Northwest Power and Conservation Council The Role of Energy Efficiency The Role of Energy Efficiency in Could (and Should) Play in Montana’s in Could (and Should) Play in Montana’s Future Future Insights from the 5 Insights from the 5 th th Northwest Northwest Power Power and Conservation Plan and Conservation Plan Tom Eckman Tom Eckman Manager, Conservation Resources Manager, Conservation Resources Northwest Power and Conservation Council Northwest Power and Conservation Council Presented October 18, 2005 Presented October 18, 2005 Montana Energy Futures Conference Montana Energy Futures Conference

Transcript

NorthwestPower andConservation

Council

The Role of Energy Efficiency The Role of Energy Efficiency in Could (and Should) Play in Montana’s in Could (and Should) Play in Montana’s FutureFuture

Insights from the 5Insights from the 5thth NorthwestNorthwest Power Power and Conservation Planand Conservation Plan

Tom EckmanTom EckmanManager, Conservation ResourcesManager, Conservation Resources

Northwest Power and Conservation CouncilNorthwest Power and Conservation CouncilPresented October 18, 2005Presented October 18, 2005

Montana Energy Futures ConferenceMontana Energy Futures Conference

slide 2Northwest

Power andConservation

Council

What You’re About To HearWhat You’re About To Hear

nn Energy Efficiency in the Region’s Current Energy Efficiency in the Region’s Current

Resource MixResource Mix

nn Regional Efficiency GoalsRegional Efficiency Goals

–– What These Might Mean for MontanaWhat These Might Mean for Montana

nn What’s Behind the GoalsWhat’s Behind the Goals

nn The Challenges AheadThe Challenges Ahead

slide 3Northwest

Power andConservation

Council

PNW Energy Efficiency AchievementsPNW Energy Efficiency Achievements1978 1978 -- 20042004

0

500

1,000

1,500

2,000

2,500

3,000

Ave

rage

Meg

awat

ts

1978 1982 1986 1990 1994 1998 2002

BPA and Utility Programs Alliance ProgramsState Codes Federal Standards

Since 1978 Utility & BPA Since 1978 Utility & BPA Programs, Energy Codes & Programs, Energy Codes & Federal Efficiency Standards Have Federal Efficiency Standards Have Produced Nearly 3000 aMW of Produced Nearly 3000 aMW of Savings.Savings.

