ALSO IN THIS ISSUE: » Drive revenue with personalizeD carDs » canaDian payments inDustry coDe of conDuct » polymer primer THE RISE OF THE MICRO- MERCHANTS An explosion of new apps is making it easy to accept payments anytime, anywhere PM40050803 The Magazine of Transactions, Cards & EBPP in Canada NOV/DEC 2012

Transcript

also in this issue:» Drive revenue with

personalizeD carDs » canaDian payments inDustry

coDe of conDuct » polymer primer

the Rise of the MicRo-

MeRchantsAn explosion of new

apps is making it easy to accept

payments anytime, anywhere

PM40050803

The Magazine of Transactions, Cards & EBPP in Canada

NO

V/D

EC 2

012

The new polymer $20is now in circulation

Are you ready?Ask your suppliers if new polymer notes work in your equipment.

ABM Vending machine

$$$

3 November / December 2012 PAYMENTSBUSINESS

NOVEMBER / DECEMBER 2012

4 editor’s Desk 8 Industry Watch 10 New & Notable

taBlE Of CONtENts

12 Get noticed with QR codesTurning promotional displays into interactive experiences.

16The Rise of the Micro-MerchantsThere’s an app for everything these days, but in the past year the number of micro-payment apps has exploded.

18 Improve your card portfolioDrive new revenue by issuing personalized cards in your branches.

26Polymer primerThere’re finding their way into everyone’s wallet but why are they so special?

columns & Departments

features

22One-on-OneDan Kelly, President and Chief Executive Officer for the CFIB, on why the Debit and Credit Code of Conduct was a landmark victory for small businesses in Canada.

For subscription, circulation and change of address information, contact [email protected]

Publications Mail Agreement No. 40050803

Return undeliverable Canadian addresses to: Circulation Department302-137 Main Street North Markham ON L3P 1Y2 t: 905.201.6600 f: 905.201.6601 [email protected] www.paymentsbusiness.caSubscriptions available for $40.00 year or $60.00 two years.

2012 Lloydmedia Inc. All rights reserved. The contents of this publication may not be reproduced by any means, in whole or in part, without the prior written consent of the publisher. Printed in Canada Reprint permission requests to use materials published in Payments Business should be directed to the publisher.

Made possible with the support of the Ontario Media Development Corporation

Next issue…

JANuArY/FEbruArY — Future of Payments

EDitOR’s DEsk

the evolution of payments

Mobility is the buzzword that keeps popping up in payments. Consumers and small businesses are looking for solutions to make banking easier, which means if they’re on the

phone, they’re probably mobile banking, not talking to a customer sales representative or even scheduling an appointment at their local branch. And mobile banking isn’t just for the younger generations anymore. According to a study done by Intuit Financial Services in California, once baby boomers and seniors become active online, they use online banking as often as Gen X and Gen Y consumers.

This is good news for financial institutions because according to this American study, people who bank online, on tablets or on other mobile devices log in about 30 times a month and are more profitable to their financial institution than those who don’t bank digitally. Russell Lester, director of analytics at Intuit Financial Services, suggests financial institutions keep these findings in mind when allocating funds. “The data is clear – greater engagement via digital channels leads to better financial outcomes for the user and the financial institution.”

Though the study is based on American consumers, it stands to reason that results would probably be similar in Canada. Mobile banking is convenient. Consumers who feel comfortable accessing their accounts on mobile devices can check their balances, make payments or make enquiries as the need arises instead of having to squeeze a visit to the local branch into busy schedules. This is just one way in which the industry is evolving to make banking easier for consumers.

In her column this month, Juanita Gonsalves looks at how payments have evolved in Canada as accepted currencies have become easier to manage and more convenient for merchants, consumers and banks. And speaking of evolution, we take a look at the new $20 polymer bank notes and Mike Vaselenac tells us how personalized credit cards can improve a financial institution’s portfolio. QR codes are another new technology; we’re just starting to understand their potential to reach tech savvy consumers.

This is my first issue of Payments Business and it provides a great introduction to the industry. I look forward to getting to know more about payments and about you. Please feel free to email me with an introduction to your company, association or to yourself. I’ll be attending industry events to reach out to readers and contributors so keep in touch and I hope I’ll see you at your next conference.

EditorAmie Silverwood

Take your ISO to the next levelPivotal Payments offers advanced front-end processing solutions and provides the back-end support and technology platforms needed to drive your ISO’s growth forward. Receive application and statement branding, 24/7 merchant support and premium

liability. Focus on writing sales, while we take care of the rest. Pivotal Payments is the partner you keep.

DRIVING PAYMENTS IN CANADA

#1 ISO in Canada$10 billion annual transaction volume

350+ employees at your service

Ready to get on board?

VALUE ADDEDSERVICES

CLIENT CARE & LEAD GEN

HARDWARE DEPLOYMENT

ACQUIRING SERVICES

PAYMENT PROCESSING

Call Murray MacGillivray at 1 877-669-5689 or visit DrivingPayments.ca

6 November / December 2012 PAYMENTSBUSINESS

C anada enjoys the reputation of having one of the most stable and efficient payment systems in

the world. Our history includes using a fascinating variety of payment methods or “currency”. Let’s review this evolution.

The first humans reached the Americas about twenty thousand years ago. When the first Europeans arrived in the late 1400s, the Native Peoples had travelled across the continent and had established a complex trade and bartering ‘payment system’ which included polished seashell beads that were woven together in strings. An interesting fact is that almost every continent including Asia, Australia, Africa and America share the use of “shells” as money at some point in their history.

With ‘dentalium’ on the west coast, and ‘wampum’ on the east coast, the Europeans realized the importance these items represented to the First Nations people; the seashells were used to facilitate trade and were soon recognized as official currency. Light coloured beads were less valuable than dark beads and before long, the first counterfeit currency appeared as people began dying the light beads black to artificially increase their buying power. This diluted their value and ultimately resulted in the First Nations no longer being interested in receiving them in exchange for pelts. Wampum was decommissioned within two hundred years.

From the 16th century onward, as growing numbers of First Nations bands valued silver and copper, the introduction of various coins was a natural evolution especially during the colonization of Canada by France and England in the 18th and 19th centuries. However, by the late 1600s, a coin shortage forced colonial authorities to use “playing cards” to compensate soldiers; the monetary value was handwritten on the back of the card. By the early 1700s, this practice was

banned but new forms of card (stock) or paper money began to circulate.

During the War of 1812, colonies issued army bills to finance the war effort. When the war ended in 1815, the British government redeemed the bills at face-value restoring people’s trust in paper money and leading to the rise of banks.

