Page 1

Department of Economics University of St. Gallen

The Pricing of Convertible BondsAn Analysis of the French market

Manuel Ammann, Axel H. Kind, Christian Wilde

March 2001 Discussion paper no. 2001-02

Page 2

Editor: Prof. Jörg BaumbergerUniversity of St. GallenDepartment of EconomicsBodanstr. 1CH-9000 St. GallenPhone ++41 71 224 22 41Fax ++41 71 224 28 85Email [email protected]

Publisher:

Electronic Publication:

Forschungsgemeinschaft für Nationalökonomiean der Universität St. GallenDufourstrasse 48CH-9000 St. GallenPhone ++41 71 224 23 00Fax ++41 71 224 26 46www.fgn.unisg.ch/public/public.htm

Page 3

The Pricing of Convertible Bonds

An Analysis of the French Market1

Manuel Ammann, Axel H. Kind, Christian Wilde

Authors‘ addresses: Dr. Manuel AmmannAxel H. Kind, lic. oec. HSGChristian Wilde, lic. oec. HSG

University of St. GallenSwiss Institute of Banking and FinanceRosenbergstrasse 52CH-9000 St. GallenTel. ++41 71 224 70 60Fax ++41 71 224 70 88Email [email protected]

[email protected] @unisg.ch

Website www.sbf.unisg.ch

======================================

1=All convertible bond time series used in this study were provided by Mace Advisers through UBS Warburg.

We thank Zeno Dürr of UBS Warburg for his assistance in obtaining the data and for very helpful discussions.

Furthermore, we thank Zac Bobolakis, Jörg Baumberger, and seminar participants at the University of St.Gallen

for useful comments.

Page 4

Abstract

We investigate the pricing performance of three convertible bond pricing models on the

French convertible bond market using daily market prices. We examine a component model

separating the convertible bond into a bond and option component, a method based on the

Margrabe model for pricing exchange options, and a binomial-tree model with exogenous

credit risk. All three models are found to deliver theoretical values for the analyzed

convertible bonds that tend to be higher than the observed market prices. The prices

obtained by the binomial-tree model are nearest to market prices and the mispricing is no

longer statistically significant for the majority of bonds in our sample. For all models, the

difference between market and model prices is greater for out-of-the money convertibles

than for at- or in-the-money convertibles.

Keywords

Convertible bonds, pricing, French market, binomial tree, derivatives

JEL Classification

G13, G15

Page 5

3

Introduction

Convertible bonds are complex and widely used2 financial instruments combining the

characteristics of stocks and bonds. The possibility to convert the bond into a predetermined

number of stocks offers participation in rising stock prices with limited loss potential, given

that the issuer does not default on its bond obligation. Convertible bonds often contain other

embedded options such as call and put provisions. These options can be specified in various

different ways, further adding to the complexity of the instrument. Especially, conversion and

call opportunities may be restricted to certain periods or stock price conditions and the call

price may vary over time.

The purpose of this study is to investigate whether prices observed on secondary markets are

below the theoretical fair values (obtained by a contingent claims pricing model), as is

believed by many practitioners.

Theoretical research on convertible bond pricing was initiated by Ingersoll (1977a) and

Brennan and Schwartz (1977), who both applied the contingent claims approach to the

valuation of convertible bonds. In their valuation models, the convertible bond price depends

on the firm value as the underlying variable. Brennan and Schwartz (1980) extend their model

by including stochastic interest rates. However, they conclude that the effect of a stochastic

term structure on convertible bond prices is so small that it can be neglected for empirical

purposes. McConnell and Schwartz (1986) develop a pricing model based on the stock value

as stochastic variable. To account for credit risk, they use an interest rate that is grossed up by

a constant credit spread. Noting that credit risk of a convertible bond varies with respect to its

2 The Bank for International Settlements reports an outstanding amount of international convertible bonds of 223.6 billion US dollars (not

including domestic issues) per December 2000. (BIS 2001)

Page 6

4

moneyness, Tsiveriotis and Fernandes (1998) and Hull (2000) propose an approach that splits

the value of a convertible bond into a stock component and a straight bond component.

Buchan (1998) extends the Brennan and Schwartz (1980) model by allowing senior debt and

implements a Monte Carlo simulation approach to solve the valuation equation.

Despite the large size of international convertible bond markets, very little empirical research

on the pricing of convertible bonds has been undertaken. Previous research in this area was

performed by King (1986), who finds that for 103 American convertible bonds, 90 percent of

his model’s predictions fall within 10 percent of market values. More specifically, his results

suggest that, on average, a slight underpricing exists, i.e., market prices are below model

prices. Using monthly price data, Carayannopoulos (1996) empirically investigates 30

American convertible bonds for a one-year period beginning in the fourth quarter of 1989.

Using a convertible bond valuation model with Cox, Ingersoll and Ross (1985) stochastic

interest rates, he finds similar results as King (1986): While deep out-of-the-money bonds are

underpriced, at- or in-the-money bonds are slightly overpriced. Buchan (1997) implements a

firm value model using also a CIR term structure model. In contrast to the above mentioned

studies, she finds that, for 35 Japanese convertible bonds3, model prices are slightly below

observed market prices on average.

A drawback of these previous pricing studies is the small number of data points per

convertible bond: Buchan (1997) tests her pricing models only for one calendar day (bonds

priced per March 31, 1994), King (1986) for two days (bonds priced per March 31, 1977, and

December 31, 1977), and Carayannopoulos (1996) for twelve days (one year of monthly

3 All but one bond were out-of-the-money on March 31, 1994.

Page 7

5

data). Our study does not suffer from this limitation because we use almost 18 months of

daily price data.

We examine the French market for convertible bonds because of the availability of accurate

daily market prices. In fact, by international comparison, the French convertible bond market

is characterized by the availability of both high quality data and relatively high liquidity.

Nonetheless, no systematic pricing study for the French convertible-bond market has

previously been undertaken. Our sample includes the 21 most liquid convertible bonds, for

which daily convertible bond data from February 19, 1999, through August 5, 2000, are

analyzed.

We test three pricing models: a simple component model, an exchange-option model and a

binomial-tree model with exogenous credit risk. While the first two models are only rough

approximations, they can serve as very simple benchmark models. The third model, however,

is able to take into account many of the complex characteristics of convertible bonds. The

model-generated convertible bond prices are then compared to the market prices of the

investigated convertible bonds.

For all three pricing models tested, underpricing is detected on average. The results of the

binomial-tree model are closest to the market prices while the simple component model shows

the biggest deviations. For all convertible bonds, the binomial-tree model produces the lowest

prices. Furthermore, it is the only model that generates prices that are not, for the large

majority of bonds, statistically significantly different from market prices. For a few

convertible bonds, even overpricing can be observed, although it is not significant.

A partition of the sample according to the moneyness indicates that the underpricing

decreases for convertible bonds that are further in-the-money. Comparing the degree of

Page 8

6

underpricing to the maturity of the convertible bonds, we find that, the longer the maturity,

the lower is the market price observed relative to the price generated by the model.

The paper is organized as follows: First, we introduce the models used in the empirical

investigation. Second, we describe the data set and discuss the specific characteristics of the

convertible bonds examined. Finally, we present results of the empirical study comparing

theoretical model prices with observed market prices.

Pricing Models for Convertible Bonds

In the following, three models for pricing convertible bonds are presented. In addition to a

simple component model as it is often used in practice, the Margrabe (1978) method for

pricing exchange options is applied to convertible bonds. As a third and most precise

approach, a binomial-tree model with exogenous credit risk is implemented. To facilitate the

description, we use the same notation for all three models:

t = current time

Ωt = fair value of the convertible bond

T = maturity of the convertible bond

N = face value of the convertible bond

St = equity price (underlying) at time t

Ft = investment value (bond floor, pseudo-floor) at time t

σS,t = stock volatility at time t

σF,t = volatility of the investment value at time t

ρ = correlation between F and S

dS = continuously compounded dividend yield

c = continuously compounded coupon rate

Page 9

7

nt = conversion ratio at time t

rt,T = continuously compounded risk-free interest rate from time t to time T

ξt = credit spread at time t

ntSt = conversion value at time t

Kt = early redemption price (call price) at time t

Ξt = call trigger at time t

Θt = safety premium

κ = final redemption ratio at time T in percentage points of the face value

τK = start of the call period

TK = end of the call period

τΓ = start of the conversion period

TΓ = end of the conversion period

Component Model

In practice, a popular method for pricing convertible bonds is the component model, also

called the synthetic model. The convertible bond is divided into a straight bond component,

denoted by Ft, and a call option Ct on the conversion price Stnt, with strike price X=Ft. The

fair value of the two components can be calculated with standard formulas. The model is

therefore straightforward to implement.

The fair value of the straight bond with face value N, a continuously compounded coupon rate

c, and a credit spread ξt is calculated using the discounting formula

( )( )[ ] ( ) ( )( )[ ]tTrNtTcrNF tTttTtt −+−⋅−+−−+−⋅= ξκξ ,, exp1exp .

Page 10

8

κ is the final repayment ratio, indicating the amount of cash (in percentage of the face value),

which is paid out in case the convertible is held until maturity. Note that the amount of the

coupon payment refers to the face value while the redemption payment at maturity may differ

from the face value.

Given geometric Brownian motion under the risk-neutral measure for the stock price, i.e.,

( ) ttStSTtt dWSdtSdrdS σ+−= , , the fair value of the call option Ct with payoff

( ),0T TC Max S X= − is

( ) ( )1 , 2( ) exp exp ( )t t S r TC S N d d T t X r T t N d = − − − ⋅ − − ,

where

( )2

,,

1,2

,

ln2S tt

t T S

S t

Sr d T t

Xd

T t

σ

σ

+ − ± ⋅ − =−

Consequently, the fair price of the convertible is given by

ttt FC +=Ω .

This pricing approach has several drawbacks. First, separating the convertible into a bond

component and an option component relies on restrictive assumptions, such as the absence of

embedded options. Callability and putability, for instance, are convertible bond features that

cannot be considered in the above separation. In fact, while the Black and Scholes (1973)

closed-form solution for the option part of the convertible is extremely simple to use, it is

only a rough approximation for any but the rather rare plain-vanilla bonds.

Second, unlike call options, where the strike price is known in advance, convertible bonds

contain an option component with a stochastic strike price. It is stochastic because the value

of the bond to be delivered in exchange for the shares is usually not known in advance unless

Page 11

9

conversion is certain not to occur until maturity. In effect, the future strike price depends on

the future development of interest rates and the future credit spread.

