12

THE ROBIN HOOD TAX: EVERYTHING YOU NEED TO KNOW robinhoodtax.org.uk

THE ROBIN HOOD TAX: EVERYTHING YOU NEED TO KNOW

robinhoodtax.org.uk

THE BIG IDEA

The idea behind the Robin Hood Tax is simple:

the financial sector has caused the greatest

recession in a generation, affecting millions of

people here in the UK and around the world. The

financial sector must now pay its fair share of

the cost of sorting out the mess it created. The

Robin Hood Tax campaign is calling on the UK

government to raise an additional £20 billion a

year from the banking industry – much needed

revenue that could fight poverty in the UK and

overseas. It could help tackle climate change.

Help protect schools and hospitals. Help stop

massive cuts across the public sector. Help build

new lives around the world…so what are we

waiting for?

The tax is just. The financial sector can afford it.

And academic heavyweights have shown that

the systems are in place to collect it.

WHAT’S THIS GUIDE FOR?

This handy guide to the Robin Hood Tax is all you

need to make you into a star Merry (Wo)Man.

It will tell you everything you need to know and

answer any tricky questions you have about the

campaign.

CONTENTS

01 What is the Robin Hood Tax?Financial Transaction TaxesWhy does the Robin Hood Tax campaign favour Financial Transaction Taxes?The Bank LevyThe Fat Tax

02 Why do we need the Robin Hood Tax? How would the money be spent? At homeAbroadClimate changeWhy should some of this money be used for fighting poverty and climate change in developing countries?

03 Why should the financial sector be taxed? How did our financial sector come to be so bloated?

04 What has the UK government done so far?

05 Has there been any progress globally?

06 Doesn’t the financial sector make an important contribution to our economy?

07 Can the UK’s banks afford to pay £20 billion extra?

08 What about when people say it needs global agreement to work?

09 Won’t companies just avoid the tax or move their businesses offshore?

10 Won’t banks just pass the costs onto us?

11 Can Financial Transaction Taxes reduce speculation and risky financial activity?

01WHAT IS THE ROBIN HOOD TAX?

�� �Robin�Hood�Taxes�would�be�paid�by�the�financial�sector.�They�target�those�who�can�afford�to�pay�more.�And�the�money�would�be�spent�on�those�who�need�it�most�–�the�poor�at�home�and�abroad.�In�the�UK�additional�taxation�of�the�financial�sector�must�meet�two�essential�criteria�to�be�worthy�of�the�name�Robin�Hood:�

•��Any�Robin�Hood�Tax�should�raise�billions�of�pounds�of�revenue�every�year.�We�call�for�a�further�£20�billion�from�the�financial�sector�in�the�UK.

•��Revenue�generated�by�a�Robin�Hood�Tax�must�be�used�to�tackle�poverty�in�the�UK�and�abroad�and�to�fight�the�worst�effects�of�climate�change.�

� �We�believe�that�a�Financial�Transaction�Tax�offers�the�most�potential�–�a�tiny�tax�of�0.05%�(on�average)�on�transactions�such�as�bonds�and�derivatives�could�raise�globally�as�much�as�£250�billion�a�year.�

FINANCIAL TRANSACTION TAXES

Financial�Transaction�Taxes�(FTTs)�are�levied�on�transactions�of�financial�assets,�including�stocks,�bonds,�foreign�exchange�and�derivatives.�With�an�FTT,�each�time�a�financial�product�is�traded,�a�tiny�percentage�(between�0.5%�and�0.005%)�of�the�value�of�the�trade�is�collected�in�tax.

WHY DOES THE ROBIN HOOD TAX CAMPAIGN FAVOUR FINANCIAL TRANSACTION TAXES?

� �The�Robin�Hood�Tax�campaign�believes�FTTs�are�the�most�appropriate�way�to�tax�the�financial�sector.�Here�are�four�reasons�why:

•��They�have�the�greatest�potential�to�raise�revenue.�Implemented�internationally,�Financial�Transaction�Taxes�could�yield�as�much�as�£250�billion�annually,�while�in�the�UK�we�could�raise�tens�of�billions�of�pounds�a�year.1

•��FTTs�are�commonplace�and�have�been�implemented�either�permanently�or�temporarily�in�at�least�40�countries�over�many�decades.2��In�the�UK,�we�have�an�FTT�on�some�share�transactions�of�0.5%,�which�raises�around�£4�billion�a�year.3 FTTs�on�a�broader�range�of�financial�products�could�raise�significantly�more.

•��They�are�simple�and�inexpensive�to�implement�and�difficult�to�avoid.�As�described�later,�whether�transactions�are�carried�out�on�centralised�exchanges�or�spread�throughout�the�world,�the�vast�majority�of�them�are�settled�through�a�handful�of�electronic�clearinghouses�making�such�a�tax�really�hard�to�avoid.4

•��There�is�a�large�amount�of�political�momentum�around�FTTs,�especially�in�Europe.�France,�Germany,�Spain,�Finland,�Austria�and�Belgium�have�all�come�out�in�support�of�an�FTT.�

� �But�we�are�open�to�a�variety�of�different�proposed�Robin�Hood�Taxes,�and�see�levies�on�profits,�remunerations�and�balance�sheets�as�potentially�complementary�with�each�other�(and�with�improved�regulation).�There�are�two�other�taxes�which�you�might�also�hear�about:

THE BANK LEVY

This�proposal,�commonly�referred�to�as�the�Bank�Levy�is�also�known�as�the�Insurance�Levy,�or�by�the�IMF�as�the�Financial�Stability�Contribution�(FSC).�It�refers�to�a�flat�rate�tax�on�financial�institutions�above�a�certain�size.�The�UK�government�announced�that�it�would�implement�a�Bank�Levy�in�the�Emergency�Budget�in�June�2010,�and�other�countries�have�made�similar�commitments�(including�Austria,�France,�Germany,�Hungary,�Portugal�and�Sweden).�

Unfortunately�these�Bank�Levies�will�raise�only�small�sums�of�money,�and�critically,�none�of�the�money�will�be�earmarked�for�helping�those�most�affected�by�the�crisis.�In�the�UK�it�will�raise�just�£2.5�billion�a�year�from�the�financial�sector.�And�shockingly,�much�of�this�will�be�offset�by�a�reduction�in�Corporation�Tax�from�28%�to�24%.�

These�amounts�are�tiny�in�comparison�to�the�implicit�subsidy�the�banks�receive�from�Government.�By�refusing�to�let�the�big�banks�go�bust,�the�UK�and�other�countries�ensure�that�the�banks�can�borrow�money�on�far�more�generous�terms�than�other�businesses.�In�the�UK,�the�Bank�of�England�have�estimated�that�this�subsidy�is�worth�approximately�£100bn�a�year.5�Even�the�Financial�Times6�is�arguing�for�further�taxes�on�the�banks.

