM, Esq.

ERISA imposes a duty on the investment fiduciaries ofa 401(k) plan, who are typically the plan committee

members, to prudently select and monitor the investmentoptions offered to the participants.

While there is little in the wayof specific guidance to help fidu-ciaries fulfill those duties, the DOLhas stated the general requirementthat a participant-directed 401(k)plan must have a “prudent andwell-diversified portfolio.” Theregulations under ERISA Section404(c) require that the plan offer a“broad range” of options – definedas investments that “in the aggre-gate enable the participant, bychoosing among them, to achievea portfolio with aggregate risk andreturn characteristics at any pointwithin the range normally appro-priate for the participant. . . .”While 404(c) offers a “safe har-bor,” or defense, for fiduciaries,rather than guidelines for fiduciarycompliance, the broad range re-quirement may well become thegeneral standard for measuring fi-duciary performance in partici-pant-directed plans.

The investment options, whichsatisfy the broad range require-ment, are known as the “core” op-tions. The core options, togetherwith the noncore investment alter-natives that are selected – or “des-ignated” – for participant direction,must be prudently selected and

monitored by the fiduciaries inorder to provide participants withsuitable vehicles for investmentdirection. That is, in a partici-pant-directed plan, the fiduciariesare responsible for providingwell-selected and properly main-tained investment options, andthe participants assume the re-sponsibility for the asset alloca-tion among those options.

Suitability RequirementThe requirement to select and

monitor investment options is com-monly seen as the primary duty ofinvestment fiduciaries. But, isthere another equally importantduty . . . that is, a duty to selectinvestment options that are suit-able, considering the investmentabilities of the participants?

ERISA does not have a specificrequirement that investment fidu-ciaries consider the investmentabilities of employees. However,the general fiduciary requirementsof ERISA are worded broadlyenough that they could be inter-preted to include such a require-ment. For example, ERISArequires that the investment fidu-ciaries select the investment op-t ions “with the care, ski l l ,

prudence, and diligence under thecircumstances then prevailing thata prudent man, acting in a like ca-pacity and familiar with such mat-ters, would use in the conduct ofan enterprise of a like character andwith like aims.” Would a prudentfiduciary designate only invest-ments that participants are capableof properly using? Further, the fi-duciaries must fulfill their duties“. . . for the exclusive purpose ofproviding benefits to participants. . ,” that is, in a participant-directed401(k) plan, the fiduciaries mustselect investments consistent withthe purpose of providing retirementbenefits for participants.

In addition, in the preamble tothe 1987 proposed regulations un-der Section 404(c), the DOL statedits view of the responsibility of in-vestment fiduciaries:

“...[T]he independent fiduciarygenerally would discharge hisoversight duties by prudentlyselecting the investment funds(or investment managers), peri-odically evaluating their per-formance, and determining,based on that evaluation,whether the funds should con-tinue to be available as partici-pant investment options. Inmaking these decisions the fi-duciary would, of course, con-sider the special characteristics

Farewell to Section 415(e)by Margery F. Paul, MSPA, MAAA, EA

F or most plans, the long awaited repeal of Code Section415(e) has taken place. Effective for limitation years

beginning after December 31, 1999, this repeal is resulting ina resurgence of defined benefit plans. Practitioners, puzzledby the complex rules described in IRS Notice 99-44, havespent a considerable amount of time attempting to determinethe maximum benefits that can be provided in defined benefitplans after 1999.

This article will discuss the impactof the repeal as it affects (1) formerplan participants who no longer par-ticipate in a defined benefit pensionplan and are either receiving annuitypayments from the plan or who re-ceived a distribution of the totalamount of benefits to which theywere entitled, (2) participants whowere covered under both a definedbenefit plan (“DB plan”) and a de-fined contribution plan (“DC plan”)prior to the repeal of Code Section415(e) and received a distribution oftheir benefits from the DB plan whenit was terminated, and (3) participantswho were covered under both a DBplan and a DC plan prior to the re-peal of Section 415(e) and who havenot received a distribution from theDB plan that is still in existence.

This article will also discuss whichemployers and participants stand tobenefit most from the repeal of415(e) and provide some examplesof possible contribution levels afterthe repeal.

1. Former plan participants, notcurrently covered by a DB plan:

As stated in IRS Notice 99-44, aDB plan can provide for benefit in-creases to reflect the repeal of Section

415(e) only for former participantswho accrue additional benefits underthe plan on or after the effective dateof the repeal. These benefits mustbe benefits that can be accrued with-out regard to the repeal.

This provision of Notice 99-44(Q&A-3) is intended to provide re-lief to plan sponsors from having toprovide additional benefits to formerparticipants whose distributions fromthe plan were limited by Section415(e), and to current employeeswho are no longer participating in theDB plan. However, all employeeswho are eligible to accrue additionalbenefits under the plan and who willdo so either because of an increasein the plan’s benefit formula or dueto cost of living increases in theSection 415 dollar limits, will ben-efit from the repeal of Section415(e). Their future benefit accru-als will not be limited by their oldDC fractions that no longer exist.

Example: Dr. Jones had spon-sored both a DB plan and a DCplan prior to the effective dateof TRA ‘86. Before the effec-tive date of the Section 415 pro-visions of TRA ‘86 (January 1,1987), Dr. Jones terminated the

DB plan and received a distri-bution of his maximum allow-able lump sum benefit takinginto account the Section 415(b)and Section 415(e) limits at thedate of distribution. Dr. Jonescontinued to make contributionsto the DC plan.

As of January 1, 2000, the ef-fective date of the repeal,Dr. Jones and his partner, Dr.White, establish a new DB plan.This plan covers Dr. Jones, Dr.White, who is Dr. Jones’younger partner, and severalemployees. Normal RetirementAge (“NRA”) under the plan isage 63. Normal form of ben-efit is life annuity. The defini-tion of actuarial equivalence inthe new plan is as follows: Pre-retirement Mortality: None;Post retirement Mortality: ’83GAM Unisex; Pre- and Post-Retirement Interest: the appli-cable interest rate under GATTwhich, for the year 2000, is de-fined by the plan to be 6.35%.

Dr. Jones asks if he can accrueadditional benefits in the newplan, especially since Section415(e) has been repealed.

Scenario 1: Assume Dr. Joneswho is currently age 63 (bornin 1937) had completed twoyears of participation in the oldDB plan prior to the date it wasterminated. NRA under theplan was age 55. Since Dr.Jones had 10 years of serviceas of the effective date of TRA‘86, and the plan provided the

SEPTEMBER-OCTOBER 2000 ▲▲▲▲▲ THE PENSION ACTUARY ▲▲▲▲▲ 5

Leased Employees,

the Plot Thickensby S. Derrin Watson, APM

The concept of “leased employees” was added to theInternal Revenue Code eighteen years ago. In the

nearly two decades that have followed, there remains sub-stantial confusion about what a leased employee really is.This confusion stems from uncertainty over who is the “real”employer of someone working under a leasing agreement.

Code §414(n)(2) begins its defi-nition, not by telling us who a leasedemployee is, but by specifying whomit is not: “…the term ‘leased em-ployee’ means any person who is notan employee of the recipient.” Oncea worker crosses that threshold, thenand only then do we ask if the affir-mative requirements of leased em-ployee status are met:

• Performance of services under anagreement between a leasing or-ganization and the recipient;

• Performance of services on a sub-stantially full-time basis for oneyear; and

• Performance of services under therecipient’s primary direction andcontrol.

Unfortunately, there are manypractitioners and clients who have themistaken view that “If you’re not onmy payroll, you’re not my em-ployee.” Therefore, anyone who is onthe payroll of a staffing firm is pre-sumably a leased employee if theyhave satisfied the substantially full-time requirement. Nothing could befurther from the truth! Going back

to the early 1970s, case after case hasfound that workers on the payroll ofstaffing firms are common law em-ployees of the companies for whichthey are performing services. Whilethere are rulings going the other way,they involve situations in which thestaffing firm had significant super-visory authority. If the recipient is thecommon law employer, then it musttreat workers obtained through astaffing firm exactly as it does othercommon law employees. Dependingon the terms of the plan, this maymean they are entitled to coverageunder the plan, although in appropri-ate situations a well-drafted provi-sion can exclude them.

