Copyright of Shell South Africa Upstream B.V. January 2013 Copyright of Shell South Africa Upstream B.V. THE POTENTIAL OF GAS IN SOUTH AFRICA – SHELL’S PERSPECTIVE Jan Willem Eggink General Manager - Shell South Africa Upstream B.V.

Transcript

Copyright of Shell South Africa Upstream B.V. 1 January 2013

Copyright of Shell South Africa Upstream B.V.

THE POTENTIAL OF GAS IN SOUTH AFRICA – SHELL’S PERSPECTIVE

Jan Willem Eggink General Manager - Shell South Africa Upstream B.V.

Copyright of Shell South Africa Upstream B.V. 2 January 2013 Copyright of Shell South Africa Upstream B.V. 2

CAUTIONARY NOTE

The companies in which Royal Dutch Shell plc directly and indirectly owns investments are separate entities. In this presentation “Shell”, “Shell group” and “Royal Dutch Shell” are sometimes used for convenience where references are made to Royal Dutch Shell plc and its subsidiaries in general. Likewise, the words “we”, “us” and “our” are also used to refer to subsidiaries in general or to those who work for them. These expressions are also used where no useful purpose is served by identifying the particular company or companies. The term “Shell interest” is used for convenience to indicate the direct and/or indirect (for example, through our 24% shareholding in Woodside Petroleum Ltd.) ownership interest held by Shell in a venture, partnership or company, after exclusion of all third-party interest.

This presentation contains forward-looking statements concerning the financial condition, results of operations and businesses of Royal Dutch Shell. All statements other than statements of historical fact are, or may be deemed to be, forward-looking statements. Forward-looking statements are statements of future expectations that are based on management’s current expectations and assumptions and involve known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied in these statements. Forward-looking statements include, among other things, statements concerning the potential exposure of Royal Dutch Shell to market risks and statements expressing management’s expectations, beliefs, estimates, forecasts, projections and assumptions.

These forward-looking statements are identified by their use of terms and phrases such as ‘‘anticipate’’, ‘‘believe’’, ‘‘could’’, ‘‘estimate’’, ‘‘expect’’, ‘‘intend’’, ‘‘may’’, ‘‘plan’’, ‘‘objectives’’, ‘‘outlook’’, ‘‘probably’’, ‘‘project’’, ‘‘will’’, ‘‘seek’’, ‘‘target’’, ‘‘risks’’, ‘‘goals’’, ‘‘should’’ and similar terms and phrases. There are a number of factors that could affect the future operations of Royal Dutch Shell and could cause those results to differ materially from those expressed in the forward-looking statements included in this presentation, including (without limitation): (a) price fluctuations in crude oil and natural gas; (b) changes in demand for the Shell’s products; (c) currency fluctuations; (d) drilling and production results; (e) reserve estimates; (f) loss of market share and industry competition; (g) environmental and physical risks; (h) risks associated with the identification of suitable potential acquisition properties and targets, and successful negotiation and completion of such transactions; (i) the risk of doing business in developing countries and countries subject to international sanctions; (j) legislative, fiscal and regulatory developments including potential litigation and regulatory measures as a result of climate changes; (k) economic and financial market conditions in various countries and regions; (l) political risks, including the risks of expropriation and renegotiation of the terms of contracts with governmental entities, delays or advancements in the approval of projects and delays in the reimbursement for shared costs; and (m) changes in trading conditions. All forward-looking statements contained in this presentation are expressly qualified in their entirety by the cautionary statements contained or referred to in this section. Readers should not place undue reliance on forward-looking statements.

Additional factors that may affect future results are contained in Royal Dutch Shell’s 20-F for the year ended 31 December, 2011 (available at www.shell.com/investor and www.sec.gov ). These factors also should be considered by the reader. Each forward-looking statement speaks only as of the date of this presentation, 4th March 2013. Neither Royal Dutch Shell nor any of its subsidiaries undertake any obligation to publicly update or revise any forward-looking statement as a result of new information, future events or other information. In light of these risks, results could differ materially from those stated, implied or inferred from the forward-looking statements contained in this presentation.

The United States Securities and Exchange Commission (SEC) permits oil and gas companies, in their filings with the SEC, to disclose only proved reserves that a company has demonstrated by actual production or conclusive formation tests to be economically and legally producible under existing economic and operating conditions. We use certain terms in this presentation, such as resources and oil in place, that SEC's guidelines strictly prohibit us from including in filings with the SEC. U.S. Investors are urged to consider closely the disclosure in our Form 20-F, File No 1-32575, available on the SEC website www.sec.gov. You can also obtain these forms from the SEC by calling 1-800-SEC-0330.

