47

© 2015 Winston & Strawn LLP Recent Trends and Legal Developments You Should Consider in 2015: Part II – Securities & Corporate Governance February 24, 2015

| Date post: | 16-Jul-2015 |

| Category: |

Law |

| Upload: | winston-strawn |

| View: | 110 times |

| Download: | 0 times |

© 2015 Winston & Strawn LLP

Recent Trends and Legal Developments You Should Consider in 2015: Part II – Securities

& Corporate Governance

February 24, 2015

© 2015 Winston & Strawn LLP

Today’s Speakers

Christina Roupas Karen A. Weber

Partner, Securities/ Corporate Governance Chicago +1 (312) 558-8794 [email protected]

Associate, Securities/ Corporate Governance Chicago +1 (312) 558-3722 [email protected]

© 2015 Winston & Strawn LLP

Agenda

• Recent Trends in Shareholder Proposals

• Recent Changes in Debt Tender Offer Rules

• Litigation-Related Bylaws

• Public Companies and Social Media

• Investors Activism Update

3

© 2015 Winston & Strawn LLP

Recent Trends in Shareholder Proposals

© 2015 Winston & Strawn LLP

Recent Trends in Shareholder Proposals - Background

• Rule 14a-8 under the Securities and Exchange Act of 1934, as amended, allows shareholders to include proposals in a company’s proxy statement

• Adopted in 1942 to allow shareholders to have a voice in the major policy decisions of companies in which they have made an equity investment

• Process • Proposal received not less than 120 calendar days before the date on which the company

released its definitive proxy statement in the prior year

• Proposal and supporting statement must be less than 500 words

• Eligibility:

• At least 1% or $2,000 in the company’s securities for at least one year

• Intent to hold such securities through the date of the shareholders’ meeting

• Only one proposal per meeting per shareholder

• Defect Notice

• Company must provide written notice of defect within 14 calendar days of receipt and provide 14 calendar days to cure

5

© 2015 Winston & Strawn LLP

Recent Trends in Shareholder Proposals - Background

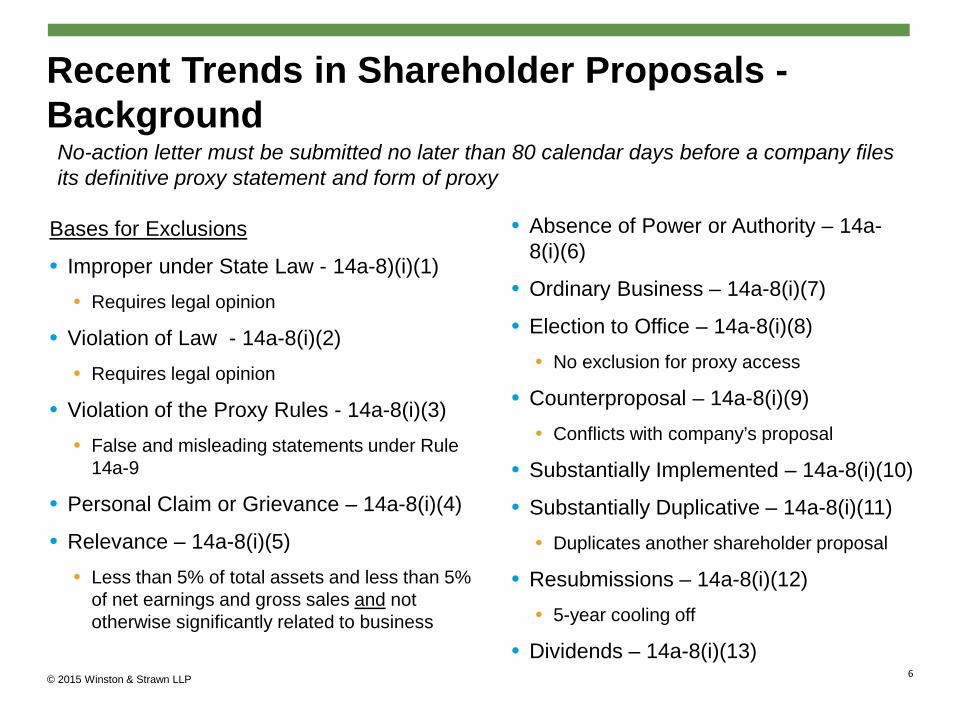

Bases for Exclusions

• Improper under State Law - 14a-8)(i)(1) • Requires legal opinion

• Violation of Law - 14a-8(i)(2) • Requires legal opinion

• Violation of the Proxy Rules - 14a-8(i)(3) • False and misleading statements under Rule

14a-9

• Personal Claim or Grievance – 14a-8(i)(4)

• Relevance – 14a-8(i)(5) • Less than 5% of total assets and less than 5%

of net earnings and gross sales and not otherwise significantly related to business

6

• Absence of Power or Authority – 14a-8(i)(6)

• Ordinary Business – 14a-8(i)(7)

• Election to Office – 14a-8(i)(8) • No exclusion for proxy access

• Counterproposal – 14a-8(i)(9) • Conflicts with company’s proposal

• Substantially Implemented – 14a-8(i)(10)

• Substantially Duplicative – 14a-8(i)(11) • Duplicates another shareholder proposal

• Resubmissions – 14a-8(i)(12) • 5-year cooling off

• Dividends – 14a-8(i)(13)

No-action letter must be submitted no later than 80 calendar days before a company files its definitive proxy statement and form of proxy

© 2015 Winston & Strawn LLP

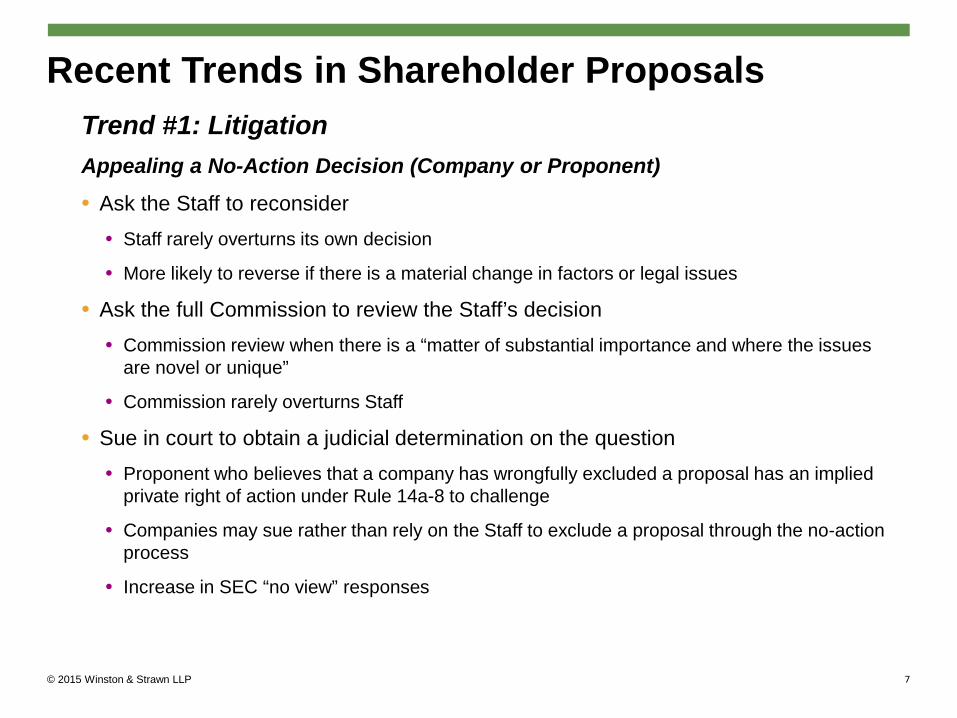

Recent Trends in Shareholder Proposals Trend #1: Litigation Appealing a No-Action Decision (Company or Proponent)

