33

Dr. Ing. Mar*n Tauber Metal Bulle*n’s 24th Interna*onal Al Recycled Alumnium Conference, Slovakia 2123.11.2016

| Date post: | 15-Apr-2017 |

| Category: |

Business |

| Upload: | martin-tauber |

| View: | 51 times |

| Download: | 0 times |

Dr. Ing. Mar*n Tauber

Metal Bulle*n’s 24th Interna*onal Al Recycled Alumnium Conference, Slovakia 21-‐23.11.2016

Content ü Which series of alloys contain magnesium and what are the main

applica*ons? è Almost all Al alloys contain Mg and demand growing

ü Examining the supply-‐demand fundamentals of magnesium – what implica*ons for procurement by aluminium companies? è Sustainable sourcing as chance for Mg

ü What other raw materials flagged as “cri*cal” are key to alloy performance and quality? è Strategic & cri*cal raw materials; conflict minerals

ü What issues do these pose for aluminium recycling loops and what are the main environmental considera*ons? è High recycling rates thanks to efficient Al set-‐up

ü How does recycling of these alloying elements contribute to resource conserva*on and efficiency? è Legal frame works and process innova*on

What are strategic or cri*cal materials? EU cri*cal raw materials are those raw materials, which are

economically and strategically important for the European economy but have a higher risk of supply interrup*on.

Candidate (inves*gated) materials

These materials represent a diverse group, including materials that are mined or cul*vated as well as some refined materials that are

considered highly important to downstream sectors.

Conflict Minerals EU poli*cal aims for EU companies to source *n, tantalum, tungsten and gold responsibly. These minerals are typically used in everyday

products such as mobile phones, cars and jewellery.

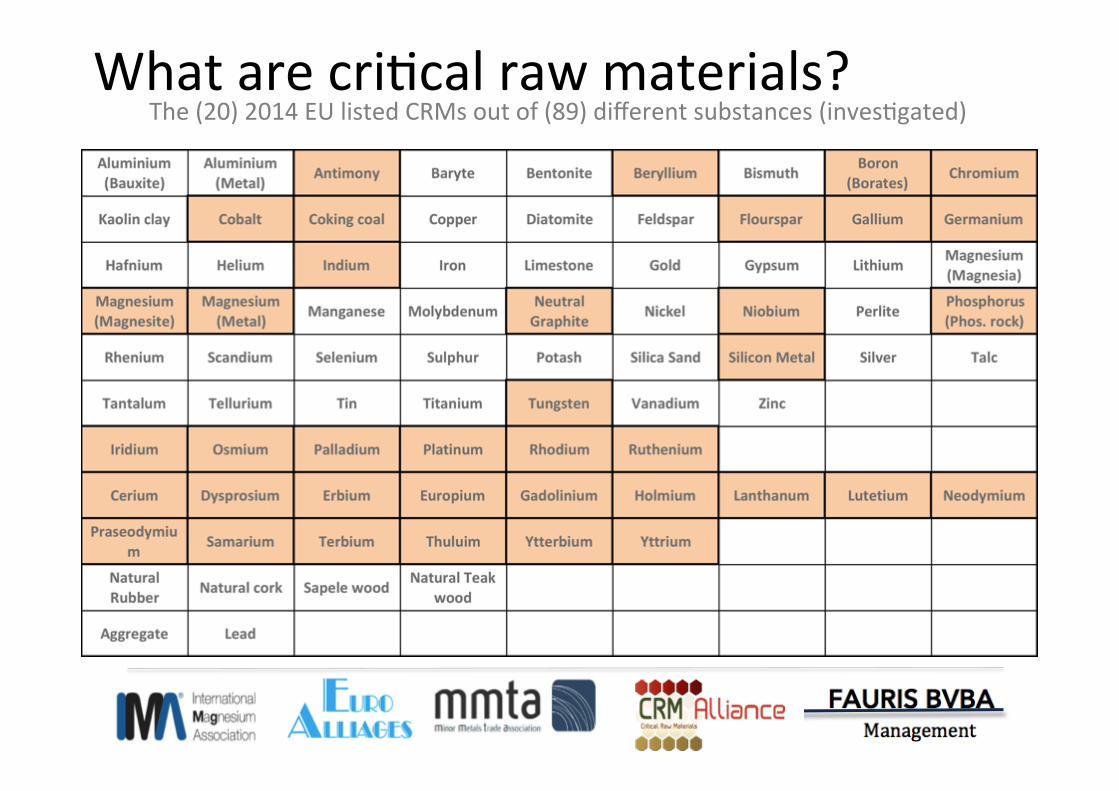

What are cri*cal raw materials? The (20) 2014 EU listed CRMs out of (89) different substances (inves*gated)

