32

THE RESPONSIBLE WAY by SYCOMORE ASSET MANAGEMENT THE ULTIMATE NEC RESOLUTELY RESPONSIBLE #7

THE RESPONSIBLE WAYb y S Y C O M O R E A S S E T M A N A G E M E N T

THE ULTIMATE NEC

RESO

LUTELYRESPONSIBLE

#7

EDITORIALOur compass for navigating the energy and environmental transition

OPINIONThe Sycomore Eco Solutions fund at the genesis of NECThomas DHAINAUT

DISCOVERING SRINEC, the ultimate metric for our planet Jean-Guillaume PÉLADAN

THE SRI TWEETS

INTERVIEWSPascal CANFIN - Managing Director of World Wild Fund FranceFinance on the front line of transition

Henri POUPART-LAFARGE - CEO of AlstomOn the (rail)road to sustainable mobility

Jean-Philippe HERMINE - Director, Environmental Planning and Strategy, Renaultand CEO of Renault EnvironnementThe deep transformation in the auto industry

THE FREEDOM TO ENGAGESRI by Sycomore

SYCOMORE ASSET MANAGEMENT

OUR EDGE

PAGE 3

PAGE 4

PAGE 7

PAGE 10

PAGE 12

PAGE 25

PAGE 30

PAGE 31

3THE RESPONSIBLE WAY - NEC, THE ULTIMATE

OUR COMPASSFOR NAVIGATING THE ENERGYAND ENVIRONMENTAL TRANSITION

“If you can’t measure it, you can’t manage it”as the saying goes. As we address the energyand environmental transition - which willhappen whether we like it or not - we striveto better measure it, in order to make betterinvestments. Leveraging on the experiencegained when we developed the CEET(Contribution to the Energy and Environ-mental Transition), created in 2015 for ourpositive impact fund Sycomore Eco Solu-tions, we improved and extended the metho-dology in 2016, which then became the NetEnvironmental Contribution in 2017.

This is a new advanced metric that enablesus to measure the strategic alignment of agiven business with the energy and environ-mental transition. Using tangible data, itprovides a snapshot, at a given moment, ofthe net environmental contribution of anybusiness activity and can be aggregated atthe company, portfolio or index levels.

2018 will be Sycomore AM’s first year withthe NEC. A tool which is proving to be a use-ful compass to measure our impact and to

separate out, within our portfolios, the winners andpioneers from the green-washers or the corporate dino-saurs, struggling beneath the weight of their ecologicaldebts. I am convinced this tool will also be of great useto our clients.

We have therefore dedicated this edition of our Res-ponsible Way to the Net Environmental Contribution.We gathered insights from the CEOs of Alstom, HenriPoupart-Lafarge, and of Renault Environnement,Jean-Philippe Hermine; these companies are addres-sing the energy and environmental transition with avery clear vision and strategy. Pascal Canfin, MD ofWWF France, also argues why he believes finance ison the front line of change.

It also seemed relevant that we present our own ini-tiatives and ambitions in this fascinating and usefularea!

We wish you a pleasant read.

Laurent DELTOURCEO Sycomore AM

EDITORIAL

THE SYCOMOREECO SOLUTIONS FUNDAT THE GENESIS OF NEC

Testimony from an experienced fund ma-nager

Launched in 2015, before COP21, SycomoreEco Solutions is a responsible investment fundwith a positive environmental impact. The stra-tegy invests in listed equities and addressesinvestors who care about the impact of their in-vestments. By its very structure, the fund onlyinvests in companies that contribute signifi-cantly to the energy and environmental tran-sition and that have a proven ability tomanage social, societal and governance risks.

An ambitious idea

Choosing to combine sustainable financialperformance and positive environmental im-pact was an ambitious project and a majorchallenge that I wanted to rise to, alongsideJean-Guillaume Péladan and Alban Préau-bert. Beyond the initial enthusiasm at theidea of creating and managing a new fund, Iwas particularly keen to take part in theproject as I believed in offering meaningfulinvestments through a new investment so-lution. Actually, it brought me much more,starting with a deeper understanding of the

energy and environmental transition – a major chal-lenge that affects us all. Environmental damage is a global reality that has deepconsequences for mankind as well as for ecosystems.According to the WHO, 23% of global mortality has en-vironment-related causes; this represents 12.6 mil-lion people every year. Furthermore, since the end ofthe 20th century, human civilisation has exceeded thephysical limits of what the biosphere could absorb.Every year, we use more natural capital than the planetcan regenerate, as the works of WWF and the GlobalFootprint Network, conducted over the past 50 years,have demonstrated.

The transition has begun across the world

The good news is that the environmental transition isunderway. I was actually struck by the number of stra-tegic deals carried out by the companies held in theSycomore Eco Solutions fund. Since the strategy waslaunched in 2015, and taking into account transforma-tive takeovers, IPOs and capital increases, 28 dealshave taken place on issuers within the portfolio – inother words, more than 30% of our holdings.

THE ENVIRONMENTAL TRANSITIONIS UNDERWAY!

by Thomas DHAINAUTPartner & Fund Manager

OPINION

The density of corporate action underpins the po-werful dynamics that are driving the environmentaltransition. Car manufacturers did not sit waiting forthe carbon tax to sell hybrid or electric cars; andenergy players had started developing renewableenergy production capacity throughout the world longbefore COP21… to the extent that since 2015, thesenewly installed capacities are exceeding those produ-ced by fossil and nuclear power plants. The compa-nies implementing and contributing to the growth ofthese solutions exist throughout the world, and par-ticularly in Europe.

Spotting eco-solutions

We have created a specific research methodology des-

igned to target the companies that develop eco-solutions.This research work, led by Sycomore AM with expertinputs from I Care & Consult and from Quantis, was aparticularly interesting challenge. Our methodology enables us to measure the extent towhich companies’ activities are aligned with the energyand environmental transition: the intensity of theircontribution, initially named Contribution to the Energyand Environmental Transition (CEET), is expressed as apercentage of their turnover. We therefore measure theCEET of each company. Companies offering a clear andfully aligned response to the issues of environmentaltransition and the fight against climate change will seetheir ‘green intensity’ indicator move closer towards100%: organic foods, plant-based products, renewableenergy, building insulation, public transport and recy-cling. If a business displays a neutral net environmental

Source: Sycomore Asset Management

5THE RESPONSIBLE WAY - NEC, THE ULTIMATE

impact, or similar to the average solutions available onthe market, its CEET will amount to 0%. Finally, if a com-pany has a negative impact, it is excluded. In short, onlycompanies with a CEET above 10% are eligible to the fund.