• Ask the Staff to reconsider • Staff rarely overturns its own decision

• More likely to reverse if there is a material change in factors or legal issues

• Ask the full Commission to review the Staff’s decision • Commission review when there is a “matter of substantial importance and where the issues

are novel or unique”

• Commission rarely overturns Staff

• Sue in court to obtain a judicial determination on the question • Proponent who believes that a company has wrongfully excluded a proposal has an implied

private right of action under Rule 14a-8 to challenge

• Companies may sue rather than rely on the Staff to exclude a proposal through the no-action process

• Increase in SEC “no view” responses

7

© 2015 Winston & Strawn LLP

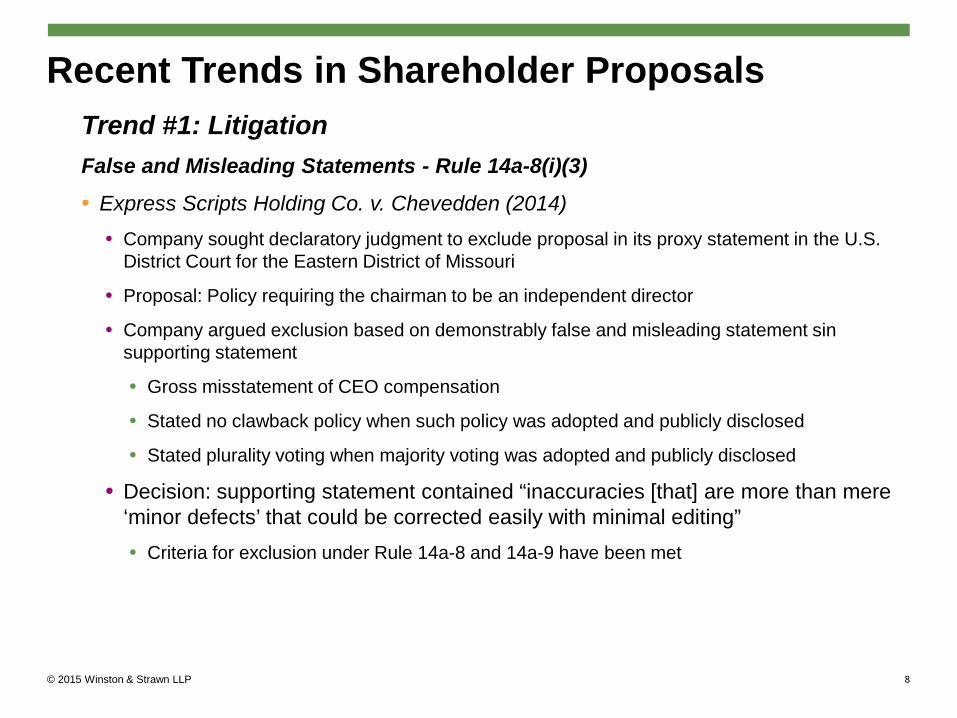

Recent Trends in Shareholder Proposals Trend #1: Litigation False and Misleading Statements - Rule 14a-8(i)(3)

• Express Scripts Holding Co. v. Chevedden (2014) • Company sought declaratory judgment to exclude proposal in its proxy statement in the U.S.

District Court for the Eastern District of Missouri

• Proposal: Policy requiring the chairman to be an independent director

• Company argued exclusion based on demonstrably false and misleading statement sin supporting statement

• Gross misstatement of CEO compensation

• Stated no clawback policy when such policy was adopted and publicly disclosed

• Stated plurality voting when majority voting was adopted and publicly disclosed

• Decision: supporting statement contained “inaccuracies [that] are more than mere ‘minor defects’ that could be corrected easily with minimal editing” • Criteria for exclusion under Rule 14a-8 and 14a-9 have been met

8

© 2015 Winston & Strawn LLP

Recent Trends in Shareholder Proposals Trend #1: Litigation Ordinary Business Matters - Rule 14a-8(i)(7)

• Trinity Wall Street v. Wal-Mart Stores, Inc. (2014) • Proposal: Amend NCGC Charter so that NCGC would oversee the “formulation and

implementation of, and the public reporting of the formulation and implementation of, policies and standards that determine whether or not [Wal-Mart] should sell a product that 1) endangers public safety and well-being; 2) has the substantial potential to impair the reputation of [Wal-Mart] and/or 3) would reasonably be considered by many offensive to the family and community values integral to [Wal-Mart]’s promotion of its brand”

• SEC granted no-action relief to Wal-Mart under the ordinary business exception • Staff did not find that proposal addressed a “significant social policy issue”

• Proponent filed suit in the District of Delaware seeking injunctive relief • Proposal was not excludable under the ordinary business exception

• Proposal raised a significant policy issue

• Court granted proponent injunctive relief and enjoined Wal-Mart from relying on the ordinary business exception to exclude the same proposal from its 2015 annual meeting

• Court afforded SEC’s no-action letter less deference than in prior decisions – “undisputed that the final determination as to the applicability of the ordinary business exception is for the [c]ourt alone to make”