Margrabe Model

Margrabe (1978) generalizes the Black and Scholes (1973) option pricing formula to price

options which give the holder the right to exchange an asset B for another asset S. Convertible

bonds can be viewed as the sum of a straight bond F plus an option giving the holder the right

to exchange the straight bond F for a certain amount of stocks, Sn ⋅ . Under the assumption

that geometric Brownian motion is a realistic process for straight bonds, the Margrabe

formula can be applied to pricing convertibles. Since both the price of a straight bond and the

price of a Margrabe option can be determined, the fair value of the convertible bond can be

calculated by simply adding the two components.

Given two correlated Brownian motions under the risk-neutral probability measure, WS and

WF with correlation coefficient ρ, we assume that ( ),S

t t T S t S t tdS r d S dt S dWσ= − + for the

stock and ( ),F

t t T t F t tdF r c F dt F dWσ= − + for the straight bond. Then the fair value of the

Margrabe option SF→Ψ with payoff ( )0,TTT FSMax −=Ψ is

( )[ ] ( )[ ]tTcdNFtTddNS tStt −−−−−=Ψ exp)(exp)( 21 ,

where

( )

tT

tTdcF

S

dS

t

t

−

−

±−+

=σ

σ2

ln2

2,1

and

tFtStFtSt ,,2

,2

, 2 σρσσσσ −+= .

Page 12

10

On the other hand, the fair value of the straight bond with face value N, a continuously

compounded coupon c and a credit spread ξt is calculated using the discounting formula

( )( )[ ] ( ) ( )( )[ ]tTrNtTcrNF tTttTtt −+−⋅−+−−+−⋅= ξκξ ,, exp1exp .

κ is the final repayment ratio, indicating the amount of cash (in percentage of the face value)

paid out if the convertible is held until maturity. Consequently, the fair price of the

convertible is given by

ttt F+Ψ=Ω .

The Margrabe method is in so far superior to the simple component model as it models the

stochastic behavior of the bond component. In particular, the correlation ρ of the two

processes is taken into account.

Unfortunately, this model also presents some drawbacks. First, the Margrabe option is

European, but almost all convertible bonds can be exercised prior to maturity. As long as the

coupon rate is less than the dividend yield, this is not a problem. As Subrahmanyam (1990)

points out, it is sub-optimal to exercise a Margrabe option prior to maturity if there is a so

called “yield advantage”, i.e., the cash flows of the exchangeable instrument is greater than

the cash flows of the obtained asset at each point.

Second, the option component of the convertible is calculated using an inflexible closed-form

solution. Similar to the component model introduced previously, additional embedded options

such as callability or putability features cannot be modeled at all.

Third, geometric Brownian motion is not necessarily a realistic assumption for the straight

bond process although, for long-maturity bonds, the distributional implications of using

geometric Brownian motion may not present a problem. However, the empirical observation

of mean-reverting interest rates is not taken into account.

Page 13

11

Binomial-Tree Model with Exogenous Credit Risk

Specifying the binomial tree

To price convertibles with a wide range of contractual specifications, we implement a Cox,

Ross and Rubinstein (1979) univariate binomial-tree model. Every pricing result is performed

using one hundred steps. For the calculation of the tree, a terminal condition and three

boundary conditions have to be satisfied.

The terminal condition is given by ( ),T T TMax n S NκΩ = ⋅ , where nT is the conversion ratio,

i.e. the number of stocks the bond can be exchanged for, κ is the final repayment ratio, and N

is the face value of the convertible. This condition is considered for all endnodes in the tree.

The following three boundary conditions are necessary due to the early-exercisable embedded

options. Because of the American character of the instrument, it is necessary to check them in

each node of the tree.

The conversion boundary condition implies that

ttt Sn ⋅≥Ω [ ]ΓΓ∈∀ Tt ,τ .

During the conversion period, the value of the convertible cannot be less than the conversion

value; otherwise, an arbitrage opportunity would exist.

The call boundary condition states that whenever tttSn Ξ> is satisfied,

( )ttttt SnMax ⋅Θ+Κ≤Ω , [ ]ΚΚ∈∀ Tt ,τ

must hold. Kt is the relevant call price at time t. Θt is a safety premium that accounts for the

empirical fact, described by Ingersoll (1977b), that the issuer usually does not call

immediately when Kt is triggered. Firms may want the conversion value to exceed the call

price by a certain amount to safely assure it will still exceed the call price at the end of the call

Page 14

12

notice period, which normally is three months in the French market. The safety premium is

set equal to zero in this study, resulting in a conservative valuation of the convertible bonds.

The price of a convertible bond cannot, at the same time, be higher than the conversion value

and higher than the call price. If such a situation occurred, the issuer could realize arbitrage

gains by calling the convertible.

The put boundary condition requires that

tt p≥Ω , [ ]pp Tt ,τ∈∀ .

pt is the relevant put price at time t. If the convertible price were below the relevant put price,

the investor could exercise the put option and realize a risk free gain. Since put features are

absent in our sample of convertible bonds, the put boundary condition does not affect the

results of this analysis.

In each node, it is necessary to check whether each boundary condition is satisfied and to

determine the implications on the value of the convertible bond with respect to the optimal

calling behavior of the issuer and the optimal conversion behavior of the investor4.

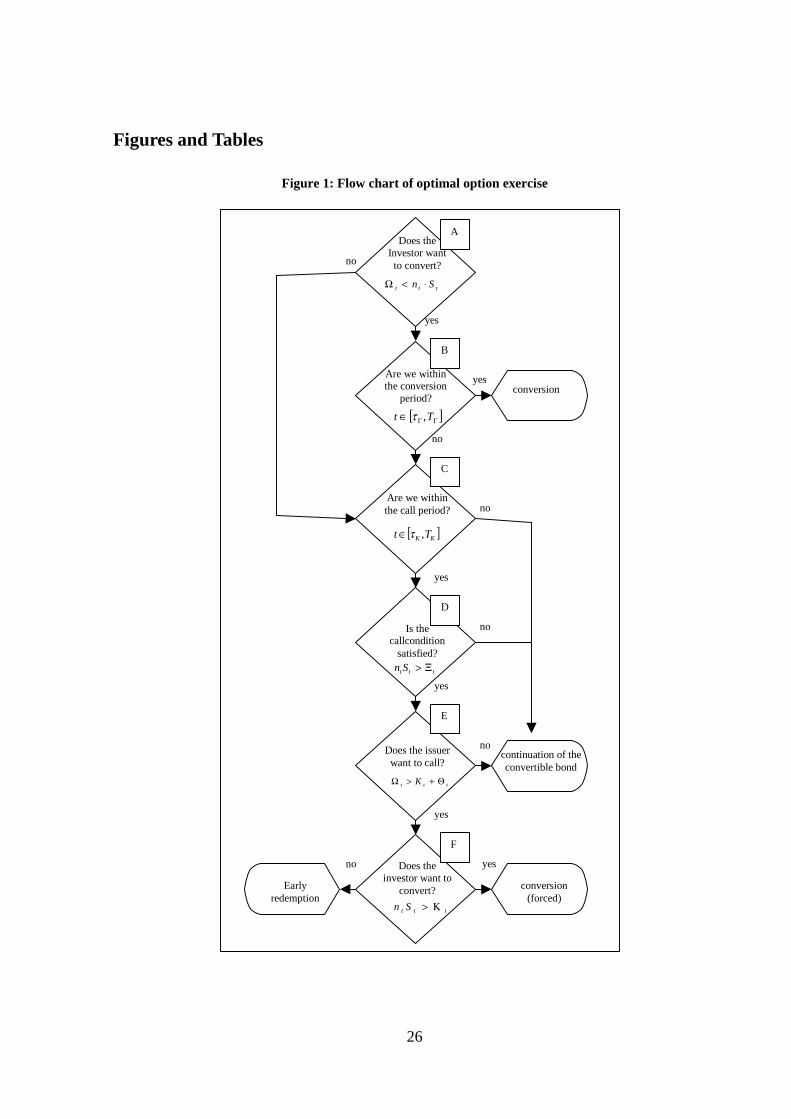

Figure 1 shows a computationally efficient way of checking the validity of the boundary

conditions and the effects on the convertible bond. There are four possible outcomes: The

convertible bond continues to exist without being called or converted. Alternatively, it may be

called by the issuer, converted by the holder, or called by the issuer and subsequently

converted by the investor. The last scenario is often called forced conversion because the

investor is induced to convert exclusively by the fact that the issuer has called the bond.

When pricing convertible bonds, a dilution effect has to be taken into account. Because, in

most cases, new shares are created upon conversion, the equity value is divided among a

4 For a discussion on the optimal call and conversion policy, see Ingersoll (1977a).

Page 15

13

higher number of shares. This effect is mitigated (but not canceled) because the liabilities of

the firm are reduced as the convertible debt ceases to exist after conversion. In order to price

convertibles correctly, it is necessary to adjust the stock price in the model downwards.

Dilution is only relevant in the nodes A and F of the flow chart, when the investor decides to

convert. In this study, the dilution effect may be overestimated because we assume that the

green shoe option was always exercised in full when the bond was issued and that the bond is

always converted into newly issued stocks.

Integration of Credit Risk

The classical convertible bond pricing articles of Ingersoll (1977a) and Brennan and Schwartz

(1977) use the firm value as a stochastic variable. This approach allows for rigorous modeling

of credit risk and dilution but is very hard to implement empirically because the firm value is

not observable.

Ingersoll (1977a) and Brennan and Schwartz (1977) assume a simplistic capital structure,

consisting solely of equity and convertible bonds. In reality, such a capital structure is rather

rare. Brennan and Schwartz (1980) adapt the terminal and boundary conditions to cope with

the problem of the existence of senior debt. What seems an elegant way of solving the capital

structure problem in theory can be very hard to implement in practice. As a practical way of

solving this problem, King (1986) suggests to subtract the value of all senior debt positions

from the firm value and to assume this variable to follow geometric Brownian motion.

Unfortunately, this procedure does not take into account the stochastic character of the senior

debt. For convertible bonds of companies with relatively large senior debt issues, this pricing

procedure can be a rather rough approximation.

McConnell and Schwartz (1986) present a pricing model based on the stock value as

stochastic variable. Since the stock price cannot become negative, it is impossible to simulate

Page 16

14

bankruptcy scenarios. In other words, the model architecture is not capable of accounting for

credit risk in a natural way. However, convertible bonds are especially popular with lower-

rated issuers. Therefore, credit risk is a very important aspect of convertible bond pricing. To

account for credit risk, McConnell and Schwartz (1986) use an interest rate that is “grossed up

to capture the default risk of the issuer” (pp. 567) rather than the risk-free rate. This solution,

however, leaves open many questions about its quantification because the credit risk of a

convertible bond varies with respect to its moneyness.