slide 4Northwest

Power andConservation

Council

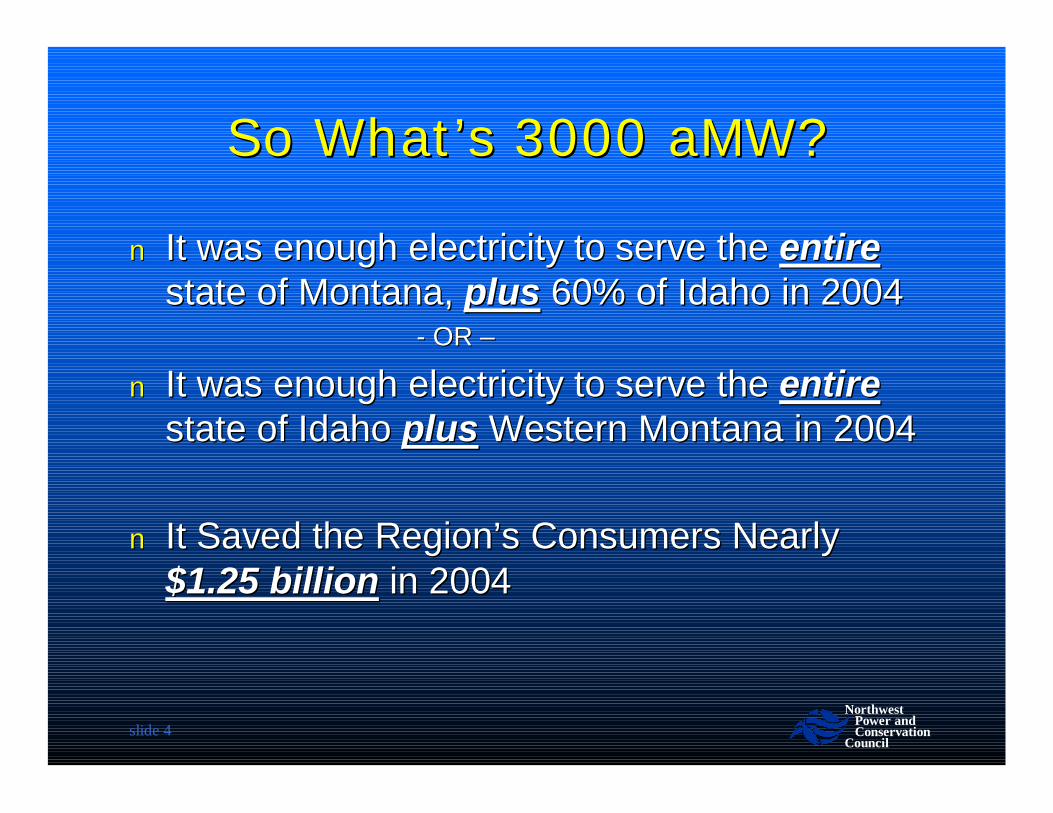

So What’s 3000 aMW?So What’s 3000 aMW?

nn It was enough electricity to serve the It was enough electricity to serve the entireentirestate of Montana, state of Montana, plusplus 60% of Idaho in 200460% of Idaho in 2004

-- OR OR ––

nn It was enough electricity to serve the It was enough electricity to serve the entireentirestate of Idaho state of Idaho plusplus Western Montana in 2004Western Montana in 2004

nn It Saved the Region’s Consumers Nearly It Saved the Region’s Consumers Nearly $1.25 billion$1.25 billion in 2004in 2004

slide 5Northwest

Power andConservation

Council

Energy Efficiency Resources Energy Efficiency Resources Significantly Reduced Projected PNW Significantly Reduced Projected PNW

