DOI: 10.1111/j.1475-679X.2012.00455.x Journal of Accounting Research Vol. 00 No. 00 xxxx 2012 Printed in U.S.A. The Role of Bank Reputation in “Certifying” Future Performance Implications of Borrowers’ Accounting Numbers ROBERT M. BUSHMAN ∗ AND REGINA WITTENBERG-MOERMAN † Received 3 January 2011; accepted 14 February 2012 ABSTRACT We investigate the role played by the reputation of lead arrangers of syndi- cated loans in mitigating information asymmetries between borrowers and lenders. We hypothesize that syndications by more reputable arrangers are indicative of higher borrower quality at loan inception and more rigorous monitoring during the term of the loan. We investigate whether borrowers with more reputable lead arrangers realize superior performance subsequent to loan origination relative to borrowers with less reputable arrangers. We fur- ther examine whether certification by high-reputation lead banks extends to ∗ Kenan-Flagler Business School, The University of North Carolina at Chapel Hill; † The University of Chicago Booth School of Business Accepted by Phil Berger. We thank the editor, an anonymous reviewer, Dan Amiram, Ray Ball, Ryan Ball, Douglas Diamond, Merle Erickson, Rich Frankel, Christian Leuz, Michael Minnis, David Ross, Florin Vasvari, Jieying Zhang, and participants at the 2010 Dopuch Con- ference at Washington University, the 2010 Duke/UNC Fall Camp, 2010 Financial Economics and Accounting Conference at the University of Maryland, the 2010 Stanford Summer Camp and seminar participants at Indiana University, Tsinghua University, and the University of Texas at Dallas for helpful comments. We thank the Thomson Reuters Loan Pricing Corpora- tion for providing loan data. We gratefully acknowledge the financial support of the Kenan- Flagler Business School, The University of North Carolina at Chapel Hill, and the University of Chicago Booth School of Business. Regina Wittenberg-Moerman also gratefully acknowledges the financial support of the Neubauer Family Fellowship. 1 Copyright C , University of Chicago on behalf of the Accounting Research Center, 2012

Transcript

DOI: 10.1111/j.1475-679X.2012.00455.xJournal of Accounting Research

Vol. 00 No. 00 xxxx 2012Printed in U.S.A.

The Role of Bank Reputation in“Certifying” Future Performance

Implications of Borrowers’Accounting Numbers

R O B E R T M . B U S H M A N ∗ A N D R E G I N AW I T T E N B E R G - M O E R M A N †

Received 3 January 2011; accepted 14 February 2012

ABSTRACT

We investigate the role played by the reputation of lead arrangers of syndi-cated loans in mitigating information asymmetries between borrowers andlenders. We hypothesize that syndications by more reputable arrangers areindicative of higher borrower quality at loan inception and more rigorousmonitoring during the term of the loan. We investigate whether borrowerswith more reputable lead arrangers realize superior performance subsequentto loan origination relative to borrowers with less reputable arrangers. We fur-ther examine whether certification by high-reputation lead banks extends to

∗Kenan-Flagler Business School, The University of North Carolina at Chapel Hill; †TheUniversity of Chicago Booth School of Business

Accepted by Phil Berger. We thank the editor, an anonymous reviewer, Dan Amiram, RayBall, Ryan Ball, Douglas Diamond, Merle Erickson, Rich Frankel, Christian Leuz, MichaelMinnis, David Ross, Florin Vasvari, Jieying Zhang, and participants at the 2010 Dopuch Con-ference at Washington University, the 2010 Duke/UNC Fall Camp, 2010 Financial Economicsand Accounting Conference at the University of Maryland, the 2010 Stanford Summer Campand seminar participants at Indiana University, Tsinghua University, and the University ofTexas at Dallas for helpful comments. We thank the Thomson Reuters Loan Pricing Corpora-tion for providing loan data. We gratefully acknowledge the financial support of the Kenan-Flagler Business School, The University of North Carolina at Chapel Hill, and the University ofChicago Booth School of Business. Regina Wittenberg-Moerman also gratefully acknowledgesthe financial support of the Neubauer Family Fellowship.

the quality of borrowers’ reported accounting numbers. Controlling for en-dogenous matching of borrowers and lead banks, we find that higher bankreputation is associated with higher profitability and credit quality in thethree years subsequent to loan initiation. We also show that bank reputationis associated with long-run sustainability of earnings via higher earnings per-sistence, and debt contracting value of accounting via a stronger connectionbetween pre-loan profitability and future credit quality. We further documentthat the enhanced earnings sustainability associated with higher reputationlead banks reflects both superior fundamentals and accruals more closelylinked with future cash flows.

1. Introduction

Information asymmetries create frictions that can impact the costs ofraising external funds. In this paper, we investigate the role played by thereputation of the lead arrangers of syndicated loans in mitigating informa-tion asymmetries between borrowers and lenders. By investing in rigorouspre-loan evaluations of borrowers’ quality and post-loan monitoring of bor-rowers’ performance, a bank can establish a strong reputation as a leadarranger via a track record of successful loans. We hypothesize that syndi-cations by more reputable arrangers indicate higher borrower quality atloan inception and more rigorous monitoring during the term of the loan.To examine this hypothesis, we investigate whether borrowers with morereputable arrangers realize superior performance subsequent to loan orig-ination, relative to borrowers with less reputable arrangers. We further ex-amine whether the quality certification supplied by high-reputation leadbanks extends to the quality of a borrower’s reported accounting numbers.

Syndicated lending, in which multiple lenders lend to a firm under acommon contract, is an interesting setting for analyzing the role of reputa-tion in certifying firm quality. Agency problems arise because lead banks’privileged access to borrowers may reveal private information not availableto other syndicate members, and a bank’s due diligence and monitoringefforts are not observable (e.g., Lee and Mullineaux [2004], Sufi [2007],Ivashina [2009]). Further, the lead bank’s formal contractual incentives toscreen and monitor are limited, as the fraction of loans retained by leadbanks is relatively small. The confluence of unobservable effort and insuffi-cient contractual incentives with the repeated nature of the syndicated loanmarket creates a role for reputation. By observing outcomes of previouslyarranged loans, market participants can assess the extent to which a bankprovides superior screening and monitoring on behalf of other investors.

A recent literature supports the importance of lead arranger reputationin syndicated lending by examining the consequences for lead banks of aborrower’s failure. Lin and Paravisini [2011] exploit large corporate fraudsand find that, consistent with reputation loss, lead banks of loans to firmswhere fraud is discovered hold larger fractions of loans they syndicate fol-lowing fraud discovery. Gopalan, Nanda, and Yerramilli [2011] focus on

ROLE OF BANK REPUTATION 3

Chapter 11 bankruptcies, showing that, following defaults, lead arrangersretain larger fractions of subsequent loans they syndicate, and are less likelyto syndicate loans and attract participant lenders.1

There is also an extensive literature documenting that loan announce-ments generate positive abnormal stock returns for borrowers.2 It is alsodocumented that these stock price responses are relatively more favorablefor loans syndicated by higher reputation banks (Billett, Flannery, andGarfinkel [1995], Ross [2010]), suggesting that bank reputation certifiesborrower quality. Ross [2010] further shows that the impact of a lead bank’sreputation on abnormal returns is stronger for more opaque borrowerswhere certification is likely more important.

This evidence is consistent with existing theories of financial interme-diary’s reputation. For example, Chemmanur and Fulghieri [1994a] showthat higher reputation banks have incentives to perform more rigorous pre-loan evaluations of borrowers’ unobservable prospects than do lower rep-utation banks. Thus, in equilibrium, high-reputation banks are more likelyto lend to borrowers with superior future prospects, reflecting favorably onthese unobservable prospects.

We extend prior literature by examining the relation between lead ar-ranger reputation and two aspects of borrowers’ performance followingloan origination: future profitability and future credit quality. Further, weinvestigate whether reputation is associated with long-run sustainability ofearnings and enhanced debt contracting value of accounting information,as reflected in a stronger relation between borrowers’ accounting numbersreported just prior to loan origination and future performance outcomes.3

Consistent with prior research (e.g., Sufi [2007], Ross [2010]), we mea-sure bank reputation based on lead banks’ market share in the syndicatedloan market.4 To isolate the future performance implications of the certi-fication role of reputation, we control for what are likely to be strong se-lection effects underpinning the matching of borrowers and lead banks.For example, borrowers with better future prospects or higher quality ac-counting may choose more reputable arrangers. Alternatively, reputablearrangers may choose to contract with borrowers likely to be lucrative con-sumers of the bank’s services in the future. We employ a matching frame-work to explicitly control for observable and unobservable factors that

1 The results in Gopalan, Nanda, and Yerramilli [2011] and Lin and Paravisini [2011] sug-gest that lead bank reputation substitutes for contractual skin in the game. We discuss this inmore detail in section 2. In section 6.2, we examine the impact of fraud on the certificationrole of reputation.