What are conflict minerals? The (4) conflict minerals; Tungsten also being a CRM

What are main alloying elements to Al? Currently, over 400 wrought and over 200 cas*ng alloys are registered

Registered alloying elements for Al Alloying (Mg content)

1xxx Aluminium 99.00% or greater 2xxx Copper 2–6% (0.3-‐1.6%) 3xxx Manganese 0.6-‐1.5% (0-‐1%) 4xxx Silicon 7-‐13% (0.3-‐1.6%) 5xxx Magnesium 1-‐6% (1-‐6%) 6xxx Magnesium & Silicon 1 & 0.6% (0.6-‐1%) 7xxx Zinc 4-‐8% (1.2-‐2.5%) 8xxx Other elements

Mg alloying use in different Al sectors?

ü Primary aluminium smelters: è Cas*ng billets, rolling slab, foundry alloys

ü Rolling mills: è Mg as alloying agent

ü Remelt billet makers and extruders: è Secondary Mg mainly from scrap

ü Secondary aluminium smelters: è Die-‐cast/foundry alloys mainly from scrap (Al & Mg)

5 principles

Main Mg alloying use per Al alloy

PRC dominant in primary Mg produc*on

Source: China Nonferrous Metals Industry Associa*on -‐ The Nonferrous Metals Society of China 2016/Kyoto

PRC dominant in primary Al produc*on

China has always pay alen*on to the magnesium alloys applica*on in the automobile industry. the instrument panel, front and rear subframe, wheels, steering bracket and other parts have been developed in the plamorm of a independent research and developed hydrogen fuel car. The total amount of

Source: China Nonferrous Metals Industry Associa*on -‐ The Nonferrous Metals Society of China 2016/Kyoto

Mg supply/demand fundamentals ü Significant long-‐term over-‐capacity in China:

è Global market of 850 kto vs. installed over-‐capacity of 1,8 mio mt

ü Regional market protec*on: è An*-‐dumping rules installed in US and Brazil

ü Environmental concerns: è Higher CO2 emipng produc*on process in China; enforcement lately

ü Main price fundamentals in China not within the Mg industry: è High dependent on FeSi (grade 75%), steel and coal industry

ü No trading regula*on: è Market volume too small for e.g. LME lis*ng

ü Small markets & non-‐favourite history: è Lightweight mix component; market development and high CAPEX caused many primary projects to fail