Professional & Executive LeasingA classic case dealing with these

situations is Professional & Execu-tive Leasing (PEL). PEL “hired” pro-fessionals and business owners towork for it. PEL then “leased” thesepeople back to their own businesses.PEL charged those businesses thesame amount they were paying insalaries and benefits, plus a percent-age to cover bookkeeping and profit.PEL covered these “employees”

under generous pension and otherbenefit plans and argued that they didnot need to provide comparable plansfor the recipient businesses.

The arrangement was clever. If ithad worked, it would have allowed abusiness owner to cover himself un-der a plan (by signing up with PEL),but not provide any benefits for hisemployees (who were not “em-ployed” by PEL).

PEL filed a petition for declara-tory relief to receive a determinationthat its plans were qualified. The IRSargued that the plans violated the ex-clusive benefit rule because the pro-fessionals and owners were not trulyemployed by PEL under commonlaw rules. The Tax Court and Courtof Appeals agreed, finding that PEL’s“right to control . . . was at best illu-sory.”

In light of this decision, it is re-markable that there are still compa-nies that put their owners on thepayroll of staffing firms in order tocover them under the staffing firmpension plans. There is no credibleargument that the owners are actu-ally employees working under thecontrol of the staffing firm. Such anarrangement could disqualify theentire plan, as it did PEL’s plan, forfailure to satisfy the exclusive ben-efit rule. The only way around this isto have the staffing firm’s client, therecipient company, cosponsor theplan. The parties must recognize for

Washington Updatethe country, participant rightsgroups enjoying newfound atten-tion as a result of the controversy,and groups representing businessesand retirement plan professionals.This, of course, includes ASPA,which believes that cash balanceplans are an effective plan designproviding quality retirement ben-efits for employees that should beallowed to continue. Further,ASPA believes that, if any reme-dial legislation is deemed neces-sary, it should be carefully tailoredto do no harm to traditional definedbenefit plans.

The only legislation resultingfrom the cash balance controversyto actually pass either chamber ofCongress has been limited to dis-closure. A provision included inthe House-passed version of pen-sion reform requires affected par-ticipants to be given written noticeof any plan amendment signifi-cantly reducing future benefit ac-cruals within a reasonable periodof time (to be defined in Treasuryregulations) before the amendmenttakes effect. The notice would haveto provide sufficient information(as defined by Treasury) to allowparticipants to understand the ef-fect of the amendment. Failure tocomply with the notice require-ment would subject the employerto an excise tax equal to $100 perday per failure, up to $500,000.This proposal would not apply toplans with 100 participants or less.This provision is effective on thedate of enactment and good faithreliance applies until Treasuryregulations are issued.

The House provision passed un-eventfully. In fact, virtually noth-ing was said about the cash

balance controversy during thedebate over the pension reformbill on the House floor. This willnot be the case in the Senate. Thepension reform bill, approved bythe Senate Finance Committee onSeptember 7, includes a muchmore detailed and rigorous disclo-sure regimen and also addresses“wearaway.” Under the Senatebill, affected participants wouldhave to be given written notice ofany plan amendment significantlyreducing future benefit accrualswithin 45 days before the amend-ment takes effect. The notice mustinclude: (1) the effective date ofthe amendment; (2) a statementthat the amendment is expected tosignificantly reduce the rate of fu-ture benefit accruals; (3) a de-scr ipt ion of the classes ofemployees reasonably expected tobe affected; and (5) notice of eachparticipant’s right to request anannual benefit statement.

In the case of a conversion to acash balance plan, no less than 15days before the effective date, af-fected participants would have tobe given a “benefit estimation toolkit” to enable participants to fig-ure out the effect of the amend-ment on their benefits. For thispurpose, a cash balance plan is adefined benefit plan where the ac-crued benefit is expressed in termsother than as a single life annuity(e.g., an accumulation account).Treasury would be given the au-thority to expand this definition toinclude other similar hybrid plans.

The penalty structure would be thesame as the House bill. However, theSenate provision would apply toplans with 100 participants or less.The provision would be effective for

amendments taking effect after thedate of enactment. In response toconcerns raised by ASPA, bothSenate Republicans and Democratsare considering delaying the effec-tive date of the provision for planswith 100 participants or less untilafter final Treasury regulations arepublished so that smaller planshave the guidance needed to com-ply.

As noted, the Senate bill alsoaddressed “wearaway” in the con-text of a conversion to a cash bal-ance plan. Under the Senateprovision, the accrued benefit un-der a converted cash balance plancould not be less than (1) the ben-efit accrued for years of serviceprior to the date of the conversion(without regard to any subsidies),plus (2) any benefit accrued foryears of service after the date ofconversion under the cash balanceplan benefit formula. If partici-pants’ opening account balancesequal the present value of the oldplan benefit as of the effective dateof the conversion, the plan wouldalways be deemed to satisfy thisrequirement. Alternatively, theold plan benefit could be providedin a lump sum separate from thecash balance plan benefit using theinterest and mortality tables in ef-fect as of the date of conversion.The Senate provision would alsoaddress the so-called “whipsaw”problem that sometimes results inthe payment of a lump sum ben-efit out of a cash balance plan thatis different than the amount in aparticipant’s accumulation ac-count.

The Clinton Administration hasalso finally weighed into this de-bate, calling for a complete elimi-nation of wearaway in the contextof cash balance plan conversions,including eliminating wearaway ofearly retirement subsidies.

SEPTEMBER-OCTOBER 2000 ▲▲▲▲▲ THE PENSION ACTUARY ▲▲▲▲▲ 7

Needless to say, the provisionhas been highly controversial, pro-voking a very negative article in theWall Street Journal and a publiccondemnation from the AmericanAssociation of Retired Persons andthe Pension Rights Center. Thesegroups argue that early retirementsubsidies should also be protected,although they provide no specificson how this would be accom-plished. However, underlying their

FSPA

Howard L. Polivy

MSPA

William A. DreherAndrew C. Martin

Laura L. Mitchell-VelaKevin J. Morris

Eric Waldschmidt

CPC

Edwin O. AkwenukeLinda S. Badilo

Kevin A. BergdorfSteven A. Blom

Rajean M. BosierJoni J. Castle

Marie F. DawsonJohn R. Dean

Karen F. DixonDaniel E. FisherSarah R. GilmoreTamara L. Grover

Gene M. GutschenritterMargaret C. HillerMartin D. JantzenRonald E. Kanar

Robert M. KaplanTerry P. Kelly

Puamana C. KoerlinHans F. KraabelSteven M. LoseffDavid Pasternack

Howard L. PolivyRenee C. Richmond

David S. RoweRussell D. SmithRobert S. WilderPaul H. Young

QPA

Brian A. AhrensRoberta C. Kress Angelo

Robert Stan AnthisKevin A. Bergdorf

David S. BewieSamuel BrandweinDavid K. Campbell

Milan J. CapelaElena J. Daniell

Patricia A. DanielsKarol Digmann

Eric C. DroblyenPhyllis A. EllisonEileen D. FabianoJennifer Garvin

Minerva A. GuinnRonald A. Hall

Margaret A. HofstaedterAnna M. Hunter

Christina M. JacobsonAaron J. Juckett

Peter A. KneedlerAnnette R. LaneValerie A. Lange

Dolores C. Lombardi

Nancy J. ManaryBradley S. Markins

Renee E. MayneThomas J. Meyer

Lori L. OrczykowskiElizabeth A. PalmerTami M. PlummerShane P. PrimmerRegina R. RayosKelly E. Renno

Kristi L. RosselandFrank D. Saia

Christopher T. SamosGregory N. SchedlerHans C. Schemmel

Jeffery A. SeedJennifer A. Self

Jeffrey S. StoltzfusRichard H. Thompson

David J. TurpinCheryl A. VanDenHandel

Mittie T.C. WatkinsWendy L. Wilson

Ichabod Yu

APM

Dianne L. HartDarren R. Telford

William Edgar Turco

Affiliate

Alieze A. AustinJohn Barron

efforts is a desire to prevent anylegislation that legitimizes the con-cept of cash balance plans. They,along with trial lawyers attackingthe viability of the design, areafraid that a statutory definition ofcash balance plans will interferewith current litigation. In otherwords, many of them would reallyprefer no legislation, even if iteliminates wearaway, despite pub-lic suggestions to the contrary.

It is far from clear how these po-litical games will play out. Unfor-tunately, it is clear that no matterthe result, pension policy will suf-fer. ▲

Brian H. Graff, Esq., is ExecutiveDirector of ASPA. Before joiningASPA, Mr. Graff was legislationcounsel to the U.S. Congress JointCommittee on Taxation.