Electricity SalesElectricity Sales

14,000

16,000

18,000

20,000

22,000

24,000

1980 1985 1990 1995 2000

Ave

rage

Meg

awat

ts

Medium High ForecastMedium LowMedium High Minus ConservationActual

slide 6Northwest

Power andConservation

Council

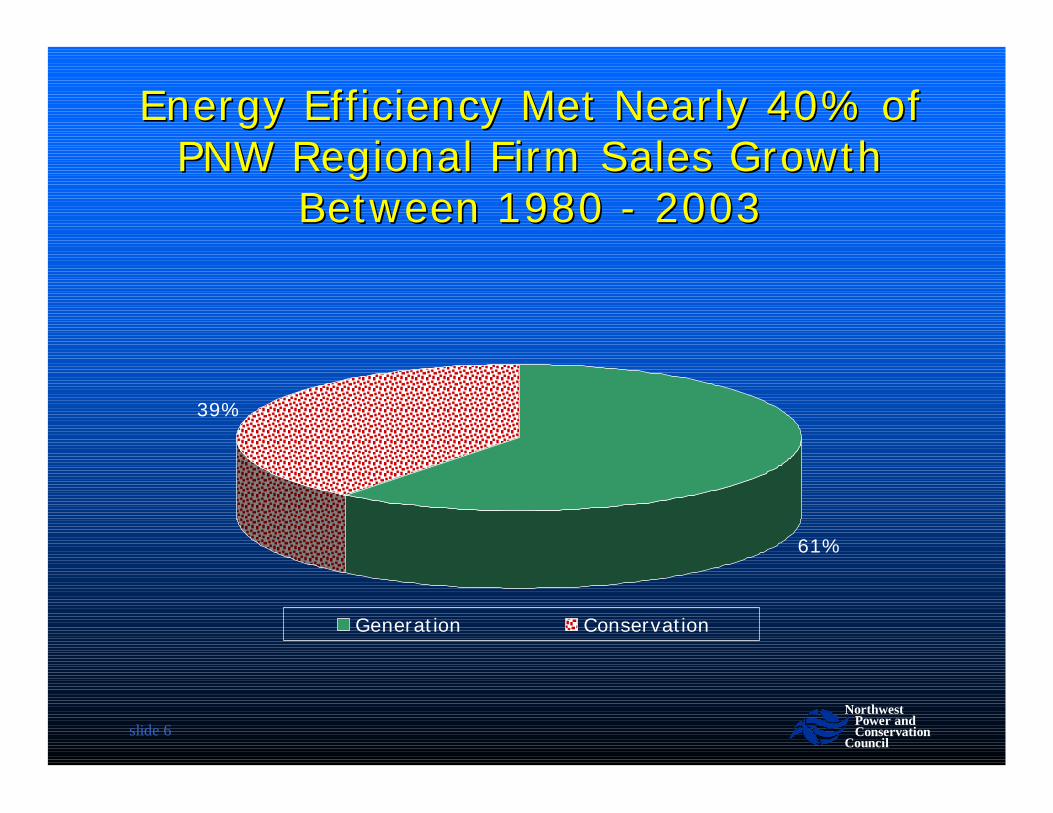

Energy Efficiency Met Nearly 40% of Energy Efficiency Met Nearly 40% of PNW Regional Firm Sales Growth PNW Regional Firm Sales Growth

Between 1980 Between 1980 -- 20032003

61%

39%

Generation Conservation

slide 7Northwest

Power andConservation

Council

Regional Utility Conservation Acquisitions Have Regional Utility Conservation Acquisitions Have Helped Balance Loads & ResourcesHelped Balance Loads & Resources

0

20

40

60

80

100

120

140

160

1978 1982 1986 1990 1994 1998 2002

Con

serv

atio

n A

cquis

itio

ns

(aM

W)

Response to West Coast

Energy CrisisResponse to NW

Recession

Response to “Restructuring

Discussions”

Creating Mr. Toad’s Wild Ride for the PNW’s Energy Efficiency InCreating Mr. Toad’s Wild Ride for the PNW’s Energy Efficiency Industrydustry

slide 8Northwest

Power andConservation

Council

Utility Acquired Energy Efficiency Has Been Utility Acquired Energy Efficiency Has Been A BARGAIN!A BARGAIN!

$0

$10

$20

$30

$40

$50

$60

$70

$80

$90

$100

May-9

6

Nov-

96

May-9

7

Nov-

97

May-9

8

Nov-

98

May-9

9

Nov-

99

May-0

0

Nov-

00

May-0

1

Nov-

01

May-0

2

Nov-

02

May-0

3

Nov-

03

May-0

4

Nov-

04

May-0

5

Whol

esa

le E

lect

rici

ty P

rice

(2000$/M

WH

)

Levelized Cost of EfficiencyAcquisitionsWholesale Market Price

slide 9Northwest

Power andConservation

Council

So Much for the Past, So Much for the Past, What’s AheadWhat’s Ahead

55thth Plan Relies on Conservation and Renewable Plan Relies on Conservation and Renewable

Resources to of Meet Load GrowthResources to of Meet Load Growth**

**Actual future conditions (gas prices, CO2 control, conservation Actual future conditions (gas prices, CO2 control, conservation accomplishments) accomplishments) will change resource development schedulewill change resource development schedule

slide 11Northwest

Power andConservation

Council

CostCost--Effective and Achievable Effective and Achievable Conservation Should Meet Over 45% of Conservation Should Meet Over 45% of

PNW Load Growth from 2005PNW Load Growth from 2005--2025*2025*

Plans Along the Efficient Frontier Permit Plans Along the Efficient Frontier Permit TradeTrade--Offs of Costs Against RiskOffs of Costs Against Risk

$35,500

$36,000

$36,500

$37,000

$37,500

$23,600 $23,800 $24,000 $24,200 $24,400 $24,600

NPV System Cost (Millions)

NPV

Sys

tem

Ris

k (M

illio

ns)

Least Risk

Least Cost

slide 17Northwest

Power andConservation

Council

Three Conservation Options TestedThree Conservation Options Tested

nn Option 1Option 1: : AcceleratedAccelerated –– Similar to the “best Similar to the “best performance” over the last 20 yearsperformance” over the last 20 years–– NonNon--lost opportunity limited to 120 aMW/yearlost opportunity limited to 120 aMW/year–– RampRamp--up lostup lost--opportunity to 85% by 2017opportunity to 85% by 2017

nn Option 2Option 2: : SustainedSustained -- Similar to typical rates over Similar to typical rates over last 20 yearslast 20 years–– NonNon--lost opportunity limited to 80 aMW/yearlost opportunity limited to 80 aMW/year–– RampRamp--up lostup lost--opportunity to 85% by 2017opportunity to 85% by 2017

nn Option 3Option 3: : Status QuoStatus Quo -- Similar to lowest rates over Similar to lowest rates over last 20 yearslast 20 years–– NonNon--lost opportunity limited to 40 aMW/yearlost opportunity limited to 40 aMW/year–– RampRamp--up lostup lost--opportunity to 85% penetration by 2025opportunity to 85% penetration by 2025

slide 18Northwest

Power andConservation

Council

Average Annual Conservation Average Annual Conservation Development for Alternative Levels of Development for Alternative Levels of

