37

1 NAREC 2019 Annual Financial & Tax Conference The State of Colorado Real Estate Kevin Kelley Executive Vice President United Properties

1

NAREC 2019 Annual Financial & Tax Conference

The State of Colorado Real Estate

Kevin Kelley Executive Vice President

United Properties

2

Since 1916, United Properties has continued to grow as an investor and developer of office, industrial and residential properties. We focus on a wide range of development projects which allows us key insights into today's challenging work/live/play environments. Our goal is to create deep roots-by successfully meeting a client's and community's goals with high quality projects that build a lasting legacy. We’ve developed signature, award winning projects that have shaped our cities and created special places in our communities. United Properties' headquarters is in Minneapolis with an office in Denver, Colorado as well. We’ve developed approximately 10 million sf of office and Industrial in Minneapolis and Denver since 2000, and have been the most active developer in MSP since 2010 as evidenced by receiving top developer status in 2014, 2015, 2016, and most recently 2017 from the Business Journal. United Properties has been one of the most active commercial developer in the Denver market since 2013, having started and/or completed the development of over 3 million sq ft of commercial office and industrial projects since 2013, much of it started without pre-leasing Our development team is a highly seasoned, energetic group that has developed and acquired property throughout the United States. Our principals include a commitment to providing a high level of expertise, to demonstrate flexibility in how our clients wish to work with us and in providing transparency to our development process. We are owned today by the Pohlad family.

United Properties The State of Colorado Real Estate

3

Colorado Overall The State of Colorado Real Estate

• Population of 5.7M as of spring 2019, 21st largest state in population; projected to grow to 7.3M by 2030.

• 7th fastest growing state in US since 2010, adding over 120K

new population per year since 2010. • In-migration peaked in 2014 at over 100,000, now has

moderated to about 50,000 new residents per year. • 2.7M total employed with a 3.5% unemployment rate. • Added over 500K jobs since 2010, average employment growth

of 63K per year since 2010 (5th highest the US since 2010). • 65K jobs 2018 and projected to add 49K jobs in 2019. • Relatively favorable business environment, a 4.63% corporate

and personal income tax rate, ranked in the top 15 states of places to do business in the US.

4

5

6

7

Denver Metro Area The State of Colorado Real Estate

• 3.24M residents, 19th largest metro area in US. • Since 2010, metro area has grown by over 800K or 3% per

year with average in-migration of 32K per year (peak of 44K in 2015).

• Population grew by 44,200 residents in 2018 (1.9%), with in-migration of 21,900 in 2018.

• Denver Metro added 350K jobs since 2010, average annual employment growth of 2.9% per year (4th highest in US).

• In 2018, GDP grew at 3.7%, 7th fastest in the US. Total employment is 1.7M.

• Overall economy grew at 1.9% in 2018, has current unemployment rate of 3.7%.

• Rankings: #1 Best Place for Business and careers (Forbes 2018) #2 Best Place to Live (US News World Report 2018) #2 Most highly educated state (US Census 2018)

8

9

10

11

Headquarters in Metro Denver The State of Colorado Real Estate

Since 2018, Denver has added 30 new HQ’s and expected to create over 7,500 new direct jobs, which will result in up to 1M sf of new commercial space. Some of these new HQ’s include:

12

Tech Industry in Denver The State of Colorado Real Estate

• Downtown Denver was the epicenter of technology growth with over 200,000 sf of positive net absorption.

• Southeast Denver, Colorado Springs and Fort Collins also had about 50,000 sf each of positive net absorption by tech companies.

• New and start-up companies often lease co-working space, which occupies at least 1.3M sf in metro Denver. Contrarily, companies that are rapidly expanding look for well located offices with attractive amenities and cost-effectiveness.

• Recent relocations and expansions include:

Accelo Apple ChannelAdvisor DTT Surveillance

Marketo Mavrck Mercer Advisors Mindflash

RLH Corp. Strava Switchfly Tapingo

Thanx Vertafore Xactly

13

Major Infrastructure Projects

14

15

16

18

19

20

Union Station &

LoDo

21

Union Station & LoDo The State of Colorado Real Estate

• The final phase of the Denver Union Station redevelopment was completed in July 2014 and was celebrated with the grand opening of the station’s Grand Hall and the Crawford Hotel.