The identification of businesses aligned with the envi-ronmental transition, and the rejection of those that areeither indifferent or opposed to this transition, turned outto be a “value creating” strategy. Two years after itslaunch, the outcome is positive: Sycomore Eco Solutionshas gained over 30%, which is twice more than Europeanindices during the period.

The CEET becomes the Net Environmental Contri-bution (NEC)

Leveraging on our success, we have decided to expandthe scope of CEET by applying this policy to all ofSycomore AM’s investments and 3 market indices.The CEET becomes the Net Environmental Contribution(NEC). The NEC provides an effective metric for mea-suring transition risk and can also be used to detectweaknesses – negative NECs – and to identify sustainablegrowth potential – positive NECs.

Illustration of NECapplied to foodand beveragecompanies

To summarise, the Net Environmental Contribution (NEC) enables us to focus our investments on dynamic segmentsthat are aligned with current and future trends driving the energy and environmental transition. These companiesbenefit from powerful tailwinds and their positive missions, both inspiring and meaningful, foster their employees’ mo-tivation. This is also the case within our investment team, particularly the team responsible for running the SycomoreEco Solutions fund.

NEC, THE ULTIMATEMETRIC FOROUR PLANET

Natural capital, at the very foundation of resilience

There can be no prosperous human activity without sta-ble ecosystems able to provide the ‘services’ that keepmankind alive day to day. These services, recorded glo-bally by the Millenium Ecosystem Assessment in 2005,go from pollination by bees to the water cycle, throughclimate stability.

7THE RESPONSIBLE WAY - NEC, THE ULTIMATE

by Jean-Guillaume PÉLADANPortfolio Manager, Head of EnvironmentalInvestments & ResearchD

ISCOVERING

SRI

In the absence of natural capital, there just is nohuman capital, no societal capital and even less finan-cial capital. And those who believe, through naivety orlaziness, that technology will be our saviour, are in-creasingly less credible in view of the sheer size andnumber of challenges we would face if the servicescurrently rendered by the Earth’s ecosystems had tobe provided artificially. Yes, there is no doubt that wi-thout natural capital, neither life – nor its sub-pro-ducts, which include human civilisations – would bepossible. By its very structure, it is the foundation ofresilience.

A painful deadlock for the traditional economy

However, this remains an “inconvenient truth”, as thisnow clearly documented and highly evident observa-tion has not yet penetrated the spheres of economicmodels, which continue to provide seemingly fore-casts to a tired audience. Theory had seemingly lockedthe debate, as this striking excerpt from Jean-Bap-tiste Say’s 1928 “Complete course in practical eco-nomic policy” confirms: “Natural resources areinexhaustible; as otherwise, we would not get themfor free. As they cannot be multiplied, or exhausted,they cannot come under the scope of economicscience”. So basically, move along, nothing here.

On the climate front

The news on the climate front is bad. Extreme wea-ther events are intensifying; hottest year records are

beaten more and more frequently, and global warmingestimates are suggesting a rise in temperature rangingbetween +3 and +6°C in 2100, which would cause sealevels to rise by 2 metres and create hundreds of mil-lions of climate-related refugees.

This observation was recently summarised by GaëlGiraud, Chief Economist of the Agence Française deDéveloppement: “It is almost too late to avoid majorglobal warming at the end of the century”, “the poorestpopulations will be the most exposed to the conse-quences and this has already begun, particularly inEastern Africa and in many islands”.

Having to adapt to climate change is already a rea-lity for entire populations and for corporations.

BY ITS VERY STRUCTURE,NATURAL CAPITAL ISTHE FOUNDATION OF RESILIENCE

Source: The World Bank - http://www.banquemondiale.org/fr/news/fea-ture/2013/06/19/what-climate-change-means-africa-asia-coastal-poor

A question of survival for all

With all due respect to Jean-Baptiste Say, the media-tised polar bear sadly clinging to what’s left of driftingpack ice is not alone in facing extinction. Many econo-mic species have started to sing the first notes of their“swan song”, including companies active in coal, li-gnite, oil sands, shale oil or even paper industries. Andthe next set of candidates for extinction is lining up: in-tensive cattle farming, monocrop agriculture, nuclearenergy, pesticides, endocrine disruptors… It is gene-rally accepted within the economic world that you haveto adapt to survive, anticipate to win, etc. And the mil-lions of companies that have already begun their tran-sition are perfectly aware of the reasons behind thedeep transformational changes affecting their indus-tries, notably car manufacturers and electric power orheat generation players. Toyota finalised its hybridPrius in the 90s; Valeo made the shift towards electriccontrol systems for vehicles in the 2000s; paper com-pany UPM Kymmene launched its transformation planin 2006 and Renault started marketing its first electriccars in 2011, they year the car sharing start-up covoi-turage.fr changed its name to Blablacar…

Our solution for action and accountability

The NEC is the result of two and a half years’ work with agrowing number of partners - a new advanced metricthat enables us to measure the strategic alignment of agiven business with the energy and environmental tran-sition. Using physical data, the methodology effectivelyphotographs the net environmental contribution of a bu-siness and can be aggregated at the company, portfolioor index levels. The NEC is measured on a scale of -100%to +100%, the middle of the scale indicating the averageoffer available worldwide on each function that is coveredby the research. This new methodology enables us to de-liver performance-driven and active fund managementas well as a positive environmental impact, as demons-trated by the Sycomore Eco Solutions fund. We can alsoproduce environmental impact reporting perfectly ali-gned with the principles of article 173of French Law go-verning Energy Transition for Green Growth.

