27

July 2015 Pensions 2015 EXPERT GUIDE

| Date post: | 17-Aug-2015 |

| Category: |

Government & Nonprofit |

| Upload: | dilan-parbat |

| View: | 20 times |

| Download: | 1 times |

July 2015

Pensions 2015

EXPERT GUIDE

2 3July 2015 July 2015

ExpErt guidE: pEnsions 2015

34

42

30

United Kingdom

Automatic Enrolment & the New Regulatory Landscape for Pensions in the UK

UK Pensions Flexibilities & Pensions Liberation

Aligning Workplace Pensions with Business Strategy

SNAPSHOT: UK Pension Trends

Pensions de-risking: A Risky Business? Legal Pitfalls in managing legacy defined benefit risk

Pensions Legislation: The Oncoming Train

Contents

The winding path to wind-up

The Introduction of Auto Enrolment Pensions and its Impact on SMEs

SNAPSHOT: UK Pension Timeline

Belgium

Belgium (finally) almost on the European track for the increase of the legal pension age

Expert Directory

6

8

12

16

20

22

26

30

34

38

40

42

4816

22

8

Contents

Fenice Media Ltd | 101 The Big Peg | 120 Vyse Street | Birmingham | West Midlands | B18 6NF | United Kingdom | Tel: +44 (0) 121 270 9468 | Fax: +44 (0) 121 345 0834 | www.corporatelivewire.com

Contributing OrganisationsGordon Dadds LLP,

Nabarro LLP, Pinsent Masons LLP,

Aries Insight, Simmons & Simmons LLP,

Broadstone Ltd, Central Wealth Management Limited,

ALTIUS

Chief Executive OfficerOsmaan Mahmood

Managing DirectorAndrew Walsh

Editor-in-ChiefJames Drakeford

Publishing DivisionJake Powers, John Hart, John Peterson

Directors Sameena YatesSiobhan Hanley

Awards DirectorsLeah Jones, Elizabeth Moore

Awards CoordinatorRoxana Moroianu

Art DirectorTimothy Nordan

Senior DesignerLai Chun Lok

Luxury Travel Guide EditorLaura Blake

Deputy EditorJosh Hill

ContributorMisbah Alvi

Marketing Development ManagerDilan Parbat

Research MangerDavid Bateson

Production Manager Sunil Kumar

Project ManagersIbrahim Zulfqar, Rocky Singh, Zoe Cannon

Account ManagersNorman Lee, Thomas Patrick, Kerry Payne, Sophie Smith, Jade Hurley, Gemma Palfrey

Competitions ManagerArun Salik

Administration ManagerNafisa Safdar

Data AdministratorDan Kells

Head of FinanceJoseph Richmond,Paul Dey

Senior Credit ControllerJorawar Johl

Accounts Assistants Jenny Hunter,

4 5July 2015 July 2015

ExpErt guidE: pEnsions 2015

Introduction

Times are changing, and so are pen-sions. There is big money to be made with pension schemes, not just by the pension providers but also by fi-nancial advisors and even insurance companies which ‘buy-out’ existing schemes. Changes occur regularly, both in the approach providers take to managing pensions and the re-strictions and regulations imposed by governments on those providers.

In the UK, George Osborne has an-nounced major changes to the way pensions are distributed, and how they are taxed. In a bid to raise more instant cash the chancellor intro-duced more pension freedoms, al-lowing over 55s to take their pensions as lump sums, rather than buying an annuity. Within just two months of the scheme being launched pension-ers had withdrawn nearly £2billion, circulating that previously isolated money in the economy, and, in some cases, paying a hefty sum in taxes too. Proposed future plans could see more changes to pensions in the UK,

with them moving to a system simi-lar to ISAs, where pension contribu-tions, rather than pension withdraw-als, are taxed. This will bring a wind-fall of new taxes into the treasury in the short term, although it is unlikely it will raise more money overall, and could even end up costing taxpayers in the long run.

Meanwhile, several key shifts are taking place among pension pro-viders. A major transition has al-ready occurred from Defined Benefit (DB) to Defined Contribution (DC) schemes in the workplace, but com-panies’ ability to manage these new DC schemes effectively will be vital in the future. One potential problem for businesses could be a refusal to retire, or workers being able to take incredibly favourable pension condi-tions under DC schemes. Employ-ers and employees must also pay increasing attention to the role of Automatic Enrolment in determining how retirement funds operate.

Editor In Chief

James Drakeford

IntroduCtIon

united Kingdom

8 9July 2015 July 2015

ExpErt guidE: pEnsions 2015unIted KIngdom

robert [email protected] +44 (0) 20 7518 0251

Automatic Enrolment & the New Regulatory Landscape for Pensions in the UK By Robert Young

integrate self-invested personal pen-sion arrangements for the directors and family members with the au-tomatic enrolment solution for any staff thus keeping administration to a minimum with everything effectively being provided through one arrange-ment while still maintaining invest-ment flexibility for the directors.

As mentioned above, obtaining a good investment return on funds in-vested in defined contribution pen-sion arrangements is an important element in achieving good retire-ment outcomes. Most members of these schemes simply leave their funds in the default investment fund which is why every qualifying work-place pension arrangement for auto-matic enrolment must have a default fund with charges no more than the current charge cap of 0.75% pa. In-deed this issue is of such importance that the Department of Work and Pensions has published criteria on default fund design.

Until recently many default funds were based around some form of “lifestyle” design whereby funds were gradually moved into less risky

assets over the 10 years or five years to retirement. Most aimed to be 25% in cash and 75% in bonds at the point of retirement as 25% of a fund could be taken in cash and the remainder was used to purchase an annuity. The issue with these funds generally was that the switches were automatic and took no account of in-vestment markets at the time of the switch. Some have added a level of governance to this so that investment experts regularly review the asset al-location of the fund and adjust the allocations should market conditions dictate. However now that there is no longer a need for annuities to be purchased at retirement and increas-ingly retirement is phased rather than at a single date the design of these funds needs to be reviewed.

A newer alternative are the funds known as Target Date funds. As the name implies these target a retire-ment year with risk being taken out as the retirement year approaches. Over time the allocation between re-turn seeking, diversifying and capital preserving assets is adjusted. The funds follow a glide path which goes through several stages.

There is no doubt that this is an in-teresting time for pensions with yet another period of major change.

Firstly we have the challenges of Au-tomatic Enrolment. Although this started back in October 2012, at that stage it was the largest employers and it is now moving into a phase where smaller employers are reach-ing their staging dates until eventu-ally reaching the micro employers. Many of these employers have not established a pension scheme before. In theory this should be straightforward but the Pensions Regula-tor has managed to write 418 pages of guidance so perhaps not so simple after all.

The key to delivering this efficiently and at reasonable cost is in the word “automatic” and linking the payroll systems through to the pension pro-vider systems with little or no manual intervention. This aids accuracy and keeps the need for internal resourc-ing as low as possible. The Pensions Regulator suggests a planning period

of 12 to 18 months but as long as a budget is created for the company contributions then the actual period can be much shorter.

The issue for the pensions industry is capacity as we move forward to peri-ods where in excess of 100,000 em-ployers stage in a single month. The selection of the pension provider is only one part of the process but an important one. There is a lot of focus on charges and we agree that charges

must be reasonable, but net investment return (i.e., return after charges) is also important if good re-tirement outcomes are to be achieved.

We can help employers prepare a suitable plan and guide them through the process and select a suitable pro-vider and generally help ensure ev-erything runs smoothly, as well as giving guidance on issues that may arise. As we work alongside a law firm we can also provide guidance on any employment contract issues that may arise. For owner managed and family businesses we can look to

10 11July 2015 July 2015

ExpErt guidE: pEnsions 2015unIted KIngdom

Robert Young is a Consulting Actuary and heads the firm’s employee ben-efit division. He qualified as an actu-ary over 20 years ago and has spe-cialised in pensions and employee benefits throughout his career. He is also regulated by the FCA to provide financial advice. He strives to pres-ent complex technical and financial issues in terms that Trustees, Spon-soring Employers and Individuals can easily understand, enabling them to consider the issues they face and en-suring they have the knowledge to be able to make informed decisions. He has worked for companies across the spectrum, ranging from large quoted companies to smaller owner and family run businesses providing advice in respect of benefits for staff and to the owners themselves re-garding their own arrangements

At the beginning is the growth phase when the focus is on long term growth with regular contributions smoothing gains and losses this es-sentially being the period up to age 40. Then comes a transition phase from around age 40 to age 55 where a balance is struck between growth and stability. Next comes a consoli-dation phase from age 55 to age 65, the key preretirement period. The focus in this phase switches to short term stability. Finally comes the sta-bility phase or at retirement phase when the focus is on preserving the capital that has been accumulated but with a modest allocation to asset classes that offer a hedge against in-flation and to insure against longev-ity risk.

