126

THE SOCIO-ECONOMIC IMPACT OF LEGALIZED GAMBLING IN THE EASTERN CAPE PROVINCE ISBN: 978-0-621-39980-6

THE SOCIO-ECONOMIC IMPACT OF LEGALIZED GAMBLING IN THE EASTERN CAPE

PROVINCE

ISBN: 978-0-621-39980-6

2

2009

Acknowledgements

The Board of Directors of the Eastern Cape, led by former Chairperson Mr Sipho Luyolo Mtika Majombozi, has always wanted to gain an understanding of the industry. This, they believed, would assist in gambling policy formulation, overall regulation of the industry as well as assist in planning and formulating interventions, such as responsible gambling programmes, avail empirical data about the industry in the province.

After successfully establishing a research unit the Board managed to commission a study which was undertaken by TNS Research Survey, one of South Africa‟s leading market research companies. They were assisted by a well known gaming industry experts, Economic Information Services based in Cape Town.

The Board would like to extend a special gratitude to the gambling industry in the province for willingly participating and contributing valuable data as required by the project.

This report was compiled by TNS Research Surveys (Political and Social Unit) and Economics Information Services.

Contact Person: Kim Larsen (Business Head, TNS Research Surveys), Tel: 011 778 7500

Authors: Megan van Vuuren, Barry Standish, Antony Boting, Brian Swing, Lesley Powell and Kim Larsen

The project was managed by Monde Duma, Manager: Research and Communication (ECGBB), Tel: 043 7028300

EXCLUSION OF CLAIMS

Despite all efforts to ensure accuracy in the assembly of information and data or the compilation thereof, ECGBB is unable to warrant the accuracy of the information, data and compilations as contained in this report. Readers are deemed to have waived and renounced all rights to any claim against the above-mentioned institution and their officers for any loss or damage of any nature whatsoever arising from the use or reliance upon such information, data or compilations.

3

FOREWORD

BY ECGBB CHIEF EXECUTIVE OFFICER, MABUTHO ZWANE

The gambling industry in the Eastern Cape has emerged from a disjointed past,

with gambling having been legal in the two former „homelands‟ of Transkei and

Ciskei, and betting allowed in the „Republic of South Africa‟ - as life was

ordered under apartheid.

Under these arrangements, illegal gambling proliferated. The advent of a

democracy order saw a liberalization of the industry and its harmonization to

allow for uniform regulation, which enabled the government to achieve broader

economic objectives including employment creation and economic

empowerment. Thus the National Gambling Act of 1996 came into effect,

repealed and replaced by National Gambling Act of 2004, followed by similar

pieces of legislation in the nine provinces.

In the Eastern Cape, the Eastern Cape Gambling and Betting Act came into

effect in 1997 establishing the Eastern Cape Gambling and Betting Board

(ECGBB). The ECGBB was allocated a total of five casino licenses for the

province, and was in that way enjoined to use them in promotion of the

endeavor to attain developmental and economic objectives. Furthermore, the

National Gambling Board also gave the ECGBB the go ahead to rollout 6 000

4

Limited Payout Machines (LPM‟s) and the concomitant right to license. Since

then, the main gambling modes that the ECGBB has regulated are the casino,

horseracing as well as the Limited Payout Machine industries, and related

activity.

Since then, no empirical data existed to guide either policy formulation in the

province or to shed enlightenment on gambling operations in general. The

commitment of the Board of Directors of ECGBB to efficiently regulating the

industry on an informed basis, and to place on a higher plane the enterprise of

regulating for socio-economic development led to the commissioning of this

report.

The study was designed to be representative of the Eastern Cape adult

population and was conducted in all six district municipalities of the province.

The study covers, inter alia, the following critical areas:

attitudes towards gambling,

participation in gambling activities,

economic impact of gambling and

the extent of problem gambling.

The study contains invaluable information and serves as an important baseline

data reference for all efforts at monitoring and evaluating progress made in our

implementation of ECGBB mandate.

The information contained in the report will be found useful by various

stakeholders and role players including government, the gambling industry,

the public, research organizations, academic institutions, and by many

others.

On behalf of the Eastern Cape Gambling and Betting Board I am exceedingly

pleased to, in presenting the report, extend appreciation to the following for the

professionalism with which they approached this important assignment: the

consortium members of TNS Research Surveys and EIS – Mrs Megan van

Vuuren, Ms Kim Larsen, Messrs Brian Swing and Lesley Powell;

economists – Messrs Antony Boting and Barry Standish; Professor Peter

Collins for his expert guidance on methodology and questions.

Monde Duma is the research manager of the ECGBB. He coordinated the

whole enterprise and over-extended himself in the process to ensure the

delivery of a credible, if authoritative, product.

____________________________ RM ZWANE CHIEF EXECUTIVE

5

CONTENTS

EXECUTIVE SUMMARY ..................................................................................................... 14 Attitudes to gambling ..................................................................................................... 16 Economic impact ..................................................................................................... 16 Macro economic contribution ............................................................................................ 16 Job creation ....................................................................................................................... 17 Corporate social investment ............................................................................................. 17 Contribution to tourism ...................................................................................................... 18 Property prices .................................................................................................................. 18 Displacement effects ......................................................................................................... 18 Income levels of gamblers ................................................................................................ 19 SECTION A (The Background) ............................................................................................. 21 1. INTRODUCTION ............................................................................................................... 22 1.1 The provincial context .............................................................................................. 22 1.2 The legislative framework ........................................................................................ 23 1.3 Concerns with gambling ........................................................................................... 25 1.4 Reseach objective .................................................................................................... 27 1.5 The structure of this report ....................................................................................... 28 2. THE METHODOLOGICAL APPROACH .......................................................................... 29 2.1 Frameworks for determining the socio-economic impact of gambling ..................... 29 2.2 Determining the costs and benefits of gambling ...................................................... 32 2.3 Indicators used in the 2009 Eastern Cape gambling survey ................................... 34 2.4 Econometric data ..................................................................................................... 35 2.5 Household survey .................................................................................................... 36 2.6 Intercept survey ..................................................................................................... 40 2.7 Qualitative data collection approaches .................................................................... 41 SECTION B (Gambling Participation) .................................................................................. 44 3. PARTICIPATION IN GAMBLING ACTIVITIES ................................................................ 45 3.1 The gambling industry in the Eastern Cape ............................................................. 45 3.2 Participation in gambling activities ........................................................................... 46 3.3 Commitment to gambling mode ............................................................................... 48 3.4 Demographic character of gambling participants..................................................... 51 3.5 Conclusion ................................. .................................................................... 62 SECTION C (The Social Impact of Gambling) ..................................................................... 66 4. PROBLEM GAMBLING.................................................................................................... 67 4.1 Incidence of problem gambling across studies ....................................................... 69 4.2 Problem gambling across modes ............................................................................ 70 4.3 Demographic profile of problem gamblers .............................................................. 73 4.4 Gambling risk (CPGI) .............................................................................................. 78 4.5 Reasons for gambling ............................................................................................. 80 4.6 Conclusion ............................................................................................................... 81