THE FAT TAX

� �The�FAT�tax�(Financial�Activities�Tax)�is�a�charge�on�financial�sector�profits�and�remuneration.�It�was�first�proposed�by�the�IMF�in�its�influential�June�2010�report,�A�Fair�and�Substantial�Contribution�by�the�Financial�Sector.�The�IMF�proposed�such�a�tax�because�it�would�correct�what�it�called�an�“under-taxed�and�hence�perhaps�‘too�big’”�financial�sector.�It�is�also�supported�by�the�European�Commission�and�the�UK�government.

� �According�to�the�IMF,�a�FAT�tax�of�10%�(half�the�rate�of�VAT)�could�raise�about�£9bn�in�the�UK.�

So�what’s�the�rationale�for�an�organisation�like�the�IMF�suggesting�a�new�tax�on�the�banks?�

Somewhat�incredibly,�whilst�VAT�goes�up�for�ordinary people,�the�financial�sector�remains�VAT�exempt.�That�means�every�time�you�buy�a�car,�you�pay�VAT.�Every�time�a�trader�sells�a�derivative�or�bond,�they�pay�nothing.�This�means�a�staggering�loss�in�tax�revenue�that�instead�helps�to�boost�bank�profits�and�pay.

The�financial�crisis�and�recession�have�left�a�massive�hole�in�the�UK’s�public�finances,�hitting�front�line�services�and�jobs.�The�largest�recession�of�a�generation�has�had�a�disastrous�impact�not�just�in�the�UK,�but�on�the�public�finances�of�many�developing�countries�as�well.�Hundreds�of�thousands�of�supporters�of�the�Robin�Hood�Tax�campaign�believe�that�banks,�hedge�funds�and�the�rest�of�the�financial�sector�should�be�asked�to�pay�their�fair�share�to�clear�up�the�mess�they�helped�create.�We�are�calling�on�the�UK�financial�sector�to�pay�an�additional�£20�billion�per�year�in�taxation.�Globally,�we�are�calling�for�Robin�Hood�Taxes�to�raise�as�much�as�£250�billion�per�year.�Our�proposal�is�that�the�money�be�split�as�follows:

•��50%�to�be�used�to�protect�the�poorest�and�most�vulnerable�at�home;

•��25%�to�be�used�to�help�those�in�developing�countries�hit�hardest�by�the�financial�crisis;

•��25%�towards�much�needed�resources�to�fight�climate�change�at�home�and�abroad.�

Here’s�why�we�need�the�Robin�Hood�Tax:

AT HOME

The�banking�crisis�has�hit�people�in�the�UK�hard.�They�are�losing�their�jobs,�crucial�services�and�most�alarmingly�their�homes.�Youth�unemployment�is�sky-rocketing.�According�to�Save�the�Children,�1.7�million�children�in�the�UK�live�in�severe�poverty,�which�means�living�without�basic�necessities�such�as�clothing�and�food.8�This�year,�the�UK�government�has�announced�plans�to�cut�£81�billion�from�the�national�budget�through�to�2015.�These�cuts�will�push�people�further�into�debt�and�deeper�into�poverty.�A�Robin�Hood�Tax�offers�an�alternative�to�the�cuts.

ABROAD

The�consequences�of�the�financial�crisis�have�been�serious�in�the�UK�and�the�developed�world,�but�they�have�been�even�worse�in�more�vulnerable�countries�that�did�nothing�to�cause�it.�As�a�direct�result�of�the�crisis,�developing�and�emerging�country�output,�exports,�migrant�remittances,�capital�inflows,�and�foreign�aid�have�all�been�lower�than�expected�over�the�last�three�years.�On�the�ground,�the�effect�is�devastating.�In�Sub-Saharan�Africa,�

an�estimated�30�to�50�thousand�extra�infants�died�in�2009.9 The World�Bank�estimates�that,�globally,�an�additional�120�million�people�have�been�forced�to�live�on�less�than�US$2�a�day�and�an�additional�89�million�on�less�than�US$1.25�a�day.10

The�Millennium�Development�Goals�are�now�in�jeopardy�as�governments�struggle�to�live�up�to�their�foreign�aid�commitments.�Tony�Dolphin,�senior�economist�at�the�Institute�for�Public�Policy�Research,�explains:�‘Although�the�worst�of�the�crisis�appears�to�be�in�the�past,�its�effect�on�emerging�and�developing�economies�will�continue�well�into�the�future.�Lower�employment�rates�and�a�lack�of�social�safety�nets�mean�that�poverty�is�higher�than�it�would�otherwise�have�been�and�achieving�the�Millennium�Development�Goal�of�halving�poverty�by�2015�will�be�that�much�harder.’11

This�crisis�was�caused�by�the�financial�sector�and�it�needs�to�pay�to�fix�the�problems�it�helped�create.