Throughout this glidepath is man-aged both strategically and tactically to reflect the economic and market

conditions by experienced invest-ment professionals. Funds are now available that deliver all of this at an economical price. They are designed so that if scheme members have no wish to personally engage in the in-vestment process, they are in a fund that is managed in an appropriate way along the journey to retirement with risks appropriately managed.

As noted above until recently funds accumulated in pension arrange-ments were generally used to pur-chase an annuity but in an environ-ment of low yields on gilts these were increasingly considered as poor val-ue and inflexible. From April 2015, however, we moved into the era of Pension Freedoms. From age 55 the whole fund accumulated in the pen-sion fund may be taken out as a cash sum although doing this is inefficient from a tax perspective

12 13July 2015 July 2015

ExpErt guidE: pEnsions 2015unIted KIngdom

Anne-marie [email protected] +44 (0) 20 7524 6143

UK Pensions Flexibilities & Pensions LiberationBy Anne-Marie Winton

members from transferring to lib-eration arrangements – often scams promising access to cash under age 55 or unrealistic investment returns.

The new flexibilities enable schemes with DC benefits to offer members a wider range of options, including unrestricted cash lump sums and flexible drawdown. Trustees, in con-sultation with the employer, should decide what, if any, new benefit op-tions they wish to provide and com-municate this to the members. New statutory transfer rules do make it easier for members to transfer their DC benefits to another arrangement that does offer the flexibilities they want. And included in the new flex-ible benefit regime is a “permissive override” which gives trustees the discretion to pay a flexible DC benefit even where it is not expressly offered under the scheme’s rules. Trustees should therefore at least be open to considering requests from members for an alternative benefit on a case-by-case basis, even where the em-ployer has decided not routinely to offer flexible access to DC benefits under the scheme (for example, be-cause this would add to the adminis-

tration costs of the scheme).

Pensions LiberationA new voluntary code of practice has been issued which sets out “industry standard due diligence” which trust-ees, scheme providers and adminis-trators (collectively referred to in this article as “trustees”) should follow when dealing with pension transfer requests.

The code follows on from a number of pensions liberation Pensions Om-budsman determinations earlier this year, which placed a high standard of due diligence and understanding of scheme documents and legisla-tion on trustees when requested by a member to make a transfer pay-ment. The code highlights, but does not resolve, the difficulty for trustees where they believe that a scam is be-ing committed but the member ap-pears to have a legal right to demand the transfer out of their built up ben-efits.

The code includes steps trustees should take including sample letters, standard information to request and

2015 has brought a new regime for UK pensions provision. In particu-lar the UK Government has radically changed the concept of “pensions saving” – allowing unprecedented (at least for the UK) access for indi-viduals to take their built up funds as lump sums, rather than be forced to buy an annuity. This article examines both the new flexibilities and the po-tentially associated risks of unlawful pensions liberation.

Given the new leg-islation and regula-tory guidance now in place, trustees and employers will have to decide what policies (if any) they wish to adopt in re-lation to money purchase and cash-balance benefits (“DC”). There has, as expected, been an increased de-mand for transfer information from members aged over 55 with defined benefits (“DB”) who are considering transferring to a DC arrangement in order to access their pension savings “flexibly”, for example, as a one off or series of lump sums.

Members must take regulated in-dependent financial advice before transferring a DB benefit into a DC scheme (unless the member’s total DB benefits are valued at £30,000 or less). Pension scheme trustees will need to make specific checks to en-sure the appropriate advice has been given, and ideally, issue a final risk warning to the member (a so-called “second line of defence”) before any transfer out of built up benefits from a DB scheme is made.

A further change is that where a trans-fer request relates to DC benefits only, or where a member is nearing retirement age, then trustees

are required to point the member in the direction of the Government’s Pension Wise service to encourage them to seek guidance on what op-tions they have.

There is also a voluntary industry Code of Practice on combating pen-sion liberation scams. The code sets out detailed due diligence steps trust-ees should take in order to protect

14 15July 2015 July 2015

ExpErt guidE: pEnsions 2015unIted KIngdom

Where there is a material risk, the trustees should check whether the member has a legal right to transfer. If the member does have a right to transfer then trustees will need to decide whether or not to proceed despite any identified pensions lib-eration risk. This may involve taking advice. If the transfer is not to pro-ceed the trustees should write to the member giving reasons why. Where appropriate, the circumstances should be reported to Action Fraud and the Pensions Regulator who has been campaigning with distinctive scorpion branding to raise aware-ness off pensions scams.

If the member supplies sufficient ad-ditional information satisfying the trustees’ concerns then a transfer could take place. Where a decision to transfer takes place, despite con-cerns, then trustees should ensure they have a suitably robust discharge – although this cannot eliminate all

risk of a claim against them. Trustees should keep records of schemes vet-ted and record their decision making in writing.

Anne-Marie has been a pensions lawyer since 1997 and advises em-ployers, group companies, trustees, in-house lawyers, local authorities, contractors and other law firms on commercial and legal pensions is-sues. She is particularly skilled in leading parties through commer-cial pensions negotiations, whether these relate to funding, benefit re-design, incentive exercises, outsourc-ing, corporate restructuring, deal-ing with the Pensions Regulator and PFF or otherwise. She has often on a number of occasions been appoint-ed as an additional legal adviser for trustees facing challenging situa-tions (such as a distressed restructur-ing, proposed pre-pack or corporate sale). She is known for giving clear, pragmatic advice.

how to report suspicious cases. It also includes checklists for recording the process and decisions made.

In addition, the code sets out three main principles:

1. Trustees should raise awareness of pension scams amongst members and beneficiaries in their scheme.2. Trustees should have robust, but proportionate, processes for as-sessing whether a receiving scheme may be operating as part of a pen-sion scam, and for responding to that risk.3. Trustees should generally be aware of the known current strate-gies of perpetrators of pension scams in order to inform their due diligence. They should refer to the Pension Reg-ulator’s warning flags, FCA alerts and Action Fraud guidance.

So trustees should conduct proper due diligence when dealing with a

transfer request and carefully con-sider whether the transfer can and should proceed.

How to spot a scam - some key risk indicators for trustees and members

• Newly established scheme with little or no formal documentation

• First contact with member made through cold calling or unsolicited text or email

• Pressure to force through the transfer quickly

• Promise of high or guaranteed rate of return

• Encouragement to take cash and reinvest it

• Offer of commission or a bonus payment in order to make the transfer

• Claims to allow access to pension before age 55

• Transfers of money into an over-seas investment

16 17July 2015 July 2015

ExpErt guidE: pEnsions 2015unIted KIngdom

tom [email protected] +44 (0) 113 225 5451

Aligning Workplace Pensions with Business StrategyBy Tom Barton

a blanket solution. For the workforce generally, if DC schemes don’t pro-vide the kind of retirement a worker had in mind, then employers can ex-pect claims to come rolling in.

Employers also need to move with the times and recognise that DC schemes are, in effect, savings and investment arrangements for their workers. This places a great deal of responsibility on the shoulders of employers. With that responsibil-ity comes potential liability if things don’t go entirely to plan. We can ex-pect a great deal of scrutiny of em-ployers’ roles in scheme selection, contribution structures, investment choices and default investment strat-egy. The law around just where em-ployers’ liability starts and stops in this respect is currently uncertain.

The starting point for a claim will be the pensions booklet and associated communications. Unfortunate draft-ing can lead to inadvertent financial advice relating to investment deci-sions, negligent mis-statement or misrepresentation or even the cre-

ation of a pensions promise in what was intended to be a true DC scheme. Recent changes to the taxation of and access to DC pension savings gives a good excuse to start afresh with a new fit for purpose set of member facing literature. This is an opportu-nity to get things right and eliminate one key area of risk for the business.