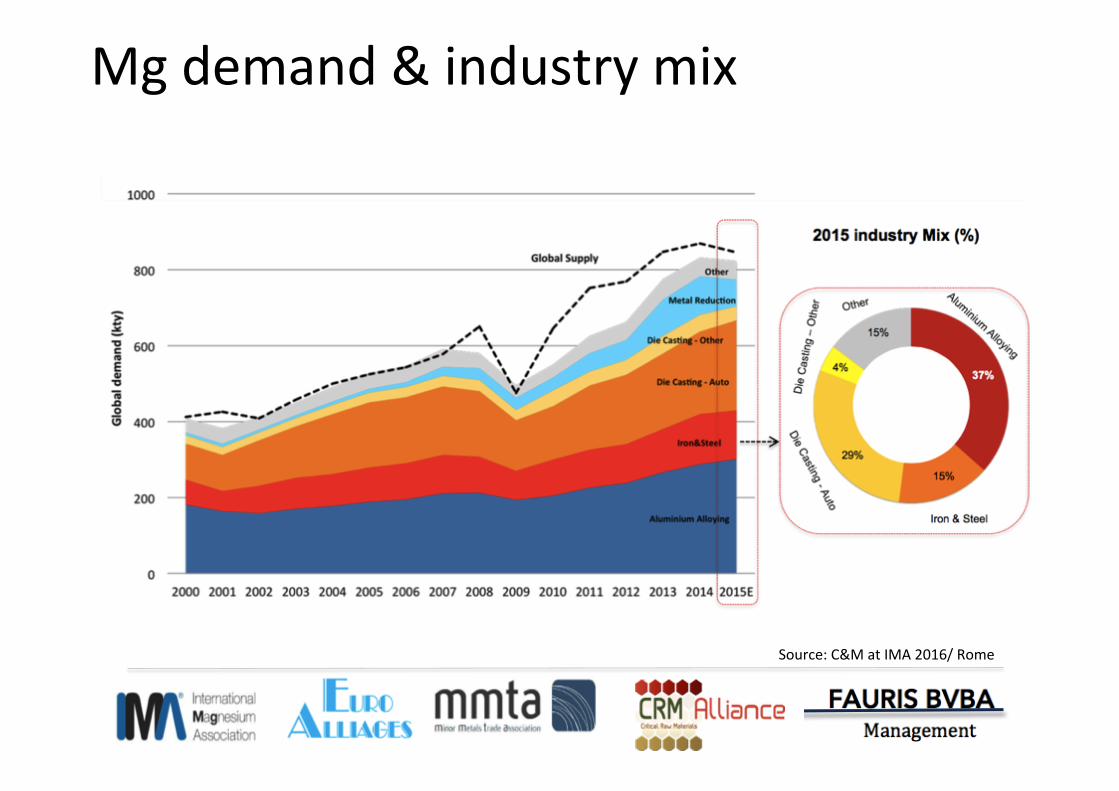

Mg demand & industry mix

Source: C&M at IMA 2016/ Rome

Main message for the Aluminium industry

• Alloying elements are essen*al for reaching compe**ve proper*es, such as strength, corrosion resistance and processing parameters

• However, CRM policy is supposed to secure supply, subs*tu*on efforts can significantly weaken the Al industry

• Primary alloying elements such as Mg and Si will most probably remain on the EU CRM list, and most of the common alloying elements are listed

• Alloying elements require equal considera*on when it comes to sustainable sourcing and resource efficiency

• Dependency on pre & post consumer recycling processes

Global & Corporate repor*ng interface

Mandatory repor*ng instrument

“Repor*ng sustainability makes it more valuable. One of the main corporate benefits is reputa*onal, another is the requirements of the supply chain. Repor*ng is an integral part of sustainability. Repor*ng mechanisms such as the GRI reinforce this.” “Global investors will only invest in companies in this part of the world if they see that companies are repor*ng honestly.”

Shis from shareholders to stakeholders

ü In 2014, the European Parliament passed a new law will require its biggest companies to include sustainability factors as part of their annual financial reports

ü Today, 2.500 companies voluntarily produce sustainability reports; that will rise to nearly 7.000 by 2017, when the law goes into effect

ü Addressing their supply chains is the next big task

From voluntarily to mandatory – a chance for profiling of alloying elements?

ü OEMs and Tiers need to talk more about their raw material procurement strategies

ü Sustainability is already used on a large scale for all stakeholder communica*on

ü Excellent examples from Aluminium and Automo*ve companies

ü Major alloying elements must claim its value for sustainable content, in all major applica*ons and markets