9

© 2015 Winston & Strawn LLP

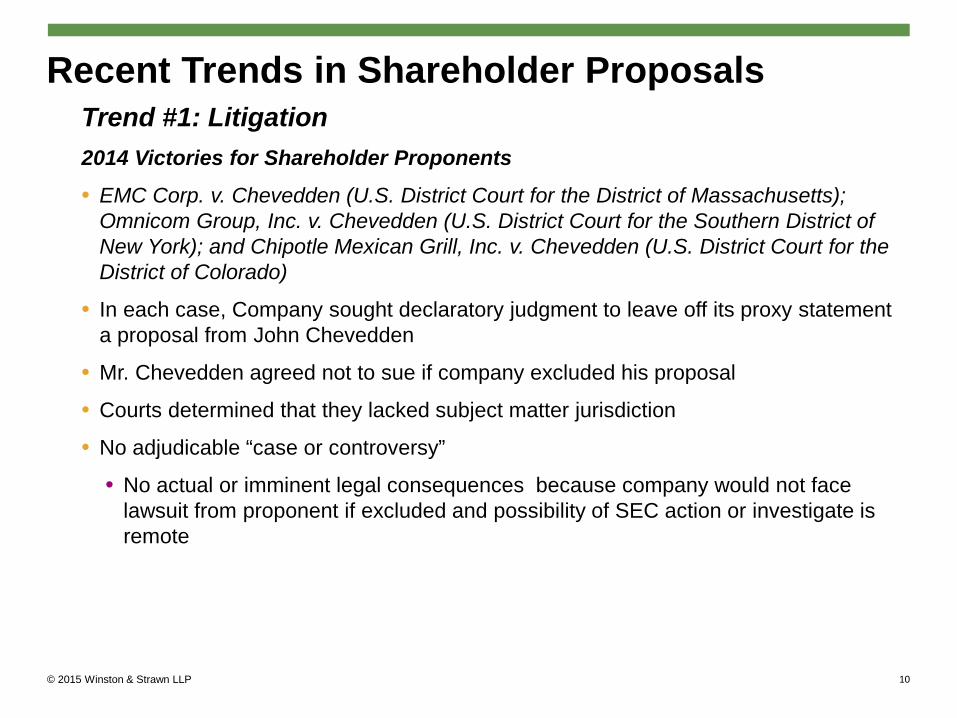

Recent Trends in Shareholder Proposals Trend #1: Litigation 2014 Victories for Shareholder Proponents

• EMC Corp. v. Chevedden (U.S. District Court for the District of Massachusetts); Omnicom Group, Inc. v. Chevedden (U.S. District Court for the Southern District of New York); and Chipotle Mexican Grill, Inc. v. Chevedden (U.S. District Court for the District of Colorado)

• In each case, Company sought declaratory judgment to leave off its proxy statement a proposal from John Chevedden

• Mr. Chevedden agreed not to sue if company excluded his proposal

• Courts determined that they lacked subject matter jurisdiction

• No adjudicable “case or controversy”

• No actual or imminent legal consequences because company would not face lawsuit from proponent if excluded and possibility of SEC action or investigate is remote

10

© 2015 Winston & Strawn LLP

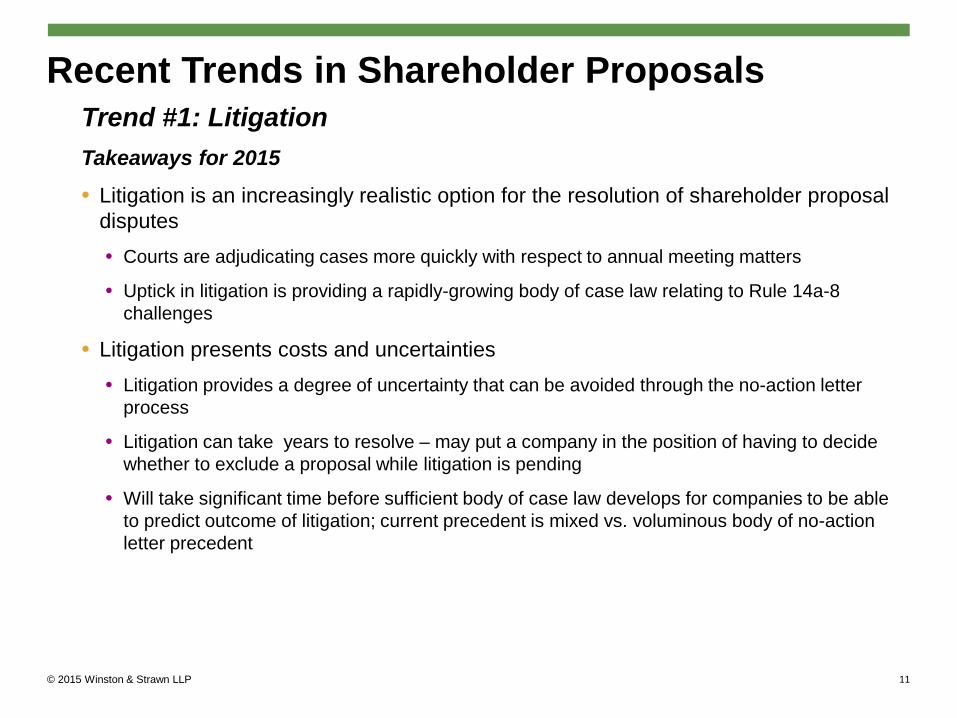

Recent Trends in Shareholder Proposals Trend #1: Litigation Takeaways for 2015

• Litigation is an increasingly realistic option for the resolution of shareholder proposal disputes • Courts are adjudicating cases more quickly with respect to annual meeting matters

• Uptick in litigation is providing a rapidly-growing body of case law relating to Rule 14a-8 challenges

• Litigation presents costs and uncertainties • Litigation provides a degree of uncertainty that can be avoided through the no-action letter

process

• Litigation can take years to resolve – may put a company in the position of having to decide whether to exclude a proposal while litigation is pending

• Will take significant time before sufficient body of case law develops for companies to be able to predict outcome of litigation; current precedent is mixed vs. voluminous body of no-action letter precedent

11

© 2015 Winston & Strawn LLP

Recent Trends in Shareholder Proposals Trend #2: Proxy Access Proposals • In 2010, the SEC adopted “proxy access” to allow eligible shareholders to include

nominees in companies’ proxy materials • Eligibility: hold at least 3% of the outstanding voting power and have continuously held such

shares for at least 3 years

• Shareholders could nominate up to 25% of the board, or one nominee, whichever is greater

• In 2011, U.S. Court of Appeals for the District of Columbia Circuit overturned proxy access

• For 2012 proxy season, SEC amended Rule 14a-8(i)(8) requiring companies to include in their proxy materials shareholder proposals addressing the director nomination process • Empowers shareholders to implement proxy access on a company-by-company basis

• In 2012 and 2013, only 39 shareholder-back proxy access proposals put into place • Only 10 proposals approved by shareholders

• 2015 – New York City Comptroller’s “2015 Boardroom Accountability Project” putting forth proxy access proposals at more than 75 public companies

• Approximately 100 companies will face proxy access proposals in 2015 12

© 2015 Winston & Strawn LLP

Recent Trends in Shareholder Proposals Trend #2: Proxy Access Proposals • Whole Foods Proxy Access Proposal

• Shareholder proposal - shareholder or group of shareholder that own at least 3% of the company’s shares continuously for 3 years can nominate up to 20% of the board

• Whole Foods proposal – single shareholder that owns at least 9% of the company’s shares continuously (amended to 5%) for 5 years can nominate the greater of (1) one director or (2) 10% of the board

• Whole Foods sought no-action relief under Rule 14a-8(i)(9) – shareholder proposal conflicts with management proposal

