45

Beach Energy Limited The road to future growth Euroz Conference, Rottnest Island 17 March 2010 1 Reg Nelson Managing Director

Beach Energy Limited

The road to future growth

Euroz Conference, Rottnest Island

17 March 2010

1

Reg Nelson

Managing Director

Disclaimer

• This presentation contains forward looking statements that are subject to risk factors

associated with oil, gas, geothermal and related businesses. It is believed that the

expectations reflected in these statements are reasonable but they may be affected by a

variety of variables and changes in underlying assumptions which could cause actual results or

trends to differ materially, including, but not limited to: price fluctuations, actual demand,

currency fluctuations, drilling and production results, reserve estimates, loss of market,

industry competition, environmental risks, physical risks, legislative, fiscal and regulatory

developments, economic and financial market conditions in various countries and regions,

political risks, project delays or advancements, approvals and cost estimates.

• All references to dollars, cents or $ in this presentation are to Australian currency, unless

otherwise stated. References to “Beach” may be references to Beach Energy Limited or its

applicable subsidiaries.

• Unless otherwise noted, all references to reserves and resources figures are as at 30 June

2009 and represent Beach‟s share.

Competent Persons Statement

• This presentation contains information on Beach‟s Reserves and Resources which have been

compiled by Mr Gordon Moseby, who is a full time employee of Beach, is qualified in

accordance with ASX listing rule 5.11 and has consented to the inclusion of this information in

the form and context in which it appears.

Compliance statements

2

Overview of Beach

Energy Limited

• Strategy

• Base business

• Growth potential

Positioning for long-

term growth

• What

• Where

• How

3

Today’s presentation

• 2P reserves of 66 MMboe

• Sustainable long-term oil and gas production

• FY 2010 production guidance of 8.0 MMboe

• $118 million cash and zero debt*

4

Beach Energy Limited (ASX : BPT): A compelling value proposition

* as at 31 Dec 2009

• Huge Cooper Basin shale gas resource potential

• High potential East African rift oil exploration acreage

• LNG supply potential from existing portfolio

• Track record of value creation

• Highly competent team

• Quality joint venture and strategic relationships

Strong base

business

‘Game changing’

long-term growth

potential

The right

people and

relationships

Corporate framework

5

• Consistent, targeted growth:

– Long-term cash flow, production and reserves

– Value driven investments

• Thinking ahead of the pack:

– Early entry, low risk, high return

– Participation in emerging technologies and opportunities

• Balanced portfolio:

– 60:30:10 risk profile

• Conservative and flexible balance sheet

• Invest in affordable low pollutant energy

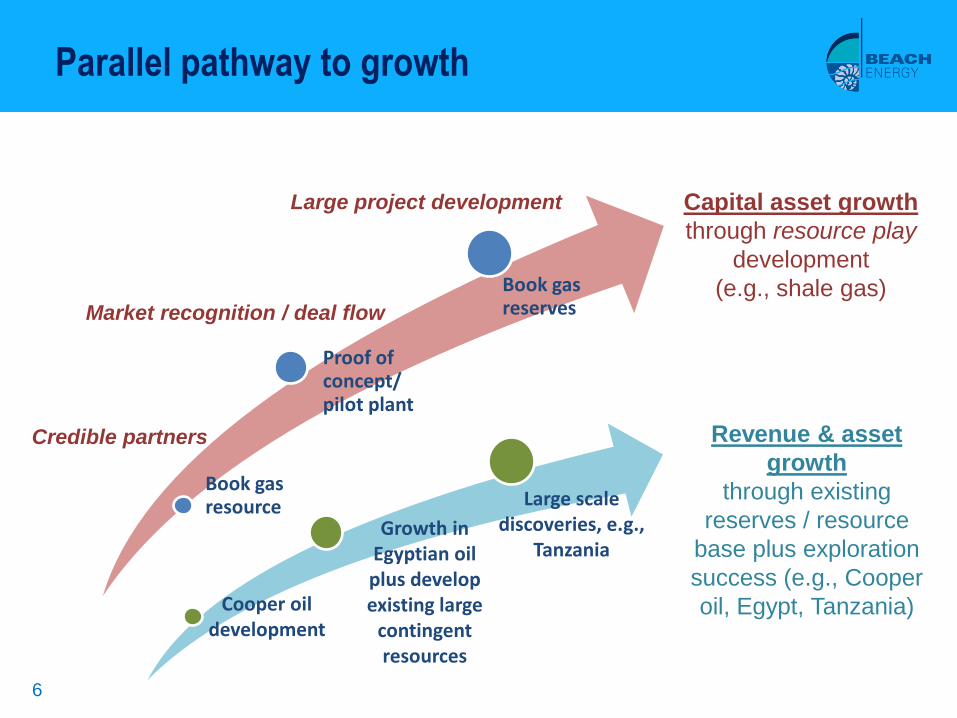

Parallel pathway to growth

6

Capital asset growth

through resource play

development

(e.g., shale gas)

Revenue & asset

growth

through existing

reserves / resource

base plus exploration

success (e.g., Cooper

oil, Egypt, Tanzania)

