Javier San Félix Head Banco Santander – America Division Head Banco Santander America Division The Rise of Emerging Market Financial Institutions: Financial Institutions: What are the implications for financial stability? WB / IMF/ FED, June 7 th 2013

Transcript

Javier San FélixHead Banco Santander – America DivisionHead Banco Santander America Division

The Rise of Emerging Market Financial Institutions:Financial Institutions: What are the implications for financial stability?yWB / IMF/ FED, June 7th 2013

2

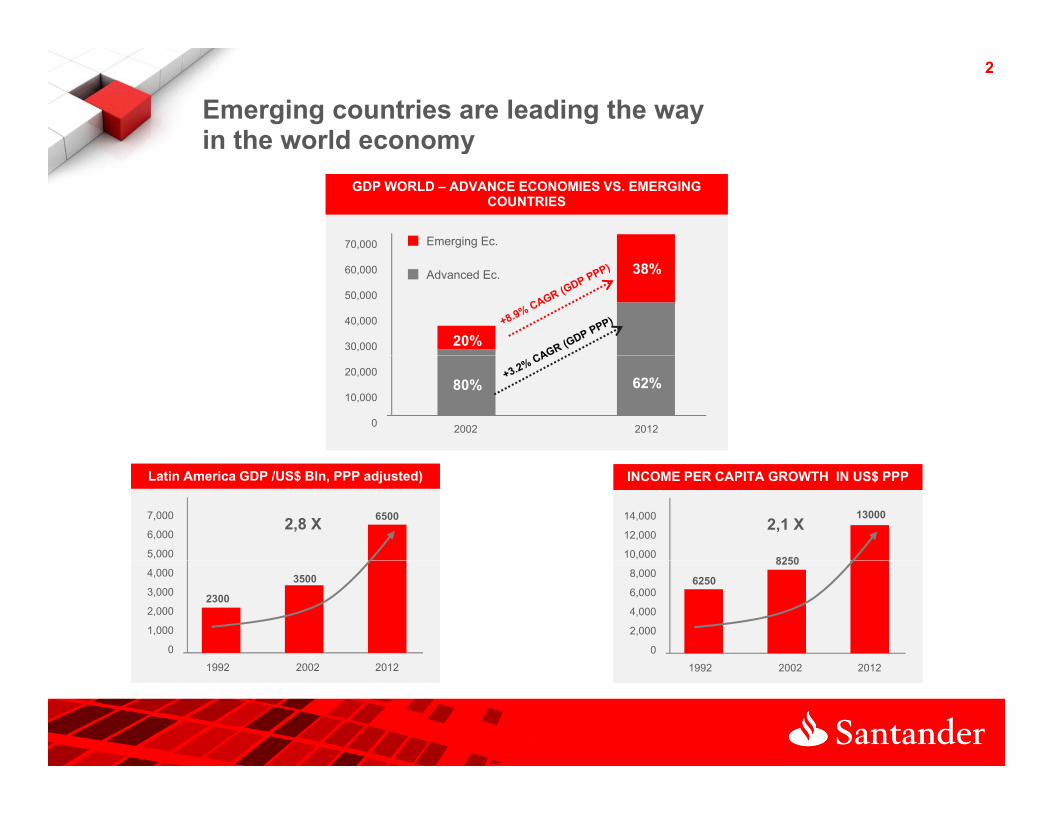

Emerging countries are leading the wayin the world economy y

GDP WORLD – ADVANCE ECONOMIES VS. EMERGING COUNTRIES

GDP WORLD – ADVANCE ECONOMIES VS. EMERGING COUNTRIES

70,000 Emerging Ec.

60,000

50,000

40,000

30,000 20%

38%Advanced Ec.