Angela BerryDenise R. Bolger

Robert L. ChristiansenLisa A. Crowell

Bert M. DeardorffMaria Delin-PellishBelinda L. FairbanksBarton G. FlemingJanice A. ForbingKristin L. Francis

Jason FuTerry GenslerAnne Hannon

Amy R. HarrenElizabeth A. Herman

Kimberly A. HlavacekChristine Hulbert

June JacobsW. Clain Jaques

Patricia Cooper JonesGary Keener

Karen KirklandJayme Lealtad

James A. LynchCameron MacLeod

Michael MallonDennis Miceli

Brenda S. MijalLaura Gene Miller

Susan L. MinerChristopher S. Moore

Melissa F. NeelyNorman J. Nicolay

Michael S. OuelletteDee Ann Pederson

Bea PerryJohn M. PetroskyApolonia RehillDiana L. RickerPeter K. Riggins

Carol J. RingwaldGerald R. Rowe, Jr.

G.R. SanidadJoan E. SchererLinda Schirmer

Jeffrey S. SkinnerTim Slavin

Jodina SnyderKelly F. Somoza

Tommy M. StringerDebra L. Sullenbarger

Doris TakieddineCynthia J. TaylorChristi ThompsonRobert J. Toth, Jr.Michael E. TripodiLoriJo S. Turner

Nancy E. TwitchellSusan A. Whittle

Raymond W. WilliamsTim Wright

Dennis E. Zobell

W E L C O M E N E W M E M B E R S

Welcome and congratulations to ASPA’s new members and recent designees.

Investment Options in a 401(k) Planof ERISA Section 404(c) [i.e.,participant-directed] plans.”(Emphasis added.)

Further, in 1992 in the preambleto the final 404(c) regulations, theDOL stated its view that, in select-ing and monitoring the investmentoptions, the fiduciaries were re-quired to determine that the optionswere “suitable and prudent invest-ment alternatives for the plan.”

Could those general responsibili-ties of ERISA fiduciaries require thatthe investment skills of theworkforce be considered in select-ing appropriate 401(k) investmentoptions; that is, is there a “suitabil-ity” requirement? Should a prudentfiduciary consider the investmentknowledge of a plan’s participants inthe process of selecting the 401(k)investment options? Apparently theDOL thinks so.

At the 1999 ASPA Annual Con-ference, representatives of the Pen-sion and Welfare BenefitsAdministration (PWBA) of theU.S. Department of Labor (DOL)were asked a general questionabout compliance with Section404(c) of ERISA. While the directanswer may not surprise you, thecomment volunteered by thePWBA at the end of its response iseye-opening:

Question: What is theDepartment’s view of the extentof ERISA Section 404(c) com-pliance? What problems has theDepartment seen in the 404(c)compliance area in conductingits investigations?

Response: In general, compli-ance with the ERISA Section404(c) regulations is not re-viewed by the Department, as

this is viewed as mainly a de-fense for the fiduciary. Theremay be an issue if a fiduciary isrepresenting to plan participantsthat the plan is a 404(c) plan,but the fiduciary is clearly notcomplying with the 404(c) regu-lations. In general, enforcementby the Department is focused onthe mandatory requirements im-posed by ERISA but not on thevoluntary aspects, unless it risesto the level of misrepresentationto plan participants. The De-partment does have a concernwith the broader issue ofwhether a 404(c) plan is ap-propriate given the nature ofa particular employer’sworkforce. (Emphasis added.)

A reasonable reading of the an-swer is that the DOL believes that,for employers with employees wholack the knowledge and sophistica-tion to manage the investment of re-tirement funds, it could be a breachof fiduciary duty to permit partici-pant-directed investments, or, at theleast, that the employer in that casewould not be entitled to 404(c) pro-tection. If this reading is correct,then by logical extension it wouldequally be a breach of fiduciary dutyto offer participants investment op-tions that were inappropriate, tak-ing into account their investmentknowledge and abilities. For ex-ample, under this line of reasoning,if the employee population wererelatively unsophisticated about in-vesting, the employer and the planfiduciaries would be obligated tolimit the investment options (per-haps both the number and type) tothose that could be understood andprudently managed by the employ-ees.

Selecting Investment OptionsBut, what if an employer wants to

offer more fund options – because,for example, the workforce includessome employees who are sophisti-cated in investment matters?

The employer should be able todo that if the program is designedin a prudent matter with an eye tothe employees’ needs. (In the dis-cussion that follows, we mentionvarious investment strategies. Indoing so, we do not mean to sug-gest that any given strategy is legallyrequired.) For example, as a basicinvestment program for employeeswho are not knowledgeable in in-vesting, the plan could offer a rangeof lifestyle funds, with well-de-signed questionnaires to assist em-ployees in picking the right fund fortheir performance goals and risk tol-erances. In addition, with a limitedselection of individual funds – forexample, one in each of the appro-priate asset classes and styles – webelieve the plan could satisfy theDOL’s interpretation of ERISA’s fi-duciary requirements, if the partici-pants were offered an investmenteducation program designed and de-livered in a manner appropriate forthe options offered and for the levelof investment knowledge of the em-ployees. Since the funds in this ex-ample are limited to one in eachasset class and style, the educationalefforts could focus on asset alloca-tion issues rather than specific fundselection. If the plan were to offermore than one fund in an asset classor style, then the investment educa-tion program would need to coverboth asset allocation and investmentselection. Additionally, the programwould need to educate the employ-ees on how to select among the in-vestment options in a given category(e.g., large capitalization U.S. equi-ties).

As the number of investment op-tions increases, the fiduciaries

SEPTEMBER-OCTOBER 2000 ▲▲▲▲▲ THE PENSION ACTUARY ▲▲▲▲▲ 9

should consider adding an invest-ment advisory service. Dependingon the characteristics of a particu-lar workforce, the employees maynot be able to manage a larger andmore complex array of investmentswith only educational programs.Under the DOL’s reasoning, prudentfiduciaries would, at that point, needto add investment advice to theirplan’s package of investment prod-ucts and services. Of course, thatadvisory service must be prudentlyselected and monitored by the fidu-ciaries.

But, what if the employer wantsto offer options that have the poten-tial for greater gains and greaterlosses, for example, sector funds –like a technology fund or a healthcare fund?

As a part of the regular invest-ment education/advice program, andperhaps as a part of the plan’s sum-mary plan description (to ensure thatthe participants received the infor-mation), a cautious fiduciary wouldprovide the employees with clearcommunication about the volatilityof those investments and about thepotential for larger losses andgreater gains. The employer/fidu-ciaries should tell the participants inwriting that, if they are not knowl-edgeable about such investments,they are assuming a high degree ofrisk by selecting them. The invest-ment education program shouldhave a segment on the more volatileoptions designed to assist employ-ees who want to participate in thoseoptions. Further, the fiduciariesshould offer an investment advisoryservice to the participants. WhileERISA imposes a burden on planfiduciaries to prudently select andmonitor the providers of investmentadvice, the risk of not providing thatadvice, particularly with an invest-ment menu that includes diverse andvolatile options, is greater than theburden.

Nondesignated InvestmentOptions

Finally, what if an employerwants to offer virtually unlimited in-vestment options, such as a broker-age window or a mutual fundwindow with 1,000 or more mutualfunds?

The ERISA Section 404(c) regu-lations divide investments into twocategories: (1) those which are“designated” by the investment fi-duciaries and (2) a universe of in-vestments which constitutes all ofthe investments administrativelyfeasible for the plan to offer (or“nondesignated” investment op-tions). DOL Reg. §2550.404c-1(e)(4) defines a “designatedinvestment alternative” as “a spe-cific investment identified by a planfiduciary as an available investmentalternative under the plan.” The pre-amble to the 404(c) regulations de-fines the nondesignated category as“those plans which permit invest-ments in any asset which it is ad-ministratively feasible for the planto hold and do not specifically de-scribe any investment alternative.”The consequence of an investmentoption being considered “desig-nated” or “nondesignated” is thatplan fiduciaries must prudently se-lect and monitor – and, where re-quired, remove – the designatedinvestment options. Such removal,at least for 404(c) compliance, is notrequired for the nondesignated op-tions. While it is easy to concludethat a limited list of funds is a set ofdesignated options and that a virtu-ally unlimited number of invest-ments is nondesignated, it is difficultto know exactly where the transitionfrom designated to nondesignatedoccurs as a plan moves from a lim-ited number of funds to an unlim-ited universe.