For this reason, Tsiveriotis and Fernandes (1998) and Hull (2000) propose an approach that

splits the value of a convertible bond into a stock component and a straight bond component.

These two components belong to different credit risk categories. The former is risk-free

because a company is always able to deliver its own stock. The latter, however, is risky

because coupon and principal payments depend on the issuer’s capability of distributing the

required cash amounts. It is straightforward to discount the stock part of the convertible with

the risk-free interest rate and the straight bond component with a risk-adjusted rate. On the

contrary, the McConnell and Schwartz (1986) procedure produces a pooling between the two

components, as if the ratio of the two parts were constant. In reality, however, the relative

weight of the bond component can vary dramatically. On the one hand, when the convertible

bond is deep in the money, its value should be discounted using the risk-free rate. On the

other hand, when the bond is out of the money, the straight bond component is very high and

so is its defaultable part. This strategy is an improvement over the McConnell and Schwartz

(1986) approach because it clearly identifies the defaultable part of the convertible and thus

its credit risk exposure. We therefore adopt this approach in incorporating a constant

Page 17

15

exogenous credit spread into our binomial-tree model5. The appropriate credit spread is given

by the difference between the yield to maturity of a straight bond of the company and the

yield to maturity of a risk-free sovereign bond. The bonds have to be comparable, i.e. they

must have similar seniority, coupon and maturity. If no straight bond comparable to the

convertible exists, the credit spread can be estimated using the rating of the issuing firm.

Data

Convertible Bonds

Because convertible bonds are often traded over-the-counter, finding reliable time series of

market prices can be difficult. Even when electronic systems are in use, the delivered prices

are often not the quotes at which the actual trades occur. Additionally, synchronic market

prices of the stocks for which the convertible bonds can be exchanged are needed for this

study. We found these data requirements best satisfied for the French market. Moreover, the

French convertible bond market is one the most liquid European convertible bond markets

with a fair number of large convertible bond issues. We therefore chose the French market for

this pricing study.

We consider all French convertible bonds outstanding as of August 5, 2000. Daily convertible

bond prices as well as the corresponding synchronic stock prices are available from February

19, 1999, through August 5, 2000.6

5 It could be argued that credit risk increases with decreasing stock price. Since our credit spread is assumed to be constant, our model does

not take this negative correlation into account.

6 Data source: Mace Advisers.

Page 18

16

To exclude illiquid issues from the sample, we require every issue to satisfy three conditions

cumulatively7:

- a minimum market capitalisation of USD 75 million,

- a minimum average exchange traded volume reported to Autex for the last two quarters of

the equivalent of USD 75 million,

- at least three market makers out of the top ten convertible underwriters quoting prices

with a maximum bid/ask spread of 2 percentage points.

In addition, cross-currency convertibles are excluded from the sample. As a result, our

convertible bond universe consists of 21 French franc/euro-denominated issues with a total of

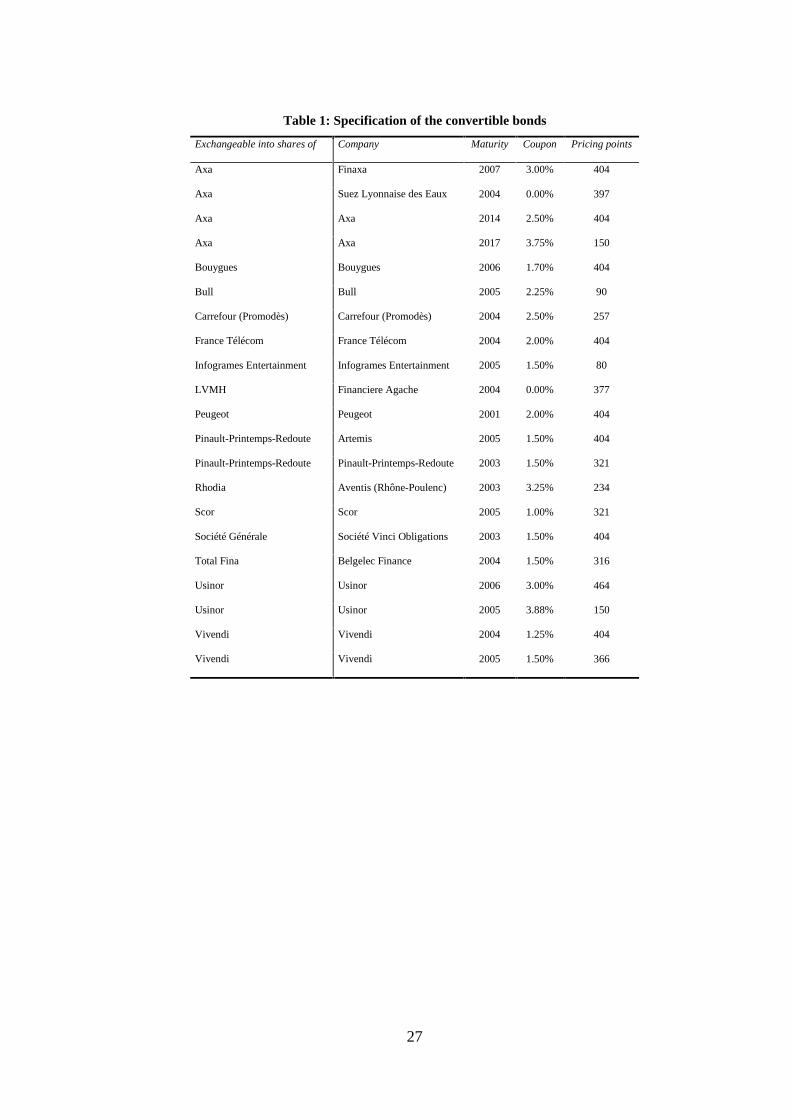

6760 data points. Table 1 gives an overview of the analyzed convertible bonds. All the

contractual specifications are extracted from the official and legally binding „offering

circulars“. This proved to be necessary because almost every electronic database tends to

suffer from an over-standardization syndrome. Although most bonds in our sample have very

similar specifications, some contractual provisions are so specific that they can hardly be

collected in predefined data types.

Several convertibles in our sample are “premium redemption” convertibles, i.e. the

redemption at maturity is above par value. In this case, the final redemption is given by κN

with the final redemption ratio κ greater than 1.

In the analyzed sample, there are seven exchangeable bonds. In these cases, the issuing firm

and the firm into the stock of which the bond can be converted are not the same firms.

7 These requirements are the same that UBS Warburg utilizes as exit criteria for its convertible bond index family.

Page 19

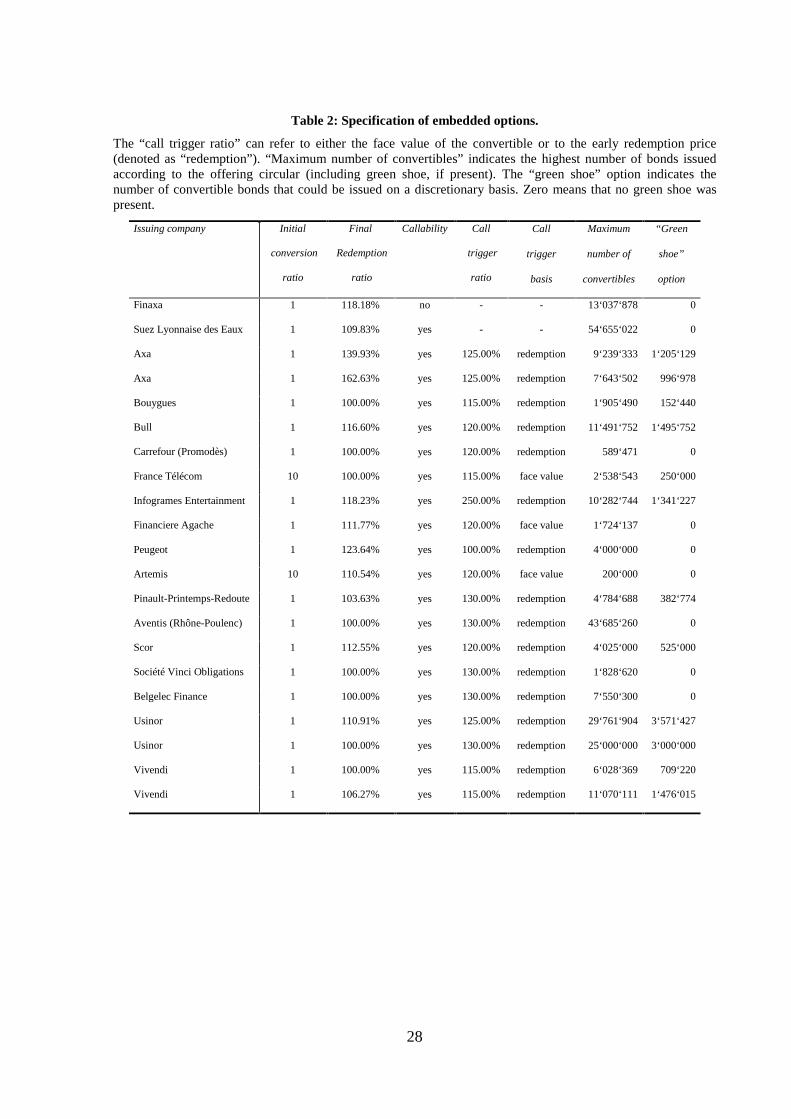

17

20 of the 21 analyzed convertibles include a call option, allowing the issuer to repurchase the

bond for a certain price Kt, called “call price” or “early redemption price”. This price varies

over time. Usually, the call price Kt is determined in such a way that the holder of the bond

obtains a similar return as when holding the convertible bond until maturity without

converting.

For almost all examined convertibles, early redemption is restricted to a certain predetermined

period from τK to TK. The period during which callability is not allowed is called the “call

protection period“. An additional restriction to callability in form of a supplementary

condition to be satisfied is given by the “call condition”. Callability is only allowed if the

parity ntSt exceeds a “call trigger” Ξt8. The call trigger is calculated as a percentage of either

the early redemption price or the face value (see Table 2). The last column shows, for each

bond, which of the two methods applies. If the trigger feature is present, the callability is

called “provisional” or “soft” call, if it is absent the callability is “absolute” or

“unconditional”. For almost all convertibles, the trigger feature is present. Only the bond

issued by Suez Lyonnaise des Eaux lacks a trigger and has an unconditional callability.

Another special case is Infograme Entertainment, which has a time-varying call trigger:

Within the period from May 30, 2000, to June 30, 2003, the call trigger is set at 250% of the

early redemption price. After July 1, 2003, the call trigger is reduced to 125% of the early

redemption price. For calculation in the binomial-tree model, we use the latter value.

