14

The revenue crisis: when will the airline industry recover? Narjess Teyssier ICAO Chief Economic Analysis & Policy Section Montréal 26 September 2010

| Date post: | 15-Dec-2015 |

| Category: |

Documents |

| Upload: | valeria-meager |

| View: | 216 times |

| Download: | 0 times |

The revenue crisis: when will the airline industry recover?The revenue crisis: when will the airline industry recover?

Narjess TeyssierICAO

Chief Economic Analysis & Policy Section

Montréal 26 September 2010

Narjess TeyssierICAO

Chief Economic Analysis & Policy Section

Montréal 26 September 2010

Regional traffic overview for 2009 Regional traffic overview for 2009

North AmericaTraffic: -3.9%Capacity: -4.7% Load Factor: +0.7 Pt

Latin America Traffic: 0.9%Capacity: 2.2% Load Factor: -0.9 Pt

Europe Traffic: -3.9%Capacity: -4.3% Load Factor: +0.3 Pt

Africa Traffic: -3.9%Capacity: -4.3% Load Factor: -0.7 Pt

Middle EastTraffic: 9.1%Capacity: 11.9% Load Factor: -1.9 Pt

Asia PacificTraffic: -0.2%Capacity: -0.9% Load Factor: +0.6 Pt

World Traffic: -2.0%Capacity: -2.2% Load Factor: +0.2 Pt

Higher Disposable incomes

Liberalization

Falling air faresGlobalization

Main drivers for air travel demand Main drivers for air travel demand

ICAN: ICAO forum for liberalizationICAN: ICAO forum for liberalization

0%

10%

20%

30%

40%

50%

60%

1995 1999 2004 2009

0%

10%

20%

30%

40%

50%Number of frequenciesNumber of country-pair routes

As a % of international scheduled services

Air transport conducted under liberal arrangementsAir transport conducted under liberal arrangements

Source : ICAO

Frequencies Country pairs

Number of LCCs : 13Deregulation : 1978

Number of LCCs : 33

Deregulation : accelerating

Number of LCCs (Africa and Middle East) : 10

Deregulation : uneven

Number of LCCs : 10

Deregulation : in progress

LCCs development by region

Network carriers

79%

LCCs

21%

Network carriers

86%

LCCs

14%

Network carriers

79%

LCCs

21%

Number of LCCs : 48

Deregulation : 1987- 1997

Network carriers

76%

LCCs

24%

Network carriers

91%

LCCs

9%

Liberalization: a necessary frame for Low Cost Carriers development

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

Traffic Billions RPK

LCCsNon Scheduled carriersLegacy carriers

Low Cost Carriers progression Low Cost Carriers progression

Source: ICAO

1999-2009:14% p.a.

1999-2009:4.3 %p.a.

Total European air traffic

Toward more consolidation: Alliances, Airlines´ mergers and acquisitionsToward more consolidation: Alliances, Airlines´ mergers and acquisitions

3 Major alliances grouping : more than 60% of the worldwide scheduled traffic

Most well-known Non Aligned airlines

Traffic recovery started in 2010, despite the volcanic ash impactTraffic recovery started in 2010, despite the volcanic ash impact

Source: ICAO

0 2 4 6 8 10 12

Africa

Asia-Pacific

Europe

Latin America

Middle East

North America

World

RPKs Growth in %

Forecast 2010 Forecast 2011 Forecast 2012

1999-2009 average growth

4.3%

*Traffic of airlines registered in each region expressed in RPKs

Regional traffic* growth forecastsRegional traffic* growth forecasts

Challenges ahead for the airline industryChallenges ahead for the airline industry

How has the financial crisis impacted airlines and other industry stakeholders?

What are the recovery strategies?

Does liberalization improve or worsen the financial condition of airlines?

How do alliances and antitrust immunity enhance revenue, reduce costs, and affect consumer welfare?

Where will the industry be in five years?

How has the financial crisis impacted airlines and other industry stakeholders?

What are the recovery strategies?

Does liberalization improve or worsen the financial condition of airlines?

How do alliances and antitrust immunity enhance revenue, reduce costs, and affect consumer welfare?

Where will the industry be in five years?