2 See James and Smith [2000] for a review of the empirical literature. Maskara andMullineaux [2011] question these studies by examining the role of self-selection in deter-mining which banks announce their loans. See also Boot [2000] and Saunders and Cornett[2004] for reviews of the special role of banks.

3 Ball, Bushman, and Vasvari [2008] define the debt contracting value of accounting as theability of accounting numbers to capture deterioration in credit quality on a timely basis.

4 In section 2, we discuss in depth this measure of reputation and its potential limitations.

4 ROBERT M. BUSHMAN AND REGINA WITTENBERG-MOERMAN

impact both the likelihood of a borrower dealing with a high-reputationbank and the borrower’s future performance (Heckman and Navarro-Lozano [2004], Ross [2010]).5 We control for observable factors that in-fluence borrower-bank matching, including borrowers’ past performance,historical persistence of earnings, extreme accruals, earnings volatility, andthe potential for cross-selling services to the borrower. Further, we includevariables based on the location of borrowers relative to potential lendersthat determine borrower–arranger matching, but that are independentof borrowers’ future performance. To investigate whether certification byhigh-reputation lead banks extends to the quality of borrowers’ reportedaccounting numbers, we estimate endogenous switching regressions sepa-rately for high and low reputation partitions.

Turning to our results, we document that higher lead arranger reputa-tion is associated with higher profitability and credit quality in the threeyears subsequent to loan initiation.6 With respect to accounting quality, wefind that earnings persistence is higher for borrowers with high-reputationlead banks than for those with lower reputation lead banks, implying thatborrower profitability reported at loan origination is more sustainable forhigh reputation banks. We also show that borrowers with high-reputationlead arrangers exhibit enhanced debt contracting value of accounting, asindicated by a stronger connection between pre-loan profitability and fu-ture credit quality.

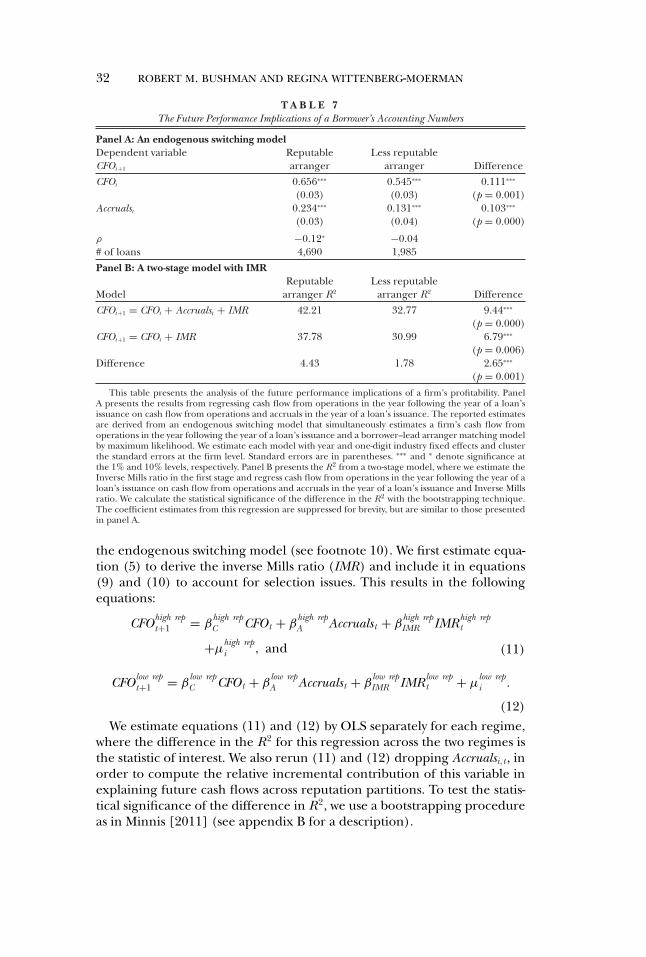

Finally, we examine whether the higher earnings sustainability associatedwith high-reputation lead banks is a consequence of better fundamentals,higher accrual quality, or both. We follow Minnis [2011] and regress one-year-ahead cash flows from operations on the contemporaneous cash flowand accrual components of earnings separately for the high and low rep-utation partitions. We find that borrowers with high-reputation banks ex-hibit higher cash flow persistence and significantly greater accruals quality.Accruals of borrowers with high-reputation lead banks are more stronglyrelated to future cash flows than are accruals of other borrowers.

While we acknowledge that we may not have controlled for all possi-ble alternative explanations, the totality of our results is consistent withthe proposition that lead bank reputation certifies the quality of borrow-ers and that this certification extends to the quality of borrowers’ account-ing numbers at loan inception. These results contribute to the literatureacross several dimensions. First, while a large literature examines relations

5 Private lending presents the possibility that private information, unobservable to the re-searcher, underpins both the decisions that determine bank-borrower matching and borrow-ers’ future performance. We also employ alternative specifications, finding that all results arerobust to using OLS, propensity matching, and firm fixed effect specifications.

6 For example, in the third year following loan origination, borrowers with reputable ar-rangers report profitability that is 2.0 percentage points higher and credit ratings that are 2.5notches lower (lower numerical ratings indicate higher credit quality) relative to borrowerswith less reputable arrangers.

ROLE OF BANK REPUTATION 5

between auditor characteristics and accounting quality, less is known aboutthe role of financial intermediaries in establishing the credibility of ac-counting numbers.7 Lee and Masulis [2011] examine the link between un-derwriter reputation and earnings management and Agrawal and Cooper[2010] examine the effect of venture capitalist reputation on restatements.We extend these studies by documenting that lead bank reputation is as-sociated with higher earnings and cash flow persistence, and with earn-ings that more strongly predict future credit quality. Our results suggestthat the process of establishing the credibility of accounting reports oper-ates through multiple channels, where intermediaries other than auditorsuse their reputation to certify firms’ accounting numbers.

Second, we add to the literature on the role of intermediary reputation inmitigating financial contracting frictions. We extend Ross [2010] by estab-lishing that the higher stock returns associated with announcements that ahigh-reputation bank syndicates a loan are consistent with reputation cer-tifying borrowers’ quality, as reflected by their future performance. Thisevidence of superior economic and accounting quality of borrowers withhigh reputation lead banks also complements Lin and Paravisini [2011]and Gopalan, Nanda, and Yerramilli [2011], who, by establishing that abank’s reputation and skin in the game are substitutes in syndicated lend-ing, show the importance of reputation for lead banks’ screening and mon-itoring incentives.

Third, our result that pre-loan profitability better predicts future creditquality for borrowers of higher reputation lead banks contributes directly tothe debt contracting literature, which posits that accounting quality is a de-terminant of a borrower’s credit risk (e.g., Francis et al. [2005], Ashbaugh-Skaife, Collins, and LaFond [2006], Zhang [2007], Bharath, Sunder, andSunder [2008]). Our analysis suggests that the debt contracting value of ac-counting also depends on the reputation of the lead bank arranging a loan.Our evidence also implies that borrowers endowed with favorable futureprospects, but facing significant investor uncertainty over their accountingquality, can mitigate this uncertainty by having a high-reputation lead bankcredibly certify its accounting quality.

The rest of the paper is organized as follows. Section 2 presents the con-ceptual basis of reputation certification. Section 3 discusses our empiricaldesign and econometric approach to self-selection issues. Section 4 de-scribes the sample and data and presents descriptive statistics, while sec-tion 5 presents our main results. Section 6 discusses robustness issues andsection 7 concludes.

7 Existing literature finds that auditor reputation is associated with fewer accounting errorsand irregularities (Defond and Jiambalvo [1991]), less IPO underpricing (Beatty [1993]),higher earnings response coefficients (Teoh and Wong [1993]), lower abnormal accruals(Becker et al. [1998]), more predictive post-IPO delistings (Weber and Willenborg [2003]),and lower cost of public debt (Lou and Vasvari [2011]). See Francis [2004] for a review of theliterature.

6 ROBERT M. BUSHMAN AND REGINA WITTENBERG-MOERMAN

2. Conceptual Basis of Reputation Certification

It has long been posited that financial intermediaries play a key role ascredible producers of information to market participants. One importantmechanism for projecting credibility is reputation (e.g., Leland and Pyle[1977], Campbell and Keracaw [1980], Diamond [1984]). Klein and Lef-fler [1981], DeAngelo [1981], and Shapiro [1983], among others, demon-strate that reputable firms have incentives to supply high-quality goods tothe market. In equilibrium, rents flow to firms as compensation for invest-ments in reputational capital, and such rents bond the firm to good behav-ior since it is vulnerable to a loss of rents if shirking is detected.