It is fair to say that in many cases em-ployers will rely heavily on third par-ties to keep them on the straight and narrow. However, standard form third party contracts will tend to allo-cate risk back to employers if things go wrong. In some contracts it is not even possible to identify with any certainty what service the supplier is actually supposed to be providing. The position becomes even murkier when trying to identify just how and in what circumstances any liability could ever be pinned on the supplier, even in the event of a serious breach.

The best way to get third party con-tracts in good shape is through a rig-orous procurement exercise. Legal risk is always most successfully ad-

There are now more members of de-fined contribution (“DC”) schemes in the UK than there are members of the traditional defined benefit (“DB”) schemes. The reason for the trend is simple: in DC schemes there is no dreaded deficit. Those deficits arose because, at least in part, em-ployers never fully got to grips with the reality of how DB schemes actu-ally worked before it was far too late.

While DC remains, in many cases, in its relative infancy, now is the time to learn a valuable lesson from the demise of DB schemes. This means getting to grips with the risks associated with workplace DC schemes. Activity of this nature often comes under the broad banner of “governance”. This is, in effect, the solution – but it’s important to make sure that this solution is aligned to business strategy too. From a risk point of view governance done badly is probably even worse than no gov-ernance at all.

Risk

It has been somewhat taken for granted that DC schemes are all very low risk on the basis that there is no employer “promise” to pay a speci-fied level of benefits when workers retire. This approach to DC is a rec-ipe for disaster. Before too long, DC schemes will be the sole or primary source of later life income for most of the UK workforce.

Where this is already the case a worry-ing phenomenon is emerging. Since the abolition of the de-fault retirement age, employers can no

longer retire older workers out of the workforce. Where workers remain in place beyond their usefulness to the business, employers face a reduction in overall productivity and a barrier to the career progression of rising stars. There are already examples of employers entering into compromise agreements with older workers to get them off the books. This is hardly

18 19July 2015 July 2015

ExpErt guidE: pEnsions 2015unIted KIngdom

risk by helping to deliver good sav-ings outcomes for their workforce. It can also be self-financing. Success-ful supplier management can not only reduce legal risk, it can also help bring down costs.

Ultimately though, it’s important to recognise that good employer gov-ernance alone cannot guarantee a good worker outcome at retirement. However good the governance, there is a risk that DC savings will not meet member expectations (whether rea-sonable or not). In such instances the effort is far from wasted. Good governance still serves a useful pur-pose, because it will help to demon-strate discharge of legal duties in the event of a claim.

Tom Barton is a Partner in the na-tional pensions practice and leads the workplace DC pension practice for Pinsent Masons. He advises many of the UK’s largest pension pro-viders, trustee boards and employ-ers on such things as member-borne charges and taxation of DC schemes. Tom is an expert in DC governance and recently presented his chapter on governance at the press launch of Lord Hutton’s and Redington’s paper entitled “Age of Responsibility”. He is a member of the ILAG committee for Workplace Benefits and a found-er member of the PMI committee re-sponsible for the industry examina-tion in auto-enrolment.

dressed at this stage, when compet-ing suppliers are making concessions to win the business. The position to take is this: if you outsource the job, then outsource the risk that goes with it.

Governance – and of the right sort

Many employers have formed gov-ernance to oversee the DC scheme. These committees can help to pro-mote the idea of saving for retire-ment and look after workers who are not always able or sufficiently en-gaged to do this for themselves.

There are a number of well-inten-tioned employers actually increasing their legal risk through overzealous

governance. The greatest risk faced by employers is where they they take responsibility for matters which should be undertaken by another party (e.g., provider or member) and then fall short of the high standards they set themselves in their own terms of reference. Investments in particular are a key risk area.

Good employer led governance should be all about aligning the work-place pension scheme(s) with wider business objectives. Assembling the right committee and resourcing it ef-fectively can help to address all of the risks outlined earlier. Through effective member engagement and successful use of third party solu-tions, employers can guard against

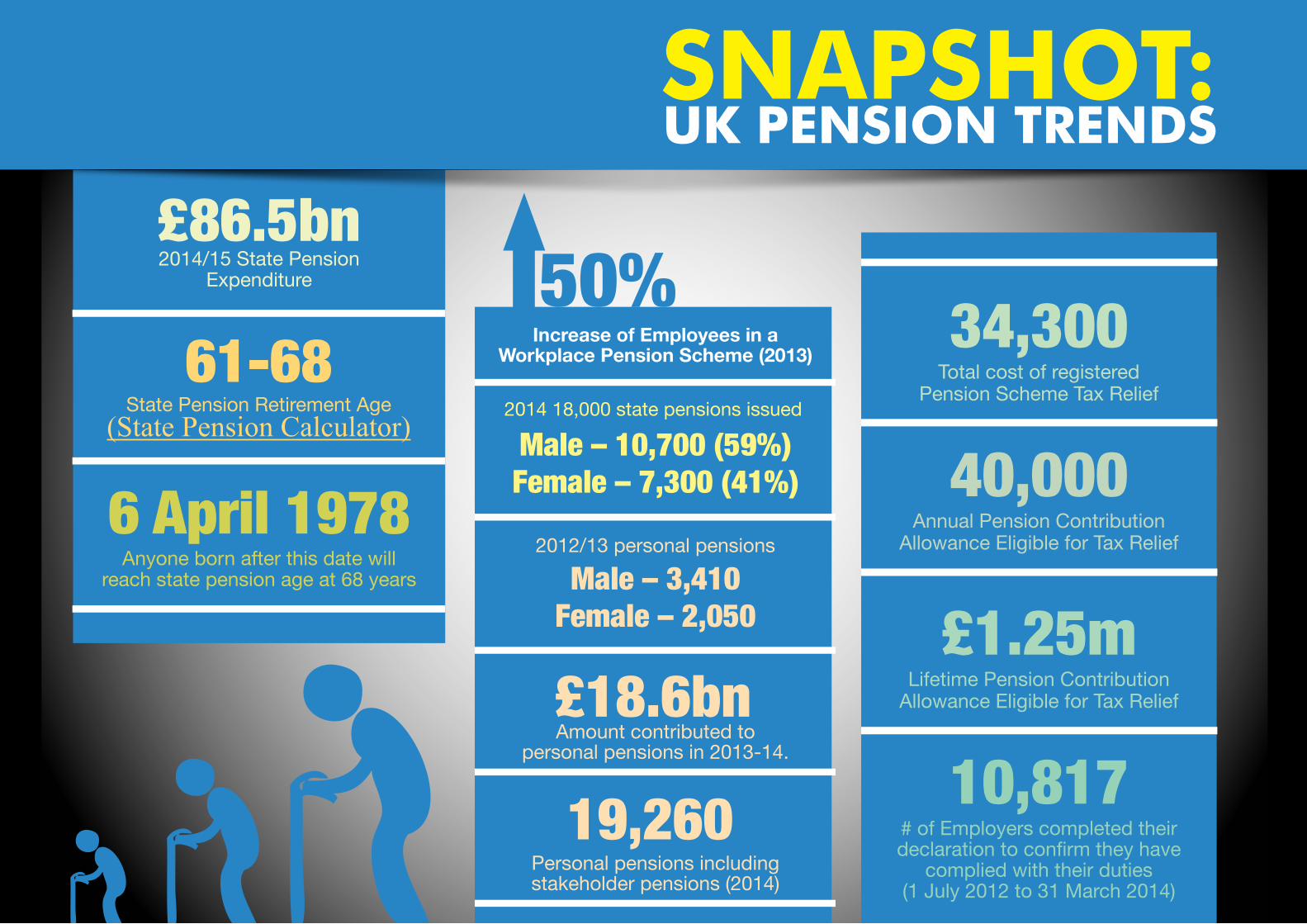

SNAPSHOT: UK PeNSiON TreNdS

Increase of Employees in a Workplace Pension Scheme (2013)

2014 18,000 state pensions issued

2012/13 personal pensions

50%

Male – 10,700 (59%)

Male – 3,410

Female – 7,300 (41%)

Female – 2,050

2014/15 state Pension expenditure

state Pension retirement Age

Anyone born after this date will reach state pension age at 68 years

£86.5bn

61-68

6 April 1978

(State Pension Calculator)

Amount contributed to personal pensions in 2013-14.