Copyright of Shell South Africa Upstream B.V. 3 January 2013 Copyright of Shell South Africa Upstream B.V. 3 January 2013

GLOBAL ENERGY OUTLOOK

ENERGY DEMAND +60% 2010 – 2050

HYDROCARBONS DOMINATE OUTLOOK

NATURAL GAS WILL PLAY A KEY ROLE

OIL

NATURAL GAS

BIOMASS

WIND

COAL

NUCLEAR

SOLAR

OTHER RENEWABLES

Copyright of Royal Dutch Shell plc.

Copyright of Shell South Africa Upstream B.V. 5 January 2013 Copyright of Shell South Africa Upstream B.V. 5

DRAMATIC IMPACT OF US TIGHT GAS REVOLUTION

Source: EIA Annual Energy Outlook 2011 Early release

bcm

Imports

2005

800

2010

Tight gas

Shale gas

Alaska

0

200

400

600

1990 2000 2020 2030

Associated gas

Offshore

Conventional

CBM

Conventional

Tight

Copyright of Shell South Africa Upstream B.V. 6 January 2013 Copyright of Shell South Africa Upstream B.V. 6 January 2013 Copyright of Shell South Africa Upstream B.V.

Copyright of Shell South Africa Upstream B.V. 7 January 2013 Copyright of Shell South Africa Upstream B.V. 7

SHARE OF GAS IN PRIMARY ENERGY MIX

THE SHARE OF NATURAL GAS IN THE PRIMARY ENERGY MIX IS EXPECTED TO INCREASE IN THE 3 LARGEST GAS MARKETS (MODERATE INCREASE IN OECD)

Source: WoodMac for USA and Europe, WoodMac and Shell analysis for China

USA EUROPE CHINA

Others Coal Natural Gas Oil

2010 2030 2010 2030 2010 2030

~16,000 ~19,500

~14,000 ~16,000 ~17,000

~31,000 Total primary energy (mln boe)

16%

38%

24%

22%

20%

33%

23%

24%

23%

36%

16% 25%

28%

31%

13%

28%

13% 17%

66%

4%

14%

25%

51%

10%

Copyright of Shell South Africa Upstream B.V. 8 January 2013 Copyright of Shell South Africa Upstream B.V. 8

RSA ENERGY SUPPLY - GAS

Its not an either-or discussion A mix of energy sources provides flexibility of supply Gas is the best back-up to intermittent sources Early gas would be imports – LNG (or pipeline) Shale gas will take some 10 years for material start-up It is key to find out soonest whether shale gas is there

-> is South Africa spending enough efforts on energy efficiency/saving ?

Copyright of Shell South Africa Upstream B.V. 9 January 2013 Copyright of Shell South Africa Upstream B.V. 9

LNG

Copyright of Shell South Africa Upstream B.V. 10 January 2013 Copyright of Shell South Africa Upstream B.V. 10

WHAT IS LNG?

WORLD LNG PRODUCTION IN 2011 = ~244 MILLION TONNES

Natural Gas production and separation from oil and water (when present)

Natural Gas cooled to liquid state at -160oC and atm. pressure (volume reduced 600 fold)

LNG transported over long distances in purpose built carriers

LNG returned to gas state and injected into the transport pipeline network for distribution and sales

PRODUCTION LIQUEFACTION SHIPPING REGASIFICATION

COST EFFECTIVE ALTERNATIVE TO PIPELINE

Copyright of Shell South Africa Upstream B.V. 11 January 2013 Copyright of Shell South Africa Upstream B.V. 11