• The station has attracted over $1 billion in private investment on nearly 20 acres of space in downtown Denver.

• In April 2016, the University of Colorado A line opened from Union Station to DEN.

22

Real Estate Market Denver Metro

23

24

Denver Office – Market Wide The State of Colorado Real Estate

• 117M sf total

• Overall Vacancy at 12.1% (18% with sublease space included)

• Decrease of 1.5% year-to-year • Class A vacancy of ___% • Sublease space at 2.6M sf which is down from 3M 18

months ago

• Net Absorption • 2.9M sf 2018 (vs. 5.5M sf 2016, 4.2M sf 2017) • 500K sf absorption Q1 2019 which is the highest since

2007 • Class A was 85% of the net in Q1

• Construction

• 2.1M sf of almost all spec. and most was located downtown

• Asking Rents

• $28.40/sf FSG, a 5.2% year-to-year increase • Class A at $31.20/sf FSG

25

Denver Office – Downtown

• Two Primary Downtown Submarkets • Midtown/CBD • Lower Downtown (LoDo)/Platte River Valley

• Plus, River North (RiNo) - to be discussed separately

• 29 M SF

• Vacancy

• 13.9% overall (19% including sublease space) • Class A at 15.9%, Class B at 11% • Sublease Space at 900K a 30% increase year-to-year of which 60%

is Class A • Chipotle

• Net Absorption

• 700K sf 2018 • 375K sf absorbed Q1 2019 (largest Q1 since 2007) • WeWork – 117K sf Midtown • Sun Run – 118 K sf Midtown

• Construction

• 1M sf • 450K in LoDo

• Asking Rents

• $35.88/sf FSG 3.6% increase year-year • $42/sf FSG LoDo

• Comments

• Limited Class A space in RiNo • Vacancy Class A distorted by three spec projects under

construction • Expense of LoDo tenants moving to Midtown for better value,

hence lower Class B vacancy

The State of Colorado Real Estate

26

Denver Office – RiNo

• North of downtown along Brighton Blvd. and commuter rail line to the National Western Center

• Created after 2015 with the opening of the University of Colorado A Line (Union Station to

DIA)

• Heavy infrastructure ongoing

• Center at 38th & Brighton commuter rail stop • 1.6M sf Class A (all opened since 2016)

• Under Construction is 429K sf

• Planned is 1.4M sf

• Absorption of 400K sf 2018

• Asking rates of $40/sf FSG

• Major Tenants include WeWork, Industry (Co-Work) and Home Advisors HQ

• Challenges

• New, hip, edgy but gritty • Safety? • Lack of amenities, lots of construction/infrastructure issues • Institutional tenants still prefer LoDo/Platte or CBD area, startups love RiNo

The State of Colorado Real Estate

27

Denver Office – Coworking Phenomenon

• Total Coworking space in CBD & River North: 1.7M sf

• Coworking companies occupy 5.6% of total inventory

• 27 coworking operators with 39 locations in Denver’s Central Business

District and RiNo • Five largest coworking tenants include:

• WeWork – 10 locations, 791,847 sf, 47% of coworking space • Industry – 2 locations, 230,00 sf, 14% of coworking space • Novel Coworking – 1 location, 125,233 sf, 7% of coworking space • Enterprise – 1 location, 66,000 sf, 4% of coworking space • Regus – 2 locations, 57,857 sf, 3% of coworking space

• Other large coworking companies in the market include:

• Taxi (Flight) • Galvanize • Serendipity Labs • Thrive • Industrious • Spaces • CTRL Collective • FirmSpace • Laundry

The State of Colorado Real Estate

28

Denver Office – Southeast

• Located I-25 southeast of Downtown between I-270 and Lincoln Ave. • Home to major regional office campuses of Fortune 1000 companies