20,000

10,000

0 2002 2012

80% 62%

Latin America GDP /US$ Bln, PPP adjusted) Latin America GDP /US$ Bln, PPP adjusted)

7,000

6,000

5,000

65002,8 X

INCOME PER CAPITA GROWTH IN US$ PPPINCOME PER CAPITA GROWTH IN US$ PPP

14,000

12,000

10,000 8250

130002,1 X

4,000

3,000

2,000

1,000

0

2300

3500 8,000

6,000

4,000

2,000

0

6250

8250

1992 2002 2012 1992 2002 2012

3

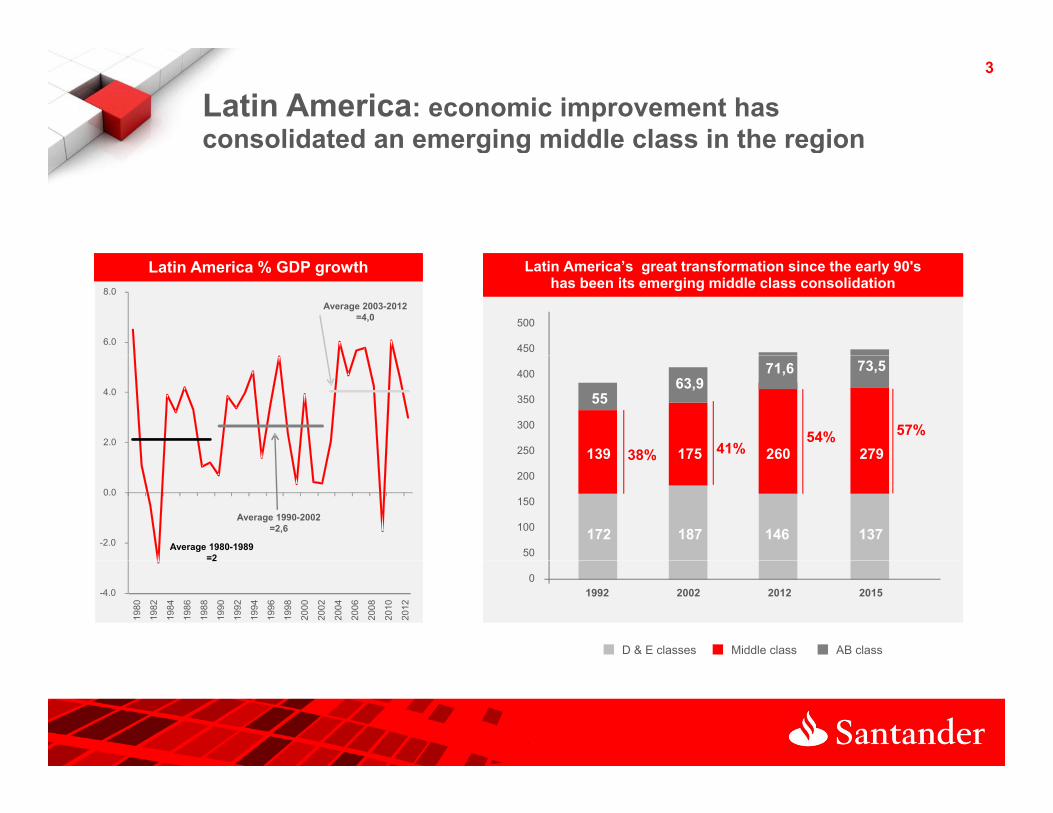

Latin America: economic improvement has consolidated an emerging middle class in the regiong g g

500

450

Latin America % GDP growthLatin America % GDP growth

6.0

8.0Average 2003-2012

=4,0

Latin America’s great transformation since the early 90's has been its emerging middle class consolidation

Latin America’s great transformation since the early 90's has been its emerging middle class consolidation

400

350

300

250 139

55

175

63,9

260

71,6

279

73,5

38% 41%54% 57%

2.0

4.0

200

150

100

50172

139

187

175

146

260

137

27938%

-2.0

0.0

Average 1980-1989=2

Average 1990-2002=2,6

01992 2002 2012 2015

D & E classes Middle class AB class

-4.0

2

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

4

2005-13: Eight years of fast development in Latin America

2005 2013

C dit t th i t tC dit t th i t tCredit to the private sector Credit to the private sector

80

60

40

20112005(as a % of GDP)

40

20

0

Argentina Brazil Chile Colombia Mexico Peru

Source: World Bank May 2013Source: World Bank, May 2013

5

Banking systems in LATAM

Latin America keeps growing at double-digit rates

CreditCredit

1,778

SavingsSavings

2,741

5515.3

19.618.7

1,082

1,2841,535

55

11.814.515.3

12 4

1,857

2,1402,450

6.1

Dec-10 Dec-11 Last. Av.Dec-09Dec-09

12.4

Dec-10 Dec-11 Last. Av.