CLIMATE CHANGE

A�tragic�parallel�between�climate�change�and�the�financial�crisis�is�that�those�least�responsible�suffer�the�most.�While�rich�countries�and�powerful�corporations,�many�with�ties�to�the�financial�sector,�have�produced�most�of�the�greenhouse�gases�that�are�causing�climate�change,�poorer�countries�are�expected�to�bear�75-80%�of�the�costs.12�Disrupted�seasonal�patterns�lead�to�failed�crops,�and�increased�floods,�droughts,�cyclones�and�storms�lead�to�severe�hunger,�poverty,�disease,�and�lost�homes.�According�to�The�Stern�Review�of�the�Economics�of�Climate�Change,�there�could�be�up�to�200�million�environmental�refugees�by�2050.13��Insurance�giant�Munich�Re�estimates�that�losses�from�climate-related�catastrophes�have�increased�10%�since�1980,�and�averaged�$100�billion�per�annum�over�the�last�decade.14��The�costs�fall�disproportionately�on�developing�countries,�which�are�less�equipped�to�deal�with�catastrophes,�and�in�which�agriculture�–�particularly�subsistence�agriculture�–�constitutes�a�significant�proportion�of�GDP.�

A�Robin�Hood�Tax�would�provide�a�new�source�of�finance�to�help�those�experiencing�climate�change�deal�with�its�devastating�effects.

WHY SHOULD SOME OF THIS MONEY BE USED FOR FIGHTING POVERTY AND CLIMATE CHANGE IN DEVELOPING COUNTRIES?

Research�for�Oxfam�has�shown�that�the�56�poorest�countries�are�facing�a�$65�billion�dollar�hole�in�their�finances�because�of�the�financial�crisis�caused�by�the�banks.�This�means�cuts�in�education�health�and�support�for�farmers.�In�desperately�poor�countries,�that�means�people�losing�their�lives.�So�a�tax�on�the�banks�should�help�those�hit�by�the�financial�crisis�in�poor�countries�as�well�as�the�UK.�

At�the�same�time�rich�nations,�who�did�the�most�to�cause�climate�change,�have�promised�to�find�$100�billion�dollars�to�help�poor�countries�who�are�hit�hardest�by�its�consequences.�It�makes�sense�for�the�financial�sector�to�contribute�to�the�urgent�financing�required�to�fight�climate�change,�a�point�recognised�by�both�Germany’s�Chancellor�Merkel�and�France’s�President�Sarkozy.�

It�is�for�these�reasons�that�we�think�that�half�the�money�raised�should�be�spent�helping�the�poorest�in�developing�countries�and�fighting�climate�change�at�home�and�abroad,�and�the�other�half�spent in�the�UK.

02WHY DO WE NEED THE

ROBIN HOOD TAX?

HOW WOULD THE MONEY

BE SPENT?

Not�only�is�the�financial�sector�the�most�able�to�pay�(and�currently�under-taxed),�but�it�is�also�the�same�sector�that�got�us�into�trouble�in�the�first�place.�The�financial�sector�precipitated�the�financial�crisis�and�the�largest�recession�since�the�1930s.�Numerous�financial�institutions�exploited�their�too-big-to-fail�status�and�engaged�in�risky�behaviour�that�took�our�economy�to�the�brink.�Through�the�bank�bailout,�UK�taxpayers�effectively�underwrote�the�financial�sector’s�get�out�of�jail�free�card.�The�IMF�has�calculated�that�the�un-recovered�cost�to�the�UK�of�the�bank�bailout�was�₤99�billion1,�the�cost�to�the�UK�economy�as�a�whole�of�the�financial�crisis�in�terms�of�lost�output�will�be�₤497�billion,�and�the�resulting�increase�in�government�debt�over�the�period�of�2008-15�will�be�₤737�billion.15�This�money�is�now�spurring�a�rapid�return�to�record�breaking�profits�and�bonuses�for�the�banks.�According�to�the�Governor�of�the�Bank�of�England,�Mervyn�King,�“never�in�the�field�of�financial�endeavour�has�so�much�money�been�owed�by�so�few�to�so�many”.16

In�the�last�two�decades�the�financial�sector�has�undergone�runaway�expansion�with�its�activities�becoming�steadily�more�divorced�from�the�real�economy�of�goods�and�services.�Much�of�the�excessive�growth�is�from�speculative�“high�frequency�trading”�

03WHY SHOULD THE

FINANCIAL SECTOR BE

TAXED?

or�casino-style�banking,�which�increases�volatility�in�the�financial�markets�(see�below�for�more�on�this).�Globally,�the�volume�of�financial�trade�weighs�in�at�a�colossal�US$3,260�trillion�–�73.5�times�the�size�of�nominal�world�GDP.�This�ratio�is�highest�in�the�UK,�where�in�2007�the�volume�of�financial�transactions�reached�a�staggering�446�times�the�size�of�our�real�economy.17�Our�over-reliance�on�the�City�of�London�is�also�the�reason�why�the�impact�of�the�recession�in�the�UK�was�so�savage.�

HOW DID OUR FINANCIAL SECTOR COME TO BE SO BLOATED?

Part�of�it,�according�to�the�IMF,�is�that�the�financial�sector�is�“under-taxed”18�relative�to�the�rest�of�the�economy.�Unlike�normal�goods�and�services�such�as�a�car,�or�a�plumber,�financial�sector�goods�and�services�are�not�subject�to�VAT.�Because�of�this�exemption,�the�IMF�argues�that�the�financial�industry�has�an�advantage�over�the�rest�of�the�economy�and�that�money�has�been�directed�to�it�and�away�from�other�sectors.�They�conclude�that�“the�financial�sector�may�be…�‘too�big’”.19��Even�Lord�Turner,�Chairman�of�the�Financial�Services�Authority�has�called�the�sector�‘swollen’.�

Yet�the�UK�government�has�not�implemented�the�financial�sector�taxes�recommended�by�the�IMF�and�the�European�Commission.�Instead,�it�announced�swingeing�spending�cuts�and�a�rise�in�VAT�to�20%.�A�hike�in�VAT�hits�the�poor�hardest,�because�with�less�income,�a�higher�proportion�of�their�income�is�spent�on�consumption.20�Furthermore,�a�rise�in�VAT�will�tilt�our�fiscal�imbalance�even�further�in�favour�of�the�financial�sector�at�the�expense�of�the�rest�of�the�economy.

