45

| Date post: | 28-Jan-2018 |

| Category: |

Documents |

| Upload: | khanyasmin |

| View: | 275 times |

| Download: | 0 times |

Investments:Investments:The ProcessThe Process

G. Kevin Spellman2/14/02

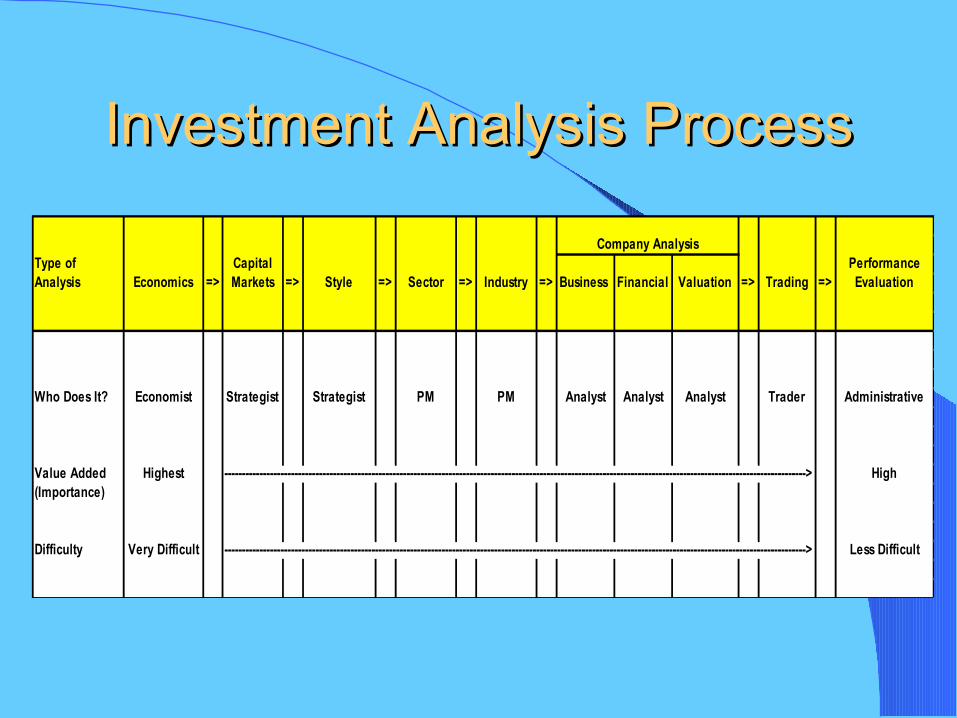

Investment Analysis ProcessInvestment Analysis Process

Type of Capital PerformanceAnalysis Economics => Markets => Style => Sector => Industry => Business Financial Valuation => Trading => Evaluation

Who Does It? Economist Strategist Strategist PM PM Analyst Analyst Analyst Trader Administrative

Value Added Highest ----------------------------------------------------------------------------------------------------------------------------------------------------------------------> High(Importance)

Difficulty Very Difficult ----------------------------------------------------------------------------------------------------------------------------------------------------------------------> Less Difficult

Company Analysis

OutlineOutline

Many roles in the investment management process

Areas overlap Left to right depicts a top-down approach to

investment management All add value and all are difficult (more

difficult and value added to the left)

Outline Cont…Outline Cont…

Today, we will focus our discussion on style analysis

Style analysis plays an important role in several areas of investment analysis– Style analysis– Sector/industry analysis– Company analysis– Trading– Performance evaluation

Investment Analysis ProcessInvestment Analysis Process

Type of Capital PerformanceAnalysis Economics => Markets => Style => Sector => Industry => Business Financial Valuation => Trading => Evaluation

Who Does It? Economist Strategist Strategist PM PM Analyst Analyst Analyst Trader Administrative

Value Added Highest ----------------------------------------------------------------------------------------------------------------------------------------------------------------------> High(Importance)

Difficulty Very Difficult ----------------------------------------------------------------------------------------------------------------------------------------------------------------------> Less Difficult

Company Analysis

EconomicsEconomics

The economic forecast is the most important forecast

Determined by the economist Major factors include: GDP, consumption,

investment, government spending, net exports, unemployment, inflation, and interest rates, etc.