1820s: banks began leveraging silver and •gold reserves to issue their own notes1841: the new Canadian pound was •issued equal in value to 4 U.S. dollars 1857: Canadian authorities abandoned •pounds sterling to issue a new, decimal based Canadian dollar coinage aligned with the U.S. dollar1858: the first minted Canadian coinage •was used throughout the provinces 1866: Province of Canada began issuing •its own paper money in denominations of $1, $2, $5, $10, $20, $50, $100 and $500In 1867 with the Dominion of Canada,

currencies of the Province of Canada, New Brunswick and Nova Scotia were merged to the Canadian dollar. The merge was completed by 1894 when Newfoundland became fully integrated with the Canadian monetary system.

By 1938, the Bank of Canada was a crown corporation of the Canadian Federal government. Fast forward to the 1980s when five of Canada’s largest banks decided to build a nation-wide (home grown) real-time ATM and POS debit network. In 1984, Interac was founded. Over the next 30 years, the following payment evolution and service enhancements transpired:

1986 - ATM Shared cash: consumers •can withdraw money from accounts using another bank’s automated teller machines1990 - Interac Debit pilot launched in •Ottawa/Hull. By 1994, the service was deployed nationally

1997 – one billionth Interac Debit •transaction milestone2000 - Interac Debit surpasses cash •as Canada’s favourite way to pay for purchases2004 - Interac eTransfer – repay friends •by sending electronic funds transfers using just an email address No banking information is required•Enhanced in 2010 to send money using •the recipient’s mobile phone number2005 - Interac Online - consumers can •pay internet merchants in real-time directly from their bank accounts without sharing banking information 2007 – first Interac EMV transaction •processed; rollout began in 2008

2010 Interac Flash announced – •customers can ‘tap’ their cards at specially equipped NFC POS readers; no PIN required

TD, Scotiabank, Royal Bank first to •offer serviceParticipating merchants currently •include: Petro Canada, Pizza Nova, McDonalds, Cineplex, Swiss Chalet / Harvey’s, Chapters/Indigo, HMV, and M&M with more who are upgrading their systems to offer the service

(refer to www.interac.ca for further details)The coming years will see exciting new

payments methods emerge using smart phones, QR codes, cloud-based payments, tokenization and biometrics…to list just a few of the ‘buzz words’ flying around the industry today. From wampum and furs to Interac Flash, I have no doubt that our made-in-Canada payments solutions will continue to serve us well. Best wishes for the holiday season and 2013!

sECtOR sCaN

Canadian payments: 16th century to present historical trek anD triviaBy Juanita Gonsalves

With just a flash in front of a reader and no PIN, the Interac Flash enhanced debit card gives

customers a faster way to pay. For you, it means quicker lines, better service, and reduced

cash handling costs. Interac Flash. It’s the Canadian way to pay, now even faster.

Find out more at InteracFlash.ca.

† Interac Association operates exclusively in Canada.®,™; Interac, the Interac logo, Interac Flash, “Everyday Simply”, the armoured truck design and the Interac Flash design are trade-marks of Interac Inc. Used under license. The Contactless Symbol is owned by EMV Co., LLC. Used under license.

CLIENT: TRIM: 8.375" x 10.875" PUBLICATION:

JOB #: LIVE:

DESCRIPTION: BLEED: +0.125" INSERTION DATE:

APPROVALS:ACCOUNT DIRECTOR: CREATIVE DIRECTOR: WRITER STUDIO MANAGER:

1910 Yonge St., Toronto, ON T: 416 484-1959

APPROVED

IT-1356-T-PM.indd 1 11-11-03 4:47 PM

8 November / December 2012 PAYMENTSBUSINESS

iNDustRy NEws

hsBcnet Mobile users authorise usD6 billion of payments over 6,000 customers demonstrate increasing demand from corporate treasurers for mobile solutions A little over a year since its launch, HSBC’s corporate mobile banking service has been used to authorise USD6 billion worth of payments worldwide, including a single payment of USD50m.

HSBCnet Mobile enables corporate treasurers to check account balances and statements, authorise payment instructions (including priority payments, payments in the Eurozone, inter-account transfers, bill payments and ACH credits/debits) and receive payment alerts using smartphones. In addition, users can authorise cross-border payments with ‘Get Rate’, which allows customers to view and instantly book foreign exchange rates when making foreign currency payments.

Diane S Reyes, Global Head of Payments and Cash Management at HSBC, commented, “When we launched HSBCnet Mobile a year ago, there was a certain amount of curiosity about whether corporate treasurers would use the technology. With USD6bn of payments authorised it’s fair to say adoption has exceeded our expectations.

“We are seeing a huge increase in the willingness of corporate customers to use smartphones and tablets for banking. This trend runs across companies of all sizes as finance managers become more mobile. They want convenient banking access and capabilities wherever they are. Increasingly, mobile devices are rivalling desktop applications for many day-to-day banking functions.” HSBCnet Mobile is a free, value-added service to customers, without the need for a cumbersome or resource-intensive installation. This means users are likely to expand the range of services they access in this way.

Marcus Treacher, Global Head of eCommerce for Payments and Cash Management, added, “We see substantial potential for extended use of mobile devices where the services we offer through them add value to anyone whose business involves travel. These devices will streamline the entire supply chain.”

In time, smartphones and tablets could bring considerable security advantages using emerging biometric features such as face recognition. Consequently, the value of mobile technology is likely to extend far beyond tools for travelling executives to similar advantages for their desk-based colleagues.

“In the future, mobile banking will combine richer, more intel-ligent interfaces with services that make use of the devices’ ability to recognise the location of the user. This has enormous value for risk management, trade, high value payments and FX services.” Treacher added.

G&D chosen by CIBC as trusted service manager for mobile payments in CanadaGiesecke & Devrient (G&D), a global market leader in secure technologies, is serving as the Trusted Service Manager (TSM) for the Canadian Imperial Bank of Commerce (CIBC) in their offering of NFC credit card payment services to their customers. G&D’s TSM service will securely download and provision the CIBC Mobile Payment Application and the credentials required for contactless payment transactions using NFC-enabled smartphones, in line with global best practices for ensuring secure NFC transactions for consumers. The TSM service is managed from G&D’s fully certified North American TSM datacenter located in Toronto, Ontario.

CIBC has launched its mobile payment solution in Canada, allowing Canadians to pay for small ticket items with their CIBC credit card at participating retailers using their NFC-enabled smartphone.

G&D’s Service Provider TSM (SP TSM) solution, the NFC Service Manager™, offers the required scalability and flexibility to deliver secure mobile contactless payment functionality for multiple payment associations acrossCanada. The TSM datacenter being used to support this functionality provides secure remote management of secure elements, applications and keys for the handling of credentials for payment transactions via a mobile device, as well as full end-to-end solutions for NFC, including issuance and lifecycle management. Collectively, these capabilities ensure that consumers can use NFC payments with confidence, knowing that all information used to process payments is managed securely.