Source: Sycom

ore Asset M

anagem

ent

9THE RESPONSIBLE WAY - NEC, THE ULTIMATE

Sycomore AM@sycomoream

Fresh #water, a crucial #issue for the#biosphere: #agriculture absorbs 70% ofthe planet’s fresh water resources #savewater #ecosolutions

Sycomore AM@sycomoream

Illustration of our NEC - Net #Environmental Contribution – indicator in the #food#industry

Sycomore AM@sycomoream

Water #footprint: a #Margherita pizza re-quires, on average, 1,300 litres of water .

Source: Water Footprint Networkhttp://waterfootprint.org/en/resources/interactive-tools/product-gallery/

SRITW

EETS

Sycomore AM@sycomoream

Over 15,000 scientists in 184 countries signan #appeal warning against devastating#environmental harm .

Sycomore AM@sycomoream

In 2016, 13 commercial windfarms to bebuilt in #Europe, which will produce asmuch power as an EPR-type pressurisedwater nuclear reactor, once finalised. #clean energy

Sycomore AM@sycomoream

Photovolatic solar power: the price of mo-dules has dropped 50% since 2013 whileglobal installed capacity has grown 57xbetween 2000 and 2015 #ecology

Sycomore AM@sycomoream

2025 Goal: reduce the percentage of #nuclearproduced electricity in France from 75% to50% “A difficult target to reach” according tothe Minister for ecological and inclusive#transition @N_Hulot

Source: Le Mondehttp://www.lemonde.fr/planete/article/2017/11/13/quinze-mille-

scientifiques-alertent-sur-l-etat-de-la planete_5214199_3244.html#D7JRUQWp09hyGsUM.99

The« Unbearable »sculpturedepicting animpaled bearon a pipelinein Bonn onNovember 8th.

PATRIKSTOLLARZ / AFP

Source: Sycomore AMhttp://www.sycomore-am.com/Notre-magazine/2017/03/351

-Coup-de-projecteur-sur-SIF-Holding

Source: AT Kearney Energy Transition Institutehttps://www.lesechos.fr/idees-debats/cercle/030823149190

-transition-ecologique-la-clef-du-succes-2127862.php

Source: Le Monde http://www.lemonde.fr/energies/video/2017/11/09/nicolas-hulot-et-le-nu-cleaire-en-france-nos-reponses-a-vos-questions_5212856_1653054.html

Sycomore AM@sycomoream

According to the #WHO, 23% of global mortality has #environment-related causes; this accountsfor 12.6 million people every year .

11THE RESPONSIBLE WAY - NEC, THE ULTIMATE

Sycomore AM@sycomoream

Wednesday, August 2nd 2017. Since this day,#mankind lives beyond its means: it hasused the entirety of ressources provided bythe Earth in a year .

Source: Global Footprint Network & Le Mondehttp://www.lemonde.fr/planete/article/2017/08/01/a-compter-

du-2-aout-l-humanite-vit-a-credit_5167232_3244.html

Pascal CANFIN Managing Director of World Wild Fund France

FINANCEON THE FRONTLINE OFTRANSITION

Former Deputy Minister in charge of Deve-lopment, Pascal Canfin is the Managing Di-rector of WWF France, one of the world’sleading wildlife conservation organisations.He is also a member of the “High Level Ex-pert Group on Sustainable Finance”, workingwith the European Commission.

A graduate in Political Science and from theUniversity of Newcastle, Pascal Canfin firstserved as a journalist for Alternatives Eco-nomiques, where he specialised in corporatesocial responsibility. He was later elected asa member of the European Parliament,where between June 2009 and May 2012, and

then between May and July 2014, he negotiated draftlegislation on financial reform.

In May 2012, Pascal Canfin was appointed DeputyMinister for Development in Jean-Marc Ayrault’sgovernment. In this role, he intended to “make sus-tainable development an imperative for the country’sdevelopment policy”. He spurred change within theAgence Française de Développement’s project fun-ding policies and launched the first draft policy andplanning bill on development and international soli-darity.

During the preparations for the COP 21 summit, PascalCanfin served as main climate advisor for the WorldResources Institute (WRI) and co-chaired the Com-mission for innovative pro-climate funding, set up bythe French President.

INTERVIEW

S

In many areas, NGOs are playing increasingly importantroles, spurring change and acting as watchdogs. Whatmission has the WWF set itself in relation to finance?

The WWF’s objective is to transform the market’srules of play and to make them environmentally sus-tainable – and this includes finance. We are convincedthat finance is an extremely powerful driver of change.In this respect, I suggest you read the works of LucBoltanski1 on the transformation of capitalism: he ex-plains that the power of an economic player is propor-tional to his or her “liquidity”, in effect the ability tocommit and disengage, and to invest elsewhere. Mar-ket finance is extremely liquid and therefore very po-werful. It is one of WWF’s main priority targets.

Furthermore, we are lucky to be working in France –in a particularly favourable environment, driven by pu-blic sector initiatives such as article 1732 or the TEECLabel, and by a dense ecosystem of engaged players,as the launch of Finance for Tomorrow, of which theWWF is a partner, demonstrates. Another example isFrance’s issuance of 9 billion euros’ worth of sove-reign green bonds in 2017, which clearly places thecountry as a leader in this field. This step paves theway to a new paradigm. Fortunately, these initiatives arenot limited to France; the European Commission laun-ched the High-Level Expert Group on Sustainable Fi-nance with a view to promoting sustainable finance inEurope; the group is expected to deliver its final reportin 2017.

As a qualified specialist, you are also a member ofthe European Commission’s High-Level ExpertGroup on Sustainable Finance. What impact couldthis work have?

The taskforce has already had an impact, as the initialrecommendations published in July 2017 providedinput for the legislative proposals of the EuropeanCommission, with a view to integrating environment,climate and sustainability-related risks into the man-dates of the 3 European agencies3 supervising banks,insurance companies and capital markets. Further-more, via the European Taskforce on Climate-relatedFinancial Disclosures or TCFD4, the idea of a Europeanarticle 173 has emerged. Two guiding principles governthis progress:• Measuring: this is the first fundamental stage; to beable to manage climate risk, it first needs to be quantifiedand monitored;

• Aligning: this is about gradually facilitating the flow of capital towards solutions, and no longer towardsinvestments that generate negative externalities.