6

5. ATTITUDES TO GAMBLING ........................................................................................... 82 5.1 Acceptability of gambling......................................................................................... 82 5.2 The importance of gambling as a form of leisure .................................................... 85 5.3 Reasons for gambling ............................................................................................. 86 5.4 Attitudes to youth gambling ..................................................................................... 89 6. PERSPECTIVES OF THE IMPACT OF GAMBLING ....................................................... 91 6.1 Gambling Impact Index ........................................................................................... 91 6.2 Attitudes to gambling ............................................................................................... 92 6.3 Attitudes to gambling by demographic criteria ........................................................ 98 6.4 Attitudes to gambling by CPGI risk segments ......................................................... 99 6.5 Attitudes towards winning and losing ...................................................................... 99 6.6 Attitudes towards discipline ................................................................................... 101 6.7 Attitudes towards gambling and substance abuse ................................................ 102 6.8 Gambler self-reported impact ................................................................................ 103 6.9 The impact of gambling on the household ............................................................ 105 6.10 The regulation of the gambling industry ................................................................ 105 6.11 Conclusion ............................................................................................................. 107 SECTION D (The Economic Impact of Gambling) ............................................................ 109 7. THE MACRO ECONOMIC IMPACT OF GAMBLING .................................................... 110 7.1 Gross Domestic Product (GDP) ............................................................................ 110 7.2 Gross Geographic Product (GGP) ........................................................................ 111 7.3 Gaming Taxes ....................................................................................................... 111 7.4 Indirect household income .................................................................................... 112 7.5 Job creation ........................................................................................................... 112 7.6 Corporate social investment .................................................................................. 113 7.7 Tourism.................................................................................................................. 113 7.8 Property values ..................................................................................................... 115 8. DISPLACEMENT EFFECTS .......................................................................................... 118 8.1 Displacement by essential versus non-essential spending ................................... 119 8.2 Gambling expenditure ........................................................................................... 120 SECTION E (SUMMARY) ..................................................................................................... 122 9. SUMMARY ...................................................................................................................... 123 9.1 Incidence of gambling ........................................................................................... 123 9.2 Perceptions of gambling ........................................................................................ 123 9.3 Youth and gambling .............................................................................................. 123 9.4 Informal gambling .................................................................................................. 124 9.5 Problem gambling ................................................................................................. 124 9.6 Economic impact of gamnling ............................................................................... 124