The literature applies this reputational capital paradigm to the certifica-tion role of financial intermediaries. Important theoretical contributionsinclude Baron [1982] and Booth and Smith [1986], who examine the roleof investment bankers in certifying the issuance of equity and risky debt se-curities. Numerous papers examine the role of financial intermediary rep-utation in equity underwriting (e.g., Beatty and Ritter [1986], Carter andManaster [1990], Nanda and Yun [1997], Fernando, Gatchev, and Spindt[2005]), supporting the importance of reputation in certifying initial andsecondary public offerings. Intermediary reputation has also been empha-sized in additional financial market settings, such as bond underwriting(Fang [2005]), venture capital (e.g., Hsu [2004], Nahata [2008], Krishnanet al. [2011]) and auditing (e.g., DeAngelo [1981], Titman and Trueman[1986], Bachar [1989], Datar, Feltham, and Hughes [1991], Ball, Jayara-man, and Shivakumar [2012]).

While reputation may be somewhat less important in the syndicated loanmarket relative to other settings, such as the equity market, where manyplayers are individual investors rather than sophisticated institutions, thenature of syndicated lending and the role played by lead banks create apotentially important role for reputation. Lead arrangers establish rela-tionships with borrowers, perform pre-loan due diligence, negotiate con-tract terms and monitor borrowers after loans are made. These actionsprovide them with access to borrowers’ private information not availableto other syndicate participants. This privileged access to information, to-gether with unobservability of due diligence and monitoring efforts, createagency problems (e.g., Lee and Mullineaux [2004], Sufi [2007], Ivashina[2009]). Further, while syndicate participants include large banks with in-dependent lending arrangements with borrowers, many syndicate partic-ipants are smaller banks and nonbank institutional investors (collateral-ized loan obligations, hedge funds, pension funds, and insurance compa-nies), who became major players in the syndicated loan market in the lastdecade (Bushman, Smith, and Wittenberg-Moerman [2010], Ivashina andSun [2011]). Small banks and institutional investors typically do not haveestablished relationships with borrowers and therefore rely heavily on leadbanks’ monitoring and due diligence.

In addition, the fraction of syndicated loans retained by the lead bank(i.e., the bank’s skin in the game) is relatively small. Sufi [2007] shows that

ROLE OF BANK REPUTATION 7

the mean (median) fraction of loans retained by the lead bank is 28.5%(23.5%). Therefore, the lead bank’s contractual incentives to screen andmonitor are limited. Further, the syndicated loan market is characterizedby repeated transactions between lead banks and participants. Unobserv-able screening and monitoring efforts, insufficient formal contractual in-centives, and the repeated nature of the syndicated lending suggest that abank’s reputation may be a vital mechanism in the syndicated loan market.

A key premise of certification is that an intermediary’s reputation is en-hanced by positive outcomes and damaged by negative outcomes. Lin andParavisini [2011] examine the effect of frauds by Enron, WorldCom, andothers on the lead arrangers of their loans outstanding during the fraudperiod, including some of the most reputable arrangers in the syndicatedloan market, such as J.P. Morgan Chase, Bank of America, and Citigroup.They find that, consistent with reputation loss, these lead banks hold alarger fraction of the loans they arrange following the frauds’ discovery.Further, Gopalan, Nanda, and Yerramilli [2011] find that when lead banks’borrowers are subject to Chapter 11 bankruptcy, the banks are less likelyto syndicate subsequent loans and attract participant lenders, and retainlarger fractions of loans they syndicate.

Pertinent to our analysis, Chemmanur and Fulghieri [1994a] modelthe ex ante evaluation of borrowers by banks. In their model, firms withunobservable future prospects seek to raise external financing, while banksevaluate a firm’s future prospects before agreeing to accept them as clients.More rigorous pre-deal screening increases the likelihood that borrowerswith poor prospects are discovered and denied loans, but more rigorousevaluation is more costly to the bank. Borrowers who pass more rigorousevaluation will perform better on average relative to firms granted financ-ing based on less rigorous evaluation. However, banks’ choice of rigor isnot observable to outsiders, and so investors assess a bank’s reputation forsupplying rigorous evaluations by conditioning on observable outcomes ofpast transactions sponsored by the bank. In equilibrium, higher reputationbanks adopt more rigorous evaluation standards than lower reputationbanks do, and so are more likely to transact with firms with superior futureprospects.

Also, Chemmanur and Fulghieri [1994b] develop a model where rep-utation provides banks with endogenous incentives to devote more re-sources to information production about firms that subsequently becomefinancially distressed. Investors believe that more reputable banks supply agreater ex post monitoring effort, and, in equilibrium, they do. Together,Chemmanur and Fulghieri [1994a,b] suggest that syndications by morereputable arrangers should indicate higher borrower quality at loan incep-tion and more rigorous monitoring during the term of the loan.

Consequently, if borrowers’ true quality is not publicly observable andhigh-reputation banks are more likely to transact with better borrowers,then the fact that a high-reputation bank contracts with a borrower revealsfavorable information about the borrower’s future prospects. However, it

8 ROBERT M. BUSHMAN AND REGINA WITTENBERG-MOERMAN

is also possible that borrowers with better future prospects or higher qual-ity accounting simply choose more reputable arrangers. Thus, empiricallyisolating the future performance implications of reputation is complicatedby potential selection effects underpinning the matching of borrowers andlead banks.

Ideally, we would like to examine a setting where borrowers are randomlyassigned to high- and low-reputation banks, and banks then choose withwhich borrowers to contract. This would allow us to cleanly isolate whetherthe act of a high-reputation bank accepting a borrower reflects favorablyon the borrower’s quality. In the absence of such a setting, our empiri-cal challenge is to control for the factors, observable and unobservable, thatsimultaneously impact the likelihood of a borrower dealing with a high-reputation bank and the borrower’s future performance. To address thischallenge, we employ an endogenous matching framework (Heckman andNavarro-Lozano [2004], Fang [2005], Ross [2010]). We control for observ-able factors that may simultaneously influence borrower-bank matchingand a borrower’s future performance, including its past performance, his-torical earnings persistence, extreme accruals, earnings volatility, and thecross-selling potential of banking services. We also include variables basedon the proximity of borrowers and potential lenders; these proximity mea-sures are expected to significantly affect borrower–arranger matching, butnot borrowers’ future performance (we extend this discussion in section 3).

Another empirical challenge is to proxy for lead bank reputation. Wedefine a lead bank as reputable if its average market share of the syndi-cated loan market over our sample period (1998–2006) is above 2% (seeappendix A for details). We classify J.P. Morgan Chase, Bank of America,Citigroup, Wachovia, Credit Suisse First Boston, and Deutsche Bank as rep-utable arrangers. We also classify J.P. Morgan, Bank One, and Fleet Bostonas reputable arrangers over the period prior to their merger/acquisition.Together, these banks syndicated over 65% of the loan issuances (by vol-ume) over the sample period. In contrast, the remaining syndicated loanswere arranged by more than 1,000 banks, the vast majority of which had amarket share of less than 0.02%.

The banks classified as reputable are among the largest and most sophis-ticated banks in the world, and are therefore likely to have a better feelfor pricing conditions, better information on potential borrowers, and su-perior competence at screening and monitoring borrowers. This suggeststhat reputation is a mechanism by which market participants come to be-lieve that a lead bank does indeed possess superior screening and monitor-ing technologies and, more importantly, that the bank consistently deploysthese technologies on behalf of other loan investors.8

8 Given that Bank of America and Citigroup had to be bailed out in the recent financialcrisis, one may question our conjecture that these banks are reputable. However, Bank ofAmerica and Citigroup remained dominant arrangers over the 2007–2009 period (with an

ROLE OF BANK REPUTATION 9

Our measure of bank reputation follows prior research (e.g., Sufi [2007],Ross [2010]). However, it is possible that dominant market share could bea consequence of factors other than reputation. First, dominant banks mayhave achieved their market share by offering more attractive terms thanother lenders or from passing on an advantage of raising money at favor-able rates. However, as argued by Ross [2010], these explanations are notplausible, given that lead banks with high market share syndicate most ofthe loan principal to other syndicate participants. Another alternative isthat these banks have achieved oligopolistic market power through struc-tural barriers that suppress competition. If so, they should be able to extractrents from borrowers, such as higher interest rates. However, Ross [2010]finds that lead banks with high market share charge lower interest rates, andare more likely to lend without the protection of a borrowing base that lim-its outstanding principal to a fraction of readily saleable assets. These resultsare consistent with such banks having a strong reputation for evaluatingborrowers’ underlying business and true default risk, allowing them to of-fer borrowers more attractive terms while still inducing syndicate membersto participate. Fang [2005] finds similar evidence in the public bond mar-ket: reputable underwriters charge higher fees, but a lower interest rate,with an overall favorable effect on issuers’ net proceeds.

