19

THE STORIES BEHIND THE NUMBERS Research on shared services and outsourcing trends and developments in Central & Eastern Europe

| Date post: | 12-Mar-2018 |

| Category: |

Documents |

| Upload: | nguyendieu |

| View: | 219 times |

| Download: | 1 times |

THE STORIES BEHIND THE NUMBERSResearch on shared services and outsourcing trends and developments in Central & Eastern Europe

2 | The stories behind the numbers The stories behind the numbers 3

Table of contents

CHAPTER 1 INTRODUCTION

CHAPTER 2 SELECTING THE RIGHT LOCATION: FROM A QUANTITATIVE TO A QUALITATIVE FOCUS

CHAPTER 3 IMPLEMENTING A SERVICE CENTRE: FIRST TIME RIGHT!

CHAPTER 4 EXECUTING GOVERNANCE: SUPPLIER OR PARTNER?

CHAPTER 5 MANAGING TALENT: ENSURING A STABLE WORKFORCE

CHAPTER 6 DRIVING EVOLUTION: AVOIDING A STEADY STATE

CHAPTER 7 FUTURE OUTLOOKA REGION TO STAY

03 07

11

16

21 24

30

CHAPTER 1INTRODUCTION

© 2015 KPMG Advisory N.V. © 2015 KPMG Advisory N.V.

4 | The stories behind the numbers The stories behind the numbers 5

Shared services and outsourcing to Central and Eastern Europe (CEE) has been on the agenda in many board rooms in the past decade. Previous KPMG publications and reports of other market specialists have been supporting this attention by recording a solid growth in both the number of captive shared services centres as BPO delivery centres in the region. The countries included in this study host around a 1.000 centres employing approximately 283,000 employees making the shared services and outsourcing industry a significant contributor to the Central and Eastern Europe economy.

Service centres1 supporting various back-office functions and processes in areas such as IT, F&A, HR, and procurement continue to grow, while at the same time front-office activities such as analytics, sales and marketing support are being added. Recent studies indicate this growth is not stagnating. To the contrary, KPMG’s “The State of Services and Outsourcing in 2014” report shows that the investments intentions in shared services and outsourcing solutions by organisations are on a record high, while a study executed by the Shared Services and Outsourcing Network (SSON) shows that 59% of the organisations involved in the study expect further growth in their shared services initiatives. This topic has evolved in an industry of a significant size and relevance for the region and shared services or outsourcing to the CEE region shall remain a viable option for many companies in the near future.

A DIFFERENT RESEARCH ANGLE

The fast majority of the reports on this topic only reflect in numbers thestate of the shared Services and outsourcing in the CEE region. We have all seen the metrics and graphs showing the inflation percentages, the economic growth, the availability of talent and language skills, presented in a wide variety of market reports. This study does not try to come up with new numbers; it approaches Central and Eastern Europe from a different point of view, trying to capture the real stories behind the numbers.

The objective of this study is to gather,define and explain the factors behindthe success of the shared service and outsourcing industry in the CEE region and most importantly the service centres itself, to capture the leading practices and latest developments and to provide a glimpse of the future of this industry in the CEE region.To get these insights, we conducted more than 50 conversations with service centre managers, delivery centre managers, investment agencies, recruitment agencies and industry experts in the period January-November 2014. By doing so, we were able to get the real ‘war stories’ on the table for discussion, that can help organisations in the implementation of their shared services and BPO strategies. We focus on five themes that dominate the agenda of service centre managers in the six countries studied.

STORIES ABOUT A REGION TO STAY

Figure 1 / Geographical scope of the research

GEOGRAPHICAL SCOPE OF THIS RESEARCH We focus on a number of countries and locations within this study. By including more sophisticated shared services and outsourcing destinations (e.g. Czech Republic, Poland) as well as the relative newcomers (e.g. Bulgaria, Latvia) we were able to obtain a balanced view of what is happening in the sector in this region.

Although we kept an open perspective, our conversations with the service centre managers were focused around five central themes that are introduced in the figure on the next page.

Poland Czech Republic Hungary Latvia Romania Bulgaria

Population 38,5 million 10,5 million 10,0 million 2,04 million 21,0 million 7,3 million

# of centres > 470 > 200 90 36 > 80 > 45

# of employees >128.000 > 50.000 34.000 4.300 45.000 > 22.000

Main Service centre / BPO location(s)

Krakow Warsaw Wroclaw Katowice Lódz Poznan

PragueBrnoOstrave

Budapest Riga BucharestClujNapocaTimisoara

Sofia

1 In this report the term service centres shall refer to both captive shared services centres as ITO / BPO delivery centres

© 2015 KPMG Advisory N.V. © 2015 KPMG Advisory N.V.

6 | The stories behind the numbers The stories behind the numbers 7

CHAPTER 2

SELECTING THE RIGHT LOCATION: FROM A QUANTITATIVE TO A QUALITATIVE FOCUS

Figure 2 / Five central research themes

Selecting the right location

Implementing a service centre

Managing talent

Executing governance

Driving evolution

FIVE CENTRAL RESEARCH THEMESMaking the right location decision is more than comparing numbers, it is about getting a sense of the location and experiencing this is the place where an important part of the business can be executed.

The complexity of transitions are no longer underestimated. It is considered as the key factor for success in the service centre journey by our service centre managers. We capture the latest trends and developments on this aspect.

Service centres are a people business. Recruitment is as important as retention and having the right talent management approach is a real differentiator.

The theme that has been and will be on the agenda for a long time. The panacea has not been found, yet experiences of service centers on how to organize yourself internally and how to position the service centre within the organisation as a whole results in valuable insights.

Service centres have to continuously reinvent themselves by adding new services and clients. It’s the best way to keep delivering added value and thus to survive. We discussed with service centre managers how they approach this and what is happening in the CEE region.

Selecting the right location – in terms of cost and quality benefits

– is an important step in the strategic phase of establishing

a service centre. It is definitely not all about cost levels: service

centre managers allocate more value to factors such as the available

talent, language availability, talent pool competition.

© 2015 KPMG Advisory N.V. © 2015 KPMG Advisory N.V.

8 | The stories behind the numbers The stories behind the numbers 9

STARTING WITH A QUANTITATIVE COMPARISON The majority of the service centre representatives indicate that their organisation executed a detailed location analysis. As one service centre manager said: “Many potential locations were tossed around, with many people having opinions on the potential of these locations. We felt we needed a detailed location analysis to enable objective decision-making. And we were right to do so”. Some of the organisations did not execute a detailed location analysis, but leveraged on existing sites. At a first glance, this makes sense, as those organisations know the existing market and culture and already have the infrastructure in place, however one service centre manager did comment that a more detailed location analysis would have made sense, “Because the stakes are high. You probably stay there for at least 15 years and once you have established yourself, you want to be able to explain to your business partners why you preferred this particular city. It helps to build your story if your argument is solid. Starting a service centre in an existing location did diminish that in our case”.

The first stage of a location analysis may involve taking a large number of quantitative factors into account. By comparing locations using these factors as criteria, organisations arrive at a shortlist of two or three locations from an initial list of between seven and ten. KPMG continuously gathers and structures data regarding these locations in order to be of value for organisations considering shared services or outsourcing. Most of this data is publicly available or can be

acquired from country investment agencies. As these analyses are confidential most of the time, organisations tend not to reach out to potential locations during this phase of the location analysis.

During the interviews, we identified the most relevant factors in evaluating a delivery location. Although cost was always mentioned, more value was placed on the available talent, language availability, talent pool competition and the ease of employing staff. Figure 3 shows the relative importance of location analysis factors as rated by the practitioners who contributed to this study.

Figure 3 / Relative importance of location analysis factors.