Option 1 - Accelerated Option 2 - Sustained Option 3 - Status Quo

NPV (

bill

ion 2

004$)

NPV System Cost NPV System Risk

slide 20Northwest

Power andConservation

Council

WECC Carbon Dioxide Emissions WECC Carbon Dioxide Emissions Reductions for Alternative Reductions for Alternative

Conservation TargetsConservation Targets

0

10

20

30

40

50

60

70

80

Mill

ion T

ons

over

20 y

ears

Option 1 - Accelerated Option 2 - Sustained Option 3 - Status Quo

slide 21Northwest

Power andConservation

Council

Why Energy Efficiency Reduces NPV Why Energy Efficiency Reduces NPV System Cost and RiskSystem Cost and Risk

nn It’s A Cheap (avg. 2.4 cents/kWh TOTAL It’s A Cheap (avg. 2.4 cents/kWh TOTAL RESOURCE COST) Hedge Against Market RESOURCE COST) Hedge Against Market Price SpikesPrice Spikes

nn It has value even when market prices are It has value even when market prices are low low

nn It’s Not Subject to Fuel Price RiskIt’s Not Subject to Fuel Price Risknn It’s Not Subject to Carbon Control RiskIt’s Not Subject to Carbon Control Risknn It’s Significant Enough In Size to Delay It’s Significant Enough In Size to Delay

“build decisions” on generation“build decisions” on generation

slide 22Northwest

Power andConservation

Council

The Plan’s Targets Are A The Plan’s Targets Are A Floor, Not a CeilingFloor, Not a Ceiling

When we took the “ramp rate” constraints offthe portfolio model it developed

1500 aMW1500 aMWof Conservation in 2005

slide 23Northwest

Power andConservation

Council

Where Are The Savings?Where Are The Savings?

slide 24Northwest

Power andConservation

Council

Sources of Savings by SectorSources of Savings by Sector

nn Estimate of 5% of 2025 forecast loadsEstimate of 5% of 2025 forecast loadsnn 350 aMW at 1.7 cents per kWh350 aMW at 1.7 cents per kWhnn Process controls, drive systems, lighting, Process controls, drive systems, lighting,

refrigeration, compressed air, etcrefrigeration, compressed air, etcnn Potential is a function of the ongoing Potential is a function of the ongoing

changes in region’s industrial mixchanges in region’s industrial mix

Plan Plan Conservation Action ItemsConservation Action Items

nn Ramp up “Lost Opportunity” conservationRamp up “Lost Opportunity” conservation»» Goal => 85% penetration in 12 years Goal => 85% penetration in 12 years »» 10 to 30 MWa/year 2005 through 200910 to 30 MWa/year 2005 through 2009

nn Accelerate the acquisition of “NonAccelerate the acquisition of “Non--Lost Lost Opportunity” resourcesOpportunity” resources

»» Return to acquisition levels of early 1990’sReturn to acquisition levels of early 1990’s»» Target 120 MWa/year next five yearsTarget 120 MWa/year next five years

nn Employ a mix of mechanismsEmploy a mix of mechanisms»» Local acquisition programs (utility, SBC Administrator & BPA Local acquisition programs (utility, SBC Administrator & BPA

programs)programs)»» Regional acquisition programs and coordinationRegional acquisition programs and coordination»» Market transformation venturesMarket transformation ventures

slide 31Northwest

Power andConservation

Council

The Total Resource Acquisition Cost* of The Total Resource Acquisition Cost* of 55thth Plan’s Conservation TargetsPlan’s Conservation Targets

*Incremental capital costs to install measure plus program administration costs estimated at 20% of capital.