6Latin America is in the forefront of implementation of new financial regulation and with solvent and liquid balance-sheetsliquid balance-sheets

Status of adoption of Basel III

Final rule bli h d

Final rule

published

Draft rulepublished

Mexico Argentina Brazil United States European Union

Source: BIS, May 2013

Solvency and liquidity indicators

Capital to Assets

Liquid Assets to Total Assets

11.7

29.0

10.0

30.2

8.1

13.2

11.1

35.0

10.4

28.3

4.7

39.7

5.1

19.0

Argentina Brazil Chile Mexico Peru USA Germany UK

12.0

13.4

Source: Financial Soundness Indicators (FSI), World Bank, May 2013

7

Santander has weathered the crisis

Recurring results… even in tough timesProfits

2012Pre-provision profit (net margin)(billions of euros)

First quarter 2013 attributable profit by geographic segments (*)

Balance between mature and emerging markets

Brazil26%

Poland4%Spain

11%G

Portugal1%

26%

Mexico13%

Germany5%

Other – Europe4%

Rest of Latin

USA12%

UK12%

Chile5%

Rest of Latin America3%

Argentina4%

(*) Ordinary attributable profit by operating area excluding discontinued real estate activity in Spain

9

…and its Business Model

The commercial model focuses on satisfying the needs of different types of customers

Commercial focus

Asset Management and Insurance 4%

Global Wh l l

Attributable profit in 2012(by business area)

78% Retail

Top World Banks: Loan/Assets (%)Top World Banks: Loan/Assets (%)

70

Commercial Banking

74%

and Insurance 4% Wholesale Banking22%

60

50

40

30

ank

1

AN ank

3

ank

4

ank

5

ank

6

ank

7

ank

8

ank

9

nk 1

0

nk 1

1

nkn1

3

ank

2

nk 1

2

nk 1

4

20

10

0

The international bank with the most branches: 14 392B

a SA Ba

Ba

Ba

Ba

Ba

Ba

Ba

Ban

Ban

BanBa

Ban

Ban

Source: Bank data

14,392

10

With a differential structure of self-standing subsidiaries

Internationalization through subsidiaries that are autonomous in capital and liquidity

Subsidiary model

They are subject to local legislation and regulation

They are supervised byThe Group’s subsidiaries

are local banks to all intents and purposes:

They are supervised by local authorities

Their deposits are guaranteed by local guarantee funds

There is no transfer of deposits or capital between Group units

11

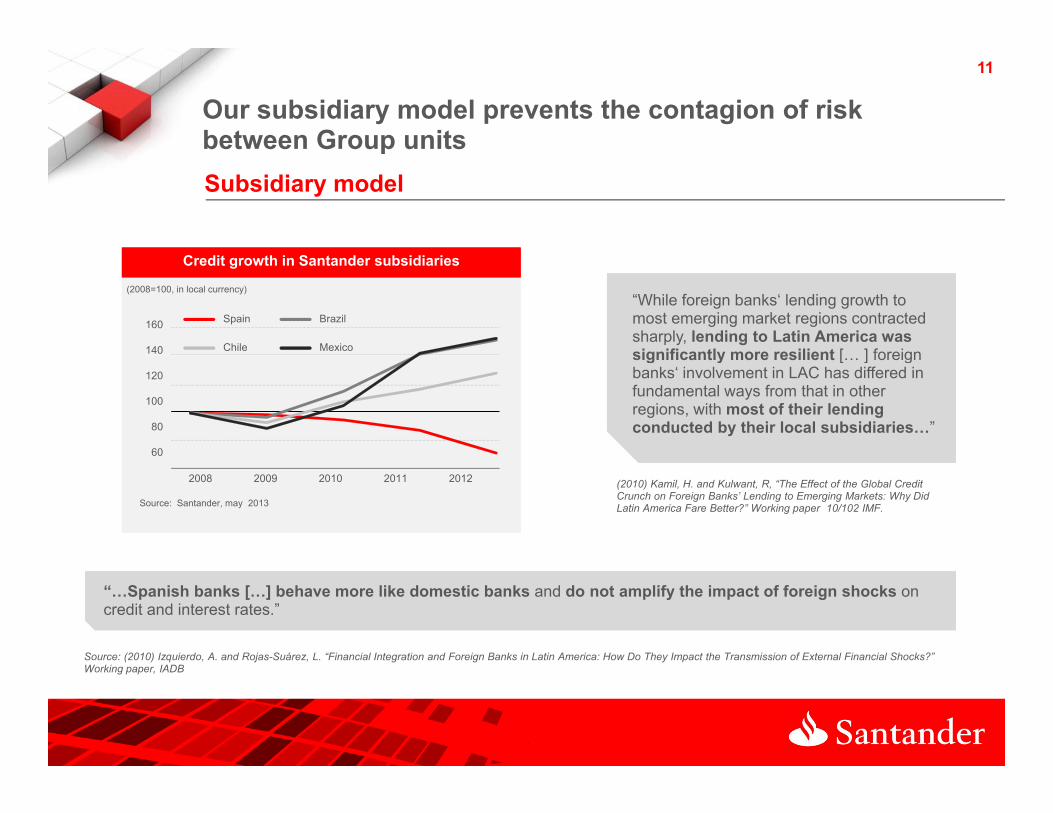

Our subsidiary model prevents the contagion of risk between Group unitspSubsidiary model

“While foreign banks‘ lending growth to most emerging market regions contracted sharply, lending to Latin America was significantly more resilient [ ] foreign(as a % of GDP)

Credit growth in Santander subsidiaries Credit growth in Santander subsidiaries

160

140

(2008=100, in local currency)

Spain Brazil

Chile Mexico significantly more resilient [… ] foreign banks‘ involvement in LAC has differed in fundamental ways from that in other regions, with most of their lending conducted by their local subsidiaries…”

120

100

80

60

(2010) Kamil, H. and Kulwant, R, “The Effect of the Global Credit Crunch on Foreign Banks’ Lending to Emerging Markets: Why Did Latin America Fare Better?” Working paper 10/102 IMF.

2008 2009 2010 2011 2012

Source: Santander, may 2013

Source: (2010) Izquierdo, A. and Rojas-Suárez, L. “Financial Integration and Foreign Banks in Latin America: How Do They Impact the Transmission of External Financial Shocks?”

“…Spanish banks […] behave more like domestic banks and do not amplify the impact of foreign shocks on credit and interest rates.”

Working paper, IADB

12

Taking advantage of Group strengths

Subsidiary modelBenefit from the Group's corporate policies…

CorporateGovernance

Sharing bestpractices

Tecnologicalenvironment

Productdevelopment

Riskmanagement

Brand name

13

Results seem to back our model

Subsidiary model

Preserving the “local touch”

160180200

Banks: Top 75 in market capitalizationBanks: Top 75 in market capitalization

6080

100120140160

IPOs:

Brazil (2009) Chile (2011) México (2012)

IPOs:

Brazil (2009) Chile (2011) México (2012)