• December – SEC granted no-action relief to SEC to exclude shareholder proposal

• Council of Institutional Investors asked the SEC to reconsider its decision

• January – SEC withdraws its no-action letter to Whole Foods in an unprecedented move

• SEC reviewing application of Rule 14a-8(i)(9)

• SEC “will express no views” for the remainder of this proxy season on 14a-8(i)(9)

• February – Whole Foods delayed annual meeting to allow board adequate time to review and evaluate the company’s alternatives

13

© 2015 Winston & Strawn LLP

Recent Changes in Debt Tender Offer Rules

© 2015 Winston & Strawn LLP

Recent Changes in Debt Tender Offer Rules

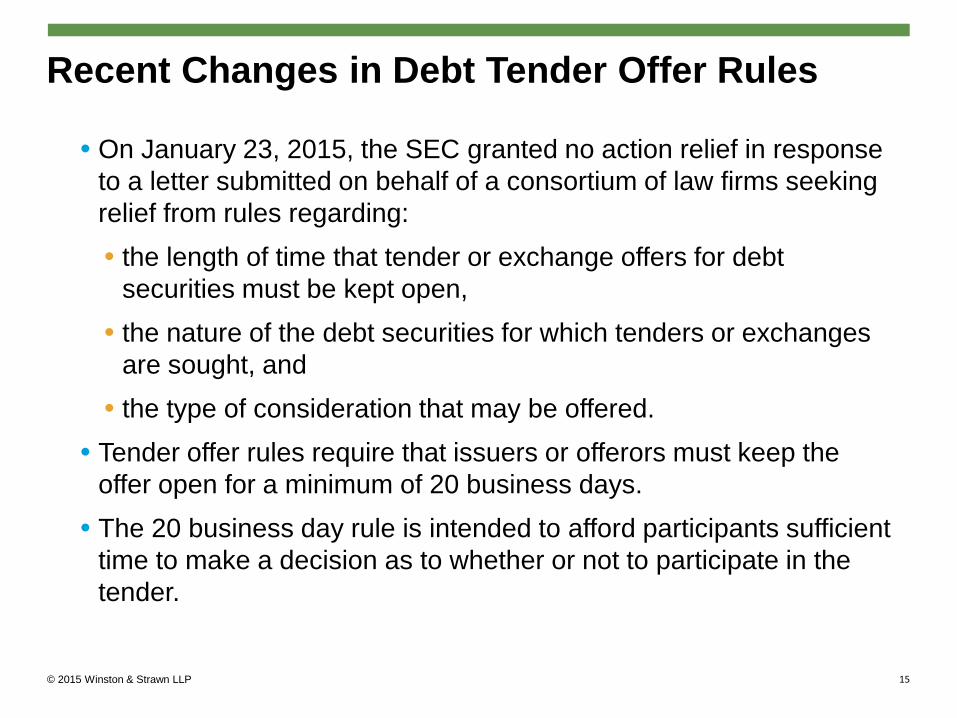

• On January 23, 2015, the SEC granted no action relief in response to a letter submitted on behalf of a consortium of law firms seeking relief from rules regarding: • the length of time that tender or exchange offers for debt

securities must be kept open, • the nature of the debt securities for which tenders or exchanges

are sought, and • the type of consideration that may be offered.

• Tender offer rules require that issuers or offerors must keep the offer open for a minimum of 20 business days.

• The 20 business day rule is intended to afford participants sufficient time to make a decision as to whether or not to participate in the tender.

15

© 2015 Winston & Strawn LLP

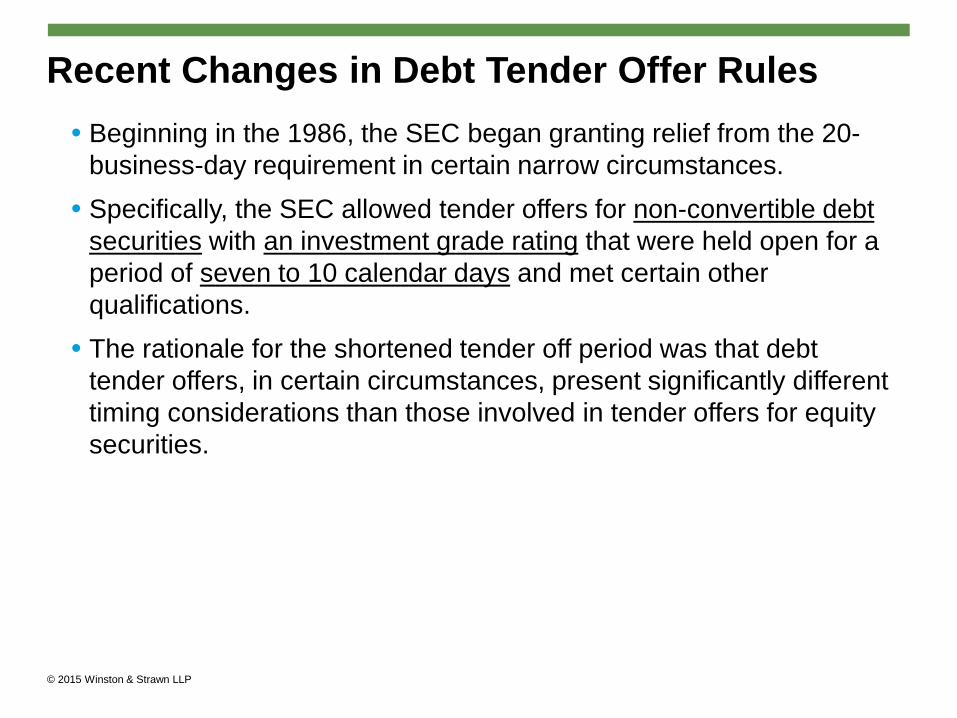

Recent Changes in Debt Tender Offer Rules • Beginning in the 1986, the SEC began granting relief from the 20-

business-day requirement in certain narrow circumstances. • Specifically, the SEC allowed tender offers for non-convertible debt

securities with an investment grade rating that were held open for a period of seven to 10 calendar days and met certain other qualifications.

• The rationale for the shortened tender off period was that debt tender offers, in certain circumstances, present significantly different timing considerations than those involved in tender offers for equity securities.