The Magnesium Metal value chain

Source: VW at IMA 2013/Xian

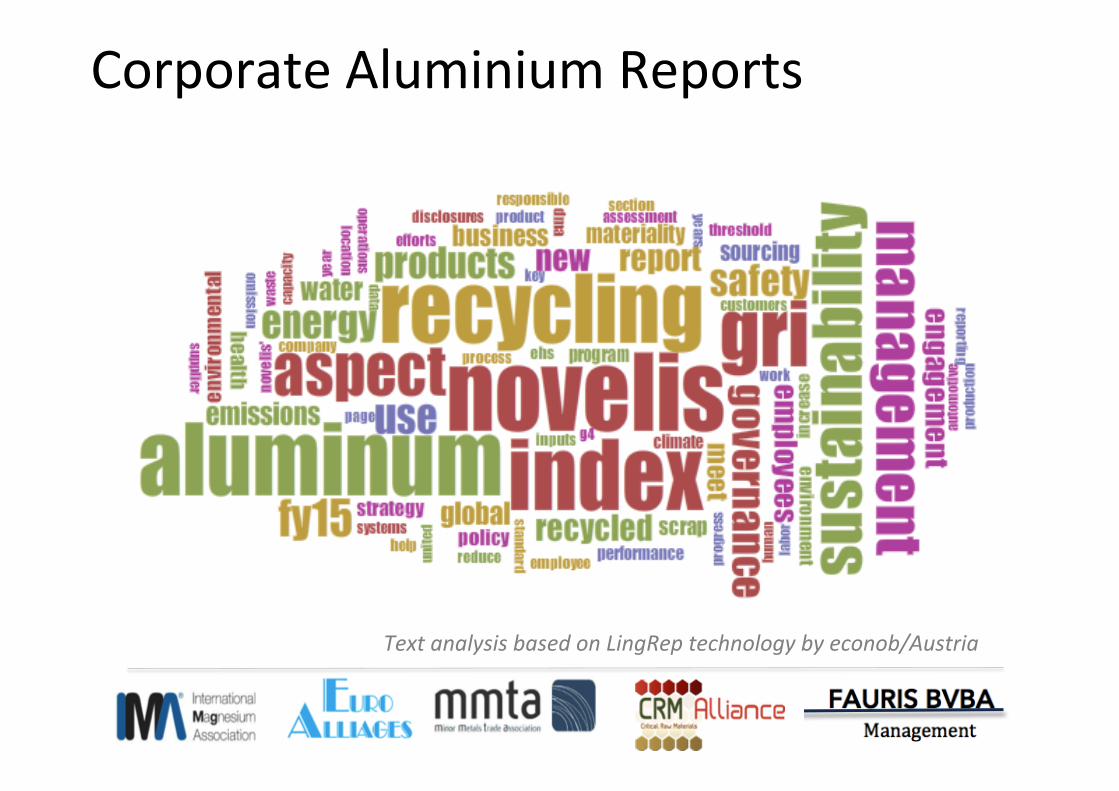

Corporate Aluminium Reports

Text analysis based on LingRep technology by econob/Austria

Corporate Aluminium Reports

Text analysis based on LingRep technology by econob/Austria

Corporate Automo*ve Reports

Text analysis based on LingRep technology by econob/Austria

Corporate Automo*ve Reports

Text analysis based on LingRep technology by econob/Austria

Concepts & Tools: Carbon Impact Factor

ü CIF enables OEMs to demonstrate and communicate their efforts to reduce carbon intensity (risk) within their supply chain

ü Osen no traceability of raw material inputs beyond the primary processing point

ü As a result, different raw material data are aggregated or compounded

Source: Introducing the The Carbon Impact Factor/2015

Sustainability – enable high volume growth? ü Magnesium industry need to invest into global spread raw material/semi-‐fabricated material supply base

ü Magnesium stakeholders need to engage into global policy process and inform & promote Magnesium

ü Magnesium needs to par*cipate in “own” Circular Economy best prac*ces projects, and close informa*on gaps on e.g. process recycling & ELV

ü Informa*on of Magnesium LCA must be up-‐dated and easy accessible for different value-‐chains and stakeholders to enable green procurement strategies