1 French sociologist born in 1940, Luc Boltanski published works on the transformation of capitalism: Le nouvel esprit du capitalisme, co-written with Ève Chiapello in1999 and Enrichissement, a criticism of merchandise, with Arnaud Esquerre in 2017.2 Act on Energy Transition for Green Growth, voted on August 17th 2015 and came into force in late 2015.3 The European Banking Authority, the European Insurance and Occupational Pensions Authority, and the European Securities and Market Authority.4 Task Force on Climate-related Financial Disclosures.

FINANCE IS ANEXTREMELY POWERFUL

DRIVER OF CHANGESource: European Com

mission

https://ec.europa.eu/info/sites/info/files/170713-

sustainable-finance-report_en.pdf

13THE RESPONSIBLE WAY - NEC, THE ULTIMATE

Initiatives for aligning development with 2°C scenariosare growing. 320 large companies throughout the worldhave joined the Science-Based Targets initiative, wherethey work on the implications of a 2 degree-world fortheir businesses. Sometimes, the WWF provides directsupport to help these companies set their own 2°C com-patible map. At government level, the adoption of car-bon-neutral targets for 2045 and 2050 respectively bySweden and France, is a powerful example of alignmentwith the key targets set during the Paris Agreement.

To conclude on the role of the HLEG, other proposalswere shared with the Commission and could lead toresults as early as December 12th, during the climatesummit organised in Paris by the French President.

June 30th 2017 was the deadline for the publicationof reports in compliance with article 173 of theFrench law governing Energy Transition for GreenGrowth. These reports are particularly heteroge-neous and not all that readable. What is your initialassessment of article 173?

This year, the WWF chose to examine the answers provi-ded by insurance companies. I suggest you take a look atthe article we published on this matter at the end of No-vember 2017. To summarise, while some insurance com-panies have made progress in aligning with the 2°Cscenario, which we recognise as a major headway in thefield of reporting, it will be important to raise awarenessand outreach to improve readability for citizens.

This edition of the Responsible Way is dedicated tocorporate environmental impact and how it ismeasured by investors. What role can these im-pact metrics have?

They are essential. As far as market finance is concer-ned, for instance, it would be interesting to know whichareas of the economy are financed by stock market in-dices: when I buy an investment vehicle aligned with theCAC 40 index, am I buying a world with 2, 3 or 4 degreesof global warming? Today, transparent information onthis matter is not available. I believe that if we were toask investors explicitly whether they wanted to investtheir savings in a +2° C or a +5° C world, most wouldopt for the +2° C option; this would lead to a majorreallocation of capital and therefore a shift in accessto capital. As long as index-linked or “passive investment”remains impermeable to environmental impact criteria,it will not, by its very nature, be able to contribute toshifting financial flows.

Furthermore, it is important to remember that the economyis not just about listed companies! Many low carbon intensiveactivities, such as education, healthcare and home care & ser-vices fall into the non-business, unlisted category. Therefore,the listed universe is carbon intensive and particularly misali-gned with sustainability targets. Hence the importance of get-ting things moving along quickly, as we are in a race againsttime as far as climate-change is concerned.

AS LONG AS INDEX-LINKEDOR “PASSIVE INVESTMENT”REMAINS IMPERMEABLE TO

ENVIRONMENTAL IMPACT CRITERIA,IT WILL NOT, BY ITS VERY NATURE,

BE ABLE TO CONTRIBUTETO SHIFTING FINANCIAL FLOWS.

What key developments have you witnessedsince your appointment as head of WWF Francein January 2016?

Other than the trends discussed above, what strikes meparticularly is the change in our everyday behaviour.Last October, we published an Ifop survey in partnershipwith Le Parisien5 on French consumer habits. To thequestion “Do you, personally, purchase organic foodproducts?” the answer given by the French populationhas changed radically over the past 20 years. While 65%had answered “rarely or never” to the question backthen, they are now only 38%. The vast majority of the po-pulation has shifted in favour of organic food, with 62%answering “often or from time to time”.

Ifop survey in partnership with Le Parisien on French consumer habits - October 2017.Answer to the question: “Do you, personally, purchase organic food products?”

We have shared this encouraging observation with thecompanies we work with and their message is clear:the change of paradigm towards healthier and moreeco-friendly food is on the right path, and is gainingmomentum!

Note also that these shifts are at work in many otherareas, such as mobility or energy, and are ushering ina new era.

5 Cf. link: http://awsassets.wwfffr.panda.org/downloads/171010_sondage_wwf_ifop_agriculture.pdf

TOTAL Often / From time to time

• Very often

• From time to time

TOTAL Rarely / Never

• Rarely

• Never

TOTAL

35

7

28

65

26

39

100

33

8

25

67

23

44

100

41

6

35

59

37

22

100

47

11

36

53

33

20

100

62

Frenchpopulation13-14 August

1998(%)

Frenchpopulation17-18 Oct.2000(%)

Frenchpopulation20-21 Feb.2008(%)

Frenchpopulation15-17 June2001(%)

Frenchpopulation3-4 Oct.20175

(%)

19

43

38

26

12

100

15THE RESPONSIBLE WAY - NEC, THE ULTIMATE

Henri POUPART-LAFARGE CEO of Alstom

ON THE (RAIL)ROADTO SUSTAINABLEMOBILITY

Henri Poupart-Lafarge is the CEO of Alstom.He also served as CEO of Alstom Transportand Executive Vice-President of Alstom from2011, until Alstom refocused on transport asits core business.

In 2010, Henri Poupart-Lafarge was appoin-ted Executive Vice-President and CEO ofAlstom Grid. From October 2004 to June2010, he served as Alstom’s CFO and was amember of the executive committee. From2002 to 2004, he was Senior Vice-Presidentof Finance for the Transmission and Distri-bution business. He joined Alstom in 1998.

Henri Poupart-Lafarge began his career in 1992 at theWorld Bank in Washington, D.C. before joining theFrench Ministry for the Economy and Finance in 1994.