Although it might be obvious that those responsible for the delivery indicate that talent and language availability is the most critical factor for them, the feedback on this was strong. As one service centre manager replied, “It’s nice to talk about costs, but if you don’t have the right people to deliver the services there will be panic. Without the right supply of talent, you can’t deliver”. Another service centre manager replied, “In the end it is about finding the right balance between talent availability, labour pool competition and cost effectiveness. We are continuously looking at that balance”.

Service providers tend to go one step further and keep analysing potential locations for their delivery centre network on all kinds of relevant factors on a continuous basis. This makes sense in light of the fact that service providers owe their existence to effective execution and continuous efficiency improvement and are in fact forced to make location analysis a core competence, such is its contribution to their competitive advantage. One service provider replied, “We have to be able to ramp up in resources fairly quickly, at least faster than captives have to. That’s why we tend to focus more on capital cities instead of second-tier cities as the resource offering (both in terms of quantity as well as diversity) is better for us in capital cities”. We have not seen captive centres actually moving from a Central or Eastern European city to another in the course of our research, but we have seen examples of service providers doing so. This is why we see service providers first in newer upcoming locations before captive centres consider a new location as a realistic alternative.

AND ENDING WITH A QUALITATIVE ASSESSMENT Our conversations show that qualitative factors carry weight in the final decision-making process. After having short-listed two to three cities in the initial phase of the location analysis process, organisations execute a deeper analysis of these cities. Project teams will visit those locations and have conversations with investment agencies, recruitment agencies and existing service centres, which gives a more subjective view of the location. As one service centre manager noted in response to our study, “We executed quite a rigorous desk research on potential service centre locations. In the end, two locations were left and senior management visited those locations. An important deciding factor in the end was the presence of an international expat community and English private schools. This actually turned the decision from city X to city Y”.

Service centre managers stress that proactive support from a government investment agency is appreciated in this phase. Experiences in this area differed

by country and/or city ranging from highly supportive in arranging meetings to limited support. Many interviewees see some room for improvement when it comes to the government support factor. As one service centre manager indicated, “Government support is too limited. The service centre environment is not being promoted. Students hardly know this is a strong employment sector and foreign investors do not realise we are good at this here. It would really help us and the economy if our government were to invest more in this”. From a macro economic perspective governments can have high (positive) impact by addressing this topic in their policies. In our view, it is important that leadership teams actively participate in the location analysis to develop real understanding and to create commit-ment. One of the options is to organise a site visit with a duration of at least two days for each of the final two to three locations, which should include meetings with other service centres, investment agencies, political representatives and recruitment agencies. Additionally, this is an important step towards understanding the atmosphere, culture and social life in the city as part of the qualitative comparison.

“As captive you don’t want to be the first to enter into a location.”Partner, KPMG Hungary

21

33

26

13

7

Cost

Talent and language

Business environment

Accessibility & infrastructure

Current client footprint

“As a new entrant, you don’t want to disrupt the existing service centre.” Shared service centre manager, Budapest

© 2015 KPMG Advisory N.V. © 2015 KPMG Advisory N.V.

10 | The stories behind the numbers

ESTABLISHED VERSUS UPCOMING LOCATIONS IN CENTRAL AND EASTERN EUROPEShould organisations locate in a proven mature city or in a growing, less mature ervice centre location? The established service centre locations in the CEE region are capital and main second-ties as Prague, Brno, Budapest, Warsaw, Krakow, and Bucharest. Locations such as Sofia, the Baltic States, second-tier cities in Poland and Romania, and

recently also in Serbia are currently seen as the newer upcoming service centre locations. In most cases, this leads to a discussion about cost effectiveness versus risk.

Service centres have strong opinions on this topic. One interviewee said, “The newer greenfield locations often look attractive, but, as a captive centre, you don’t want to be the first in a certain location. The risk is simply too high. If number two moves in, your attrition rates will go through the roof!” and another service centre manager

Established locations Upcoming locations

Pros Pros

- Better general awareness of the shared services and outsourcing industry

- Good talent and language availability as shared services and outsourcing is a well-known industry

- Better availability of local middle and senior management

- Higher-quality infrastructure in terms of road network and office space

- Increased government support

- Better cost attractiveness due to lower labour and infrastructure costs

- More ‘freedom to operate’, as the shared services and outsourcing industry is less industrialised

- More incentive opportunities- Less talent competitiveness

Con’s Con’s

- Less cost attractive due to higher labour and infrastructure costs

- Higher level of competitiveness in attracting and retaining talent

- Shared services and outsourcing sector is more industrialised

- Higher impact of new entrants on the attrition rate of the service centre

- Business environment less adjusted to shared services and outsourcing industry (e.g. government support and university cooperation)

- More limited labour pool and less awareness of the shared services and outsourcing industry within the available workforce

said: “As captive you only want to move to a certain location if there is are a reasonable number of similar organisations already active with the same service scope you want to offer”.

Bear in mind the size of your centre compared to other centres at the location; you don’t want to start a centre of 250 people in a location with an industry size of 80,000. This also works the other way around; you cannot start a centre of 2,500 FTEs in a location with a current industry size of 12,500 FTEs. Balance is the key here”. Service centres can encounter difficulties in establishing a brand for the service centre and attracting top talent if their size is not in line with the market size.

Service providers can be more aggressive in this respect as they are able to temporarily backfill locations with staff from other delivery centres. One delivery centre replied, “When starting a new delivery centre, we often start by transferring the non-complex activities from an existing centre. This allows us to gently introduce a new delivery centre into a network and let it grow from there”. The ITO / BPO service providers are experienced in setting up delivery locations, training staff and getting a centre up and running.

“The ability of a location to attract sufficient talent does not only depend on the number of universities but also on the locations’ social life such as the number of clubs.”Delivery centre manager, Budapest

CHAPTER 3

IMPLEMENTING A SERVICE CENTRE: FIRST TIME RIGHT!

The stories behind the numbers 11

The transition of activities from existing parts of an

organisation towards a shared service centre of

outsourcing provider has a huge impact. Not only from

an employee perspective, but also from a way of working

perspective. A successful implemen tation is key for

service centre success in general. What the expert say: take

sufficient time to prepare, take one step at a time, get experienced

practitioners in, do not apply short-term fixes, but apply a ‘first time right’

methodology.

© 2015 KPMG Advisory N.V. © 2015 KPMG Advisory N.V.

12 | The stories behind the numbers The stories behind the numbers 13

A SUCCESSFUL TRANSITION IS THE KEY FACTOR FOR ESTABLISHING A SERVICE CENTRE

A well-executed transition is the key to achieving a successful service centre. Nearly all service centre managers confirmed this: without a proper transition, the service centre strategy is doomed for failure or at the very least it can take a long time to regain the trust of (internal) clients and reach a stable situation.

“Transition is king!” Service centre manager, Budapest

The prerequisites for a successful implementation are robust project management, sufficient investment capabilities, senior management support, and the involvement of experienced service centre practioners (“those who have done it before will help you deliver throughout the process”) in combination with team members with a high level of company knowledge. A last prerequisite confirmed by nearly all service centre managers is that of perseverance. There will always be issues and resistance and overcoming this resistance requires huge effort.

“Be persistent, stay in control, and have stamina. Expect to be blamed, but keep going.”Shared service centre manager, Poland

Overall, we are impressed withthe methodologies used by theorganisations who contributed to this research. The majority of the

organisations use formalised transition methodologies that involve detailed project plans, planning overviews, handover documentation and sign-off criteria. The implementation of a completely new captive service centre generally takes about eight to ten months: three to four months to complete a contract for the establishment, three to four months to arrange for furniture and fixtures and two to three months for the recruiting and training of personnel. “We used extremely detailed transition plans. It was very clear to everyone what work and which employee was being moved in what timeframe. It also included detailed training plans and dual location

visits.”