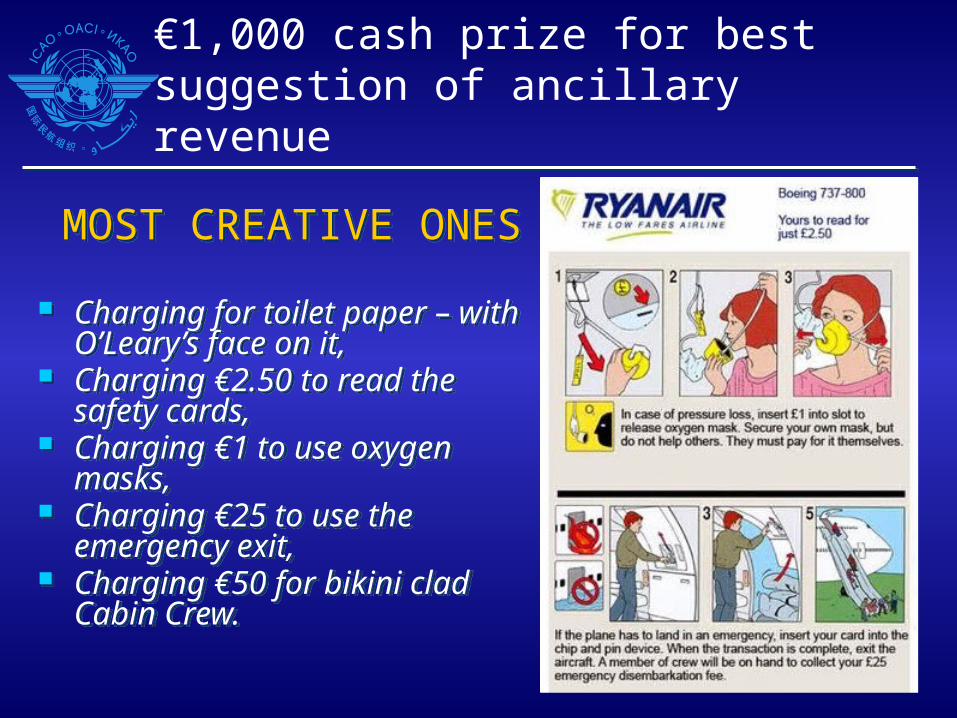

MOST CREATIVE ONES

Charging for toilet paper – with O’Leary’s face on it,

Charging €2.50 to read the safety cards,

Charging €1 to use oxygen masks,

Charging €25 to use the emergency exit,

Charging €50 for bikini clad Cabin Crew.

MOST CREATIVE ONES

Charging for toilet paper – with O’Leary’s face on it,

Charging €2.50 to read the safety cards,

Charging €1 to use oxygen masks,

Charging €25 to use the emergency exit,

Charging €50 for bikini clad Cabin Crew.

€1,000 cash prize for best suggestion of ancillary revenue

© ICAO All rights reserved.

This document and all information contained herein is the sole property of ICAO. No intellectual property rights are granted by the delivery of this document or the disclosure of its content. This document shall not be reproduced or disclosed to a third party without prior permission of ICAO. This document and its content shall not be used for any purpose other than that for which it is supplied.

The statements made herein are based on the mentioned assumptions and are expressed in good faith. Where the supporting grounds for these statements are not shown, ICAO will be pleased to explain the basis thereof.

0

500

1000

1500

2000

2500

3000

3500

4000

4500

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Low Cost Carriers progression Low Cost Carriers progression

Source: ICAO, IATA

Pas

sen

ger

r tr

affi

c B

illio

n R

PK

s

1999-2009+4.3 % p.a.

Non IATA airlines

7%

IATA members 93%

Passenger traffic market shareBy airline type

Non IATA airlines

25%

IATA members 75%

Passenger traffic market shareBy airline type

1999-2009+14 % p.a.

Market shares* achievedMarket shares* achieved

* Market share of the scheduled traffic of the airlines domiciled in the region

Europe 41%

Latin America 4%

North America 17%

Asia Pacific 25%

Africa *3%

Middle East 10%

International passenger traffic** Domestic passenger

traffic**

North America

55%

Africa *1%

Middle East 1%

Latin America 5%

Europe 8%

Asia Pacific 30%

International traffic represents 60% of the total passenger traffic

**Expressed in Revenue Passenger Kilometre