Henri Poupart-Lafarge is a graduate of Ecole Polytech-nique, of the École nationale des Ponts et Chausséesand from the Massachussetts Institute of Technology(MIT).

Using the metric developed by Sycomore AM, Als-tom comes out with the highest NEC of +100%*.This rating corresponds to an eco-solution in pas-senger and goods transportation that is as “green”as cycling and car-sharing. Does this surprise you?

Intrinsically, rail transportation emits less carbondioxide and particles than any other means of trans-port, such as cars for instance, in terms of passen-ger.kilometre or ton.kilometre. Therefore, it comes asno great surprise to me that Alstom has emerged asan eco-solution; but I would like to add two furthercomments.

On the one hand, the number of diesel trains currentlyin circulation remains high in many countries; this is aproblem when trains operate on long non-electrifiedsections, which is the case for instance in Germany.Considering the high cost of electrification, the hydrogentrain is an attractive alternative to diesel. Alstom is oneof the pioneers in the development of green hydrogentrains, with the Coradia iLint1 solution, now operationaland offering an autonomy of 600 kilometres.

On the other hand, the physical footprint of transportinfrastructure is an important parameter in environ-mental assessments. As an example, in Paris today,cars account for 7% of travel and 77% of publicspace2, while the subway operates underground. It iseasy to imagine that recovering this space would allowfor the development of more green areas in cities. Thisrepresents a great challenge when considering thecity of the future. Underground railways or tramways,such as the integrated Attractis3 system, are muchmore economical in their use of urban spaces.

Finally, beyond gas emissions and the use of physicalspace generated by our solutions, we work conti-nuously on further minimising the energy used fortrain manufacturing purposes.

What are Alstom’s thoughts on the challengesrelated to climate change?

First of all, as mentioned previously, we are lookingfor solutions that will help to mitigate climatechange. But today, the question is also about adaptingto this change. In this respect, the World Bank haspaved the way and is encouraging others to follow suit:we now have to determine, systematically and in fulldetail, the resilience of our systems to scenarios of ri-sing ocean levels, for all projects funded by the orga-nisation and for a growing number of multilateralfinancial institutions.

On this matter, I was struck by the practical responsesuggested by the New York municipal authorities forthe city’s subway, which was devastated by hurricaneSandy in 2012, with some stations only recently re-opened. To avoid a repetition of incidents on such asscale, the situation was carefully analysed. Theconclusion was that in the event of another flood, asit is impossible to make a subway totally waterproof,

Source: Coradia iLint - Credits: Alstom / Anne-Sophie Wittwer

* Based on greenhouse gas emissions and air pollution per passen-ger.kilometre and ton.kilometre.

17THE RESPONSIBLE WAY - NEC, THE ULTIMATE

the electric installations would have to be moved.Consequently, the first floors of neighbouring buil-dings have been taken over for the installation of theelectric cabinets required for operating the subway. Ifhurricanes become increasingly frequent, the damagethey cause should however be less severe than whenSandy tore through the city.

Alstom, and the broad rail transportation industry,seem to be well-aligned with the objectives ofenergy and environmental transition, which contri-butes to the resilience of your outlook. What othermodes of transport or solutions could become rivalsin the foreseeable future (hyperloop, etc.)?

Unlike the energy sector, which has seen a series ofdifferent production methods using incredibly variedtechnology, the evolution of the transportation industryhas been much more limited. Since it was invented, nobetter alternative has been found to wheel transport,steel on steel. Consequently, I do not believe that ano-ther form of transport could supersede rail travel. Inmy opinion, the real limits to rail travel are “non-mo-bility” or immobility – and here, our next competitorsbecome telecom operators.

And if mobility continues to grow, and does not sufferfrom political headwinds, as did energy, this growthwill naturally reach a peak at some time in the future.

Does the energy and environmental transition offerAlstom other opportunities?

At a time when the issues around mobility have be-come global, cities have no option but to think aboutthese challenges, through the prism of environmentalprotection but also of physical congestion. As part ofour strategy, Alstom has chosen to be a global playerand is looking to anchor its presence throughout theworld. Hence our merger with Siemens.

Second, rail systems have not evolved that much, whe-reas other forms of transport are changing fast, parti-cularly the car industry, with the development of hybridand electric vehicles. Mobility challenges are funda-mental and we can no longer afford to optimise eachform of transport individually. It is important now to ap-prehend the issue as a “global system”, which pointstowards global turnkey solutions for cities. For exam-ple, we have recently showcased our multimodalcontrol centre in Montreal, able to manage under-ground and bus traffic, but also the presence of policeforces, ambulance routes, etc.

Historically, rail transportation has developed on a ra-ther isolated basis. However it needs to step out of this

IN MY OPINION,THE REAL LIMITS TO RAIL TRAVELARE “NON-MOBILITY”OR IMMOBILITY – AND HERE,OUR NEXT COMPETITORSBECOME TELECOM OPERATORS

Source: Control center (ALS060 CS 2214) - Credits: Alstom Transport /TOMA - C.Sasso

