26

The Rise of the Prosumers Technical Innovation & Regulatory Gap in the Global Power Sector Alejandro S. CORE [email protected] Washington, DC; July 1 st 2015 1

| Date post: | 16-Aug-2015 |

| Category: |

Economy & Finance |

| Upload: | alejandro-s-core |

| View: | 130 times |

| Download: | 4 times |

The Rise of the ProsumersTechnical Innovation & Regulatory Gap

in the Global Power Sector

Alejandro S. [email protected]

Washington, DC; July 1st 2015

1

Table of Content• Who are the Prosumers• Technical Innovation and Regulatory Gap• Why this Happens - The disruption• The Potential Solution• Opportunity for further research• What Next• References

2

Who are the Prosumers (1)• Producer and consumer: Marshall McLuhan and Barrington Nevitt

suggested in their 1972 book Take Today, (p. 4) that with electrictechnology, the consumer would become a producer.

• In the 1980 book, The Third Wave, futurologist Alvin Toffler coinedthe term "prosumer" when he predicted that the role of producersand consumers would begin to blur and merge (even though hedescribed it in his book Future Shock from 1970).

• In the 1982 book, The Energiewende “The Energy Transition”, theGerman Institute of Applied Ecology described the problems that theenergy transition faces in Germany and it proposed some solutionssuch as “One power plant per company/consumer” using Solar,Wind and Biogas energy.

• !n 2013, the Australian CSIRO (Commonwealth Scientific andIndustrial Research Organisation) introduced the Rise of theProsumers as one of their energy future scenarios for 2050, whereconsumers actively design or customise solutions.

3Here some examples from USA and Germany…

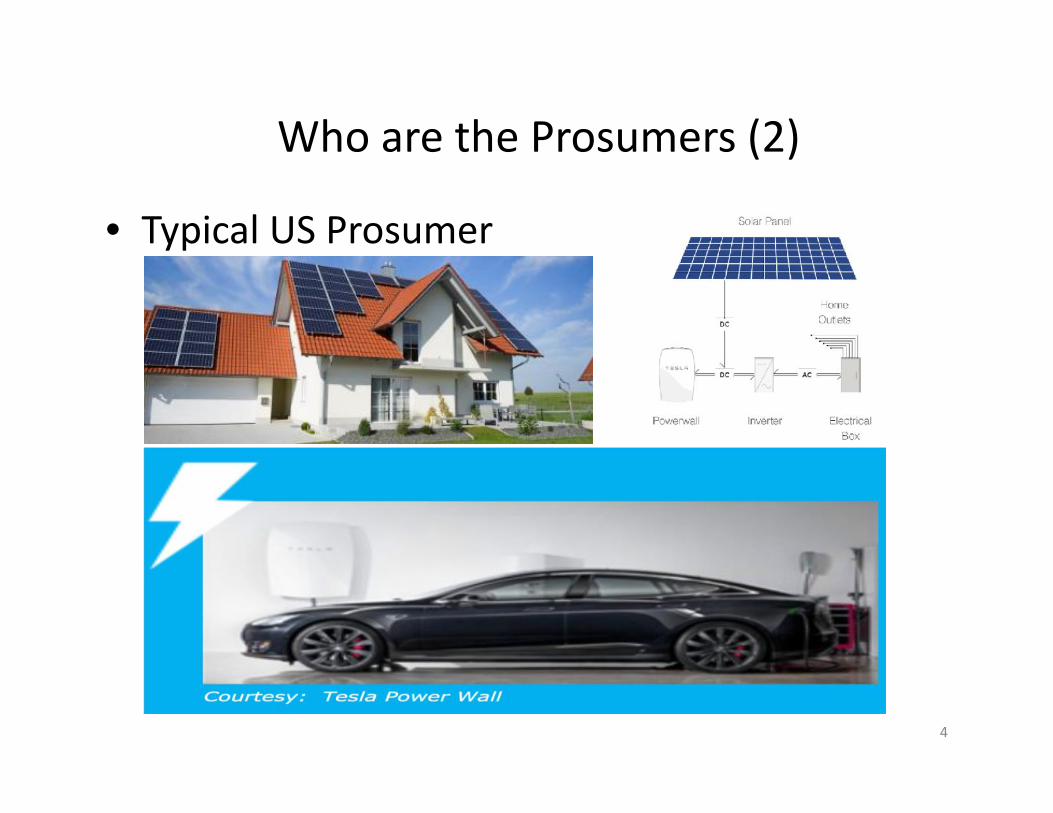

Who are the Prosumers (2)

• Typical US Prosumer

4

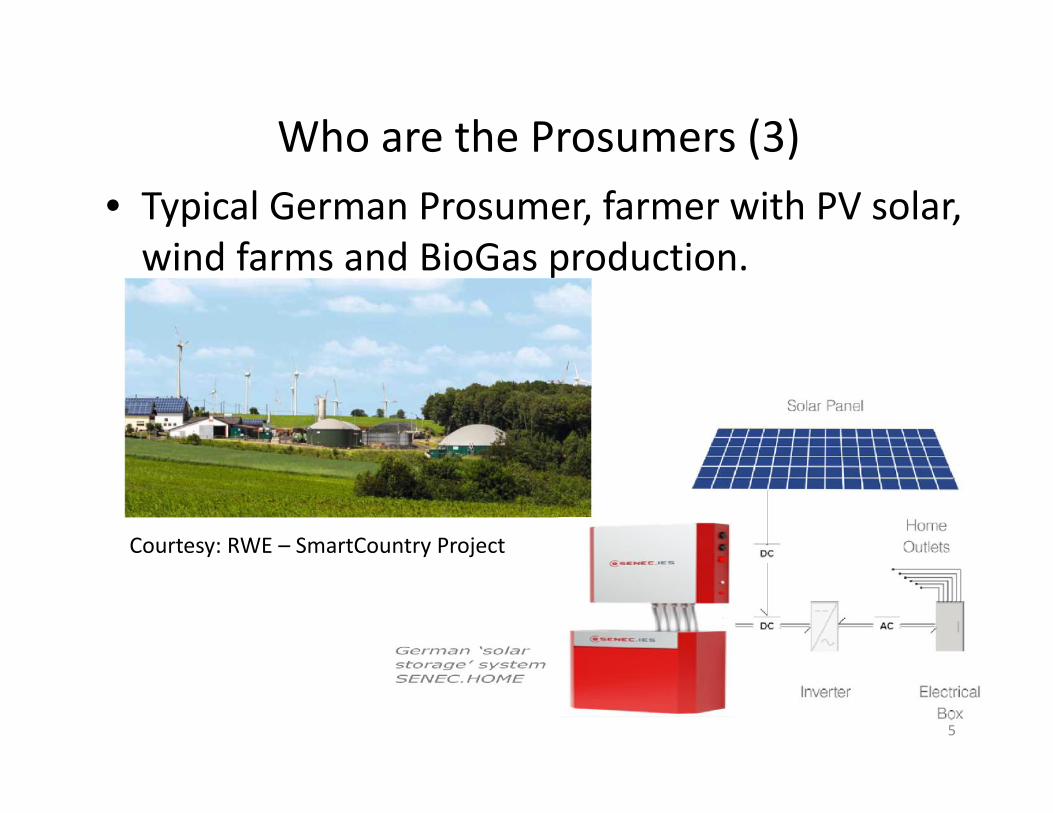

Who are the Prosumers (3)• Typical German Prosumer, farmer with PV solar,

wind farms and BioGas production.