7

LIST OF TABLES

Table 1 The sample

Table 2 Profile of participation across gambling modes

Table 3 Profile of most often participation across gambling modes

Table 4 Participation across informal gambling modes

Table 5 Participation by area type across gambling modes

Table 6 Location of gambling activities

Table 7 Frequency of participation in gambling modes located less than 10

minutes from home

Table 8 Desire for more gambling sites by district

Table 9 Participation by gambling mode and gender

Table 10 Participation by gambling mode across race groups

Table 11 Incidence of problem gambling by mode

Table 12 Gambling frequency

Table 13 CPGI risk segments by gambling mode

Table 14 Reasons for gambling

Table 15 Acceptability of gambling across gambler types

Table 16 Acceptability of gambling by importance of religion

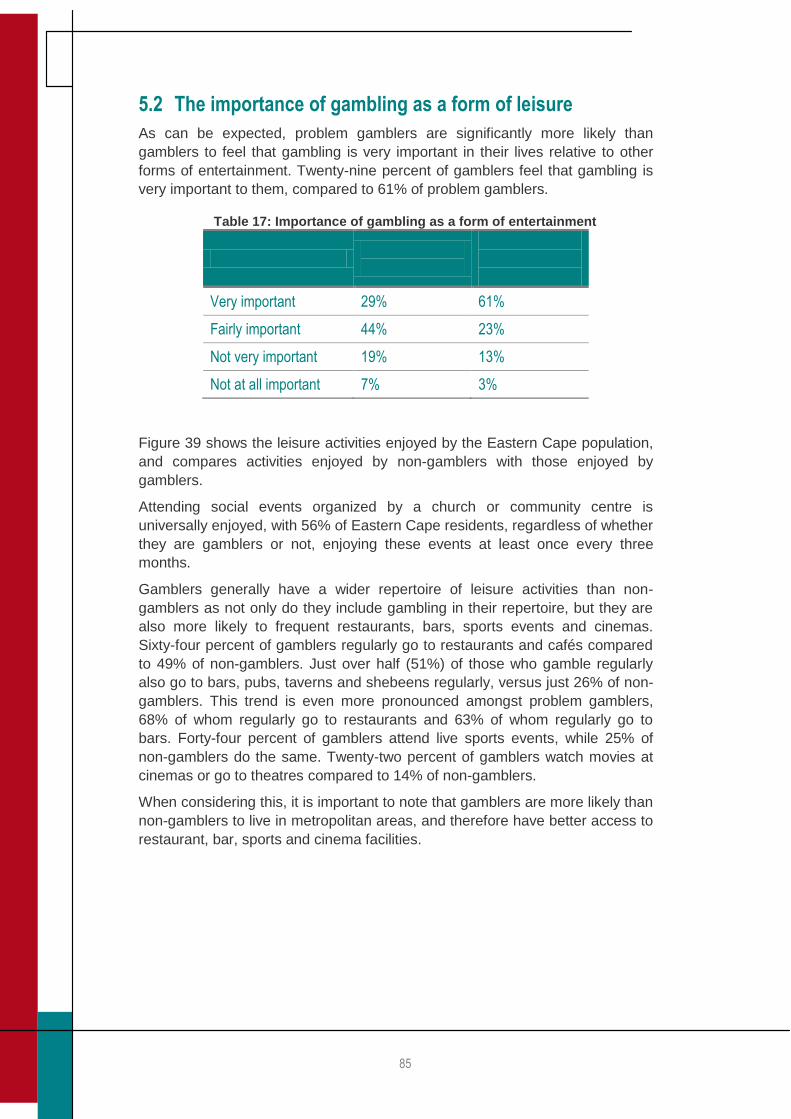

Table 17 Importance of gambling as a form of entertainment

Table 18 Attitudes towards gambling – the positives: gamblers compared to

non-gamblers

Table 19 Attitudes towards gambling – the negatives: gamblers compared to

non-gamblers

Table 20 Self-reported gambling impact

Table 21 Awareness of gambling entities and support programmes

Table 22 Contribution to GDP

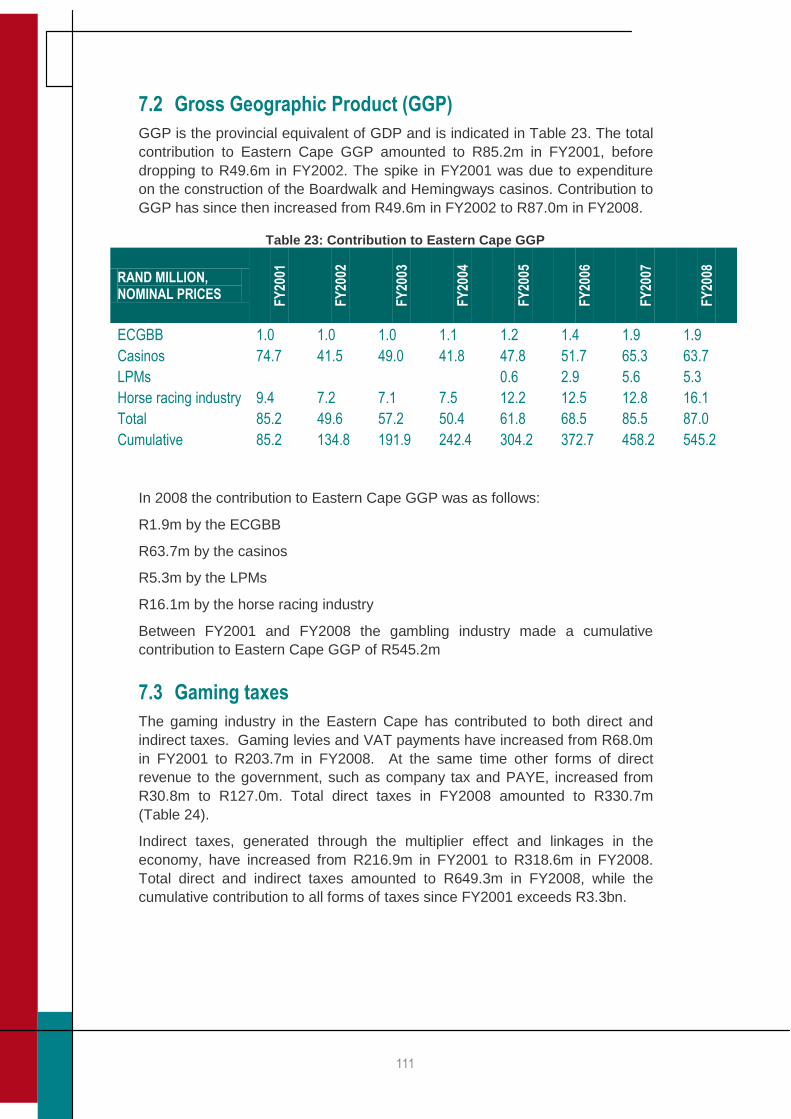

Table 23 Contribution to Eastern Cape GGP

Table 24 Contribution to direct and indirect taxes

Table 25 Contribution to indirect household income

Table 26 Contribution to direct and indirect job creation

Table 27 Contribution to corporate social investment

Table 28 Source of Wild Coast Sun GGR in 2007

Table 29 Boardwalk property price premium

Table 30 Hemingways property price premium

Table 31 Mean gambling spend

8

Table 32 Median gambling spend

9

LIST OF FIGURES

Figure 1 Frequency of participation across gambling modes

Figure 2 Commitment to gambling mode

Figure 3 Profile of participation by area type

Figure 4 Profile of participation by proximity to nearest bar or pub with slot

machines

Figure 5 Profile of participation by proximity to nearest horse or sports

betting outlet

Figure 6 Profile of participation by proximity to nearest casino

Figure 7 Profile of participation by gender

Figure 8 Profile of participation across age groups

Figure 9 Age at which gamblers started gambling regularly

Figure 10 Participation by mode amongst youth gamblers

Figure 11 Profile of participation across work status groups

Figure 12 Profile of participation across education levels

Figure 13 Profile of participation across monthly household income levels

Figure 14 Median monthly household income by gambling mode

Figure 15 Profile of participation across race groups

Figure 16 Profile of participation across religious groups

Figure 17 Profile of participation by importance of religion

Figure 18 Overview of gambling participation in the Eastern Cape

Figure 19 Comparative profiles of gambling trialists vs. non-trialists

Figure 20 Comparative profiles of regular gamblers vs. irregular gamblers

Figure 21 Incidence of problem gambling

Figure 22 Gambling and problem gambling participation compared

Figure 23 Gambling and problem gambling most often participation compared

Figure 24 Profile of problem gambling participation by area type

Figure 25 Incidence of problem gambling by district

Figure 26 Incidence of gambling more often if gambling site within 10 minutes

Figure 27 Profile of problem gambling participation by gender

Figure 28 Profile of problem gambling participation across age groups

Figure 29 Age at which problem gamblers started gambling regularly

Figure 30 Profile of problem gambling participation across work status groups

Figure 31 Profile of problem gambling participation across education levels

10

Figure 32 Profile of problem gambling participation across monthly household

income levels

Figure 33 Profile of problem gambling participation across race groups

Figure 34 CPGI risk segments

Figure 35 Acceptability of gambling

Figure 36 Against any form of gambling by gender

Figure 37 Against any form of gambling by area type

Figure 38 Against any form of gambling by age

Figure 39 Leisure activities enjoyed at least once every three months

Figure 40 Factors prompting the initiation into gambling

Figure 41 Six degrees of separation for non-gamblers

Figure 42 Reasons for gambling

Figure 43 Reasons for never trying gambling

Figure 44 Attitudes towards under-aged gambling

Figure 45 Gambling Impact Index

Figure 46 Associations with gambling held by the Eastern Cape population

Figure 47 Attitudes towards gambling – the positives

Figure 48 Attitudes towards gambling – the negatives

Figure 49 Profiling the Gambling Impact Index

Figure 50 How attitudes differ across CPGI segments

Figure 51 Attitudes towards winning

Figure 52 Attitudes towards losing

Figure 53 Attitudes towards discipline

Figure 54 Attitudes towards various aspects of gambling

Figure 55 Attitudes towards substances used when gambling

Figure 56 Statements about gamblers in the household

Figure 57 Displacement across categories

Figure 58 Displacement by essential versus non-essential expenditure

Figure 59 Gambling spend from most recent gambling activity

11

GLOSSARY

CONSUMER SURPLUS: The difference between the amount that a person

pays for a product and the maximum amount that the consumer is prepared to

pay rather than do without it.

GAMBLING: An activity in which something valuable is staked in the hope of

winning something of greater value and where the outcome is unknown to

participants. Investing on the stock market is excluded but playing the lottery,

bingo and charity „jackpots‟ in newspapers are included as well as Fafi,

scratch-cards, casino games and betting on horses and other sporting events.1

In the context of this study, bingo and charity „jackpots‟ in newspapers are

excluded.

GAMBLERS: In this report, Gamblers are defined as individuals who engage in

formal or informal gambling (as outlined above) at least once every three

months.

GAMBLING PARTICIPATION: The percentage of people who gamble at least

once every three months. This may be expressed as a percentage of the entire

population of the Eastern Cape, or as a percentage within certain defined

demographic or geographic cohorts (for example, within the Nelson Mandela

District Municipality or within the 18-24 year age group).

PROBLEM GAMBLING: Gambling behaviour where the individual gambles

excessively and thereby causes significant harm to themselves and to others

and fails to control this excessive behaviour.2

In this study, Problem Gamblers have been identified according to responses

to the 20 questions offered by Gamblers Anonymous (GA).

NON-GAMBLERS: Non-gamblers either never engage in gambling, or gamble

less than once every three months.

1 As applied in Collins and Barr (2006) 2 Derived from Collins and Barr (2006)

12

ACRONYMS

CASA Casino Association of South Africa

CPGI Canadian Problem Gambling Index

ECGBB Eastern Cape Gambling and Betting Board

GA Gamblers Anonymous

GDP Gross Domestic Product

GGP Gross Geographic Product

GGR Gross Gaming Revenue

LPMs Limited Payout Machines

NRGP National Responsible Gambling Programme

SAM Social Accounting Matrix

SU Small Urban

FY Financial Year

13

REPORT NOTES

This report exists as a synthesis of the reports produced during the 12 months

of the study on the socio-economic impact of the gambling industry in the

Eastern Cape. It draws liberally from the existing reports and frequently

references and refers the reader to these reports. The synthesis report

highlights the key findings and should be read in conjunction with the

background reports which exist as appendices to this document. These reports

are:

APPENDIX A: The economic impact of gambling in the Eastern Cape

APPENDIX B: The socio-economic impact of gambling in the Eastern Cape:

Findings of the qualitative study

APPENDIX C: The social impact of gambling in the Eastern Cape: Key

quantitative findings

Please note that all economic data presented, unless otherwise stated, refers

to gaming and gambling as it takes place in the casino, LPM and horse racing

industries in the Eastern Cape.

Also, the study focused on legal gambling, whilst participation and awareness

of illegal gambling is also reported on, online gambling was not a focus of the

study.

Small base sizes

Base sizes are reflected throughout the report and in some cases, an asterisk

will appear next to a base size. This indicates a small base size which must be

treated with caution.

*Note: Small base size

**Note: Extremely small base size – results indicative only

14

EXECUTIVE SUMMARY

Legalised gambling, with the exception of horse racing which has always been

legal, has been legal for more than a decade now. Since the legalization of

gambling in the Eastern Cape in 1997, all but one of the five provincial casino

licences have been issued and, of the 2 000 LPM licences awarded to the

province, a total of 1 345 LPMs have been rolled out that function across 252

LPM sites. The number these sites has since been reduced to 110 due to

liquidation of one of the two route operators in 2009.

Two legal casinos, the Wild Coast Sun and the Fish River Sun, were in the

Eastern Cape when gambling was liberalised. Today there are four casinos

with a fifth licence pending. These are the Wild Coast Sun in Bizana; Queens

Casino in Queenstown; Hemmingway's Casino Resort in East London; and

Boardwalk Casino and Entertainment World in Port Elizabeth. A pending

licence is expected to be located in Zone 4 (Mthatha or surrounding areas).

The Fish River Sun continues to operate as a holiday resort but no longer has

a casino licence.

The LPM industry is made up of route operators and site operators. Site

operators are the premises at which the LPMs are located which, in this

province, are taverns, clubs and pubs. The route operators lease the machines

to the site operators and give them logistical and other support. All sites are

linked electronically to the route operator. There are two route operators in the

Eastern Cape: Vukani and Luck At It. Luck At It has since been liquidated.