£18.6bn

Personal pensions including stakeholder pensions (2014)

19,260

total cost of registered Pension scheme tax relief

Lifetime Pension Contribution Allowance eligible for tax relief

Annual Pension Contribution Allowance eligible for tax relief

# of employers completed their declaration to confirm they have

complied with their duties (1 July 2012 to 31 march 2014)

34,300

£1.25m

40,000

10,817

22 23July 2015 July 2015

ExpErt guidE: pEnsions 2015unIted KIngdom

danny tsang edward [email protected] + 44 (0) 207 825 4153

[email protected] +44 (0) 207 825 4261

Pensions de-risking: A Risky Business?Legal Pitfalls in managing legacy defined benefit risk By Danny Tsang & Edward Smith

• Managing down past service liabilities: moving DB pension liabili-ties off the corporate balance sheet including through enhanced transfer out exercises, pension increase ex-changes and insurance buy-out solu-tions.• Liability driven investment: re-

mapping a pension scheme’s invest-ments to more closely match its li-abilities, including hedging interest rate, inflation and longevity risks, and insurance buy-in solutions (which may be combined with captive insur-ance where an insurance buy-in with a third party insurer is re-insured with an insurance company within the corporate’s group).• Pension scheme funding solu-

tions: parent company guarantees, linking deficit repair contributions to corporate performance, asset backed contribution structures, letters of credit and escrow arrangements.

The Legal Challenges & Potential So-lutions

One of the key tests any proposed de-risking solution needs to meet is whether it effectively manages legal (as well as financial) risk. Not only

does the solution need to be deliv-ered at the right price and at the right time, but it needs to be legally effective. A “solution” which seeks to reduce risk or volatility is not a real solution if there is a high degree of legal risk that it will be unpicked further down the line.

Effective de-risking is rarely “one size fits all”, so the legal risks involved will be different from case to case. But examples of the common legal chal-lenges that de-risking poses, and their potential solutions, include:

• Incentive exercises (e.g. pen-sion increase exchanges and en-hanced transfer values): these exer-cises will only be effective if they do actually move legacy liabilities out of the pension scheme, and therefore off the corporate balance sheet. The key legal risk is future “mis-selling” claims. This risk can be mitigated by ensuring that member communica-tions are clear and comply with re-cent regulatory guidance and case law.• Curtailing, or amending the

basis of, future DB pension accrual: pension scheme closures and amend-

The drivers towards de-risking

Many defined benefit (DB) pension schemes in the UK are already closed to new members or to future accrual. Traditionally, companies have used these methods to try to control and reduce their DB pension liabilities.

However, corporates with DB pen-sion schemes continue to face a number of challenges, including:• The uncertain-

ties of funding DB pension schemes as a result of rapidly in-creasing longevity, volatile markets and a complex legislative framework.• The obligation

to make provision for DB pension li-abilities in company balance sheets.• Prolonged funding negotiations

with trustees.• The impact of DB pension liabil-

ities on corporate activity, whether in the context of mergers and acqui-sitions, exits from joint venture ar-rangements, payments of dividends within a corporate group or other-wise.

As a result, corporate sponsors and also trustees are increasingly look-ing at new ways in which pension scheme risk can be better (and in some cases more finally) managed. Such “de-risking” covers a number of options which can be used to reduce the risk and liability attached to DB pension schemes (and in some cases extinguish all future liability) whilst at the same time ensuring security for members and their pension ben-

efits. The Options De-risking solutions include:• Mitigating on-

going defined benefit accrual risk: includ-

ing closing DB pension schemes to future accrual or amending the basis of future pensionable service accrual (e.g. altering the DB pension accrual formula for future service, altering the composition of pensionable pay, removing fringe benefits such as en-hancements on redundancy or ill-health, increasing normal retirement age and making the rate of increase of pensions in payment less generous).

24 25July 2015 July 2015

ExpErt guidE: pEnsions 2015unIted KIngdom

Danny Tsang specialises in pensions law and has over 20 years’ experi-ence in advising on all aspects of pensions and benefits matters. His practice focuses on advising clients in relation to pension strategy and includes the restructuring of pen-sion schemes such as scheme merg-ers and changes to benefit structures and de-risking solutions.

Edward Smith specialises in pensions law and his experience includes ad-vising FTSE 100 companies on pen-sion benefit redesigns (from modify-ing ongoing defined benefit accrual through to scheme closures), fund-ing negotiations with pension trust-ees, reduction of past service liabili-ties (including transfer out exercises) and the legal aspects of pension fund investment (including buy-ins, buy-outs and liability hedging).

ments clearly need to be legally wa-tertight – and mitigate the risks of member (or union) claims that the changes are invalid. Members might claim that they are entitled to enjoy their current level of pension pro-vision, and successful claims could “unpick” the amendments. It is therefore important to identify what the risks of challenge are and seek to mitigate them: e.g. establish what employees’ contractual rights to pensions are; and consider whether past statements by employers have engendered members’ “reasonable expectations” of continued accrual (which, if breached without a strong business justification, could give rise to claims).• Insurance buy-outs: the “right”

benefits need to be bought out to en-sure there is an effective transfer of risk out of the pension scheme, and therefore off the corporate balance sheet. It is often the case, particu-larly where a corporate has been ac-quisitive in the past, that there will be

a number of different benefit catego-ries in the same DB pension scheme – with different member categories entitled to different “shape” benefits (e.g. different accrual rates, rates of revaluation in deferment and pen-sion increases). An effective buy-out needs to ensure that all these legacy benefit differences are identified and bought out.• Pension scheme investments: it

is a truism that more complex invest-ment solutions (e.g. interest rate, inflation and longevity hedges) of-ten require more complex legal doc-umentation – and a key risk is that the detailed legal terms (e.g. re col-lateralisation, re measuring the rel-evant risk that is being hedged) do not marry up with the product that has been “sold”. It is therefore im-portant to ensure that there is clar-ity in the legal documentation of the key commercial terms and that they work “on the ground”.

26 27July 2015 July 2015

ExpErt guidE: pEnsions 2015unIted KIngdom

Ian [email protected] +44 (0) 153 676 3352

Pensions Legislation: The Oncoming TrainBy Ian Neale

As with everything else in the UK, ‘terms and conditions apply’. For a start, flexible access is essentially limited to money purchase (DC = De-fined Contribution) pension arrange-ments, and members normally have to be at least 55. There are different possibilities – flexible drawdown and the ‘uncrystallised pension funds lump sum’ (UFPLS), to name two - but the law does not oblige any DC scheme or provider to offer the full range. Drawdown in particular is expensive to administer; it’s hard to see many scheme sponsors taking on the additional cost burden. Oh, and whichever way you go there are tax implications for the member too, which can be hard to communicate.

Some new rules about transferring from a defined benefit (DB) arrange-ment have combined with flexible access to DC benefits to stimulate member interest in transfers, while creating hoops and hurdles to frus-trate them – for good reason, many would acknowledge. Flexible access has also boosted the nefarious activi-ties of pension liberation scammers – a major and ever-growing threat to combat which all pension providers

need to divert time and money.

The latest distraction on the horizon is a Government proposal to allow annuity holders to assign their future income to a third party, in exchange for a lump sum. For a host of prac-tical reasons this is unlikely to work, but at a time when new legislation to limit charges and improve scheme governance is just being introduced, the last thing providers need is an-other costly diversion of resources.

Back to auto-enrolment: if as an em-ployer you thought you’d ‘been there, done that’, think again: you have to do it all over again every three years. The largest employers face their first cyclical automatic re-enrolment ex-ercise this autumn. Most employ-ers have not even reached the start-ing line yet, though. While every employer whose PAYE Scheme on 1 April 2012 had at least 50 employees has passed their staging date, they amount to just 3% of the total num-ber of employers.

The avalanche of small and micro employers, most of whom have nev-er offered a pension to employees

It just never ends, does it? Gone are the days when ‘all’ an employer had to worry about was managing the defined benefit pension scheme deficit. Since the advent of auto-matic enrolment in 2012, pension provision for workers has come onto everyone’s radar. This article looks ahead from within the turbulence created by non-stop tinkering with pensions legislation to warn of what else is coming.

The limits to pensions tax relief have repeat-edly been altered, with the lifetime al-lowance slashed from £1.8m to £1.5m in 2012, reduced again to £1.25m in 2014, and about to be cut down to £1m next year. Higher earners have been offered Fixed Protection 2012, Fixed Protection 2014, and Individual Pro-tection 2014. The annual allowance has also been dramatically reduced, from £255,000 to just £50,000 in 2011, and again in 2014 to £40,000. Simplification it isn’t.