Consequently, the model price may underestimate the fair value of this particular convertible

bond.

8 The exact contractual specification of the call condition often states that the inequality ntSt>Ξt must hold for a certain time (often 30 days)

before the bond becomes callable. This “qualifying period” introduces a path dependent feature not considered in the analysis.

Page 20

18

Usually, the conversion ratio tn is constant over time. It changes in case of an alteration of the

nominal value of the shares (stock subdivisions or consolidations), extraordinary dividend

payments and other financial operations that directly affect the stock price.

Conversion is possible within a certain period, called conversion period. The conversion

period starts at time τΓ and ends at time TΓ. For all the issues in our sample, the end of the

conversion period coincides with the maturity of the convertible bond, i.e. TΓ = T.

Dilution has been calculated on the basis of the number of shares outstanding9 and the number

of bonds to be issued as specified in the offering circulars. In twelve cases a “green shoe”

option was present, allowing the underwriter to increase the overall number of bonds. Because

we do not have any information regarding the exercise of the green shoe, we use the

maximum number of bonds (green shoe fully exercised) to estimate the dilution effect. Table

2 exhibits the number of bonds issued and the size of the green shoe option.

Interest Rates

For interest rates of one year or less (7 days, 1, 2, 3, 6, 12 months), we use Eurofranc rates10.

For longer maturities (1-10 years), we extract spot rates from swap rates using the standard

procedure. We observed that the one-year Eurofranc rate was systematically lower than the

corresponding one-year swap rate. Under the assumption that the Eurofranc rates represent a

better proxy for the theoretical credit risk-free rates, we adjust down the swap-extracted term

structure by the difference between the one-year Eurofranc rate and the one-year swap rate.

Furthermore, we use linear interpolation to obtain the complete continuous term structure of

spot rates.

9 Data source: Primark Datastream.

Page 21

19

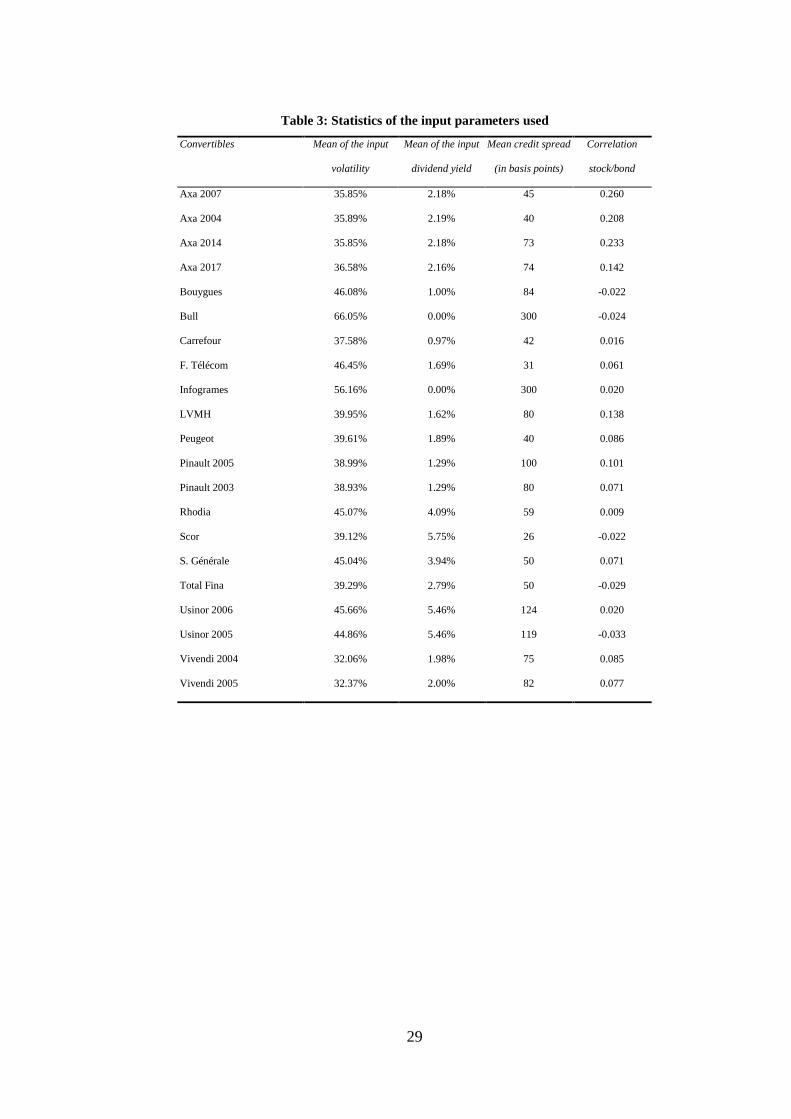

Unobservable Parameters

Besides directly observable input parameters, such as stock prices and interest rates, the

pricing models require input parameters that have to be estimated and thus are a source of

estimation error. These variables include volatility, dividends, correlations and credit spreads.

The most important input parameter to be estimated is the volatility of the underlying stock

price. Research on stock volatility estimation is plentiful. A popular approach is the implied

volatility concept. With option pricing formulas, it is possible to extract market participants’

volatility estimations from at-the-money option prices. However, most liquid options have

shorter maturities than convertibles. We therefore estimate volatility on a historical basis. The

relevant volatility is calculated as the standard deviation of the returns of the last 520 trading

days.

We model future dividends using a continuously compounded dividend yield. More precisely,

we assume that the best estimator for future dividends is the ratio of the current dividend11

level and the stock price. Furthermore, we assume that this ratio is constant over time.

The Margrabe model requires the correlation between the straight bond and the stock as an

input variable. Unfortunately, straight bonds with the same characteristics (coupon, maturity,

seniority) as the convertible bond are very rarely available. For this reason, we calculate the

correlation using time series of stock price and the theoretical investment value. The

investment value denotes the value of the convertible bond under the hypothetical assumption

that the conversion option does not exist.

10 All interest rate data is obtained from Primark Datastream.

11 Dividend information is obtained from Primark Datastream.

Page 22

20

Table 1 shows the mean credit spread expressed in basis points over the relevant period12.

Where the issuer has straight debt in the market, the credit spread is calculated on the basis of

the traded yield spread. Otherwise, it is calculated on the basis of credit spread indices, e.g.

the Bloomberg Fair Market Curves and UBS Credit Indices, according to the characteristics

of the sector in the relevant rating category.

Results

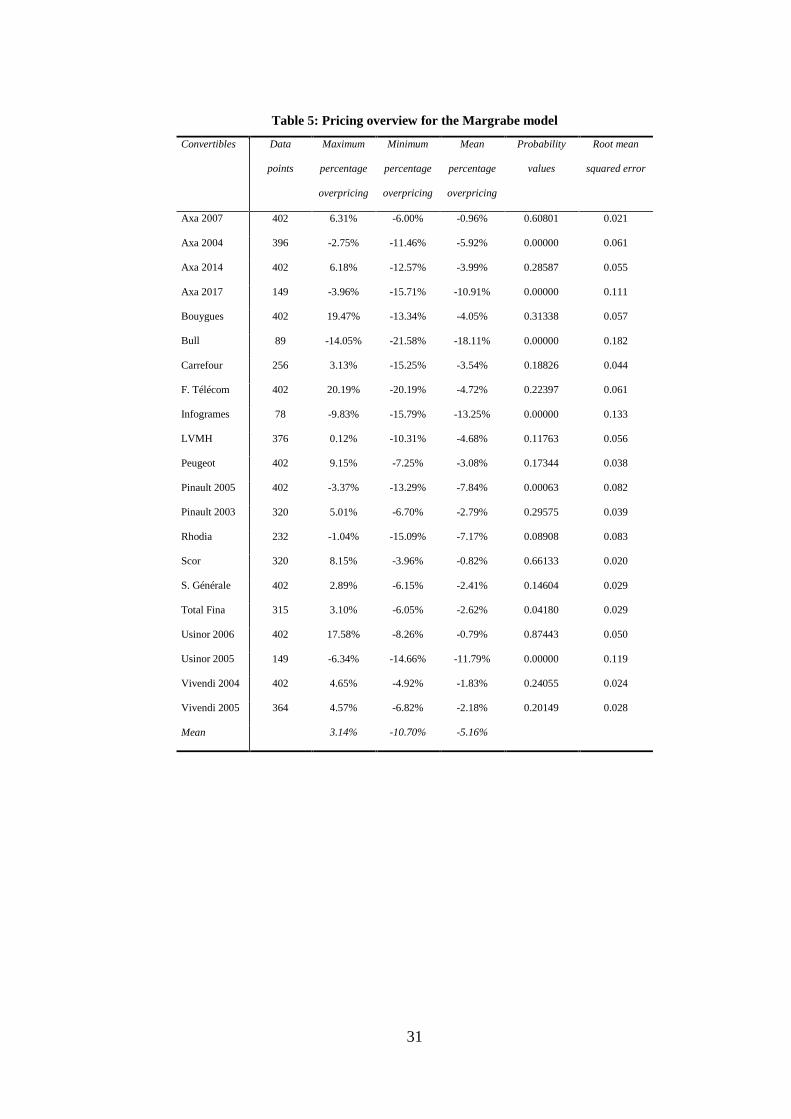

The observed convertible bond prices on the French market are compared with theoretical

prices obtained with three convertible bond pricing models. The main results of the three

implemented models are summarized13 in Table 4, Table 5, and Table 6. In analogy to the

methodology used by Sterk (1982) and others to test option pricing formulas, the tables

provide data about the maximum, minimum and mean percentage overpricing of each issue.

The mean percentage overpricing is presented for each convertible bond as an average of the

deviation between the theoretical and observed price for each observation. A negative value

indicates an underpricing, i.e. the theoretical value is above the observed market price.

Additionally, the probability values of a test for the null hypothesis of a mean overpricing of

zero are presented for each convertible. The last column shows the root mean squared error of

the relative mispricing. The RMSE shows the non-central standard deviation of the relative

deviations of model prices from market prices. It can be interpreted as a measure for the

pricing fit of the model relative to market prices.

With all three models, we observe on average substantially lower market prices than

theoretical prices. We obtain the largest underpricing for the component model (-8.74%),

12 We thank Rupert Kenna, credit analyst at UBS Warburg in London, for providing the daily credit spread time series.

13 Pricing results for each individual convertible bond are graphically displayed in the appendix.

Page 23

21

followed by the Margrabe model (-5.60%). The binomial-tree model is closest to the market

prices, but exhibits an average underpricing of -2.78%. This underpricing prevails even

though we value the convertible bond conservatively by assuming maximum dilution and

setting the safety premium to zero. For almost all convertibles, the binomial-tree model

produces the lowest theoretical price, followed by the Margrabe and the component model.