Third, reputable banks may achieve high market share because the largescale and scope of their operations allows them to offer borrowers lowerinterest rates based on expectations that the bank can later cross-sell sig-nificant services to the borrower (investment banking, derivatives, struc-tured finance, etc.). Yasuda [2005] shows that serving as the loan’s leadarranger helps banks to gain future underwriting of a borrower’s publicbonds. Drucker and Puri [2005] find that private lending increases theprobability of receiving the current and future underwriting of a borrower’sequity securities. In the context of syndicated loans supporting leveragedbuyouts, Ivashina and Kovner [2011] find evidence that lead banks priceloans to cross-sell future fee services. In our empirical tests, we explicitlycontrol for the cross-selling potential of banking services to the borrower.9

3. Empirical Design

Section 3.1 describes the econometric framework. In section 3.2, we dis-cuss our empirical strategy for isolating the implications of reputation cer-tification for borrowers’ future performance and accounting quality.

average market share of 18.3 and 14.4 percent, respectively), suggesting that their reputationcontinues to be strong in the syndicated loan market. J.P. Morgan Chase, Credit Suisse FirstBoston, Deutsche Bank, and Wachovia (until its merger with Wells Fargo) also continued tolead syndicated loan issuances over the crisis period (Bank One and Fleet Boston merged withJ.P. Morgan Chase and Bank of America, respectively, in 2004).

9 We thank an anonymous reviewer for suggesting that we address the cross-selling potentialin our analyses.

10 ROBERT M. BUSHMAN AND REGINA WITTENBERG-MOERMAN

3.1 ECONOMETRIC FRAMEWORK

Consistent with recent research on intermediary reputation (Fang,[2005], Ross [2010]), we employ an endogenous matching framework de-signed to explicitly control for observable and unobservable factors asso-ciated both with the choice of lead arranger and the borrower’s futureperformance (e.g., Heckman and Navarro-Lozano [2004]). The appropri-ateness of this framework rests on the presumption that private lendingarrangements involve access to confidential information and that such pri-vate information may underpin the observed matching between banks andborrowers and also be associated with future performance.

The basic framework consists of a binary outcome equation that modelsmatching between borrowers and lead banks, and two regression equations,one for each reputation partition (see Maddala [1983], chapters 8 and 9).Formally, we have:

Reputation∗i = Ziγ + εi , (1)

FuturePerformancehigh repi = xiβ

high rep + μhigh repi , and (2)

FuturePerformancelow repi = xiβ

low rep + μlow repi . (3)

Equation (1) is the borrower–lead arranger matching equation. We im-plement equation (1) as a probit model where the dependent variable is anindicator variable set equal to one if a loan is arranged by a high-reputationbank, and zero otherwise. Equation (2) is the performance equation forreputable banks, and equation (3) is that for less reputable banks, wherefuture performance is either profitability or credit quality. The vector xi in-cludes observable borrower and loan characteristics posited to directly in-fluence borrowers’ future performance. Equations (2) and (3) effectivelyallow interactions between arranger reputation and the explanatory vari-ables xi in the borrower performance models. To control for unobservablefactors affecting both bank-borrower matching and future performance,we allow the residuals in equations (2) and (3) to be correlated with theresidual in equation (1). The three error terms (εi , μ

high repi , μ

low repi ) are as-

sumed to have a trivariate normal distribution. We simultaneously estimateequations (1), (2), and (3) by maximum likelihood.10

The vector Zi in (1) represents observable variables important to de-termining matching between borrowers and lead banks. This vector iscomprised of two distinct subsets. The first subset contains factors thatdetermine borrower–lead arranger matching and at the same time may beassociated with borrowers’ future performance and accounting quality. The

10 All results are robust to using a two-step procedure which: 1) estimates equation (1) asa probit model and derives the inverse Mills ratio from the fitted values of Reputationi , andthen 2) includes the inverse Mills ratios in equations (2) and (3) to account for unobservablefactors.

ROLE OF BANK REPUTATION 11

second subset includes two variables based on the location of borrowers rel-ative to potential lenders that determine borrower–arranger matching, butthat are independent of borrowers’ future performance and are properlyexcluded from the future performance regressions.

With respect to the first subset, recall that one of our main research ob-jectives is to examine whether reputation certifies borrowers’ accountingquality. It is thus important to control for the possibility that borrowerswith higher earnings quality simply select higher reputation lead banks. Inaddition to a borrower’s prior earnings, we include a range of variablesthat capture observable earnings quality at a loan’s issuance. In particular,we include two measures of historical earnings persistence (see appendixA for a detailed description of all variables). We estimate our first persis-tence measure—Earnings-persistence-1—by the coefficient from a time se-ries regression of earnings on prior year earnings (e.g., Ali and Zarowin[1992], Francis et al. [2004], Frankel and Litov [2009], Dechow, Ge, andSchrand [2010]). Alternatively, we follow Skinner and Soltes [2011], whofind that reported earnings are significantly more persistent for dividend-paying firms and firms that make stock repurchases. We define Earnings-persistence-2 as an indicator variable taking the value of one if a bor-rower paid cash dividends and performed stock repurchases in the ma-jority of years over the five-year period preceding a loan’s issuance, zerootherwise.

To further control for historical earnings persistence, we include a mea-sure of extreme positive accruals (Accruals-pos-extreme), as such accruals tendto quickly reverse and decrease future profitability (Sloan [1996]). We alsocontrol for whether a borrower reported losses in the year prior to the yearof a loan’s issuance (Loss), as losses are typically transitory and less persis-tent (Hyan [1995], Basu [1997], Frankel and Litov [2009]). In addition,we address the possibility that firms with a more stable performance selectmore reputable arrangers and include a measure of earnings volatility. Wemeasure Earnings-volatility by the standard deviation of the ratio of EBITDAto total assets over the 10-year period prior to a loan’s issuance (Dichev andTang [2009]). In untabulated analysis, we substitute earnings volatility bycash flow volatility and find that the results are unchanged.

The first subset of variables in the borrower-lead arranger matching equa-tion also includes controls for a variety of firm- and loan-specific character-istics, such as credit risk; leverage; and a loan’s size, maturity and purpose.In addition, we incorporate a measure of cross selling potential to controlfor the possibility that high-reputation lead banks cherry pick borrowers towhom they can cross-sell significant services in the future. We adopt theapproach of Ivashina and Kovner [2011] and proxy for a lead bank’s ex-pectations of future fee business with a borrower’s past business. We mea-sure a borrower’s past business by the amount of total equity and bond is-suances in the five-year period preceding the year of the loan. We focus onequity and bond issuances as Drucker and Puri [2005] and Yasuda [2005]show that serving as the loan’s lead arranger helps banks to gain future

12 ROBERT M. BUSHMAN AND REGINA WITTENBERG-MOERMAN

underwriting of a borrower’s equity and public bonds, respectively.11 Thevalue of equity and bond transactions should represent a good proxy forbank fee amounts because, in these transactions, fees are typically stronglyrelated to the transaction value (Chen and Ritter [2000], Ivashina andKovner [2011]).12 We define Cross-selling-potential as an indicator variabletaking the value of one if a borrower’s cross-selling potential, estimated bythe value of past equity and bond transactions, is above the sample median,zero otherwise.13

For the second subset in the vector Zi , we follow Ross [2010] and includetwo variables based on the proximity of borrowers and potential lendersthat impact borrower–arranger matching but not borrowers’ future per-formance. The first variable derives from the idea that a borrower is morelikely to borrow from a high-reputation bank if it is in close proximity to thebank. The importance of proximity is supported by evidence that a shorterdistance between the borrower and the lender enhances lenders’ informa-tion gathering and monitoring abilities (Peterson and Rajan [2002], Bergeret al. [2005], Sufi [2007], Dass and Massa [2011]). In particular, proxim-ity to the borrower facilitates lenders’ collection of soft information (Pe-terson and Rajan [2002], Berger et al. [2005]) and access to private in-formation (Dass and Massa [2011]). Further, the home bias literature alsosuggests that investors have better access to information about local firms(e.g., Coval and Moskowitz [1999] and [2001]). We define the variable Near-reputable-arranger as equal to one if the borrower’s headquarters is within60 km of any high reputation banks’ headquarters, zero otherwise.14 Weexpect Near-reputable-arranger to be positively associated with the choice ofa high-reputation lead bank.