In fact, executing transitions has become a core capability of more mature shared services centres and BPO centres. As centres grow over time, more processes are moved into the centre and centres become more experienced in managing transition projects. They create their own standards and procedures. Within

some organisations, some members of the service centre staff are flagged as ‘experienced transition managers’, which means they get involved when a new service or organisational unit is being brought into the scope of the centre.

We see a dominance of phased transitions in CEE countries. Organisations avoid a big bang approach as they do not want to take the risk of the process getting out of control. ‘Better safe than sorry’ is a widely used phrase.

“A big bang approach is a recipe for disaster.” Shared service centre manager, Riga

After a preparation and planning period, the implementation usually starts with a pilot in which the knowledge transfer methodology and the service centre on boarding concept is tested.

A handover plan is applied in most cases, in which the work is gradually migrated towards the centre. Some organisations apply a formal sign-off methodology in which business units must complete a checklist before it is allowed to move services towards a service centre; other organisations offer more latitude to the business units. In general, organisations apply a gradual approach in which initially, for example, 50% of the work is performed by the service centre and 50% by the business unit to secure performance and prevent backlog. In most cases, service levels need to be met for a number of consecutive weeks before the service centre personnel is allowed to take over activities completely. This more formalised method requires a lot of effort in preparing the organisation for the transition.Phased transitions are most often organised along the axis of processes, more so than along the lines of business units. This means that for example all accounts receivable activities from various business units/countries are moved into the service centre instead of

on boarding all the in-scope processes from one business unit before moving onto the next business unit. The latter approach has rarely been applied in the organisations we spoke with as part of this study. Hybrid alternatives tend to make things too complicated.

Many organisations wonder what the best practice transition strategy is. In general, organisations design their own organisation specific implementation strategy selecting the best ingredients from the jungle of ‘lift and shift’, ‘move and improve’, ‘shifting with some fixing’.

“Make sure you prove yourself from day one. During the start-up phase commitment, budget and resources are available. After go-live it becomes much harder to acquire this level of support.”Shared service centre manager, Krakow

While some organisations execute transitions using a ‘lift, shift and fix’ approach in which activities are moved ‘as-is’ from the originating location to the service centres, other organisations apply a ‘standardise, fix and shift’ approach in which activities are changed to the ‘to-be’ state before they are moved to the service centre. Some organisations apply both, depending on the maturity of the business unit or country organisation. We have not identified a single best practice in Central and Eastern Europe.

“We have a standard approach to doing a transition, but we always tailor it to fit the context of the organisation from whom the services are being taken over.”Delivery centre manager, Prague

© 2015 KPMG Advisory N.V. © 2015 KPMG Advisory N.V.

The stories behind the numbers 15

THE CHANGE OF KNOWLEDGE TRANSFER METHODOLOGYAlthough there is a need for experienced personnel in more senior positions, most service centres hire new graduates for non-managerial positions. In the past this new inexperienced personnel was trained by means of job shadowing. This type of knowledge transfer methodology means that the bulk of service centre employees sit next to (‘job shadowing’) the personnel of the originating business unit to be trained in the processes to be executed.

“It is crucial to know thebaseline performancelevels, because otherwise it is impossible to accurately compare service centreservice levels and measure improvement.”Shared service centre manager, Riga

After this initial period the service centre employees perform the work, while the former personnel are sitting next to them (‘reverse job shadowing’) to make sure the work is performed correctly. Although this is a well-proven method, it is a rather expensive way of training personnel. Over the last few years, the knowledge transfer methodology has increasingly switched to the cheaper concept of ‘train the trainer’. In this alternative, a limited number of employees, so called subject matter experts (SMEs), are in charge of capturing the current way of working by learning from the originating business units. These SMEs, who require less time to fully

grasp the process, are then appointed to train the new hires of the service centres at the service centre location. This latter approach is currently the preferred option as it is more cost effective and less confrontational towards existing personnel.

The use of experienced resources for a transition is key. Some organisations tend to use the existing talent pool within the organisation, using this type of project as experience programmes. However, these transition projects require specific knowledge and expertise. Involving practitioners who have done it before can prevent time-consuming discussions and bring the necessary authority to the project team. The transition manager therefore should be a person who has overseen a similar transition at least once or twice before. Secondly, the transition manager should be accompanied by an employee who has worked in the existing organisation for at least 10 years. To guarantee the connection with the local recruitment market, it is wise to hire a local HR manager who is familiar with the talent pool and the culture of the targeted workforce.

INCREASING FOCUS ON THE RETAINED ORGANISATIONMore and more organisationsacknowledge the significant impacton an organisation when establishing a service centre, leading to an increased assistance in guiding the retained organisation to the new situation. The broadened scope of change management activities underpin this increasing focus on that part of the organisation transitioning activities to the service centre.

“The energy is automatically driven towards the new setting, with fresh people, new offices and systems. That’s where you immediately see the change!”Shared service centre manager, Warsaw

“Based on our prior experience, we now reserve a budget for supporting the retained organisations as part of a transition initiative. The operations in the respective countries also need training on their new role in a changed operating model.” Organisations that have gone through the transition process a few times strongly recommend managing the expectations of the retained organisation. The correct message has to be spread, openly, honestly, and concretely. he worst thing that canhappen is that rumours startand key personnel decides to leave. We have seen the following practices being applied by the more mature organisations:

• Execute clear and open communication on the initiatives undertaken;

• Ensure early identification of affected staff and clarity on a per employee basis about potential redeployment or redundancy;

• Increase commitment from former personnel to support knowledge transfer using retention bonuses and transition performance bonuses;

• Establish co-ownership of local senior management of the targets to be achieved by the service centre. By doing this, the management of the service centre is not seen as just the ‘bad guys’;

• Gain buy-in from local senior management, activities which are seen as problematic or underperforming in the current situation are tackled first by the service centre transition team;

• Implement improvements (‘quick wins’) are implemented immediately by the service centre in order to convince non-believers;

• Take sufficient time to prepare, take one step at a time. Do not apply short-term fixes, but instead apply a ‘first time right’ methodology.

We believe that the business units /country organisations need to be involved prior to, during and after the transition and that their expectations have to be managed according to the capabilities of the centre. As a

way of providing sufficient attention, one organisation created a support program making sure that investments were available not only for the new service centre but also for the retained organisations. Those parts of the organisation which transitioned activities to the service centre also need to be trained on their new role within a totally different operating model.

“For the business itself the continuity of the services is more important than getting cost advantages.” Shared service centre manager, Bucharest

It is advised to start an implementation with the end in mind, not only for the centre but also for the retained organisation. The organisation needs a vision of where it will stand in five years’ time, not just a vision of the moment of go-live.

14 | The stories behind the numbers

© 2015 KPMG Advisory N.V. © 2015 KPMG Advisory N.V.

The stories behind the numbers 17

STRETCHING THE INTERNAL SPAN OF CONTROL Service centres across Central and Eastern Europe follow a traditional approach to how they are structured internally. The centres apply the usual pyramid organisation structure and a simple management approach. The build-up of staffing levels are alike with the following role structure been applied (from most senior to most junior): shared service manager, functional managers, manager, supervisor, team lead and (junior) agent/clerk. Depending on the process executed, job titles may differ, however the principles applied remain the same.Management staff of the service centres continuously focuses on the span of control being applied to the operational staffing levels. Two perspectives, which contradict each other to some extent, play a role here:

• From a cost perspective, it makes sense to stretch the span of control of Supervisors and Team Leads as much as possible;

• From a talent management perspective, a more reluctant approach to the span of control makes sense as employees demand the opportunity to move up and want to see opportunities. Service centres introduce intermediate levels within their operations to distinguish between less and more experienced operational staff as well as recognising these differences among the staff at hand.