The�Robin�Hood�Tax�campaign�believes�that�rather�than�punishing�ordinary�people�for�the�financial�crisis,�we�should�be�looking�to�the�very�sector�that�got�us�into�this�mess�to�help�get�us�out.�So�far�the�government�has�implemented�a�disappointing�Bank�Levy�that�will�eventually�generate�only�£2.5�billion�a�year�in�the�UK�(and�be�partially�offset�by�the�government’s�decision�to�reduce�corporation�tax�from�28%�to�24%).�The�Robin�Hood�Tax�campaign�is�calling�on�George�Osborne�to�implement�financial�sector�taxes�of�£20�billion�a�year�in�the�UK.�By�comparison,�the�global�profits�and�bonus�pot�for�2010�is�likely�to�have�been�between�$600�billion�and�a�$1,000�billion�(a�trillion)�dollars.21

05HAS THERE BEEN ANY

PROGRESS GLOBALLY?

The�popular�momentum�behind�the�campaign�has�helped�make�financial�sector�taxes�a�mainstream�political�issue�around�the�world.�In�a�report�in�June�2010,�the�IMF�acknowledged�that�the�financial�sector�was�“under-taxed”�and�urged�governments�to�implement�new�financial�sector�taxes.�

In�Europe,�several�countries�have�come�out�in�support�of�a�Financial�Transaction�Tax.�President�Sarkozy�has�outlined�that�financial�sector�taxes�are�at�the�top�of�France’s�agenda�for�its�presidency�of�both�the�G8�and�G20,�and�has�commissioned�Bill�Gates�to�write�a�report�investigating�them�and�other�forms�of�innovative�finance�for�development..�The�German�government�is�already�planning�to�introduce�an�FTT�in�2012�or�2013,�and�countries�including�Spain,�Finland,�Austria�and�Belgium�are�also�in�favour.�The�European�Parliament�has�also�voted�in�favour�of�introducing�a�European-level�FTT�and�there�is�a�real�possibility�that�there�will�be�an�agreement�on�an�FTT�within�Europe�by�the�end�of�the�year.�

A�large�number�of�developing�countries�also�support�an�FTT.�Brazil�and�South�Africa�have�implemented�their�own�Financial�Transaction�Taxes,�while�the�South�African�Finance�Minister�has�said�he�is�in�favour�of�a�European-level�FTT.�At�the�2011�Spring�Meetings�of�the�International�Financial�Institutions,�20�low-income�Francophone�countries�said�they�support�a�broad-based�FTT.�

04WHAT HAS THE UK

GOVERNMENT DONE SO

FAR?

Chancellor�George�Osborne�introduced�a�Bank�Levy�in�January�2011�but�it�misses�the�mark�as�it�will�only�raise�£2.5�billion�annually,�and�doesn’t�ring�fence�any�money�to�help�the�people�hit�hardest�by�the�financial�crisis.�Reductions�in�corporation�tax�mean�the�actual�revenue�collected�is�even�lower.�

This�is�nowhere�near�enough.�So,�based�on�research�as�to�how�much�it�can�afford�to�pay,�we�are�calling�on�the�Chancellor�to�tax�the�UK’s�financial�sector�by�an�extra�£20�billion�a�year.�

One�of�the�reasons�the�government�has�not�done�more�is�the�immense�power�of�the�City�of�London�in�lobbying�and�influencing�politicians.�That�is�why�huge�public�pressure�is�needed�to�convince�the�government�it�is�more�costly�to�ignore�the�people�than�to�ignore�the�banks.�

06DOESN’T THE

FINANCIAL SECTOR

MAKE AN IMPORTANT

CONTRIBUTION TO OUR

ECONOMY?

Absolutely,�it�accounts�for�about�8%�of�UK�GDP.�A�healthy�and�robust�financial�sector�is�essential�to�our�society’s�well-being�as�it�lends�to�businesses�and�individuals�and�provides�high�street�banking�services.�However,�unfettered�by�regulation,�a�distinct�area�of�the�financial�sector�–�namely�casino-style�trading,�the�worst�of�which�is�the�high�frequency�trading�–�has�grown�out�of�control.�Lord�Turner,�Chairman�of�the�Financial�Services�Authority,�has�questioned�this�area’s�contribution,�calling�the�sector�‘swollen’�and�‘socially�useless’.�By�taxing�this�area�of�business�we�can�raise�much�needed�revenue�and�help�to�rebalance�our�economy�away�from�our�over-reliance�on�the�City�of�London.

The Robin�Hood�Tax�campaign�ultimately�wants�to�see�a�Financial�Transaction�Tax�introduced�that�would�raise�money�from�the�financial�world�and�curb�the�worst�aspects�of�its�behaviour.�High�frequency�trading�(HFT)�has�developed�to�such�an�extent�that�dealers�such�as�those�from�Tradebot�in�the�US�hold�a�stock�on�average�for�just�11�seconds.22 These purchases�aren’t�made�like�normal�business�decisions�because�they�take�no�account�of�the�fundamental�determinants�of�a�stock’s�worth,�but�instead�try�to�second-guess�other�market�participants’�actions�and�benefit�from�tiny�movements�in�price.�Computer�programs�trade�and�sell�large�volumes�in�very�short�time�periods,�generally�milliseconds�or�microseconds�(one�millionth�of�a�second).�“Tens�of�thousands�of�trades�are�executed�by�these�trading�machines�in�the�blink�of�an�eye,”�explains�Martin�Wheatly,�CEO�of�the�Securities�and�Future�Commission�in�Hong�Kong�and�former�deputy�chief�executive�of�the�London�Stock�Exchange,�“There�are�some�estimates�that�HFT�now�represents�60-70�per�cent�of�the�trading�volume�in�the�US�market.”23��A�similar�picture�exists�here�in�the�UK.��

Beyond�contributing�little�value�to�the�real�economy,�HFT�also�increases�volatility,�as�traders�make�large�gambles�on�very�small�changes�in�the�market.�This�volatility�is�illustrated�best�by�the�“flash�crash”�of�May�6,�2010�when�a�trader�sold�75�thousand�stocks�worth�USD�4.1�billion�in�20�minutes.�The�sudden�drop�in�value�spurred�high�frequency�traders�to�go�into�a�spiral�of�selling,�causing�US�stock�prices�to�plummet,�some�down�to�a�cent,�and�then�rebound�within�minutes.�

Many�serious�commentators�have�highlighted�the�dangers�of�this�process,�and�have�called�for�an�FTT�to�calm�this�frenzied�whirlpool�of�transactions.�This�includes�Martin�Wheatley,�the�new�head�of�the�Consumer�Protection�and�Markets�Authority�and�Lord�Turner,�head�of�the�Financial�Services�Authority.24

08WOULD THIS ONLY WORK

IF ALL COUNTRIES ACTED

TOGETHER?