The second variable captures the idea that a borrower will be less likelyto borrow from a high-reputation bank if there are credible local alter-native lenders nearby. We consider a local bank to be a credible alterna-tive if it arranges, on average, at least 30 syndicated loan deals per yearover the sample period, suggesting that it has a considerable expertise in

11 The total amount of a borrower’s equity and bond issuance over the five-year period pre-ceding the loan issuance is 54%, correlated with the total amount of a borrower’s equity andbond issuances over the five-year period following loan issuance, supporting the appropriate-ness of the cross-selling measure based on borrower past business. In unreported analysis, webase the cross-selling variable on the amount of future transactions. The results continue tohold.

12 The Thompson One Banker database, from which we obtain transactions values, reportsfee amounts very sparsely; fees are not available for the vast majority of the sample borrowers’past and future transactions.

13 In untabulated analyses, we find that our inferences are similar if we employ the contin-uous measure of cross- selling potential (the total value of a borrower’s past equity and bondtransactions) instead of the indicator variable. The economic and statistical significance of thecross-selling potential variables are somewhat smaller in this case.

14 Following Ross [2010], we conjecture that, while reputable banks have satellite offices,these offices rarely engage in the syndicated loan activities of the large, public borrowers thatare the focus of this study.

ROLE OF BANK REPUTATION 13

syndicated lending.15 This variable, Near-local-arranger , is set equal to oneif a borrower’s headquarters is within 60 km of a credible regional lead ar-ranger’s headquarters and zero otherwise. We expect Near-local-arranger tobe negatively associated with the choice of a high reputation lead bank.16

While location likely plays a large role in determining the propensity oflenders and borrowers to do business together, it is not plausible that alender or borrower would change the location of its headquarters solelyfor the purpose of consummating a loan (Ross [2010]). Moreover, twootherwise observationally equivalent borrowers should not differ in theirsusceptibility to the loan certification effect and in post-loan performancemerely because the borrowers’ headquarters are located in different re-gions of the United States. Therefore, we treat the Near-reputable-arrangerand Near-local-arranger variables as valid instruments that are independentof borrowers’ future performance and are properly excluded from the fu-ture performance regressions.

3.2 ESTIMATING THE FUTURE PERFORMANCE IMPLICATIONS OF BANKREPUTATION

We first investigate the basic question of whether firms with high repu-tation banks exhibit a superior future performance (section 5.2). Here, weutilize a treatment effects model that includes a reputation dummy vari-able.17 The specification simplifies equations (1), (2), and (3) to a two-equation framework that retains equation (1), and replaces equations (2)and (3) with a single equation (4) that restricts βhigh rep = β low rep . The singleequation takes the form:

Reputationi is set equal to one if a loan is arranged by a reputable bank,zero otherwise. The error terms (εi , μi ) are assumed to be jointly normallydistributed. The coefficient βR represents an unbiased estimate of the im-pact of reputation certification on future performance. FuturePerformanceiis either a borrower’s profitability or credit rating in each of the three yearssubsequent to loan initiation. The set of control variables includes the samevariables as in the borrower-matching equation, including borrowers’ pastprofitability, historical earnings quality and volatility measures, cross-sellingpotential, and various firm and loan characteristics. In addition, we control

15 The results are not sensitive to the threshold number of syndicated loan deals. When wechange the threshold to 40 or 60 deals per year, this instrument performs similarly in both thearranger–borrower matching equation and the future performance equation.

16 Our results are robust when we define Near-reputable-arranger and Near-local-arranger basedon the distance between the borrower’s and the lender’s headquarters within 150 km.

17 We use the treatment effects model primarily to facilitate simple comparisons of theresults using the matching model to alternatives such as OLS, propensity matching, and firmfixed effects. We also compute treatment effects using counterfactuals constructed from theendogenous switching model estimated in section 5.3.

14 ROBERT M. BUSHMAN AND REGINA WITTENBERG-MOERMAN

for loan interest rate and whether institutional investors participate in aloan syndicate.18 When FuturePerformance is credit ratings, we augment thecontrols with measures of whether the borrower is on the S&P watch list orhas an S&P outlook at the time of a loan’s issuance.

To investigate whether reputation operates through the quality of bor-rowers’ accounting numbers, we estimate the full switching regressionframework represented by equations (1), (2), and (3) above (see section5.3). We estimate separate performance mappings for high and low rep-utation partitions. The implication of reputation for accounting quality iscaptured by significant differences in the mapping between borrowers’ pre-loan profitability and future performance across high and low reputationpartitions. With respect to future profitability, significant differences in themapping between borrowers’ pre-loan profitability and future profitabil-ity capture differences in earnings persistence across reputation partitions.When future performance is credit quality, significant differences capturedifferences in the strength of the connection between pre-loan profitabilityand future credit ratings.

4. Sample, Data, and Descriptive Statistics

4.1 DATA SOURCES AND SAMPLE SELECTION

We employ the DealScan database provided by the Thomson ReutersLoan Pricing Corporation (TRLPC). We obtain firm characteristics fromCompustat. Firms’ senior debt ratings, watch list additions, and outlookchanges (at the firm level) are retrieved from the S&P historical database. Ifthe S&P historical database does not cover a particular firm, we retrieve theMoody’s, Fitch, or DPR senior debt rating from the Mergent Fixed IncomeSecurities Database (FISD). For borrowers missing ratings on S&P andFISD, we hand-collect ratings from the Internet-based version of TRLPC.CDS data is obtained from Markit. We employ Thompson One Banker tocompile information on sample borrowers’ equity and bond transaction;this database covers all bond and equity issuances in the United States.

Table 1 summarizes the sample selection process. For the period 1998to 2006, DealScan reports 68,368 facilities outstanding to U.S. firms and is-sued in U.S. dollars. Merging this data with Compustat allows us to identify25,518 facilities issued to public firms. Next, we exclude facilities with insuf-ficient loan data, leaving 19,141 facilities. We also require sample borrowers

18 We require all the variables in the borrower–lead arranger matching model to be ob-servable prior to the matching process. We exclude the interest rate spread and institutionalinvestor indicator variables from the model because these variables become known later inthe loan syndication process, when the lead arranger assesses the market demand for the loanand recruits syndicate participants. At the same time, the matching model does comprise anumber of loan characteristics, including size, maturity, and purpose. While the first two char-acteristics may be subject to some negotiation between the borrower and the syndicate, theborrower typically requires a particular loan size and duration when approaching the leadarranger. Loan purpose is also known prior to loan initiation.

ROLE OF BANK REPUTATION 15

T A B L E 1Sample Selection

Filters Number of facilities

Syndicated loans to U.S. borrowers, in U.S. dollars, issued over theperiod from 1998 to 2006

68,368

Intersection with Compustat 25,518After elimination of facilities with missing loan data 19,141After elimination of facilities with insufficient firm data, including

past and future profitability9,857

After elimination of unrated facilities 6,675

This table presents the sample selection process.

to have sufficient Compustat data for estimating a borrower’s performanceprior to and following a loan’s issuance; this restricts our sample to 9,857 fa-cilities.19 Finally, we exclude loans of non rated borrowers. The remainingsample contains 6,675 facilities related to 1,272 firms.

4.2 DESCRIPTIVE STATISTICS

Panel A of table 2 reports that 70% of sample loans are issued by rep-utable arranger. Sample loans have, on average, a size of $546M, a matu-rity of 43 months, and an interest spread of 156 basis points. Institutionalloans represent 12% of the sample loans, 14% of the loans are issued forrestructuring purposes, and 49% are syndicated by a relationship arranger.In terms of credit quality characteristics at loan origination, sample firmshave a mean and median S&P senior debt rating of BBB. The mean CDSspread for the firms with traded CDS is 1.62%, and 8% (18%) of the loansrelate to firms on the S&P negative watch list (Outlook). Sample firms arerelatively large, with a mean and median value of total assets of 9,439M and2,776M, respectively, and they have average profitability, as measured by theratio of EBITDA to total assets, of 13%.

In panels B and C of table 2, we report summary statistics for the rep-utable and less reputable arranger samples, respectively. The two samplesdiffer along a number of dimensions. Loans syndicated by reputable ar-rangers are larger, have a shorter maturity, and are also more likely to beissued by arrangers that have a previous relationship with the borrower;loans with a prior lending relationship represent 52% of the reputable ar-ranger sample, relative to 43% of the less reputable arranger sample. Assuggested by the Interest-spread, Credit-rating , CDS-spread, and Leverage vari-ables, reputable arrangers’ loans are issued to less risky firms relative to thefirms of less reputable arrangers. Reputable arrangers’ borrowers are sig-nificantly larger but do not differ in terms of profitability at the time of theloan’s origination.

19 We require at least nine years of profitability-related data to estimate a borrower’s pastearnings persistence and volatility, and profitability following the loan issuance.