© 2015 Winston & Strawn LLP

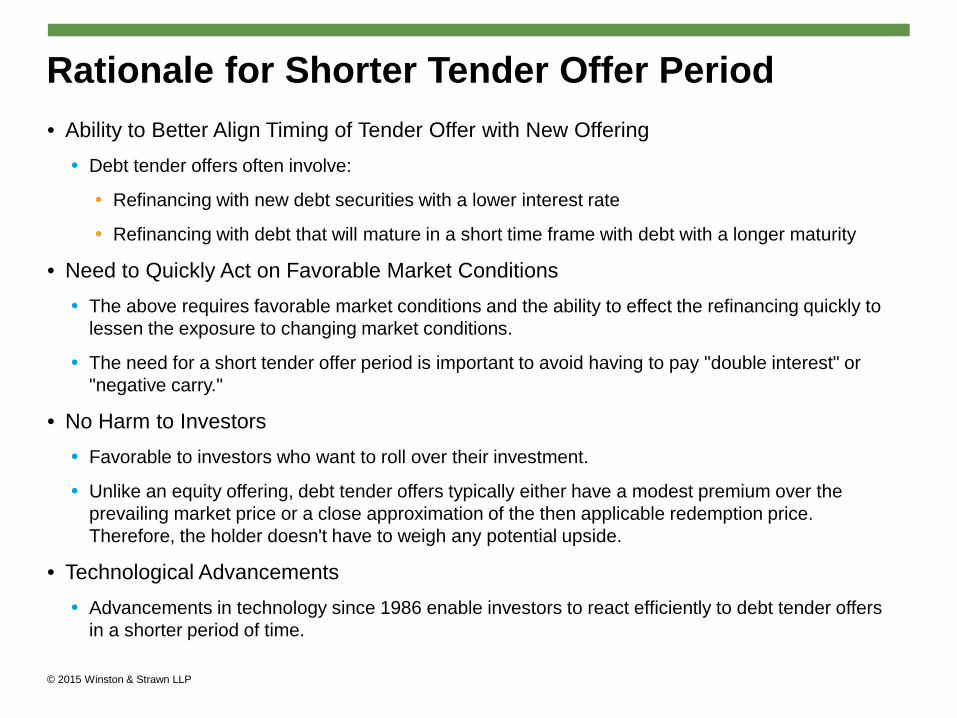

Rationale for Shorter Tender Offer Period • Ability to Better Align Timing of Tender Offer with New Offering

• Debt tender offers often involve:

• Refinancing with new debt securities with a lower interest rate

• Refinancing with debt that will mature in a short time frame with debt with a longer maturity

• Need to Quickly Act on Favorable Market Conditions • The above requires favorable market conditions and the ability to effect the refinancing quickly to

lessen the exposure to changing market conditions.

• The need for a short tender offer period is important to avoid having to pay "double interest" or "negative carry."

• No Harm to Investors • Favorable to investors who want to roll over their investment.

• Unlike an equity offering, debt tender offers typically either have a modest premium over the prevailing market price or a close approximation of the then applicable redemption price. Therefore, the holder doesn't have to weigh any potential upside.

• Technological Advancements • Advancements in technology since 1986 enable investors to react efficiently to debt tender offers

in a shorter period of time.

© 2015 Winston & Strawn LLP

SEC Relief - Debt Tender Offer Rules • The relief granted by the SEC has changed its previous position in the

following principal ways: • Change to Five Business Day Requirement: Under the new relief, offers may be

kept open for a period as short as five business days, instead of the old seven-to-10-calendar-day requirement for certain debt tender offers.

• Consideration May Consist of Qualified Debt Securities: Under the new relief, the consideration in such offers may consist of cash or “Qualified Debt Securities” or a combination of the two. • "Qualified Debt Securities" are generally defined as "non-convertible debt securities that are identical in all

material respects. . . To the debt securities that are the subject of the tender offer except for the maturity date, interest payment and record dates, redemption provisions and interest rate."

• Elimination of Investment Grade Requirement: Under the new relief, offers may be made for debt securities that are not given an investment grade rating by a nationally recognized statistical rating organization.

• Immediate Widespread Dissemination: For tender and exchange offers to qualify under the SEC’s new relief, the offeror must provide “Immediate Widespread Dissemination” of the offer materials in the manner specified by the SEC and described below; the prior practice for 10-day offers was to deliver the offer documents before midnight on the first day of the offer.

© 2015 Winston & Strawn LLP

SEC Relief - Conditions

• There are a number of detailed conditions that the issuer must follow in order to qualify for the relief granted. Key among those conditions are as follows: • All five day offers must be announced by press release through a widely

disseminated news or wire service disclosing the basic terms of the offer and an active hyperlink to the instructions or documents relating to the tender of securities.

• The press release must be issued no later than 10:00 a.m. (Eastern time) on the first business day of the offer.

• Public reporting companies must furnish the press release in a Form 8-K filed no later than 12:00 p.m. on the first business day of the offer.

• With respect to fixed spread tender offers that are tied to a benchmark such as Treasury or LIBOR, as well as exchange offers, the exact consideration offered (including the principal amount and interest rate of any Qualified Debt Securities offered) must be disclosed no later than 2:00 p.m. on the last business day of the offer.

• Also, the offer may expire as early as 5:00 p.m. on the last business day, which is significantly earlier than what prior Staff interpretations allowed, which required an offer to remain open until midnight for that day to count as a full business day.

© 2015 Winston & Strawn LLP

Offers Explicitly Precluded From Relief

• Some offers are explicitly precluded from the relief, including: • Consent Solicitation

• Partial Tender Offers

• Third-Party Tender Offers

• Waterfall Debt Tender Offers

• Offers made when there is a default or event of default under the indenture or other material credit agreement

• Offers made when the issuer is the subject of a bankruptcy or insolvency proceeding

• Offers made in anticipation of or in response to a change of control or other extraordinary transaction such as a merger or other tender offer

© 2015 Winston & Strawn LLP

Recent Changes in Debt Tender Offer Rules - Conclusion • The Staff is recognizing technological advances and has taken a step

towards updating the rules as they relate to tender and exchange offers for non-convertible debt securities.

• By applying these new procedures across the board to all non-convertible debt securities, regardless of rating, the SEC has leveled the playing field for all.

• This relief does not go without conditions mentioned earlier.

• General consensus among issuers and their counsels is that this a positive step, but they continue to seek to liberalize the rules related to debt tenders to allow the market to function in the most efficient way possible.

• The no-action letter is available in its entirety at http://www.sec.gov/divisions/corpfin/cfnoaction/2015/abbreviated-offers-debt-securities012315-sec14.pdf.

© 2015 Winston & Strawn LLP

Litigation-Related Bylaws

© 2015 Winston & Strawn LLP

Litigation-Related Bylaws

• Exclusive forum and fee-shifting bylaws are a response to the increasing volume of costly, multi-forum litigation challenging a transaction or board decision and “forum shopping”

• 2013 M&A litigation landscape* • In 2013, 94% of M&A deals over $100 million were challenged by

shareholders

• Average of 5 lawsuits per transaction for deals $100 million to $1 billion

• Average of 6.2 lawsuits for deals over $1 billion

• 62% of deal litigation was multi-jurisdictional • After Delaware Court of Chancery, most active courts:

• New York County, NY (Manhattan)

• Santa Clara County, CA (San Jose)

• Harris County, TX (Houston) * Cornerstone Research, Shareholder Litigation Involving Mergers and Acquisitions – Review of 2013 M&A Litigation, http://www.cornerstone.com/ShareholderLitigation-Involving-M-and-A-2013-Filings .