The horse racing industry is a wide and disparate industry that is made up of

horse breeders, horse trainers and racers, the race courses themselves (of

which there are two, Arlington and Fairview, both in Port Elizabeth) and the

betting industry. There are two types of betting operations: totalisator (tote)

betting and fixed odds betting. The difference between the two is that the tote is

a pool from all bets taken on a specific race while fixed odds betting is,

accurate to the description, a wager with fixed odds. Phumelela and Gold

Circle are the only licensed racing tote betting operators in South Africa

although only Phumelela is active in the Eastern Cape. There are seven fixed

odds bookmakers in the province.

Fifty six percent of the Eastern Cape population has gambled at some time in

their life and 39% can be considered regular gamblers (gamble at least once

every three months). The key difference between regular gamblers (gamblers)

and those who gamble less than once every three months rests in the

following:

Proximity to gambling site: Gamblers tend to live closer to gambling sites

Household income: Gamblers tend to be in the mid-range income band

(R1,200-R6,400 per month) whereas those who gamble less than once every

three months tend to be in the low income band (less than R1,200 per month)

Race and gender: Gamblers are most likely to be male and Coloured, while

those who gamble less than once every three months are most likely to be

female

15

Participation in gambling modes other than the lottery is undertaken by those

who have limited access to lottery, generally because they live in rural areas;

they are more likely to be young (18-24 years), black, have a low level of

education and limited income (LSM 1-3, not working). They tend to resort to

informal gambling, particularly dice games.

Those who only participate in the National Lottery and not any other forms of

gambling are more likely to be females, divorced, separated or widowed. Those

who participate in the lottery and other forms of gambling tend to live in

metropolitan areas (all forms of gambling easily accessible); are more likely to

be high income (LSM 7-10), working, educated and non-black.

The Eastern Cape has a problem gambling incidence of 2.8% which has

declined since 2001 when it had an incidence of 7.3% and 2003 when it had an

incidence of 4.1%.

The highest incidences of problem gambling are found amongst gamblers who

play at LPMs (28%), who play card games (25%) and who play dice games

(24%). The lowest is amongst gamblers who play the lottery (7%) and amongst

those who play scratch cards (8%).

Males have a greater propensity to become problem gamblers with 61% of

problem gamblers being male and 39% female. The highest incidence of

problem gambling of 5% is seen amongst Coloured people. White people have

the lowest incidence at 1%.

Attitudes to gambling

Attitudes to gambling in the province exist along a continuum from positive to

negative with a Gambling Impact Index score midway between positive and

negative (although leaning slightly towards the negative) of 48.6. The overall

attitude to gambling is strongly shaped by the individual‟s gambling behaviour

with the score derived from the responses provided by non-gamblers being

45.5, that from gamblers being more positive at 52.8 and the score from the

responses provided by problem gamblers being even more positive at 59.3.

The attitude is also shaped by proximity to others who gamble. Thirty eight

percent of non-gamblers who live with a gambler provided at least one negative

experience related to gambling, with 22% indicating that the gambler living in

their household has gambled until their last Rand was gone; 21% that gambling

makes them depressed; 19% that the gambler gambles to get money to pay

their debts and solve their financial problems, 16% that gambling leads to more

frequent drinking and smoking and 15% that gambling leads to arguments

about money in the home.

Negative attitudes to gambling are influenced by the harmful effects of

gambling on the individual and on society with key aspects being: (i) The

dangers involved in gambling; (ii) The costs of gambling and the implications

for gamblers who either cannot afford to gamble or, who are gambling in

excess of the money that they can afford to use for gambling; (iii) The

marketing of gambling which focuses on the positives of gambling and on the

possibility of winning without warning of the risks involved in gambling; and (iv)

The ease with which an individual can become addicted to gambling.

16

Positive attitudes are influenced by the entertainment value that the gambling

industry provides to individuals and the economic benefits of the industry to the

province. Specifically, the following key aspects were highlighted as positive

for the industry: (i) The industry provides entertainment that is fun, harmless

when used responsibly and that is safe for family and friends to enjoy together;

(ii) The gambling industry contributes to the community through local

investment and social corporate investment; and (iii) The gambling industry

makes a contribution to the local economy through casino revenue, the

provision of jobs and through attracting tourists into the Eastern Cape.

Almost half (49%) of the Eastern Cape population believe that gambling is

harmless when it is done responsibly; 44% believe that it is a fun leisure activity

and 42% that the gambling industry provides employment in the region.

Economic impact

The shift to legalised gambling and the growth in the sector since then have

been beneficial in several ways. First, they have given consumers an additional

choice of entertainment. Second, they have largely eradicated the illegal

(casino type) gambling industry and generated considerable tax revenue of

various sorts. Third, they have funded other infrastructure including roads and

hotels. The casinos in both Nelson Mandela Bay Metro and Buffalo City

brought about major regeneration in their local areas. There has also been

considerable spending on corporate social investment of various types.

Incomes have been generated, jobs created and a tourist attraction has been

established in Port Elizabeth.

The casino industry dominates the gambling industry and there has been a

relative decline in the contribution from horse racing. In 2000/1 total gross

gaming revenue (GGR) was a little over R500m with racing contributing

R70.1m. By 2008/9 GGR had grown to R1.1bn with LPMs making a R108m

contribution and racing a R120m contribution. In 2000/1 racing contributed

14.2% of GGR while by 2008/9 this share had fallen to 10.7%. At the same

time the LPM contribution had grown to 9.6%.

Macro-economic contribution

The most all encompassing measure of macroeconomic economic contribution

is contribution to Gross Domestic Product (GDP). This is reported as well as

contribution to Eastern Cape Gross Geographic Product (GGP), which is the

provincial share of GDP, contribution to taxes and contribution to indirect

household income.

In the 2008 financial year the Eastern Cape Gambling and Betting Board

(ECGBB), casinos, LPMs and the horse racing industry contributed R1.578bn

to GDP. Of this R34.3m was by the ECGBB itself; R1 175.7m by casinos

(includes an estimate of the contribution by concessionaires); R113.9m by

LPMs; and R254.2m from the horse racing industry. This contribution to GDP is

the equivalent of 0.8% of the overall Eastern Cape economy. Between 2001

and 2008 the cumulative contribution to GDP totalled R9.7bn.

17

GGP is the provincial equivalent of GDP. Total contribution to Eastern Cape

GGP amounted to R85.2m in FY2001, before dropping off to R49.6m in

FY2002. The high contribution in FY2001 was due the construction of The

Boardwalk and Hemingways. Contribution to GGP has then shown a steady

increase from R49.6m in FY2002 to R87.0m in FY2008. Between FY2001 and

FY2008 the gambling industry made a cumulative contribution to Eastern Cape

GGP of R545.2m.

The gaming industry in the Eastern Cape has contributed to both direct and

indirect taxes. Gaming levies and VAT payments have increased from R68.0m

in FY2001 to R203.7m in FY2008. At the same time other forms of direct

revenue to the government, such as company tax and PAYE, increased from

R30.8m to R127.0m. Total direct taxes in FY2008 amounted to R330.7m.

Indirect taxes, generated through the multiplier effect and linkages in the

economy, have increased from R216.9m in FY2001 to R318.6m in FY2008.

Total direct and indirect taxes amounted to R649.3m in FY2008, while the

cumulative contribution to all forms of taxes since FY2001 exceeds R3.3bn.

Indirect household income is generated through the multiplier effects. In

FY2008 the gaming industry in the province generated R796.8m in indirect

household income. Between FY2001 and FY2008 there was a cumulative

increase in indirect household income of over R5bn.

Job creation

The gambling industry has created and sustained three types of jobs. The first

are jobs in the provincial construction industry where the construction and

ongoing maintenance have sustained jobs in the industry. The second type of

jobs are those due to the ongoing running of the industry. The third type of jobs

are the so-called indirect jobs which are the result of the multiplied spending on

construction and operations.