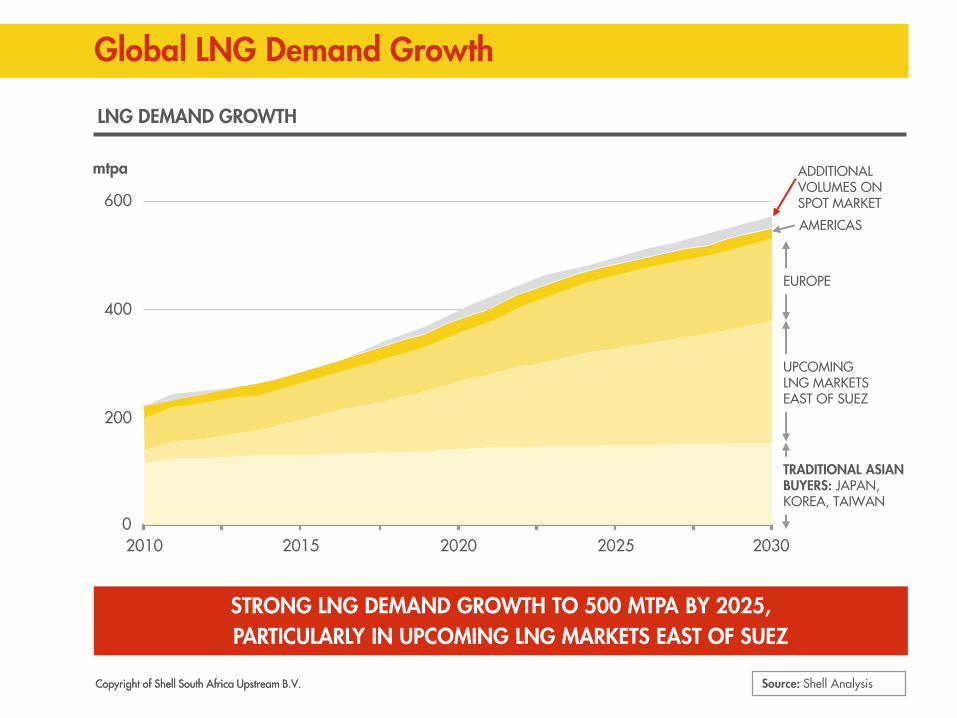

Global LNG Demand Growth

600

2020

0

200

400

2010 2015 2025 2030

TRADITIONAL ASIAN BUYERS: JAPAN, KOREA, TAIWAN

LNG DEMAND GROWTH

STRONG LNG DEMAND GROWTH TO 500 MTPA BY 2025, PARTICULARLY IN UPCOMING LNG MARKETS EAST OF SUEZ

mtpa ADDITIONAL VOLUMES ON SPOT MARKET

UPCOMING LNG MARKETS EAST OF SUEZ

EUROPE

AMERICAS

Source: Shell Analysis

Copyright of Shell South Africa Upstream B.V. 12 January 2013 Copyright of Shell South Africa Upstream B.V. 12

GLOBAL LNG MARKET DEVELOPMENTS

LNG IMPORTERS LNG EXPORTERS

2010 2020

NUMBERS OF COUNTRIES IMPORTING LNG EXPECTED TO ALMOST DOUBLE BETWEEN 2010 AND 2020

# COUNTRIES 1990 2000 2010 2011* 2020 EST

EXPORTERS 8 12 18 18 ~25

IMPORTERS 9 11 24 25 ~40

Source: Wood Mackenzie LNG (April 2010)

* Source: PFC Energy (2011 Actuals)

Copyright of Shell South Africa Upstream B.V. 13 January 2013 Copyright of Shell South Africa Upstream B.V. 13

GLOBAL LNG LEADERSHIP

SHELL GLOBAL LNG CAPACITY GROWTH SHELL LNG LEADERSHIP

0

5

10

15

20

25

30

Shell Exxon Chevron BG Total BP

Year end mtpa

2017 2011

~90% Long-term contracted ~80% of portfolio oil price linked

mtpa

CONSTRUCTION ONSTREAM OPTIONS

2011 ~2020+

0

5

10

15

20

25

30

35

40

45

Pluto T1 (Woodside)

Gorgon T1-3

Wheatstone & Prelude

SHELL

PROJECTS IN OPERATION OR UNDER CONSTRUCTION

Copyright of Shell South Africa Upstream B.V. 14 January 2013 Copyright of Shell South Africa Upstream B.V. 14 January 2013

SPAIN HAZIRA BAJA DUBAI ELBA ISLAND ALTAMIRA COVE POINT AC

CES

S

TO K

EY

STRA

TEG

IC

MA

RKET

S

ARKAT

SHIPPING

GREEN CORRIDOR

LNG FOR TRANSPORT

Copyright of Shell South Africa Upstream B.V. 15 January 2013 Copyright of Shell South Africa Upstream B.V. 15 January 2013

PRELUDE FLNG

2011: FIRST INDUSTRY FID ON FLNG ON PRELUDE

CONSTRUCTION SOUTH KOREA: OPTIONS FOR FURTHER PROJECTS

TARGETING NEW EXPLORATION FOR FLNG

FLOATING LNG LEADERSHIP

Dec 2012

10

Copyright of Shell South Africa Upstream B.V. 16 January 2013 Copyright of Shell South Africa Upstream B.V. 16

LNG FOR TRANSPORT OVERVIEW

Conventional

LNG carrier FSRU / Import terminal Power plant

LNG trailer truck LNG refuelling station LNG fuelled truck

Small-scale liquefaction

(e.g. MMLS, bio-LNG)