23

© 2015 Winston & Strawn LLP

Litigation-Related Bylaws – Exclusive Forum

• Board-adopted provision designating Delaware as the exclusive forum for certain shareholder suits

• Adoption through amendment to certificate of incorporation (requiring shareholder approval) or bylaws (unless prohibited by the certificate of incorporation, board only)

• 2013 – Boilmakers Local 154 Retirement Fund v. Chevron Corporation • Board adopted forum selection provision

• Chancellor Strine upheld the facial validity of the forum selection bylaw adopted by the board

• Shareholders purchasing stock were on notice that the certificate of incorporation gave the board the authority to adopt and amend bylaws unilaterally and that board-adopted bylaws were binding on shareholders

• Bylaws not intended to regulate what suits may be brought against the corporation, only where internal governance suits may be brought

24

© 2015 Winston & Strawn LLP

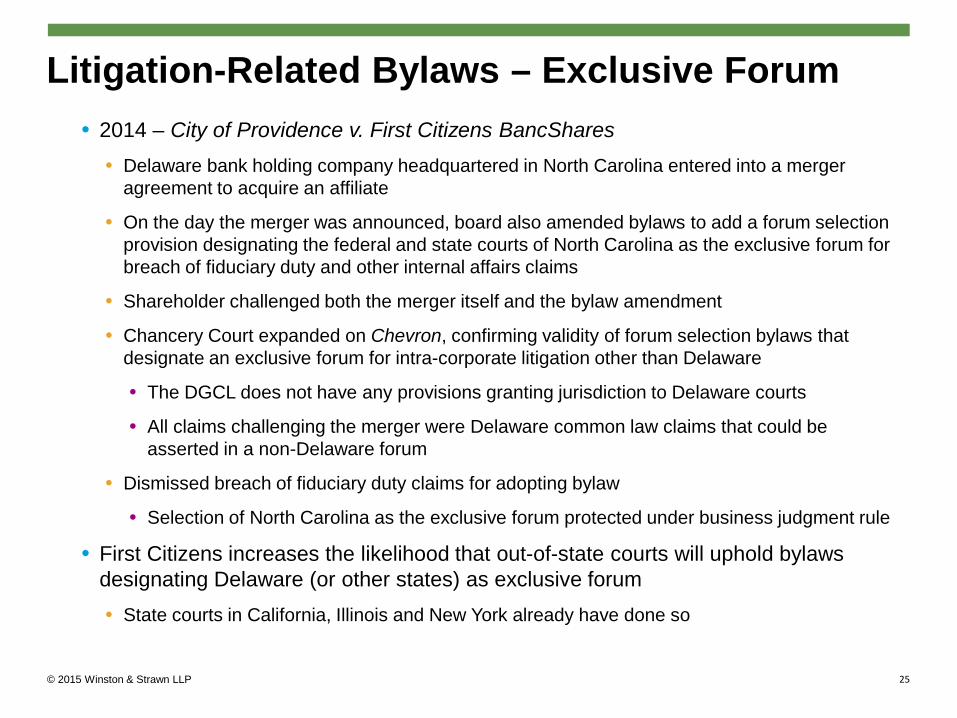

Litigation-Related Bylaws – Exclusive Forum • 2014 – City of Providence v. First Citizens BancShares

• Delaware bank holding company headquartered in North Carolina entered into a merger agreement to acquire an affiliate

• On the day the merger was announced, board also amended bylaws to add a forum selection provision designating the federal and state courts of North Carolina as the exclusive forum for breach of fiduciary duty and other internal affairs claims

• Shareholder challenged both the merger itself and the bylaw amendment

• Chancery Court expanded on Chevron, confirming validity of forum selection bylaws that designate an exclusive forum for intra-corporate litigation other than Delaware

• The DGCL does not have any provisions granting jurisdiction to Delaware courts

• All claims challenging the merger were Delaware common law claims that could be asserted in a non-Delaware forum

• Dismissed breach of fiduciary duty claims for adopting bylaw

• Selection of North Carolina as the exclusive forum protected under business judgment rule

• First Citizens increases the likelihood that out-of-state courts will uphold bylaws designating Delaware (or other states) as exclusive forum • State courts in California, Illinois and New York already have done so

25

© 2015 Winston & Strawn LLP

Litigation-Related Bylaws – Exclusive Forum

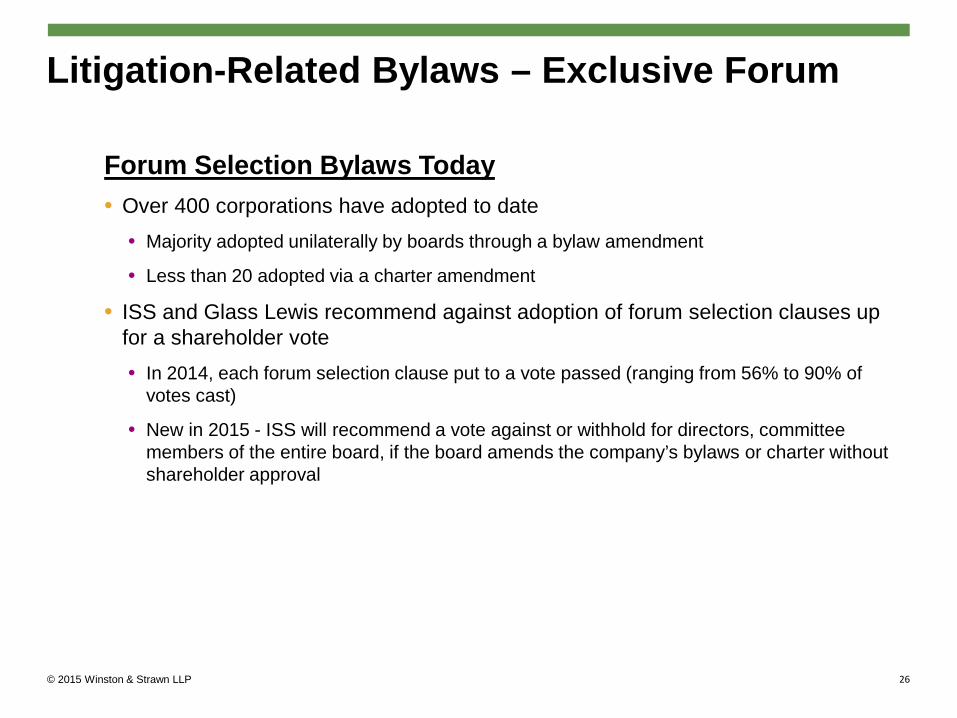

Forum Selection Bylaws Today • Over 400 corporations have adopted to date

• Majority adopted unilaterally by boards through a bylaw amendment

• Less than 20 adopted via a charter amendment

• ISS and Glass Lewis recommend against adoption of forum selection clauses up for a shareholder vote • In 2014, each forum selection clause put to a vote passed (ranging from 56% to 90% of

votes cast)