5

Courtesy: RWE – SmartCountry Project

Technical Innovation and Regulatory Gap (1)

• Utility Business model has over 100 yrs Old…• 1980/Present - Attempts to reform utility

market• Recent technological advances, DERs (e.g. PV),

batteries and micro-grids – new businessmodels

• …Players providing consumers off-gridsolutions

• Fast growing of DERs Scheme worldwide

6DERs: Distributed Energy Resources

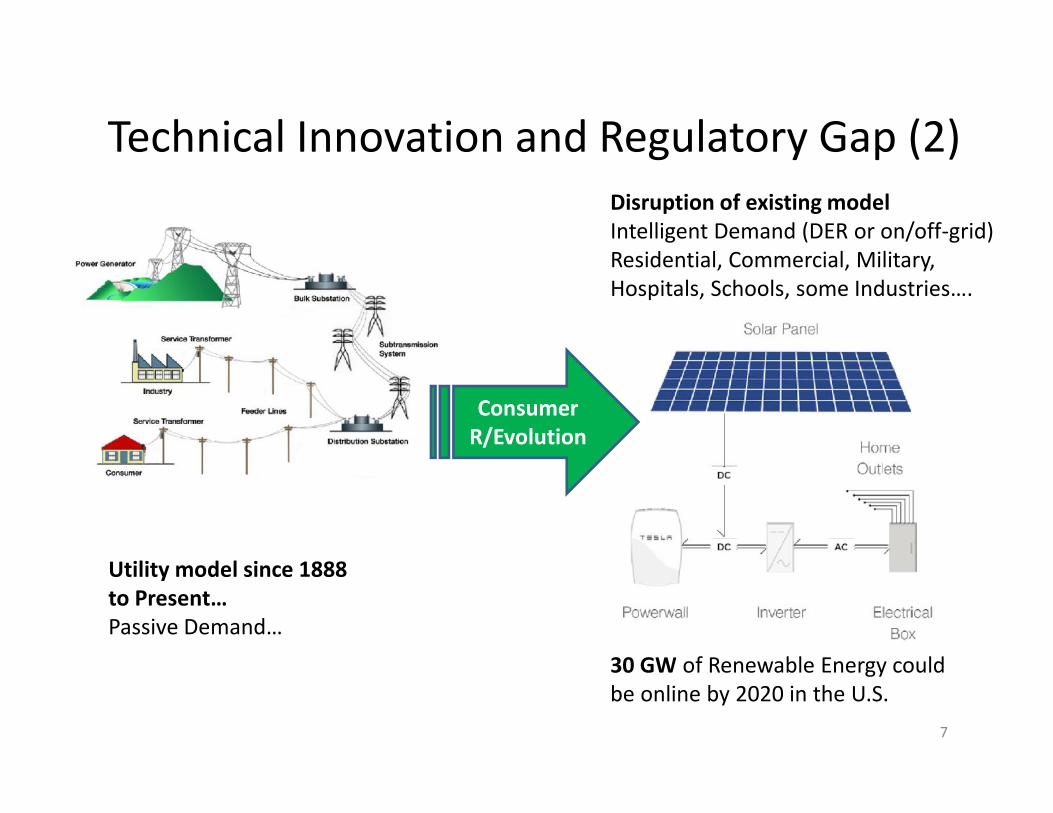

Technical Innovation and Regulatory Gap (2)

Utility model since 1888to Present…Passive Demand…

7

Disruption of existing modelIntelligent Demand (DER or on/off-grid)Residential, Commercial, Military,Hospitals, Schools, some Industries….

ConsumerR/Evolution

30 GW of Renewable Energy couldbe online by 2020 in the U.S.

…8

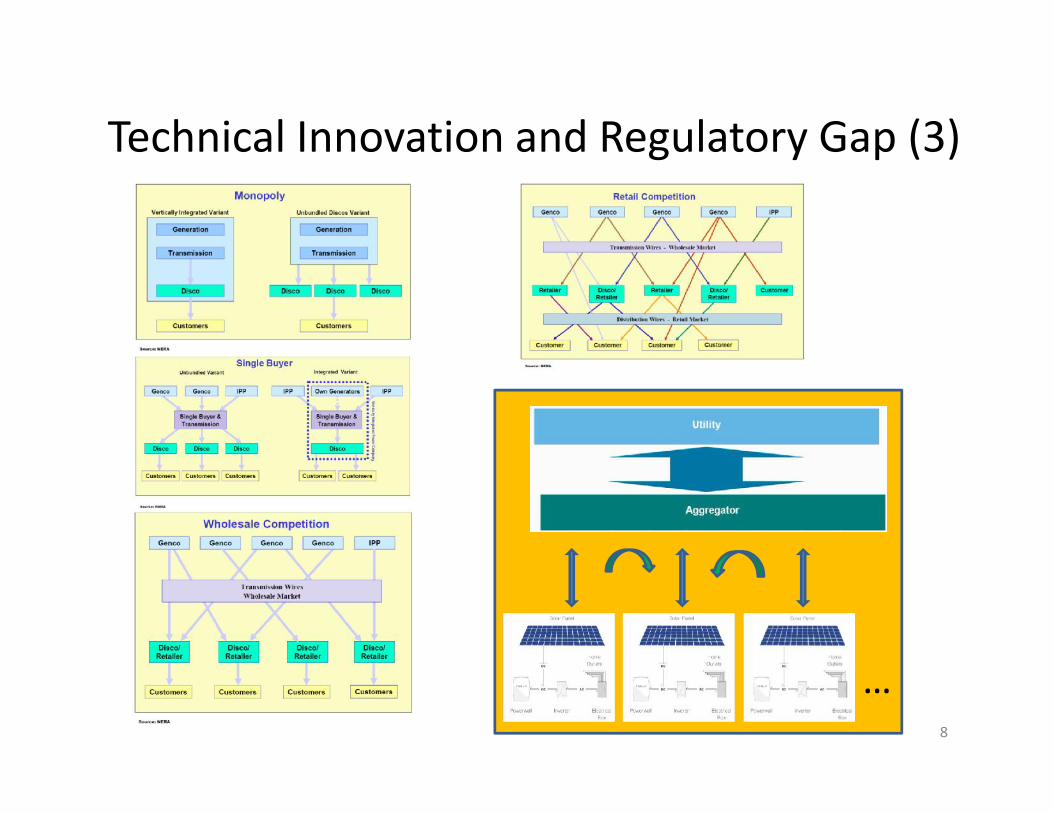

Technical Innovation and Regulatory Gap (3)

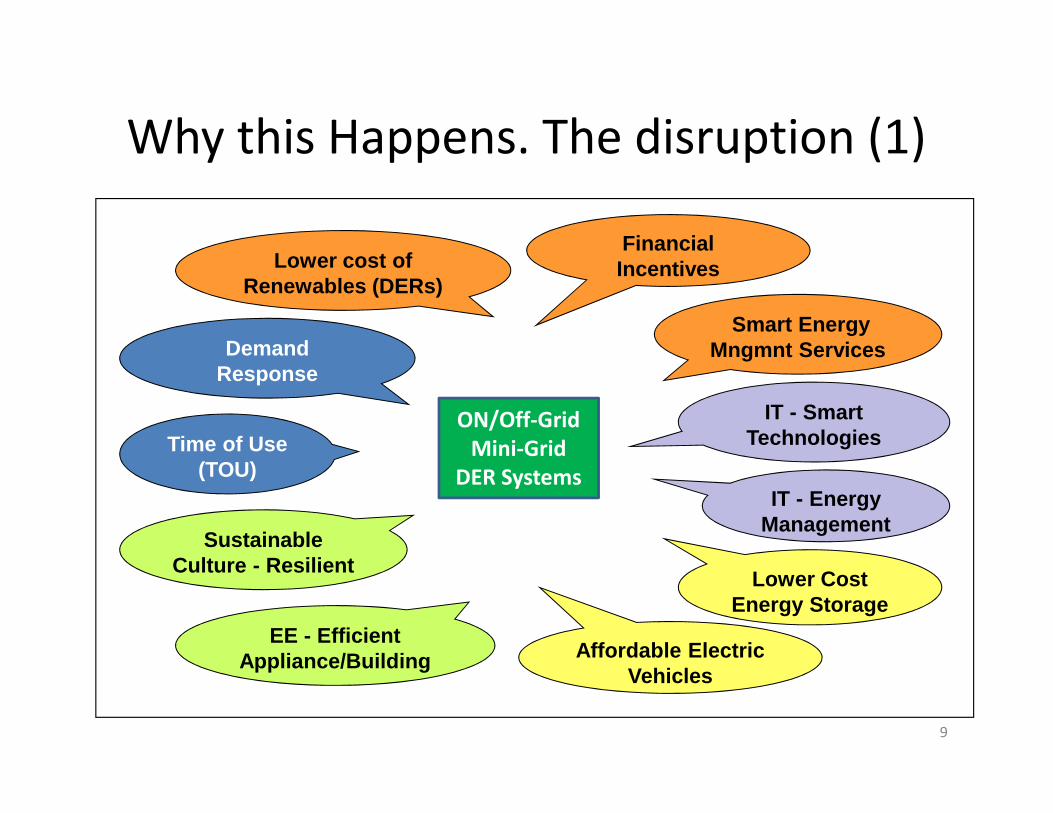

Why this Happens. The disruption (1)