The only exception is the LVMH-convertible, where the overvaluation detected by the

Margrabe model is slightly higher than that of the binomial-tree model.

The binomial-tree model is the only model that in the entire sample detects cases of

overpricing. Among those five cases, the overpricing ranges from 3.78% (Usinor 2006) to

0.47% (Vivendi 2005). However, the mispricing is not significantly different from zero at a

five percent level. In contrast, sixteen convertible bonds have a mean percentage

underpricing. The significance test indicates that the mean price deviation of five of them is

significantly different from zero. Even though the overall theoretical pricing of the binomial-

tree model is close to the market data, the maximum and minimum percentage overpricing for

each convertible that occurred during the observation period often is very different. In some

cases, this may be caused by data outliers, which have not been removed in this study.

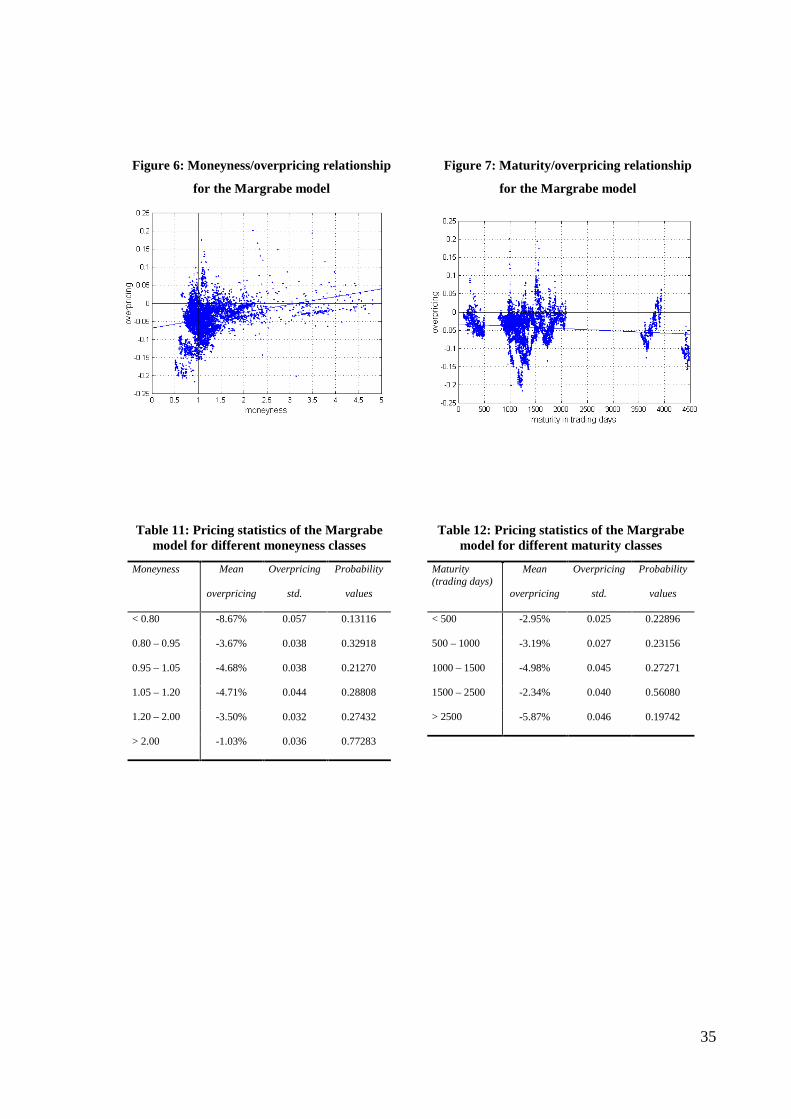

Prices calculated with the Margrabe model are substantially higher than both market prices

and theoretical binomial-tree prices, representing an underpricing for each convertible bond.

This can be explained by the fact that the model does not account for the call feature, which is

present in all but one of the examined convertible bonds. Callability reduces the stock-driven

upward-potential and thus has a negative impact on convertible prices.

For the component model, the mean percentage deviations from market prices are

significantly different from zero for 16 of the 21 convertible bonds, all of which are

overpriced by the model. Model prices are biased upwards because of two reasons: As in the

Page 24

22

Margrabe model, callability is neglected. Second, the strike price remains constant instead of

growing at a rate equal to the difference between interest rate and coupon. This distortion is

larger the longer the maturity of the bond and the lower the coupon rate is.

The fact that convertibles can be converted before maturity of the bond is accounted for

neither by the component model nor by the Margrabe model. This effect is of opposite

direction to the omission of the call feature. For eight convertibles in our sample, the dividend

yield is higher than the coupon rate. This is of interest, because it may make early conversion

optimal in a world of continuously compounded dividend yields and coupon rates.

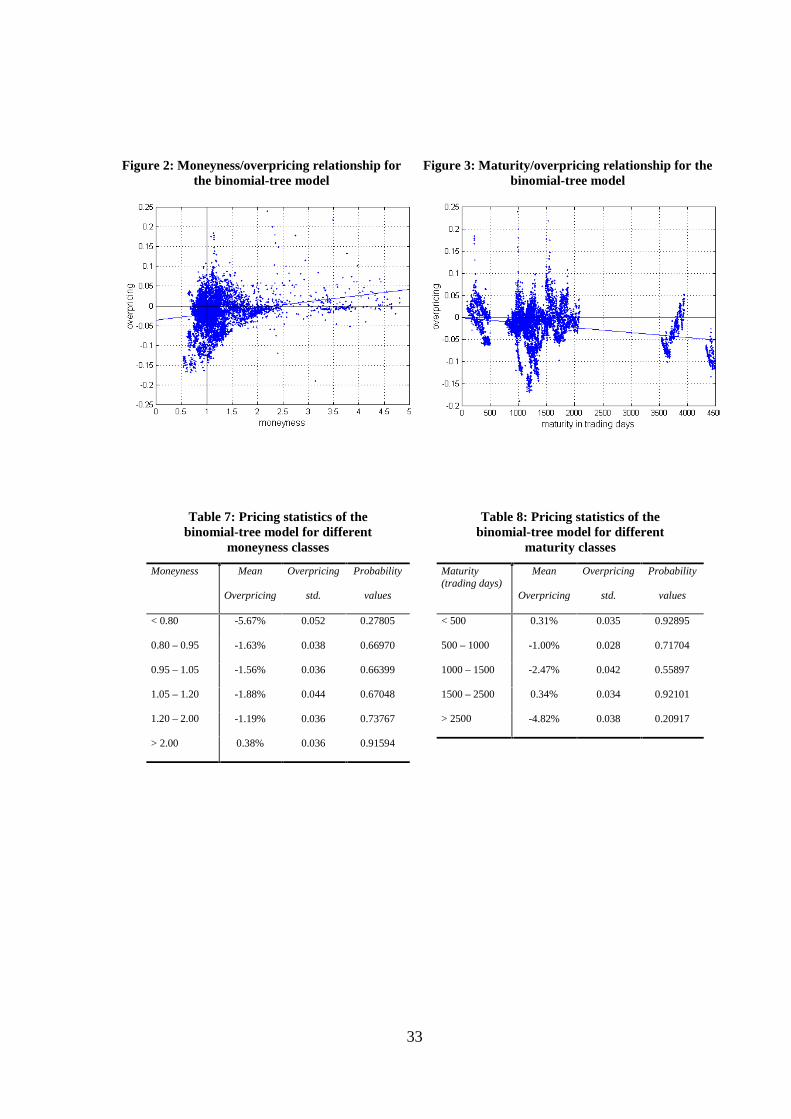

Figure 2 exhibits the overpricing of the observed market prices as detected by the binomial-

tree model plotted against the moneyness. The relationship is non-linear. The model

overprices bonds that are at-the-money and out-of-the money and underprices in-the-money

convertibles. These results are similar to those obtained by Carayannopoulos (1996). There

seems to be a slight relationship between overpricing and maturity (see Figure 3). The longer

the time to maturity, the more convertibles tend to be underpriced. However, these results rely

heavily on only two bonds (Axa 2014 and Axa 2017) that have a maturity far longer than the

others.

These results are similar for the other models. The relationship between overpricing and

moneyness is also positive. However, the relationship between overpricing and maturity is

slightly more negative for the component model. This finding is consistent with the above

mentioned fact that the component model tends to overprice bonds with long maturities and

with coupon rates below the interest rate level.

Page 25

23

Conclusion

We undertake a pricing study for the French convertible bond market. A simple component

model, a model based on exchange options, and a binomial-tree model are implemented.

Unlike the first two models, the binomial-tree model incorporates embedded options, dilution,

and credit risk. The model-generated prices are compared to the market prices of the

investigated convertible bonds using a sample of convertible bond prices of nearly 18 months

of daily data. For all three pricing models, on average, underpricing is detected. The results of

the binomial-tree model are closest to the market prices while the simple component model

has the greatest deviation. For all convertible bonds, the binomial-tree model gives the lowest

prices. Moreover, for the majority of bonds in our sample, the underpricing is not significant

for this model. A partition of the sample according to the moneyness indicates that the

underpricing is decreasing for bonds that are further in-the-money. Our findings of

underpricing, particularly for out-of-the-money bonds, are consistent with two previous

studies for the American market and anecdotal evidence from traders and other convertible

bond practitioners.

Page 26

24

References

BIS (2001), Bank for International Settlements Quarterly Review, March, pp. 71.

BLACK, F., and M. SCHOLES (1973): “The Pricing of Options and Corporate Liabilities”,

Journal of Political Economy, 81, 637-654.

BRENNAN, M.J., and E.S. SCHWARTZ (1977): “Convertible Bonds: Valuation and

Optimal Strategies for Call and Conversion”, The Journal of Finance, 32 (5), 1699-

1715.

BRENNAN, M.J., and E.S. SCHWARTZ (1980): “Analyzing Convertible Bonds”, Journal of

Financial and Quantitative Analysis, 15 (4), 907-929.

BUCHAN, J. (1997):”Convertible Bond Pricing: Theory and Evidence”, Unpublished

Dissertation, Harvard University.

BUCHAN, J. (1998):”The Pricing of Convertible Bonds with Stochastic Term Structures and

Corporate Default Risk”, Working Paper, Amos Tuck School of Business, Dartmouth

College.

CARAYANNOPOULOS, P. (1996): “Valuing Convertible Bonds under the Assumption of

Stochastic Interest Rates: An Empirical Investigation”, Quarterly Journal of Business

and Economics, 35 (3), 17-31.

COX, J.C., S.A. ROSS and M. RUBINSTEIN (1979): “Option Pricing: A simplified

Approach”, Journal of Financial Economics, 7 (3), 229-263.