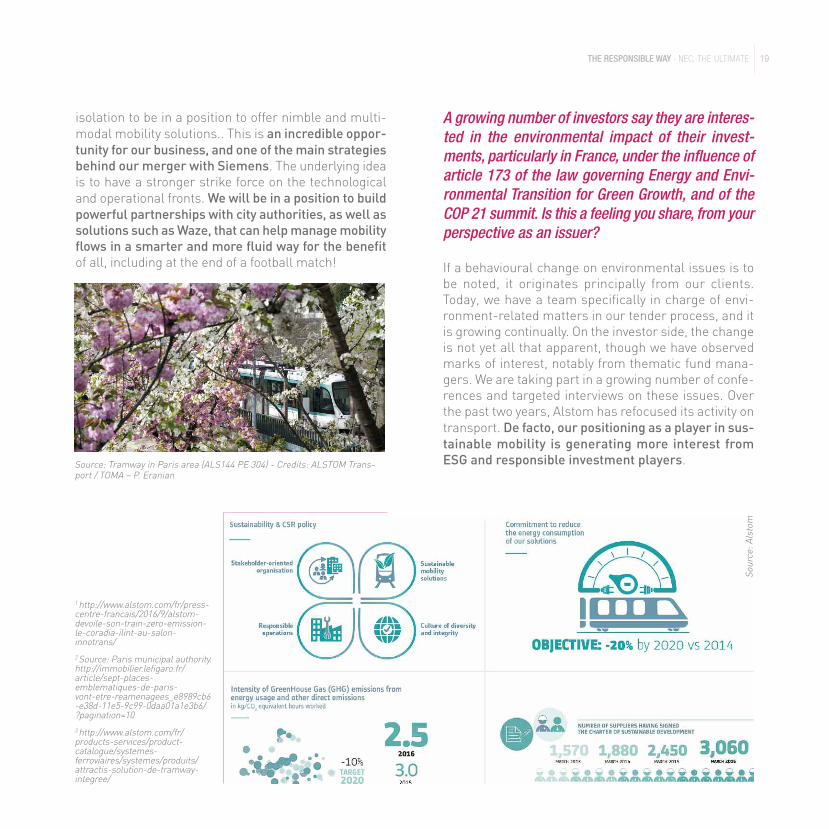

A growing number of investors say they are interes-ted in the environmental impact of their invest-ments, particularly in France, under the influence ofarticle 173 of the law governing Energy and Envi-ronmental Transition for Green Growth, and of theCOP 21 summit. Is this a feeling you share, from yourperspective as an issuer?

If a behavioural change on environmental issues is tobe noted, it originates principally from our clients.Today, we have a team specifically in charge of envi-ronment-related matters in our tender process, and itis growing continually. On the investor side, the changeis not yet all that apparent, though we have observedmarks of interest, notably from thematic fund mana-gers. We are taking part in a growing number of confe-rences and targeted interviews on these issues. Overthe past two years, Alstom has refocused its activity ontransport. De facto, our positioning as a player in sus-tainable mobility is generating more interest fromESG and responsible investment players.

1 http://www.alstom.com/fr/press-centre-francais/2016/9/alstom-devoile-son-train-zero-emission-le-coradia-ilint-au-salon-innotrans/2 Source: Paris municipal authority.http://immobilier.lefigaro.fr/article/sept-places-emblematiques-de-paris-vont-etre-reamenagees_e8989cb6-e38d-11e5-9c99-0daa01a1e3b6/?pagination=103 http://www.alstom.com/fr/products-services/product-catalogue/systemes-ferroviaires/systemes/produits/attractis-solution-de-tramway-integree/

isolation to be in a position to offer nimble and multi-modal mobility solutions.. This is an incredible oppor-tunity for our business, and one of the main strategiesbehind our merger with Siemens. The underlying ideais to have a stronger strike force on the technologicaland operational fronts. We will be in a position to buildpowerful partnerships with city authorities, as well assolutions such as Waze, that can help manage mobilityflows in a smarter and more fluid way for the benefitof all, including at the end of a football match!

Source: Alstom

19THE RESPONSIBLE WAY - NEC, THE ULTIMATE

Source: Tramway in Paris area (ALS144 PE 304) - Credits: ALSTOM Trans-port / TOMA – P. Eranian

Jean-Philippe HERMINEDirector, Environmental Planning and Strategy, Renault

and CEO of Renault Environnement

THE DEEPTRANSFORMATIONIN THEAUTO INDUSTRY

After graduating from the Ecole NationaleSupérieure de Géologie in Nancy in 1987,Jean-Philippe Hermine joined a team of re-searchers in the North of Sweden workingon glaciers in the Arctic and Antarctic.

In 1992, he moved to the United States to de-velop a specialist knowledge in the nascentarea of soil and groundwater industrial pol-lution, with the largest Environmentalconsultancy firm, CH2M Hill.

He then joined the group’s Paris office to de-velop the business of environmental auditsin the context of disposals/acquisitions.

In 1996, he moved to Renault, where he

managed all environmental audits for the group’srestructuring programmes and corporate deals (RVI,Volvo, Dacia, Samsung, …)

In 2009, he was appointed Group Head of Energy,Health and Safety and Environment for Renault’s in-dustrial plants worldwide.

Since July 1st 2011, he has served as Renault’s Directorfor Environmental Planning and Strategy, and is res-ponsible for drawing up and implementing the Group’senvironmental policy, covering products, productionand all brands and businesses. He is also the CEO ofRenault Environnement, the holding that managesRenault’s interests in three recycling subsidiaries.

Based on the metric developed by Sycomore AM,the Renault-Nissan group stands out with a posi-tive NEC that is well above the average* displayedby the auto industry - ahead of BMW and VW, butbehind Toyota and PSA. Is this a surprise to you?

Neither the fact that the Renault-Nissan alliance recei-ved a positive NEC nor that we feature in the top 3comes as a surprise to me. This result is consistent withthe consensus on these major issues; it could only varyslightly according to the time horizon (short or mid-term) or the focus (climate-related, emissions of pollu-tants etc.) considered.

Our DNA is about developing affordable and disruptivetechnological solutions. In this respect, Renault-Nissanwas very quick to position itself on electric vehicles at atime when the rest of the industry was not yet fully

convinced. Over the past ten years, our investments havebeen focused in this area, giving us a considerable stepahead.

Our offer now includes a full range of electrified vehicles.This range will expand going forward, both on the lightcommercial vehicle segment and with specific productsadapted to different geographies. We are already recei-ving valuable feedback on the electric market and areworking on an on-going basis to improve our industrialpractices in engine manufacturing.

Furthermore, our most recent 6-year strategic plan, pu-blished on October 6th, is particularly ambitious in thearea of electrification. All recent statements confirm ourstrategic leadership in the 100% electric segment, on aglobal scale for the Renault-Nissan alliance and on aEuropean scale for Renault.

Renault Z.E. range of electric vehicles

Source: R

enault Group - Credits: ©

Renault Marketing 3D-Com

merce

* Based on greenhouse gas emissions and air pollution per passenger.kilometre and ton.kilometre.