The construction of The Boardwalk and Hemingways in FY2001 was a major

contributor to the 8 941 direct jobs created in that year. Employment by the

gambling industry has sustained over 4 000 for most years between FY2001

and FY2008. A total of 4 568 direct jobs were sustained in FY2008. This is the

equivalent of 0.3% of all formal employment in the Eastern Cape.

The LPM part of the industry is estimated to employ about 169 people. This is

up from an estimated 40 in 2005 when the first LPMs were installed. The horse

racing industry is estimated to employ about 329 people. This is up from 301 in

2001.

In FY2008 7 503 indirect jobs were created, with the majority resulting from the

casinos. Total contribution to jobs (both direct and indirect) totalled 12 070 in

FY2008.

Corporate social investment

The total value of corporate social investment (CSI) increased from R30 000 in

FY2001 to over R5.6m in FY2008. Most of this comes from casino

contributions. Total contribution to CSI since FY2001 exceeded R16.7m. We

18

were unable to source CSI by Luck At It or the horse racing industry. Anecdotal

evidence suggests that Phumelela donates all racing gate money to charity, but

we were not able to verify this.

CSI expenditure by the casino industry covers a wide range of initiatives.

These include community support like HIV/AIDs, supporting orphanages and

youth hostels; supporting local sports clubs and music events. There is poverty

alleviation; support for education; and promotion of arts and culture.

Contribution to tourism

There is general consensus amongst role players that the Eastern Cape has

significant tourism potential but this potential is not currently being put to good

use. The Boardwalk has added significant value to Port Elizabeth‟s tourism

sector and has enhanced Port Elizabeth‟s tourist appeal. The Boardwalk was,

at the time, the largest tourism investment in the Eastern Cape. Over 22 million

people have visited The Boardwalk since its opening which, after the beaches,

is the most popular tourism venue in the city. It is the only pure entertainment

venue in Port Elizabeth. Entertainment and shopping has consistently been the

second most important reason why people visit the Nelson Mandela Bay Metro.

Furthermore, the proportion of visitors coming primarily for the region‟s

entertainment and shopping almost doubled to 27% during the summer of

2007/8 compared to around 16% previously. The Boardwalk, after the beaches,

featured second on the list of the top 10 favourite attractions of visitors to

Nelson Mandela Bay, outranking Bayworld in third place.

The Wild Coast Sun is a well known destination casino that draws patrons from

far and wide. In doing this it helps promote tourism. In particular most of the

gambling taxes that accrue to the Eastern Cape come from people living in

other provinces. In 2007 the bulk of people visiting the Wild Coast Sun were

from KwaZulu Natal, with 31% originating from the Durban metropolitan area. It

can be safely assumed that these people would have spent a night or two at

the resort. Surprisingly 16% were from Gauteng and only 3% from the Eastern

Cape.

Property prices

The analysis of property value changes was limited to the three new casinos.

To quantify the impacts on property values, estate agents operating in the

areas surrounding the three new casinos were asked whether the casino had

changed property values and by how much. In total, property prices have

increased by about R1 084m on average as a result of the building of the three

new casinos.

Displacement effects

When people choose to gamble they are making choices within a finite amount

of disposable income. If people do choose to gamble with their money then

they choose not to spend it on other things. What does this mean for jobs and

expenditure? Any increase in jobs and expenditure which will occur as a result

19

of the establishment of a casino, for example, will be offset, to a larger or lesser

extent, by a loss of jobs in other sectors.

There are three circumstances when a casino will not displace other forms of

economic activity. The first is when there is a general increase in income. The

second is when the operation of the casino itself leads to an increase in

income. The third is when the displacement reduces imports from other

provinces or countries.

Survey results for the Eastern Cape, which were done as part of this study

reveal the following types of displacement.

The highest incidence of displacement is food for the household with 274

responses. This is followed by the „nothing specific‟ category with 111

responses. Other categories include:

Other entertainment with 107 responses

Transport had 53 responses

Savings or stokvel clubs 48 responses

Alcohol and housing 47 each

Medical aid or expenses and children/grandchildren received the least

responses with one and two respectively

Gambling displaces essential spending more than non-essential spending.

There were 468 essential and 154 non-essential responses, while „nothing

specific‟ received 111. The „other‟ and „don‟t know‟ categories received 13 and

34 responses respectively. This information was analysed in more detail and

the more important findings are:

While essential spending is the major category across all forms of gambling, it

is more prevalent for informal gambling and scratch cards, at about 65%. In

both cases household food is the category with the highest incidence

Displacement of essential spending is proportionately the lowest for casino

spending, at 50%. Casino spending is also the type of gambling where

displacement of non-essential spending is the highest, at 28%

The „nothing specific‟ category varies from 9.9% for other formal gambling to

14.9% for the lottery. The „other‟ category varies from 1.0% for casinos to 2.9%

for informal gambling, while the „don‟t know‟ category varies from 2.9% for

informal gambling to 8.1% for casinos

Gamblers in the 18 to 24 year and 40 to 49 year age groups are less inclined to

use essential spending than gamblers in the 25 to 39 year and over 50 year

age groups. The incidence of non-essential spending remains more or less

constant across all age groups

The incidence of essential spending declines as household incomes increase.

The incidence of non-essential spending fluctuates but tends to exhibit an

increase as household incomes increase. The „don‟t know‟ category shows an

increase with household incomes

20

The incidence of essential spending increases from around 55% for working

people to 67% for non-working people. The incidence of non-essential

spending compensates for this increase in essential spending, and decreases

from around 24% for working people to 14% for non-working people. The

„nothing specific‟, „other‟ and „don‟t know‟ categories are similar for both

working and non-working people

Income levels of gamblers

Part of the survey focused on the income levels of gamblers and what kind of

gambling they indulged in. There were two types of surveys, a household

survey (households generally) and an intercept survey (where people were

interviewed at the place where they were gambling).

The following characteristics were revealed by the household survey:

The majority of casino gamblers (53%) fall into the income categories of

R3 201 to R12 800 per month. Very few gamblers at casinos (6%) earned more

than R12 800 a month

About 89% of people who gamble on other formal types of gambling earned

between R801 to R12 800 per month, with the highest proportion (22%) being

in the R3 201 to R6 400 category

LPMs show a normal distribution about the R1 201 to R1 600 and R1 601 to

R3 200 per month income groups

Gamblers participating in horse betting are fairly well distributed across all

income groups up to R12 800 per month, with spikes in the R801 to R1 200

income group and the R3 201 to R6 400 income group. About 11% of all horse

gamblers fall into the up to R400 monthly income category

The majority of sports betting gamblers fall into the R801 to R12 800 income

categories, with the peak of 35% occurring in the R3 201 to R6 400 income

group

21

SECTION A

The Background

22

1. INTRODUCTION

Legalised gambling has grown markedly over the past decade. Since the

passing of the National Gambling Act in 1996, the industry has extended from

horse-racing to include casinos, bingo, sports betting, national lottery and,

recently, Limited Payout Machines (LPMs). It has grown from a limited activity

to one that is commonplace with almost half the South African population

having engaged in some form of gambling.3 As legalised gambling continues to

grow in popularity and prevalence, and new forms of gaming are introduced

and expanded, there is much public debate about the costs and benefits of this

sector to our society and to our economy.

It is against this backdrop that the Eastern Cape Gambling and Betting Board

(ECGBB) commissioned an assessment of the socio-economic impact of the

Eastern Cape gambling sector. While national studies to the effect have been

undertaken by the National Gambling Board (NGB); small sample sizes

disallow disaggregation by province, area (metropolitan, small urban or rural)

and by demographic variables such as race, gender, age, employment status

and income.

This report sets out to determine the extent and manner in which legalised

gambling has impacted, both socially and economically, on the Eastern Cape.

The specific impact referred to is one that touches the individual gambler, the

household and the community in the province and focuses on the positive and

negative impacts of legalised gambling and, in particular, the preventable

negative consequences.