Book gas resource

Proof of concept/ pilot plant

Book gas reserves

Credible partners

Market recognition / deal flow

Large project development

Cooper oil development

Growth in Egyptian oil plus develop existing large

contingent resources

Large scale discoveries, e.g.,

Tanzania

Next two to five years

7

Exploration Growth

Oil & gas discoveries in Cooper with aim to add up to

20 MMboe new reserves

Develop opportunities in Egypt with aim to add up to 30+ MMbbl of new reserves

Drill high value targets, e.g., Barque prospect in New

Zealand, PNG targeting 100+ MMboe potential

Development Growth

Develop large contingent conventional gas resource of

approx. 500 PJ already booked in Cooper & elsewhere

Acquire producing or near producing assets suited to

Beach’s skills with a focus on upside potential

Assess and quantify large shale gas resource in Cooper Basin

Aim:Double

production &

reserves &

access high

value markets

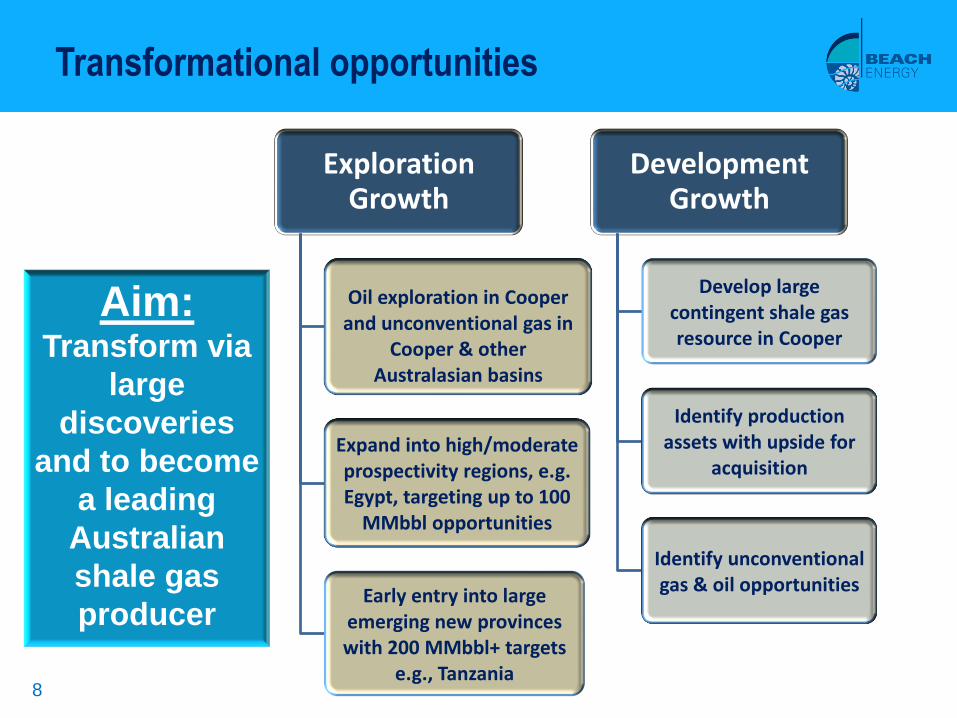

Transformational opportunities

8

Exploration Growth

Oil exploration in Cooper and unconventional gas in

Cooper & other Australasian basins

Expand into high/moderate prospectivity regions, e.g. Egypt, targeting up to 100

MMbbl opportunities

Early entry into large emerging new provinces with 200 MMbbl+ targets

e.g., Tanzania

Development Growth

Develop large contingent shale gas resource in Cooper

Identify production assets with upside for

acquisition

Identify unconventional gas & oil opportunities

Aim:Transform via

large

discoveries

and to become

a leading

Australian

shale gas

producer

Cooper / Eromanga Gippsland Egypt

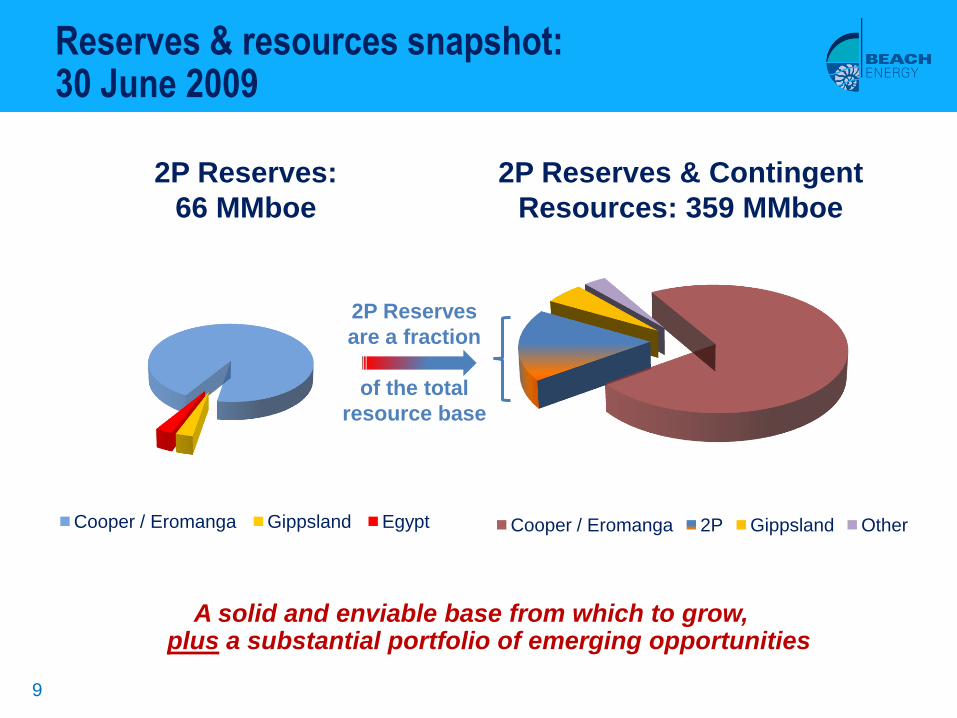

Reserves & resources snapshot: 30 June 2009

9

A solid and enviable base from which to grow,plus a substantial portfolio of emerging opportunities

2P Reserves:

66 MMboe

2P Reserves & Contingent

Resources: 359 MMboe

Cooper / Eromanga 2P Gippsland Other

2P Reserves

are a fraction

of the total

resource base

Reserves and production

10

0

1

2

3

4

5

6

7

8

9

10

FY 2007 FY2008 FY 2009 FY 2010 est.