Although the 404(c) regulationsare not entirely clear on this issue,the brokerage windows would argu-

ably be considered “nondesignated.”That is, since such a large body ofinvestments is being offered, theywould likely be considered to be allthe options that are “administra-tively feasible” for the plan to offer.However, it is less clear whether thefunds in the mutual fund windowwould be considered “designated.”The preamble to the 404(c) regula-tions defines the “nondesignated”category as one that does “not spe-cifically describe any investment al-ternative.” Theoretically, anymutual fund window can “describe”the funds it contains, so the appli-cation to a mutual fund window isless than clear.

If funds are not designated – thatis, if the plan offers all the invest-ment options that are administra-tively feasible for the plan to hold,the employer and the investment fi-duciaries are not considered to haveselected the individual investments.Thus, while the fiduciaries’ dutieswould cover the “process” of mak-ing sure that the “window” is work-ing as it should, those duties wouldnot require that the specific invest-ments be prudently selected andmonitored by the fiduciaries. In thatcase, it is advisable for the fiducia-ries to inform the participants thatthey have not selected the individualinvestment options in the brokerageor mutual fund window and that theyare not monitoring them. It shouldbe clear to the participants that theyare not protected by the selectionand monitoring process, as they arefor the designated options. That ex-planation should be in writing (per-haps in the SPD), and it should beregularly distributed or made avail-able to the participants. Further, theparticipants should be told that theappropriate use of the window re-quires investment expertise, thatthey are proceeding at their ownrisk, and that investment options inthe window have the potential for

ASPA and BNA are working together to provide ASPA members witha discount on the BNA web publication, Pension & Benefits Daily.This on-line publication is a resource for news reports and source docu-ments in the pension and benefits industry. The daily news serviceupdates subscribers on pension and tax legislation and regulation; sig-nificant case law developments; tax policy and guidance; IRS revenuerulings and procedures; ESOPs; fiduciary responsibilities; deferredcompensation; multi-employer plans; plan terminations; …and more!Subscribers receive daily e-mail highlights that link instantly to thefull text of any Pension & Benefits Daily article.

Through mid-October, ASPA members were able to access this on-line publication free of charge. Full text articles of the Pension &Benefits Daily were available at http://web.bna.com/alpha.htm byentering ASPA’s temporary Username: aspatrial and Password: aspa.

ASPA and BNA will assess the success of the program, and givensufficient interest, all active members of ASPA will be able to sub-scribe to the Pension & Benefits Daily at a 30% discount. We hope tointroduce this discount program at ASPA’s Annual Conference on Oc-tober 29 , 2000.

Both ASPA and BNA are confident that this new member benefit isone that will be invaluable to all benefits professionals! For comments,questions, or for more details, please contact Amy Iliffe, Director ofMembership, at (703) 516-9300 or e-mail [email protected].

ASPA's Education and Exami-nation Committee's divisionalchairs have selected Cheryl L.Morgan, CPC, as the recipient ofthe 2000 Educator's Award. Cherylcurrently delivers pension educa-tion on the Internet and is a fre-quent speaker and author onretirement plan topics. She servedas a member of the Education andExamination Committee and asASPA's director of technical edu-cation.

Cheryl has been involved inASPA's education program for

over 19 years.On the basisof her manyachievements,ASPA is proudto honor andpresent Cherylwith the 2000E d u c a t o r ' sAward.

Past recipients of the Educator'sAward include Charles J. Klose,FSPA, CPC; Janice M. Wegesin,CPC, QPA; and David Farber,MSPA, EA, ASA.

2000 Educator's

Award Recipient

greater volatility and for greaterlosses. The DOL’s position on“suitability” could arguably requirethat, for employees who lack theknowledge to prudently invest in amutual fund or brokerage window,the fiduciaries offer appropriateinvestment education, and adviceprograms. With the appropriatecombination of communication, in-vestment education, and advice, fi-duciaries should be able to satisfythe DOL’s position that the 401(k)investments be suitable for theworkforce.

ConclusionIf the DOL’s reading of the law

is correct, then employers and in-vestment fiduciaries need to con-sider the “suitability” of the 401(k)investments for their workforce.There are a variety of ways to de-sign the investments to match theworkplace, taking into considerationthe number of funds, the types offunds, the complexity and volatilityof the investments, the programs inplace for investment education andadvice, and communication aboutthe risks and the degree of fiduciaryoversight. But the key criteria is thatthe investment options, the invest-ment abilities of the participants,and the education, advice, and com-munication programs be coordi-nated to enable the participants tointelligently choose and allocateamong the options. ▲

C. Frederick Reish, APM, Esq., is afounder of and partner with the LosAngeles law firm Reish & Luftman.He is a former cochair of ASPA’sGovernment Affairs Committee andis currently the chair of GAC’s LongRange Planning Committee. BruceL. Ashton, APM, Esq., a partnerwith Reish & Luftman, is cochair ofthe Government Affairs Committeeand serves on ASPA’s Board of Di-rectors.

SEPTEMBER-OCTOBER 2000 ▲▲▲▲▲ THE PENSION ACTUARY ▲▲▲▲▲ 11

maximum allowable Section415 benefit after 10 years ofservice, he was fully accruedin his DB plan annual benefitof $75,000 payable at age 55.Assume Dr. Jones’ DC fractionas of December 31, 1986 was.5. Therefore, Dr. Jones’ ac-crued DB plan benefit limitedby Section 415(e) was$75,000 x .5, or $37,500. Dr.Jones, who was 49 at the plantermination date, was paid thepresent value of the $37,500annual benefit as a lump sumon December 20, 1988. Thisamount was $395,000.

The plan’s actuary determinedthat, as of December 31, 2000,Dr. Jones would have two yearsof participation in the old planand one year of participation inthe new plan. For purposes ofSection 415, the old plan andthe new plan are aggregated.Therefore, Dr. Jones’ totalyears of participation as of De-cember 31, 2000 is three years.Since NRA in the new plan isage 63, the maximum accruedbenefit to which Dr. Joneswould be entitled in the newplan, under current Section415(b) limitations, [(3/10 x$135,000 x .8667 (the reduc-tion for NRA less than 65)], is$35,100. This is less than the$37,500 benefit he had previ-ously accrued in the old plan,even before his old plan benefitis adjusted to an actuariallyequivalent benefit at age 63.Under Notice 99-44, Dr. Jonesis not eligible to accrue a ben-efit in the new plan unless anduntil he is able to accrue anadditional benefit without re-

C O N T I N U E D F R O M P A G E 4

Farewell to Section 415(e)gard to the repeal of Section415(e). This is a different re-sult from the one that would beobtained if Notice 99-44 hadsaid that, effective in the year2000, the 415(e) limitationswould be treated as though theyhad never existed. If this ap-proach had been taken, Dr.Jones’ accrued annual benefitas of December 31, 1986 mighthave “popped up” to $75,000,allowing funding of the portionthat was not paid.

Conclusion: Dr. Jones is noteligible to accrue a benefit inthe new plan. He would haveto be credited with severalyears of participation beforethe current 415(b) limit wouldexceed the amount he was pre-viously paid.

2. Participants who were coveredby both a DB plan and a DCplan, who received a distribu-tion from the DB plan and whoaccrue additional benefits in anewly established DB plan in2000:

Scenario 2: The facts are thesame as in Scenario 1 exceptthat Dr. Jones had 10 years ofparticipation in the prior planat the time it was terminated.Effective January 1, 2000, Dr.Jones and his partner, Dr.White, establish a new DBplan.

Dr. Jones again asks if his prioraccrued benefit, which waslimited by Section 415(e), canbe restored.

The plan must determine if Dr.Jones will be able to accrue ad-ditional benefits under the DBplan due to cost-of-living in-

creases in the Section 415(b)limits. If yes, Dr. Jones’ maxi-mum allowable Section 415(b)benefit in the new plan will becalculated without regard toany prior DC fraction.

To determine whether Dr. Jonescan accrue additional benefits,Dr. Jones’ maximum Section415(b) benefit in the new planmust be reduced by the actu-arial equivalent of the benefithe received from the old DBplan. For this purpose, actu-arial equivalent is determinedbased on the new plan’s defi-nition of actuarial equivalenceat the time the calculations areperformed.