“Given our well-established relationships with Canadian banks and mobile network operators, G&D is uniquely positioned to fulfill the required role within the Canadian mobile NFC ecosystem as the trusted third party required to securely provision consumer credentials and payment applications,” said Michael Kuemmerle, Group Executive Mobile Security and member of G&D’s Management Board.

9 November / December 2012 PAYMENTSBUSINESS

FEXCO Merchant Services, an Irish-based specialist provider of financial transaction processing, and First Data Corporation, a global leader in electronic commerce and payment processing, have announced the Canadian expansion of First Data’s GlobalChoice™ dynamic currency conversion (DCC) solution.

GlobalChoice is now live in over 300 merchant loca-tions throughout Canada with the number of participating merchants expected to increase significantly over the next 12

months. For the past ten years, First Data and FEXCO have jointly offered their DCC services at the point of sale (POS) to merchants all over the world.

“The expansion of our partnership enables Canadian merchants and ultimately consumers to benefit from FEXCO’s fully-managed treasury management service and First Data’s industry-leading payment solutions and processing platforms,” said Dermot O’Shea, executive director of FEXCO. “Entry into the Canadian market, and the opportunity to work with First Data Canada to offer GlobalChoice to merchants, represents a big opportunity for FEXCO. Strong external markets are key for Irish businesses at the moment, and we are confident we will achieve strong growth through expanding our activities into Canada.”

In addition to the conve-

nience of currency conversion at the point of transaction, GlobalChoice eliminates much of the merchant and consumer’s guesswork related to exchange rates and fees. GlobalChoice also promotes a greater transparency of the true value of goods and services in the cardholder’s home currency.

“This is a very exciting development for the Canadian payments market,” said Brian Green, general manager of First Data Canada. “With the introduction of GlobalChoice, First Data is helping merchants grow their international sales volumes while providing an additional customer service benefit. Providing consumers a choice of paying in their home currency enhances the purchase and checkout experience.”

Canada represents the 20th country in which FEXCO has expanded its services. The Canadian market offers

an exceptional opportunity for merchants who use GlobalChoice as their currency conversion solution. In 2011, international visitors spent more than $16 billion in retail purchases as reported by the Canadian Tourism Commission.

The GlobalChoice expansion announcement coincided with the recent Enterprise Ireland’s Trade Mission to Canada led by Richard Bruton, Ireland’s Minister for Jobs, Enterprise and Innovation with the objective of increasing the level of Irish exports to Canada.

“The collaboration between FEXCO and First Data on the expansion of the GlobalChoice solution into the Canadian mar-ket is a great example of what is achievable for innovative Irish companies with ambitions to grow their export markets” said Minister Bruton. “I commend all involved and wish them every success in the future.”

iNDustRy NEws

FEXCO and First Data announce expansion of GlobalChoice™ Dynamic Currency Conversion Solution in Canada

10 November / December 2012 PAYMENTSBUSINESS

As part of their ongoing commitment to provide innovative payment solutions for businesses of all sizes, Pivotal Payments, North America’s fastest growing payment processor, announced a new mobile payment platform that can be used on smartphones and tablets. PivotalMOBILE is an integrated payment solution that includes an ap-plication for iOS, Android and BlackBerry devices, along with a card reader that plugs directly into the mobile device’s audio port.

PivotalMOBILE is a cost-effective add-on that lets small to mid-sized businesses process credit card payments from virtually any location. Pricing is flexible unlike many industry competitors and not based on a single published rate. The mobile payment solution includes the following features:

Sales and refunds•Accepting and editing tips•E-mailing receipts to clients•Verifying transactions with on-screen signature •capture and transaction geolocationPivotalMOBILE is Payment Card Industry (PCI)

compliant and offers end-to-end encryption between the mobile device and Pivotal Payments’ secure servers. Credit card information is never stored on the mobile device.

“As smartphones are becoming increasingly ubiquitous, it’s only natural that merchants and

their customers want to integrate them into every aspect of their lives,” said Philip Fayer, President and CEO of Pivotal Payments. “At Pivotal, we’re always evolving to meet and exceed the needs of our clients and partners and we’re extremely pleased to offer this innovative, new processing platform.”

Businesses using PivotalMOBILE also gain access to Pivotal Payments’ proprietary merchant account reporting platform, Pivotal360. This online service provides transaction history, detailed sales reports, monthly statements and other valuable business management tools.

Mobile payment processing is typically used by contractors, direct sellers, at trade shows, by de-livery and other service businesses operating from various locations, however they also give retailers the flexibility to process payments from virtually any location within their store. No longer confined to the checkout line, customers can complete their purchases anywhere with a data or Wi-Fi signal. Commonly known as “line busting,” PivotalMO-BILEwill be a vital sales tool during peak shopping periods such as the upcoming holiday sales rush.

PivotalMOBILE is now available for iPhone, iPad, Android and BlackBerry users through Pivotal Pay-ments and its network of sales partners through-out North America.

Pivotal Payments introduces mobile payment options for businesses in North America

Full speed ahead: everlink offers Interac Flash™ PoS TerminalsEverlink Payment Services Inc., a leading provider of comprehensive, innovative and integrated payment solutions & services, is pleased to announce that it now offers Interac Flash enabled point-of-sale (POS) terminals to its clients. Effective immediately, new and existing Everlink clients will be able to leverage this new payment technology via Ingenico’s Telium 2 POS devices with integrated contactless acceptance, available directly from Everlink.

The two major benefits of this Everlink offering are: that it provides ISOs and their merchant clients with the ability to improve customer service with reduced lineups and increased efficiency and profitability while maintaining a high level of security. And that it eliminates the need for a bulky external contactless reader thanks to the integrated nature of the Ingenico iCT250, iWL 250 3Gand iPP320 devices.

Optimal Payments integrates its NETBANX Payment gateway for new e-commerce website Optimal Payments will integrate it NETBANX payment gateway to RONA’s new e-commerce website. RONA recently launched its online store allowing customers to purchase items online or reserve them for in-store pick-up.

Consumers shopping on the RONA website can create an account, which can be used to facilitate subsequent purchases, or make a one-time guest purchase. A hosted-payment page, imbedded into the checkout process and using iFrame technology, allows them to enter their credit card

information directly into the NETBANX, PCI DSS compliant environment.

The NETBANX solution complements RONA’s acquiring relationship with Desjardins Group to offer Visa, Master-Card and RONA’s private label credit cards as payment options. To minimize fraud losses, all transactions are verified using NETBANX fraud detection and protection tools including cardholder authentication, CVV validation and 3D Secure verification. The NETBANX back-office suite provides RONA with comprehensive reporting including data by card type.

“Using the NETBANX gateway to process payments from its e-commerce site allows RONA to offer multiple payment options, minimize our PCI compliance requirements and reduce our fraud exposure,” said Linda Michaud, vice president, information technologies at RONA.