Gas & Gas Liquids Oil

0

20

40

60

80

100

120

140

160

FY 2006 FY2007 FY 2008 FY 2009

Gas & Gas Liquids Oil

2P ReservesProduction

• Consistent production performance:

– Oil represents 38% of est. FY 2010

production (34%, FY 2009)

• Solid reserves growth in recent years:

– Offset by Tipton West gas divestment in

FY 2009

MM

bo

e

MM

bo

e

Overview of financial position

11

HY09 FY09

Net cash on hand $118 million $136 million

Production volume 4.0 MMboe 9.6 MMboe

Sales revenue $259 million $581 million

Cash flow from operations $22 million $173 million

Net profit after tax $34 million $260 million

Underlying net profit $26 million $64 million

Interim dividend declared 0.75 cents / share 3.75 cents / share

Underlying earnings per share 2.41 cents / share 6.21 cents / share

HY09 - a steady result with our eye on the future

• Cooper Basin is a key supplier

of onshore oil and gas to

eastern Australian markets:

– Diversified asset, product and

market mix

• Beach participates in

approximately 300 exploration

and production licenses:

– Equity interests range from

approximately 17% to 100%

• Numerous exploration and

development opportunities

The ‘base business’: Cooper Basin production, development & exploration

12

Cooper Basin Oil

2P reserves 14.3 MMbbl

• Comprised of three key areas:

– Western flank (Beach operated)

– Central Cooper Basin (Santos

operated)

– Eastern flank (Beach operated)

• Successful development of the

Beach operated western flank:

– Beach discovered approximately

10 MMbbl over the past 8 years

• Beach operated six well drilling

campaign planned for 2010

The ‘base business’: Conventional Cooper Basin oil & gas

13

Cooper Basin Gas

2P reserves 228 PJ & 7.4 MMboe

• Gas & ethane contracts with major

retailers and end consumers

• Domestic and export LPG contracts

• Export naptha contracts

• Quality joint venture partners in

Santos and Origin Energy

• Drilling program planned to convert

500 PJ (gross) of conventional gas

resources into 2P reserves

14

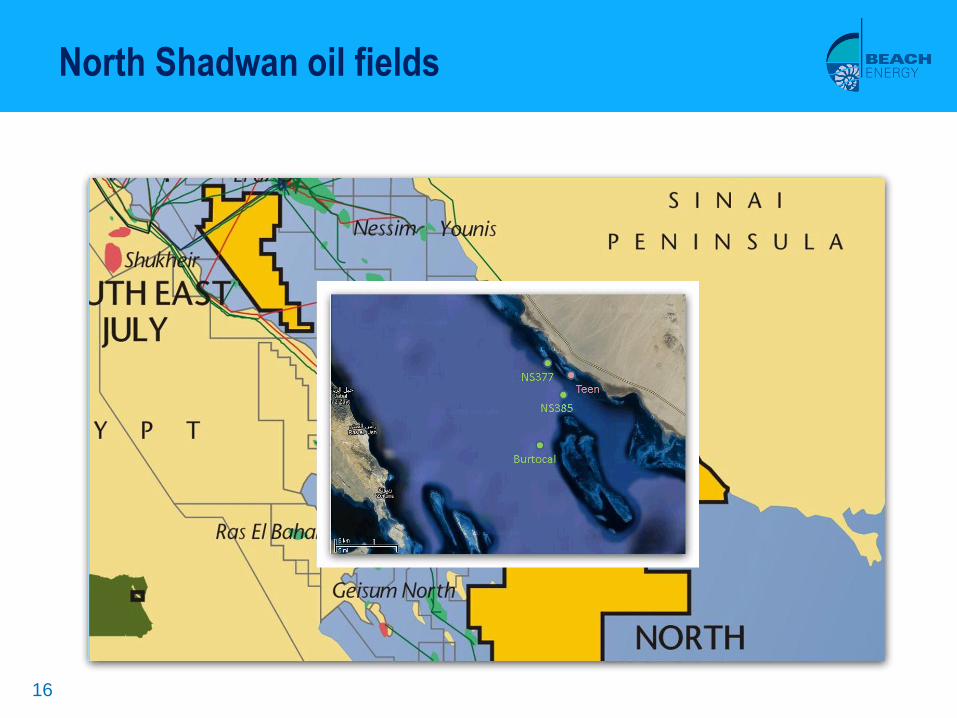

The ‘base business’ - Gulf of Suez: First oil within months

• Beach 20% interest

• High potential Gulf of Suez

acreage

• Three existing oil

discoveries:

– NS 377 and 385

(„near shore fields‟)