• New in 2015 - ISS will recommend a vote against or withhold for directors, committee members of the entire board, if the board amends the company’s bylaws or charter without shareholder approval

26

© 2015 Winston & Strawn LLP

Litigation-Related Bylaws – Fee Shifting

• Provision in governing documents that allows a corporation to recover legal expenses from an unsuccessful plaintiff in an intra-corporate dispute

• 2014 – ATP Tour, Inc. v. Deutscher Tennis Bund • Delaware Supreme Court upheld the facial validity of a fee-shifting bylaw of a non-stock

corporation

• Fee-shifting bylaws “may be enforceable if adopted by the appropriate corporate procedures and for a proper corporate purpose”

• Enforceability will depend on the manner in which it was adopted and the circumstances under which it was invoked

• “[T]he intent to deter litigation…is not invariably an improper purpose”

• If enforceable, fee-shifting bylaws can be enforced against losing claimants whether or not they were shareholders at the time the bylaw provision was adopted

• Robert Strougo v. First Aviation Services - Test case for fee-shifting bylaws in a stock corporation in briefing stages in Delaware

27

© 2015 Winston & Strawn LLP

Litigation-Related Bylaws – Fee-Shifting

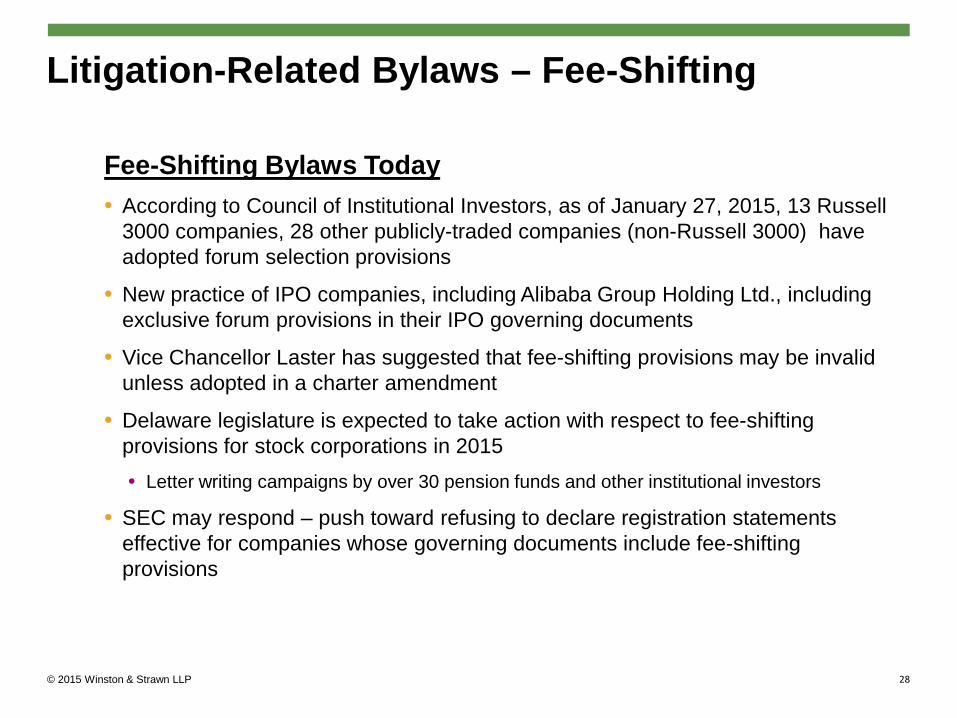

Fee-Shifting Bylaws Today • According to Council of Institutional Investors, as of January 27, 2015, 13 Russell

3000 companies, 28 other publicly-traded companies (non-Russell 3000) have adopted forum selection provisions

• New practice of IPO companies, including Alibaba Group Holding Ltd., including exclusive forum provisions in their IPO governing documents

• Vice Chancellor Laster has suggested that fee-shifting provisions may be invalid unless adopted in a charter amendment

• Delaware legislature is expected to take action with respect to fee-shifting provisions for stock corporations in 2015 • Letter writing campaigns by over 30 pension funds and other institutional investors

• SEC may respond – push toward refusing to declare registration statements effective for companies whose governing documents include fee-shifting provisions

28

© 2015 Winston & Strawn LLP

Public Companies and Social Media

© 2015 Winston & Strawn LLP

Public Companies and Social Media

• New technologies, including social media, provide companies with easy-to-use, low-cost tools that companies could be using to tell their stories better.

• However, in the age of social media, corporate communications disseminated through non-traditional outlets such as corporate blogs, Facebook and Twitter may face increased scrutiny by the SEC.

• Netflix Example: A few years ago Netflix, Inc. and its CEO, Reed Hastings, received “Wells Notices” from the Staff of the SEC indicating the Staff’s intent to recommend that the SEC bring suit against Netflix and Mr. Hastings for violations of Regulation Fair Disclosure (“Regulation FD”) and other related provisions of the Federal securities laws.

• At issue is whether disclosure that Mr. Hastings posted on his Facebook page that Netflix exceeded 1 billion hours of video streaming in a month for the first time violated prohibitions on the selective disclosure of material non-public information.

31

© 2015 Winston & Strawn LLP

SEC Approves Use of Company Website for Purposes of Regulation FD • In 2008, in light of the development and proliferation of company websites and an

expectation that continued technological advances would further enhance the quality of, and speed with which, information would be delivered and available to investors and the market generally, the SEC issued interpretive guidance that, among other things, provided guidance on when information posted on a company website would be considered “public” for purposes of satisfying Regulation FD.

• The guidance requires companies evaluating whether information posted on a company website is “public” to consider whether: • (1) the website is a “recognized channel of distribution;”

• (2) posting of information on the website disseminates the information in a manner making it available to the securities marketplace in general; and

• (3) there has been a reasonable waiting period for investors and the market to react to the posted information.

• As satisfaction of these conditions is somewhat subjective, many issuers have continued to use press releases and other time-tested distribution methods as their primary means of complying with Regulation FD.

© 2015 Winston & Strawn LLP

Netflix Investigation • Although no further action was taken against Netflix or its CEO, the

investigation revealed that there was some uncertainty regarding Regulation FD and the 2008 Guidance, as far as the rules applying to information released through social media are concerned.

• Rather than revise the 2008 Guidance, the SEC’s Report of Investigation into the Netflix matter was issued as an update, explaining how the existing guidance extends to social media disclosures.

• The SEC recognizes and understands that companies can and should use the Internet and other electronic communications to disseminate company information, since it promotes efficiency and transparency.

• The SEC also stated that it does “not wish to inhibit the content, form, or forum of any such disclosure, and we are mindful of placing additional compliance burdens on issuers.”

© 2015 Winston & Strawn LLP

Public Companies and Social Media

• The investigation and report presented a good opportunity to make these two points: • Issuer communications through social media channels require careful

Regulation FD analysis comparable to communications through more traditional channels; and

• The principles outlined in the 2008 Guidance — and specifically the concept that the investing public should be alerted to the channels of distribution a company will use to disseminate material information — apply with equal force to corporate disclosures made through social media channels.