ü Magnesium must show its “sustainable value” in the Aluminium industry

ü Aluminium needs to name Magnesium in their overall/sustainable communica*on

EU policy and (cri*cal) raw materials

Circular Economy needs (also) raw materials

LCA example – Magnesium sourcing

Source: LCA study DLR 2015 for ESAN Magnesium/Turkey

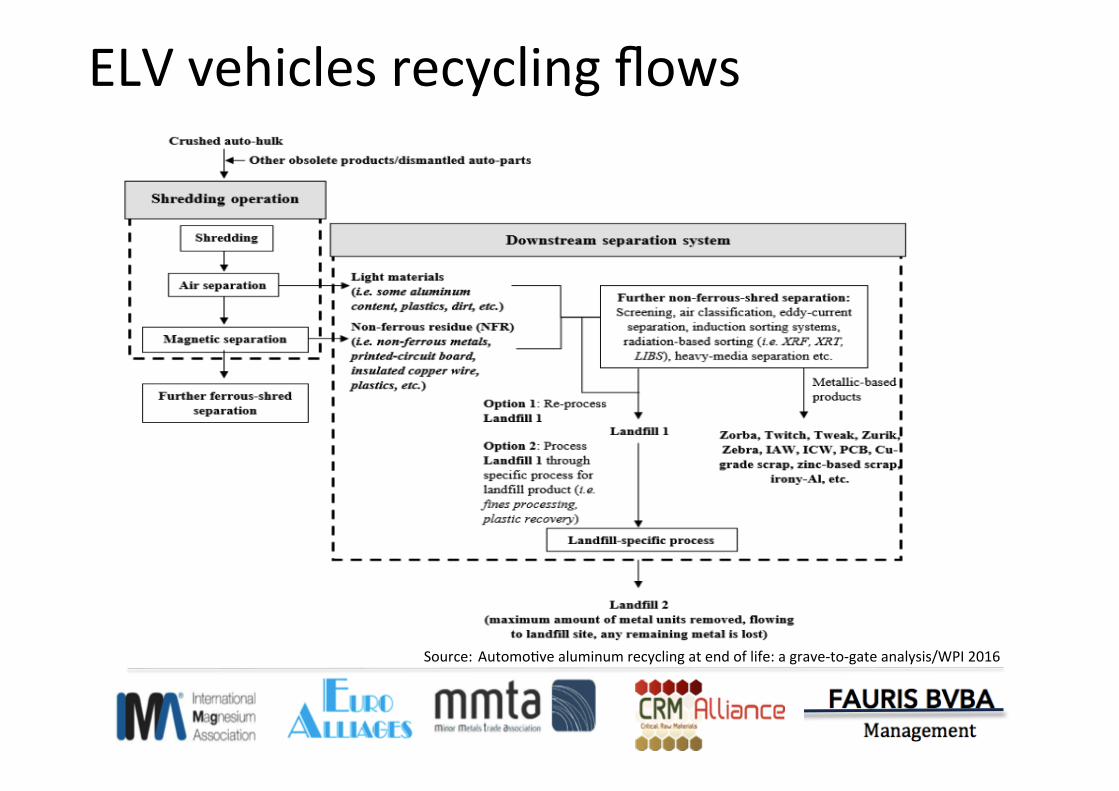

ELV vehicles recycling flows

Source: Automo*ve aluminum recycling at end of life: a grave-‐to-‐gate analysis/WPI 2016

ELV vehicles recycling flows

Source: Automo*ve aluminum recycling at end of life: a grave-‐to-‐gate analysis/WPI 2016

Example embedded recycling flows – Light gauge frac*on

ü Fragmented non-‐ferrous metal mixture “ZORBA” typically 65% Al è contains copper, lead, magnesium, stainless steel, nickel, *n and zinc

ü Floated, fragmented scrap stream “TWITCH” typically 90-‐98% Al è contains no more than 1% free zinc, 1% free magnesium, 1% of free iron, less than 2% non-‐metallic and 1% free rubber or plas*c

ü Fragmented auto scrap “TWEAK” è contains max. 4% free zinc, 1% free magnesium, 1,5% of analy*cal iron and no more than a total 5% non-‐metallic.

Source: Automo*ve aluminum recycling at end of life: a grave-‐to-‐gate analysis/WPI 2016

ü Growing markets -‐ Alloying elements, such as magnesium, manganese, silicon, zinc and copper play a vital role in proper*es of Al alloys. Growing applica*ons for Mg, like automo*ve sheet and can stock contain significant quan**es for their own markets and are high important for its supply/demand development.

ü Overall LCA -‐ Alloying elements should be part of individual sustainable procurement strategies, and also CO2 saving on alloy element sourcing should be featured.

ü Cri*cal materials – Alloying elements must play an integrated role in mandatory and green procurement.

ü End of life scrap – Alloying elements material flow (Material Flow Analysis, Circular Economy) are an integrated part of the e.g. Aluminium recycling loops.

Conclusions

Links & info • EU CRM list 2014: hlps://ec.europa.eu/growth/sectors/raw-‐materials/specific-‐interest/cri*cal_en • Interna*onal Magnesium Associa*on (IMA): hlp://www.intlmag.org/default.asp? • Minor Metal Trade Associa*on (MMTA): hlp://www.mmta.co.uk • Associa*on of Euro Ferro-‐Alloys producers (Euro Alliages): hlp://www.euroalliages.com

• Cri*cal Raw Material (CRM) Alliance • Rue de l’Industrie 4 • B-‐1000 Brussels • Tel: +32 (0)2 213 74 20 • Email: [email protected] • hlp://cri*calrawmaterials.org

![Li Alloying Nanomaterials - greenlionproject.eu · where M represents a group IV alloying element.[5] This equation implies a 3.75:1 lithium to alloying element atomic ratio at full](https://static.documents.pub/doc/80x56/5f7894293cf36b12a9415e0d/li-alloying-nanomaterials-where-m-represents-a-group-iv-alloying-element5-this.jpg)

![Final Draft - HZG · 2019. 2. 1. · 44 magnesium above 200°C only by alloying remains a challenge [2]. A complementary route 45 consists in strengthening Mg -baseand Mgd alloys](https://static.documents.pub/doc/80x56/6121affd5cc5695c72224786/final-draft-2019-2-1-44-magnesium-above-200c-only-by-alloying-remains-a.jpg)