The following calculations areperformed:

Dr. Jones’ lump sum payoutat age 49 was $395,000. Theactuarially equivalent benefitunder new plan assumptionsis determined as fol lows:$395,000 x (1.0635)14/11.3172which equals $82,639. Sincethe Section 415(b) limit in theyear 2000 at NRA=63 is$117,000, i.e., $135,000 x.8667 (the reduction factor forNRA less than 65), Dr. Jonesis able to accrue additional ben-efits under the new plan.Therefore, his accrued benefitunder the new plan is no longerlimited by Section 415(e). Infact, since Dr. Jones has at-tained NRA under the new plan(age 63), he is now fully ac-crued in the 415(b) limit at age63 which is $117,000. There-fore, additional funding of($117,000 - $82,639) x 11.3172which equals $388,870 will berequired to fully fund Dr. Jones’plan benefits. Depending onthe plan’s funding method andactuarial assumptions, it is pos-sible that this contribution

Note: A plan sponsor who doesnot wish to provide this “pop-up” in DB plan benefits, shouldamend the plan prior to the endof the remedial amendment pe-riod to limit the increase due tothe repeal of Section 415(e). Ofcourse, if the plan incorporatedthe Section 415 limits by refer-ence, as stated in Notice 99-44,an amendment would need tohave been made prior to the be-ginning of the 2000 year.

A new plan should include anysuch limits at the time of itsadoption.

3. Participants who were coveredunder both a DB plan and a DCplan prior to the repeal of Sec-tion 415(e) and who have not re-ceived a distribution from theDB plan:

Scenario 3: Mr. Smith has par-ticipated in both a DB plan anda DC plan for more than 10years. The plan year is a calen-dar year. NRA under the plansis age 65 and the DB plan’s ben-efit formula is 100% of pay.Mr. Smith’s high 3-year aver-age compensation is $160,000.Assume that the normal form ofbenefit under the plan is a lifeannuity and that Mr. Smith wasborn in 1940. Also assume thatas of December 31, 1999, Mr.Smith’s DC plan fraction is .6.Therefore, his maximum pro-jected annual annuity benefitunder the DB plan is $126,000[($135,000 x (1-.06667)] x .4,or $50,400. Effective January1, 2000, the plan is no longerrequired to limit Mr. Smith’sbenefit due to the application ofSection 415(e). This means thatMr. Smith’s maximum pro-jected annual benefit under thePlan as of January 1, 2000 is

$126,000, i.e., an increase of$75,600. If Mr. Smith’s lumpsum benefit is to be fully fundedat age 65, the additional fund-ing requirement at age 65 is$75,600 x 10.8221, whichequals $818,151 based on the’83 GAM Unisex Table and6.35% interest. Dependingupon the plan’s actuarial as-sumptions and methods, thisamount funded over five yearswould require an annual contri-bution of more than $100,000.Assuming Mr. Smith’s benefitsin the plan were fully fundedprior to the repeal of Section415(e), the annual contributionrequired to fund his normal re-tirement benefit increases fromzero to more than $100,000.

See the note in Scenario 2above regarding plans that donot want to provide this typeof “pop-up.”

Who Will Benefit the Most?The repeal of Section 415(e) will

provide most executives who, at anytime, participated in a DC plan withthe opportunity to accrue substantialbenefits in DB plans. Nonhighlycompensated participants will alsobenefit from the rebirth of the DBplan because employers will be re-quired to make larger contributionson their behalf.

We expect the greatest benefits toinure to professional firms andclosely held businesses with olderpartners, owners or shareholders.Because of TRA ‘86, many compa-nies terminated their DB plans dueto the impact of Section 401(a)(26),which requires a DB plan to coverthe lesser of 40% of eligible employ-ees or 50 employees and reducedSection 415 limits. Most of theseplans were terminated prior to theend of 1989. They were generallyreplaced by 401(k) profit sharing andmoney purchase pension plans. After

TRA ‘86 was passed, many employ-ees under the age of 45, when giventhe choice, participated in DC plansbecause they could accrue larger ben-efits in a DC plan than in a DB plan.However, with the aging of the popu-lation (those 40 year old employeesin 1989 are now in their fifties), sub-stantial benefits can now be accruedin DB plans. In addition, many em-ployers can continue to sponsor theirpopular 401(k) profit sharing plans.

Just as companies with existingDC plans can now set up DB plans,companies that currently sponsor DBplans can now establish DC plans. Inaddition, many employers who spon-sored overfunded or fully funded DBplans that were terminated and wereprecluded from setting up DC plansfor their owners, partners and share-holders because of the limitations ofSection 415(e), can now establish DCplans.

Caution: If any participant ben-efits from both a DB plan and aDC plan of the same employer,Section 404(a)(7) limits theemployer’s maximum deduct-ible contribution to the greaterof 25% of the pay of all eligibleemployees, or the requiredminimum contribution to theDB plan.

The above limitation dictates thata company that sponsors both a DBplan and a DC plan for its sole share-holder employee will be limited to amaximum deductible contributionfor the year 2000 of $42,500 (i.e.,25% of $170,000). If a $30,000 con-tribution is made to the DC plan, themaximum deductible contribution tothe DB plan is $12,500. In this situ-ation, the employer will most likelyopt not to set up the DB plan. How-ever, if the sole shareholder is in hisor her mid-forties or older, the DBplan will often require a contributionin excess of $42,500 which will makethe DC plan unnecessary. While

SEPTEMBER-OCTOBER 2000 ▲▲▲▲▲ THE PENSION ACTUARY ▲▲▲▲▲ 13

there are ways to use the rules re-garding the timing of contributionsto increase the total deduction whenan employer maintains both amoney purchase plan and a DB plan,these techniques are beyond thescope of this article.

The repeal of Section 415(e) isalso helpful in dealing withoverfunded DB plans (i.e., plans inwhich there are excess assets thatcannot be distributed to participantswithout creating a reversion of theseexcess assets to the employer).Sponsors of these plans can now setup qualified replacement DC plans,transfer at least 25% of the DB planexcess assets to the newly estab-lished plan, and allocate maximumcontributions under Section 415(c)to the plan participants to use up asmuch of the excess assets as pos-sible. Prior to the repeal, it was notpossible for a participant who hadaccrued maximum benefits in a DBplan (i.e., their DB fraction was 1.0),to receive additional allocations ina DC plan sponsored by the sameemployer.

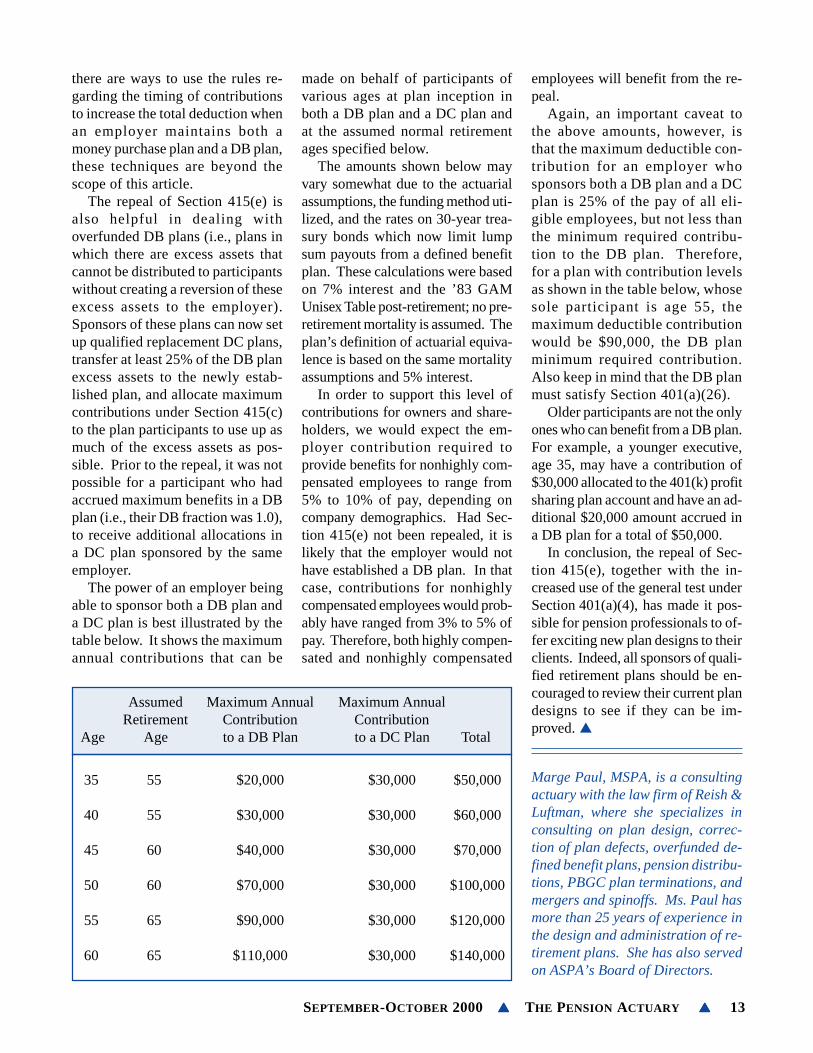

The power of an employer beingable to sponsor both a DB plan anda DC plan is best illustrated by thetable below. It shows the maximumannual contributions that can be

made on behalf of participants ofvarious ages at plan inception inboth a DB plan and a DC plan andat the assumed normal retirementages specified below.