9

Lower cost ofRenewables (DERs)

DemandResponse

FinancialIncentives

Smart EnergyMngmnt Services

Time of Use(TOU)

IT - EnergyManagement

IT - SmartTechnologies

Lower CostEnergy Storage

Affordable ElectricVehicles

SustainableCulture - Resilient

EE - EfficientAppliance/Building

ON/Off-GridMini-Grid

DER Systems

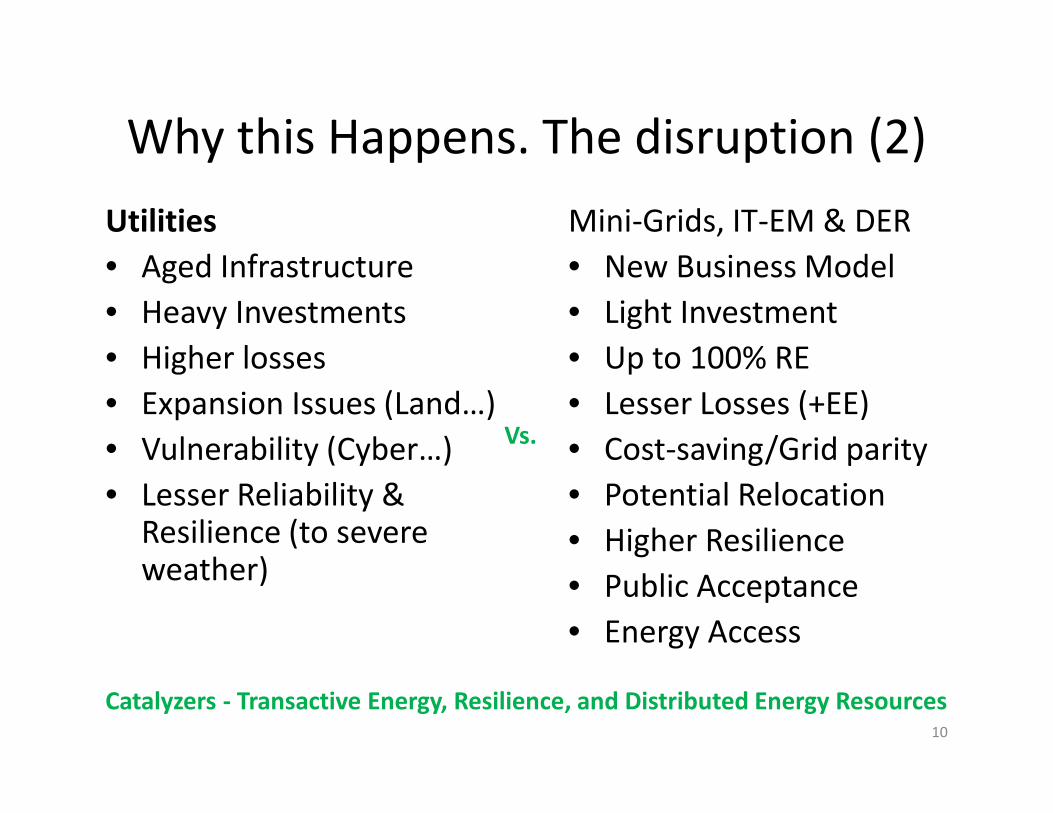

Why this Happens. The disruption (2)

10

Utilities• Aged Infrastructure• Heavy Investments• Higher losses• Expansion Issues (Land…)• Vulnerability (Cyber…)• Lesser Reliability &

Resilience (to severeweather)

Mini-Grids, IT-EM & DER• New Business Model• Light Investment• Up to 100% RE• Lesser Losses (+EE)• Cost-saving/Grid parity• Potential Relocation• Higher Resilience• Public Acceptance• Energy Access

Catalyzers - Transactive Energy, Resilience, and Distributed Energy Resources

Vs.

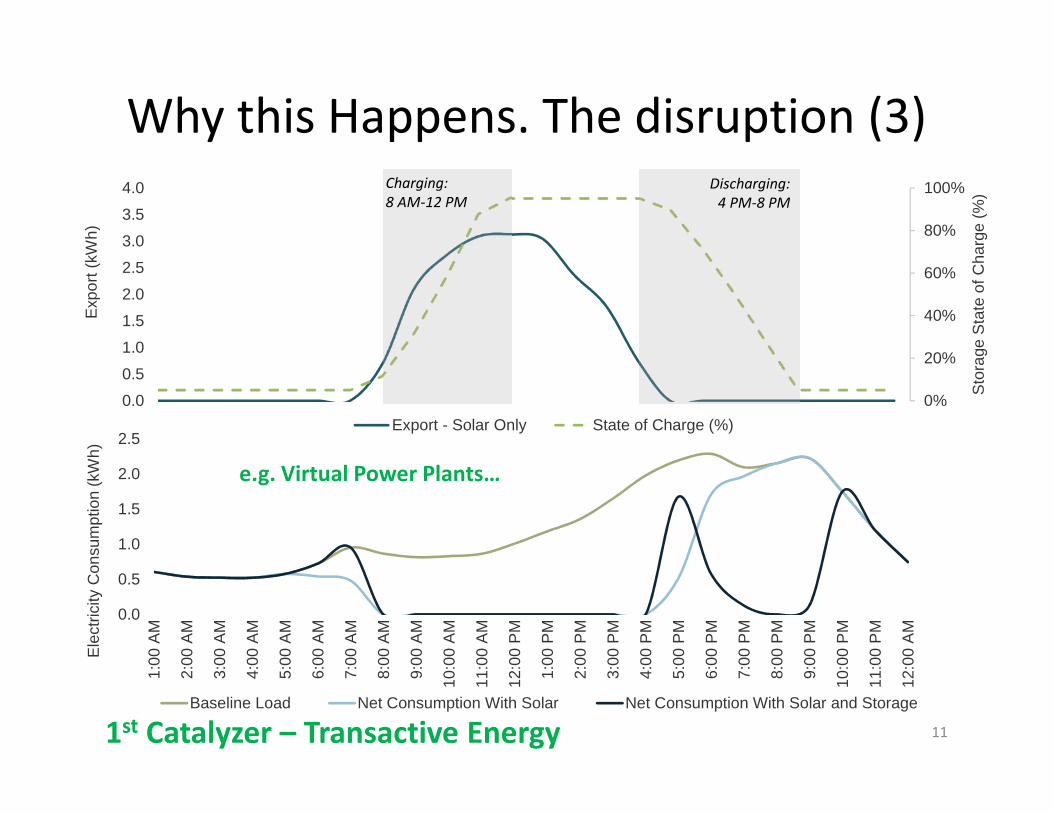

Why this Happens. The disruption (3)

1st Catalyzer – Transactive Energy 11

0.0

0.5

1.0

1.5

2.0

2.5

1:00

AM

2:00

AM

3:00

AM

4:00

AM

5:00

AM

6:00

AM

7:00

AM

8:00

AM

9:00

AM

10:0

0 AM

11:0

0 AM

12:0

0 PM

1:00

PM

2:00

PM

3:00

PM

4:00

PM

5:00

PM

6:00

PM

7:00

PM

8:00

PM

9:00

PM

10:0

0 PM

11:0

0 PM

12:0

0 AM

Elec

trici

ty C

onsu

mpt

ion

(kW

h)