Hardly an environment to encourage

investment in pensions, you might feel. Who knows what will happen next? (This article is being written in late June, while we nervously await the Budget on 8 July.) The Govern-ment is being urged from all sides to agree to set up an independent re-tirement savings commission, to de-velop the kind of long-term strategy consensus which politicians alone cannot. What we need above all are stable and predictable rules govern-ing pension saving.

This year everyone is trying to accom-modate the pension flexibility rules in last December’s Taxa-tion of Pensions Act, supplemented by the

Finance Act 2015. For once the en-tire pensions industry seems united in pleading for a pause: no more changes while we get to grips with the last lot. While last year’s Budget bombshell has certainly stimulated new interest in pensions, especially in new ways to get money out and pass it on to later generations, it has also created a problem in managing expectations.

28 29July 2015 July 2015

ExpErt guidE: pEnsions 2015unIted KIngdom

sions. As if the inexorable growth in funding deficits was not enough, next year the sun sets on contract-ing-out. The challenges that brings include how to cope with the loss of the rebate, and the tar pit that is GMP (guaranteed minimum pension) reconciliation. There are differences in all schemes between the GMP li-abilities a scheme thinks it has and what HMRC records show; you might guess whose view is likely to prevail. More cost!

So much to cope with; it’s hardly sur-prising that the watchword among employers these days when it comes to pensions is often simply ‘compli-ance’. Many will not go beyond the absolute minimum (and even feel threatened by that). Who can blame them? Since the abolition of the de-fault retirement age in 2011, and the demise of well-funded final salary pensions which used to offer a way of facilitating affordable early retire-ment, employment costs have only been going in one direction.

Is there any good news to draw from this maelstrom? Perhaps. With pen-sions undeniably in the spotlight, people are becoming more aware of the need to take control of fund-ing for their later life. In the recruit-ment field, a remuneration package that offers more than the minimum might be an attractive differentiator.

Ian Neale is a Director and co-found-er with Gary Chamberlin of the pen-sions legislation specialists Aries In-sight. He has over 25 years’ experi-ence of serving the pensions industry in a mission to help administrators and others make sense of the legisla-tion. The Aries Pensions System ex-plains all the requirements, not only of UK pensions law but covering a range of overseas regimes as well. A frequent communicator, often quot-ed in the pensions press, his passion is to save people time. Ian is a sci-ence graduate of Monash University (Melbourne) and Loughborough Uni-versity.

and know little about the issues in-volved, is a huge and imminent chal-lenge. The payroll and pensions in-dustries are working hard to cope with the projected ‘capacity crunch’ next spring, but will there be enough help for employers who want to take advantage of legislative changes since 2012?

And there’s more: much more loom-ing. The coalition government put something called ‘pot follows mem-ber’ on the statute book, in the 2014 Pensions Act. If and when actually brought into force, this will mandate automatic transfer of small pension pots when a ‘qualifying member’ (more ‘complification’) leaves a DC pension after being auto-enrolled. Steve Webb was all set to start this in autumn 2016. We shall see whether the new government persists in load-ing this extra administration burden onto providers.

For sponsors of occupational DC schemes, another blow this year comes with the abolition of short

service refunds from 1 October, ex-cept where the member leaves with-in 30 days of joining the scheme. This will remove a convenient fund-ing cushion, presently available from retained employer contributions when a member leaves in the first two years.

It’s early days with the new govern-ment, of course. But for employers the signs are not good. Before the General Election the Conservative Party manifesto promised to taper the annual allowance from £40,000 down to just £10,000 for higher earners with ‘annual income’ (to be defined!) between £150,000 and £210,000. It would not raise a huge amount of extra tax, but the sheer complexity of implementation looks formidable. Ironically the last La-bour government proposed some-thing similar; swiftly scrapped by the incoming coalition.

Meanwhile many employers are still burdened by the long goodbye to de-fined benefit (aka final salary) pen-

30 31July 2015 July 2015

ExpErt guidE: pEnsions 2015unIted KIngdom

John Broome [email protected] +44 (0) 207 893 3441

The winding path to wind-upBy John Broome Saunders

when lingering doubt exists over what those benefits actually are.

Secondly, there is the question of data. Thanks to the efforts of the Pensions Regulator, pension schemes are beginning to take data qual-ity more seriously. However, most schemes will still have gaps, either where benefit-critical data is held in paper files archived in the murky depths of some former salt mine, or where information on benefits has simply been lost. Insurers may agree to take on liabilities where there is a degree of uncertainty over the prom-ised benefits, but they will build a lot of fat into their quoted premium to take that uncertainty into account. Getting to grips with scheme data is the sort of geeky work that many more strategic trustees will shy away from, but it is of critical importance; moreover, trustees should not be afraid of giving their administrators a bloody nose if necessary, since keep-ing accurate and complete records is probably their most important basic function.

Trustees should not ignore other governance issues. These can often

derail a carefully planned buy-out process. Do they have a complete set of validly executed deeds? Can they confirm that historic participat-ing employers have all been properly discharged from their obligations? Do they have a sensible and consis-tent policy in relation to members who don’t claim benefits? These sorts of issues may not naturally find their way to the top of the trustees’ agenda, but they are an important part of the overall management of the scheme.

Whilst trustees are scrubbing up the scheme, sponsors might want to give some thought to liability man-agement. If the buy-out timetable is measured in years rather than months, the sponsor may have time to implement a selection of the usual slew of strategies with a view to re-ducing the final buy-out cost. How-ever, a word of caution - introducing or enhancing scheme options does materially increase the likelihood of selection. Insurers are now wising up to this, and are starting to adjust premiums if they know that schemes have been heavily “pruned”. An en-hanced transfer value exercise may

Life’s certainties may be death and taxes, but for defined benefit pen-sion schemes a new certainty is emerging – that responsibility for paying pensions will ultimately be passed to an insurance company. No scheme will continue to exist in its present form until its very last ageing member passes away. Invariably, ev-ery scheme will get to a point where the only sensible step is to chuck on-going responsibility for paying pen-sions to an insurer (a process usually known as “buy-out”), and for the trustees responsible for run-ning the scheme to bow out. The key un-certainty is when this might happen.

Unfortunately, buy-out comes at a considerable cost. Insurance compa-nies won’t take on the risk of paying long-term pension obligations, un-less they obtain a chunky premium for the pleasure of doing so. Whilst the current cost of buy-out may be deeply off-putting, the financial dy-namics of schemes will change over time - all other things being equal, the cost should gradually fall of its

own accord. So trustees and scheme sponsors need to start thinking now about the steps they need to prepare for buy-out, even if the sponsor’s fi-nance director still has his cheque-book securely locked away in his bot-tom draw.

One key component of buy-out prep-aration is sorting out the housekeep-ing; for example, all those lingering issues about benefits that haven’t quite been resolved - the sort of

things that appear regularly on trustee meeting agendas, usually to be deferred until subsequent meetings, pending some further analy-sis or development.

As well as the hoary old chestnut of GMP equalisation, this could include classic issues such as sex equalisa-tion timing, or lingering question-marks over exactly what benefits were promised to certain employees thanks to some ill-conceived hurried pension letter sent by the HR direc-tor in the middle of a transaction. It is difficult to get an insurer to take on responsibility for paying benefits

32 33July 2015 July 2015

ExpErt guidE: pEnsions 2015unIted KIngdom

and investment modelling.

In particular, John helps clients un-derstand and manage the legacy risks associated with defined benefit pension provision. He has developed a number of innovative approaches that can both increase trustee secu-rity and reduce sponsor risks.

A mathematics graduate from the University of Durham, John spent the early part of his actuarial career with international consulting firm Tow-ers Perrin, and has been at BROAD-STONE for over 10 years.

EXAMPLES OF RECENT WORK• Ongoing advice to sponsor of £30m DB pension scheme on closure to accrual, funding, introduction of additional benefit options and invest-ment benchmarking• Strategic investment and gover-nance advice for trustees of a £140m pension scheme

• Ongoing advice to sponsor of £160m multi-employer DB pension scheme on covenant, funding as-sumptions and recovery plan struc-ture• Ongoing appointment as invest-ment advisor to trustees of £80m DB scheme sponsored by multi-national industrial products distribution firm• Advice to building services com-pany on participation in the Local Government Pension Scheme, and leadership of negotiations with con-tracting authority on pension risk sharing• Pensions due diligence support-ing the trade purchase of a UK man-ufacturing firm• Pension scheme risk and cost management advice to sponsor of £5m legacy DB scheme• Advice to not-for-profit mem-bership organisation on how to ap-proach funding discussions with pen-sion scheme trustees

provide some cost reductions on paper, but if the result is that all the sickly singletons leave the scheme, the profile of the remaining mem-bership may turn out to be rather more expensive to insure.