– NS 394 „Burtocal‟

• First oil expected Q3 2010

from near shore fields

• Seeking new opportunities

to expand growth

15

Gulf of Suez oil fields

15

16

North Shadwan oil fields

17

North Shadwan:Near shore fields conceptual development

GH-377 Field

GH-385 Field

To Ghara Facilities

2 wells to be drilled

from onshore

4 wells to be drilled

from onshore

18

Finding more oil in Egypt

• Highly prospective region

• Long established industry -

favourable legislative & fiscal

regime

• Home to giant oil fields (500 -

800 MMbbl) such as Morgan,

July & Ramadan

• Extensive infrastructure

• Low cost

• Large opportunity deal flow

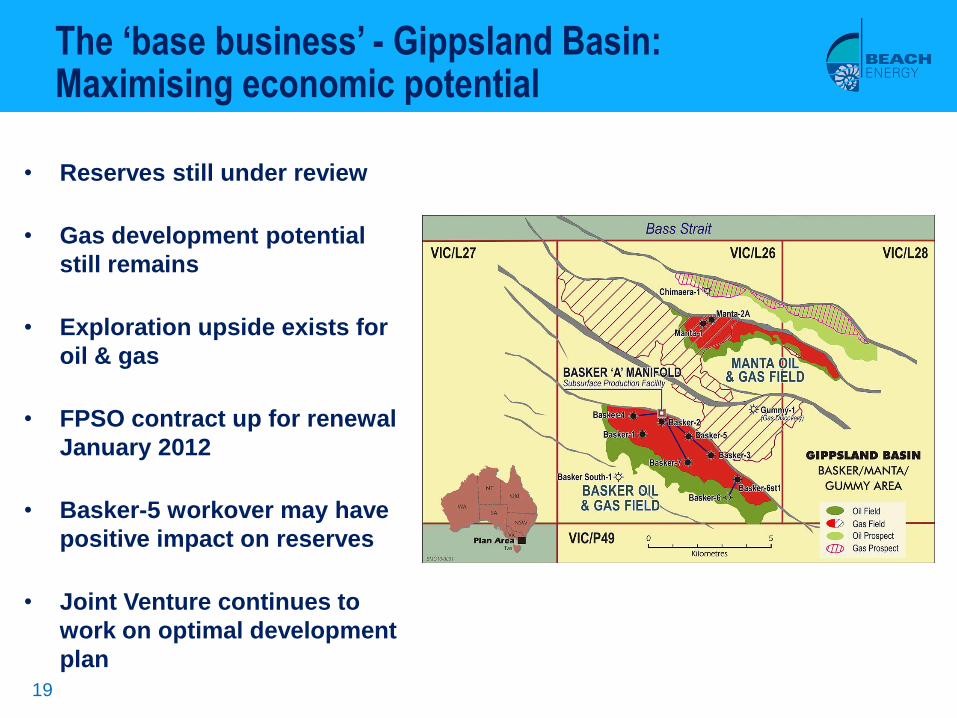

• Reserves still under review

• Gas development potential

still remains

• Exploration upside exists for

oil & gas

• FPSO contract up for renewal

January 2012

• Basker-5 workover may have

positive impact on reserves

• Joint Venture continues to

work on optimal development

plan

19

The ‘base business’ - Gippsland Basin:Maximising economic potential

• Beach is seeking to grow its

base gas business in eastern

Australian markets from the

Cooper Basin

• Good long-term growth

opportunities for eastern

Australian gas resources:

– Strong projected domestic and

export demand

– Carbon policies

• Cooper Basin shale gas is a

‘sleeper’ in the options for long-

term domestic and export gas

supply

Expanding the base business:Positioning for long-term Australian gas supply

20

• Early identification of Cooper

Basin shale gas potential

• Captured prospective acreage

with high equity participation

• Huge resource potential:

– Comparable to combined NSW

and Queensland coal seam gas

volume

• Access to multiple market

opportunities via existing

and future infrastructure

• Developing key relationships

to deliver technologies and

new markets

Cooper Basin:Significant shale gas potential

21

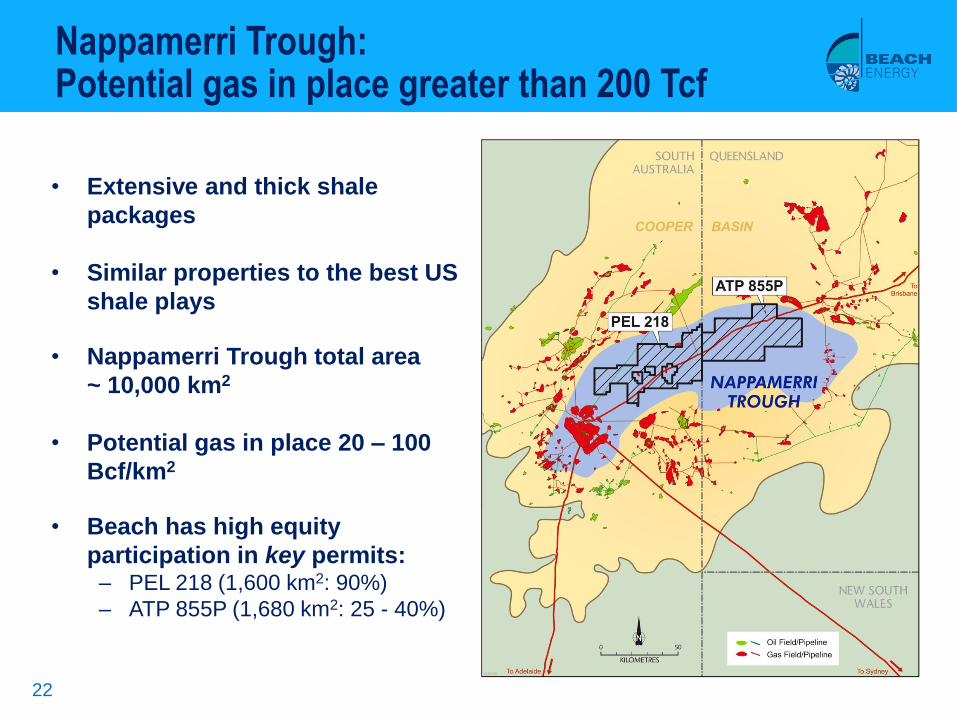

Nappamerri Trough: Potential gas in place greater than 200 Tcf

• Extensive and thick shale

packages

• Similar properties to the best US

shale plays

• Nappamerri Trough total area

~ 10,000 km2

• Potential gas in place 20 – 100

Bcf/km2

• Beach has high equity

participation in key permits:– PEL 218 (1,600 km2: 90%)

– ATP 855P (1,680 km2: 25 - 40%)

22

Geological properties

Thick shale sequence 150m thick over 10,000 km2

Organically rich 5% Total Organic Carbon (TOC)

Gas prone Proven

Thermally mature Proven

Overpressure Proven

Tight gas sands Potential upside

Mechanical properties

Suitability for fracturing Probable

Containment of fracture Low risk

Commercial aspects

Infrastructure Significant infrastructure already exists

Cost structure To be determined

Market Multiple options; dependent on cost structure

Why the Nappamerri Trough?