International�agreement�would�be�great,�but�we�don’t�have�to�wait.�At�least�40�countries�around�the�globe�have�implemented�Financial�Transaction�Taxes�on�their�own.28 The UK�has�a�long�and�commendable�history�of�spearheading�new�approaches�to�financial�sector�taxation,�including�a�FTT�on�share�transactions,�known�as�the�Stamp�Duty�on�shares.�The�0.5%�Stamp�Duty�yields�£4�billion�a�year�and�hasn’t�stopped�the�London�Stock�Exchange�being�one�of�the�most�profitable�markets�in�the�world.�More�recently�the�UK�government�pressed�ahead�with�France�and�Germany�to�implement�the�£2.5�billion�bank�levy.�Momentum�is�building�behind�an�EU-wide�FTT,�but�it�is�entirely�possible�for�countries�to�lead�with�unilateral�action.�The�IMF�conclude�that�FTT’s�“do�not�automatically�drive�out�financial�activity�to�an�unacceptable�extent”.29

07CAN THE UK’S BANKS

AFFORD TO PAY £20

BILLION EXTRA?

Firstly,�we�are�asking�for�a�fairer�contribution�from�not�just�banks�but�from�the�entire�financial�sector�–�that’s�hedge�funds,�asset�managers�and�the�rest.�Furthermore,�the�Bank�of�England�have�estimated�that�by�underwriting�the�banks,�the�Treasury�provides�them�with�an�implicit�subsidy�worth�approximately�£100bn�a�year.25�It’s�clear�that�the�banks�are�under-taxed�(the�IMF�agrees),�and�as�a�result�there�is�plenty�of�spare�money�sloshing�about�in�the�financial�sector�as�their�latest�round�of�bonuses�shows.�They�can�easily�afford�to�pay�their�way.

The�UK�financial�sector’s�income�chargeable�to�tax�could�reach�£75�billion�in�2011,�25�per�cent�higher�than�in�2007-08.�Bonus�payments�could�be�as�much�as�£7�billion�in�the�same�year,�making�a�total�of�more�than�£80�billion.26�But�the�true�total�is�much,�much�higher�once�you�include,�for�example,�hedge�funds�that�are�registered�in�the�Cayman�Islands�and�trading�in�the�UK.�These�funds�are�notoriously�secretive,�but�in�just�six�months�the�ten�leading�hedge�funds�alone�made�$28bn�for�their�customers�in�the�second�half�of�2010.27��Add�to�this�commonly�used�‘creative’�accounting�techniques,�and�it�is�clear�that�the�financial�sector’s�true�total�profit�is�many�tens�of�billions�higher.�It�can�easily�afford�another�£20�billion.�

When�looking�at�taxes�you�have�to�compare�like�with�like.�Consider�what�taxes�you�have�to�pay.�Income�tax�is�paid�on�everything�you�earn.�The�equivalent�of�income�tax�for�the�financial�sector�is�corporation�tax�(which�will�be�reduced�from�28%�to�24%�as�a�result�of�the�2010�Emergency�Budget).�You�also�pay�VAT�on�most�goods�and�services�that�you�buy (which�was�increased�in�January�2011�to�20%�from�17.5%),�yet�incredibly�the�financial�sector�remains�VAT�exempt.� Each�time�a�financial�good�or�service�is�bought�not�a�penny of�VAT�is�paid.�

09WON’T COMPANIES

JUST AVOID THE TAX OR

MOVE THEIR BUSINESSES

OFFSHORE?

Critics�of�the�FTT�often�say�it�will�lead�to�a�mass�exodus�from�the�City.�This�claim�is�unsubstantiated�and�overblown.�It�is�used�as�a�bargaining�chip�by�the�banks�to�cajole�the�government�into�not�acting.�Before�looking�at�the�details,�to�illustrate�this,�here’s�an�anecdote:�Terry�Smith,�head�of�Tullett�Prebon,�a�City�broker,�famously�said�in�December�2009�that�he�would�allow�any�of�the�company’s�950�London-based�staff�to�move�overseas�before�the�Labour�governments�one-off�50%�supertax�on�bonuses�over�£25�thousand�came�into�force�in�December�2009.�The�Guardian�reported�on�14�April�2010�that�so�far�‘none�…�have�taken�him�up�on�the�offer.’30�Even�the�Financial�Times�has�argued�that�banks�threats�to�leave�“should�be�faced�down,�not�just�because�they�are�unreasonable�but�because�they�are�of�questionable�credibility”.31

FTTs�are�commonplace�and�have�raised�billions�of�dollars�of�predictable�revenue�without�serious�avoidance.�As�stated�by�the�IMF,�FTTs�(which�it�calls�STTs)�“are�certainly�feasible�as�witnessed�by�their�use�in�numerous�developed�countries.�The�fact�that�major�financial�centers�such�as�the�UK,�Switzerland,�Hong�Kong,�Singapore,�and�South�Africa�levy�forms�of�STTs�indicates�that�such�taxes�do�not�automatically�drive�out�financial�activity�to�an�unacceptable�extent.”32

The�lack�of�avoidance�stems�from�the�multiplicity�of�reasons�for�which�investors�trade�in�a�particular�location�–�reasons�that�hold�more�significance�than�the�domestic�tax�regime.�Consider�the�advantages�gained�by�investors�from�being�concentrated�in�one�marketplace�with�immediate�access�to�information,�support�services,�and�trading�partners.�The�gains�from�these�so-called�network�externalities�greatly�outweigh�the�potential�burden�from�Robin�Hood�Taxes,�and�would�mitigate�any�incentive�for�firms�to�move�to�an�untaxed�location�in�the�case�of�unilateral�implementation.�And�of�course,�banks�need�to�locate�in�a�country�with�a�big�enough�budget�to�bail�them�out�if�things�go�wrong.�There�are�not�many�governments�with�the�ability�or�willingness�to�provide�this�implicit�guarantee,�certainly�not�the�Cayman�Islands�or�even�Switzerland.