HULL, J.C. (2000): Options, Futures & Other Derivatives. Prentice-Hall, Upper Saddle

River, N.Y., 4th ed.

Page 27

25

INGERSOLL, J.E. (1977a): “A Contingent Claim Valuation of Convertible Securities”,

Journal of Financial Economics, 4, 289-322.

INGERSOLL, J.E. (1977b): “An examination of corporate call policy on convertible

securities”, Journal of Finance, 32, 463-478.

KING, R. (1986): “Convertible Bond Valuation: An Empirical Test”, Journal of Financial

Research, 9 (1), 53-69.

MARGRABE, W (1978): “The Value of an Option to Exchange One Asset for Another”,

Journal of Finance, 33 (1), 177-186.

McCONNELL, J.J., and E.S. SCHWARTZ (1986): “LYON Taming”, The Journal of

Finance, 41 (3), 561-576.

STERK, W. (1982): “Tests of Two Models for Valuing Call Options on Stocks with

Dividends”, The Journal of Finance, 37 (5), 1229-1237.

SUBRAHMANYAM, M.G. (1990): “The Early Exercise Feature of American Options” in

FIGLEWSKI, S., W.L. SILBER and M.G. SUBRAHMANYAM (1990): “Financial

Options – From Theory to Practice”, Irwin, Burr Ridge, Illinois.

TSIVERIOTIS, K., and C. FERNANDES (1998): “Valuing Convertible Bonds with Credit

Risk”, The Journal of Fixed Income, 8 (3), 95-102.

Page 28

26

Figures and Tables

Figure 1: Flow chart of optimal option exercise

yes

no

yes

Does theInvestor want

to convert?

ttt Sn ⋅<Ω

Are we withinthe conversion

period?conversion

Are we withinthe call period?

[ ]KK Tt ,τ∈

Is thecallcondition

satisfied?

ttt Sn Ξ>

Does the issuerwant to call?

ttt K Θ+>Ω

Does theinvestor want to

convert?

ttt Sn Κ>

yes

no

yes

yes

yes

conversion(forced)

continuation of theconvertible bond

no

no

no

no

Earlyredemption

[ ]ΓΓ∈ Tt ,τ

A

B

C

F

E

D

Page 29

27

Table 1: Specification of the convertible bonds

Exchangeable into shares of Company Maturity Coupon Pricing points

Axa Finaxa 2007 3.00% 404

Axa Suez Lyonnaise des Eaux 2004 0.00% 397

Axa Axa 2014 2.50% 404

Axa Axa 2017 3.75% 150

Bouygues Bouygues 2006 1.70% 404

Bull Bull 2005 2.25% 90

Carrefour (Promodès) Carrefour (Promodès) 2004 2.50% 257

France Télécom France Télécom 2004 2.00% 404

Infogrames Entertainment Infogrames Entertainment 2005 1.50% 80

LVMH Financiere Agache 2004 0.00% 377

Peugeot Peugeot 2001 2.00% 404

Pinault-Printemps-Redoute Artemis 2005 1.50% 404

Pinault-Printemps-Redoute Pinault-Printemps-Redoute 2003 1.50% 321

Rhodia Aventis (Rhône-Poulenc) 2003 3.25% 234

Scor Scor 2005 1.00% 321

Société Générale Société Vinci Obligations 2003 1.50% 404

Total Fina Belgelec Finance 2004 1.50% 316

Usinor Usinor 2006 3.00% 464

Usinor Usinor 2005 3.88% 150

Vivendi Vivendi 2004 1.25% 404

Vivendi Vivendi 2005 1.50% 366

Page 30

28

Table 2: Specification of embedded options.

The “call trigger ratio” can refer to either the face value of the convertible or to the early redemption price(denoted as “redemption”). “Maximum number of convertibles” indicates the highest number of bonds issuedaccording to the offering circular (including green shoe, if present). The “green shoe” option indicates thenumber of convertible bonds that could be issued on a discretionary basis. Zero means that no green shoe waspresent.

Issuing company Initial

conversion

ratio

Final

Redemption

ratio

Callability Call

trigger

ratio

Call

trigger

basis

Maximum

number of

convertibles

“Green

shoe”

option

Finaxa 1 118.18% no - - 13‘037‘878 0

Suez Lyonnaise des Eaux 1 109.83% yes - - 54‘655‘022 0

Axa 1 139.93% yes 125.00% redemption 9‘239‘333 1‘205‘129

Axa 1 162.63% yes 125.00% redemption 7‘643‘502 996‘978

Bouygues 1 100.00% yes 115.00% redemption 1‘905‘490 152‘440

Bull 1 116.60% yes 120.00% redemption 11‘491‘752 1‘495‘752

Carrefour (Promodès) 1 100.00% yes 120.00% redemption 589‘471 0

France Télécom 10 100.00% yes 115.00% face value 2‘538‘543 250‘000

Infogrames Entertainment 1 118.23% yes 250.00% redemption 10‘282‘744 1‘341‘227

Financiere Agache 1 111.77% yes 120.00% face value 1‘724‘137 0

Peugeot 1 123.64% yes 100.00% redemption 4‘000‘000 0

Artemis 10 110.54% yes 120.00% face value 200‘000 0

Pinault-Printemps-Redoute 1 103.63% yes 130.00% redemption 4‘784‘688 382‘774

Aventis (Rhône-Poulenc) 1 100.00% yes 130.00% redemption 43‘685‘260 0

Scor 1 112.55% yes 120.00% redemption 4‘025‘000 525‘000

Société Vinci Obligations 1 100.00% yes 130.00% redemption 1‘828‘620 0

Belgelec Finance 1 100.00% yes 130.00% redemption 7‘550‘300 0

Usinor 1 110.91% yes 125.00% redemption 29‘761‘904 3‘571‘427

Usinor 1 100.00% yes 130.00% redemption 25‘000‘000 3‘000‘000

Vivendi 1 100.00% yes 115.00% redemption 6‘028‘369 709‘220

Vivendi 1 106.27% yes 115.00% redemption 11‘070‘111 1‘476‘015

Page 31

29

Table 3: Statistics of the input parameters used

Convertibles Mean of the input

volatility

Mean of the input

dividend yield

Mean credit spread

(in basis points)

Correlation

stock/bond

Axa 2007 35.85% 2.18% 45 0.260

Axa 2004 35.89% 2.19% 40 0.208

Axa 2014 35.85% 2.18% 73 0.233

Axa 2017 36.58% 2.16% 74 0.142

Bouygues 46.08% 1.00% 84 -0.022

Bull 66.05% 0.00% 300 -0.024

Carrefour 37.58% 0.97% 42 0.016

F. Télécom 46.45% 1.69% 31 0.061

Infogrames 56.16% 0.00% 300 0.020

LVMH 39.95% 1.62% 80 0.138

Peugeot 39.61% 1.89% 40 0.086

Pinault 2005 38.99% 1.29% 100 0.101

Pinault 2003 38.93% 1.29% 80 0.071

Rhodia 45.07% 4.09% 59 0.009

Scor 39.12% 5.75% 26 -0.022

S. Générale 45.04% 3.94% 50 0.071

Total Fina 39.29% 2.79% 50 -0.029

Usinor 2006 45.66% 5.46% 124 0.020

Usinor 2005 44.86% 5.46% 119 -0.033

Vivendi 2004 32.06% 1.98% 75 0.085

Vivendi 2005 32.37% 2.00% 82 0.077

Page 32

30

Table 4: Pricing overview for the binomial-tree model

“Data points” indicates the number of days for which model prices are computed. “Probability values” is a twosided test for the H0 hypothesis that model prices and observed prices are equal in the mean. The “root meansquared error” is the non-central standard deviation of the relative deviations of model prices from market prices.