NEw aND NOtaBlE

www.gemalto.com

Secure, convenientsolutions worldwide

> 1.5 billion secure devices produced and personalized globally a year

> 400 mobile operators - connecting over 2 billion mobile subscribers

> 500 million people use our banking cards

> 200 million citizens use our electronic passports

Giving you the freedom to enjoy your digital lifestyle

12 November / December 2012 PAYMENTSBUSINESS

T he holiday shopping season is going full tilt and the competition for retailers to capture and retain the attention of

potential customers throughout the buying cycle is fierce. For small businesses looking to promote themselves during this hectic and promising time of year, QR codes are a cost and time effective option. If you’re ramping up for post-holiday sales, you still have time to incorporate them into your promotions.

QR codes can transform promotional displays into an interactive experience for customers. They help consumers become familiar with a product by providing additional information to help them make purchase decisions. Reaching consumers at the moment of purchase will give your business an edge over the competition.

qR CODEs

stiCking to the Code: how Qr codes can make purchasing easier By: Bill Mackrell

13 November / December 2012 PAYMENTSBUSINESS

The Canadian Institute’s 8th Annual Forum on

PAYMENTS COMPLIANCE IN CANADAProactive Core Compliance and Risk Prevention Strategies for Payment Cards and Emerging Systems

Canada’s Premier Conference on Payments Compliance!

February 27 & 28, 2013

1-877-927-7936 Priority Service Code: 434PAYBUS2

qR CODEs

If you’re interested in using QR codes, here are a few tips, just in time for the final shopping rush:

1)What will your offer be?It’s important for consumers to have a reason to scan your QR code, therefore, it’s recommended that you include a coupon, promotion, exclusive information or a demo to entice consumers to interact with your QR code. If you want to sell a specific product, link a QR code to a special promotion or coupon deal directly at the point of purchase, giving consumers a final incentive to buy.

2) Promote your offer through multiple channelsJust like a great interactive marketing campaign, it’s important to get your QR code offers out to consumers through multiple channels. Email marketing, social media apps and printed materials such as direct mail can help small businesses reach consumers in many demographics. QR codes can be placed everywhere: from print advertising to billboards, retail stores, business cards and more.

3) Time is of the essenceEspecially during the holiday season, it’s a great idea to give consumers a reason to buy quickly. Creating an expiration date on a great offer or promotion will motivate consumers to move quickly and purchase the product you’re Remember that consumers will be scanning via a

smartphone, so it’s important that whatever your QR code links to is mobile friendly.

4) relevant information is keyInformation you choose to include in your QR codes must be relevant to your target audience and add value to their shopping experience – similar to an in person sales representative It’s important to have an idea of who will be scanning your QR code—will they want product information, a demo experience or a coupon? It’s easy to frustrate customers by sending them to the wrong location or mis-representing a promotion—the same rules apply to QR codes. Instead of just taking consumers to a company website, ensure that the information you are giving them is interesting and beneficial to them.

5) Creativity can open doorsIf you’re looking to make a statement to customers about your brand, QR codes can be the best way to go about it. When developing the messaging for a QR code site, ensure that the content represents your brand in addition to promoting a specific product or promotion. Some consumers may scan a QR code because they are excited by the prospect and haven’t done so before. In order to keep them interacting with your store or brand, the content you provide them has to be creative and top-notch the first time around so that you are creating a fun and informative experience for consumers. 6) Fresh ideas=happy consumers

Whether you’re getting ready to implement QR codes for the holiday season, or you use them consistently throughout the year, it’s important to keep your QR code content updated to keep consumers interested. If someone scans a code multiple times and always sees the same content, you may lose their interest.

When it comes to creating QR codes for your business, there are many easy to use and affordable online turn-key solutions that do all the work for you. Look for an offering that not only helps you create your unique QR code patterns but also those that allow you to track when customers have scanned them. This will ensure you continue to evolve your program and are engaging your customers effectively.

A creative marketing program can be cost effective and successful with the right tools. The bustling holiday season is a great time to use QR codes to attract consumer attention. There are various ways for small businesses to use QR codes, and many different channels retailers can use to display them to consumers.

Bill Mackrell, is General Manager for Pitney Bowes canada and vice President, leasing for north america. He’s also responsible for the development and implementation of strategic and tactical sales and marketing plans to help other companies grow their business and make connections with their customers. For additional information, Bill Mackrell can be reached at [email protected]

Visit us at these upcoming shows:Health Achieve, November 5-7, Toronto, ON

Cartes 2012, November 6-8, Paris, FranceCUTA Trans-Expo, November 10-14, Quebec City, QC

ConnectedDevices

TSM

PaymentSchemes

POSTerminals

OTA

Platforms & Applications

SecureElements

Store

Internetwi�

Wallet

µSD

Mobile Security

MNO’S

Transit

Identify

FinancialInstitutions

Pay

Communicate

Enterprise& OEM

Retailers

Discoverthe futureof mobilesecurity

For more information use your favorite QR code reader.

16 November / December 2012 PAYMENTSBUSINESS

MOBilE apps

PayPal heRe Available for iPhones and iPads (trial period)Though consumers have been using the PayPal Mobile App for a while, PayPal didn’t introduce its PayPal HERE system for Canadian retailers until last March and it’s still undergoing a trial period to selected merchants on only iPhones and iPads. PayPal won’t guarantee full functionality on iPads until it releases a tablet version later. Androids will follow in the near future.

Like other payment apps, the card reader and software are free while PayPal charges 2.7 per cent per swiped transaction on Mastercard, Visa and American Express, and of course PayPal accounts. (Like all payment apps, PayPal HERE’s manual transaction fee is higher, 3.5 per cent.) PayPal HERE supplies electronic receipts sent by text or email, configures sales taxes, tip rates and discounts and tracks cash payments.

A key difference between PayPal HERE from its competitors is that merchants are directly linked to their existing PayPal accounts. Payments are deposited instantly so merchants can access those funds to say, buy more inventory.

Pushing the technology further, PayPal customers can use the Local feature on their mobile app to find PayPal-friendly merchants. In turn, the I’m Here feature tells merchants when a PayPal customers is nearby and once that customer is ready to pay, the app will reference just their name and photo and won’t require the customer to take out his phone or wallet.

Payfirma Available for iPhones, iPads, Androids and BlackberrysVancouver’s Payfirma processes a wider variety of credit cards (Visa, Mastercard, American Express and three others) that can be processed on more handheld devices than its competitors. The basic software is straightforward, offering tax and tipping options, receipts and refunds, and sales performance by day, week or month. Expect a standard processing time of two or three business days for funds to reach your bank account. However, Payfirma’s fees are higher than others: a set-up fee of $25, then each month $10 plus two to three per cent per credit card transaction that altogether must total at least $40. Make sure to check your sales volume before signing up. A free demo is available online.