Baseline Load Net Consumption With Solar Net Consumption With Solar and Storage

0%

20%

40%

60%

80%

100%

0.00.51.01.52.02.53.03.54.0

Stor

age

Stat

e of

Cha

rge

(%)

Expo

rt (k

Wh)

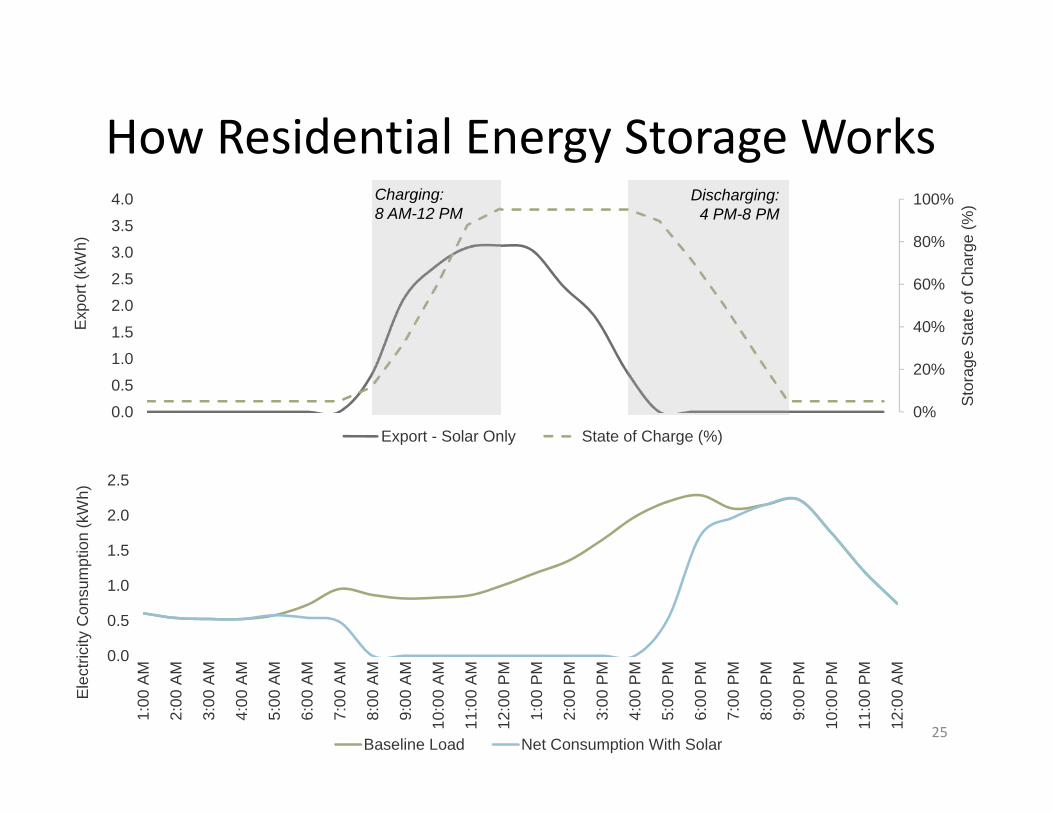

Export - Solar Only State of Charge (%)

Charging:8 AM-12 PM

Discharging:4 PM-8 PM

e.g. Virtual Power Plants…

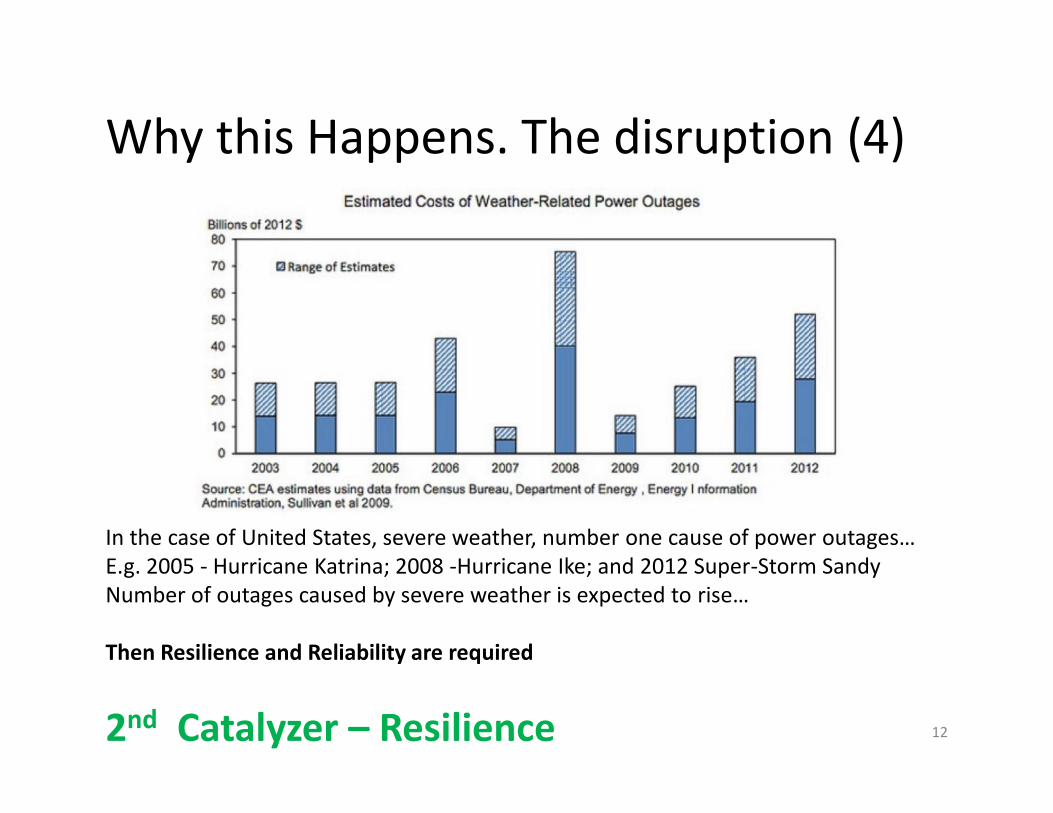

Why this Happens. The disruption (4)

122nd Catalyzer – Resilience

In the case of United States, severe weather, number one cause of power outages…E.g. 2005 - Hurricane Katrina; 2008 -Hurricane Ike; and 2012 Super-Storm SandyNumber of outages caused by severe weather is expected to rise…

Then Resilience and Reliability are required

Why this Happens. The disruption (5)Intelligent Demand is growing fast…(PV/DER)• China -> 110 GW by 2020 (IEA)• USA ~ Germany -> 50 GW/each by 2020 (IEA)• India ~ Italy -> 25 GW/each by 2020 (IEA)• …• SE4ALL Programme - Achieving 40% of universal

electrification by 2030…DERs…• OPEC Fund for International Development (OFID)