The amounts shown below mayvary somewhat due to the actuarialassumptions, the funding method uti-lized, and the rates on 30-year trea-sury bonds which now limit lumpsum payouts from a defined benefitplan. These calculations were basedon 7% interest and the ’83 GAMUnisex Table post-retirement; no pre-retirement mortality is assumed. Theplan’s definition of actuarial equiva-lence is based on the same mortalityassumptions and 5% interest.

In order to support this level ofcontributions for owners and share-holders, we would expect the em-ployer contribution required toprovide benefits for nonhighly com-pensated employees to range from5% to 10% of pay, depending oncompany demographics. Had Sec-tion 415(e) not been repealed, it islikely that the employer would nothave established a DB plan. In thatcase, contributions for nonhighlycompensated employees would prob-ably have ranged from 3% to 5% ofpay. Therefore, both highly compen-sated and nonhighly compensated

employees will benefit from the re-peal.

Again, an important caveat tothe above amounts, however, isthat the maximum deductible con-tribution for an employer whosponsors both a DB plan and a DCplan is 25% of the pay of all eli-gible employees, but not less thanthe minimum required contribu-tion to the DB plan. Therefore,for a plan with contribution levelsas shown in the table below, whosesole participant is age 55, themaximum deductible contributionwould be $90,000, the DB planminimum required contribution.Also keep in mind that the DB planmust satisfy Section 401(a)(26).

Older participants are not the onlyones who can benefit from a DB plan.For example, a younger executive,age 35, may have a contribution of$30,000 allocated to the 401(k) profitsharing plan account and have an ad-ditional $20,000 amount accrued ina DB plan for a total of $50,000.

In conclusion, the repeal of Sec-tion 415(e), together with the in-creased use of the general test underSection 401(a)(4), has made it pos-sible for pension professionals to of-fer exciting new plan designs to theirclients. Indeed, all sponsors of quali-fied retirement plans should be en-couraged to review their current plandesigns to see if they can be im-proved. ▲

Marge Paul, MSPA, is a consultingactuary with the law firm of Reish &Luftman, where she specializes inconsulting on plan design, correc-tion of plan defects, overfunded de-fined benefit plans, pension distribu-tions, PBGC plan terminations, andmergers and spinoffs. Ms. Paul hasmore than 25 years of experience inthe design and administration of re-tirement plans. She has also servedon ASPA’s Board of Directors.

Assumed Maximum Annual Maximum AnnualRetirement Contribution Contribution

testing purposes, that the owners, andalmost certainly all the rest of the work-ers, are employees of the recipient, notthe staffing firm.

Of course, it isn’t just the ownersthat are a problem. Most cases in whichthis issue has been reviewed have con-cluded that the staff members are alsocommon law employees of the recipi-ent. (For a complete discussion of thisissue, see Chapter 4 of Who’s the Em-ployer, a Guide to Employee and Ag-gregation Issues Affecting QualifiedPlans, by S. Derrin Watson.)

Dual EmployersSome companies have felt that the

solution to this issue lies in strength-ening the employee relationship be-tween the worker and the staffing firm.They reasoned that if they could showthat the worker is an employee of thestaffing firm, then they show theworker is not the employee of the cli-ent. The 9th Circuit Court of Appealsdashed that argument last year in itsdecision in Vizcaino v. Microsoft.

Microsoft had moved many of its“permatemps” over to staffing firms.The workers claimed they were stillcommon law employees of Microsoft,and hence entitled to coverage. TheCourt held that these workers could beMicrosoft employees, even if theywere also employees of the staffingfirm. Thus, it raised the possibility thatsomeone might have dual employersfor plan purposes. Employee status ofthe workers was to be determined bygeneral common law principles, underwhich Microsoft was clearly an em-ployer, if not the employer. Either way,the workers were entitled to coverageas common law employees.

While we have not seen a court de-cide that a dual employer arrangementactually exists in a staffing firm situa-tion, the court’s holding means that,

as far as a staffing firm’s client is con-cerned, all that matters is the degree ofcontrol that client has over its work-ers. The existence or nonexistence ofan employee relationship with thestaffing firm is irrelevant in determin-ing whether the worker is a commonlaw employee of the recipient.

Direction and ControlCongress compounded this prob-

lem in leased employee cases when itadopted SBJPA of 1996. SBJPAamended IRC §414(n) to provide thata leased employee must operate underthe primary direction and control of therecipient. Therefore, the recipient of aleased employee has to have enoughcontrol to make the worker a leasedemployee, but not enough control tomake them a common law employee.This creates a narrow window indeed.

The committee reports to SBJPArecognize the problem:

“As under present law, the determi-nation of whether someone is aleased employee is made after de-termining whether the individual isa common-law employee of the re-cipient . . . .The fact that a person isor is not found to perform servicesunder primary direction or controlof the recipient for purposes of theemployee leasing rules is not deter-minative of whether the person isor is not a common-law employeeof the recipient.”

The 9th Circuit Court of Appealsagreed with the committee reports inits case of Burrey v. Pacific Gas andElectric. PG&E had argued that whenIRC §414(n) insisted that a leasedemployee not be the recipient’s em-ployee, it must mean something otherthan common law employee, becausemost workers who are under therecipient’s primary direction and

control are its employees. The Courtdisagreed, noting that direction andcontrol is just one (albeit a very im-portant one) of the factors indicatingemployee status. It directed the Dis-trict Court to determine if people pro-viding services to PG&E were theircommon law employees.

Exclusion ClausesPG&E had sought to exclude these

workers from their plans. Their planexcluded all persons found to be leasedemployees under IRC §414(n). TheCourt of Appeals pointed out that thisclause was practically worthless in thissituation. If the workers were the com-mon law employees of PG&E, then bydefinition they are not leased employ-ees under IRC §414(n).

A case in the 11th Circuit dem-onstrated how these workers couldbe excluded. In the case of Wolf v.Coca-Cola, Coke’s plans excludedpeople who were not “regular employ-ees” of the company. Included amongthe “irregular” employees were peopleon the payroll of a staffing firm. Byavoiding the statutory definition ofleased employee, and basing the ex-clusion entirely on who writes the pay-checks, Coke was able to exclude adisgruntled worker from a staffingfirm.

The author suggests using the fol-lowing clause to exclude staffing firmworkers:

“Persons who are on the payrollof another company, and are noton the payroll of the Employer[or an Affiliate of the Employer]are not eligible to participate inthis plan. The purpose of thisprovision is to exclude from par-ticipation in the plan all personswho may be working for the Em-ployer pursuant to a staffing orleasing relationship with anothercompany. They are to be ex-cluded, regardless of whetherthey are common law employ-ees of the Employer, or are

C O N T I N U E D F R O M P A G E 5

Leased Employees, the Plot Thickens

SEPTEMBER-OCTOBER 2000 ▲▲▲▲▲ THE PENSION ACTUARY ▲▲▲▲▲ 15

leased employees of the Em-ployer as defined in Code§414(n).”

The chief advantage to such aclause is that it excludes workerswhether they are common law em-ployees or leased employees. How-ever, it is important to remember that,with very few exceptions, all com-mon law employees and leased em-ployees who meet the age and servicerequirements are counted in deter-mining if the coverage tests of IRC§410(b) and the participation tests ofIRC §401(a)(26) are satisfied. Thus,such an exclusion clause can be usedeffectively only if employees makeup a relatively small portion of acompany’s total non-highly compen-sated workforce.

Safe Harbor; OffsetsOne of the exceptions that allows

a company to disregard its leased em-ployees for retirement plan purposesis if they are covered by a safe har-bor lease. However, this exclusion isonly available to companies wholease no more than 20% of their non-highly compensated workforce.Moreover, it applies only to trueleased employees. It does not affectat all common law employees whomay be covered under a lease.