We currently expect a mild recession and then a recovery in the second half of 2002, with continued low inflation

Investment Analysis ProcessInvestment Analysis Process

Type of Capital PerformanceAnalysis Economics => Markets => Style => Sector => Industry => Business Financial Valuation => Trading => Evaluation

Who Does It? Economist Strategist Strategist PM PM Analyst Analyst Analyst Trader Administrative

Value Added Highest ----------------------------------------------------------------------------------------------------------------------------------------------------------------------> High(Importance)

Difficulty Very Difficult ----------------------------------------------------------------------------------------------------------------------------------------------------------------------> Less Difficult

Company Analysis

Capital MarketsCapital Markets Economic forecast leads to the asset allocation

decision (the most important decision)– Asset classes do not move together– Asset classes are large in size

Difficult decision that can make or break performance

Determined by the Strategy team If the economy is strong and inflation is low, then

this is normally good for the stock market – Remember: P = (E1 * payout) / (r –g))

Currently over-weighted equities and real estate

-1.3%

0.1%

0.5%

1.1%

3.3%

Peak

LagLead

-2.9%-1.9%-0.7%-0.2%5 mo

-1.6%-0.6%0.8%1.3%1 moLag

-1.2%-0.2%1.2%1.7%Trough

-0.6%0.5%1.8%2.4%1 moLead

1.9%2.7%4.1%4.6%5 mo

5 mo1 mo1 mo5 mo

Capital Markets Cont…Capital Markets Cont…

Investment Analysis ProcessInvestment Analysis Process

Type of Capital PerformanceAnalysis Economics => Markets => Style => Sector => Industry => Business Financial Valuation => Trading => Evaluation

Who Does It? Economist Strategist Strategist PM PM Analyst Analyst Analyst Trader Administrative

Value Added Highest ----------------------------------------------------------------------------------------------------------------------------------------------------------------------> High(Importance)

Difficulty Very Difficult ----------------------------------------------------------------------------------------------------------------------------------------------------------------------> Less Difficult

Company Analysis

Style Style The style decision adds substantial value

– Movements in styles can differ greatly in magnitude– There are only a few styles– Style decisions impact all other parts of investment

analysis Difficult decision that can make or break

performance Determined by the Domestic Equities Strategy team Style is classified by size and valuation; although,

there are many characteristics that are applicable to investment managers/stocks

Morningstar Boxes

Value Blend GrowthLargeMid

Small

Valuation

Size

Style Cont…CharacteristicsStyle Cont…Characteristics

STRS Domestic Equities

Benchmarks----------------------- Value All Growth:: Value Blend Growth

S&P 500 Large A & I A & I A

S&P 400 Mid A I A

S&P 600 Small E P E=

S&P 1500

Specialty Funds: Technology and Health Care

Valuation/Style

Size

A = Active, E = External, I = Index, P = Passive

Style Cont…CharacteristicsStyle Cont…CharacteristicsCharacteristic Value Stock/Manager Growth Stock/Manager

Growth Rate *Low to High/ Average to *HighCyclical/Mature Defensive/Growth

Valuation of Stocks Low (i.e. P/E) High (i.e. P/E)Dividends High LowTime horizon Long Short to LongPatience of PM with Investment High LowDebt Mid to High Low to MidProfitability Low ROE High ROETrading Activities of PMs Supply Liquidity Pay up for Liquidity Management of Companies Bad to Good GoodCoverage by Sell Side Under-followed Highly followedView Cruddy to Good Glamour or Trendy

Turnaround Stories Look at Sales GrowthLook for Catalysts Look for Trends

Previous company performance Low HighPrevious stock performance Low HighMistakes of PMs Buy/Sell Too Early Extrapolate Current Growth (Too