1.1 The provincial context

The Eastern Cape is a predominantly rural province with a largely agro-based

economy; other key drivers being tourism and motor-car manufacturing. The

province consists of seven district municipalities with thirty eight local

municipalities. It has a population of over six and a half million and is regarded

as one of the poorer provinces in the country; more than half the population are

unemployed and 71% live in extreme poverty.

Further exacerbating the socio-economic challenges of the province is the

global crisis which has resulted in a decline in the motor manufacturing industry

internationally, in South Africa, and in the Eastern Cape. In a province where

the motor industry is a major employer and key contributor to the GDP, the

effects are ravaging. It is estimated, that the Eastern Cape will lose between 14

000 and 39 000 jobs this year. 4

Contrary to the economic decline experienced in the motor and construction

industries, the legalised gaming and gambling industry has achieved significant

growth since 1997/8, when first legalised in the Eastern Cape. Since then it has

made a noteworthy mark on the economy; during the 2007/8 financial year, a

total of R67.3 million was collected between April and December 2008 as

3. National Gambling Board (2005) indicates that at least half of the population, over the age of 18 had engaged in gambling activities in the three months prior to the study 4. http://www.info.gov.za/speeches/2009/09063016451002.htm

23

gambling taxes and fees from the gambling industry in the province. This is a

huge growth when compared to the R27 million collected in 1997/8.

It is for these reasons that the Honourable MEC, Mcebisi Jonas, suggests that

the Eastern Cape explore alternatives for expanding the gaming and gambling

industry in a manner that supports and facilitates economic development.

“Currently the Eastern Cape Gambling and Betting Board (ECGBB) are

making a substantial contribution towards the fiscus in a very effective and

efficient manner. We believe that the expansion and optimal regulation of

a number of potential new gambling activities such as traditional horse

racing and the development of the on-line gaming industry in the province,

will lead to an increase in the revenue base of the province.” 5

Notwithstanding this, the MEC recognises that the economic gains of the

gambling industry need to be measured and balanced against the social costs

of the industry. In this regard, the gambling sector has always been viewed as

different from other sectors of the economy. Unlike other industries in which the

market is the principal determinant of supply and demand, government

decisions have largely determined the size and form of the legalised gambling

sector. The result being that the gambling sector in the Eastern Cape, in South

Africa, and for that matter the rest of the world, exists as one of the most highly

regulated economic sectors; together with the alcohol and tobacco industries.6

1.2 The legislative framework

The framework for legalised gambling in South Africa was provided in 1996 by

the National Gambling Act (No. 33 of 1996)7 which aimed to consolidate and

harmonize the control of gambling activities in the Republic. This was

superseded, repealed and replaced by the National Gambling Act (No. 7 of

2004). These legislations aim to establish the principles and mechanisms by

which legalised gambling is regulated, controlled, policed and licensed and by

so doing to bring about uniformity in the legislation relating to gambling in the

Republic and in the provinces.

In the Eastern Cape, the gaming and gambling industry was legalised under

the „homelands governments‟ of Transkei and Ciskei. Gambling in Eastern

Cape areas administered then under the Cape Province continued to be illegal

with the exception of horse racing which was always legal. Legalised gambling

in the Eastern Cape was established in 1997 through the Eastern Cape

Gambling and Betting Act (No. 5 of 1997) which aimed to implement the

national regulatory framework as set out in the National Gambling Act (No. 33

of 1996) in the Eastern Cape.

This legislation, together with the National Gambling Regulations (2004), seeks

to protect the public from „over-stimulation of the latent demand for gambling‟.8

It does so by establishing a number of restrictions and guidelines including,

inter-alia, the following: (i) The protection of minors by limiting their access and

5. http://www.info.gov.za/speeches/2009/09063016451002.htm 6. Casino Association South Africa (2005): The National Gambling Act. http://www.casasa.org.za/newact.htm 7. This bill replaced The Lotteries and Gambling Board Act (No. 210 of 1993) 8. National Gambling Act (No. 33 of 1996)

24

ensuring that gambling premises are at specified distances away from schools;

(ii) Restrictions on the granting of credit or discounts to gamblers and

limitations on the directions to and distances from auto banking facilities; (iii)

Restricting the content of advertising for gambling activities; (iv) Ensuring that

gambling premises close for a minimum of six hours in every 24 hours; (v)

Enabling self exclusion from gambling and (vi) Making the posting of notices

announcing the dangers of gambling a prerequisite at licenced premises.

The Act (2004) includes a description – in relation to the norms and standards

of gambling – of the roles, functions and limitations of the Minister, the National

Gambling Policy Council and the National and Provincial Gambling Boards.

The legislation allows the Minister to establish limits on the total licences in

South Africa by providing the Minister the responsibility of determining the

maximum number of licences to be granted in the Republic and in each

province.9

At the provincial level, gambling and betting boards were established under

provincial gambling and betting legislations. In the Eastern Cape, the Eastern

Cape Gambling and Betting Board (ECGBB) was established as a statutory

body under the ECGB Act (No.5 of 1997). The most important functions of the

Board are the licensing of the legal gambling industry, the regulation of licence

holders, the collection of gambling taxes on behalf of the Province and

ensuring the abolition of unlicensed gambling.10 The control of gambling and

betting activity allows for the exclusion of problem gamblers, protection of the

public against unscrupulous gambling practices and the general control of

gambling activities in the Eastern Cape. Further, it is the responsibility of the

Board to ensure that a responsible legal gambling industry exists in the

province and that internationally recognised standards are complied with.11 The

Eastern Cape was granted five casino licenses under the National Gambling

Act to dispense. The province has been divided into five zones for these

purposes, with the objective of granting one license per zone. Currently, there

are four casinos operating in the province with one licence unallocated. The

Eastern Cape was provided licences for 2 000 LPMs of which 1 345 have been

allocated.

A more recent development in the gambling industry is that of online gambling.

The National Gambling Bill 48 of 2003 defines online gambling, or „interactive

gambling‟ as it is otherwise known, as „gambling games played or available to

be played through the mechanism of an electronic agent accessed over the

Internet‟. Interactive gambling was outlawed by the National Gambling Act of

2004 because government considered that more time was needed to conduct

research into this form of gaming. The National Gambling Amendment Bill

submitted to parliament in 2008 served to address this thorny issue by

providing for the licensing and regulation of interactive gambling within the

republic; putting in place effective mechanisms to control online gambling;

preventing gambling from becoming a source of crime and money laundering

and providing protection for vulnerable persons such as youth and problem

9. National Gambling Act (No. 33 of 1996) 10. ECGBB Terms of Reference 11. ECGBB Terms of Reference

25

gamblers. The nuts and bolts of implementing the regulation needs much work

and further debate.

One explanation for the high degree of regulation of the gambling sector is the

history of gambling and associated therewith moral objections to gambling as a

legitimated form of entertainment. Another is concern that legalised gambling

would produce a number of negative effects on society. These include the

negative consequences for gamblers themselves, such as the financial and

family distress caused by problem gambling and the negative externalities

imposed on society, such as increased poverty and crime.

1.3 Concerns with gambling

These concerns are not necessarily without merit. Wits Enterprise (2004), in a

study on the participation of under 18 year olds (school students) in gambling,

found that 13.5% exhibited what can be described as a mild predisposition to

gambling, whilst 5.1% indicated a strong predisposition to gambling. The study

found that students with a strong predisposition to gamble were

disproportionately more likely to be victims of physical assault (from both

parents and teachers), and to live in families where alcohol and gambling were

widely tolerated. Students who gambled excessively were also more likely to

hold strongly narcissistic and fatalistic views on life, which typically

underpinned attitudes to sex and HIV-AIDS and other risk-taking behavior. The

study did, however, argue that the findings are consistent with international

trends where some under-age gambling is experienced in the gambling

industry, given difficulties in enforcing age restrictions and monitoring individual

activity.12 Similar to this, the NGB (2003) found that gambling activity across all

modes of gambling decreases in proportion to age, with the prevalence of

gambling strongest in the 18 to 30 year old category.

