19

1 Deep dive into the Asian market Sylvie Cornot-Gandolphe Paris, 14 December 2016 THE THIRD IEA-IEF-OPEC SYMPOSIUM ON GAS AND COAL MARKET OUTLOOKS

1

Deep dive into the Asian market Sylvie Cornot-Gandolphe Paris, 14 December 2016

THE THIRD IEA-IEF-OPEC SYMPOSIUM ON

GAS AND COAL MARKET OUTLOOKS

2

Key Coal Market Trends in Asia

3

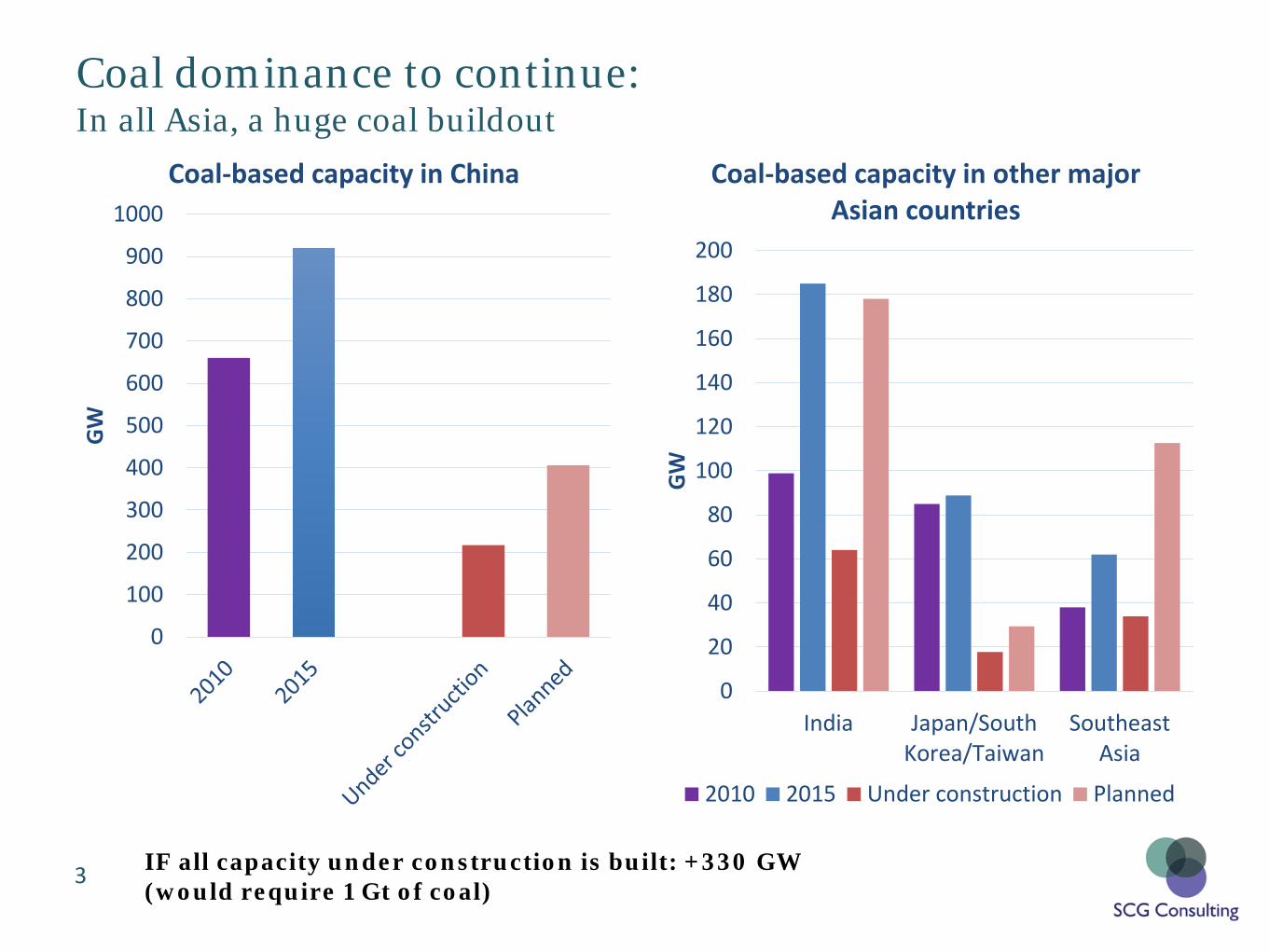

Coal dominance to continue: In all Asia, a huge coal buildout

0

100

200

300

400

500

600

700

800

900

1000

GW

Coal-based capacity in China

0

20

40

60

80

100

120

140

160

180

200

India Japan/SouthKorea/Taiwan

SoutheastAsia

GW

Coal-based capacity in other major Asian countries

2010 2015 Under construction Planned

IF all capacity under construction is built: +330 GW (would require 1 Gt of coal)