It is also important to rememberthat since common law employeesare not leased employees; there isnothing in the Internal Revenue Codethat allows the recipient company tooffset benefits provided by the staff-ing firm to its common law employ-ees. Unless the workers are trueleased employees, and not commonlaw employees, the only way the re-cipient can offset staffing firm con-tributions (which ultimately therecipient is paying for) is to cospon-sor the staffing firm’s plan.

Proposed LegislationMuch of the uncertainty regard-

ing leased employees could be re-solved with passage of the

Professional Employer OrganizationWorkers Benefits Act, a bill proposedlast year in the House, and very re-cently introduced in the Senate. Thebill would establish a category ofstaffing firms, Certified ProfessionalEmployer Organizations, whichwould automatically be consideredthe employer of its “work-site em-ployees.”

Although the clarifications of thisbill would be valuable, it has been sub-ject to serious opposition and its im-mediate prospects are not bright. Thisis unfortunate, because the intent be-hind the bill, bringing clarity to agrowing industry and its customers,is worthwhile, and Congress alone hasthe power to bring that clarity.

ConclusionTruly, recent court decisions have

highlighted the need for caution indetermining whether a worker is a

common law employee or a leasedemployee. Certainly, a client’s char-acterization of someone as a leasedemployee cannot be taken at facevalue. Recent decisions also demon-strate the need in many plans for awell-drafted exclusion clause. Ulti-mately, the confusion in this area isa signal for the need of Congressionalaction to clarify the rules affecting agrowing number of employers andworkers. ▲

S. Derrin Watson, APM, is a taxattorney in Santa Barbara specializ-ing in employee, leased employee,and aggregation issues, and is theauthor of a book dealing with thoseissues, Who's the Employer? He isthe managing sysop of the PensionInformation eXchange (PIX). He lec-tures and tells jokes frequently forASPA.

ABC Events

Date Location Event

September 14 Chicago Plan Restatement ProcessSpeaker: Lanning R. Hochhauser, APM, of Datair Systems

September 28 South Florida PEOs; EPCRSSpeakers: Attorneys Roger Rovell and Brett Hamlin

October 4 Atlanta Who is an EmployerWorkshop

Speakers: John R. Hickman and David Godofsky

October 18 North Florida Defined Benefit Plans Speaker: Lorraine Dorsa, MSPA

October 19 Cleveland Fiduciary ResponsibilitiesSpeaker: Mike Olah

November 9 Atlanta Technology Trends forRetirement Plans

Speaker: Richard Carpenter, The Technical Answer Group

November 14 Central Florida Topic: TBAPanelists: TBA

November 29 Western Pennsylvania Government AffairsUpdate

Speaker: Brian H. Graff, Esq., ASPA Executive Director

Wrap-up on the ASPASummer Academy – KevinDonovan Big Winner, Virtuallyby S. Derrin Watson, APM

Participants at ASPA’s SecondSummer Conference last July,were treated to a game show“Who Wants to Be a MillionairePension Guru?” Host DerrinWatson grilled contestants AlexBrucker, APM, George Taylor,MSPA, and Kevin Donovan,MSPA, on all facets of pensionlaw and pension lore.

Kevin Donovan came out ontop, correctly answering the$250,000 question, and missing

only a very difficult $500,000question. Alex Brucker came insecond, winning $32,000 (butmissing the next question).George Taylor also did well,meeting his Waterloo at a $16,000attribution question.

Although there was plenty oflaughter and applause from the au-dience, perhaps the biggest ovationcame when Derrin announced thatASPA dues would not be raised topay the prize money!

Try your hand at the final question and see if you could have helpedKevin: Which of these are not related parties for 414(n)? Fred andMary are husband and wife.

❑ A: Fred’s wholly owned C Corp and an S Corp with Mary as 60%shareholder.

❑ B: Two non-grantor trusts Mary set up, one for her niece and onefor a charity.

❑ C: Fred’s sole proprietorship and a charity controlled by Fred’s family.

❑ D: Two C Corporations with 11 equal, identical shareholders in both.

Lifeline: Check IRC 267 Correct answer on page 23

Attention FSPAs,MSPAs, CPCs,

QPAs, andAPMs!

The deadline for completingand submitting your Continu-ing Educat ion Report ingForm for the 1999-2000 CEcycle is Monday, January 8,2001. Al l ASPA memberswho received a designationafter December 31, 1990 mustsatisfy continuing educationrequirements in order to retaintheir designation(s). TheseCE requirements also apply tothose who received an addi-tional designation or had adesignation reinstated afterDecember 31, 1990. Most des-ignated members must earn 40continuing education credits,however, the number of cred-its required are prorated forthose who earned a designationin the middle of the current CEcycle.

Members subject to CE who donot complete and return a re-porting form, and those who donot meet the CE requirements,will have their designation sus-pended and will not receiverecognition for satisfying therequirements in the 2001 ASPAYearbook.

Please submit your form bymail or fax to the ASPA of-fice at (703) 516-9308 assoon as possible. If you mis-placed your reporting form,you can v is i t the ASPAwebsite (www.aspa.org) todownload the form or [email protected] with your re-quest. Please include your faxnumber.

The Pension Actuary on the Web

Faster and easier!

Go to the Members Onlysection on the ASPA website at

www.aspa.org/memonly/ASPAmemonly.htm

and check out the TPA on the web –indexed by author and article title

for easier referencing.

SEPTEMBER-OCTOBER 2000 ▲▲▲▲▲ THE PENSION ACTUARY ▲▲▲▲▲ 17

CALL FOR PAPERS: SOCIETY OF ACTUARIES

Retirement Implications of

Demographic and Family

Change

ASPA and the Society of Actuaries, in cooperationwith other actuarial, employee benefits, govern-

ment, and research organizations, are sponsoring a call forpapers to encourage and expose new ideas and fresh in-sights on the retirement implications of demographic andfamily change. Retirement and family patterns have changedconsiderably since the U.S. and Canadian Social Securitysystems were instituted, and further change is likely. Asignificant number of individuals are working part-time orintermittently before completely leaving the workforce.Further, the proportion of divorced and single people in thepopulation has increased and the median length of marriagebefore divorce has gone down. Two-earner families havealso become the norm rather than the exception. Whilesome revisions have been made to the social insurancesystems to handle the new patterns, several issues stillremain. Moreover, some of the reform solutions beingdiscussed related to strengthening the solvency of socialinsurance systems may worsen the problems presented bynew retirement and family structures.

These demographic and lifestylechanges are creating a need for re-examination of the structure of so-cial insurance systems andemployer retirement benefit pro-grams. With this call for papers,we hope to encourage a deeper ex-ploration of these issues as theyapply to the U.S. and Canada, aswell as to other countries. We also

want to promote an integratedview, whereby the impact of reformin the social insurance system onemployer pension and other retire-ment benefit systems (and vice-versa) under the stimulus ofchanging demographic and familypatterns can be examined. We hopefor the development and sharing ofideas by our members and other

professionals. Prizes wil l beawarded for the best papers.

The deadline for submitting ab-stracts for proposed papers isNovember 30, 2000. We anticipatethat the papers will be presentedand discussed at a conference in au-tumn 2001. We encourage you toreview the complete call for paperswhich you can download from theSociety of Actuaries’ web site atwww.soa.org/research/ridfc.htmlor order from:

Sandy RosenSociety of Actuaries475 North Martingale RoadSuite 800Schaumburg, IL 60173-2226Attention: Call for PapersPhone: 847-706-3587Fax: 847-706-3599E-mail: [email protected] ▲

Ideas? Comments?

Questions?

Want to write an article?

The Pension Actuary welcomes yourviews! Send to:

The Pension ActuaryASPA, Suite 7504245 North Fairfax DriveArlington, VA 22203(703) 516-9300

ASPA is now offering the Top 5of 1999, an inexpensive way toearn up to 7.5 CE credits with-out leaving your home.

You’ll get:• Five audiotapes

from the 1999Annual Confer-ence

• A binder withcomplete ses-sion outlines

• Five True/Falsequizzes to earn CE. Each quizis worth 1.5 CE credits

Questions? Call ASPA at (703)516-9300, check www.aspa.org,or e-mail [email protected].

American College of Employee Benefits Council

Welcomes Six ASPA Members

The American College of Employee Benefits Council, established bythe American Bar Association, was established to recognize employeebenefits attorneys who have made significant contributions to the ben-efits community.