The NGB (2005) looked at the prevalence of problem gambling in South Africa

and concluded that 0.52% of all respondents who gambled could be classified

as problem gamblers, suggesting an approximate 0.26% of all South Africans.13

In the same study, respondents were asked to comment on the extent to which

gambling by members within the household had a negative impact on their

household welfare. While the large majority of respondents did not report a

negative impact, a significant minority of 6,7% confirmed that gambling had a

negative impact on their households.14

Cosatu, coming from an economic rather than moral perspective, argued in

their 2003 submission to the Portfolio Committee on Trade and Industry that

gambling contributes negatively to the socio-economic wellbeing of the country

in that it increases poverty by encouraging poor people to „sink their hard-

earned money into gambling operations and gambling machines in the hope

that they will win‟.15 They provided, as an example, the Mpumalanga province

12. http://www.ecgbb.co.za 13. The report indicates that approximately half of South Africans engaged in gambling. As such, to determine the total % of problem gamblers the total percentage was halved. 14. NGB (2005): Socio economic impact of gambling 15. Cosatu submission on the National Gambling Bill to the Portfolio Committee on Trade and Industry, 2003.

26

which they argued granted casino licences despite being aware that a sizable

displacement of household expenditure was the main income for these

casinos. Similarly, the Northern Cape where pensioners gambled with the little

pension money that they have in the hope that they will be lucky and win the

funds that they need. With respect to Lotto, they stated that 40% of the adults

who buy Lotto tickets earn between R800 and R4000 a month, and 11% earn

under R800 a month with some admitting that they cut spending on necessities

like food and clothing in order to play the Lotto.

In support of Cosatu‟s argument of 2003, the NGB (2005) found that less

affluent members of the South African population are important participants in

gaming activities: 27,2% of gambling participants were unemployed; 13,5%

occupied part time jobs; almost 4% had no formal schooling; almost 13% had

only primary school qualifications and just over half earned less than R1 000

per month. Among low income earners and the unemployed, purchase of lotto

tickets comprised the large majority of gambling activity (just under three

quarters).

On the other side of the debate, supporters of legalised gambling recognize the

increase in consumer welfare for those who enjoy gambling and participate

„responsibly‟ in gambling as a choice of leisure entertainment. Further, the

importance of a legalised gaming and gambling industry for the eradication of

potential economic benefits, including job creation and development. Those in

favor of expanded gambling operations point to the revenue-generating

potential for lotteries and the taxation of casino revenues. As stated by the

Casino Association of South Africa,

By its very nature, gambling in some sectors of society remains a

controversial issue, although independent research commissioned by the

NGB shows that 73% of South Africans believe gaming is acceptable, and

89% do not have a moral, philosophical or religious objection to this form

of entertainment. About one in eight South Africans (12.2%) are opposed

to gaming, while the rest may choose not to gamble, but have no objection

if others do so.

In line with its role, the NGB has undertaken a number of studies assessing

trends in gambling activity since the early 2000‟s. The first major study of the

socio-economic impact of gambling, conducted in 2002, revealed a developing

gambling market showing considerable levels of volatility.16 A follow up impact

assessment in 2005 indicated maturation of the gambling market with a decline

in the number of people participating in the various legalised forms of gambling

available in the country.17

http://docs.google.com/gview?a=v&q=cache:K4dbpWCIR5cJ:www.cosatu.org.za/docs/2003/NatGamblingBill.B.pdf+cosatu+gambling&hl=en&gl=za 16. http://www.ecgbb.co.za 17. http://www.ecgbb.co.za

27

1.4 Research objective

This study, as the first study into the socio-economic impact of the legalised

gambling industry specifically in the Eastern Cape, provides a baseline on

which future policy decisions can be determined and from which changes in the

gambling industry can be monitored. The research outcomes of the study are

to determine awareness and participation in gambling; to assess the social and

economic impact of legalised gambling and to devise a replicable methodology

that can be used to monitor the sector in the future, highlight and identify

preventable negative consequences of legalised gambling, and make

recommendations as to how these might be addressed. As a first socio-

economic impact assessment of gambling in the Eastern Cape these research

outcomes have been achieved by addressing, inter alia, the following:

The awareness of legal and illegal gambling activities

Attitudes to legalised gambling by determining personal views of the

acceptability of gambling; the importance of gambling for recreation purposes;

the motives and perceived benefits from gambling and the negative and

positive impacts of gambling for the household, the community and the

province

The level of participation in legal and illegal gambling activies by understanding

the mindsets regarding participation in various modes of gambling and reasons

for participation or abstaining from doing so

Prevalence of problem and compulsive gambling by determining problem

gambling incidence and prevalence rates; possible negative impact of gambling

on household welfare levels and awareness of assistance available to and for

problem gambling

Prevalence of youth participation in gambling and the specific modes – both

legal and illegal - in which they engage and the motives for such.

The socio-economic contributions of gambling since its legalization. In order to

do so, the study will apply socio-economic indicators that can be used in the

future for monitoring the socio-economic impact of gambling. These will

include, inter-alia, the following:

With respect to impact on the economy: turnover and gross gaming revenue

(GGR); total winning payouts; government revenues from gambling including

taxation; contributions to capital expenditure including, where possible, analysis

of capital gains to consumers and industry including increases in private and

commercial property values related to gambling venues and development;

direct, indirect and induced contributions to the GDP; social corporate

investments made by the gambling industry; net growth in revenue and sales

from spill-off or feeder sectors

With respect to impact on household expenditure: Propensity to spend on

gambling; gambling expenditure in comparison with and as a proportion of

other household expenditure items; expenditure displacement effects;

household expenditure replacement analysis; allocation of winnings and

incidence of impulsive gambling expenditure

28

With respect to impact on development: Direct and indirect employment (and

the nature of such); job intensity: gambling related jobs created per R1 million

of gambling income (or GDP) compared with other sectors in the economy;

changes in employment and unemployment rates resulting directly from the

gaming industry development and the gambling tourism rate used to determine

the extent to which the gambling industry enhances tourism in the province

1.5 The structure of this report

The report consists of FIVE sections.

Section A provides the background to the study and contains the introduction

and the methodology chapters. The methodology chapter provides the

methodological basis for the study. It presents the methodological

assumptions, the sampling frame and the assumptions underlying the

methodology.

Section B focuses on gambling particiaption. It provides a description of the

gambling industry in the Eastern Cape, the participation therein and the

attitudes thereto.

Section C examines the impact of gambling in the Eastern Cape. It examines

the social impacts by presenting the perspectives of Eastern Cape residents on

the gambling industry overall; by focusing on problem gambling, youth

gambling and illegal gambling and the economic impacts of gambling.

Section D examines the impact of gambling in the Eastern Cape. It examines

the social impacts by presenting the perspectives of Eastern Cape residents on

the gambling industry overall; by focusing on problem gambling, youth

gambling and illegal gambling and the economic impacts of gambling

Section E examines the impact of gambling in the Eastern Cape. It examines

the social impacts by presenting the perspectives of Eastern Cape residents on

the gambling industry overall; by focusing on problem gambling, youth

gambling and illegal gambling and the economic impacts of gambling

29

2. THE METHODOLOGICAL APPROACH

Studies on the socio-economic impact of gambling rest on the theoretical

foundations of social cost estimations combined with cost-benefit analysis. In

terms of social cost estimations the focus is on the way in which the behavioral

outcomes of gambling impact on communities. Cost benefit analysis, on the

other hand, focuses specifically on the financial costs and benefits of gambling.

These quantitative measures are supported by qualitative studies that

determine the day to day lived experience of gamblers and the perspectives of

communities.

2.1 Frameworks for determining the socio-economic impact of gambling

A number of research frameworks exist for determining the socio-economic

impact of gambling. Where appropriate, this study drew from the lessons of

these research frameworks, most notable for this study are the Socio-

Economic Impact of Gambling (SEIG) framework developed in Canada, the

approach utilised in New Zealand and the method used by the National

Gambling Board in South Africa.