16 ROBERT M. BUSHMAN AND REGINA WITTENBERG-MOERMANT

AB

LE

2D

escr

iptiv

eSt

atis

tics

Pan

elA

:Tot

alsa

mpl

e

Num

ber

ofD

istr

ibut

ion

Loa

nan

dFi

rmC

har

acte

rist

ics

obse

rvat

ion

sM

ean

SD25

%50

%75

%

Loa

nch

arac

teri

stic

s:R

eput

atio

n6,

675

0.70

Loa

n-si

ze(i

nm

illio

ns)

6,67

554

6.4

985.

312

5.0

296.

060

0.0

Mat

urity

(in

mon

th)

6,67

542

.67

25.7

312

.00

48.0

060

.00

Inte

rest

-spre

ad(i

nbp

s)6,

675

156.

413

0.59

50.0

130.

0025

0.00

Inst

itutio

nal

6,67

50.

12R

estr

uctu

ring

-pur

pose

6,67

50.

14Pr

ior-r

elat

ions

hip

6,67

50.

49C

redi

tris

kch

arac

teri

stic

s:C

redi

t-rat

ing

6,67

510

.44

3.98

8.00

10.0

013

.00

CD

S-sp

read

(in

%)

2,35

21.

621.

910.

390.

772.

03W

atch

-neg

ativ

e(W

atch

-pos

itive

)6,

675

0.08

(0.0

2)O

utlo

ok-n

egat

ive

(Out

look

-pos

itive

)6,

675

0.18

(0.0

7)A

ddit

ion

alfi

rmch

arac

teri

stic

s:Fi

rm-si

ze(i

nm

illio

ns)

6,67

59,

439

25,5

731,

056

2,77

69,

533

Lev

erag

e6,

675

0.33

0.22

0.19

0.29

0.42

RO

A6,

675

0.13

0.08

0.09

0.12

0.17

Inte

rest

-cov

erag

e6,

675

10.8

434

.99

2.88

4.91

9.43

Earn

ings

-per

sist

ence

-16,

675

0.48

0.40

0.25

0.51

0.72

Earn

ings

-vol

atili

ty6,

675

0.04

0.04

0.02

0.03

0.05

Earn

ings

-per

sist

ence

-26,

675

0.33

Acc

rual

s-pos

-extr

eme

6,67

50.

10L

oss

6,67

50.

02N

ear-r

eput

able

-arr

ange

r6,

675

0.21

Nea

r-loc

al-a

rran

ger

6,67

50.

17C

ross

-selli

ng-p

oten

tial

6,67

50.

50

(Con

tinue

d)

ROLE OF BANK REPUTATION 17

TA

BL

E2

—C

ontin

ued

Pan

elB

:Rep

utab

lear

rang

ersa

mpl

e

Num

ber

ofD

istr

ibut

ion

Loa

nan

dFi

rmC

har

acte

rist

ics

obse

rvat

ion

sM

ean

SD25

%50

%75

%

Loa

nch

arac

teri

stic

s:L

oan-

size

(in

mill

ion

s)4,

690

639.

9∗∗∗

1060

.017

0.0

350.

075

0.0

Mat

urity

(in

mon

th)

4,69

041

.73∗∗

∗25

.79

12.0

048

.00

60.0

0In

tere

st-sp

read

(in

bps)

4,69

014

0.2∗∗

∗12

1.02

4010

0.00

230.

00In

stitu

tiona

l4,

690

0.11

∗∗∗

Res

truc

turi

ng-p

urpo

se4,

690

0.11

∗∗∗

Prio

r-rel

atio

nshi

p4,

690

0.52

∗∗∗

Cre

ditr

isk

char

acte

rist

ics:

Cre

dit-r

atin

g4,

690

9.87

∗∗∗

3.82

7.00

10.0

013

.00

CD

S-sp

read

(in

%)

1,97

01.

55∗∗

∗1.

850.

370.

731.

95W

atch

-neg

ativ

e(W

atch

-pos

itiv

e)4,

690

0.08

(0.0

2)O

utlo

ok-n

egat

ive

(Out

look

-pos

itiv

e)4,

690

0.18

(0.0

7)A

ddit

ion

alfi

rmch

arac

teri

stic

s:Fi

rm-si

ze(i

nm

illio

ns)

4,69

010

,907

∗∗∗

24,2

461,

511

3,67

511

,499

Lev

erag

e4,

690

0.32

∗∗∗

0.21

0.19

0.29

0.40

RO

A4,

690

0.14

0.07

0.09

0.13

0.17

Inte

rest

-cov

erag

e4,

690

11.0

334

.99

3.04

5.22

9.86

Earn

ings

-per

sist

ence

-14,

690

0.49

∗∗0.

390.

270.

520.

73Ea

rnin

gs-v

olat

ility

4,69

00.

04∗∗

∗0.

030.

020.

030.

05Ea

rnin

gs-p

ersi

sten

ce-2

4,69

00.

36∗∗

∗

Acc

rual

s-pos

-extr

eme

4,69

00.

09∗∗

∗

Los

s4,

690

0.01

∗∗∗

Nea

r-rep

utab

le-a

rran

ger

4,69

00.

24∗∗

∗

Nea

r-loc

al-a

rran

ger

4,69

00.

15∗∗

∗

Cro

ss-se

lling

-pot

entia

l4,

690

0.55

∗∗∗

(Con

tinue

d)

18 ROBERT M. BUSHMAN AND REGINA WITTENBERG-MOERMANT

AB

LE

2—

Con

tinue

d

Pan

elC

:Les

sre

puta

ble

arra

nger

sam

ple

Num

ber

ofD

istr

ibut

ion

Loa

nan

dFi

rmC

har

acte

rist

ics

obse

rvat

ion

sM

ean

SD25

%50

%75

%

Loa

nch

arac

teri

stic

s:L

oan-

size

(in

mill

ion

s)1,

985

325.

573

5.5

75.0

015

5.0

350.

0M

atur

ity(i

nm

onth

)1,

985

44.9

025

.44

18.0

048

.00

60.0

0In

tere

st-sp

read

(in

bps)

1,98

519

4.5

143.

7975

180.

0028

0.00

Inst

itutio

nal

1,98

50.

14R

estr

uctu

ring

-pur

pose

1,98

50.

20Pr

ior-r

elat

ions

hip

1,98

50.

43C

redi

tris

kch

arac

teri

stic

s:C

redi

t-rat

ing

1,98

511

.73

4.03

9.00

12.0

014

.00

CD

S-sp

read

(in

%)

382

1.96

2.14

0.50

0.96

2.58

Wat

ch-n

egat

ive

(Wat

ch-p

ositi

ve)

1,98

50.

07(0

.02)

Out

look

-neg

ativ

e(O

utlo

ok-p

ositi

ve)

1,98

50.

18(0

.08)

Add

itio

nal

firm

char

acte

rist

ics:

Firm

-size

(in

mill

ion

s)1,

985

5,97

528

,165

604.

21,

358

3,80

6L

ever

age

1,98

50.

360.

240.

200.

320.

47R

OA

1,98

50.

130.

080.

090.

120.

17In

tere

st-c

over

age

1,98

510

.41

35.0

22.

354.

187.

89Ea

rnin

gs-p

ersi

sten

ce-1

1,98

50.

460.

410.

220.

480.

70Ea

rnin

gs-v

olat

ility

1,98

50.

050.

060.

020.

030.

06Ea

rnin

gs-p

ersi

sten

ce-2

1,98

50.

24A

ccru

als-p

os-ex

trem

e1,

985

0.12

Los

s1,

985

0.03

Nea

r-rep

utab

le-a

rran

ger

1,98

50.

14N

ear-l

ocal

-arr

ange

r1,

985

0.21

Cro

ss-se

lling

-pot

entia

l1,

985

0.38

Th

ista

ble

prov

ides

desc

ript

ive

stat

isti

cs(s

eeta

ble

1fo

rth

esa

mpl

ese

lect

ion

proc

edur

e).P

anel

Apr

ovid

esde

scri

ptiv

est

atis

tics

for

allf

acili

ties

.Pan

els

Ban

dC

prov

ide

desc

ript

ive

stat

isti

csfo

rth

ere

puta

ble

arra

nge

ran

dle

ssre

puta

ble

arra

nge

rsa

mpl

es,r

espe

ctiv

ely.

∗∗∗

and

∗∗in

dica

tew

het

her

ava

riab

le’s

mea

nva

lue

issi

gnifi

can

tly

diff

eren

tfo

rth

ere

puta

ble

arra

nge

rsa

mpl

eth

anit

isfo

rth

en

onre

puta

ble

arra

nge

rsa

mpl

esat

the

1%an

d5%

leve

ls,r

espe

ctiv

ely.

Vari

able

sar

ede

fin

edin

appe

ndi

xA

.