slide 32Northwest

Power andConservation

Council

Meeting the Plan’s Efficiency Targets Will Meeting the Plan’s Efficiency Targets Will Likely Require Increased Regional InvestmentsLikely Require Increased Regional Investments

$0

$50

$100

$150

$200

$250

$300

$350

$400

$450

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

Aver

age 19

91-0

4

Aver

age 20

01-2

00420

0520

09Utilit

y I

nvest

ments

(m

illio

n 2

000$)

slide 33Northwest

Power andConservation

Council

Although, The Share of Utility Although, The Share of Utility Revenues Required is ModestRevenues Required is Modest

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

1991

199219

9319

9419

9519

9619

9719

9819

9920

0020

0120

0220

0320

04

Aver

age 19

91-0

4

Aver

age 20

01-2

00420

0520

09Shar

e of

Ret

ail Rev

enues

(%

)

Regional Average Revenues/kWh will need to increase by $0.000006/kWh

slide 34Northwest

Power andConservation

Council

Utility* Efficiency Acquisition Plans for 2005 Are Utility* Efficiency Acquisition Plans for 2005 Are Close to 5Close to 5thth Plan TargetsPlan Targets

0

20

40

60

80

100

120

2005 5th Plan Target 2005 Utility Acquistion Plan

Co

nserv

ati

on

Levels

(M

Wa)

*Targets for 15 Largest PNW Utilities. These utilities represent approximately 80% of regional load.

slide 35Northwest

Power andConservation

Council

Most IOU Efficiency Plans are Close Most IOU Efficiency Plans are Close to 5to 5thth Plan’s TargetsPlan’s Targets

0

5

10

15

20

25

Pacif

iCor

p (O

R,WA,

ID)

Puge

t Sou

nd Ene

rgy

Portl

and

Gener

al

Idah

o Po

wer

Avist

a Ut

ilities

North

weste

rn E

nerg

y

Conse

rvation L

evels

(M

Wa)

Plan Targets

Utility Plans

slide 36Northwest

Power andConservation

Council

However, Several Large Public Utility Efficiency However, Several Large Public Utility Efficiency

Plans Are Well Below 5Plans Are Well Below 5thth Plan TargetsPlan Targets

0

1

2

3

4

5

6

7

8

9

10

Seat

tle C

ity Light

Snoh

omish

PUD

Taco

ma Po

wer

Cowlit

z PU

D

Clar

k PU

D

EWEB

Grant

PUD

Bent

on PUD

Flathe

ad R

EA

Con

serv

ation L

evels

(M

Wa)

Plan Targets

Utility Plans

slide 37Northwest

Power andConservation

Council

SummarySummary

nn The 5th Plan’s Goal IsThe 5th Plan’s Goal Is To Make The To Make The InefficientInefficient Use of Electricity . . .Use of Electricity . . .–– ImmoralImmoral–– IllegalIllegal–– UnprofitableUnprofitable

If We Fail Both If We Fail Both CostsCosts and and Risk Risk Will Be HigherWill Be Higher

slide 38Northwest

Power andConservation

Council

Backup SlidesBackup Slides

slide 39Northwest

Power andConservation

Council

Montana Electric Sales Montana Electric Sales 1,490 aMW in 2004 1,490 aMW in 2004

Industrial625 aMW

42%

Commercial440 aMW

30%

Residential425 aMW

28%

Source: US DOE/EIA

slide 40Northwest

Power andConservation

Council

Montana Electricity Sales Represent Montana Electricity Sales Represent 8% of Regional Sales Across All 8% of Regional Sales Across All

What’s Left To Do At What’s Left To Do At Home?Home?

65 Average MW

slide 42Northwest

Power andConservation

Council

Montana Has The Region’s Lowest Montana Has The Region’s Lowest Market Shares of Electric Water and Market Shares of Electric Water and

Space HeatingSpace Heating

0%

10%

20%

30%

40%

50%

60%

70%

80%

Mar

ket

Sat

ura

tion

ID MT OR WA Region

Electric Water Heater Electric Heating Central Air Conditioning

slide 43Northwest

Power andConservation

Council

Montana’s Average Electricity Montana’s Average Electricity Use/Residential Customer Is The Use/Residential Customer Is The

Lowest in the RegionLowest in the Region

0

2000

4000

6000

8000

10000

12000

14000

Ave

rage

Annual

Use

/Cust

omer

(k

Wh)