On average, the span of control applied for team leads is somewhere between 1:15 to 1:20, although it has to be said that more extreme ratios have been

recorded. One respondent mentions: “For the more transactional processes we try to push the ratio to 1:30 but this doesn’t always make sense as according to me these teams require more attention as the attrition in these teams are higher than in others”. Team leads still take a part of the work to be executed upon themselves, while for the supervisor role the focus shifts to managing the teams. Naturally, a service centre requires supporting departments such as HR and Finance well. In the course of this research, we record from 5% up to 10% of the total service centre staff as being employed in supporting functions.

“To allow employees to have ample opportunity for growth and to support Supervisors in handling the complexity difference between countries, we had to introduce the Team Lead layer.” Shared service centre manager, Krakow

Despite all these similarities, we recorded differences in how the execution of operational activities is structured, which is represented in Figure 4 (see next page). In the first years of their operation, service centres tend to organise their teams around business units, the geographies being serviced and they execute scoped activities (e.g. finance and procurement operations) within this team structure. Processes have not been standardised yet for all clients of the service centre and the IT landscape is not harmonised. We characterise this as the regional structure.

“It provides us with a straightforward structure, not raising too many staffing question while enabling us to achieve efficiencies.” Shared service centre manager, Sofia

Over time, once a stable state has been achieved and when IT systems and process designs allow, team structures are increasingly formed around the functions and processes being executed. We characterise this as the functional structure. This implies for example that procurement activities for all the service centres’ clients are executed within same team (with sub-teams for meeting the language requirements) to achieve maximum levels of standardisation and efficiency. This structure may therefore be preferred over the regional structure. The majority of the service centres we visited are organised around this principle. As one responded replied;

The most mature centres however go one step further and apply end-to-end ownership; implying that teams are structured around business processes which transcend the functional activities being executed. Examples are purchase-to-pay and order-to-cash processes, which both include activities performed within the finance and procurement functions. Service centres applying this structure strive to achieve the most sophisticated method of process execution. We have not seen many service centres achieving this end-to-end stage. The question to be asked is whether this should be the level which centres should aspire as it requires significant investments and change management effort.

A broad spectrum of subjects can be covered

under the topic of gover-nance as it relates to for

example author it ies, hierarchy, control, service

management and com-pliance. In our conversations,

we focused on how service centres organize them selves

internally, how the service centre is positioned in the overall

organisation and how performance reporting is taking place. There are

strong similarities in how service centres in Central and Eastern Europe

organise themselves internally, but we saw a stronger diversity in the

approach organi sations take to external governance.

16 | The stories behind the numbers

CHAPTER 4EXECUTING GOVERNANCE: SUPPLIER OR PARTNER?

© 2015 KPMG Advisory N.V.© 2015 KPMG Advisory N.V.

18 | The stories behind the numbers The stories behind the numbers 19

THE CHANGING BALANCE IN EXTERNAL GOVERNANCE

Compared to internal governance, our conversations on external governance have been more diverse. It transpires to be a delicate topic as it is much discussed within organisations. These discussions focused on the level of authority of the service centre, the role of the client’s headquarters and the operational freedom of the clients of the service centre. Topics such as decision-making, process ownership and investment decisions are debated.

“It remains a sensitive topic. As service centre we continuously have to fight for our position and continuously convincing headquarters and service clients can be difficult.”Shared service centre manager, Krakow

Although the reporting line from the service centre management to the organisation CFO/COO and the consistent reporting of delivered (quality of) services to the service centre’s clients seem to be constant factors, we have identified certain development stages where service centres are positioned in terms of overall governance. This development is presented in figure 5.

In the situation where a service centre is non-existent (T0), the client’s headquarters and the respective business units (in this context the sphere represents the clients of the service centre, which also can be the country organisations) are operating in a equilibrium. This equilibrium is affected when the decision is made that the client shall make use of a service centre for central delivery of certain services. In this stage (T1), the role of the business seems to decline and the attention moves to the creation of the service centre, which is sponsored by the client’s headquarters. The focus is on the creation of the service centre, transferring services from the business units into the Service centre and creating a new stable environment. Process ownership for the services being executed in the centre is allocated to the service centre

Figure 4 / Governance structure

management and the headquarters show a high level of interest in how the service centre is operating. The service centre management reports to the COO/CFO. Over time, a change occurs in this balance. Multiple service centre managers confirm that after this first implementation stage, a more balanced relationship between the business units and the service centre develops. After a period of relative disconnect, the business unit demands a bigger say in how processes (and which activities within those processes) are executed and the service centre focuses on tprocess improvement based on feedback from the client (T2). The role of the headquarters is less present as the hurdles of the implementation have been overcome and a more stable situation has been realised. As one service centre manager indicated:

“We had to give our clients a bigger say again. Now they can even determine whether we should use more resources in our centre to improve quality for example. This is only to a certain extent of course, but in essence we have become more an extension of their operations whereas in the beginning we acted too much as two different entities.” Service centre manager, Riga

When service centres reach the stage of maturity where they are used as a strategic vehicle to optimise business performance; and the scope of activities being executed in the service centre increases; the role of the client’s headquarters increases again (T3). Some of the organisations with whom we spoke have installed global process owners at headquarters’ level; a single person who is responsible and accountable for the consistent design and deployment of a given process as well as the standard for process performance. As the scope of the service centre increases, the relevant importance and risk profile of the service centre also increase significantly. The global process ownership model is installed to improve compliance with, and performance of, the business process. Global process owners determine

which processes and activities are executed in the service centre and which processes and activities remain within the business functions. They advocate standardisation, improvement, and professionalization. They increase the equilibrium in the business unit, client headquarters and shared service centre triangle. As one service centre manager said:

“The installation of the process owners have both helped us as our clients. They streamline the discussions we have with our clients on responsibility issues and scoping elements.” Delivery centre manager, Warsaw

NL

BE

LX

NL

BE

LX

NL

BE

LX

NL

BE

LX

NL

BE

LX

NL

BE

LX

NL

BE

LX

IT

SP

PO

IT

SP

PO

E.g. South of Europe Finance

Proc.

Proc.

Proc.

Proc.

Proc.

Proc.

Fin.

Fin.

Fin.

Fin.

Fin.

Fin.

E.g. Benelux Procurement Eg Procedure to Pay

Regional Functional End to End

IT

SP

PO

Figure 5 / The governance triangle

T = 0 T = 1 T = 2 T = 3

BU

HQ HQHQ

HQ

BUBU BUService centre

Service centre

Service centre

© 2015 KPMG Advisory N.V. © 2015 KPMG Advisory N.V.

20 | The stories behind the numbers

FROM SERVICING TO PARTNERING

All the service centre organisations with whom we spoke in the course of our research have invested heavily in service level management and key performance indicator measurement. Performance reporting is not only used to communicate performance to external stakeholders but is also applied internally in the service centre, up to and including being used to judge the performance of individual employees. Although this was to be expected, it remains impressive to see what service centres are able to achieve at the level of performance improvement.

“Although cost-saving objectives were the primary objective for us in creating this Service centre, the level of transparency we have created in business performance may be of equal value. We have taken a quantum leap

forward in how we execute the activities under our influence compared to the situation where there was no service centre operating in our organisation...” Shared service centre manager, Bucharest

Service centres formally agree on the services to be delivered and the quality thereof (and in some instances the financial settlement thereof as well) with their clients which in most instances is confirmed via a service level agreement (SLA). The quality of the services and the most important issues arising are discussed in frequent performance meetings. It has become common practice now that a service centre client is assigned a single point of contact for all the services being delivered by the service centre, as clients do not want to speak with different managers for each different service. As the relationship develops and the service centre becomes more accepted by the organisation, the focus of performance management

changes. Whereas at the beginning of the relationship, clients are critical and sceptical about the performance of service centre, once the it has proven its value, the clients tend to make more use of the service centre’s critical and analytical capabilities where they can improve the client’s own processes and add value. Figure 6 represents this development.