© 2015 Winston & Strawn LLP

Social Media – Factors to Consider

• Before using social media as a means of communication, each company should carefully weigh the pros and cons before doing so.

• Some factors to consider include: • How much time does it take to write a blog entry of a few paragraphs or a tweet and

have it vetted before posting?

• How many investors and analysts will follow what you blog and tweet?

• How many follow-up questions might be prompted by your blogs and tweets? Once you start engaging through social media channels, the expectations of transparency in that manner increase.

• How many questions that your investors would otherwise call you about would get answered in a blog or tweet?

© 2015 Winston & Strawn LLP

Social Media – Factors to Consider

• How much value is associated with providing information to the market quickly in a crisis?

• How much will implementing a social media plan cost in terms of controls, education?

• Does your legal department and IR and corporate communications departments have a sufficiently close partnership and enough trust to pull this off?

• Do your designated spokespersons for Regulation FD purposes have the capacity to assume this role for social media communication purposes?

© 2015 Winston & Strawn LLP

Existing vs. New Content • Existing Content

• It's a non-issue to use social media to expand the distribution of information a company is already distributing via other channels (e.g. SEC filings, website updates).

• No cost

• Can be automated

• Strive for simultaneous dissemination - reasonable investor will expect the company to use that channel consistently and in a timely manner.

• Establish separate IR social media accounts rather than relying on the main corporate ones (which are cluttered with content related to marketing and customers).

© 2015 Winston & Strawn LLP

Existing vs. New Content

• New Content • From a Regulation FD standpoint, you need to regularly use and direct

people towards your social media channels as a source of information if you want to make them legally acceptable outlets for disclosure of material information. It’s not enough to blog, have a Twitter presence, etc.

• For example, Twitter includes the following in each of its earnings releases: • "Twitter has used, and intends to continue to use, its Investor Relations website (investor.twitterinc.com),

as well as certain Twitter accounts (@dickc, @twitter and @twitterIR), as means of disclosing material non-public information and for complying with its disclosure obligations under Regulation FD."

• Again, look to the SEC’s 2008 website guidance that provides nonexclusive factors for companies to consider in evaluating whether a company website (and seemingly by extension, blogs or other social media channels) is (1) a recognized channel of distribution and (2) whether the company information on such platform is “posted and accessible” - and therefore “disseminated” as required by Regulation FD.

© 2015 Winston & Strawn LLP

Common Topics on Social Media • Announcement of deals

• Interviews with company leaders

• Earnings announcements

• Product announcements

• Recap of annual shareholder meeting

• Recap of investor/analyst meeting

• Recap of earnings call

• How shareholder engagement is evolving at the company

• Filings made with the SEC

• Live-tweeting earnings calls

• Articles or blogs about the company

• Articles or blogs in which company leaders are quoted

© 2015 Winston & Strawn LLP

Social Media Conclusion • Weigh the pros and cons of using social media.

• Examine whether they are using a “recognized channel of distribution” for communicating with their investors and provide appropriate notice to investors of the specific channels a company will use.

• Identify on corporate website any social media channels a company intends to use for the dissemination of material, nonpublic information, to give investors and the markets the opportunity to subscribe, join, register or review them.

• Have a Social Media Policy • Ensure that the statements communicated via social media are consistent in

substance and tenor, accurate and not misleading, and are in conformance with Regulation FD and other applicable securities laws, including Rule 10b-5, Reg G, proxy solicitation rules, Exchange listing rules, disclosure laws and practices, including your usual "disclaimers," forward-looking statements, and your other codes and policies.

© 2015 Winston & Strawn LLP

Social Media Conclusion

• Any doubt, supplement – don't replace

• Although times are changes, most companies still use social media to supplement existing modes of communication, not replace them.

© 2015 Winston & Strawn LLP

Investor Activism Update

© 2015 Winston & Strawn LLP

Investor Activism Update

Hedge Funds and other activist investors have gained significant traction in recent years

• Increased Financial Ability - nearly $200 billion in activist hedge funds

• New funds started by individuals who previously worked for well-known successful activists • Examples include Corvex Management, launched in 2010 by Keith Meister (former protégé of

Carl Icahn) and Marcato Capital Management Fund, launched in 2010 by Mick McGuire (former protégé of Bill Ackman)

• Increased Sophistication • More nuanced approach to activism not focused solely on short-term gains

• Support from Traditional Long Equity Investors • Traditional investors view activists as bringing value to investors

• 76% of institutional investors viewed shareholder activism as positive in a 2014 survey

• Increase in Media Attention • Activists have successfully used the media as a tool to effect change

• Larger Companies More Vulnerable • Larger companies have become more exposed as a result of governance initiatives such as

elimination of classified boards and shareholder rights plans 43

© 2015 Winston & Strawn LLP

Investor Activism Update

Activist Tactics • Focus on strategic initiatives as a way to increase stock price and liquidity

• Merger with competitor

• Sale of company

• Spin-offs

• Divestitures of underperforming assets

• Stock buybacks

• Increased cash dividend or extraordinary one-time dividend

• Management changes

• Proxy contests

• Stopping pending or proposed strategic transaction

44

© 2015 Winston & Strawn LLP

Investor Activism Update

Proxy Contests • In 2014, 92 proxy contests

• Only includes fights where dissident filed proxy materials or provided public notice of an intent to solicit proxies

• Excludes companies where changes or agreements were reached prior to any public filings

• Of 182 proxy fights in 2013 and 2014, only 34% resulted in a shareholder vote • 81% of proxy fights result in a settlement or negotiated resolution involved management giving

activist at least one board seat

• ISS and Glass Lewis support activists in most campaigns by supporting some or all of a dissident’s nominees

45

© 2015 Winston & Strawn LLP

Investor Activism Update Company Action Items • Stock watch programs

• Program to monitor trading patterns in company shares

• Monitor ownership reports filed with the SEC

• Generally watch activists that play in industry or sector

• Monitor early warning signs • Be on the lookout for small gestures – letters to management, attendance on an earnings call,

etc.

• These can serve as warning signs in advance of an SEC filing that will garner more attention

• Shareholder outreach and communications plan • Ongoing communications with significant shareholders to tell the company’s story

• Provide feedback from shareholders and built relationships in the event an activist emerges

• Develop a plan to reach out to smaller investors and the analyst community

• Be aware of Regulation FD compliance

• Company responses to activists can be won with the success of a communications and investor relations plan

46

© 2015 Winston & Strawn LLP

Questions?

Christina Roupas Karen A. Weber

Partner, Securities/ Corporate Governance Chicago +1 (312) 558-8794 [email protected]

Associate, Securities/ Corporate Governance Chicago +1 (312) 558-3722 [email protected]

© 2015 Winston & Strawn LLP

Thank You