Santander Mexico

Santander Brazil

Santander Group

0204060

ICBC

Wel

lsFa

rgo

HSB

Cct

ion

Bank

gan

Cha

seC

itiG

roup

nkof

Chi

naof

Amer

ica

nkof

Chi

naw

ealth

Bank

subi

shiU

FJst

pac

Bank

ofC

anad

aú

Uni

banc

od

NZ

Ban

kac

hsG

roup

Sber

bank

Sant

ande

rin

ion

Bank

tralia

Bank

NP

Parib

aso

Brad

esco

UBS

ova

Scot

iaoy

dsBa

nkS

Banc

orp

Barc

lays

tom

oM

itsu

ofSc

otla

ndC

harte

red

mun

icat

ions

ncia

lGro

upor

dea

Bank

BBVA

anSt

anle

yha

nts

Bank

sche

Bank

edit

Suis

seris

hBa

nks

ofM

ontre

alst

rialB

ank

PNC

Hon

gKo

ngo

doBr

asil

Nom

ura

DBS

Gro

upe

Gen

eral

eU

nicr

edit

Citi

cBa

nkSe

ngBa

nkD

evel

Bank

peria

lBan

ka

Sanp

aolo

nese

Bank

DFC

Bank

nkof

Indi

ade

lban

ken

Swed

bank

der(

Bras

il)ay

anBa

nkio

nalB

ank

entra

lAsi

aD

NB

ASA

Raj

hiBa

nkse

asBa

nknt

iBan

kasi

ICC

IBan

kdi

riPe

rser

odi

tAgr

icol

eka

Ensk

ilda

ank

Rak

yat

BB&T

Cor

pAk

bank

Sant

ande

rer

cial

Bank

México (2012)México (2012)

2 out of the 5 biggest

commercial banks

2 out of the 5 biggest

commercial banks

W

Chi

naC

onst

ruJP

Mor

g

Agric

ultu

ralB

anBa

nk Ban

Com

mon

wM

itsW

eR

oyal

Bank Ita

úAu

stra

liaan

dG

oldm

anSa

Banc

oTo

ront

oD

omN

atio

nalA

ust

BNBa

nco

Bank

ofN Ll U

Sum

iR

oyal

Bank

oSt

anda

rdBa

nkof

Com

mM

izuh

oFi

nan

No

Mor

gaC

hina

Mer

chD

eut

Cre

Allie

dI

Bank

oIn

du

BOC

HBa

nco D

Soci

ete

Chi

naH

ang

SSh

anga

iPud

ong

DC

anad

ian

ImIn

tesa

Ove

rsea

Chi

n HSt

ate

BaSv

ensk

aH

an

Banc

oSa

ntan

dM

ala

Qat

arN

atBa

nkC

e

AlR

Uni

ted

Ove

rTu

rkiy

eG

aran

Bank

Man

dC

red

Skan

dina

visk Ba B

Gru

poFi

nSi

amC

omm

e

Source: Bloomberg, May 2013

of the regionof the region

15

Due to its Geographical Diversification (II) …With significant shares in 10 main markets (data as of 12/31/2012)With significant shares in 10 main markets (data as of 12/31/2012)

Share5: 12%Branches: 1,189Customers: 26.2 mln

UK 4UK 4

Share1: 10%Branches: 3,788Customers: 27 3 mln

BrazilBrazilBranches: 722Customers: 1.7 mln

USA Sovereign

Share1: 14%Branches: 1,170

MexicoMexico

Customers: 27.3 mln

Share3: 14%Branches: 296Customers: 6 5 mln

GermanyGermany

Share1: 9%

ArgentinaArgentina

Portugal4Portugal4Sh 1 19%

ChileChile

,Customers: 10.0 mln Customers: 6.5 mlnBranches: 370

Customers: 2.4 mln

Share: 9%

Poland 2, 4Poland 2, 4

Share1: 13%Branches: 4,683Customers: 15.0 mln

Spain4Spain4Share1: 10%Branches: 667Customers: 2.3 mln

Share1: 19%Branches: 504Customers: 3.5 mln

Branches: 1,062Customers: 5.8 mln

(1) Credits (2) Business total including Kredyt Bank (4) Includes Santander Consumer Finance business(2) Business total, including Kredyt Bank(3) Consumer term loans

(4) Includes Santander Consumer Finance business (5) Includes all mortgage loans, UPLs, and SMEs