23

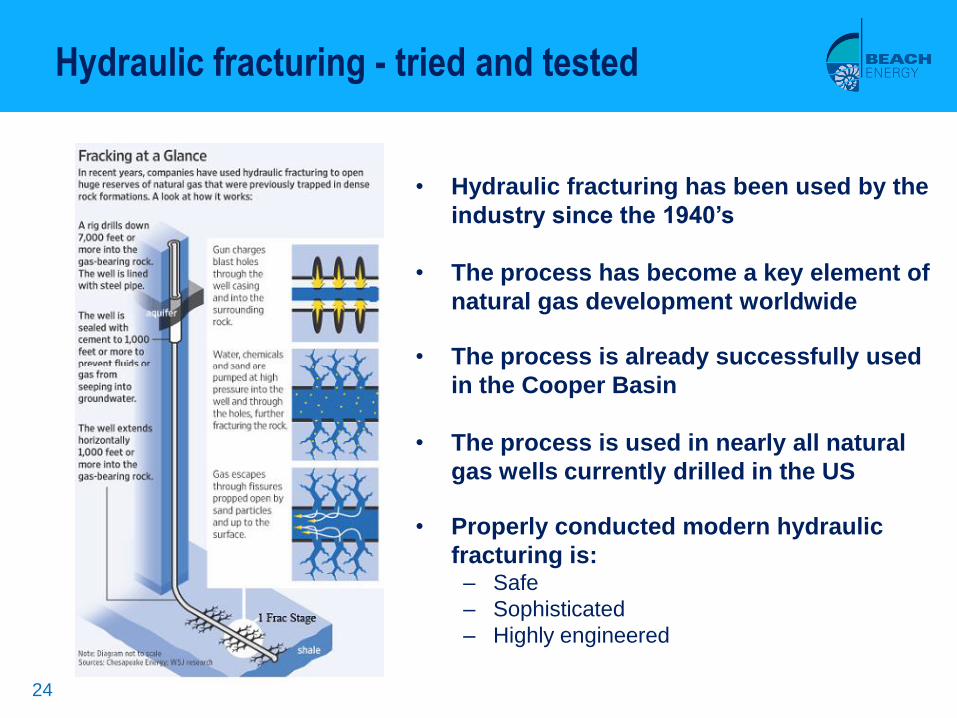

Hydraulic fracturing - tried and tested

24

• Hydraulic fracturing has been used by the

industry since the 1940’s

• The process has become a key element of

natural gas development worldwide

• The process is already successfully used

in the Cooper Basin

• The process is used in nearly all natural

gas wells currently drilled in the US

• Properly conducted modern hydraulic

fracturing is:– Safe

– Sophisticated

– Highly engineered

Cooper Basin shale gas:Indicative shale gas development timeline

25

Holdfast-1 vertical

exploration well

Q3 2010

Design pilot production

well Q2

Q4 2010/

Q1 2011

BOOK GAS RESOURCE

Q2 2011

Pilot production

well

Drill Q2 2011

Frac Q4 2011

Test Q1 2012

Pilot development

Commence FY13

BOOK GAS

RESERVE

Target FY13/14

FIRST GAS SALES

Target FY15

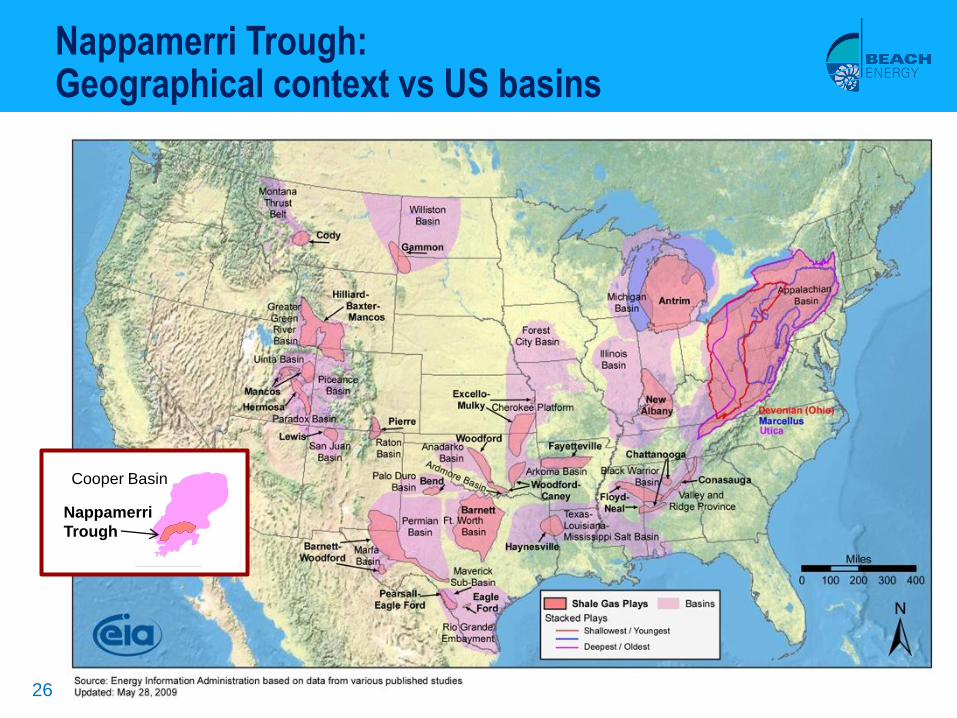

Nappamerri Trough: Geographical context vs US basins

26

Cooper Basin

Nappamerri

Trough

0

5

10

15

20

25

30

35

40

2006 2007 2008 2009

No. of frac stages/well

F&D cost (US$/bbl)