Buy Without a Catalyst High) Too Long—Result is Pay Too Much for Inflated Expectations

Beta Low < 1 High > 1Size of Companies *Small to Large Small to *LargeExpectations for Companies Low HighIn/Out Out of Favor/Style In Favor/StyleBelief of PM Reversion to the Mean The Trend is My FriendStrategy of PMs (in Brief) Buy Low Valuation Stocks Buy High Price and

with Catalysts Earnings Momentum Stocks, Valuation Less Important

Style Cont…FactorsStyle Cont…Factors

Major factors include: inflation, interest rates, earnings growth, the phase of the economic cycle, phase of life cycle, etc.

The simple DDM captures many of these factors

P0 = (E1 * payout) / (r – g)

Interest rate moves do not affect all styles equallyGrowth stocks rise more than value securities as

rates move downExample:

– 2 stocks differ only with regard to growth rates (7% and 10%)

– RP = 6%, B = 1, E1 = $1, Payout = 40%

Style Cont…RatesStyle Cont…Rates

Style Rotation and Interest Rates

5.7 6.2 6.7 7.3 8.08.9

10.0

11.413.3

16.0

20.0

26.7

40.0

10.0

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

8.0% 7.5% 7.0% 6.5% 6.0% 5.5% 5.0%

T-Bill Rate

Pric

e

10% Growth Stock

7% Value Stock

Changes in economic growth do not affect all styles equally

Value stocks outperform growth stocks (ex tech) as the economy picks up– Why pay up for growth stocks during a recovery

when earnings growth is abundant?

Style Cont…EarningsStyle Cont…Earnings

The out-performance of growth stocks over value stocks from 1993-1998 can be explained by movements in interest rates and earnings– Both of these factors favored growth stocks

Earnings growth was slowingInflation was slowing, and interest rates were falling

Style Cont…1993-1998Style Cont…1993-1998

Style Cont…1999-TodayStyle Cont…1999-Today

1999-1Q2000 rates and earnings growth rose, but growth outperformed value (the bubble)—Why?

2Q2000-today rates have been falling but so has earnings growth and both value and growth have had their runs

Style Cont…1999-1Q2000Style Cont…1999-1Q2000

At this time, the Fed was pumping money into the system to get ready for Y2K– M * V = P * Q

P and Q were not rising rapidly, so V was falling

V falling means more people were investing versus spending—they invested in growth stocks

Style Cont…RecoveryStyle Cont…Recovery

What happens when rates fall and earnings rise? (i.e. the current environment?)

Value/small stocks tend to perform well during economic expansions even as rates fall– The “E” matters more than the “r” in the DDM

We are currently over-weighted mid-cap/growth and favor small/value during the next few quarters

Style Cont…What to Do?Style Cont…What to Do? Managers alter their styles only after they notice

events have changed (just before they change again)

Difficult to predict rotations– Must forecast many difficult to predict factors

(interest rates, economy, politics, etc.)

Unexpected events can (and do) arise (regularly)

You either win big or lose big, and the chance of winning is low

Style Cont…What to Do?Style Cont…What to Do?

Be consistent with whatever style chosen – Value and growth both “work”, but at different

times

Easier to forecast at the sector/industry level (and within the industry), where the probability of success is higher

Investment Analysis ProcessInvestment Analysis Process

Type of Capital PerformanceAnalysis Economics => Markets => Style => Sector => Industry => Business Financial Valuation => Trading => Evaluation

Who Does It? Economist Strategist Strategist PM PM Analyst Analyst Analyst Trader Administrative

Value Added Highest ----------------------------------------------------------------------------------------------------------------------------------------------------------------------> High(Importance)

Difficulty Very Difficult ----------------------------------------------------------------------------------------------------------------------------------------------------------------------> Less Difficult

Company Analysis

Sector/Industry Sector/Industry

The sector/industry decision adds value– Sectors do not move together (but generally in the same

direction)– Only 10 sectors

Driven by the economic cycle, so it is difficult to forecast

Determined by the portfolio managers The Domestic Equities department is currently

over-weighted technology; however, we took a lot of money off the table during the tech run in 4Q2001