4

Coal Consumption and Production Trends in China

Beg of 2016: Coal supply reforms Moratorium on new coal mines Closing of small coal mines In April 2016, reduction of operating days in coal mines from 330 to 276 days

3.3

3.6

4.0 4.1 4.2 4.1 3.9

3.6

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

Gt

Coal consumption

The new “normal” Fight against air pollution Renewables/Hydro development

Apparent consumption

3.2 3.4

3.8 3.8 3.9 3.8 3.7

3.4

0

0.5

1

1.5

2

2.5

3

3.5

4

4.5

Gt

Coal production

5

China is the price setter for international steam coal

-500

50100150200250300350

Mt

ImportsExportsNet imports

Coal imports account for only 5% of Chinese supplies…but 16% to 20% of global steam coal imports Chinese imports are driven by price arbitrage Regulation on coal imports (2014/2015) The government wants ‘reasonable’ coal prices The increase in coal imports/coal prices may be short-lived But coal prices are not expected to return to the low levels of beg. 2016

40

50

60

70

80

90

100

110

120

130

140

$/t

Australia FOB price

Futures (as of 8 Dec. 2016)

6

China’s 13th Energy Plan (2016-2020)

• Energy demand is capped

• Share of coal: 58% by 2020 (reduction is steeper than previously planned)

• Energy intensity: -15%

• Carbon intensity: -18%

• Coal share in power capacity to decrease to 55% (making room for renewables)

• Coal-based additions: 180 GW over the planning period (compared to 300 GW in the 12th FYP)

• Current low utilization rates of coal-fired power plants (less than 50%)

• Rationalization of the power fleet (“new” coal to displace old inefficient coal early retirement) and delays/cancellations

• China has just cancelled 17 GW of under construction capacity

64

58

12 15

0

10

20

30

40

50

60

70

2015 2020

%

Coal in the energy mix

Share of coal Share of non-fossil fuels

7

Coal Consumption and Production trends in India

Coal production on the rise again (even if less than planned)

FY2016: Total coal demand much lower than planned (830 Mt vs. 910 Mt)

0

100

200

300

400

500

600

700

800

900

Mt

Hard coal production

CIL SCCL Others

0

100

200

300

400

500

600

700

800

900

Mt

Hard coal consumption

Power sector Steel Cement Others

8

The government intends to stop steam coal imports by end 2017

• Major reforms in the coal sector to boost efficiency of Coal India Ltd, and introduce competition and transparency in the sector

• New Mining Law opens the sector to private operators

• Government targets: Coal India Ltd to double its

production by 2020 to 1,000 Mt

(but was relaxed recently)

Private and other producers: 500 Mt by 2020

Domestic coal production to continue rising, certainly not as steeply as planned

494 536.5

599 661

774

908

0

100

200

300

400

500

600

700

800

900

1000

Mt

Coal India Ltd planned production

9

Indian coal imports

Imports projected to decrease to 160 Mt in FY2017…(unlikely)

• Domestic or imported coal? • Major efforts to increase domestic coal

production AND strong political willingness to be independent (for steam coal)

• But still many hurdles (land acquisition, transportation bottlenecks, green clearance, poor quality of coal)

• Coal power plants built to burn imported coal

• Environmental regulation (limit on transport of coal with high-ash content)

• Prices of domestic vs. International coal • There are still some room for regulation

to decrease steam coal imports… • And coal demand not expected to rise as

steeply as planned (‘over-building’ in the coal power sector and low utilization factor)

0%

5%

10%

15%

20%

25%

30%

0

50

100

150

200

250

Mt

Coal imports

Coking coal

Steam coal

Import dependence (RHS)

10

Other importing markets

0

50

100

150

200

250

300

350

Mt

Japan/South Korea/Taiwan - Steam coal imports

Japan South Korea Taiwan

0

20

40

60

80

100

120

140

160

2000

2005

2010

2011

2012

2013

2014

2015

2016

2020

Low

2020

Hig

h

Mt

Southeast Asia - Steam coal imports

Thailand Viet Nam Philippines

Malaysia Others

Increase in coal imports secured by the building of 25 GW of new coal capacity

Stable demand. Some new coal PP replacing aging capacity

Coal tax favors imports of higher calorific value coal

11

The key role of Indonesia on the supply side

• Indonesia still the top steam coal exporter (2015)

• A large part is low-ranked coal (future market?)