ROLE OF BANK REPUTATION 19

Highlighting the importance of historical earnings quality, we find thatreputable arrangers’ borrowers have higher earnings persistence, estimatedby both the Earnings-persistence-1 and Earnings-persistence-2 measures; havelower earnings volatility; and are less likely to have extreme accruals andto experience a loss in the period prior to the loan origination. It is alsothe case that high cross-selling potential is more prevalent for reputablearrangers’ borrowers than for borrowers from less reputable banks. Finally,we find that the borrowers of reputable arrangers are significantly morelikely to be in close geographical proximity to a reputable lead bank andare significantly less likely to be located close to a credible local lead bank.

5. Empirical Results

5.1 THE BORROWER–LEAD ARRANGER MATCHING MODEL

Table 3 presents the estimation of the following Probit model ofborrower–arranger matching, which includes loan- and firm-specific char-acteristics and year and industry fixed effects:

(5)Table 3 shows that prior profitability does not affect bank-borrower

matching. We find modest evidence that historical earnings quality impactsthe matching, where only Earnings-persisternce-2 is significant at the 10%level. Reputable arrangers syndicate the loans of larger firms and largerloans; larger loans generally require larger syndicates, which are likely moredifficult to arrange. Interestingly, borrowers with high cross-selling poten-tial are more likely to end up with high-reputation lead banks. Reputablearrangers are less likely to issue restructuring purpose loans. This may occurbecause restructuring purpose loans are often accompanied by significantchanges in a firm’s capital structure and thus are associated with high un-certainty, deterring reputable arrangers from syndicating such loans. Butthis relation could also be driven by the fact that smaller, less reputablebanks have superior local market knowledge, which may be especially im-portant for arranging restructuring purpose loans. Firms are more likelyto hire the same lead arranger used for previous loan transactions if thelead arranger is reputable. This evidence is consistent with Fang [2005],who finds that reputable underwriters in the public bond market are morelikely to have a prior relationship with the issuers, compared to less rep-utable underwriters.

Lastly, both of our geography variables are significant with the predictedsigns. First, Near-reputable-arranger is significantly positively associated with

20 ROBERT M. BUSHMAN AND REGINA WITTENBERG-MOERMAN

(0.12) (0.12)Pseudo R -Square 17.43% 18.02%AUC (area under ROC curve) 0.782 0.787# of loans 6,675 6,675

This table presents the borrower–lead arranger matching model. We regress an indicator variable thatreflects whether a loan is issued by a reputable arranger on a set of loan- and firm-specific characteristics.We estimate the model with year and one-digit industry fixed effects and cluster the standard errors at thefirm level. Standard errors are in parentheses. ∗∗∗, ∗∗, and ∗ denote significance at the 1%, 5%, and 10%levels, respectively. Variables are defined in appendix A.

the choice of a high reputation lead. Economically, being in proximity to areputable lead arranger increases the probability of a borrower–reputablearranger match by 7.8% (7.9%) in the first (second) model. The secondvariable, Near-local-arranger , has a significantly negative coefficient, consis-tent with borrowers being less likely to borrow from a high-reputation bankif there are credible local alternatives. Close proximity to a local credi-ble lead arranger decreases the probability that a loan is syndicated by a

ROLE OF BANK REPUTATION 21

reputable arranger by 6.1% (6.3%) in the first (second) model. A partial-F statistic of 13.84 and 13.96 (p-values of 0.00) in the first and secondmodels, respectively, indicates that the Near-reputable-arranger and Near-local-arranger variables are collectively strong instruments for the choice of bankreputation. Also, the partial R -square of 3.0% (3.1%) in the first (second)model reveals that these variables have significant explanatory power. TheAUC (area under ROC curve) of 0.782 and 0.787 for the first and sec-ond models, respectively, suggests that our model successfully explains theborrower–arranger matching.

5.2 BANK REPUTATION AND BORROWERS’ FUTURE PROFITABILITY ANDCREDIT RATINGS

Our first series of future performance analyses employs a treatment ef-fects model, which includes loan- and firm-specific characteristics and yearand industry fixed effects. For this analysis, we use our second earningspersistence measure, as there is a significant relation between Earnings-persistence-2 and Reputation in the borrower–arranger matching model,while Earnings-persistence-1 does not explain Reputation:20

Panel A of table 4 provides a univariate comparison of the future prof-itability and credit ratings of borrowers of reputable and less reputable ar-rangers. There is no significant difference in the mean profitability of theborrowers of reputable and less reputable arrangers prior to a loan’s is-suance, but borrowers with reputable arrangers exhibit a higher mean prof-itability over the three-year period following a loan’s issuance. This result isdriven by the drop in the mean profitability of borrowers of less reputablearrangers, from 0.13 prior to a loan issuance to 0.12 in the following years.Borrowers of reputable arrangers have a lower (i.e., better) credit rating,by approximately 2 notches, than borrowers of less reputable arrangers.

Table 4, panel B, reports the results of estimating equation (6) withFuturePerformance measured as profitability. The coefficient of 0.012 on Rep-utation in column (1) indicates that, in the year following a loan issuance,borrowers with reputable arrangers report an ROA that is 1.2 percentagepoints higher than it is for borrowers with less reputable arrangers. Thisdifference is economically significant, representing 9.6% of the mean prof-itability of borrowers of nonreputable arrangers in that year. The differencein profitability across borrowers of reputable and non-reputable arrangersincreases over time. In the second (third) year following the year of a loanissuance, borrowers with reputable arrangers report an ROA that is 1.8(2.0) percentage points higher than that of borrowers with nonreputable

20 For robustness, we replicated all our future performance analyses with Earnings-persistence-1 and find that our inferences are unchanged.

22 ROBERT M. BUSHMAN AND REGINA WITTENBERG-MOERMAN

TA

BL

E4

Bor

row

erPr

ofita

bilit

yan

dC

redi

tRat

ing

Follo

win

ga

Loa

nIs

suan

ce

Pan

elA

:Des

crip

tive

stat

isti

cs

Rep

utab

lear

ran

ger

Les

sre

puta

ble

arra

nge

rD

iffe

ren

ce

Mea

nR

OA

RO

A0.

135

0.13

20.

003

RO

At+

10.

130

0.12

40.

006∗∗

RO

At+

20.

131

0.12

30.

008∗∗

∗

RO

At+

30.

132

0.12

30.

009∗∗

∗

Mea

nC

redi

t-rat

ing

Cre

dit-r

atin

g9.

8711

.73

−1.8

5∗∗∗

Cre

dit-r

atin

g t+1

10.0

911

.83

−1.7

5∗∗∗

Cre

dit-r

atin

g t+2

10.2

911

.94

−1.6

6∗∗∗

Cre

dit-r

atin

g t+3

10.5

012

.32

−1.8

2∗∗∗

Pan

elB

:Atr

eatm

ente

ffec

tsm

odel

offu

ture

profi

tabi

lity

Trea

tmen

teff

ects

mod

elO

LS

Dep

ende

ntv

aria

ble

RO

At+

1R

OA

t+2

RO

At+

3R

OA

t+1

RO

At+

2R

OA

t+3

(1)

(2)

(3)

(4)

(5)

(6)

Rep

utat

ion

0.01

2∗∗0.

018∗∗

∗0.

020∗∗

∗0.

004∗

0.00

6∗∗0.

007∗∗

(0.0

0)(0

.00)

(0.0

0)(0

.00)

(0.0

0)(0

.00)

RO

A0.

604∗∗

∗0.

516∗∗

∗0.

475∗∗

∗0.

606∗∗

∗0.

506∗∗

∗0.

457∗∗

∗

(0.0

3)(0

.03)

(0.0

4)(0

.03)

(0.0

3)(0

.03)

Earn

ings

-per

sist

ence

-20.

003

0.00

30.

002

0.00

30.

003

0.00

2(0

.00)

(0.0

0)(0

.00)

(0.0

0)(0

.00)

(0.0

0)A

ccru

als-p

os-ex

trem

e−0

.013

∗∗∗

−0.0

21∗∗

∗−0

.021

∗∗∗

−0.0

14∗∗

∗−0

.018

∗∗∗

−0.0

22∗∗

∗

(0.0

0)(0

.01)

(0.0

1)(0

.00)

(0.0

1)(0

.01)

Los

s0.

019

0.02

00.

012

0.01

80.

019

0.00

9

(Con

tinue

d)

ROLE OF BANK REPUTATION 23

TA

BL

E4

—C

ontin

ued

Pan

elB

:Atr

eatm

ente

ffec

tsm

odel

offu

ture

profi

tabi

lity

Trea

tmen

teff

ects

mod

elO

LS

Dep

ende

ntv

aria

ble

RO

At+

1R

OA

t+2

RO

At+

3R

OA

t+1

RO

At+

2R

OA

t+3

(1)

(2)

(3)

(4)

(5)

(6)

(0.0

1)(0

.02)

(0.0

2)(0

.01)

(0.0

2)(0

.02)

Earn

ings

-vol

atili

ty0.