recent commitment, including DERs…

133rd Catalyzer – Distributed Energy Resources

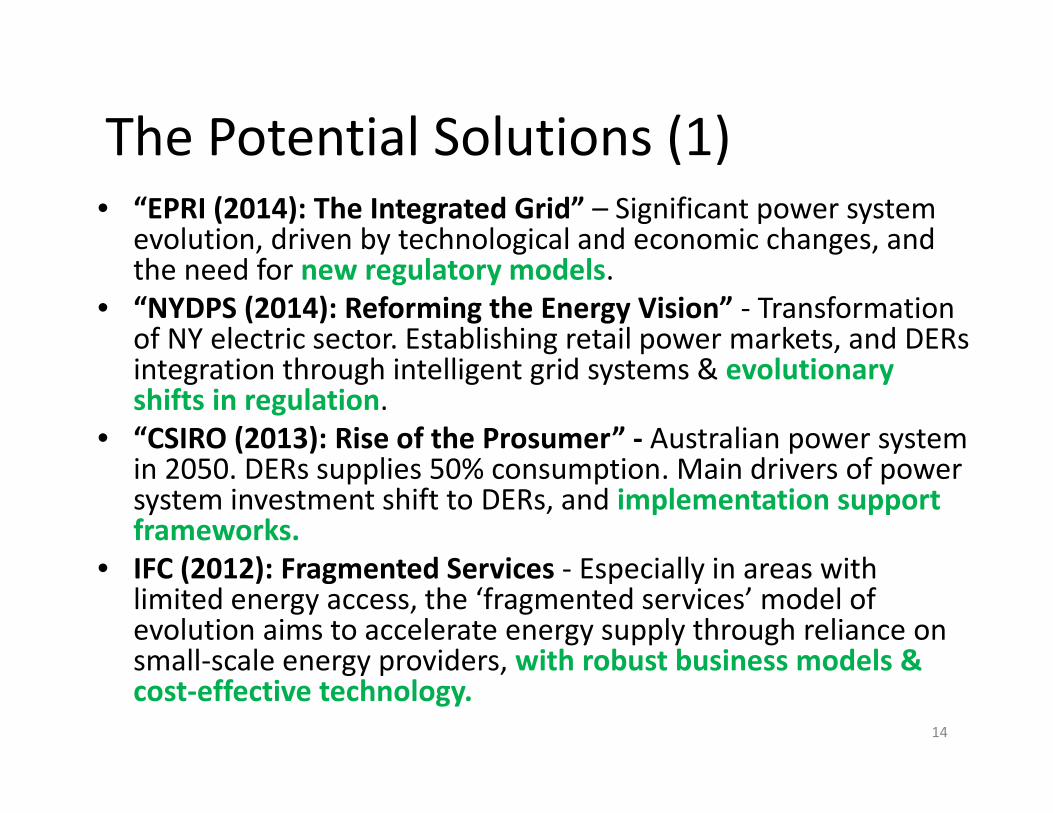

The Potential Solutions (1)• “EPRI (2014): The Integrated Grid” – Significant power system

evolution, driven by technological and economic changes, andthe need for new regulatory models.

• “NYDPS (2014): Reforming the Energy Vision” - Transformationof NY electric sector. Establishing retail power markets, and DERsintegration through intelligent grid systems & evolutionaryshifts in regulation.

• “CSIRO (2013): Rise of the Prosumer” - Australian power systemin 2050. DERs supplies 50% consumption. Main drivers of powersystem investment shift to DERs, and implementation supportframeworks.

• IFC (2012): Fragmented Services - Especially in areas withlimited energy access, the ‘fragmented services’ model ofevolution aims to accelerate energy supply through reliance onsmall-scale energy providers, with robust business models &cost-effective technology.

14

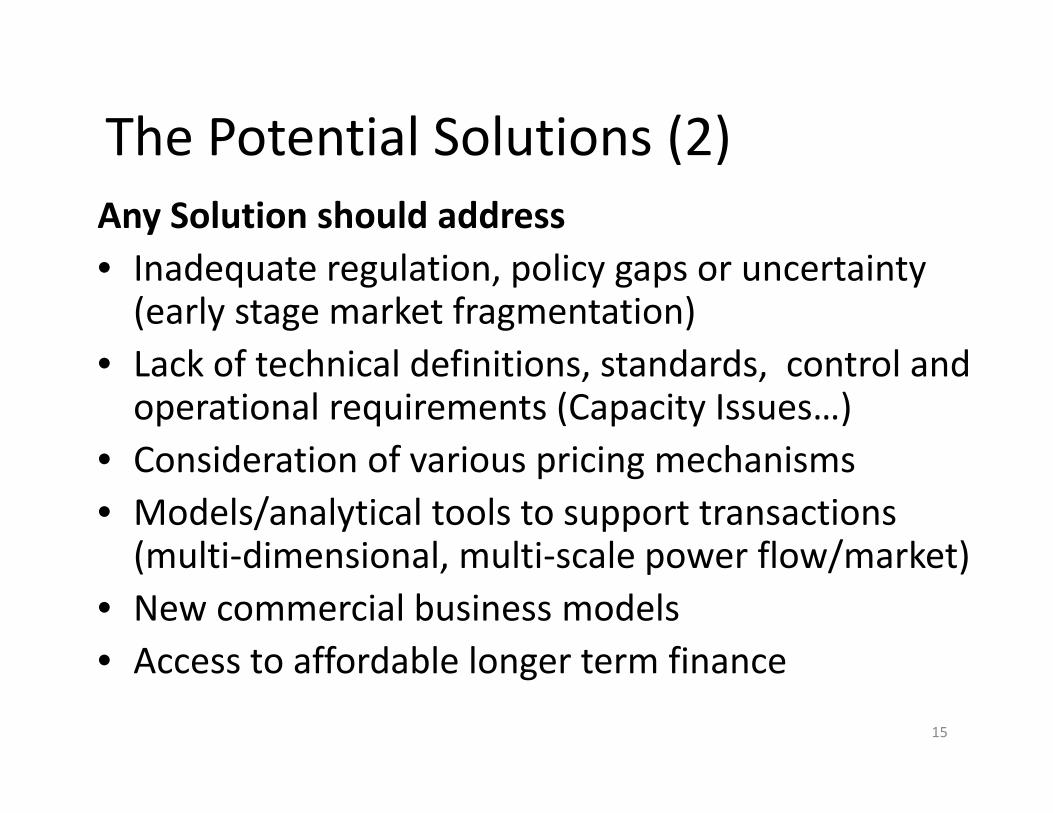

The Potential Solutions (2)Any Solution should address• Inadequate regulation, policy gaps or uncertainty

(early stage market fragmentation)• Lack of technical definitions, standards, control and

operational requirements (Capacity Issues…)• Consideration of various pricing mechanisms• Models/analytical tools to support transactions

(multi-dimensional, multi-scale power flow/market)• New commercial business models• Access to affordable longer term finance

15

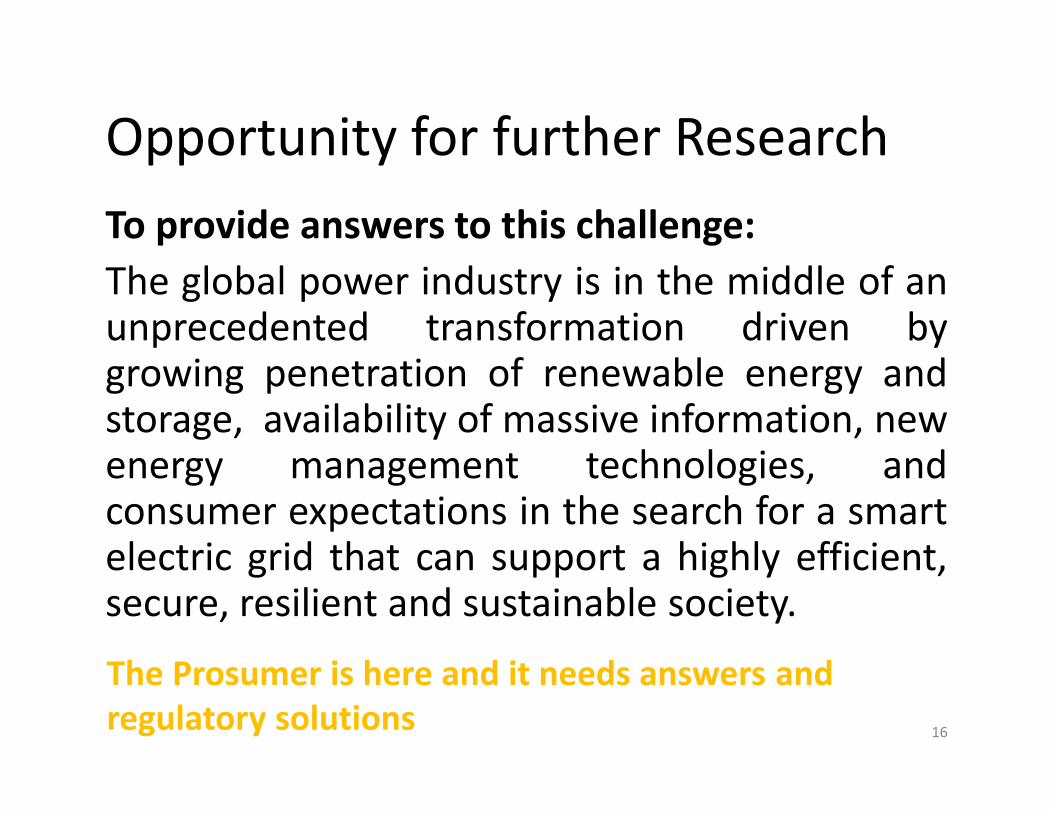

Opportunity for further ResearchTo provide answers to this challenge:The global power industry is in the middle of anunprecedented transformation driven bygrowing penetration of renewable energy andstorage, availability of massive information, newenergy management technologies, andconsumer expectations in the search for a smartelectric grid that can support a highly efficient,secure, resilient and sustainable society.