Investment strategy needs to be given consideration - as buy-out be-comes closer upon the horizon, many sponsors will want to move into as-sets that move more closely in line with buy-out premiums. Typically that means bonds. Of course, there is an alternative view - namely that riskier strategies can be maintained, as long as the overall financial posi-tion can be monitored carefully and frequently. The idea here is that the higher expected returns (from a greater proportion of equities, for example) help to reduce the ultimate cost of buy-out. Some sponsors may take the view that a roller-coaster ride is OK, if they think they are in a position to hit the big red transact

button when the price is right.

Many sponsors and trustees may still think they are generations away from buy-out, especially if they are finding that even agreeing a recovery plan to ensure that a funding deficit is elimi-nated is proving a struggle. However, trustees must take the long view, and prepare for the next challenge, even if it a challenge that ultimately puts them out of a job.

John Broome Saunders is a quali-fied consulting actuary and FCA au-thorised investment adviser, with 17 years’ experience of providing analytically-focussed advice on the management of complex long-term financial structures such as defined benefit pension schemes.

John provides advice on funding, in-vestment, accounting and manage-ment issues, drawing on BROAD-STONE’s wider expertise in financial

34 35July 2015 July 2015

ExpErt guidE: pEnsions 2015unIted KIngdom

Ian [email protected]+44 (0) 845 006 6204

The Introduction of Auto Enrolment Pensions and its Impact on SMEsBy Ian Smith MSc, APMI, FPFS, IMC, FIFP, CFP

For someone who just wants a bet-ter fund choice than a traditional insurance company pension, for ex-ample a wide range of Unit Trusts and funds from well-known fund managers or to buy your own choice of shares, investment trusts etc., via an execution, only stockbrokers have various low cost self-invested plans. For some people however they want access to the widest possible range of investments so full self-invested plans are the most appropriate – they cost more but allow proper self-invested choice.

There are two types of such plans each with slightly different rules when it comes to investments.

The original version of a company sponsored self-invested pension was the small self-administered scheme or SSAS, set up under trust the com-pany acts as the original sponsor, although once it has appeared on the initial documents, the company need not have further involvement if they do not want to. Such schemes can be for individuals or a number of individuals, typically the direc-tors of the company, or possibly the

directors, and their families. Exist-ing pensions can be transferred into the scheme. In terms of investment all of the usual suspects, like shares, unit trusts, cash, etc., are allowed, but most business owners are more interested in the self-invested op-tions that can be used more to di-rectly benefit their own business. Al-though it is no longer a requirement most SSAS arrangements will have an independent trustee or practitio-ner working with the scheme to en-sure it meets all the HM Revenue & Customs (HMRC) rules and submits the required documents and returns.

The SSAS scheme can make a loan back to the company of up to 50% of scheme assets, although this loan now has to be secured by first charge on security provided by the company or its directors. The loan can be for any purpose and needs to be repaid within five years. Given the current lack of bank funding for small busi-nesses the chances of being able to be their own lender via their pension is proving very popular. The require-ment to provide security for the loan may be an issue but there is no re-striction on what the company or its

For many owners of SMEs, the intro-duction of auto enrolment pensions may be viewed as more unwelcomed red tape or an opportunity for them to attract and retain staff, but it could also be viewed as a reminder that pensions can still be useful as a tax planning tool for the business own-ers themselves.

Contributions made by a company for directors working in a business will usually be fully allowed as a cor-poration tax deduc-tion and will attract no benefit in kind tax or national insur-ance. Although there is now a lifetime limit of £1m and the limit on how much can be contributed to a pension scheme in a year has been reduced to £40,000. These are still reasonably high fig-ures for many SMEs and the option to carry forward up to three years previous unused contributions can mean a £180,000 per director con-tribution can be made. With corpo-ration tax scheduled to be reduced each tax year putting in a contribu-tion now will give you a greater tax

break than if you wait. It is even pos-sible to use a pension contribution to create a trading loss and reclaim corporation tax.

Standard off the peg pension prod-ucts may be much better than they were historically, but still many direc-tors find it hard to get enthusiastic about such insurance based arrange-ments. Hence the popularity of self-invested pensions which allows a much greater level of investment

freedom. As well as a better choice and spread of invest-ments than a normal personal pension, the self-invested market opens our options like loans and prop-

erty purchase that can help integrate pension, tax, and business planning. With a self-invested plan there is generally a flat charge for the tax ef-ficient wrapper and administration and then the investments are cho-sen by the member and/or their ad-visers. For larger funds these plans can be cost effective and are ideal for those who want more involvement in the investment choice.

36 37July 2015 July 2015

ExpErt guidE: pEnsions 2015unIted KIngdom

their premises back off the company.

There is now no longer any require-ment to purchase an annuity at any age so a director can draw retirement income directly from the fund so in-vestments such as property or third party loans can make ideal invest-ments as the rentals/repayments can be used to fund regular income pay-ments. There are no limits on how much income can be drawn.

Care needs to be taken when choos-ing a self-invested scheme provider. Cost should not be the only consid-eration, as some cheaper plans only allow a more limited investment choice or may take a commission on investments purchased. Even some providers that seem to offer a wide investment choice include that self-investment will not allow certain transactions or may require the use of specific providers, legal advisers, surveyors etc. So for anyone looking

to set up a self-invested plan know-ing what type of investment they in-tend is important, so that the most appropriate arrangement can be se-lected. IAN SMITh MSC, APMI, FPFS, IMC, FIFP, CFP

Ian Smith accidentally ended up in pensions industry over 20 years ago and has been an Independent Finan-cial Adviser for most of this time. In 2002, he started his own IFA prac-tice. Ian and the firm have won many national awards; with the latest be-ing Central Wealth Planning Limited being named as one of the five best firms in the UK by Retirement Plan-ner magazine. He is both a Char-tered and Certified Financial Planner and has a Master’s Degree in Finan-cial Planning and is working on a PhD on investment portfolios.

directors put up as security. As long as it can be valued appropriately and can have a legal first charge placed on it then it may be used.

The personal pension version of the self-invested plan, the self-invested personal pension (SIPP) cannot make such a loan to any business that is linked to the scheme member. Both the SIPP and SSAS however can make third party loans to other businesses. We have seen with our own clients a number of such investments being made from a business angle or where the pension member, has worked with the other company in the past and is happy to provide funds for a specific project like property devel-opment, for example. There is no re-quirement to lend on a secured basis, for a higher interest rate the scheme could advance an unsecured loan.

Property purchase has always been very attractive via pension fund, due

to rental income, rolls up tax-free and there is no capital gains tax on the eventual disposal of the prop-erty. Only commercial properties are acceptable for example offices, factories, warehouses, shops and hotels. The pension scheme is al-lowed to borrow money to help with the purchase although the limit is quite restrictive at 50% of scheme assets. It is, however, possible for the pension scheme to make part purchases of property so either mul-tiple schemes can buy one property or a business and its directors can buy a property alongside their own pension arrangements. As long as a proper third party valuation is ob-tained, pension plans can purchase property from the business or its owners. We have seen this being used as an excellent source of pro-viding liquidity back to the company from the pension arrangements. For example, when the companies direc-tors use their pension funds to buy