27

US technology improvements drive down costs: e.g. - Bakken Shale

• Technology advancements in

multi – stage frac completions

is driving efficiencies in US oil

& gas developments

• Key advancements are

particularly associated with

long lateral drilling + multi-

stage fracs

• Advances in technology is

delivering:– Increased reserves & production

– Lower finding & development

costs

• Australian shale projects can

benefit from the US experience

& learning gained by others

Bakken Shale (oil), North Dakota

Source: Sundance Energy

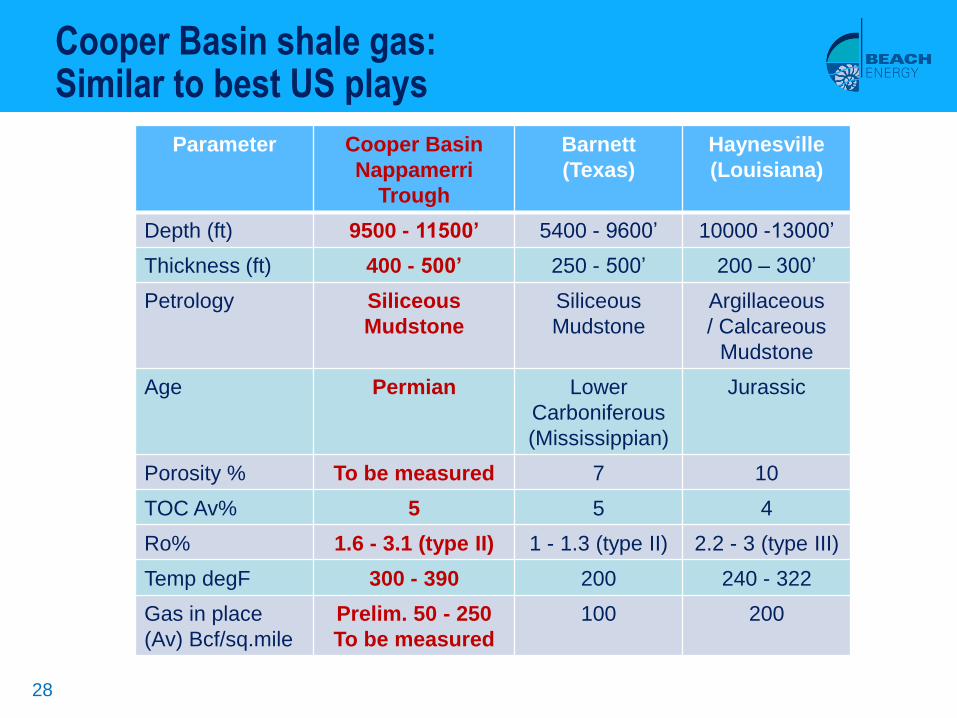

Cooper Basin shale gas:Similar to best US plays

28

Parameter Cooper Basin

Nappamerri

Trough

Barnett

(Texas)

Haynesville

(Louisiana)

Depth (ft) 9500 - 11500’ 5400 - 9600‟ 10000 -13000‟

Thickness (ft) 400 - 500’ 250 - 500‟ 200 – 300‟

Petrology Siliceous

Mudstone

Siliceous

Mudstone

Argillaceous

/ Calcareous

Mudstone

Age Permian Lower

Carboniferous

(Mississippian)

Jurassic

Porosity % To be measured 7 10

TOC Av% 5 5 4

Ro% 1.6 - 3.1 (type II) 1 - 1.3 (type II) 2.2 - 3 (type III)

Temp degF 300 - 390 200 240 - 322

Gas in place

(Av) Bcf/sq.mile

Prelim. 50 - 250

To be measured

100 200

Multiple long-term shale gas market options

Market opportunities

Existing customers –

extension contracts

Existing customers –incremental

contracts

New domestic

customers

Gas Swaps

Mature existing MOUs

Export LNG

• Good prospects to increase

Cooper Basin supply over time

• New domestic gas supply

opportunities include:

– Power generation

– Feedstock

– Liquid fuels

• LNG supply a long-term

objective

• Holdfast-1 shale gas exploration

well to be drilled Q3 2010

• Targeting first Beach-operated

shale gas sales in FY 2015

29

• Australian unconventional gas M&A activity has been mainly associated

with Queensland coal seam methane (CSM):

– Approximately $20 billion worth of recent CSM deals

– Purchasers include BG Group, ConocoPhillips, Shell and PETRONAS

• Australian unconventional gas M&A activity has lagged overseas ‘action’

whilst the industry was developing technology, resources and markets

When will Cooper Basin shale gas value recognition occur?

30

Deal Location Date Value

Mitsui - Anadarko Marcellus Feb 10 US$1.4b

Total - Chesapeake Barnett Jan 10 US$2.25b

ExxonMobil – XTO Energy Included 1 million

acres of various

shale gas acreage

Dec 09 US$41b

BG Group – EXCO Resources Haynesville Aug 09 US$1.1b

Some recent US shale gas transactions

31

Some other long-term growth opportunities: ‘Big oil’ and ‘big gas’

Tanzania

Papua New Guinea

Australia

New Zealand

32

Tanzania - East African Rift:An emerging ‘big oil’ province

• Beach 100%

• Under - explored, high potential

region

• Significant success in nearby

analogous areas (Uganda)

• Recent M&A activity in Uganda

highlights regional potential

• Potential for large (> 200+ MMbbl)

discoveries

• Petroleum Sharing Agreement

signing expected within months

• Exploration activity to commence

in 2010

33

Two rift systems of comparable size –And potential?