• Exports to China have declined sharply since 2014. Those to India also fell in 2015

• Consolidation of the coal mining sector and crack down on illegal mining and exports (production cap)

• Domestic sales are prioritized

• Fast Track Program to add 35 GW of capacity by 2019 (20 GW coal-based)

• Coal demand expected to double by 2019 less coal available for exports

0

50

100

150

200

250

300

350

400

450

Mt

Indonesian steam coal exports

China IndiaSouth Korea JapanTaiwan Other AsiaEurope Americas

12

Sustainability issues in Asia

13

Huge coal buildout but local pollution and CO2 emissions 1. Adopt Clean Coal Technologies

280

290

300

310

320

330

340

350

360

370

380

g/KW

h

Average coal consumption by coal power plants in China

70 Mtce/year saved between 2010 and 2015 CO2 emissions reduced by 170 Mt/year

• Meaning High-Efficiency/Low Emission Ultra-Supercritical plants

• To reduce local pollution and CO2 emissions per kWh

Ultra-low emission plants in China

• Ultra-low emission coal PP nearly equivalent to natural gas for non-carbon emissions

• CO2 emissions reduced…but still too high (CCSU?, but costs and huge investment required)

• Rationalization of the power fleet (“new” coal to displace old inefficient coal early retirement) and delays/cancellations

Typical emissions Regulation Dust 1 -10 mg/Nm3 ≤ 10 mg/Nm3 SO2 16-32 mg/Nm3 ≤ 35 mg/Nm3 NOx 21-50 mg/Nm3 ≤ 50 mg/Nm3

<310

14

2. Add renewables (and nuclear) to decrease the overall carbon footprint of the power sector

0

20

40

60

80

100

120

CoalCO2 emissions0.775 t/MWh

SolarCO2 emissions

0 t/MWh

CCGTCO2 emissions0.345 t/MWh

$/M

Wh

Generation costs (2015)

Capital and non-fuel costs Fuel costs

Total cost of 45% of coal and 55% of solar is cheaper than an equivalent 100% gas-based strategy, with the same amount of CO2 emissions

Strong RE push everywhere in Asia

• China (13th FYP): 210 GW of wind, 110 GW of solar by 2020

• India: 175 GW by 2022, mainly solar

• Southeast Asia: + 75 GW by 2025, mainly hydro and solar

15

But the current coal fleet is not flexible enough to accommodate (future) RE variability

Experience in Germany Solar + Coal in Luzon (Philippines)

Add flexible plants: hydro storage (when available) and Gas (LNG) peak units

Also retrofit coal-fired power plants to allow more flexibility (China)

Integrate the grid (ASEAN Power Grid)

Electricity generation in Germany Week 32 2016

Electricity generation in Germany Week 1 2016

16

Conclusion

17

Conclusion

More than ever, energy policy/regulation in China is dictating the price of coal

And therefore the price of electricity in coal importing countries: Southeast Asia, and Europe!

Rebalancing a huge market, such as the Chinese one, is not an easy task.

Volatility of coal prices to stay

Potentially exacerbated by 5 years of lack of investment in the mining sector

On the supply side, the role of Indonesia is key in the short/medium term

18

Conclusion In most Asian countries, the current least-cost strategy is towards ‘new coal’ and renewables + nuclear + some gas

The relatively low gas prices and high coal prices have not (yet?) been translated into gas-power investment

Two perceived issues: security of gas supply (despite ample availability) and lack of gas infrastructure (grid). LNG can help provided it remains affordable

Additions to the coal fleet in Asia are being reassessed (not only in China)

0

2

4

6

8

10

12

14

16

18

20

$/M

Btu

LNG prices vs coal prices: The coal window is closing?

Coal LNG Coal (efficiency-adjusted)

Coal window Coal window

Gas buildout

19

THE THIRD IEA-IEF-OPEC SYMPOSIUM ON GAS AND

COAL MARKET OUTLOOKS

Thank you for your attention