Convertibles Data

points

Maximum

percentage

overpricing

Minimum

percentage

overpricing

Mean

percentage

overpricing

Probability

values

Root mean

squared error

Axa 2007 402 5.83% -5.42% -0.58% 0.72974 0.018

Axa 2004 396 4.23% -7.56% -0.56% 0.77267 0.020

Axa 2014 402 5.19% -10.08% -3.37% 0.31523 0.048

Axa 2017 149 -2.55% -13.34% -8.71% 0.00000 0.089

Bouygues 402 21.84% -9.76% -1.40% 0.68053 0.037

Bull 89 -9.75% -16.81% -14.07% 0.00000 0.142

Carrefour 256 7.99% -10.87% 1.46% 0.59718 0.031

F. Télécom 402 23.92% -18.97% -1.60% 0.66270 0.040

Infogrames 78 -8.49% -14.36% -11.72% 0.00000 0.118

LVMH 376 -0.62% -9.65% -4.76% 0.06953 0.054

Peugeot 402 18.39% -2.78% 2.46% 0.31557 0.035

Pinault 2005 402 0.00% -8.67% -3.73% 0.04404 0.042

Pinault 2003 320 5.41% -6.40% -2.39% 0.37238 0.036

Rhodia 232 0.32% -13.00% -5.40% 0.17815 0.067

Scor 320 9.88% -2.67% 0.67% 0.72626 0.020

S. Générale 402 3.74% -5.19% -1.61% 0.30344 0.022

Total Fina 315 3.64% -4.82% -1.60% 0.18626 0.020

Usinor 2006 402 17.51% -4.51% 3.78% 0.18799 0.047

Usinor 2005 149 -3.51% -11.11% -8.13% 0.00000 0.082

Vivendi 2004 402 6.64% -3.83% -0.28% 0.86665 0.017

Vivendi 2005 364 7.66% -3.72% 0.47% 0.79780 0.019

Mean 5.33% -8.34% -2.78%

Page 33

31

Table 5: Pricing overview for the Margrabe model

Convertibles Data

points

Maximum

percentage

overpricing

Minimum

percentage

overpricing

Mean

percentage

overpricing

Probability

values

Root mean

squared error

Axa 2007 402 6.31% -6.00% -0.96% 0.60801 0.021

Axa 2004 396 -2.75% -11.46% -5.92% 0.00000 0.061

Axa 2014 402 6.18% -12.57% -3.99% 0.28587 0.055

Axa 2017 149 -3.96% -15.71% -10.91% 0.00000 0.111

Bouygues 402 19.47% -13.34% -4.05% 0.31338 0.057

Bull 89 -14.05% -21.58% -18.11% 0.00000 0.182

Carrefour 256 3.13% -15.25% -3.54% 0.18826 0.044

F. Télécom 402 20.19% -20.19% -4.72% 0.22397 0.061

Infogrames 78 -9.83% -15.79% -13.25% 0.00000 0.133

LVMH 376 0.12% -10.31% -4.68% 0.11763 0.056

Peugeot 402 9.15% -7.25% -3.08% 0.17344 0.038

Pinault 2005 402 -3.37% -13.29% -7.84% 0.00063 0.082

Pinault 2003 320 5.01% -6.70% -2.79% 0.29575 0.039

Rhodia 232 -1.04% -15.09% -7.17% 0.08908 0.083

Scor 320 8.15% -3.96% -0.82% 0.66133 0.020

S. Générale 402 2.89% -6.15% -2.41% 0.14604 0.029

Total Fina 315 3.10% -6.05% -2.62% 0.04180 0.029

Usinor 2006 402 17.58% -8.26% -0.79% 0.87443 0.050

Usinor 2005 149 -6.34% -14.66% -11.79% 0.00000 0.119

Vivendi 2004 402 4.65% -4.92% -1.83% 0.24055 0.024

Vivendi 2005 364 4.57% -6.82% -2.18% 0.20149 0.028

Mean 3.14% -10.70% -5.16%

Page 34

32

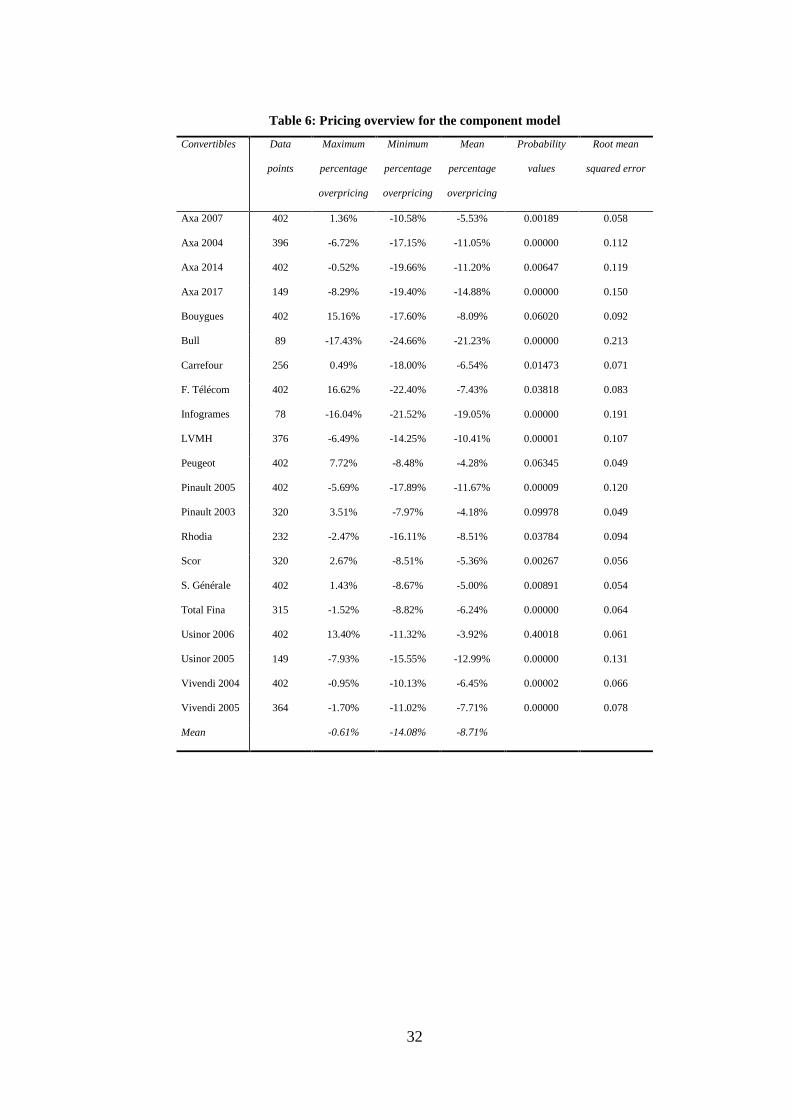

Table 6: Pricing overview for the component model

Convertibles Data

points

Maximum

percentage

overpricing

Minimum

percentage

overpricing

Mean

percentage

overpricing

Probability

values

Root mean

squared error

Axa 2007 402 1.36% -10.58% -5.53% 0.00189 0.058

Axa 2004 396 -6.72% -17.15% -11.05% 0.00000 0.112

Axa 2014 402 -0.52% -19.66% -11.20% 0.00647 0.119

Axa 2017 149 -8.29% -19.40% -14.88% 0.00000 0.150

Bouygues 402 15.16% -17.60% -8.09% 0.06020 0.092

Bull 89 -17.43% -24.66% -21.23% 0.00000 0.213

Carrefour 256 0.49% -18.00% -6.54% 0.01473 0.071

F. Télécom 402 16.62% -22.40% -7.43% 0.03818 0.083

Infogrames 78 -16.04% -21.52% -19.05% 0.00000 0.191

LVMH 376 -6.49% -14.25% -10.41% 0.00001 0.107

Peugeot 402 7.72% -8.48% -4.28% 0.06345 0.049

Pinault 2005 402 -5.69% -17.89% -11.67% 0.00009 0.120

Pinault 2003 320 3.51% -7.97% -4.18% 0.09978 0.049

Rhodia 232 -2.47% -16.11% -8.51% 0.03784 0.094

Scor 320 2.67% -8.51% -5.36% 0.00267 0.056

S. Générale 402 1.43% -8.67% -5.00% 0.00891 0.054

Total Fina 315 -1.52% -8.82% -6.24% 0.00000 0.064

Usinor 2006 402 13.40% -11.32% -3.92% 0.40018 0.061

Usinor 2005 149 -7.93% -15.55% -12.99% 0.00000 0.131

Vivendi 2004 402 -0.95% -10.13% -6.45% 0.00002 0.066

Vivendi 2005 364 -1.70% -11.02% -7.71% 0.00000 0.078

Mean -0.61% -14.08% -8.71%

Page 35

33

Figure 2: Moneyness/overpricing relationship forthe binomial-tree model

Figure 3: Maturity/overpricing relationship for thebinomial-tree model

Table 7: Pricing statistics of thebinomial-tree model for different

moneyness classes

Moneyness Mean

Overpricing

Overpricing

std.

Probability

values

< 0.80 -5.67% 0.052 0.27805

0.80 – 0.95 -1.63% 0.038 0.66970

0.95 – 1.05 -1.56% 0.036 0.66399

1.05 – 1.20 -1.88% 0.044 0.67048

1.20 – 2.00 -1.19% 0.036 0.73767

> 2.00 0.38% 0.036 0.91594

Table 8: Pricing statistics of thebinomial-tree model for different

maturity classes

Maturity(trading days)

Mean

Overpricing

Overpricing

std.

Probability

values

< 500 0.31% 0.035 0.92895

500 – 1000 -1.00% 0.028 0.71704

1000 – 1500 -2.47% 0.042 0.55897

1500 – 2500 0.34% 0.034 0.92101

> 2500 -4.82% 0.038 0.20917

Page 36

34

Figure 4: Moneyness/overpricing relationship

for the component model

Figure 5: Maturity/overpricing relationship

for the component model

Table 9: Pricing statistics of the componentmodel for different moneyness classes

Moneyness Mean

overpricing

Overpricing

std.

Probability

values

< 0.80 -10.35% 0.062 0.09389

0.80 – 0.95 -7.19% 0.038 0.05918

0.95 – 1.05 -7.94% 0.040 0.04975

1.05 – 1.20 -8.70% 0.051 0.09094

1.20 – 2.00 -8.03% 0.038 0.03423

> 2.00 -4.89% 0.035 0.16323

Table 10: Pricing statistics of the componentmodel for different maturity classes

Maturity(trading days)

Mean

overpricing

Overpricing

std.

Probability

values

< 500 -4.24% 0.024 0.07898

500 – 1000 -6.69% 0.029 0.01996

1000 – 1500 -9.02% 0.044 0.03819

1500 – 2500 -6.16% 0.040 0.12380

> 2500 -12.20% 0.040 0.00227

Page 37

35

Figure 6: Moneyness/overpricing relationship

for the Margrabe model

Figure 7: Maturity/overpricing relationship

for the Margrabe model

Table 11: Pricing statistics of the Margrabemodel for different moneyness classes

Moneyness Mean

overpricing

Overpricing

std.

Probability

values

< 0.80 -8.67% 0.057 0.13116

0.80 – 0.95 -3.67% 0.038 0.32918

0.95 – 1.05 -4.68% 0.038 0.21270

1.05 – 1.20 -4.71% 0.044 0.28808

1.20 – 2.00 -3.50% 0.032 0.27432

> 2.00 -1.03% 0.036 0.77283

Table 12: Pricing statistics of the Margrabemodel for different maturity classes

Maturity(trading days)

Mean

overpricing

Overpricing

std.