Later this month, Payfirma will be updated to allow a merchant to synch their transaction history onto several handheld devices. Before New Year’s, Payfirma will unveil a new feature, PayHQ, that lets merchants track their transactions in real-time through a scrolling tickertape on their handhelds. Retailers will also be able to pinpoint which employees are selling the most product and upload their sales reports to any software that uses the common CSV format. Payfirma will release the PayHQ’s cost and details in late December.

Early next year, Payfirma will unveil the Tablet POS in Canada. It will offer the same functions as the smartphone version, but the app also allow merchants to store inventory SKUs and product images. Pricing is not available yet.

The riseof the micro-merchantsBy AllAn TOnG

T here’s an app for everything these days, but in the past year the number of micro-payment apps has exploded making it easier than ever for merchants to accept payments anywhere, anytime. This technology is revolutionizing small businesses like food trucks and golf coaches who used to shun credit cards, because of the high cost of terminals. Today, the same vendors are flocking to these apps,

because they’re affordable and easy to use on their smartphones and tablets. All it takes is a quick download and attaching a small card swiper to the headphone jack of a handheld device. We look at four apps that have recently hit Canada.

17 November / December 2012 PAYMENTSBUSINESS

mobIle APPS

square Available for iPhones, iPads and AndroidsIn October, Square expanded into Canada after establishing itself in America. Aggressive marketing and competitive pricing have driven U.S. sales of Square ever since Twitter co-founder Jack Dorsey launched it in 2010. Square processes $8 billion a year for two million Americans who are selling everything from french fries to piano lessons.

Square’s pricing is attractive. At a 2.75 per cent commission, merchants can process Visa and Mastercard without paying a set-up fee or monthly minimum (3.5% + $0.15 manually). The software and card reader are both free. Square processes accepts card payments, but also lets merchants track inventory, monitor daily sales, create loyalty programs and list themselves in the Square online directory. Though some U.S. merchants say it takes three or four days, Square promises that payments will reach a vendor’s bank account by the next business day.

intuit’s GoPayment Available for iPhones and iPadsThe folks who gave us QuickBooks now offer GoPayment. The software and card swiper are free to download, and the system is competitively priced. GoPayment demands no set-up fees nor monthly minimums, and charges a 2.7 per cent swiped transaction fee (3.3 per cent for manual). You pay as you go, so no monthly minimums. That’s a serious incentive for merchants who make relatively few transactions. Just expect two to four business days for funds to reach your bank account. However, GoPayment in Canada currently processes only Visa and MasterCard.

Essentially, GoPayment is a no-frills device. It emails receipts to customers and sets tax and tip rates, but doesn’t indicate inventory status, make cost reports or allow additional devices to use the same account like some of its competitors. Also, Canadian GoPayment doesn’t synch with other Intuit software like QuickBooks (though it is in the States), and is limited to iPhones and iPads.

18 November / December 2012 PAYMENTSBUSINESS

fEatuRE

iMprove

porTfolio your card

19 November / December 2012 PAYMENTSBUSINESS

fEatuRE

the opportunity: Canadian card trendThis is a time of challenge and opportunity for Canadian retailers and financial institutions.

New technologies and changing consumer preferences are dramatically altering the payment

ecosystem. From a financial card perspective, many forward-thinking retailers and banks

are replacing generic vault cards with highly personalized credit and debit cards. They are issuing them instantly in branch bank locations to reduce card issuance costs — but more importantly, to attract new customers and drive more revenue with existing cardholders.

Mobile payment platforms, powered by emerging technologies such as near-field communications (NFC), are also

changing the payment landscape. Retailers and banks that capitalize on mobile wallets and other

mobile offerings are strategically positioning themselves for

an increased share of a rapidly changing

market.

an established opportunity: debit and credit cardsAccording to 2012 Nilson Report data, Canadian consumers use more than 38.4 million debit cards issued through Interac®, a PIN-based nationwide network owned by the issuers. Payments made with these debit cards — which are typically not personalized — represent more than half of all card-based transactions at the point of sale. Also, there are more than 75 million credit cards in circulation in Canada. The average Canadian carries four personalized credit cards, but only 37% of these are active. The quest to acquire cardholders is one battle, but securing top-of-the-wallet position and driving card usage is yet another.

Consumers chose credit and debit card brands based on a number of factors, including value, loyalty programs, customization and convenience. True differentiation in this environment requires both innovative strategies and advanced card issuance technologies. While some aspects of card marketing seem to be marked by parity, innovative ideas — such as instant issuance of highly personalized cards in bank branches and retail locations — present card issuers with opportunities to create true differentiation. To stay competitive in this market, financial institutions and retailers need to begin evaluating their card issuance platforms and infrastructures so that they can easily and readily

iMprove

porTfolio

Drive new revenue by issuing personalized cards in your branchesBy Mike vaselenak, Director, instant issuance, canaDa, DatacarD GrouP

20 November / December 2012 PAYMENTSBUSINESS

adapt to gain market share and differentiate themselves.

new revenue driver: instant issuanceThe traditional model for centralized credit and debit card issuance is well established. Larger issuers tend to build efficient, high-volume operations and distribute cards through the mail after consumers have successfully completed application processes for new or replacement cards. Small issuers tend to outsource their programs to high-volume service bureaus and follow the same general “centralized” process.

From end-to-end, the process of personalizing and mail cards, assigning PINs and activating cards typically takes five to seven days. A recent study, however, shows that Canadian consumers believe the process takes about three weeks. This perception heavily affects which cards consumers apply for activate and use.

Forward-thinking card issuers in Canada and other markets have recognized this consumer perception and used it to drive new instant issuance strategies in recent years. With instant issuance, consumers walk into the branch and provide application information to a staff member.

Applicant information is entered into a software program that drives both the approval process and card personalization. In a matter of minutes, customers can walk out of the branch or retail location with permanent, ready-to-use financial cards. Cards are highly personalized, unlike typical vault cards, which

tend to be generic. Instead of waiting days or weeks, cardholders get immediate purchasing power and personalized cards.

Instantly issued and personalized cards have shown to have much higher activation rates, higher usage rates and greater appearance at the “top of the wallet.” In fact, virtually every personalized card issued is instantly activated, compared with an industry average of less than 59% for mailed cards. The ability to use cards instantly also greatly improves on the average industry usage rate of less than 39%. These critical metrics can help banks drive new revenue that may have been lost in recent years due to drops in checking and interchange fees.

In addition to securing more card-based transactions, instant issuance also helps issuers capture fees from payments that would otherwise have been made with cash or checks. Making cards convenient, personalized and top-of-mind encourages consumers to use them as their primary payment platforms.