21THE RESPONSIBLE WAY - NEC, THE ULTIMATE

Source: www.alliance-2022.com (Renault | Nissan | Mitsubishi)

As a matter of fact, the synergies between the Renaultand Nissan platforms will strengthen, which willmake Renault-Nissan the largest manufacturer ofelectric vehicles in the world. These new develop-ments were probably not factored into your rating, soI have high hopes that our NEC will improve even fur-ther.

Several car manufacturers had to face seriousquestions over the actual pollution levels of theirvehicles on the market. As the energy and environ-mental transition gathers momentum, it will continueto fuel these concerns. In light of these ongoingtransformations, Renault started a strategic shift infavour of electric vehicles very early on. Do you seethese transformations as threats or opportunities?

Our most recent strategic plan shows our level ofconfidence and our commitment to electrification inthe area of mobility. Considering the favourable publicpolicy trends, the auto industry is facing a deep changeof paradigm. Having already risen to the challenge ofelectric vehicles, the new Renault-Nissan-Mitsubishialliance is in a rather strong position. From our pointof view, the energy and environmental transition is, un-deniably, an opportunity. Over the strategic planninghorizon – effectively by 2022 – Renault’s objective isto electrify 50% of its offer. This involves offering se-veral ranges of electric vehicles to suit different needs:from classic hybrid or “plug in” solutions to electrifiedengines. And this will have to unfold on a global scalefor the Renault-Nissan alliance, and in a higher pro-portion in Europe and in China, where expectations areclearly much higher.

Furthermore, we have set ourselves highly ambitious

Alliance 2022:Overview and Key figures

Renault | Nissan | Mitsubishi

store electricity and help manage the intermittence ofwind or sun-generated electricity. A car battery cantherefore create value for clients and auto manufactu-rers beyond its primary function, the electric propul-sion of a vehicle.

The life cycle analysis (LCA) approach is broadly usedby our group to compare the impacts of different ve-hicles: electric vehicles clearly generate gains (forexample, the LCA of the Fluence ZE model). The LCAalso provides valuable insights into how the auto in-dustry can curb the carbon footprint inherent to themobility ecosystem (decarbonisation of the electricmix, frugal use of resources and circular economy, op-timisation of battery functionality, etc.).

*https://group.renault.com/engagements/environnement/politique-environnementale/

objectives in the area of connectivity, including driver-less cars – the first versions could be on the roads inthe early 2020s. We are even targeting the deploy-ment of a fleet of driverless electric taxis in 2022, withRenault-Nissan acting as service operators.

Does the energy and environmental transition offerany other opportunities?

Yes, many. The development of electric vehicles iscreating a need for smart charging services and newinteractions with electric grids. Batteries can have asecond “stationary” life, for example as a buffer or to

Renault’s electric vehicle ecosystem

Source: Groupe Renault - Credits: © Publicis Net Intelligenz

23THE RESPONSIBLE WAY - NEC, THE ULTIMATE

A growing number of investors say they are inte-rested in the environmental impact of their invest-ments, particularly in France, under the influenceof article 173 of the law governing Energy and En-vironmental Transition for Green Growth, and of theCOP 21 summit. Is this a feeling you share, fromyour perspective as an issuer?

I have observed that investors are expressing growing in-terest for decarbonisation, and that broadly speakingthey understand that environmental issues are funda-mental for the auto industry. For example, they look atthe percentage of our Research & Development budgetallocated to environment-related issues (more than 50%for Renault) and they keep a close eye on our strategyand on our compliance with European legislation on theaverage emissions of the vehicles we sell. This has beenvery noticeable over the past 3 years.

What have been the major changes in your businessover the past 10 years?

Everyone agrees that the auto industry is undergoingseveral transformations at the same time. On the onehand, the core B2C model is receding in response tonew user modes and final clients looking for greaterinter-modality and flexibility; they are not as interes-ted as they once were in the ownership of the vehicle:the nature of demand is changing deeply. And on theother, the energy and environmental transition anddigitalisation are introducing new playing rules. I amparticularly struck by the interest shown by the youn-ger generation in the auto industry, which they rightlyperceive as an area of major transformation, full ofchallenges and opportunities.

I HAVE OBSERVED THATINVESTORS ARE EXPRESSINGGROWING INTEREST FORDECARBONISATION, AND THATBROADLY SPEAKINGTHEY UNDERSTAND THATENVIRONMENTAL ISSUES AREFUNDAMENTAL FORTHE AUTO INDUSTRY.

SRI BY SYCOMOREESG-CFOOTPRINTOur ESG analysis is based on the in-depth un-derstanding of extra-financial criteria with afocus on 5 main areas: Suppliers & society,People, Investors, Clients, Environment. Theobjective of this research process, whichcomes in complement to the business and fi-nancial analysis, is to provide insights thathelp to refine the risk/opportunity analysis ofcompanies over the mid and long-term.

Sycomore AM takes into account ESG ele-ments when determining the risk premia of all

ESG RATING BREAKDOWN OF PORTFOLIO HOLDINGS BY ESG RATINGS

FUNDS ESG rating (from 1 to 5)

FRANCECAP 3.2SHARED GROWTH 3.3EUROPEAN RECOVERY 3.1SÉLECTION PME 3.4PARTNERS 3.0SÉLECTION CRÉDIT 3.0SÉLECTION RESPONSABLE 3.5ECO SOLUTIONS 3.4HAPPY@WORK 3.6EURO STOXX 3.1

Data as of 31.10.2017. Fund performance may be partly driven by the ESG indicators of portfolio positions but these are not the sole determining factors. Past performance is no guide to futurereturns. The funds offer no guaranteed yield or performance and carry a risk of capital loss. Prior to making an investment decision, investors are requested to consult the relevant KIID available onour website: www.sycomore-am.com.

companies under analysis. The investment universe as awhole is analysed using a proprietary research model in-tegrated to the financial valuation tool.

Developed in-house, this ratings model is built around80 criteria. It is primarily fed by raw data from compa-nies and is refined based on regular meetings with ma-nagement and on-site visits. At the end of the process,each company is awarded a rating ranging from 1 to 5.

The ESG footprint reflects each fund’s sustainable de-velopment characteristics and provides additional infor-mation.