“We don’t speak of service level agreements, we apply partnership agreements. We want to focus on the overall business performance.” Shared service centre manager Krakow

Where in the beginning clients are mainly interested in the performance of the service centre and its employees, over time they tend to become more interested in the overall execution of the processes, which may include activities executed by the client itself. In the end, it is the overall performance that matters.

Figure 6 / From service level management to performance measurement

CHAPTER 5MANAGING TALENT: ENSURING A STABLE WORKFORCE

Service Centre Activity Service Centre Activity Service Centre Activity Client activity Service Centre Activity

Receive & Scan Invoice

Process Invoice

IdentifyDiscrepancy

ResolveDiscrepancy

IssuePayment

Performance Measure

Service Centre Service Level

ClientObligation

Service Centre Service Level

The stories behind the numbers 21

Talent management is seen as a core com petence in

operating a succesful service centre. Stability in the workforce is extremely important

for optimal performance. What is impor tant to realise is that the

young and ambitious workforce in the service centre industry in the

CEE region require a specific management approach and expect

more from than work environment than providing a salary alone.

© 2015 KPMG Advisory N.V. © 2015 KPMG Advisory N.V.

22 | The stories behind the numbers The stories behind the numbers 23

UNDERSTANDING YOUR WORKFORCE

Effective talent management is not a straightforward thing, or as one service centre manager put it, “Asking how to do talent management well is like asking someone to describe the colour blue”. One of the factors to realise is that approximately 90% of employees in the shared services and outsourcing industry in Central and Eastern Europe are under 30 and that 65% is female. These characteristics require organisations to adopt and create specific HR strategies that differ from the overall company HR strategy. As one service centre manager explaines, “In the beginning we as a management team came to work in our usual business suits with our nice ties, but as we found out, this created a certain distance between us and the employees which was not helpful to us. This generation does not respond to hierarchy and seniority. They respond to examples and persons from which they can learn. They do not simply follow; they question things to a certain extent and want to have a discussion with you. This is sometimes difficult and time-consuming, but is required if you want to improve things. We threw away our ties and after four to six weeks it was difficult to find suits in our centre”.

As well as the above, our conversations teach us that the following characteristics are also key to understanding the shared services and outsourcing workforce in the CEE region: • “They get bored fast” – Employees

want to move forward quickly and expect to do more things at the same time. They have ambitions. Organisations need to prepare for employees’ two-year ‘itch’, meaning that every two years employees want to do something new and different either by promotion or rotation;

• “They learn fast” – Generation Y picks things up fast. They are able to learn new activities quickly and are able to adjust to new situations swiftly. Their capabilities during transition programmes should certainly not be underestimated;

• “Money isn’t everything” – Generation Y expects more than just a job and financial compensation from employers. Employees want to be part of something, want to have a community feeling, and expect to be given the opportunity to contribute positively to society.

RECRUITING THE RIGHT TALENT IS NOT EASY, BUT KEEPING THEM ON BOARD IS THE REAL CHALLENGE

One aspect of talent management is getting this young workforce in. In the conversations we conducted, it was confirmed that recruiting new talent is an ongoing activity. Based on our research, we conclude that service centres are running with a continuous vacancy rate ranging between 3% and 10%. Service centres usually establish a strong connection with local universities to tap into the young workforce and make sure the curriculum is aligned with the desired competences. Alternatively, organisations utilise their own international network to attract young professionals through internal rotation. Service centres typically tend to make use of recruitment agencies when a combination of a minority or less common language and specialised skillsets is needed or in a situation where a significant ramp-up in employee numbers is required (e.g. seasonal peaks).

“We are continuously in touch with the talent market and, to do so, you need to have an excellent HR manager.” Delivery centre manager, Krakow

The biggest challenge in employee recruitment is finding employees with the right combination of language capabilities and the right professional skills. The centres we visited support eight to ten languages on average, with

one delivery centre even supporting 38 languages, but keeping required language support up to standard can be a struggle and organisations do have to invest heavily in it. Employees who speak more than two languages often receive a bonus on top of their base salary. This bonus increases when it is more challenging to find speakers of the language, for example Arabic. One organisation even offered three months of full-time language courses to its employees to safeguard their language capabilities.

Once in, talent management is about retaining those employees who are difficult to replace. In general, these are the middle management and senior management functions and those employees with rarer language capabilities. Replacing these employees is costly and can take a lot of time and there are numerous centres eager to compete for and acquire their talents. The majority of service centres in the CEE region demonstrate double-digit attrition rates. Such a competitive environment makes the job of HR directors and managers more difficult.

“We do not only ask why employees leave, but also why they stay.”Delivery centre manager, Krakow

As previously stated, generation Y gets bored fast, learns fast and is not solely focused on monetary compensation. Service centres need to consider these factors as part of their retention programmes. Our service centre managers therefore mostly emphasised the importance of providing sufficient career opportunities, challenging work and facilitating social activities (e.g. voice of the employee programs,

community-building events, charity events and wellbeing programs) and service centres invest heavily in these types of employee conditions. Providing the right contractual terms, conditions and fringe benefits is often just a hygiene factor. Another key to retaining talent is continuously proving to employees that growth opportunities do exist. This can be challenging as not all employees can actually be offered such a next step. One organisation even has adjusted its role structure and introduced two additional hierarchy levels for operational employees, simply to create more growth opportunities. Another organisation has pictures hanging on the wall of past employees who had successful careers, both inside and outside the organisation. One service centre manager responds; “It is my personal objective that my replacement will be an employee who comes from this region and has worked for us for several years. It would be a good statement if we were able to achieve this.”

“Employees have to be convinced that at a certain moment they can take the next step. You need to offer career paths or else be prepared to let them go.”Shared service centre manager, Budapest

MANAGING A HEALTHY ATTRITION RATE

Attrition rates are an important performance indicator for captive shared service centres and the delivery centres managed by service providers. It is an

important topic in the shared services and outsourcing industry. Although the figures were not always shared with us, we are able to establish from the figures received that the attrition rates of the centres included in our research ran between 10% and 25%.

It is important to realise that attrition is not necessarily a bad thing. Attrition is simply part of the shared services and outsourcing industry and a method used to manage the cost base. Too low attrition rates eventually affect the cost effectiveness of a centre. Attrition rates between 10% and 20% are what organisations should aim for.

“I start to get worried when our attrition rates fall below 10%. It means that I have too many employees who have been here for quite a while, which is more expensive.”Shared service centre manager, Budcharest

One important method for managing attrition is to have a succession plan in place. In this sense, succession planning is similar to having a disaster recovery plan. We advise having a back-up plan in place for at least 75% of the key positions (middle management, resources with specific language capabilities) within a service centre; the ‘75% ready now target’. This can be challenging, but it is important to ensure stable delivery and quality of services.

© 2015 KPMG Advisory N.V. © 2015 KPMG Advisory N.V.

The stories behind the numbers 25

CHAPTER 6DRIVING EVOLUTION: AVOIDING A STEADY STATE

MAXIMISING CONTINUOUS IMPROVEMENTService centres are constantly challenged by (internal) customers, business owners and other stakeholders to improve quality and lower operational costs. Continuous improvement is therefore a fundamental principle that requires to be anchored in the organisational structure and culture. Our service centre managers acknowledge this and emphasise they actively invest in process improvement to meet client expectations.