16

The Prosumer is here and it needs answers andregulatory solutions

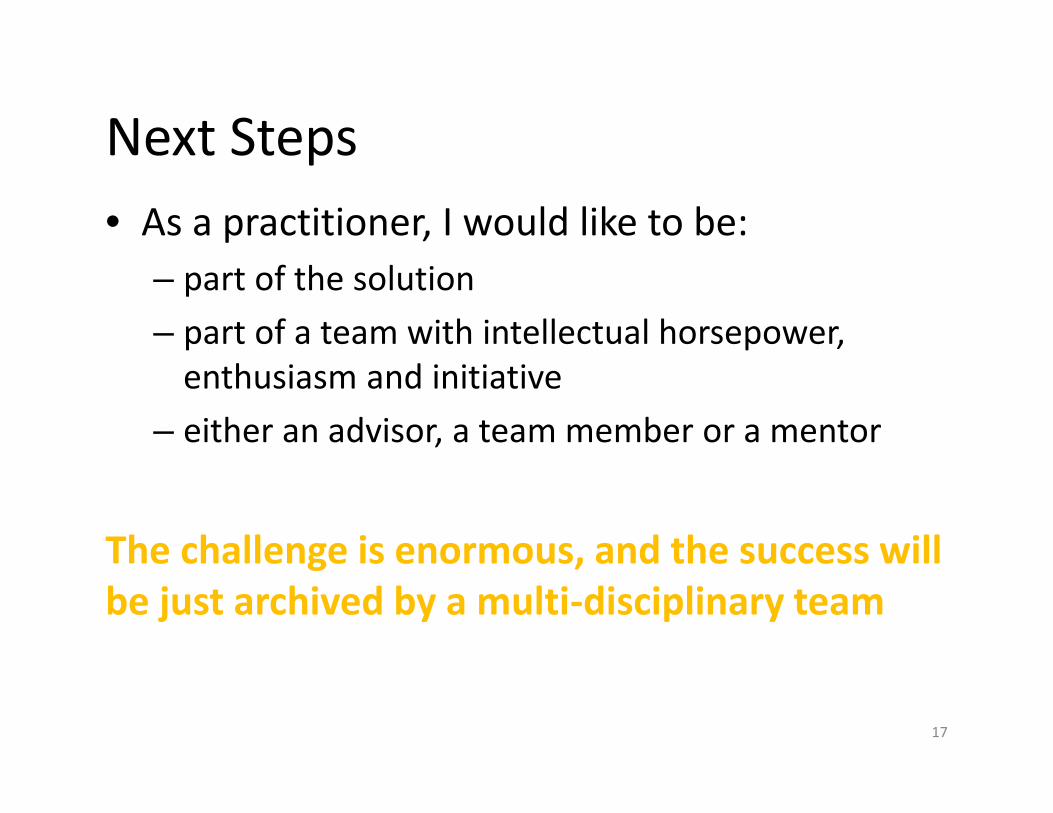

Next Steps• As a practitioner, I would like to be:

– part of the solution– part of a team with intellectual horsepower,

enthusiasm and initiative– either an advisor, a team member or a mentor

The challenge is enormous, and the success willbe just archived by a multi-disciplinary team

17

Thank youReferences (1)• Is Rooftop Solar Finally Good Enough to Disrupt the Grid? – HBR, May 2015• The future of solar energy – MIT, May 2015• Power Systems of the Future – NREL, February 2015• Sources of energy by households - Australia Bureau of Statistics, December 2014• Top 9 Things You Didn't Know About America's Power Grid – US DOE, November 2014• NIST’s Smart Grid Advisory Committee Report – US National Institute of Standards and

Technology (NIST), June 2014• From the Bottom Up, How Small Power Producers and Mini-Grids Can Deliver

Electrification and Renewable Energy in Africa – World Bank, 2014• Engineering IT-Enabled Sustainable Electricity Services, The Tale of Two Low-Cost Green

Azores Islands - Ilic, Marija et Al, Springer, 2013• Making Competition Work in Electricity – Hunt, Wiley, 2002• International Comparisons of Electricity Regulation – Cambridge University Press, 1996

18

References (2)• Wikipedia – accessed on Saturday June 27 2015 -

https://en.wikipedia.org/wiki/Prosumer• Craig Morris, and Martin Pehnt. “Energy Transition - The German Energiewende”. The

Heinrich Böll Foundation. Nov 2012 http://energytransition.de/wp-content/themes/boell/pdf/en/German-Energy-Transition_en.pdf

• CSIRO. “Change and choice - The Future Grid Forum’s analysis of Australia’s potentialelectricity pathways to 2050”. Dec 2013.https://publications.csiro.au/rpr/download?pid=csiro:EP1312486&dsid=DS13

• NYSPSC. “Reforming the Energy Vision”. Jun 2015.http://www3.dps.ny.gov/W/PSCWeb.nsf/All/26BE8A93967E604785257CC40066B91A?OpenDocument

• GTM Research. “Is the Power Secttor Ready for a New Phase of ComplementaryDisruption? - according to Steve McBee…”. June 2015.http://www.greentechmedia.com/articles/read/is-the-power-sector-ready-for-a-new-phase-of-complimentary-disruption

• GTM Research. “First Solar CEO: ‘By 2017, We’ll Be Under $1.00 per Watt FullyInstalled’”. June 2015. http://www.greentechmedia.com/articles/read/First-Solar-CEO-By-2017-Well-be-Under-1.00-Per-Watt-Fully-Installed

• Navigant Research. “Capacity of Distributed Generation is Expected to Double by 2023”.Dec 2014. http://www.navigantresearch.com/newsroom/the-annual-installed-capacity-of-distributed-generation-is-expected-to-double-by-2023

• Santiago Grijalva. “Research Needs in Multi-Dimensional, Multi-Scale Modeling andAlgorithms for Next Generation Electricity Grids”. Georgia Institute of Technology. Feb2011.