• More auto centric, close to preferred suburbs, but light rail line has become a big

draw for recent tenants

• 36.5M sf • 370K sf under construction

• Little spec, mostly preleased (Newmont Mining)

• 12.6% vacancy, increase of 1%Taxi (Flight) • Highest vacancy is Class B at _____%

• Net absorption in 2017 and 2018 was between 800K to 1M per year

• However, negative net absorption of 200K Q1 2019

• Asking Rents - $25.70/sf FSG which is flat year-to-year

• Comments

• Flight to quality, TOD locations, or… • Class A with large parking for corporate tenants (INOVA) • Large Class B buildings vacancy with aging infrastructure, low parking • Smaller tenants relocate to Class C

The State of Colorado Real Estate

29

Denver Industrial Market The State of Colorado Real Estate

• 243M SF • S. CA at 2.2B SF (Inland Empire - 550M sf)

• Three Major markets

• I-70 east/Central Denver/Airport (130M sf, 54% of total) • Main large warehouse distribution market

• Northwest/Boulder Turnpike (30M sf) • Tech/RD/light manufacturing market

• Southeast (20M sf) • Smaller regional tenants, distribution/light manufacturing

• Vacancy of 6% (6.3% with sublease)

• Up from 4.7% EOY 2017

• Construction • 3.7M sf of which 2.7M sf in the I-70 market • Only 15% preleased

• Absorption

• 500K sf net absorption in Q1 2019, however, due to net of Amazon delivery in late 2018, net absorption in 2018 was off 25% • In 2014 - 2017, absorption was greater than new deliveries

• I-70/Airport Market

• Largest submarket at 84M sf • Under construction is 2.7M sf with absorption in 2018 of 1.1M sf

• Three new projects of 500K or greater U/C with one 750K sf building still vacant 18 mos. after completion

• Comments • Industrial is hot in capital markets, low cap rates and developers loaded with equity looking to build, driving up land prices • Amazon completed two large fulfillment centers but not a plethora of other large E-Commerce tenants have located here • Large users (>500 SF) can wait for a BTS or buy land • Sweet spot for spec developers is to be ready for tenants in the 100-200K sf range that can afford or wait for a BTS

30

Denver Residential Market The State of Colorado Real Estate

Multi-Family (Denver Metro) • Trends are positive despite the enormous supply of new

projects

• Net absorption Q1 of 5,500 units vs 3,950 units supplied

• Net absorbs in 2018 was 13,708 units and 11,800 units in 2017.