“Innovation, innovation and more innovation.” Delivery centre manager Budapest

Service centres adopt the Lean Six Sigma methodology as strategy to continuously improve performance. We came across impressive examples. For example, one service centre has trained over 1.000 of their resources in Lean and Innovation principles. To support these resources, a Performance Excellence Team of 30 experience Black Belt practitioners

is installed. Multiple simultaneous Improvement Project Teams consisting out of trained operational personnel mentored in Lean Six Sigma are constantly identifying and implementing (process) improvements. Continuous improvement is simply part of their responsibility and a track record on this aspect is essential for moving up. As the service centre manager mentioned: “Improving execution is where we can deliver the added value to our clients. It’s our ticket to success. We are simply better in it than our clients. We have been able to achieve approximately 10 to 13% efficiency improvement per year and as reward, the clients gave us the responsibility to adopt more complex processes in our portfolio which is good for employee motivation”.

From our conversations we conclude that continuous improvement are addressed from two different angles:

1. Inside the centre: This focus is currently still formal agreements as SLAs (see chapter 4 “Executing Governance”) As said, Lean Six Sigma is the most dominant methodology applied to accomplish this.

“Driving a Lean Six Sigma program does not only benefit the performance, but also the development and ambitions of our high-potential staff.” Shared service centre manager Bucharest

2. Outside the centre: When service centre’s become more mature, the focus of improvement management shifts from internally focussed towards being more externally focused. Organisations realise that continuous improvement does not affect only the service centre, but also those delivering input for and receiving the services. In other words, the clients of the service centre. To really harvest the potential value of a service centre, clients also have to adopt a different attitude and change their way of working . More and more clients expect service centres to be in the driver’s seat in improving process execution from a overall perspective. This creates inroads for end-to-end process ownership across organisational units.

“Right now, we drive a company wide improvement project named “Bureaucracy Buster.”” Shared service centre manager Warsaw

Driving evolution is essential to remain competitive. All

service centre managers we spoke to are constantly seeking

ways to increase performance and expand the scope, either in

the type of processes executed or the client base to which services are

delivered. Additionally, centres need to match the expected performance

improvements for each specific process year-on-year.

24 | The stories behind the numbers

© 2015 KPMG Advisory N.V. © 2015 KPMG Advisory N.V.

26 | The stories behind the numbers The stories behind the numbers 27

One remarkable point, when speaking about driving improvement, is that our service centre managers often mentioned the existing IT environment as a limiting factor in achieving the full improvement potential. Continuous improvement inevitably is linked directly to IT and automation. Having to work with multiple systems and applications in combination with limited standardisation has a negative impact on process optimisation and workforce scalability. Rationalizing the IT landscape is high on the wish list of many service centre managers.

“We could achieve double-digit efficiency improvement in the centre if our IT environment was rationalised.”Shared service centre manager, Warsaw

Although it was acknowledged by centres that they do not have full control over the IT landscape of their clients, and therefore are limited therefore in really driving the IT innovation agenda, we did see a number of interesting initiatives in IT innovation. More mature service centres indicate they spend more than 20% of their budget on IT innovation. The following interesting examples were mentioned in our conversations:

• Digital service offering – one service centre ambitions to execute up to 80% of their service offering via intranet/workflow and thereby limiting the capacity required;

• Use of robotics – we have seen examples of service centres (predominantly external service providers) testing the use of robots

which can replace operational staff (ratios of 1 robot replacing 7 FTE have been mentioned);

• Data analytics – a number of service centres where standardizing their database with aligned formats and forms with highly-integrated external data components. Use of highly advanced data analysis and visualisation is coming to the surface more and more;

• Dynamic reporting – service centres are adopting predictive modelling which provides service centre staff with prescriptive analysis of real-time data from internal and external sources that informs future direction.

EXPANDING THE SCOPE; GOING MULTIFUNCTIONAL AND MOVING UP THE VALUE CHAIN

One conclusion which is apparent from our research: gone are the days when single-function homogeneous towers dictated the service centre landscape. The majority of the service centres we visited supported multiple functions for their clients (see Figure 7). As one service centre manager mentioned:

“We have been able to prove to our organisation we can deliver, we can improve and we can integrate. The decision to expand our scope is a direct result of that and I see it as our biggest accomplishment.”Shared service centre manager, Krakow

Two kinds of expansion are clearly present in the market:

1. The integration of multiple functions in the service centre offering – we see organisations broadening the scope of the services they offer to include Finance and Accounting, Human Resources, IT, Procurement and more;

2. The move towards more value adding, expertise-driven processes in the value chain – more complex knowledge base processes such as Controlling, Data Analytics and Strategic Sourcing are becoming part of the service centre offering.

“The moment we as Service Centre do not expand functionally or numerically, we are destined to fail.” Shared service centre manager Sofia

Usually a service centre starts with execution of the usual suspects in the organisation’s supporting functions, being (parts of) Finance, HR, IT and Procurement. When the service centre has proven its value, organisations are willing to transfer more non-traditional functions to these centres, including for example:

• Customer Contact • Sales Support• Order Management;• Supply Chain;• Risk and Security;• Marketing;• Industry-specific processes.

In our research, we have seen examples of service centres executing sales support activities (e.g. tracking orders, follow up calls with customers etc.) from the Central and Easter European region for the complete business geography of the organisation, which included the US and Asia. These team have operate in shifts on a 24-hour basis to support different time zones. As one service centre manager strikingly explained:

“Our value is not sought exclusively in cost efficiency anymore, but increasingly in transparency. By executing these processes for the entire organisation from one place under one responsibility results in better insights and information.” Shared service centre manager, Riga

Service centre managers see a change in the way in which centres operate, the service portfolio they offer and the potential added value for their clients. Existing language capabilities and skillsets within service centres are used more extensively and new skills are developed to ensure their success in a competitive market.

Multifunctional

Single function

64%

36%

Figure 7 / Service centre offering

© 2015 KPMG Advisory N.V. © 2015 KPMG Advisory N.V.

28 | The stories behind the numbers The stories behind the numbers 29

The scope is not only changing by going multifunctional, the increased focus on moving up the value chain and adopting more value-adding services is also clearly on the service centre agenda. This applies to all functions, whether it is Finance (Finance reporting, Budgetting), Human Resources (Recruitment support, Expat support) or Procurement (Strategic Sourcing services). By including these kind of activities, service centre get more control and oversight over the complete process which enable additional opportunities for improvement.

Figure 8 represents a concrete example of how the scope of a service centre expended at one of the companies we spoke to. Business support processes have been classified on two axis; the level of potential standardization and the required customer contact. The organisation started with the lower left side of the graphic moving towards

upper right half. As the service centre manager explained; “For us it seems more natural to achieve growth by adding additional processes per stream. A stream is usually started with a base of relatively simple classic transactional back office activities to prevent business interruption. The next step usually is to add more complex activities which are more judgement incentive and require another skill level. We have a dedicated project team to ensure growth by stream over all the countries. Although we had a clear path for development, convincing our organisation of this path is a continuous task”.

“We actively use our strong internal brand to incorporate new services in our portfolio.”Shared service centre manager, Riga

“We see great value in adopting new services as we broaden our staff-development opportunities. Eagerness can be rewarded.” Shared service centre manager Krakow

A related benefit of the move towards value-adding activities support by nearly all service centre managers is that the HR agenda is supported. Employees active in the service centre sector differ from employees active in other sectors such as manufacturing or retail. They are younger, more ambitious and work in a fast-growing sector. This creates many opportunities for them, but also results in many challenges for the centres. By organising more and more value-adding services, service centres can offer employees more development opportunities and thereby reduce attrition, but also attain economies of scale.