Furthermore,�time�zones�are�critical�for�financial�transactions,�with�London�being�ideally�situated�between�the�Asian�and�US�markets.�This�means�that�banks�and�other�financial�institutions�cannot�all�move�to�New�York�as�a�major�financial�

centre�will�still�be�needed�in�Europe.�Germany,�the�main�competitor�in�the�European�time�zone�is�already�committed�to�implementing�an�FTT.

Ideally�Robin�Hood�Taxes�would�be�implemented�internationally.�However,�in�working�towards�an�international�consensus,�individual�countries,�or�regions�like�the�EU,�can�and�should�take�the�lead�by�unilaterally�implementing�Robin�Hood�Taxes�within�their�own�market,�especially�as�the�evidence�so�far�shows�that�this�will�not�result�in�a�mad�dash�of�capital�out�of�the�countries�that�are�implementing�a�tax�on�their�financial�sectors.�

Global�currency�markets,�the�largest�financial�market�in�the�world�at�$4�billion�per�day,�in�which�speculators�have�been�free�to�reap�huge�profits�at�the�expense�of�wider�society,�offer�a�clear�first�step�for�FTT�implementation.�Every�high�value�Sterling�transaction,�no�matter�where�in�the�world�it�takes�place�–�New�York,�Johannesburg,�or�Timbuktu�–�is�settled�via�the�Continuous�Linked�Settlement�(CLS)�Bank,�making�a�FTT�on�currency�transactions�impossible�to�avoid.�But�even�with�other�Robin�Hood�Taxes,�the�assertion�that�they�will�lead�to�a�mass�exodus�is�unfounded.

For�example,�the�UK’s�existing�stamp�duty�on�share�purchases�applies�to�all�trading�in�shares�listed�in�the�UK,�no�matter�where�the�trade�takes�place.�If�a�share�of�a�company�listed�in�London�changes�hands�anywhere�in�the�world,�then�UK�stamp�duty�is�payable.�Moving�your�trading�business�out�of�the�UK�doesn’t�help�you�avoid�the�tax.

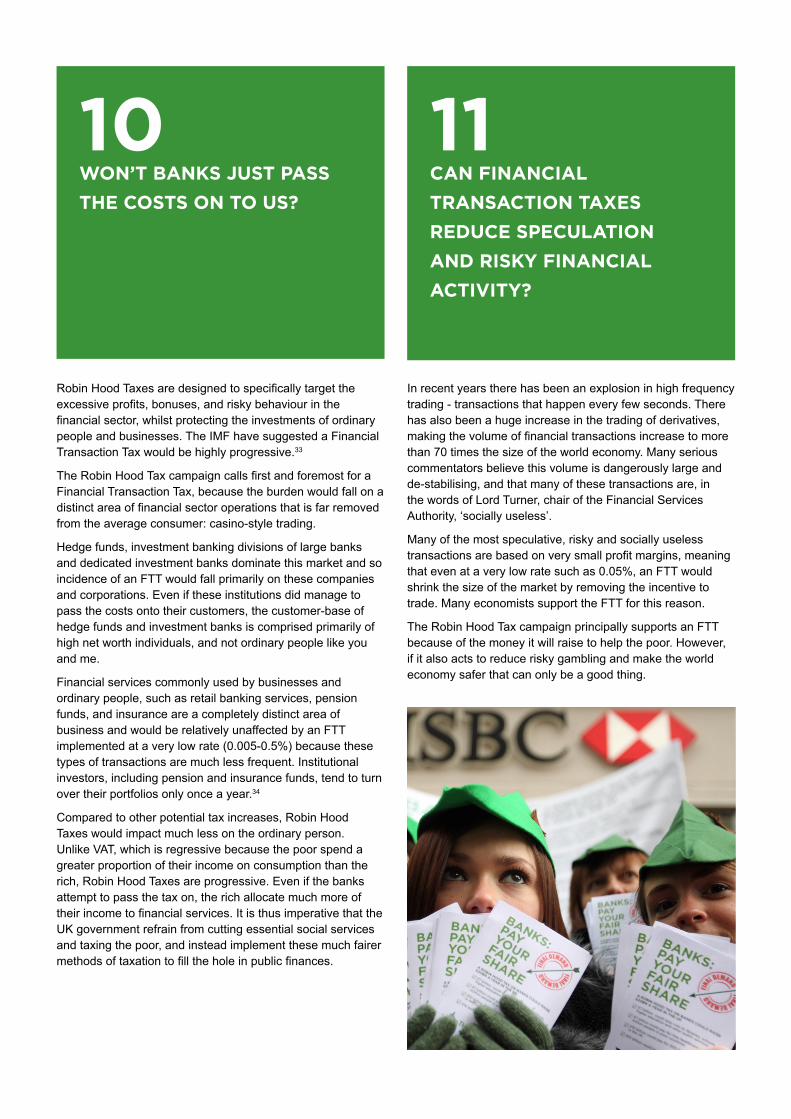

11CAN FINANCIAL

TRANSACTION TAXES

REDUCE SPECULATION

AND RISKY FINANCIAL

ACTIVITY?

10WON’T BANKS JUST PASS

THE COSTS ON TO US?