WA OR ID MT Region

slide 44Northwest

Power andConservation

Council

But Residential Customer Use Has Not But Residential Customer Use Has Not Declined Since 1990, While Use in Other Declined Since 1990, While Use in Other

PNW States HasPNW States Has

0

2000

4000

6000

8000

10000

12000

14000

16000

1990 1992 1994 1996 1998 2000 2002 2004

Ave

rage

Annual

Use

/Cust

om

er (

kWh)

ID MT OR WA

slide 45Northwest

Power andConservation

Council

Montana’s Housing Stock is Montana’s Housing Stock is Predominantly Single Family and Predominantly Single Family and

Regional Residential Sector Realistically Regional Residential Sector Realistically Achievable Potential for AppliancesAchievable Potential for Appliances

Clothes Washers - 135

aMW75%

Dishwashers - 10 aMW

6%

Refrigerators - 35 aMW

19%

slide 49Northwest

Power andConservation

Council

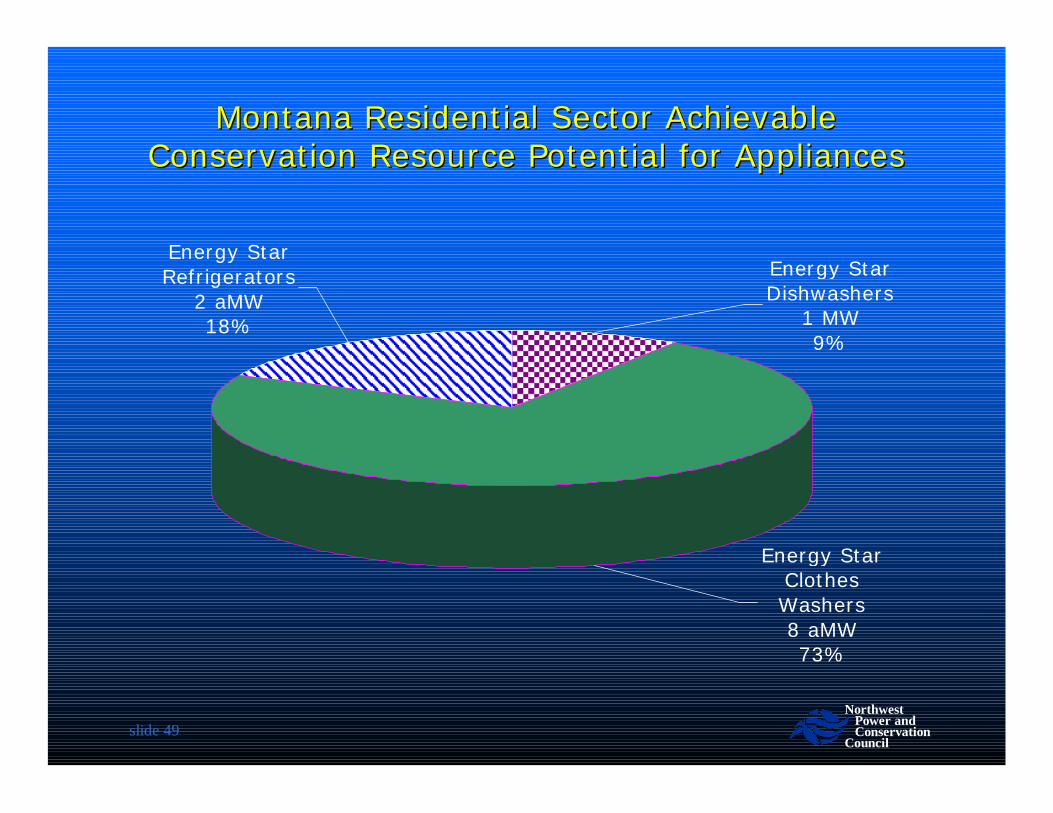

Montana Residential Sector Achievable Montana Residential Sector Achievable Conservation Resource Potential for AppliancesConservation Resource Potential for Appliances

Energy Star Dishwashers

1 MW9%

Energy Star Refrigerators

2 aMW18%

Energy Star Clothes Washers8 aMW73%

slide 50Northwest

Power andConservation

Council

Regional Residential Sector Realistically Regional Residential Sector Realistically Achievable Potential for Water HeatingAchievable Potential for Water Heating