LNG bunker vessel LNG fuelled vessel Small terminal

Small LNG carrier

Marine

Road

Mining Rail

Copyright of Shell South Africa Upstream B.V. 17 January 2013 Copyright of Shell International Exploration and Production MOST CONFIDENTIAL Copyright of Shell International Exploration and Production

SHELL INNOVATION: Moveable Modular Liquefaction Station

Solution for Mini or ‘Small Scale’ LNG Production

Can Unlock Coal Bed Methane/Shale Gas Reserves

Construction times: FID to 1st LNG < 24 months for first unit and ~12 months for repeat systems

Standardized and Fully-Modularized & Re-Deployable

Capacity 0.1 - 0.25 MPTA (~150-400K LNG g/d)

Cost Competitive and LNG Supply

All equipment, including pipe-racks

come in skids which fit on ‘regular’

trucks

Copyright of Shell South Africa Upstream B.V. 18 January 2013 Copyright of Shell South Africa Upstream B.V. 18

Shale Gas

Copyright of Shell South Africa Upstream B.V. 19 January 2013 Copyright of Shell South Africa Upstream B.V. 19

KAROO SHALE GAS IN SOUTH AFRICA

Cape Town

Mossel Bay Port Elizabeth

East London

Queenstown

Bloemfontein

Johannesburg

Sutherland Beaufort West

Oil Gas Refined Products Pipelines:

Falcon ER Application Bundu ER

Shell TCP

Shell ER Applications

Copyright of Shell South Africa Upstream B.V. 20 January 2013 Copyright of Shell South Africa Upstream B.V. 20 January 2013

Permeable Sandstone Shale Tight Sandstone

Oil Window

Gas Window

Shale Gas Potential

Liquids-Rich Potential Oil Window

Gas Window

Low Permeability

Stratigraphically Trapped Oil

CONVENTIONAL OIL VS. LIQUIDS-RICH SHALES

Copyright of Shell South Africa Upstream B.V.

Copyright of Shell South Africa Upstream B.V. 21 January 2013 Copyright of Shell South Africa Upstream B.V. 21 January 2013

Copyright of Shell South Africa Upstream B.V. 22 January 2013 Copyright of Shell South Africa Upstream B.V. 22

KEY EXPERIENCE AND TECHNOLOGIES

Sweet Spotting

Well Design to protect water resources Pad Drilling to reduce surface foot print

Copyright of Shell South Africa Upstream B.V. 23 January 2013 Copyright of Shell South Africa Upstream B.V. 23 January 2013

Copyright of Shell South Africa Upstream B.V. 24 January 2013 Copyright of Shell South Africa Upstream B.V. 24 January 2013

ECONOMETRIX ECONOMIC STUDY

Source: Econometrix March 2012 – based on constant 2010

20 tcf 50 tcf

Potential Life of Resource (years) 25 years 25 years

Potential Contribution to GDP (ZAR bn) ZAR 35bn ZAR 90bn

Potential Permanent Employment 300,000 700,000

Copyright of Shell South Africa Upstream B.V. 25 January 2013 Copyright of Shell South Africa Upstream B.V. 25

SHALE GAS EXPLORATION AND DEVELOPMENT

Nine year exploration period (>ZAR 1.5 Bln, limited jobs) Followed by 30 year production period (ZAR xx Bln, jobs) Development concept is through multi-well ‘well pads’ Volume potential 0 to >> 100 Tcf (EIA estimate = 485 Tcf) 6 Tcf development would generate > 40,000 GWh from 6 GW base-

load at 80% load South Africa needs 56 GW of new electricity generation by 2030 (IRP 2010)

Need operator with high standards – environmentally safe High energy intensity/footprint : energy from a single 20 well pad

equates ~180 2MW wind turbines or 8-10 sqkm solar PV

Copyright of Shell South Africa Upstream B.V. 26 January 2013 Copyright of Shell South Africa Upstream B.V. 26 January 2013

LOCATION MAP – ORANGE BASIN & SHELL BLOCK

Kudu

DSDP 361

Copyright of Shell South Africa Upstream B.V. 27 January 2013 Copyright of Shell South Africa Upstream B.V. 27

OVERALL GAS SUMMARY

Energy demand in South Africa will more than double by 2050, CO2 becomes a challenge

LNG allows early access to gas with its advantages (clean, available, multiple sources, fast)

Shale gas may be a game changer to South Africa (self-sufficiency in energy?)

Mix of Energy required, with flexible supply options Demand growth can be reduced through energy

efficiency/savings

Copyright of Shell South Africa Upstream B.V. 28 January 2013 Copyright of Shell South Africa Upstream B.V. 28 January 2013 28