ASPA members Jeffrey C. Chang, APM; R. Bradford Huss, APM; HarryV. Lamon, Jr., APM; David R. Levin, APM; C. Frederick Reish, APM;and Roger C. Siske, APM, were inducted as “Charter” Fellows of theAmerican College.

The new Charter Fellows met the following criteria:

a) Twenty years’ experience as an employee benefits practitioner follow-ing admission to the practice of law, in the private sector, government,or academics

b) A demonstrated, sustained commitment to the development and pur-suit of public awareness and understanding of the law of employeebenefits through activities such as writing, speaking, participating inpublic policy analysis, public education or public service and repre-sentation projects, and leadership in the employee benefits activitiesof bar associations or other professional organizations

c) Consistent exemplary character and ethical behavior

d) Recognition by their peers for expertise in the field and intellectualexcellence

Congratulations to these ASPA members on their accomplishments!

2000 Eidson Award Recipient

ASPA is pleased to announce thatLeslie S. Shapiro, J.D., has been se-lected as the 2000 Harry T. EidsonAward recipient. Mr. Shapiro is cur-rently President of the Padgett Busi-ness Services Foundation, afoundation dedicated to the en-hancement of small businessthrough education, research, andscholarship.

Mr. Shapiro began his career in1964 as Attorney Advisor for the U.S.Department of Treasury. In 1973, hewas appointed Director of Practiceand also served as Executive Direc-tor of the Joint Board for the Enroll-ment of Actuaries until 1995. Mr.Shapiro subsequently served as Gen-eral Counsel for the National Soci-ety of Accountants until joining thePadgett Foundation in 1998.

In his position as Director of Prac-tice and as Executive Director of theJoint Board for the Enrollment of Ac-tuaries, Mr. Shapiro contributed agreat deal to the education of enrolledactuaries by enforcing standards ofprofessionalism imposed by the regu-lations, which he, among others, wasinstrumental in writing.

Mr. Shapiro worked tirelessly tohelp ASPA gain credibility amongother actuarial organizations in theUnited States. When the Joint BoardAdvisory Committee was created,ASPA was granted equal representa-tion with the Society of Actuaries,thanks in large part to Mr. Shapiro’sinvolvement in the deliberations.

Mr. Shapiro will be presented withthe award at the 2000 ASPA AnnualConference. The 2000 nominees rep-

resented a groupof well-deservingcandidates, andASPA would liketo thank all ofthose who sub-mitted nomina-tions.

The Harry T. Eidson Award rec-ognizes exceptional accomplish-ments that contribute to ASPA, theprivate pension system, or both. Theaward is given in honor of ASPA’slate founder, Harry T. Eidson, FSPA,CPC. Previous winners of the Eidsonaward are as follows: Howard J.Johnson, MSPA, in 1999; Andrew J.Fair, APM, in 1998; Chester J.Salkind in 1997; John N. Erlenbornin 1996; and Edward E. Burrows,MSPA, in 1995.

SEPTEMBER-OCTOBER 2000 ▲▲▲▲▲ THE PENSION ACTUARY ▲▲▲▲▲ 19

wwwwwwwwwwwwwww.aspa.org.aspa.org.aspa.org.aspa.org.aspa.orgCheck out theConferencesWebpageto downloadinformation,brochures, andregistration formsfor upcomingconferences.

E&E Seeks Technical

Education Consultant

ASPA’s Education and Exami-nation Committee is taking appli-cations from pension professionalsinterested in working part time onediting study guides, reviewingexaminations, and providing tech-nical education support. Deadline:October 26, 2000.

If interested, send resume and acover letter expressing how youcan help to Jamie Swank, Dir. ofEd. Svcs, 4245 N. Fairfax Dr., Ste.750, Arlington, VA 22203.

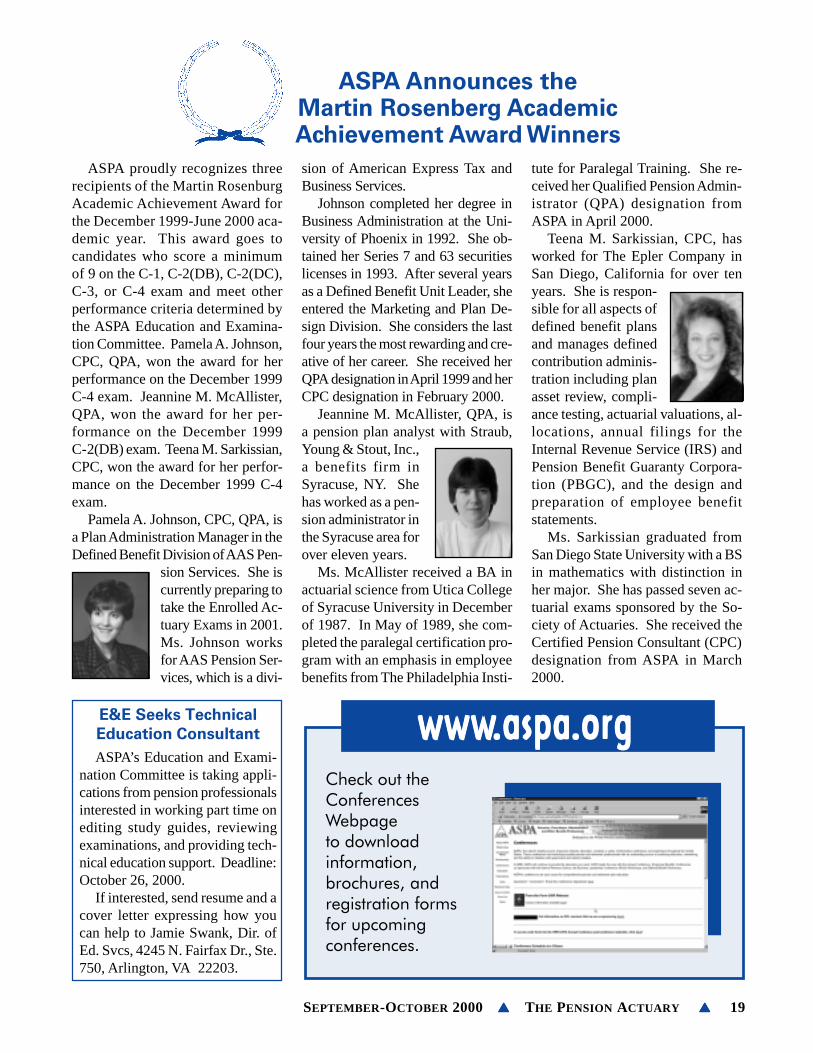

ASPA proudly recognizes threerecipients of the Martin RosenburgAcademic Achievement Award forthe December 1999-June 2000 aca-demic year. This award goes tocandidates who score a minimumof 9 on the C-1, C-2(DB), C-2(DC),C-3, or C-4 exam and meet otherperformance criteria determined bythe ASPA Education and Examina-tion Committee. Pamela A. Johnson,CPC, QPA, won the award for herperformance on the December 1999C-4 exam. Jeannine M. McAllister,QPA, won the award for her per-formance on the December 1999C-2(DB) exam. Teena M. Sarkissian,CPC, won the award for her perfor-mance on the December 1999 C-4exam.

Pamela A. Johnson, CPC, QPA, isa Plan Administration Manager in theDefined Benefit Division of AAS Pen-

sion Services. She iscurrently preparing totake the Enrolled Ac-tuary Exams in 2001.Ms. Johnson worksfor AAS Pension Ser-vices, which is a divi-

sion of American Express Tax andBusiness Services.

Johnson completed her degree inBusiness Administration at the Uni-versity of Phoenix in 1992. She ob-tained her Series 7 and 63 securitieslicenses in 1993. After several yearsas a Defined Benefit Unit Leader, sheentered the Marketing and Plan De-sign Division. She considers the lastfour years the most rewarding and cre-ative of her career. She received herQPA designation in April 1999 and herCPC designation in February 2000.

Jeannine M. McAllister, QPA, isa pension plan analyst with Straub,Young & Stout, Inc.,a benefits firm inSyracuse, NY. Shehas worked as a pen-sion administrator inthe Syracuse area forover eleven years.

Ms. McAllister received a BA inactuarial science from Utica Collegeof Syracuse University in Decemberof 1987. In May of 1989, she com-pleted the paralegal certification pro-gram with an emphasis in employeebenefits from The Philadelphia Insti-

ASPA Announces theMartin Rosenberg AcademicAchievement Award Winners

tute for Paralegal Training. She re-ceived her Qualified Pension Admin-istrator (QPA) designation fromASPA in April 2000.