The desktop card printing systems used for instant issuance make it possible to issue cards with customized backgrounds. Customers can provide service representatives with personal photos or other artwork, which can be quickly scanned and used as the primary card background. Customers are often willing to pay $5-$10 for these customized cards. Photo cards also tend to rise to the top of the wallet. Statistics show much higher activation and usage rates for personalized photo cards.

Benefits of instant issuancerevenue increase

Improved activation rates (up •to 14%)Growth in transaction •volume (up to 50%)Instant use fee increase (up •to $400)Custom card or photo card •fees (up to $15)

portfolio lift Average balance increase (up •to 10%)Customer retention rate •increase (up to 3%)Cardholder acquisition rates •(up to 15%)Cross-selling of additional •products and services

Cost reductionFewer cards lost in the mail•Reduction in paper, handling •and postageLower card inventory costs•Reduced card pre-printing •costs

Secure and scalable infrastructuresThe central and instant issuance processes share many elements, including security protocols. This allows issuers who already have central issuance infrastructures in place to simply expand and add instant issuance at the branch or store level. There is typically little or no special training required for IT staffs or customer service representatives.

In most deployments, approval is virtually instant. Consumers typically choose a card design, which can include personal photos, co-branded logos and other meaningful elements. Ready-to-use, fully activated cards are printed instantly and handed directly to the consumer. Information is retained in the system in

the event replacement cards are needed. Consumers are immediately able to use their permanent cards to make purchases or withdraw cash from ATMs.

The flexibility of instant issuance infrastructures — or hybrid issuance models — allows for fast, affordable and secure issuance of a wide variety of card types, including debit, credit, prepaid, ATM and gift cards. A variety of issuance technologies allow for embossed or flat (unembossed) cards and EMV™-compliant smart cards. Inline color printing capabilities even allow cardholders to choose custom backgrounds, including their own photos or artwork.

Advanced instant issuance infrastructures also allow issuers to enter the mobile payment era. NFC-enabled microSD cards can be personalized instantly or over the air with some infrastructures. This allows banks to turn customer smartphones into mobile payment devices. These capabilities are critical, as some experts predict that more than 80% of all smartphones in Canada will be NFC-enabled by 2016.

Benefits beyond revenue generationInstant issuance helps minimize costs, maximize revenue, increase activation rates and enhances usage levels, as well as gain top-of-mind/wallet brand recognition. In addition, it also offers these benefits:

improved customer experience: Customers receive cards immediately and use them right away. The ability to offer custom card designs

FeATUre

21 November / December 2012 PAYMENTSBUSINESS

— including backgrounds that feature the cardholder’s own photos or artwork — add to the overall experience and provide significant differentiation for issuers.

Competitive advantage: “How” banks and retailers issue cards is becoming the strongest point of differentiation in a crowded market. Consumers are looking for products and services that align with their lifestyle. They want speed, customization and value. In fact, customers are often likely to trade loyalty for these attributes.

Cross-selling: Because the instant issuance process is conducted in-person, service representatives have new opportunities to strengthen personal relationships with customers and cross-sell additional products and services.

product versatility: Instant issuance models accommodate multiple payment schemes, including Visa®, MasterCard®, American Express®, and Interac® bank cards. They provide complete personalization at the branch location that includes full name, expiry date, CVC code, graphics, custom photos and optional EMV®-compliant card personalization.

lower issuance costs: Instant issuance eliminated many of the traditional costs associated with card programs. Cards delivered instantly require no mail packages, postage or mail handling. Also, card pre-printing and inventory costs are greatly decreased. Desktop printing technologies allow banks and retailers to use blank or very simply preprint card stock to issue multiple

card types. Card design elements that were once part of the long and expensive pre-printing process can now be managed on demand.

piN selection: A global consulting firm recently revealed results from a study that indicates EMV®-compliant cards are likely not to be activated or used if there is any PIN confusion on the part of the cardholder. Instant issuance allows cardholders to determine their own PINs and select them as they receive their cards. This results in higher activation rates and increased card usage.

emergency card replacement: Instant issuance directly addresses the issue of replacement cards being stolen in the mail — and it allows customers to get cards without waiting days or weeks for the central issuance process. This improves customer satisfaction and reduces issuance costs.

enhanced security: Data encryption technologies and a host of physical and logical security features make the instant issuance process fully compliant with security requirements of Visa®, MasterCard® and other institutions. These technological benefits — along with the reduced risk of cards being lost or stolen in the mail — measurably improve security outcomes for card issuers.

reporting and management tools: Instant issuance software typically includes a variety of custom and standard reporting tools that provide issuers with strategic insights into their card programs. In addition to providing complete audit trail information, these reports allow senior leaders to view

important consumer trends and behaviors.

Instant issue implementation recommendationsWhen considering an instant issuance system, it is important for financial institutions to consider their particular needs, as well as whether the package would integrate easily into their existing backend systems. They should look for an enterprise-type system with single-server control for multiple desktops and seamless connection to host networks. The solution should be easy to implement at the branch level, while offering robust reporting, monitoring and security tools for the management team.

Datacard® solutions have helped issue over five million smart cards everyday world-wide. We understand the drivers and best practices for eMv-compliant and chip card imple-mentations, and have success-fully implemented in over 200 card production environments for eMv-compliant programs. our smart card experts can help simplify the smart card issuance process with proven solutions and our broad port-folio of smart card issuance solutions can accommodate the unique needs and specific busi-ness strategies for any card program — including scalable, flexible hardware, software, supplies, consultation and project management. Best of all, our solutions are fully tested and integrated to ensure seamless operations.

You do everything else through your smart phone, why not process a sale?

❱ speed, efficiency, and reliability all at your figure tips

❱ now with live access to your accounting data

For more information please contact Marc Cashman: (613) 221-5950 or marc.cashman @ wirelessmerchant.comor visit: www.wirelessmerchant.com

FeATUre

22 PAYMENTSBUSINESS November / December 2012

ONE ON ONE

Dan Kelly, President and chief executive officer for the cFIb talks to Payments Business about why the Debit and credit code of conduct was a landmark victory for small businesses in canada and what changes have to happen in 2013 for it to stay relevant and effective.

23 November / December 2012 PAYMENTSBUSINESS

By aMy Bostock

pB: Why did the cfiB feel that the payments industry needed a code of conduct?dk: For decades the situation in the Canadian payments world was reasonably stable with nothing particularly troublesome on the payments side from a merchant perspective. People accepted that costs were what they were and they moved on.