19

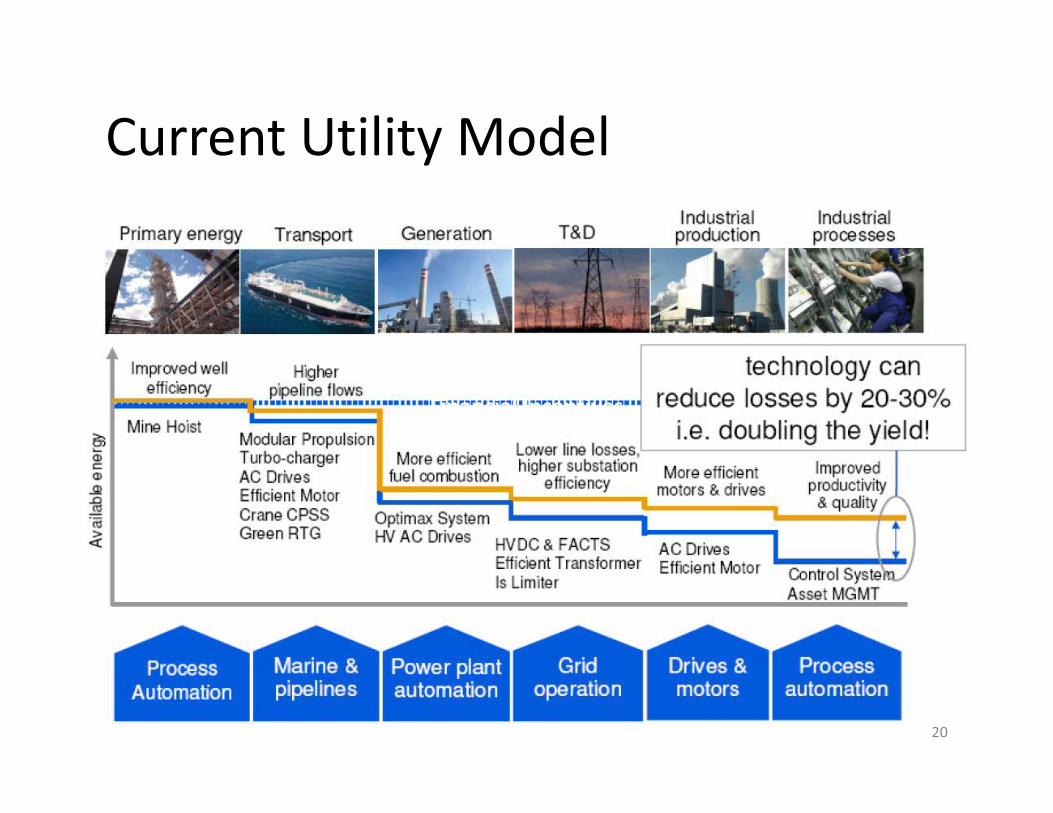

Current Utility Model

20

Financial Incentives

The disruption trendsCurrent 10 Trends• Renewable Energy Cost Reductions• Innovations in Data, Intelligence, and System Optimization• Energy Security, Reliability, and Resilience Goals• Evolving Customer Engagement• A Tale of Two Electricity Demand Forecasts• Increased Interactions with Other Sectors• Local and Global Environmental Concerns over Air Emissions• Energy Access Imperatives• Increasingly Diverse Participation in Power Markets• Revenue and Investment Challenges

21

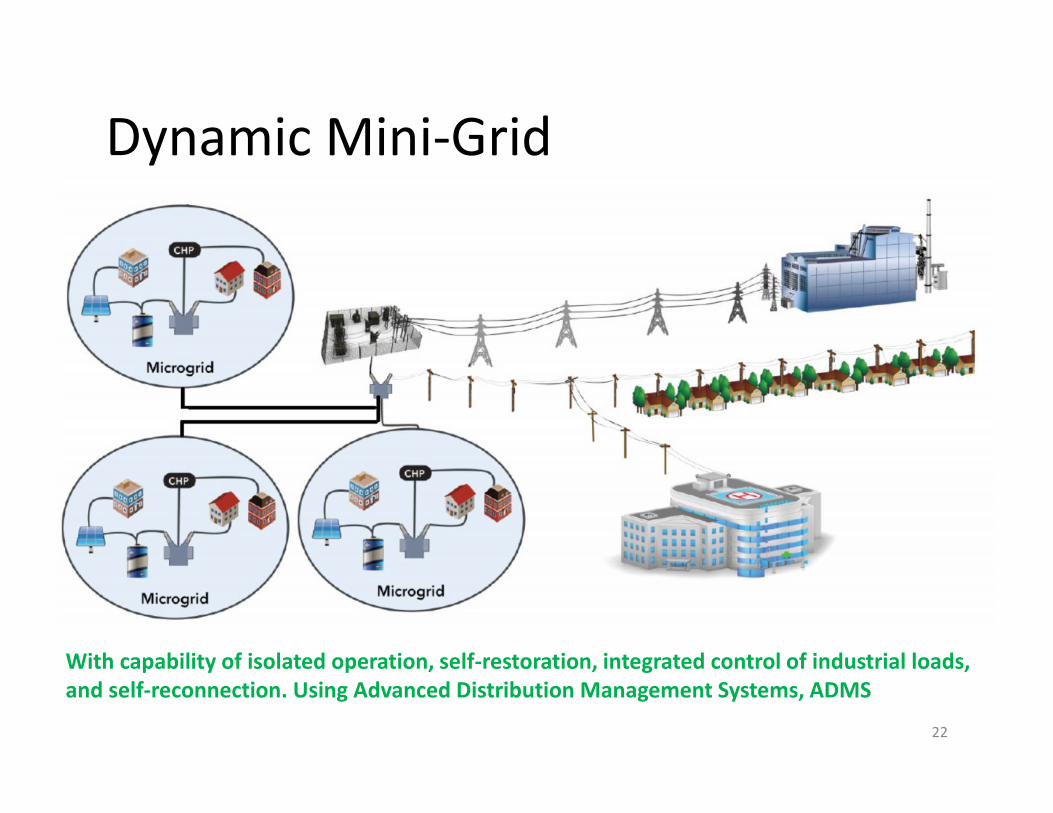

Dynamic Mini-Grid

22

With capability of isolated operation, self-restoration, integrated control of industrial loads,and self-reconnection. Using Advanced Distribution Management Systems, ADMS

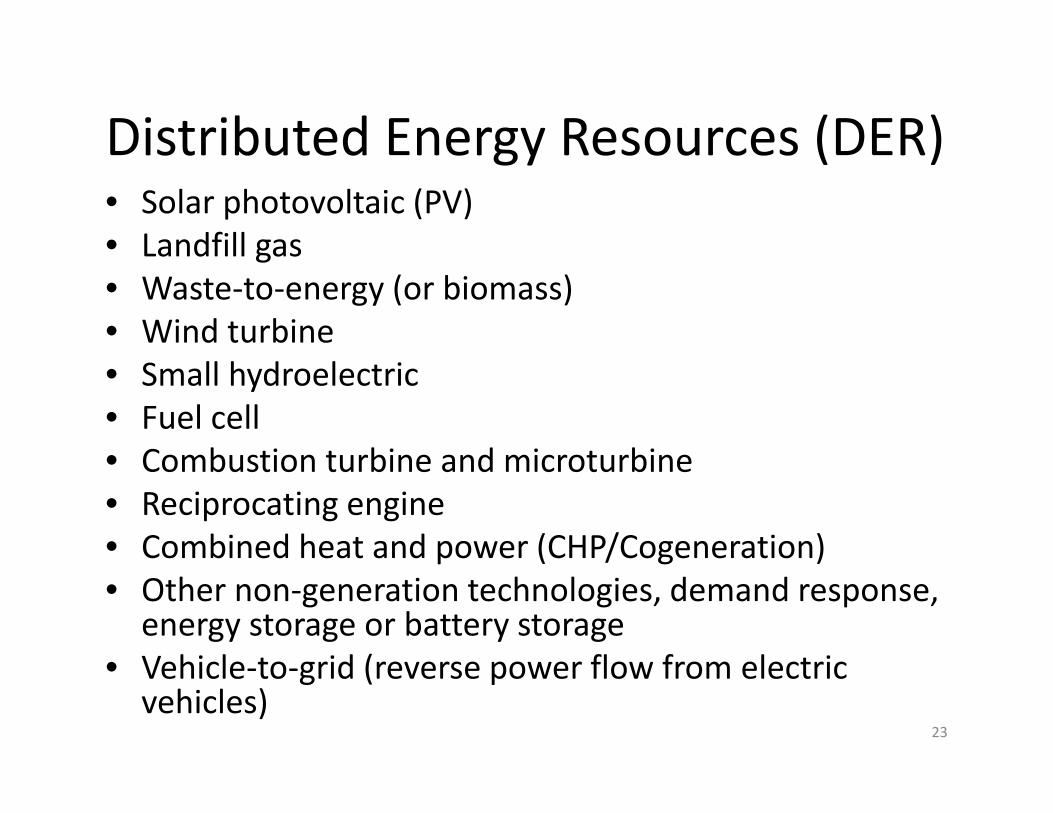

Distributed Energy Resources (DER)• Solar photovoltaic (PV)• Landfill gas• Waste-to-energy (or biomass)• Wind turbine• Small hydroelectric• Fuel cell• Combustion turbine and microturbine• Reciprocating engine• Combined heat and power (CHP/Cogeneration)• Other non-generation technologies, demand response,