• Vacancy decreased to 5.4% vs. 6.1% same period 2018

• Average rents increased to $1.74/sf vs $1.67/sf same period 2018

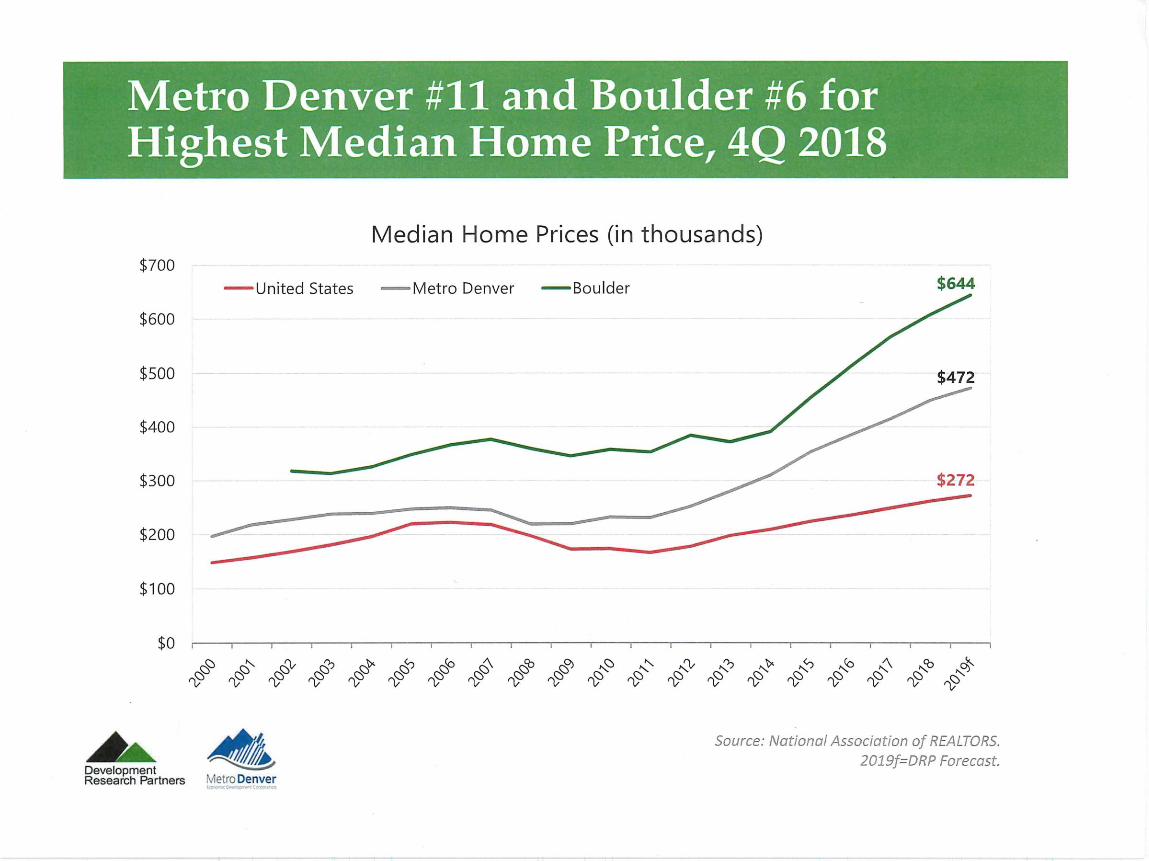

Housing • Affordability is big issue (see attached)

• Few condo’s have been built despite some changes to

construction defects legislation

• Total permits in metro area leveling out at 14K per year still not enough supply to satisfy demand

• Home sales slowing due to lack of low-end inventory, and prices • Market is saturated in exurbia, particularly homes