Efficient Tanks29%

95 aMWWaste Water

Heat Recovery4%

15 aMW

Heat Pump Water Heaters

67%225 aMW

slide 51Northwest

Power andConservation

Council

Montana Residential Sector Conservation Montana Residential Sector Conservation Resource Potential for Water HeatingResource Potential for Water Heating

High Efficiency Water Heaters

3 aMW27%

Waste Water Heat Recovery

1 aMW9%

Heat Pump Water Heaters

7 aMW64%

slide 52Northwest

Power andConservation

Council

Regional Residential Sector Realistically Regional Residential Sector Realistically Achievable Potential for Space Achievable Potential for Space

ConditioningConditioningNew Construction -

Shell Measures 40 aMW

16%

Duct Sealing & System

Commissioning & Controls 15 aMW

6%

Weatherization60 aMW

24%

Heat Pump Upgrades 55 aMW

22%

Heat Pump Conversions

75 aMW32%

slide 53Northwest

Power andConservation

Council

Montana Residential Sector Conservation Montana Residential Sector Conservation Resource Potential for Space ConditioningResource Potential for Space Conditioning

CostCost--Effective Commercial Conservation Potential Effective Commercial Conservation Potential in 2025 For Building Lighting, HVAC & Equipmentin 2025 For Building Lighting, HVAC & Equipment--

nn Fifth Plan is lower due to changing (less Fifth Plan is lower due to changing (less electrically intensive) industrial mix ) = 5% electrically intensive) industrial mix ) = 5% of 2025 sector loadsof 2025 sector loads

nn Montana potential @ 5% of 2004 salesMontana potential @ 5% of 2004 sales= 30 aMW= 30 aMW

slide 60Northwest

Power andConservation

Council

While PNW Annual Utility System While PNW Annual Utility System Investments in Energy Efficiency Have Declined Since Investments in Energy Efficiency Have Declined Since

Total PNW Annual Energy Efficiency Total PNW Annual Energy Efficiency Achievements Have Been Growing, Largely Due Achievements Have Been Growing, Largely Due To The Impact of Energy Codes and StandardsTo The Impact of Energy Codes and Standards

0

50

100

150

200

250

300

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

Con

serv

atio

n A

cquis

itio

ns

(aM

W) Federal Standards

State Codes

Alliance Programs

slide 62Northwest

Power andConservation

Council

PNW Utilities Now Invests Less Than 2% of PNW Utilities Now Invests Less Than 2% of Their Retail Sales Revenues in Energy Their Retail Sales Revenues in Energy

Fortunately . . . The “First Year” Cost ($/aMW) of Fortunately . . . The “First Year” Cost ($/aMW) of Utility Acquired Energy Efficiency Has DeclinedUtility Acquired Energy Efficiency Has Declined

PNW Utilities Have Gotten More Efficient at Acquiring PNW Utilities Have Gotten More Efficient at Acquiring Energy Efficiency Energy Efficiency -- Cost Are Now Below $15 MWHCost Are Now Below $15 MWH

Cumulative 1978 Cumulative 1978 -- 2004 Efficiency 2004 Efficiency Achievements by SourceAchievements by Source

Alliance Programs185 aMW

6%

State Codes560 aMW

19%

Federal Standards545 aMW

19%

BPA and Utility Programs1635 aMW

56%

slide 66Northwest

Power andConservation

Council

The Share of PNW Retail Electricity Sales The Share of PNW Retail Electricity Sales Revenues Invested In Energy Efficiency Has Revenues Invested In Energy Efficiency Has

Declined Since The Early 1990’sDeclined Since The Early 1990’s

$0.0$1.0$2.0$3.0$4.0$5.0$6.0$7.0$8.0$9.0

$10.0

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

Tot

al R

etail

Ele

ctrici

ty S

ales

Rev

enue

(bill

ion 2

000$)

Revenues Invested In EfficiencyRevenues Dedicated to Other Costs

slide 67Northwest

Power andConservation

Council

Utility Acquired Energy Efficiency Has Been CostUtility Acquired Energy Efficiency Has Been Cost--Competitive with Market PurchasesCompetitive with Market Purchases