Sector/Industry Cont…Sector/Industry Cont… Sectors can be divided by into value and

growth

Growth?Defensive?Utilities

Growth?Defensive?Telecom

CyclicalMaterials

GrowthCyclical?Info Tech

CyclicalIndustrials

Defensive/GrowthHealth Care

Growth?CyclicalFinancials

Growth?CyclicalEnergy

DefensiveCons Staples

Growth?CyclicalCons Discretionary

GrowthValueSector

Investment Analysis ProcessInvestment Analysis Process

Type of Capital PerformanceAnalysis Economics => Markets => Style => Sector => Industry => Business Financial Valuation => Trading => Evaluation

Who Does It? Economist Strategist Strategist PM PM Analyst Analyst Analyst Trader Administrative

Value Added Highest ----------------------------------------------------------------------------------------------------------------------------------------------------------------------> High(Importance)

Difficulty Very Difficult ----------------------------------------------------------------------------------------------------------------------------------------------------------------------> Less Difficult

Company Analysis

Company AnalysisCompany Analysis

Company analysis adds less value than other types of analysis (on an individual basis) – Stocks in an industry generally move in the same

direction– Many stocks in a portfolio

Determined by the analysts Must compare business, financial and valuation

fundamentals of one company to another firm in the same industry

Co Analysis Cont…Co Analysis Cont… Business analysis:

– Compare/contrast strategy, products, management, phase of life cycle, etc.

Financial analysis: – Utilize history to project the future – Can the firm finance the business plan? – A lot of room for manipulation (cash flow is best)

Valuation: – The art and science of a recommendation– To determine whether the business and financial

fundamentals are appropriately priced into the stock

Co Analysis Cont…CharacterCo Analysis Cont…CharacterCharacteristic Value Stock/Manager Growth Stock/Manager

Growth Rate *Low to High/ Average to *HighCyclical/Mature Defensive/Growth

Valuation of Stocks Low (i.e. P/E) High (i.e. P/E)Dividends High LowTime horizon Long Short to LongPatience of PM with Investment High LowDebt Mid to High Low to MidProfitability Low ROE High ROETrading Activities of PMs Supply Liquidity Pay up for Liquidity Management of Companies Bad to Good GoodCoverage by Sell Side Under-followed Highly followedView Cruddy to Good Glamour or Trendy

Turnaround Stories Look at Sales GrowthLook for Catalysts Look for Trends

Previous company performance Low HighPrevious stock performance Low HighMistakes of PMs Buy/Sell Too Early Extrapolate Current Growth (Too

Buy Without a Catalyst High) Too Long—Result is Pay Too Much for Inflated Expectations

Beta Low < 1 High > 1Size of Companies *Small to Large Small to *LargeExpectations for Companies Low HighIn/Out Out of Favor/Style In Favor/StyleBelief of PM Reversion to the Mean The Trend is My FriendStrategy of PMs (in Brief) Buy Low Valuation Stocks Buy High Price and

with Catalysts Earnings Momentum Stocks, Valuation Less Important

Co Analysis Cont…BusinessCo Analysis Cont…BusinessMethod of Analysis

Sustained Competitive Advantage (SCA) Value Manager/Stock Growth Manager/Stock

General Information

Corporate Strategy Focus, Differentiation, Low Costs Worse Better

Life Cycle Focus, Differentiation, Low Costs Stable/Decline Pioneer/Growth

Quality of Company Focus, Differentiation, Low Costs Worse Better

Financial Summary Focus, Differentiation, Low Costs Worse Better

Products and Markets Focus Less Important More Important

Production and Distribution Low Cost More Important Less Important

Competition Differentiation More Less

Other Topics

Research and Development Focus, Low Cost, Differentiation Less Important More Important

Foreign Sales and Earnings Focus Important Important

Government Regulation Focus, Differentiation, Low Costs More Likely Less Likely

Personnel Low Cost Unions?/Incentives Incentives

Properties Low Cost More Important Less Important

Management Focus, Differentiation, Low Costs Worse Better

Focus = an example is a firm selecting a narrow customer base that is underserved by the industry.