Probability

values

< 500 -2.95% 0.025 0.22896

500 – 1000 -3.19% 0.027 0.23156

1000 – 1500 -4.98% 0.045 0.27271

1500 – 2500 -2.34% 0.040 0.56080

> 2500 -5.87% 0.046 0.19742

Page 38

36

Appendix

0 50 100 150 200 250 300 350 400 45060

80

100

120

140

160

180

trading days

valu

es

pricing of the Axa 2007, 3% convertible

theoretical fair valueempirical value parity investment value

0 50 100 150 200 250 300 350 400 450-0.06

-0.04

-0.02

0

0.02

0.04

0.06

trading days

ove

rva

luat

ion

percentage overvaluation of the Axa 2007, 3% convertible

0 50 100 150 200 250 300 350 400100

110

120

130

140

150

160

170

180

190

trading days

valu

es

pricing of the Axa 2004, 0% convertible

theoretical fair valueempirical value parity investment value

0 50 100 150 200 250 300 350 400-0.08

-0.06

-0.04

-0.02

0

0.02

0.04

0.06

trading days

ove

rva

luat

ion

percentage overvaluation of the Axa 2004, 0% convertible

0 50 100 150 200 250 300 350 400 450100

110

120

130

140

150

160

170

180

190

200

trading days

valu

es

pricing of the Axa 2014, 2.5% convertible

theoretical fair valueempirical value parity investment value

0 50 100 150 200 250 300 350 400 450-0.12

-0.1

-0.08

-0.06

-0.04

-0.02

0

0.02

0.04

0.06

trading days

ove

rva

luat

ion

percentage overvaluation of the Axa 2014, 2.5% convertible

0 50 100 150120

130

140

150

160

170

180

190

200

210

220

trading days

valu

es

pricing of the Axa 2017, 3.75% convertible

theoretical fair valueempirical value parity investment value

0 50 100 150-0.14

-0.12

-0.1

-0.08

-0.06

-0.04

-0.02

trading days

ove

rva

luat

ion

percentage overvaluation of the Axa 2017, 3.75% convertible

Page 39

37

0 50 100 150 200 250 300 350 400 450100

200

300

400

500

600

700

800

900

1000

trading days

valu

espricing of the Bouygues 2006, 1.7% convertible

theoretical fair valueempirical value parity investment value

0 50 100 150 200 250 300 350 400 450-0.1

-0.05

0

0.05

0.1

0.15

0.2

0.25

trading days

ove

rva

luat

ion

percentage overvaluation of the Bouygues 2006, 1.7% convertible

0 10 20 30 40 50 60 70 80 906

8

10

12

14

16

18

20

trading days

valu

es

pricing of the Bull 2005, 2.25% convertible

theoretical fair valueempirical value parity investment value

0 10 20 30 40 50 60 70 80 90-0.17

-0.16

-0.15

-0.14

-0.13

-0.12

-0.11

-0.1

-0.09

trading days

ove

rva

luat

ion

percentage overvaluation of the Bull 2005, 2.25% convertible

0 50 100 150 200 250 300700

800

900

1000

1100

1200

1300

trading days

valu

es

pricing of the Carrefour 2004, 2.5% convertible

theoretical fair valueempirical value parity investment value

0 50 100 150 200 250 300-0.12

-0.1

-0.08

-0.06

-0.04

-0.02

0

0.02

0.04

0.06

0.08

trading days

ove

rva

luat

ion

percentage overvaluation of the Carrefour 2004, 2.5% convertible

0 50 100 150 200 250 300 350 400 450600

800

1000

1200

1400

1600

1800

2000

2200

trading days

valu

es

pricing of the France Télécom 2004, 2% convertible

theoretical fair valueempirical value parity investment value

0 50 100 150 200 250 300 350 400 450-0.2

-0.15

-0.1

-0.05

0

0.05

0.1

0.15

0.2

0.25

trading days

ove

rva

luat

ion

percentage overvaluation of the France Télécom 2004, 2% convertible

Page 40

38

0 10 20 30 40 50 60 70 8020

25

30

35

40

45

50

trading days

valu

es

pricing of the Infogrames Entertainment 2005, 1.5% convertible

theoretical fair valueempirical value parity investment value

0 10 20 30 40 50 60 70 80-0.15

-0.14

-0.13

-0.12

-0.11

-0.1

-0.09

-0.08

trading days

ove

rva

luat

ion

percentage overvaluation of the Infogrames Entertainment 2005, 1.5% convertible

0 50 100 150 200 250 300 350 400200

250

300

350

400

450

500

550

trading days

valu

es

pricing of the LVMH 2004, 0% convertible

theoretical fair valueempirical value parity investment value

0 50 100 150 200 250 300 350 400-0.1

-0.09

-0.08

-0.07

-0.06

-0.05

-0.04

-0.03

-0.02

-0.01

0

trading days

ove

rva

luat

ion

percentage overvaluation of the LVMH 2004, 0% convertible

0 50 100 150 200 250 300 350 400 450100

150

200

250

trading days

valu

es

pricing of the Peugeot 2001, 2% convertible

theoretical fair valueempirical value parity investment value

0 50 100 150 200 250 300 350 400 450-0.05

0

0.05

0.1

0.15

0.2

trading days

ove

rva

luat

ion

percentage overvaluation of the Peugeot 2001, 2% convertible

0 50 100 150 200 250 300 350 400 4501200

1400

1600

1800

2000

2200

2400

2600

2800

3000

trading days

valu

es

pricing of the Pinault-Printemps 2005, 1.5% convertible

theoretical fair valueempirical value parity investment value

0 50 100 150 200 250 300 350 400 450-0.09

-0.08

-0.07

-0.06

-0.05

-0.04

-0.03

-0.02

-0.01

0

0.01

trading days

ove

rva

luat

ion

percentage overvaluation of the Pinault-Printemps 2005, 1.5% convertible

Page 41

39

0 50 100 150 200 250 300 350140

160

180

200

220

240

260

280

300

trading days

valu

espricing of the Pinault-Printemps 2003, 1.5% convertible

theoretical fair valueempirical value parity investment value

0 50 100 150 200 250 300 350-0.08

-0.06

-0.04

-0.02

0

0.02

0.04

0.06

trading days

ove

rva

luat

ion

percentage overvaluation of the Pinault-Printemps 2003, 1.5% convertible

0 50 100 150 200 25015

20

25

30

trading days

valu

es

pricing of the Rhodia 2003, 3.25% convertible

theoretical fair valueempirical value parity investment value

0 50 100 150 200 250-0.14

-0.12

-0.1

-0.08

-0.06

-0.04

-0.02

0

0.02

trading days

ove

rva

luat

ion

percentage overvaluation of the Rhodia 2003, 3.25% convertible

0 50 100 150 200 250 300 35040

45

50

55

60

65

trading days

valu

es

pricing of the Scor 2005, 1% convertible

theoretical fair valueempirical value parity investment value

0 50 100 150 200 250 300 350-0.04

-0.02

0

0.02

0.04

0.06

0.08

0.1

trading days

ove

rva

luat

ion

percentage overvaluation of the Scor 2005, 1% convertible

0 50 100 150 200 250 300 350 400 450120

140

160

180

200

220

240

260

280

300

trading days

valu

es

pricing of the Société Générale 2003, 1.5% convertible

theoretical fair valueempirical value parity investment value

0 50 100 150 200 250 300 350 400 450-0.06

-0.05

-0.04

-0.03

-0.02

-0.01

0

0.01

0.02

0.03

0.04

trading days

ove

rva

luat

ion

percentage overvaluation of the Société Générale 2003, 1.5% convertible

Page 42

40

0 50 100 150 200 250 300 350110

120

130

140

150

160

170

180

190

200

trading days

valu

espricing of the Total Fina 2004, 1.5% convertible

theoretical fair valueempirical value parity investment value

0 50 100 150 200 250 300 350-0.05

-0.04

-0.03

-0.02

-0.01

0

0.01

0.02

0.03

0.04

trading days

ove

rva

luat

ion

percentage overvaluation of the Total Fina 2004, 1.5% convertible

0 50 100 150 200 250 300 350 400 45010

12

14

16

18

20

22

trading days

valu

es

pricing of the Usinor 2006, 3% convertible

theoretical fair valueempirical value parity investment value

0 50 100 150 200 250 300 350 400 450-0.05

0

0.05

0.1

0.15

0.2

trading days

ove

rva

luat

ion

percentage overvaluation of the Usinor 2006, 3% convertible

0 50 100 15010

12

14

16

18

20

22

24

trading days

valu

es

pricing of the Usinor 2005, 3.875% convertible

theoretical fair valueempirical value parity investment value

0 50 100 150-0.12

-0.11

-0.1

-0.09

-0.08

-0.07

-0.06

-0.05

-0.04

-0.03

trading days

ove

rva

luat

ion

percentage overvaluation of the Usinor 2005, 3.875% convertible

0 50 100 150 200 250 300 350 400 450150

200

250

300

350

400

450

trading days

valu

es

pricing of the Vivendi 2004, 1.25% convertible

theoretical fair valueempirical value parity investment value

0 50 100 150 200 250 300 350 400 450-0.04

-0.02

0

0.02

0.04

0.06

0.08

trading days

ove

rva

luat

ion

percentage overvaluation of the Vivendi 2004, 1.25% convertible

Page 43

41

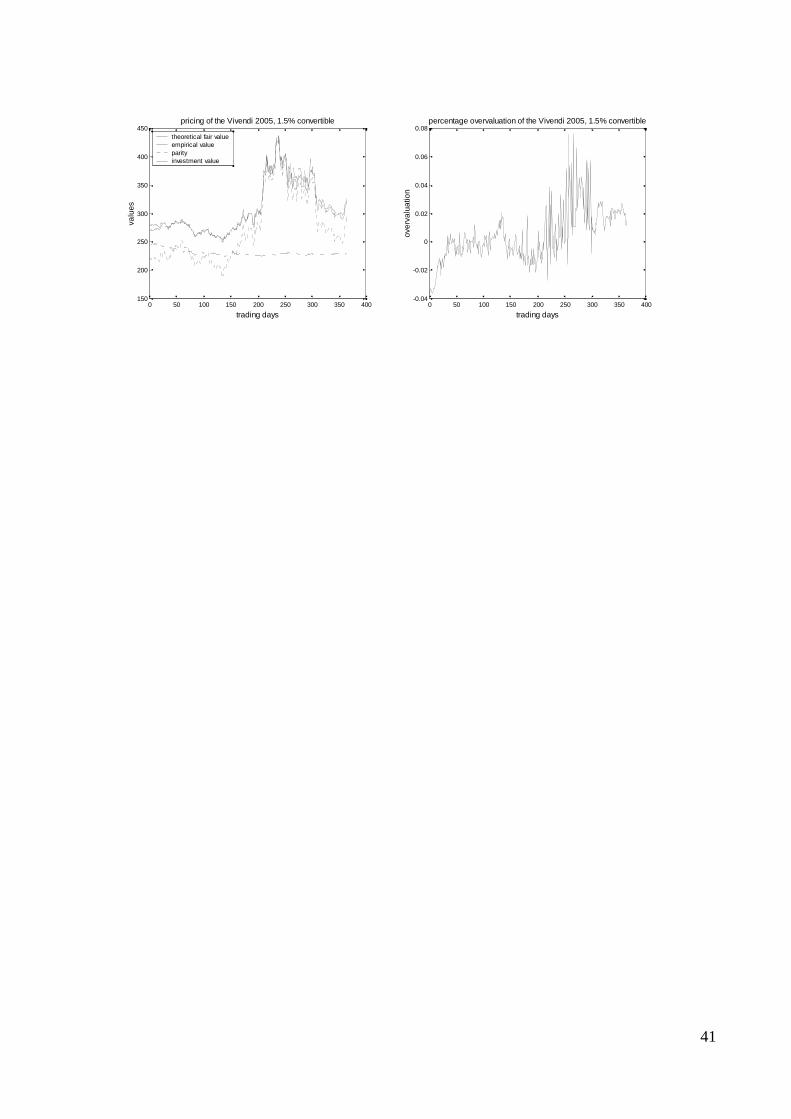

0 50 100 150 200 250 300 350 400150

200

250

300

350

400

450

trading days

valu

espricing of the Vivendi 2005, 1.5% convertible

theoretical fair valueempirical value parity investment value

0 50 100 150 200 250 300 350 400-0.04

-0.02

0

0.02

0.04

0.06

0.08

trading days

ove

rva

luat

ion

percentage overvaluation of the Vivendi 2005, 1.5% convertible