Note: Maps depicted at approximate scale Source: Google

Gulf of Suez Lake Tanganyika

Offshore ‘big gas’ opportunities

• LNG supply potential from existing portfolio:

– Burnside (multi-Tcf discovery made in 2009, Beach 7.34%)

– Pandora (mean gas resource approx. 0.8 Tcf, Beach 6.36%)

– Barque gas prospect (multi-Tcf potential, Beach 20%)

Browse Basin Gulf of Papua Canterbury Basin

34

• Sustainable underlying base business:

– Long-life reserves

– Long-term production and cash-flow

– Asset, product and market diversity

• Tangible growth potential targeting

regionally specific opportunities:

– Cooper Basin shale gas

– Egypt

– Game-changing exploration and

development potential

• Robust balance sheet

• The right people and strong strategic

relationships to deliver long-term growth

Beach Energy

35

Reference Slides

36

Aim: To double production and reserves within 2 - 5 years

Corporate strategy

37

Risk / Reward Timeframe: 2 – 5 years Timeframe: 5 – 10 years

Low

(60%)

• Add up to 20 MMboe new reserves via

exploration

• Develop contingent Cooper conventional

gas resource of approx. 500 PJ

• Continue Cooper exploration for oil and

unconventional gas

• Develop contingent shale gas resource

in Cooper

Moderate

(30%)

• Add up to 30 MMbbl+ of new reserves in

Egypt

• Acquire assets suited to Beach‟s skills

with upside potential

• Expand into other regions targeting up

to 100 MMboe opportunities

• Acquire assets suited to Beach‟s skills

with upside potential

High

(10%)

• Mature Cooper shale gas opportunity

• Drill high value exploration and appraisal

targets

• Early entry into emerging new

provinces with 200 MMbbl+ targets

• Drill high value exploration and

appraisal targets

Low carbon /

value adding

• Continue to build value / new markets through downstream alliances

• Pursue clean fuel and commodity markets

• Pursue low carbon energy opportunities, e.g., biodiesel, geothermal, carbon

sequestration

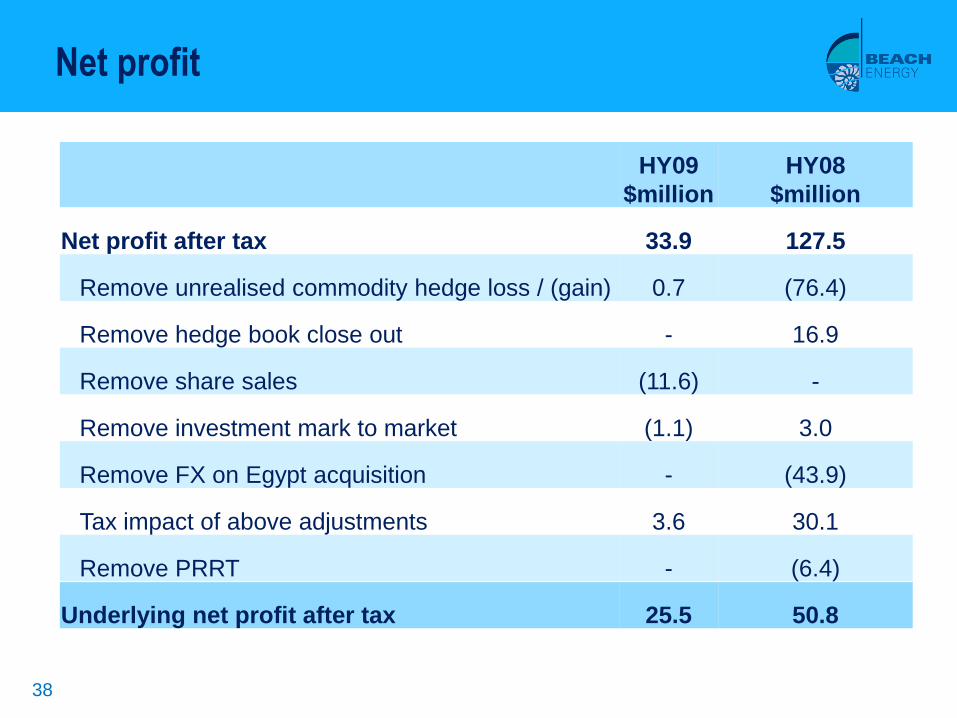

Net profit

38

HY09

$million

HY08

$million

Net profit after tax 33.9 127.5

Remove unrealised commodity hedge loss / (gain) 0.7 (76.4)

Remove hedge book close out - 16.9

Remove share sales (11.6) -

Remove investment mark to market (1.1) 3.0

Remove FX on Egypt acquisition - (43.9)

Tax impact of above adjustments 3.6 30.1

Remove PRRT - (6.4)