Robin�Hood�Taxes�are�designed�to�specifically�target�the�excessive�profits,�bonuses,�and�risky�behaviour�in�the�financial�sector,�whilst�protecting�the�investments�of�ordinary�people�and�businesses.�The�IMF�have�suggested�a�Financial�Transaction�Tax�would�be�highly�progressive.33

The�Robin�Hood�Tax�campaign�calls�first�and�foremost�for�a�Financial�Transaction�Tax,�because�the�burden�would�fall�on�a�distinct�area�of�financial�sector�operations�that�is�far�removed�from�the�average�consumer:�casino-style�trading.�

Hedge�funds,�investment�banking�divisions�of�large�banks�and�dedicated�investment�banks�dominate�this�market�and�so�incidence�of�an�FTT�would�fall�primarily�on�these�companies�and�corporations.�Even�if�these�institutions�did�manage�to�pass�the�costs�onto�their�customers,�the�customer-base�of�hedge�funds�and�investment�banks�is�comprised�primarily�of�high�net�worth�individuals,�and�not�ordinary�people�like�you�and�me.

Financial�services�commonly�used�by�businesses�and�ordinary�people,�such�as�retail�banking�services,�pension�funds,�and�insurance�are�a�completely�distinct�area�of�business�and�would�be�relatively�unaffected�by�an�FTT�implemented�at�a�very�low�rate�(0.005-0.5%)�because�these�types�of�transactions�are�much�less�frequent.�Institutional�investors,�including�pension�and�insurance�funds,�tend�to�turn�over�their�portfolios�only�once�a�year.34

Compared�to�other�potential�tax�increases,�Robin�Hood�Taxes�would�impact�much�less�on�the�ordinary�person.�Unlike�VAT,�which�is�regressive�because�the�poor�spend�a�greater�proportion�of�their�income�on�consumption�than�the�rich,�Robin�Hood�Taxes�are�progressive.�Even�if�the�banks�attempt�to�pass�the�tax�on,�the�rich�allocate�much�more�of�their�income�to�financial�services.�It�is�thus�imperative�that�the�UK�government�refrain�from�cutting�essential�social�services�and�taxing�the�poor,�and�instead�implement�these�much�fairer�methods�of�taxation�to�fill�the�hole�in�public�finances.

In�recent�years�there�has�been�an�explosion�in�high�frequency�trading�-�transactions�that�happen�every�few�seconds.�There�has�also�been�a�huge�increase�in�the�trading�of�derivatives,�making�the�volume�of�financial�transactions�increase�to�more�than�70�times�the�size�of�the�world�economy.�Many�serious�commentators�believe�this�volume�is�dangerously�large�and�de-stabilising,�and�that�many�of�these�transactions�are,�in�the�words�of�Lord�Turner,�chair�of�the�Financial�Services�Authority,�‘socially�useless’.�

Many�of�the�most�speculative,�risky�and�socially�useless�transactions�are�based�on�very�small�profit�margins,�meaning�that�even�at�a�very�low�rate�such�as�0.05%,�an�FTT�would�shrink�the�size�of�the�market�by�removing�the�incentive�to�trade.�Many�economists�support�the�FTT�for�this�reason.�

The�Robin�Hood�Tax�campaign�principally�supports�an�FTT�because�of�the�money�it�will�raise�to�help�the�poor.�However,�if�it�also�acts�to�reduce�risky�gambling�and�make�the�world�economy�safer�that�can�only�be�a�good�thing.�

1.�McCulloch,�N.,�and�Pacillo,�G.,�2010.�The�Tobin�Tax�–�A�Review�of�the�Evidence.�Institute�of�Development�Studies.�University�of�Sussex,�UK

2.�Financial�Transaction�Taxes�have�been�implemented�in�Argentina,�Australia,�Austria,�Belgium,�Brazil,�Chile,�China,�Colombia,�Denmark,�Ecuador,�Finland,�France,�Germany,�Greece,�Guatemala,�Hong�Kong,�India,�Indonesia,�Ireland,�Italy,�Japan,�Malaysia,�Morocco,�Netherlands,�New�Zealand,�Pakistan,�Panama,�Peru,�Philippines,�Portugal,�Russia,�Singapore,�South�Africa,�South�Korea,�Sweden,�Switzerland,�Taiwan,�UK,�US,�Venezuela�and�Zimbabwe.�See�Pollin,�R.�2005.�‘Applying�a�Securities�Transaction�Tax�to�the�US.�Design�Issues,�Market�Impact,�and�Revenue�Estimates,’�in�Epstein�G�(ed)�Financialization�and�the�World�Economy.�Edward�Elgar�

3.�European�Commission.�2010.�Financial�Sector�Taxation.�Commission�Staff�Working�Document.�Brussels,�Belgium.�

4.�Leading�Group�on�Innovative�Financing�for�Development,�2010.�Globalizing�Solidarity:�The�Case�for�Financial�Levies.�Also�Schmidt,�R.�2010.�The�Financial�Transaction�Tax:�Feasibility�of�taxing�OTC�derivatives�transactions.�The�North-South�Institute.�Forthcoming.

5.�Bank�of�England,�June�2010.�Financial�Stability�Report.�

6.�http://www.ft.com/cms/s/0/72402fea-2d6f-11e0-8f53-00144feab49a.html#axzz1GwrPQXT0,�accessed�on�18th�March�2011

7.�Save�the�Children,�February�2011,�Severe�Child�Poverty:�Nationally�and�Locally

8.�Dolphin,�T.,�and�Chappal,�L.�2010.�The�Effect�of�the�Global�Financial�Crisis�on�Emerging�and�Developing�Economies.�Institute�for�Public�Policy�Research.�London,�UK

9.�Friedman,�J.,�and�Schady,�N.�(2009)�How�Many�More�Infants�Are�Likely�to�Die�in�Africa�as�a�Result�of�the�Global�Financial�Crisis?�Policy�Research�Working�Paper�5023.�World�Bank.�Washington�DC,�USA

10.�Ravallion,�M.�2009.�The�Crisis�and�the�World’s�Poorest,�Development�Outreach.�World�Bank�Institute.�Washington�DC,�USA

11.�Dolphin,�T.,�and�Chappal,�L.�2010.�The�Effect�of�the�Global�Financial�Crisis�on�Emerging�and�Developing�Economies.�Institute�for�Public�Policy�Research.�London,�UK