Differentiation = does the firm offer something that is unique?

Low Costs = is the firm's cost of producing its goods/services lower than the competition?

Co Analysis Cont…FinancialCo Analysis Cont…Financial

Characteristic Value Manager/Stock Growth Manager/Stock

Margins * Lower Higher

Asset Utilization * Lower Higher

Interest Burden * Higher Lower

Financial Leverage * Higher Lower

Tax Effect = ? ?

ROE * Lower Higher

Retention = Lower Higher

Growth Lower Higher

Co Analysis Cont…ValuationCo Analysis Cont…Valuation

Expectation (i.e. growth) and valuation (i.e. value) factors work

These factors work at different times and in different sectors of the market

Time

+391na+459+389na+314+504+3961963-8/99

+484+377+127-262+41+149-326-2411994-8/99

+428+357+415+254+257+154+291+2101978-8/99

Price MoEPS Rev

FCF/PCF/PEst E/PT4Q E/PP/SP/BYear

Co Analysis Co Analysis ContCont… Valuation… Valuation Sectors—value/growth factors for value/

growth sectors

+740+274+1137+1662+526+8+1614+812Commodities

+213+711-1139-809+463+503-1493-1914Health

Care

-1948-348+237+541-292-314+1361+2067Energy

+97+948+1837+1264+213+1034+331+1175Technology

+12-132+1094+994+113+874+832+535Capit Equip

Price Mo

EPS Rev

FCF/PCF/PEst E/PT4Q E/PP/SP/BSector

1994-8/99

Investment Analysis ProcessInvestment Analysis Process

Type of Capital PerformanceAnalysis Economics => Markets => Style => Sector => Industry => Business Financial Valuation => Trading => Evaluation

Who Does It? Economist Strategist Strategist PM PM Analyst Analyst Analyst Trader Administrative

Value Added Highest ----------------------------------------------------------------------------------------------------------------------------------------------------------------------> High(Importance)

Difficulty Very Difficult ----------------------------------------------------------------------------------------------------------------------------------------------------------------------> Less Difficult

Company Analysis

TradingTrading Trading is an important component of the

investment process– Average round-trip cost is over 2%– Many of the costs are invisible

Trading is performed by the traders Keys

– Communication/networking– Technical analysis (e.g. price momentum and volume

—growth factors)

Investment Analysis ProcessInvestment Analysis Process

Type of Capital PerformanceAnalysis Economics => Markets => Style => Sector => Industry => Business Financial Valuation => Trading => Evaluation

Who Does It? Economist Strategist Strategist PM PM Analyst Analyst Analyst Trader Administrative

Value Added Highest ----------------------------------------------------------------------------------------------------------------------------------------------------------------------> High(Importance)

Difficulty Very Difficult ----------------------------------------------------------------------------------------------------------------------------------------------------------------------> Less Difficult

Company Analysis

Performance Evaluation Performance Evaluation

Performance evaluation has value (knowing how you are doing can prompt you to make decisions)

Performance evaluation is performed by the back office (with the great help of the ITS staff)

Performance evaluation can take place at the asset level, style level, portfolio level, sector/industry level, company (i.e. analyst) level, and execution level

Investment Analysis ProcessInvestment Analysis Process

Type of Capital PerformanceAnalysis Economics => Markets => Style => Sector => Industry => Business Financial Valuation => Trading => Evaluation

Who Does It? Economist Strategist Strategist PM PM Analyst Analyst Analyst Trader Administrative

Value Added Highest ----------------------------------------------------------------------------------------------------------------------------------------------------------------------> High(Importance)

Difficulty Very Difficult ----------------------------------------------------------------------------------------------------------------------------------------------------------------------> Less Difficult

Company Analysis