energy storage or battery storage• Vehicle-to-grid (reverse power flow from electric

vehicles)23

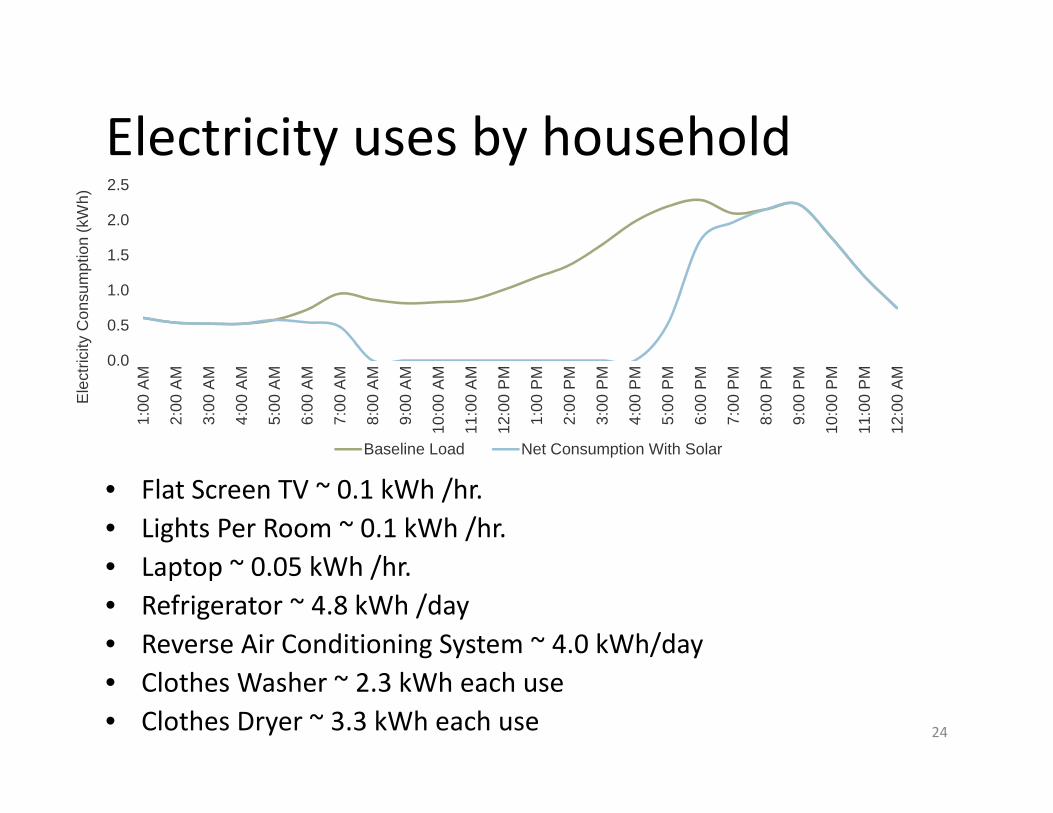

Electricity uses by household

• Flat Screen TV ~ 0.1 kWh /hr.• Lights Per Room ~ 0.1 kWh /hr.• Laptop ~ 0.05 kWh /hr.• Refrigerator ~ 4.8 kWh /day• Reverse Air Conditioning System ~ 4.0 kWh/day• Clothes Washer ~ 2.3 kWh each use• Clothes Dryer ~ 3.3 kWh each use 24

0.0

0.5

1.0

1.5

2.0

2.5

1:00

AM

2:00

AM

3:00

AM

4:00

AM

5:00

AM

6:00

AM

7:00

AM

8:00

AM

9:00

AM

10:0

0 AM

11:0

0 AM

12:0

0 PM

1:00

PM

2:00

PM

3:00

PM

4:00

PM

5:00

PM

6:00

PM

7:00

PM

8:00

PM

9:00

PM

10:0

0 PM

11:0

0 PM

12:0

0 AM

Elec

trici

ty C

onsu

mpt

ion

(kW

h)

Baseline Load Net Consumption With Solar

How Residential Energy Storage Works

25

0%

20%

40%

60%

80%

100%

0.00.51.01.52.02.53.03.54.0

Stor

age

Stat

e of

Cha

rge

(%)

Expo

rt (k

Wh)

Export - Solar Only State of Charge (%)

0.0

0.5

1.0

1.5

2.0

2.5

1:00

AM

2:00

AM

3:00

AM

4:00

AM

5:00

AM

6:00

AM

7:00

AM

8:00

AM

9:00

AM

10:0

0 AM

11:0

0 AM

12:0

0 PM

1:00

PM

2:00

PM

3:00

PM

4:00

PM

5:00

PM

6:00

PM

7:00

PM

8:00

PM

9:00

PM

10:0

0 PM

11:0

0 PM

12:0

0 AM

Elec

trici

ty C

onsu

mpt

ion

(kW

h)

Baseline Load Net Consumption With Solar

Charging:8 AM-12 PM

Discharging:4 PM-8 PM

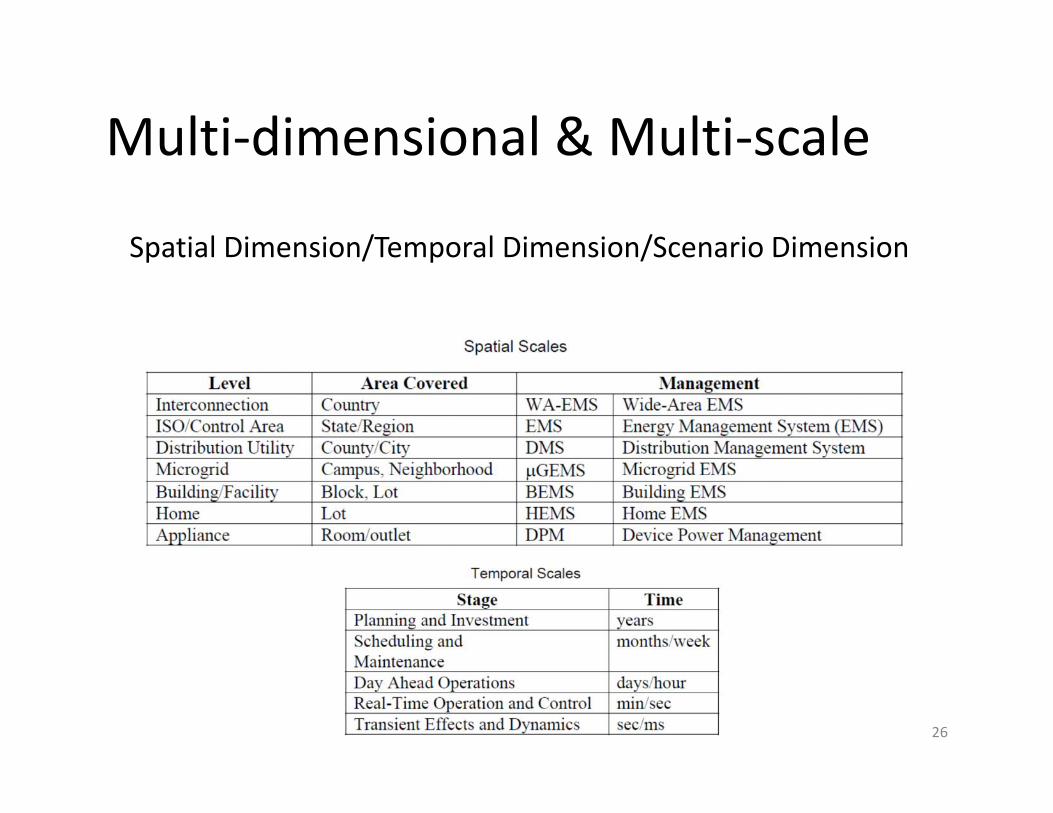

Multi-dimensional & Multi-scale

26

Spatial Dimension/Temporal Dimension/Scenario Dimension