HYBRID MODELS ARE BECOMING THE STANDARD

An upcoming trend in the Central and Eastern European region is the fact service centres themselves are taking a critical view on their service delivery approach. As service centres are growing in the services they execute and are moving up the value chain, they now have sufficient scale to start outsourcing certain services to a professional Service Provider. 0 10 20 30 40 50 60 70 80

65%

61%

35%

34%

20%

17%

12%

9%

7%

6%

F&A

IT

HR

Procurement / source to pay

All areas, including IT

Supply chain

Customer care

REFM

All business functions

Vertical industry specificbus. functions

Figure 8 / functions executed in service centre in Central and Eastern Europe

Figure 9 / Example; Increasing the scope of the service centre

Cu

sto

mer

co

nta

ct

Standardisation High Medium

Day to day transactions with customers Order management

Sales Ops

Tax compliance

Tax

Routine processes and helpdesk, Functional Application Management

IT ‘Run’

Routine, repetitive, back office

services

Analytic support Data Management

Marketing

Administrative support and planning

Supply chain

Purchase order Processing Contract admin Content Mngt Catalogue Mngt Category analysis

Procurement

Cash Mngt Payment processing

Treasury

Structured data services MDM, BI Unstructured data services Predicative analytics e.g. marketing, S&OP social media support

Business decision support service

Accounts payable Accounts receivable General ledger Fixed assets External reporting T&E processing Cost accounting

Accounting

Payroll processing Payroll/Bens admin

HR

Knowledge management

Document management

Expat/relocation Admin Recruit staff L&D materials Helpdesks

HR

Insurance admin Financial reporting Mngt reporting Month end closing Budgeting Consolidation Profitability analysis Internal controls Capex analysis Working capital mngt Business cases support Commercial asset effectiveness

Finance

Strategic buying Specialist support Contract Management

Procurement

Document mngt Expertise Services

Legal

Administrative support

Tax

Expertise/ consultative ‘high

touch’ services

We foresee the route across CEE that hybrid models shall become the norm whereby organisations balance the usage of their delivery channels. Finding the right combination of delivery models between captive near-shore, captive offshore and outsourced shall be the challenge for the upcoming years.

As such, Central and Eastern Europe is increasingly used as a location to crystallize processes so that they can be sourced to more cost effective locations as India or the Philippines. Less complex transactional processes are replaced by more complex processes. As one responded indicated;

“Tell me, why should we organise the non-client facing processes in CEE if that piece of work can be done cheaper offshore. We are not creating value by doing that in Europe.” Shared service centre manager, Krakow

A fast majority of the organisations opt for a combination of outsourcing transactional processes to a professional Services Provider while retaining more complex value-adding services in Central and Eastern Europe. Outsourcing is perceived as bringing

additional advantages as further reductions of cost and increased risk mitigation. Risks are expected to be mitigated, because not all activities will be performed at one location and the organisation can steer upon expected results while operational risk is allocated to a Service Provider. One international investment bank, for example, has sourced the more complex valuation processes in a service centre in Eastern Europe, while the less complex transactional processes are sourced in a captive centre India. Another international beverages company uses a service centre in Eastern Europe as its primary contact point for its organisation, but has contracted a

© 2015 KPMG Advisory N.V. © 2015 KPMG Advisory N.V.

The stories behind the numbers 31

CHAPTER 7FUTURE OUTLOOKA REGIONTO STAY

The five service centre management themes outlined are likely to remain dominant agenda items in the coming years. We expect Talent management, Governance and Evolution to keepdemanding management focus as these factors enables management to position the centre in a unique way both within the client organisation itself as well as in relation to other centres. This is what makes the difference in the services provided and value added and makes a centre stand out from the crowd.

“Even if robotics are kicking in seriously, talent management remains a top 3 item for my management team’ Shared service centre manager Budapest

To further sharpen the view of the way ahead, we conclude this research with three items.

A REGION TO STAY!Our journey across Central and Eastern Europe has shown energy across centre management, investment and recruitment agencies and our Central and Eastern Europe colleagues. The state of the service market is attractive in many ways. The numbers simply add up and our conversations with various people – managers, clients, recruitment agencies and investment offices – have convinced us that this market has a lot of potential to become a sustainable contributor to the regional economy. We expect that the service centre market in this region will continue to grow by at least 10 % per year for the next five years. This is based on a number of strong ingredients:

• Availability of talent and languages for value-adding services;

• Accessibility and infrastructure;• Alignment with European culture;• Flexibility in locations.

In addition to the locations we investigated, new countries are getting into the industry as well. Serbia and Estonia are just examples of destinations that could become important players in the coming years.

THE EVOLUTION OF GLOBAL BUSINESS SERVICES Even though it does not dominate the current service centre agenda in CEE, it is likely that global business services (GBS) – the integration of organisations’ end-to-end processes across service delivery models for both back and front offices – will become the new standard in the next five years. This new phenomenon focuses on optimising the combination of human capital, service delivery models, process innovation and technology to deliver various type of services (e.g. HR, finance and accounting, supply chain

management, IT) on an enterprise-wide, cross-functional basis, to support the business strategy. As a logical continuation from the hybrid models we saw in the course of this exercise, global business services is the perfect integrated platform to deliver enterprise business services and thereby drive efficiency and business outcomes and evolve with the market and company needs.

“Global Business Services seems to be somewhere around the corner, not sure when it will hit us though.”Shared service centre manager Krakow

The key capabilities of GBS are:

• Multi-functional business processes (including operations);

• Shared information technology;• Multi-channel service delivery

– outsourced, shared services and centres of excellence;

• Process ownership and management;• Enterprise-wide governance.

Continuous improvement is essential to remain competitive.

The service industry is constantly seeking ways to improve and

grow, either in the scope of the processes executed or the client base

to which services are delivered. Additionally centres need to match the

expected performance improvements for each specific process year-on-year.

30 | The stories behind the numbers

© 2015 KPMG Advisory N.V. © 2015 KPMG Advisory N.V.

32 | The stories behind the numbers The stories behind the numbers 33

Even though organisations will cherry-pick from the listed key capabilities, we believe that centres will drive the further integration and alignment of business support processes, including value-adding services.

GREATER ROLE OF DISRUPTIVE TECHNOLOGY

Remarkably, disruptive technological changes are not dominating the service centre strategy while all major service providers currently investing in this new technology. The understanding and implementation of for example robotic process automation (RPA) has moved on very significantly the

last year. This technology enables non-engineers to automate certain business processes quickly and cheaply. In a couple of months RPA has moved from the margins of the BPO market place to a central component of the strategy and delivery plans of every major service provider. RPA strategies are now in place or under development across the service provider landscape where in 2013 they didn’t exist and now are beyond the proof of concept or pilot stage.

Although the potential influence of robotics or cognitive platforms does not seem to be on the agenda (see also our comments and findings regarding IT and innovation) we believe

that it is just a matter of time before the entire landscape of the service centre industry is dramatically altered by the use of disruptive technology. Effecting the type of work, necessary skills, processes, roles and most important strategic decisions regarding the future of the service centre.

Level 05

Level 04

Level 03

Level 02

Level 01

SUB-OPTIMIZEDDecentralized andduplicative functions ;little central controlover business supportservices

RATIONALIZEDSingle function sharedservices with tacticalonshore or offshoreprovider relationships

OPTIMIZEDTraditional outsourcingrelationships with globaldelivery; non-integratedinternal shared servicescapabilities

STRATEGICOptimized balance ofinternal and externaldelivery capabilities,global sourcing withmultifunction focus

INTEGRATEDGlobally integratedservices portfolio withaggressive use ofalternative and mixeddelivery models

The maturity model of global business services provides the following details:

Figure 10 / Maturity model of global business services

© 2015 KPMG Advisory N.V. © 2015 KPMG Advisory N.V.