priced at over $800K

31

32

33

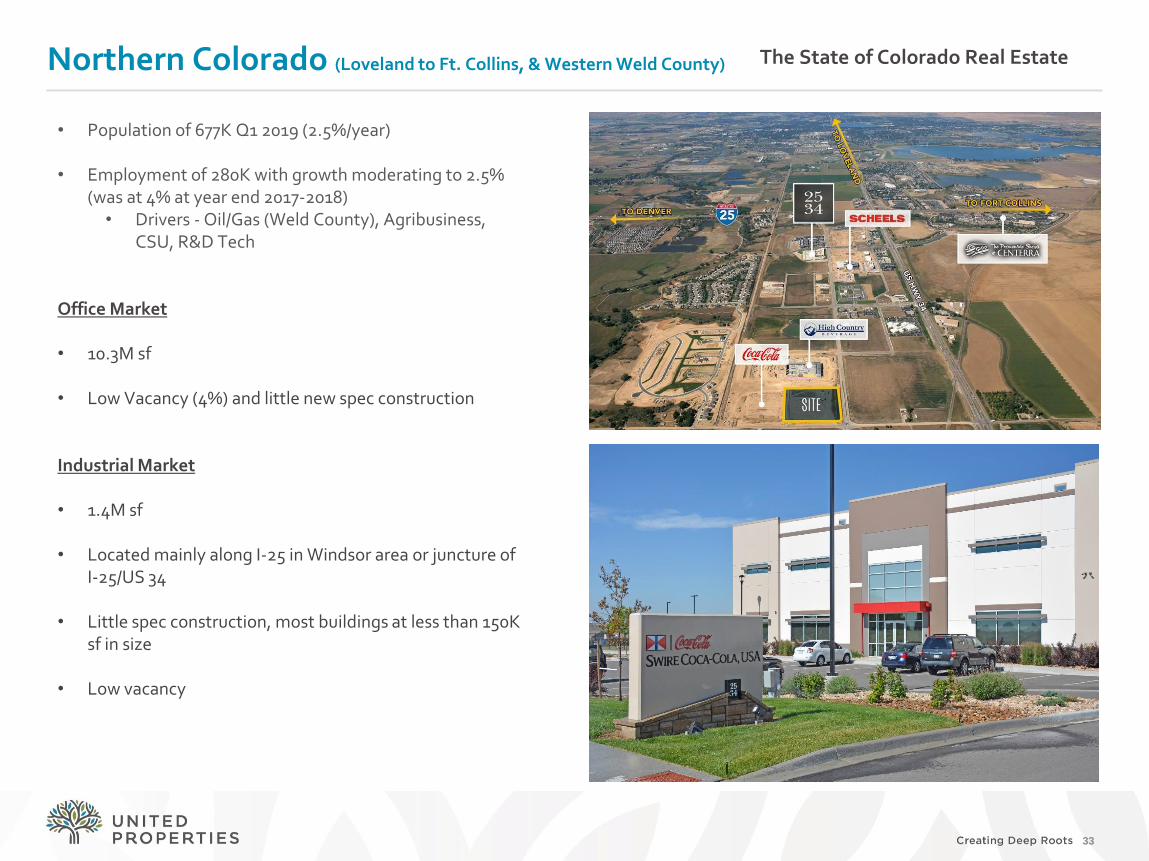

Northern Colorado (Loveland to Ft. Collins, & Western Weld County) The State of Colorado Real Estate

• Population of 677K Q1 2019 (2.5%/year)

• Employment of 280K with growth moderating to 2.5% (was at 4% at year end 2017-2018) • Drivers - Oil/Gas (Weld County), Agribusiness,

CSU, R&D Tech Office Market • 10.3M sf

• Low Vacancy (4%) and little new spec construction Industrial Market • 1.4M sf

• Located mainly along I-25 in Windsor area or juncture of

I-25/US 34

• Little spec construction, most buildings at less than 150K sf in size

• Low vacancy

34

Colorado Springs The State of Colorado Real Estate

Population of 775K in the metro area (El Paso County) Employment base of just under 300K people with unemployment rate of 3.7% • Drivers - Military, US Olympic HQ, Defense contractors, Religious organizations

• Low power rates have driven data center business

• Lower costs of labor and housing is affordable

(average home price is $100K less than Denver) Office Market • Low vacancy rate (8.5%), 400K sf net absorption

with little new construction

• Average NNN rental rate ($13.25), rates need to justify new construction due to higher land and materials costs, makes it difficult to justify new spec construction

Industrial Market • Low vacancy (7%) with almost 940K sf of absorption 2018

• Like Northern Colorado, companies with a large presence in Denver are looking for a

smaller presence in Colorado Springs (Amazon, USAF)

• Most Industrial located south of the Airport Comments • Colorado Springs is becoming a bedroom community for Denver residents who are

looking for affordability and don’t mind the commute

35

Big Picture Ideas

Positives • Reputation of getting big projects done

• Attracts outside capital

• Colorado is second most highly educated

populace in US

• 4th highest concentration of high-tech workers

• Second largest employer in the aeronautics industry

• 7th fastest employment growth rate and has ranked in the top 10 over past 7 years

• #1 healthiest state for the past 15 years

• Top ten in population growth for past 12 years (#1 in 2014, #8 in 2018)

The State of Colorado Real Estate

Negatives • Commercial Real Estate Taxes

• Amendment Fatigue

• Political Climate (national & local)

• Colorado getting younger, and “bluer”

• Labor pool • Affordable housing

• Low graduation rate at K-12

• 6th lowest graduation rate in the US

• Lagging Infrastructure • Transportation (road) funding lags, expenditures

per capita of $543/person, 26th in US

36

QUESTIONS??

37

Thank You!