025

0.07

40.

077

0.01

80.

048

0.05

9(0

.05)

(0.0

5)(0

.07)

(0.0

5)(0

.04)

(0.0

6)C

redi

t-rat

ing

0.00

00.

000

−0.0

030.

000

0.00

0−0

.001

(0.0

0)(0

.00)

(0.0

0)(0

.00)

(0.0

0)(0

.00)

Lev

erag

e0.

035∗∗

∗0.

040∗∗

∗0.

049∗∗

∗0.

033∗∗

∗0.

037∗∗

∗0.

047∗∗

∗

(0.0

1)(0

.01)

(0.0

1)(0

.01)

(0.0

1)(0

.01)

Inte

rest

-cov

erag

e0.

000

0.00

00.

000

0.00

00.

000

0.00

0(0

.00)

(0.0

0)(0

.00)

(0.0

0)(0

.00)

(0.0

0)Fi

rm-si

ze−0

.004

∗∗∗

−0.0

04∗∗

∗−0

.005

∗−0

.004

∗∗∗

−0.0

04∗∗

∗−0

.004

∗∗∗

(0.0

0)(0

.00)

(0.0

0)(0

.00)

(0.0

0)(0

.00)

Cro

ss-se

lling

-pot

entia

l−0

.001

−0.0

02−0

.005

0.00

0−0

.001

0.00

0(0

.00)

(0.0

0)(0

.01)

(0.0

0)(0

.00)

(0.0

0)L

oan-

size

−0.0

01−0

.002

−0.0

060.

000

−0.0

01−0

.002

(0.0

0)(0

.00)

(0.0

0)(0

.00)

(0.0

0)(0

.00)

Mat

urity

0.00

3∗∗0.

002∗

0.00

2∗0.

003∗∗

0.00

3∗∗0.

003∗∗

(0.0

0)(0

.00)

(0.0

0)(0

.00)

(0.0

0)(0

.00)

Inte

rest

-spre

ad−0

.008

∗∗∗

−0.0

10∗∗

∗−0

.007

∗∗−0

.008

∗∗∗

−0.0

09∗∗

∗−0

.006

∗∗∗

(0.0

0)(0

.00)

(0.0

0)(0

.00)

(0.0

0)(0

.00)

Res

truc

turi

ng-p

urpo

se−0

.012

∗∗∗

−0.0

08∗

−0.0

02−0

.011

∗∗∗

−0.0

09∗∗

−0.0

08∗

(0.0

0)(0

.00)

(0.0

0)(0

.00)

(0.0

0)(0

.00)

Inst

itutio

nal

0.00

30.

009

0.00

40.

003

0.00

10.

005

(0.0

0)(0

.00)

(0.0

0)(0

.00)

(0.0

0)(0

.00)

Prio

r-rel

atio

nshi

p0.

000

0.00

0−0

.002

0.00

00.

000

−0.0

01(0

.02)

(0.0

0)(0

.00)

(0.0

2)(0

.00)

(0.0

0)

ρ−0

.08∗

−0.1

1∗∗−0

.13∗∗

––

–Pr

(F-s

tati

stic

/Wal

dX

2)

0.00

0.00

0.00

0.00

0.00

0.00

#of

loan

s6,

675

6,67

56,

675

6,67

56,

675

6,67

5

(Con

tinue

d)

24 ROBERT M. BUSHMAN AND REGINA WITTENBERG-MOERMAN

TA

BL

E4

—C

ontin

ued

Pan

elC

:Atr

eatm

ente

ffec

tsm

odel

offu

ture

cred

itra

ting

Trea

tmen

teff

ects

mod

elO

LS

Dep

ende

ntv

aria

ble

Cre

dit-r

atin

g t+1

Cre

dit-r

atin

g t+2

Cre

dit-r

atin

g t+3

Cre

dit-r

atin

g t+1

Cre

dit-r

atin

g t+2

Cre

dit-r

atin

g t+3

(1)

(2)

(3)

(4)

(5)

(6)

Rep

utat

ion

−1.3

44∗∗

∗−2

.059

∗∗∗

−2.4

65∗∗

∗−0

.472

∗∗−0

.643

∗∗∗

−0.8

29∗∗

∗

(0.2

7)(0

.28)

(0.6

6)(0

.20)

(0.2

2)(0

.26)

RO

A−1

.351

∗∗∗

−2.1

23∗∗

∗−2

.569

∗∗−1

.577

∗∗∗

−2.2

38∗∗

∗−2

.432

∗∗

(0.4

2)(0

.72)

(0.9

6)(0

.36)

(0.6

3)(0

.89)

Earn

ings

-per

sist

ence

-2−0

.096

∗−0

.138

−0.1

58−0

.097

∗−0

.141

∗−0

.160

(0.0

6)(0

.09)

(0.1

3)(0

.05)

(0.0

8)(0

.12)

Acc

rual

s-pos

-extr

eme

−0.0

68−0

.103

−0.0

95−0

.042

−0.0

65−0

.054

(0.0

9)(0

.11)

(0.1

4)(0

.08)

(0.1

0)(0

.13)

Los

s0.

062

−0.2

99−0

.538

0.13

6−0

.183

−0.4

18(0

.29)

(0.5

3)(0

.64)

(0.2

7)(0

.52)

(0.6

3)Ea

rnin

gs-v

olat

ility

1.48

3∗∗0.

782

0.83

01.

765∗∗

∗1.

534

1.58

6(0

.68)

(1.2

2)(1

.49)

(0.6

1)(0

.97)

(1.2

5)C

redi

t-rat

ing

0.77

8∗∗∗

0.69

4∗∗∗

0.64

9∗∗∗

0.79

4∗∗∗

0.70

4∗∗∗

0.65

9∗∗∗

(0.0

3)(0

.03)

(0.0

4)(0

.03)

(0.0

3)(0

.03)

Wat

ch-n

egat

ive

0.74

6∗∗∗

0.78

3∗∗∗

0.73

0∗∗∗

0.76

4∗∗∗

0.77

7∗∗∗

0.71

4∗∗∗

(0.1

0)(0

.11)

(0.1

5)(0

.10)

(0.1

2)(0

.15)

Wat

ch-p

ositi

ve−0

.736

∗∗∗

−0.8

67∗∗

∗−0

.712

∗−0

.749

∗∗∗

−0.8

57∗∗

∗−0

.707

∗

(0.1

3)(0

.22)

(0.4

0)(0

.13)

(0.2

2)(0

.40)

Out

look

-neg

ativ

e0.

329∗∗

∗0.

644∗∗

∗0.

767∗∗

∗0.

324∗∗

∗0.

640∗∗

∗0.

766∗∗

∗

(0.0

6)(0

.09)

(0.1

3)(0

.06)

(0.0

9)(0

.13)

Out

look

-pos

itive

−0.2

47∗∗

∗−0

.325

∗∗∗

−0.5

33∗∗

∗−0

.267

∗∗∗

−0.3

58∗∗

∗−0

.554

∗∗∗

(0.0

6)(0

.12)

(0.1

5)(0

.06)

(0.1

2)(0

.15)

Lev

erag

e0.

359∗∗

0.30

40.

522

0.39

3∗∗∗

0.35

10.

583∗

(0.1

7)(0

.26)

(0.3

4)(0

.16)

(0.2

4)(0

.30)

(Con

tinue

d)

ROLE OF BANK REPUTATION 25

TA

BL

E4

—C

ontin

ued

Pan

elC

:Atr

eatm

ente

ffec

tsm

odel

offu

ture

cred

itra

ting

Trea

tmen

teff

ects

mod

elO

LS

Dep

ende

ntv

aria

ble

Cre

dit-r

atin

g t+1

Cre

dit-r

atin

g t+2

Cre

dit-r

atin

g t+3

Cre

dit-r

atin

g t+1

Cre

dit-r

atin

g t+2

Cre

dit-r

atin

g t+3

(1)

(2)

(3)

(4)

(5)

(6)

Inte

rest

-cov

erag

e0.

001

0.00

10.

000

0.00

10.

000

0.00

0(0

.00)

(0.0

0)(0

.00)

(0.0

0)(0

.00)

(0.0

0)Fi

rm-si

ze0.

011

−0.0

14−0

.037

−0.0

47−0

.104

∗∗−0

.129

∗

(0.0

4)(0

.05)

(0.0

7)(0

.03)

(0.0

5)(0

.06)

Cro

ss-se

lling

-pot

entia

l−0

.013