Then about two years ago when credit card companies started offering premium cards with higher merchant fees, all heck broke loose and I think that the credit card industry lost the trust of merchants who didn’t understand why fees were increasing. There was a black hole of transparency.

pB: What was the impetus behind creating the current credit and Debit card code of conduct?dk: We [CFIB] learned that there were plans to bring some negative practices to the debit card side of the industry – very advanced plans by VISA and MasterCard to get in to the debit business. We were very worried that we would loose the competitive advantage that Canadian merchants have if these practices came into being. And because of the bad blood on the premium credit card side and the threat on the debit side [to merchants] the CFIB decided to look at ways that we, as an organization, could help to address this mess.

We had worked on a voluntary

ONE ON ONE

“ at First tHere Was stronG oPPosition

– tHey DiDn’t Want a sMall Business GrouP tellinG tHeM WHat to Do in tHeir inDustry.

24 November / December 2012 PAYMENTSBUSINESS

code of conduct for the banking industry and that seemed to work quite well so we thought that might be a good tool to bring as a suggestion to Minister of Finance Jim Flaherty as a means of addressing it.

We didn’t want our first move to be an attempt to regulate prices or put caps in place so we thought a volun-tary code of conduct would be able to address what we saw as unfair practices in the credit and debit card industries.

pB: Did the canadian government support your initiative?dk: We put forth a draft to the government who ultimately came back with their own draft of practices to be put in place which was brought for consultation with the industry as a whole. Minister Flaherty said that if the industry didn’t accept it voluntarily that he would make it involuntary. Ultimately we didn’t get everything that we wanted but we got a lot of solutions to bad practices.

pB: how did the credit and debit card industry respond to the code of conduct?dk: At first there was strong opposition – they didn’t want a small business group telling them what to do in

their industry. Over time the industry seemed to get its head around it and I think that the smart thing that Minister Flaherty did was show them that although they may not love the Code, they would like it a lot better than if he were to step in and start to regulate. It really is a less negative result for the industry than it could have been and has been in other countries. For example in Australia merchant fees were capped and in Europe fees are regulated. Even in the U.S. there has been some corralling of debit card fees.

pB: What would you say was the best thing to come out of this code for merchants?dk: Quite frankly I think the biggest accomplishment of the Code was that it actually slowed down VISA and MasterCard’s push to get into in-store debit in a very sneaky way. Prior to the Code they had both announced plans to get into in-store debit by piggybacking in Interac. They were going to have a card with both Interac and VISA/MasterCard debit – depending on the store’s capabilities – and we felt that this was very unfair. We didn’t want to block them from getting into debit but we didn’t think that they should use their competitor to do it.

pB: can you talk abut the competition Bureau’s case currently before a competition tribunal and how it relates to the code?dk: Two of the biggest things we asked for in the Code are actually the subject of this case. The first is powers for merchants to push back against premium credit cards and rising fees. We want them to have the right to refuse certain cards – no more ‘honour all cards’ rule. The other point relates to a prohibition on surcharging – we believe that merchants should be allowed limited access to surcharging.

Minister Flaherty didn’t add these two things to the Code but the Competition Bureau later came out and said that they are, in fact, anti-competitive. They have taken VISA and MasterCard to the Competition Tribunal and they are set to rule any day now.

pB: after two years, what changes do you feel are now necessary in order to keep the code relevant and effective?dk: Since the Code has come into being, there are some emerging gaps that need to be addressed. Things that couldn’t have been contemplated when the Code was initiated. Because of developments in the industry, there are two elements that CFIB feels need to be addressed. The first deals with processor practices and some unethical practices by processors who are skirting the Code to trap small businesses into terrible deals.

The second change pertains to mobile payments. We want to make sure that

merchants have the ability to say no. There’s a lot of emerging technology in this space and we’re seeing some backdoor attempts to push merchants into accepting mobile payments. We feel this is bad a practice so we want new technology to require express consent on the part of the merchant before it is implemented.

But the bigger worry we have is with respect to mobile wallets. We are not opposed to digital wallets but we want to make sure it’s consumers who are choosing which payment they use from the numerous possibilities in their digital wallet and that merchants can choose which options they put on offer. What we don’t want are default settings by tech providers that pushes payment to the highest cost payment option in the digital wallet.

pB: What is on cfiB’s agenda for 2013?dk: The big news will be the result of the tribunal. Beyond that we will be dealing with the fallout of the crushing fee increase that VISA has announced. They have announced three price hikes – an across the board fee increase for assessment fees, a foreign card transaction fee and an new ‘uber-premium’ card in Fall 2013. We’ll be keeping an eye out for possible copy-cat action by MasterCard. Finally, we’ll be planning for mobile.

Minister Flaherty has already announced a review of the Code and has a group looking at updates. We’re expecting to see these updates in early 2013.

ONE ON ONE

“ since tHe coDe Has coMe into BeinG, tHere are soMe eMerGinG GaPs tHat neeD to Be aDDresseD.

tHinGs tHat coulDn’t Have Been conteMPlateD WHen tHe coDe Was initiateD.

November / December 2012 PAYMENTSBUSINESS 25

To learn more call Paul DeRosse, Senior Vice President, Sales at 905.530.2351 or visit www.apriva.com.

SECURE DEVICES | RELIABLE SERVICE | EXCEPTIONAL SUPPORTApriva is North America’s Leading Wireless Gateway.

secure payment solutions

secure payment solutions emv & nfc consulting

carD manufactures integrateD payments solutions

creDit unions

Secure Solutions for Pay-ment & Identification

Toll Free: 1-800-387-9794 www.gi-de.com

Since 1852, G&D has been an integral partner that is solutions orientated and trusted by banks, governments and carriers. Our solutions are founded on trust, integrity and the creation of value through Confidence.• Contact, Contactless and Dual-Interface Smart Cards • Mobile Payment • On-line Secure Authentication • Enhanced Card Identification

Integrated PaymentSolutions and Services

www.everlink.caToll Free: 1.866.388.0076

One of the most advanced and reliable payment delivery solutions

in financial services technology.