12.�The�World�Bank�Group,�World�Development�Report�2010

13.�Stern,�N.�2006.�The�Stern�Review�on�the�Economics�of�Climate�Change.�HM�Treasury.�London,�UK

14.�Munich�Climate�Insurance�Initiative.�2009.�Climate�Risk�Management�Mechanisms�including�Insurance,�in�the�context�of�Adaptation�to�Climate�Change.�Submitted�to�the�on�UNFCCC�24�April�2009�

15.�The�IMF�says�the�cost�of�the�bailout�to�the�UK�was�5.4%,�that�the�advanced�G20�economies�will�see�an�increase�in�debt�of�40%,�and�that�the�countries�‘that�experienced�a�systemic�crisis’�[confirmed�by�the�IMF�as�the�UK,�US�and�Germany]�will�experience�an�eventual�overall�loss�of�output�equivalent�to�27%�of�GDP.�UK�GDP�in�2008�was�2,�674�billion�dollars.�

16.�http://www.independent.co.uk/news/business/news/mervyn-king-never-has-so-much-money-been-owed-by-so-few-to-so-many-1806247.html;�accessed�on�21/3/11.

17.�Schulmeister,�S.�2009.�A�General�Financial�Transaction�Tax:�A�Short�Cut�of�the�Pros,�the�Cons,�and�a�Proposal.�Working�Paper�No.�344.�Östreichisches�Institut�Für�Wirtschaftsforschung.

18.�Claessens,�S.,�Keen,�M.,�Pazarbasioglu,�C.�2010.�Financial�Sector�Taxation.� The�IMF’s�Report�to�the�G-20�and�Background�Material.�International�Monetary�Fund.�Washington�DC,�USA

19.�Claessens,�S.,�Keen,�M.,�Pazarbasioglu,�C.�2010.�Financial�Sector�Taxation.� The�IMF’s�Report�to�the�G-20�and�Background�Material.�International�Monetary�Fund.�Washington�DC,�USA

20.�VAT�takes�up�12.1%�of�the�income�of�the�poorest�20%,�compared�to�5.9%�of�the�richest�20%.�Barnard,�A.�(2009)�The�effects�of�taxes�and�benefits�on�household�income,�2007/08,�Economic�&�Labour�Market�Review,�Vol.�3,�No�8,�August�2009,

21.�Estimates�from�Murphy,�R,�Taxing�Banks,�http://www.taxresearch.org.uk/Documents/IMFTaxingBanks.pdf�and�Kapoor,�S.�(2010)�Financial�Transaction�Taxes:�Tools�for�Progressive�Taxation�and�Improving�Market�Behaviour,�http://robinhoodtax.org.uk/files/ReDefine-FTTs-as-tools-for-progressive-taxation-and-improving-market-behaviour.pdf�

12ENDNOTES

22.�http://dealbook.nytimes.com/2010/05/17/speedy-new-traders-make-waves-far-from-wall-st/

23.�Wheatley,�M.�2010.�‘We�need�rules�to�limit�the�risks�of�superfast�trades.’�Financial�Times.�Published�20�September�2010�on�FT.com�

24.�http://www.ft.com/cms/s/0/ad7f31f6-c4cd-11df-9134-00144feab49a.html#axzz1H9xo7RF3,�and�http://www.fsa.gov.uk/pages/Library/Communication/Speeches/2011/0218_at.shtml�

25.�Bank�of�England,�June�2010.�Financial�Stability�Report.�

26.�Source:�http://www.guardian.co.uk/politics/2011/jan/10/banks-unlimited-bonuses-ministers.�Accessed�on�7/4/11

27.�Source:�http://www.guardian.co.uk/business/2011/mar/02/hedge-funds-bounce-back-79bn-pounds-profit.�Accessed�on�7/4/11

28.�Financial�transaction�taxes�have�been�implemented�in�Argentina,�Australia,�Austria,�Belgium,�Brazil,�Chile,�China,�Colombia,�Denmark,�Ecuador,�Finland,�France,�Germany,�Greece,�Guatemala,�Hong�Kong,�India,�Indonesia,�Ireland,�Italy,�Japan,�Malaysia,�Morocco,�Netherlands,�New�Zealand,�Pakistan,�Panama,�Peru,�Philippines,�Portugal,�Russia,�Singapore,�South�Africa,�South�Korea,�Sweden,�Switzerland,�Taiwan,�UK,�US,�Venezuela�and�Zimbabwe.�See�Pollin,�R.�2005.�‘Applying�a�Securities�Transaction�Tax�to�the�US.�Design�Issues,�Market�Impact,�and�Revenue�Estimates,’�in�Epstein�G�(ed)�Financialization�and�the�World�Economy.�Edward�Elgar

29.�Claessens,�S.,�Keen,�M.,�Pazarbasioglu,�C.�2010.�Financial�Sector�Taxation.�The�IMF’s�Report�to�the�G-20�and�Background�Material.�International�Monetary�Fund.�Washington�DC,�USA

30.�Teather,�D.�2010.�‘City�veteran�Terry�Smith�pockets�£4m�bonus.’�Guardian.�Published�14�April�2010�on�guardian.co.uk�

31.�http://www.ft.com/cms/s/0/2e6ba9a6-49bd-11e0-acf0-00144feab49a.html#axzz1G7ES1kdG,�accessed�on�9/3/11.

32.�Claessens,�S.,�Keen,�M.,�Pazarbasioglu,�C.�2010.�Financial�Sector�Taxation.�The�IMF’s�Report�to�the�G-20�and�Background�Material.�International�Monetary�Fund.�Washington�DC,�USA

33.�Claessens,�S.,�Keen,�M.,�Pazarbasioglu,�C.�2010.�Financial�Sector�Taxation.�The�IMF’s�Report�to�the�G-20�and�Background�Material.�International�Monetary�Fund.�Washington�DC,�USA

43.�Kapoor,�S.�2010.�Financial�Transaction�Taxes:�Tools�for�Progressive�Taxation�and�Improving�Market�Behaviour.�Re-Define.

![Robin Hood[1]](https://static.documents.pub/doc/80x56/577d21d71a28ab4e1e960121/robin-hood1.jpg)