The carbon footprint has been disclosed for all of Sy-comore AM’s funds since 2015. The idea behind this in-dicator is to enable investors to compare the carbonfootprint of different funds relative to their benchmarks(in tonnes CO2 equivalent per year) for a one million euroinvestment. Calculations are based on scope 1, scope 2and part of scope 3 emissions and do not take into ac-count the full amount of emissions generated or avoidedby the company.

25THE RESPONSIBLE WAY - NEC, THE ULTIMATETH

EFREEDOM

TOENGAGE

OUR MOST RECENT ESG MEETINGS

TOP 10 PORTFOLIO RATINGS

ESG rating(1 to 5)

UPM KYMMENE 4.0SEB 3.9DIRECT ENERGIE 3.8KAUFMAN & BROAD 3.6CELLNOVO 3.5ONTEX 3.5EIFFAGE 3.4SMITH AND NEPHEW 3.4FOCUS HOME INTERACTIVE 3.4SODEXO 3.3

ESG rating(1 to 5)

DELFINGEN 3.3KORIAN MEDICA 3.3ACCOR 3.3BIOCARTIS 3.2SOUTHWEST AIRLINES 3.1ADESSO 3.1HEINEKEN 3.1ORSERO 3.0SES GLOBAL 3.0ROYAL DUTCH SHELL 1.9

Data as of 31.10.2017

STOCKS ESG rating(1 to 5)

LEGRAND 4.1SCHNEIDER ELECTRIC 4.1TARKETT 4.0UPM KYMMENE 4.0ADIDAS 3.9

STOCKS ESG rating(1 to 5)

AIR LIQUIDE 3.9ASML 3.9EDENRED 3.9HALMA 3.9LENZING 3.9

Data as of 31.10.2017. Fund performance may be partly driven by the ESG indicators of portfolio positions but these are not the sole determining factors. Past performance is no guide to future returns. The funds offerno guaranteed yield or performance and carry a risk of capital loss. Prior to making an investment decision, investors are requested to consult the relevant KIID available on our website: www.sycomore-am.com.

SRI BY SYCOMOREOUR INVESTMENTCAPABILITIES

ESG RATINGS & CARBON EMISSIONS

ENVIRONM

ENT

SOCIAL

CARBON

GOVERNANCE

27THE RESPONSIBLE WAY - NEC, THE ULTIMATE

SYCOMORE SÉLECTION RESPONSABLE

A responsible selection of European equities that meet with the principles of sustainable development

SYCOMORE SÉLECTION CRÉDIT

A responsible selection of European corporate bonds covering the full market capitalisation and credit rating spectrum (IG, HY and NR)

PERFORMANCE SINCE INCEPTION (01.24.2011)

1 year performance: 24.1%1 year volatility: 9.5%

PERFORMANCE SINCE INCEPTION (12.05.2012)

1 year performance: 5.0%1 year volatility: 1.0%

Since 2011 Since 2016

Since 2013 Since 2016 Since 2016

Sources: Sycomore AM, Factset. Data as of 31.10.2017, I shares. *TR = Dividends reinvested. NR = Net Return. Fund performance may be partly driven by the ESG indicators of portfolio positions but these are notthe sole determining factors. Past performance is no guide to future returns. The funds offer no guaranteed yield or performance and carry a risk of capital loss. Prior to making an investment decision, investors arerequested to consult the relevant KIID available on our website: www.sycomore-am.com.

SYCOMORE HAPPY@WORK 1

A responsible selection of companies that emphasise well-being at work

SYCOMORE ÉCO SOLUTIONS

A responsible selection of innovative companies able to anticipate environment-related challenges

1 year performance: 20.4%1 year volatility: 7.2%

PERFORMANCE SINCE INCEPTION (08.31.2015)

1 year performance: 27.0%1 year volatility: 8.8%

Since 2011 Since 2016

Sources: Sycomore AM, Factset. Data as of 31.10.2017, I shares. *TR = Dividends reinvested. NR = Net Return. Fund performance may be partly driven by the ESG indicators of portfolio positions but these are notthe sole determining factors. Past performance is no guide to future returns. The funds offer no guaranteed yield or performance and carry a risk of capital loss. Prior to making an investment decision, investors arerequested to consult the relevant KIID available on our website: www.sycomore-am.com.

1 A subfund of the « Sycomore Fund Sicav » (Luxembourg) PERFORMANCE SINCE INCEPTION (07.06.2015)

29THE RESPONSIBLE WAY - NEC, THE ULTIMATE

Since 2016Since 2016

SYCOM

OREASSETM

ANAGEM

ENT

AN ENGAGEDASSET MANAGER

*Data as of 31.10.2017.

CONTRIBUTION TO LEADERSHIP THINKING

Created in 2001 and majority-owned by its founding partners and employees

Recognised expertise on publicly listed company

Performance-driven investment culture based on active management

A team of 59 people of which 7 are ESG specialists

Recognised expertise with investment capabilities rated “High Standard”by Fitch Ratings since 2008

OUR SRI ASSETS UNDER MANAGEMENT: €2,653 m

Growth of SRI assets under management (in million €)

31THE RESPONSIBLE WAY - NEC, THE ULTIMATE

OUREDGE

PROPRIETARY ESG research

AN ANALYSIS MODEL,exclusively fed with raw data published by the companies themselves

On-going and CONSTRUCTIVE DIALOGUE with Sustainable Developmentand Investor Relations teams within companies

A CONVICTION-DRIVEN SRI APROACH recognised by the Novethic Label since 2011and by the government since 2016

Firm ENGAGEMENT with key playersin the field of SRI: PRI, CDP, French-SIF (FIR), SFAF, Government, Ministries, Academics

A team of 7 specialists dedicated to ESG RESEARCH

*Dat

a as

of 3

1.10

.201

7.

TH

ERESPONSIBLEW

AY

Published document by Sycomore Asset M

anagem

ent. Any reproduction, whole or in part, is strictly prohibited.@December2017

14 avenue Hoche 75008 Paris

www.sycom

ore-am

.com

bySYCOM

OREASSETM

ANAGEM

ENT