Socio-Economic Impact of Gambling (SEIG) framework

The Socio-Economic Impact of Gambling (SEIG) framework was developed by

Aneilski for the gambling sector in Canada to help researchers report on the

social and economic impact – both positive (benefits) and negative (costs) – of

gambling in Canada‟.18 It aims, because of the nature of the gambling, to

determine an actual, authentic and unbiased manner in which the worth of the

gambling industry can be determined.19

The methodology represents, according to the authors, „the highest standard

yet attained for a measurement methodology of assessment‟. The authors

expect that „the framework will assume the recognized and accepted position

as the preferred methodology for assessing the gaming industry‟s impact on

the individual and on society‟20. The SEIG framework reflects the

interdisciplinary and complex nature of gambling and takes a broad and

integrated systems approach to measuring impact.21 It consists of six impact

themes each with underlying variables and indicators that allow the positive

and negative impact to be determined. These themes are:

Impact Theme One: Health and Wellbeing

Impact Theme Two: Economic and Financial

Impact Theme Three: Employment and Education

Impact Theme Four: Recreation and Tourism

18. Ibid 19. Ibid 20. Ibid 21. SEIG

30

Impact Theme Five: Legal and Justice

Impact Theme Six: Culture

The methodology, whilst widely used in Canada, contains a number of

limitations and challenges that are worth noting as these were pertinent to the

transferability of the framework to the South African context and to this study in

particular. The first and most important challenge is the absence in South

Africa of adequately robust data to populate the various impact domains. The

framework provides the highest possible ambition in terms of variables and

data. Within the South African context data limitations are a major concern in

the implementation of the model as many of the variables and indicators

highlighted are not routinely collected and if so, certainly not validated and

acceptable for research purposes. The data required is for the full range of

social, economic and health aspects including co-morbidity, depression and

suicide. Much of this data would need to be collected from health clinics which

would be costly, time consuming and would exist as a large and challenging

research project in its own right.

The framework does not impose a hierarchy of variables. While this enables

the framework to be transferable and flexible, it makes it almost impossible to

determine the importance of variables as compared to each other as all

variables are provided equal weight. As such, the framework fails to provide a

streamlined approach to be used in the context of limited data, restricted time

and tight budgets – a description that best describes the South African context.

The challenge of estimating the full monetized cost and benefits of gambling on

a society is a challenge for any framework. While conventional cost-benefit

analyses are beneficial, there is still considerable disagreement among

economists as to the taxonomy of cost and benefit for gambling and how to

measure the impact.

The model is not concerned with transfers; for example, the impact on the

educational status of children of gamblers versus the impact on the educational

status of the children of employees of gambling institutions. In the Eastern

Cape, where social development is a key aspect, this is an important failing of

the model.

Nonetheless, and despite the concerns raised with the framework, the SEIG

framework provided the study with a systematic systems approach by providing

key analytic tools drawn from multiple disciplines and highlighting a set of

indicators to be considered when assessing the socio-economic impact of

gambling.

The New Zealand approach

Massey University developed an approach to determine the propensity for and

the socio-economic impact of gambling in New Zealand. In doing so they

adopted the following useful steps which they recommend for defining and

refining the methodology to be utilized. First, a review of the literature is to be

undertaken. This is followed by interviews with key informants. Data available

in a number of impact categories is then assessed. These categories overlap

very closely with that developed by the SEIG framework and might very well

31

have been drawn from the SEIG framework. Finally, a draft quantitative

instrument is developed which is piloted and then finalised.

The New Zealand approach provided the study with a useful approach to

finalizing the methodology and the instruments used in this study. It suggested

that the development of a methodology should be undertaken as a study in its

own right to ensure that the variables collected and the instruments utilized are

appropriate for the long term monitoring and assessment of the impact of

gambling in the region. While this was clearly a luxury that this study could not

afford, we used this research opportunity as an opportunity to test, pilot and

refine key research tools to be used by the ECGGB for the monitoring and

assessment of the impact of gambling in the future.

The National Gambling Board

The National Gambling Board (NGB) provided the study with an approach

piloted within the South African context. The NGB study was based on a

household survey combined with qualitative focus groups with gamblers and

the general public. It focused on:

Awareness of, attitudes to and participation (including the frequency of

participation) in gambling and in different modes of gambling

Negative social impacts of gambling such as the belief that gambling can lead

to negative social behavior and have negative impacts on the community

The extent to which respondents believe that gambling as a leisure activity is

valuable and furthermore, perspectives on the adequacy of gambling outlets

The incidence of problem gambling including youth gambling. Here the focus,

was on the impact on personal health, interpersonal relationships, work,

studies, crime and the financial well being of the person, the family and the

community

Household expenditure which included the total expenditure on gambling, i.e.

propensity to gamble; household expenditure displacement; allocation of

winnings and the extent to which gambling expenditure is budgeted or due to

impulsive spending

Analysis was undertaken by key demographics such as age, employment

status, educational level, race, gender, income

The approach utilized by the NGB provided an excellent case study of the data

available to the study of gambling in South Africa. This study, together with the

work undertaken by Collins and Barr (2001) and (2006) on problem gambling

was widely used in the design of this study.

32

2.2. Determining the costs and benefits of gambling

As provided by the studies above, particularly by the SEIG framework, an

analysis of the socio-economic impact of gambling should take into account all

the costs and all the benefits associated with gambling.

The benefits

In this regard, the benefits of the gambling industry would include job creation,

the generation of incomes and consumer surplus where consumer surplus is

defined as the difference between the amount that a person pays for a product

and the maximum amount that the consumer is prepared to pay rather than do

without it. In the context of this study consumer surplus refers to the

entertainment value that people derive from gambling which is just as important

as the pleasure and enjoyment that people derive from watching movies, going

to the theatre or engaging in sport.

The social costs of gambling

The benefits of gambling need to be balanced against the social costs of

gambling, some of which are quantifiable and some of which are not. One of

the most concerning is problem gambling and the impact that it has on the life

of the individual, that of the family unit and on the community. The definition of

problem gambling developed by Collins and Barr (2006) and the NGB (2005) is

applied in this report. In terms of this definition, problem gamblers are people

who,

“spend so much money and/or time gambling that they do significant

damage to themselves in areas of their lives which are important to them,

notably their personal relationships, their work, their sense of security or

self-respect find it difficult to control their gambling without assistance”.22

In addition to these characteristics, problem gamblers “… are obsessed with

gambling and think about it for much of the time when they are not gambling”

and use gambling “not as a means of enhancing the pleasure in their lives but

as a means of escaping pain”. 23

The challenge facing research into problem gambling lies not only in defining it,

but also in identifying the problem gambler. Here the difficulty lies in the

reluctance of the problem gambler to talk truthfully to strangers and even to

themselves, as addicts often lie to themselves about their problem. The

Gamblers Anonymous 20 Questions are used for this purpose in this report.

For the purposes of analysis seven affirmative responses were used to identify

problem gamblers and 14 affirmatives to determine pathological problem

gamblers. Furthermore, the Canadian Problem Gambling Index (CPGI) was

used to segment gamblers into groups using the following scoring regime: No

risk = score of 0, Low risk = score of 1 to 2, Moderate risk = score of 3 to 7 and

High risk = score of 8 to 27.

The Gamblers Anonymous 20 Questions were used by the National Gambling

Board in their national studies on gambling in South Africa and by the National

22 Collins and Barr (2006): p.30 23 Collins and Barr (2006): p.31

33

Centre for the Study of gambling. Using this framework made it possible to

compare the findings from the Eastern Cape to other studies undertaken in the

country.

Internationally there have been many attempts to measure the cost of problem

gambling. Aspects included in the assessment are increases in law

enforcement costs, in healthcare costs, in welfare payments and in other social

services costs. Other negative impacts which may or may not be thought of as

social costs include job losses, bankruptcies, family breakdown, personal

unhappiness and community breakdown. This is similarly so for determining

the negative impacts on local communities where it is probably fair to list the