Underlying net profit after tax 25.5 50.8

Net profit

39

HY08

Tax

Borrowing expense Other expenses

and revenue

Gross profit

HY09

$50.8

$19.3

$8.3

$25.5

$13.7

$39.2

0

10

20

30

40

50

60

70

80

90

$m

Underlying net profit after tax comparison

$25.3 million

total decrease

40

Gross profit

HY08

Depreciation

Cash production

costs

Inventory3rd party

purchases

Sales revenue

HY09

$84.1

$23.7

$15.6

$7.8

$44.9

$11.8

$74.5

0

20

40

60

80

100

120

140

$m

Gross profit comparison

$39.2 million

total decrease

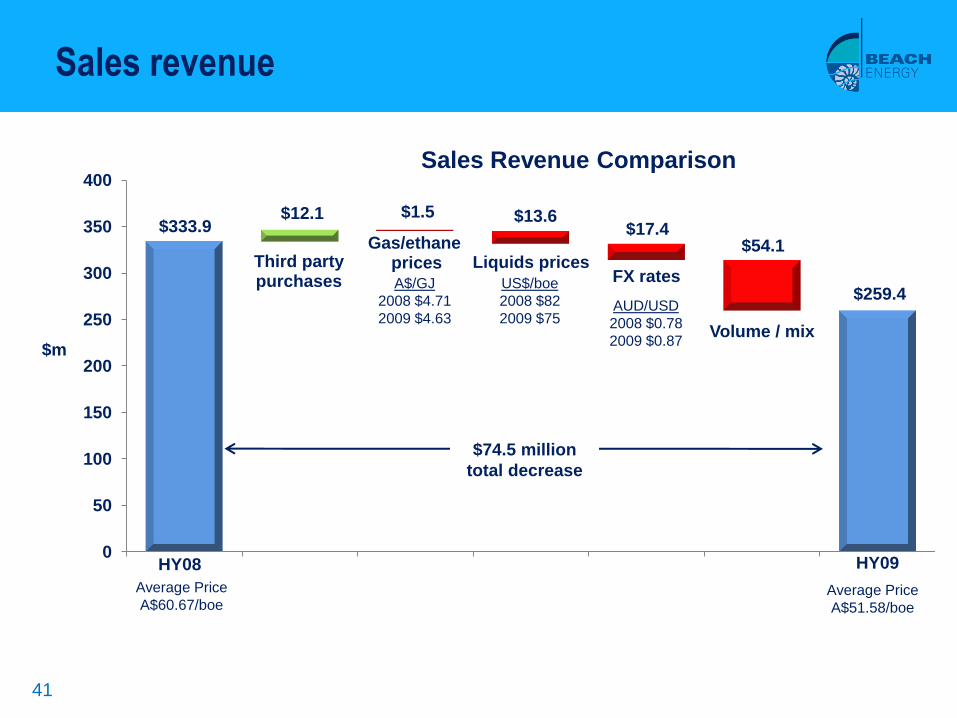

Sales revenue

41

HY08

Third party purchases

Gas/ethaneprices Liquids prices

FX rates

Volume / mix

HY09

$333.9 $12.1

$259.4

$1.5 $13.6 $17.4

$54.1

0

50

100

150

200

250

300

350

400

$m

Sales Revenue Comparison

AUD/USD

2008 $0.78

2009 $0.87

A$/GJ

2008 $4.71

2009 $4.63

US$/boe

2008 $82

2009 $75

Average Price

A$60.67/boeAverage Price

A$51.58/boe

$74.5 million

total decrease

Sales revenue

42

• Sales revenue $259 million –

down 22%:

– Lower oil price

– Lower BMG production

– Sale of Tipton West

– Softer demand from gas customers

• HY09 average gas price

$4.63/GJ – down 2%

• HY09 average oil price

$86/bbl – down 20%

-

20

40

60

80

100

120

2005/06 2006/07 2007/08 2008/09 2009/10 (H)

A$/bbl

Oil Price

Actual Average ($92/bbl)

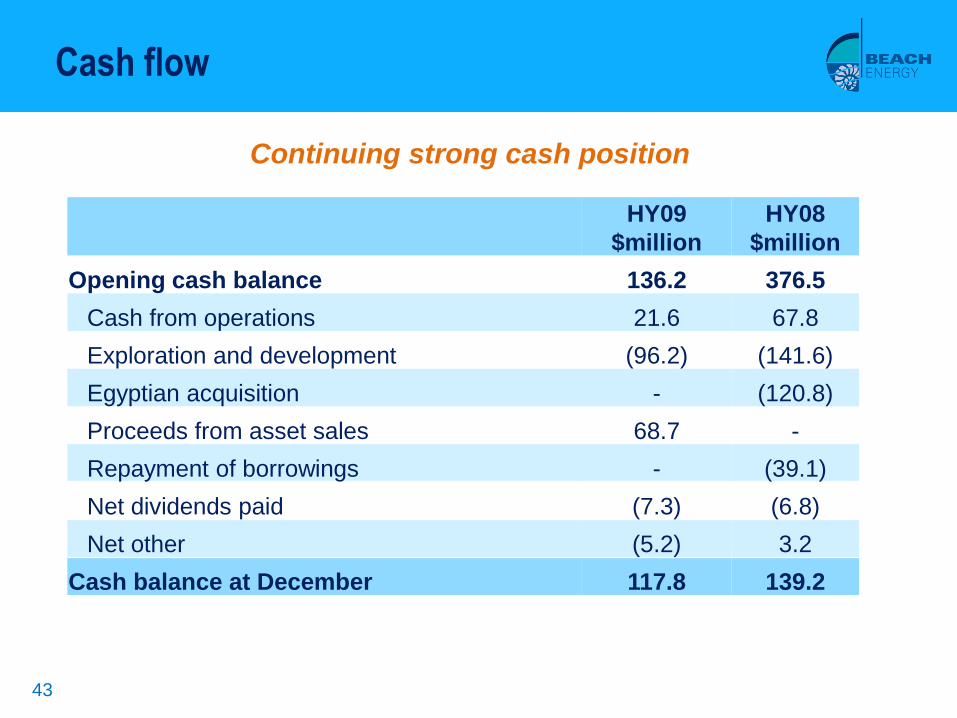

Cash flow

43

HY09

$million

HY08

$million

Opening cash balance 136.2 376.5

Cash from operations 21.6 67.8

Exploration and development (96.2) (141.6)

Egyptian acquisition - (120.8)

Proceeds from asset sales 68.7 -

Repayment of borrowings - (39.1)

Net dividends paid (7.3) (6.8)

Net other (5.2) 3.2

Cash balance at December 117.8 139.2

Continuing strong cash position

Current financial risk management

44

Oil Price

Period

Floor

US$80/bbl

TAPIS

Floor

US$55/bbl

WTI

Total Hedged

Volume

(bbls)

FY 2010 300,000 - 300,000

FY 2011 - 300,000 300,000

Total Hedged 300,000 300,000 600,000

• US$108 million (A$120.0

million) in foreign exchange

hedged

• Aim to hedge 50% of net USD

exposure

Currency

Period

Collars &

Ceilings

$A million

Collars &

Ceilings

$US million

FY 2010 $40.0 $36.0

FY 2011 $80.0 $72.0

Total Hedged $120.0 $108.0

• Uncomplicated oil price floors to limit downside commodity price risk

• 25% of oil production currently hedged

45