34 | The stories behind the numbers The stories behind the numbers 35

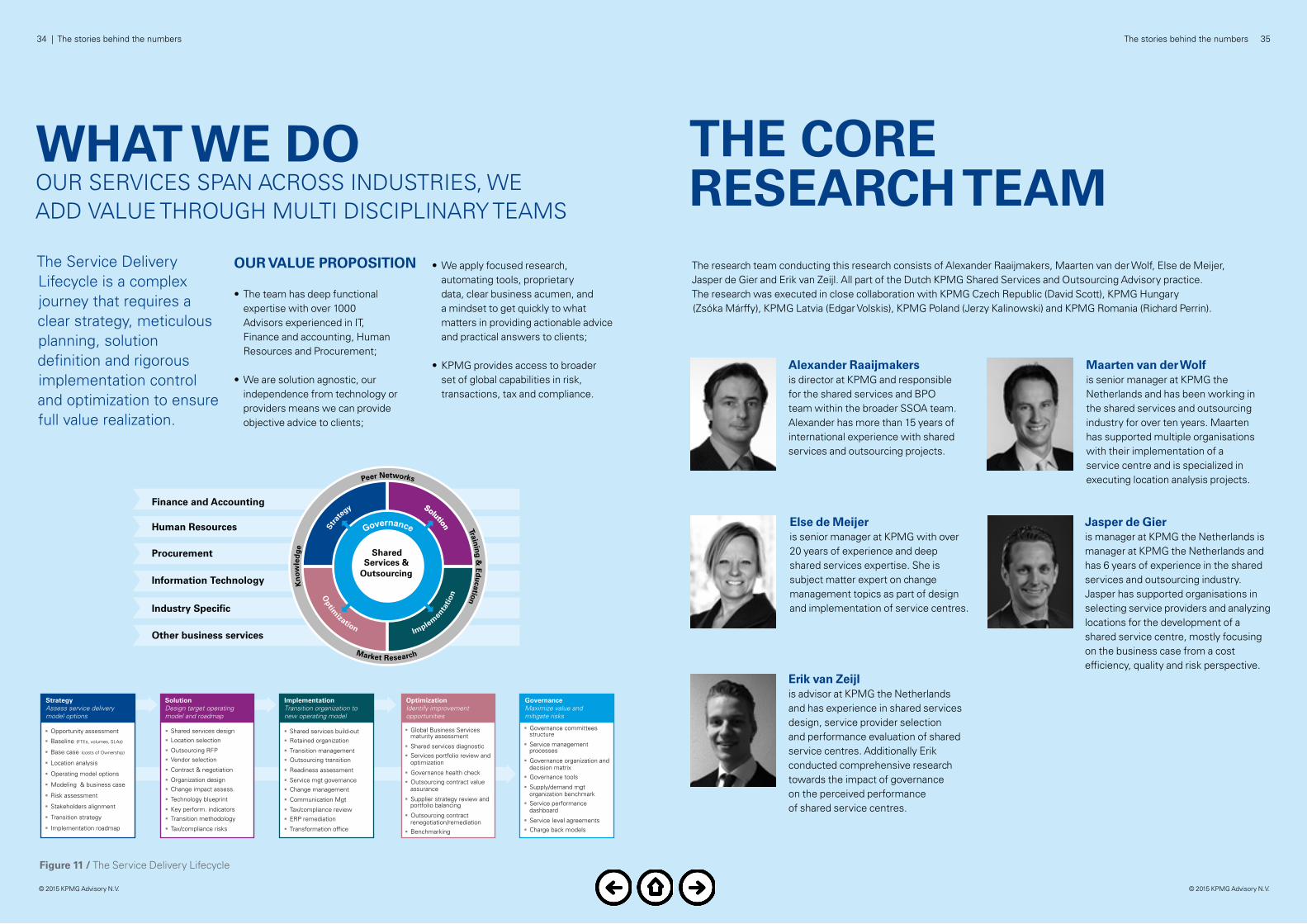

OUR VALUE PROPOSITION

• The team has deep functional expertise with over 1000 Advisors experienced in IT, Finance and accounting, Human Resources and Procurement;

• We are solution agnostic, our independence from technology or providers means we can provide objective advice to clients;

• We apply focused research, automating tools, proprietary data, clear business acumen, and a mindset to get quickly to what matters in providing actionable advice and practical answers to clients;

• KPMG provides access to broader set of global capabilities in risk, transactions, tax and compliance.

The Service Delivery Lifecycle is a complex journey that requires a clear strategy, meticulous planning, solution definition and rigorous implementation control and optimization to ensure full value realization.

Opportunity assessment

Baseline (FTEs, volumes, SLAs)

Base case (costs of Ownership)

Location analysis

Operating model options

Modeling & business case

Risk assessment

Stakeholders alignment

Transition strategy

Implementation roadmap

Shared services design Location selection

Outsourcing RFP Vendor selection

Contract & negotiation

Organization design Change impact assess.

Technology blueprint

Key perform. indicators Transition methodology

Tax/compliance risks

Shared services build-out Retained organization

Transition management Outsourcing transition

Readiness assessment

Service mgt governance Change management

Communication Mgt

Tax/compliance review ERP remediation

Transformation office

Global Business Services maturity assessment

Shared services diagnostic Services portfolio review and optimization

Governance health check Outsourcing contract value assurance

Supplier strategy review and portfolio balancing

Outsourcing contract renegotiation/remediation Benchmarking

Governance committees structure

Service management processes

Governance organization and decision matrix Governance tools

Supply/demand mgt organization benchmark Service performance dashboard

Service level agreements Charge back models

Peer Networks

Solution

SolutionStra

tegy

Implem

enta

tionO

ptim

ization

Market Research

Training &

Ed

ucation

Kn

owle

dge

Finance and Accounting

Human Resources

Procurement

Other business services

Information Technology

Industry Specific

Shared Services &

Outsourcing

StrategyAssess service delivery model options

SolutionDesign target operating model and roadmap

ImplementationTransition organization to new operating model

OptimizationIdentify improvement opportunities

GovernanceMaximize value and mitigate risks

Figure 11 / The Service Delivery Lifecycle

WHAT WE DO OUR SERVICES SPAN ACROSS INDUSTRIES, WE ADD VALUE THROUGH MULTI DISCIPLINARY TEAMS

THE CORERESEARCH TEAM

Alexander Raaijmakers is director at KPMG and responsible for the shared services and BPO team within the broader SSOA team. Alexander has more than 15 years of international experience with shared services and outsourcing projects.

Erik van Zeijlis advisor at KPMG the Netherlands and has experience in shared services design, service provider selection and performance evaluation of shared service centres. Additionally Erik conducted comprehensive research towards the impact of governance on the perceived performance of shared service centres.

Jasper de Gier is manager at KPMG the Netherlands is manager at KPMG the Netherlands and has 6 years of experience in the shared services and outsourcing industry. Jasper has supported organisations in selecting service providers and analyzing locations for the development of a shared service centre, mostly focusing on the business case from a cost efficiency, quality and risk perspective.

Else de Meijer is senior manager at KPMG with over 20 years of experience and deep shared services expertise. She is subject matter expert on change management topics as part of design and implementation of service centres.

Maarten van der Wolf is senior manager at KPMG theNetherlands and has been working in the shared services and outsourcing industry for over ten years. Maarten has supported multiple organisations with their implementation of a service centre and is specialized in executing location analysis projects.

The research team conducting this research consists of Alexander Raaijmakers, Maarten van der Wolf, Else de Meijer, Jasper de Gier and Erik van Zeijl. All part of the Dutch KPMG Shared Services and Outsourcing Advisory practice. The research was executed in close collaboration with KPMG Czech Republic (David Scott), KPMG Hungary (Zsóka Márffy), KPMG Latvia (Edgar Volskis), KPMG Poland (Jerzy Kalinowski) and KPMG Romania (Richard Perrin).

© 2015 KPMG Advisory N.V. © 2015 KPMG Advisory N.V.

© 2015 KPMG Advisory N.V., registered with the trade register in the Netherlands under number 33263682, is a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved. The name KPMG, logo and ‘cutting through complexity’ are registered trademarks of KPMG International.