Ensure a successful NFC project with FIME’s consulting team!

see youR company name heReContact Mark Henry - [email protected] x 223

sERViCEDiRECtORy

26 November / December 2012 PAYMENTSBUSINESS

CuRRENCy

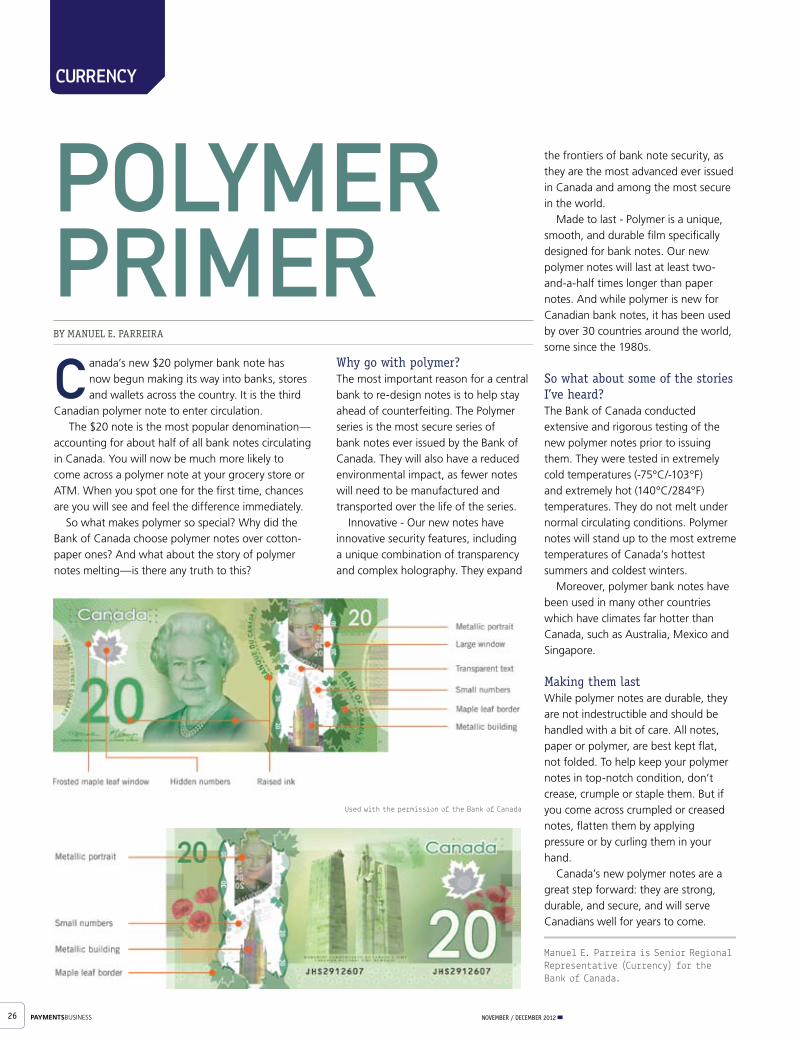

Why go with polymer?The most important reason for a central bank to re-design notes is to help stay ahead of counterfeiting. The Polymer series is the most secure series of bank notes ever issued by the Bank of Canada. They will also have a reduced environmental impact, as fewer notes will need to be manufactured and transported over the life of the series.

Innovative - Our new notes have innovative security features, including a unique combination of transparency and complex holography. They expand

the frontiers of bank note security, as they are the most advanced ever issued in Canada and among the most secure in the world.

Made to last - Polymer is a unique, smooth, and durable film specifically designed for bank notes. Our new polymer notes will last at least two-and-a-half times longer than paper notes. And while polymer is new for Canadian bank notes, it has been used by over 30 countries around the world, some since the 1980s.

So what about some of the stories I’ve heard?The Bank of Canada conducted extensive and rigorous testing of the new polymer notes prior to issuing them. They were tested in extremely cold temperatures (-75°C/-103°F) and extremely hot (140°C/284°F) temperatures. They do not melt under normal circulating conditions. Polymer notes will stand up to the most extreme temperatures of Canada’s hottest summers and coldest winters.

Moreover, polymer bank notes have been used in many other countries which have climates far hotter than Canada, such as Australia, Mexico and Singapore.

Making them lastWhile polymer notes are durable, they are not indestructible and should be handled with a bit of care. All notes, paper or polymer, are best kept flat, not folded. To help keep your polymer notes in top-notch condition, don’t crease, crumple or staple them. But if you come across crumpled or creased notes, flatten them by applying pressure or by curling them in your hand.

Canada’s new polymer notes are a great step forward: they are strong, durable, and secure, and will serve Canadians well for years to come.

Manuel e. Parreira is senior regional representative (currency) for the Bank of canada.

C anada’s new $20 polymer bank note has now begun making its way into banks, stores and wallets across the country. It is the third

Canadian polymer note to enter circulation. The $20 note is the most popular denomination—

accounting for about half of all bank notes circulating in Canada. You will now be much more likely to come across a polymer note at your grocery store or ATM. When you spot one for the first time, chances are you will see and feel the difference immediately.

So what makes polymer so special? Why did the Bank of Canada choose polymer notes over cotton-paper ones? And what about the story of polymer notes melting—is there any truth to this?

polyMer priMerBy MAnuEl E. PArrEIrA

used with the permission of the Bank of canada

readerboard

SUMMER ���� contactmanagement.ca ��

4 MAGAZINES DELIVER yourAUDIENCE in PRINT and ONLINEAccess more than 57,000 prospects authorizing and approving expenditures in theboardroom, on the front lines, in the IT corridors, in the centres of support and ful�illment,on the road with delivery, to create customer loyalty. Our readers link you to all theright executives and managers in FOUR KEY ROLES at the largestand fastest growing companies in Canada.

Lloydmedia, Inc, #302-137 Main St N, Markham, ON L3P 1Y2

ONLINENEospects authorizing and approving expenditures in the

and ful�illment, link you to all the

right executives and managers in FOUR KEY ROLES at the largest

TO ADVERTISE OR GET MORE INFORMATION AND MEDIA KITS 905-201-6600 | 1-800-668-1838 | Mark Henry x223 | Peter O'Desse x222

FUND Finance & Credit Prospects via CANADIAN TREASURERCT is published bi-monthly and reaches more than 10,000 readers, inabout 6,000 organizations, who are responsible for capital, credit andrisk in all forms of financial operations. Readers are in charge ofcorporate finances and how funding is approved, obtained, budgeted,loaned, processed, allocated, and distributed.www.canadiantreasurer.com

SELL Marketing & Sales via DIRECT MARKETINGPublished monthly since October 1988, DM is Canada's magazine for interactive marketingand sales, reaching about 17,000 readers in marketing and sales at about 6,400 organizations.Readers devise strategies, create campaigns, choose media, select tactics, implementprograms, track response, analyze results, measure ROI, and generate sales for their companies.www.dmn.ca

PAY Transactions & Billings via PAYMENTS BUSINESSPublished bi-monthly, PB reaches more than 20,000 readers in the transactions, cardsand ebilling/epayments sector at about 9,000 of Canada’s largest corporations includingbanks, credit unions, retailers and online sellers.www.paymentsbusiness.ca

SERVICE Customer Service, IT & Fulfillment via CONTACT MANAGEMENTCM is published quarterly and reaches more than 10,000 readers in about 5,000 callcentres across Canada. Readers manage all forms of customer interaction andengagement, including outsourcers who conduct those activities on behalf of their clients.www.contactmanagement.ca

TO ADVERTISE OR GET MORE INFORMATION AND MEDIA KITS905-201-6600 | 1-800-6681838 | Maria Kelebeev x221 | Peter O’Desse x222 | Mark Henry x223