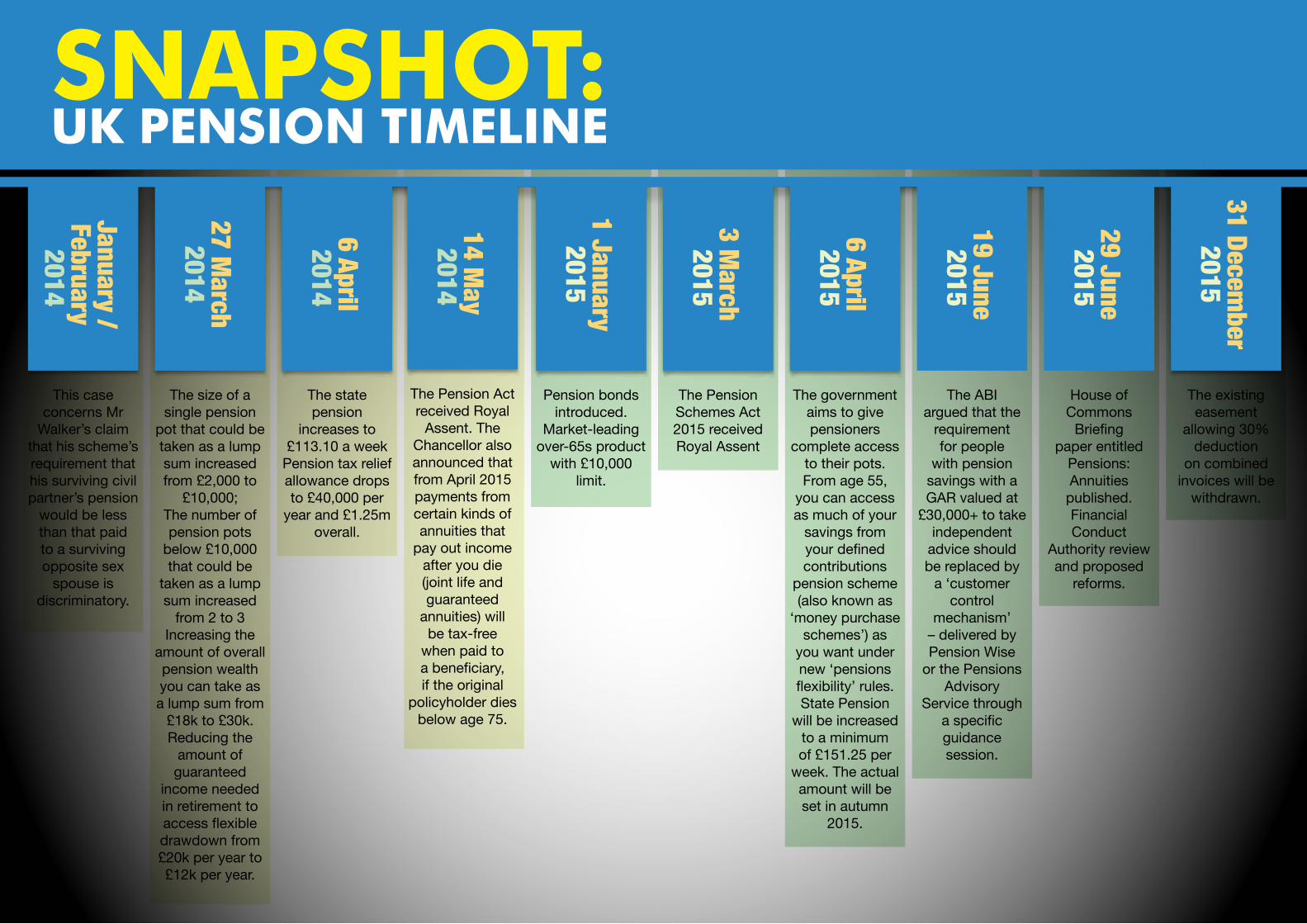

SNAPSHOT: UK PeNSiON TimeliNe

January /February

2014

27 March

2014

6 April 2014

14 May

2014

1 January 2015

3 March

2015

6 April 2015

19 June 2015

29 June 2015

31 December

2015

the state pension

increases to £113.10 a week

Pension tax relief allowance drops to £40,000 per

year and £1.25m overall.

this case concerns mr

Walker’s claim that his scheme’s requirement that his surviving civil partner’s pension

would be less than that paid to a surviving opposite sex

spouse is discriminatory.

the Pension Act received Royal

Assent. the Chancellor also announced that from April 2015 payments from certain kinds of annuities that

pay out income after you die (joint life and guaranteed

annuities) will be tax-free

when paid to a beneficiary, if the original

policyholder dies below age 75.

the size of a single pension

pot that could be taken as a lump sum increased from £2,000 to

£10,000;the number of pension pots

below £10,000 that could be

taken as a lump sum increased

from 2 to 3Increasing the

amount of overall pension wealth you can take as a lump sum from

£18k to £30k.reducing the

amount of guaranteed

income needed in retirement to access flexible drawdown from £20k per year to £12k per year.

Pension bonds introduced.

market-leading over-65s product

with £10,000 limit.

the ABI argued that the

requirement for people

with pension savings with a GAR valued at

£30,000+ to take independent

advice should be replaced by

a ‘customer control

mechanism’ – delivered by Pension Wise

or the Pensions Advisory

Service through a specific guidance session.

the Pension schemes Act 2015 received royal Assent

House of Commons

Briefing paper entitled

Pensions: Annuities published. Financial Conduct

Authority review and proposed

reforms.

The government aims to give pensioners

complete access to their pots. From age 55,

you can access as much of your

savings from your defined contributions

pension scheme (also known as

‘money purchase schemes’) as

you want under new ‘pensions flexibility’ rules. state Pension

will be increased to a minimum of £151.25 per

week. the actual amount will be set in autumn

2015.

the existing easement

allowing 30% deduction

on combined invoices will be

withdrawn.

Belgium

42 43July 2015 July 2015

ExpErt guidE: pEnsions 2015BeLgIum

Isabellen [email protected] +32 2 426 14 14

Belgium (finally) almost on the European track for the increase of the legal pension age By Isabellen Timmerman

regime for employees.

1. Increase in the legal pension age to 67 years

The legal pension age in Belgium currently is 65 years. However, it will be increased to 66 years in 2025, and then to 67 years in 2030.

2. Increase in the early retirement age and career conditions

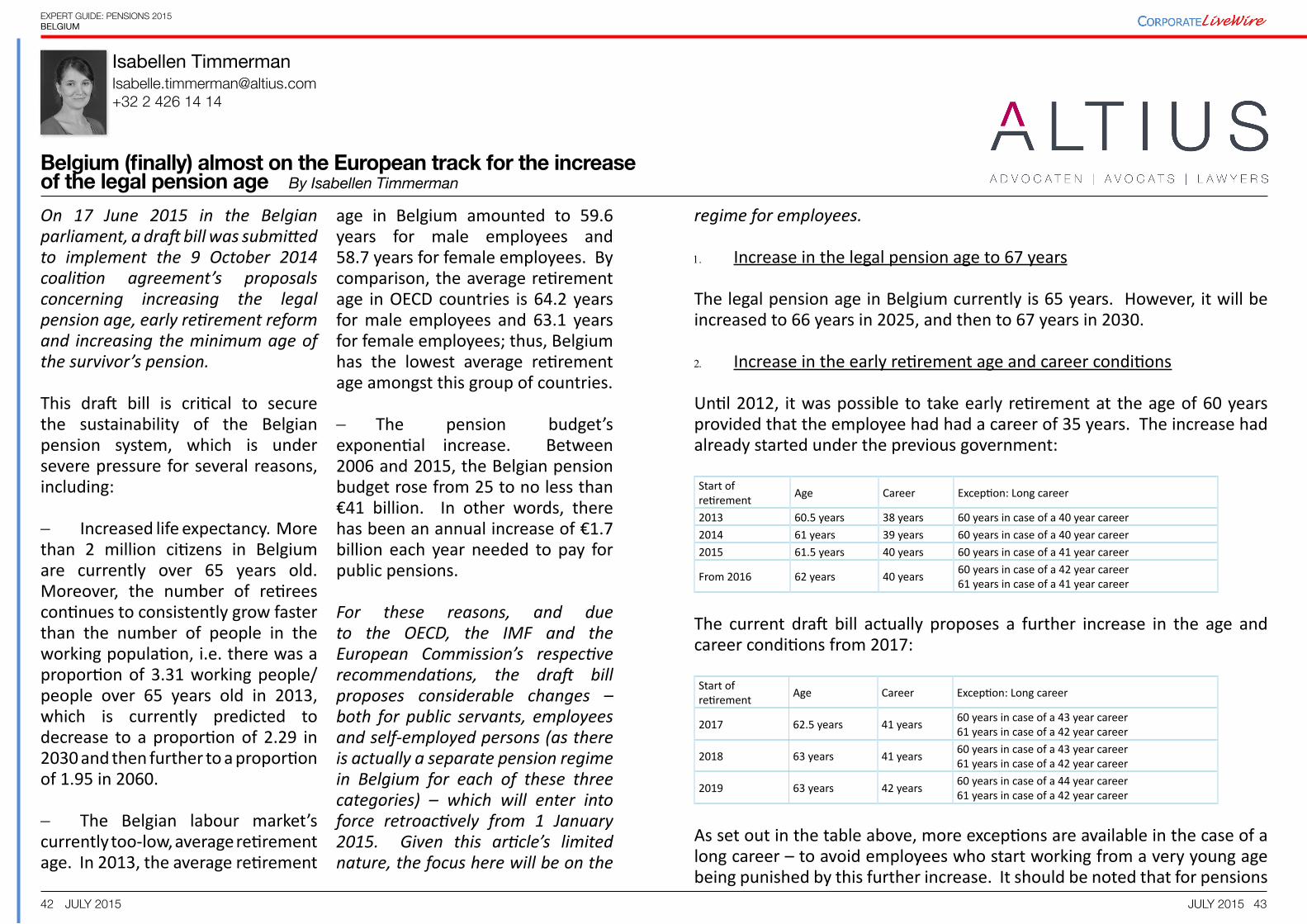

Until 2012, it was possible to take early retirement at the age of 60 years provided that the employee had had a career of 35 years. The increase had already started under the previous government:

Start of retirement Age Career Exception: Long career

2013 60.5 years 38 years 60 years in case of a 40 year career 2014 61 years 39 years 60 years in case of a 40 year career 2015 61.5 years 40 years 60 years in case of a 41 year career

From 2016 62 years 40 years 60 years in case of a 42 year career 61 years in case of a 41 year career

The current draft bill actually proposes a further increase in the age and career conditions from 2017:

Start of retirement Age Career Exception: Long career

2017 62.5 years 41 years 60 years in case of a 43 year career 61 years in case of a 42 year career

2018 63 years 41 years 60 years in case of a 43 year career 61 years in case of a 42 year career

2019 63 years 42 years 60 years in case of a 44 year career 61 years in case of a 42 year career

As set out in the table above, more exceptions are available in the case of a long career – to avoid employees who start working from a very young age being punished by this further increase. It should be noted that for pensions

On 17 June 2015 in the Belgian parliament, a draft bill was submitted to implement the 9 October 2014 coalition agreement’s proposals concerning increasing the legal pension age, early retirement reform and increasing the minimum age of the survivor’s pension.

This draft bill is critical to secure the sustainability of the Belgian pension system, which is under severe pressure for several reasons, including:

- Increased life expectancy. More than 2 million citizens in Belgium are currently over 65 years old. Moreover, the number of retirees continues to consistently grow faster than the number of people in the working population, i.e. there was a proportion of 3.31 working people/people over 65 years old in 2013, which is currently predicted to decrease to a proportion of 2.29 in 2030 and then further to a proportion of 1.95 in 2060.

- The Belgian labour market’s currently too-low, average retirement age. In 2013, the average retirement

age in Belgium amounted to 59.6 years for male employees and 58.7 years for female employees. By comparison, the average retirement age in OECD countries is 64.2 years for male employees and 63.1 years for female employees; thus, Belgium has the lowest average retirement age amongst this group of countries.

- The pension budget’s exponential increase. Between 2006 and 2015, the Belgian pension budget rose from 25 to no less than €41 billion. In other words, there has been an annual increase of €1.7 billion each year needed to pay for public pensions.

For these reasons, and due to the OECD, the IMF and the European Commission’s respective recommendations, the draft bill proposes considerable changes – both for public servants, employees and self-employed persons (as there is actually a separate pension regime in Belgium for each of these three categories) – which will enter into force retroactively from 1 January 2015. Given this article’s limited nature, the focus here will be on the

44 45July 2015 July 2015

ExpErt guidE: pEnsions 2015BeLgIum

a notice period or payment of an indemnity in lieu of notice, provided that (i) the indemnity in lieu of notice or the period covered by the indemnity in lieu of notice has started prior to 9 October 2014 (the date of the coalition agreement) and terminates after 31 December 2016 and (ii) provided that the age and career conditions for early retirement have been met either at the end of the notice period, or the period covered by the indemnity in lieu of notice.

• employees whose employment contract with their employer has been terminated by mutual consent, to the extent (i) this agreement has been concluded in writing prior to 9 October 2014 (ii) beyond the context of a bridging pension and (iii) is based on legal or regulatory provisions, either in the working rules, a collective bargaining agreement or a pension regulation and (iv) the age and career conditions for early retirement have been met at the

time of the end of the employment contract.

3. Increase in the minimum age of the survivor’s pension

Finally, the age condition for the survivor’s pension, which is currently set at 45 years, will also increase systematically – similarly to the legal pension – i.e. until 50 years in 2025 and 55 years in 2030. This change is intended to encourage widowers/widows to undertake a professional activity, even when they benefit from a survivor’s allowance.

Finally, the draft bill applies some changes and amendments to the survivor’s pension and the transitional allowance (i.e. the surviving spouse, who does not meet the conditions for a survivor’s pension, can, as long as they do not remarry, receive a temporary allowance (24 months or 12 months, depending on the situation of any dependent children).

starting in the month of January, the age and career conditions of the previous year’s December (i.e. the preceding month) will apply.

Furthermore, the following transitional measures have been provided:

Employees having reached the age of at least 59 years in 2016 will still be entitled to early retirement on the basis of the age and career conditions to which they would have been entitled if no further changes would have taken place, each increased by one year.

For example: An employee is 59 years old in 2016 and has a 37 year career. This situation implies that – on the basis of the current conditions (table 1) – the employee would be able to take their early retirement in 2019 (i.e. at the age of 62 years and a 40 year career). However, the current draft bill (table 2) sets the age and career conditions in 2019 at

respectively 63 years and 42 years, which means that the employee would have to work 2 years longer. The transitional measures allow the employee to limit the number of years to be worked further to one year, as a consequence of which the employee will already be able to take their early retirement in 2020 rather than in 2021.

Following the consultation with the social partners, two other transitional measures have been provided towards employees who have been dismissed/who have resigned or whose employment contract will be terminated by mutual consent.

In particular, the current conditions for early retirement continue to apply towards:

• employees who have been dismissed, who have resigned or who have concluded an agreement terminating their employment contract upon the performance of

46 47July 2015 July 2015

ExpErt guidE: pEnsions 2015

The Belgian coalition government’s original intention was that the Belgian parliament’s Commission on Social Affairs would vote on the draft bill on 22 June 2015. However this vote did not happen due to the opposition’s lack of support after a session of 16 hours. The Commission finally voted on the draft bill on 30 June

She also has experience in advising corporate clients in transfer of business, outsourcing and co-sourcing projects and employment issues related to the sale or purchase of businesses or part of businesses.. She is also heavily involved in

Isabelle assists national and international companies in the daily operation of the company on all employment matters of individual/collective labour and social security law (e.g., employment contracts, negotiations in view of reaching a settlement following the termination of high level management personnel).

employment disputes before the Employment Courts and Employment Appeal Courts.

She specializes in pension law and all aspects of employee representation.

BeLgIum

48 49July 2015 July 2015

ExpErt guidE: pEnsions 2015exPert dIreCtorY

Expert Directory

Gordon Dadds LLP

robert [email protected]+44 (0) 207 518 0251

www.gordondadds.com

Nabarro LLP

Anne-marie [email protected]+44 (0) 207 524 6143

www.nabarro.com

Pinsent Masons LLP

tom [email protected]+44 (0) 113 225 5451

www.pinsentmasons.com

Aries Insight

Ian [email protected]+44 (0) 153 676 3352

www.ariesinsight.co.uk

Simmons & Simmons LLP

danny [email protected]+ 44 (0) 207 825 4153

edward [email protected]+44 (0) 207 825 4261

www.simmons-simmons.com

Broadstone Ltd

John Broome [email protected]+44 (0) 207 893 3441

www.broadstoneltd.co.uk

Central Wealth Management Limited

Ian [email protected]+44 (0) 845 006 6204

www.centralfinancialplanning.co.uk

ALTIUS

Isabellen [email protected]+32 2 426 14 14

www.altius.com

United Kingdom Belgium

Corporate LiveWire Expert Guides are available on all platforms. Access everything from our latest publication to our archived collection through your computer, laptop, tablet or smart phone. It ’s as easy as one click of the button or a tap of the screen.

An InsIght Into the CorporAte World

Connecting The Corporate WorldWired