MAY 2013 01 Introduction 02 Market Potential 04 Challenges for Japan’s Asset Management Sector 06 Changing Mindset 08 The Way Forward The Trend Toward Outsourcing: A Case Study of Japan Japan’s financial services outsourcing market is rapidly evolving. Japan-based asset managers are beginning to embrace the global move by financial institutions toward the increased outsourcing of back- and middle-office functions to manage costs and facilitate expansion in line with global best practices. While Japan’s outsourcing market is at a relatively early stage, it is beginning to overcome a traditional resistance to outsourcing operations, driven by increased pressures to remain competitive in the face of global economic challenges. The new openness to outsourcing means increased flexibility, by reducing asset managers’ ongoing investment in infrastructure and ensuring that the scale required to support expansion is available when required. Equally, outsourcing provides Japan’s asset managers the ability to focus on their core competency and achieve enhanced insights into their performance. Outsourcing is set to play an increasingly large role in promoting growth in the Japanese market.

Transcript

MAY 2013

01 Introduction

02 Market Potential

04 Challenges for Japan’s

Asset Management Sector

06 Changing Mindset

08 The Way Forward

The Trend Toward Outsourcing: A Case Study of JapanJapan’s financial services outsourcing market is rapidly evolving. Japan-based asset managers are beginning to embrace the global move by financial institutions toward the increased outsourcing of back- and middle-office functions to manage costs and facilitate expansion in line with global best practices. While Japan’s outsourcing market is at a relatively early stage, it is beginning to overcome a traditional resistance to outsourcing operations, driven by increased pressures to remain competitive in the face of global economic challenges. The new openness to outsourcing means increased flexibility, by reducing asset managers’ ongoing investment in infrastructure and ensuring that the scale required to support expansion is available when required. Equally, outsourcing provides Japan’s asset managers the ability to focus on their core competency and achieve enhanced insights into their performance. Outsourcing is set to play an increasingly large role in promoting growth in the Japanese market.

This is State Street

With $24.4 trillion in assets under custody and administration, and $2.1 trillion in assets under

management* as of December 31, 2012, State Street is a leading financial services provider

serving some of the world’s most sophisticated institutions. We offer a flexible suite of services

that spans the investment spectrum, including investment management, research and trading,

and investment servicing. With operations in 29 countries serving clients in more than 100

geographic markets, our global reach, expertise, and unique combination of consistency and

innovation help clients manage uncertainty, act on growth opportunities and enhance the value

of their services.

*This AUM includes the assets of the SPDR Gold Trust (approx. $72.2 billion as of December 31, 2012), for which State Street Global Markets, LLC, an affiliate of State Street Global Advisors, serves as the marketing agent.

State Street’s Vision Series distills our unique research, perspective and opinions into

publications for our clients around the world.

THE TREND TOWARD OUTSOURCING: A CASE STUDY OF JAPAN • 1

Japan’s outsourcing market is evolving from a domestic-focused service to one that

is more aligned with global best practices. The market is beginning to overcome a

traditional resistance to outsourcing key operations such as back- and middle-

office functions, driven by increased pressures to remain competitive in the face

of global economic challenges. The new openness to outsourcing offers asset

managers increased flexibility, by reducing their ongoing investment in infrastructure

and ensuring that the scale required to support expansion is available when

required. Equally, Japan’s asset managers are benefiting from enhanced insights

into performance available via outsourcing functions. Outsourcing is set to play an

increasingly large role in the Japanese market, and that in turn offers strong growth

potential for global outsourcing firms.

Introduction

As is the case elsewhere in the Asia Pacific region,

Japan’s outsourcing market is, however, at a relatively

early stage of development. Traditionally, both the asset

manager affiliates of major Japanese financial institutions

and the local operations of international asset managers

have resisted moves to outsource key back- and middle-

office operations. Now, this mindset is beginning to

change as firms face competitive and cost pressures

and become more comfortable with providers and the

services they offer. This trend toward outsourcing is

likely to spread across Asia Pacific as many of the same

drivers of outsourcing in Japan exist in other markets in

the region, such as China.

2 • VISION FOCUS

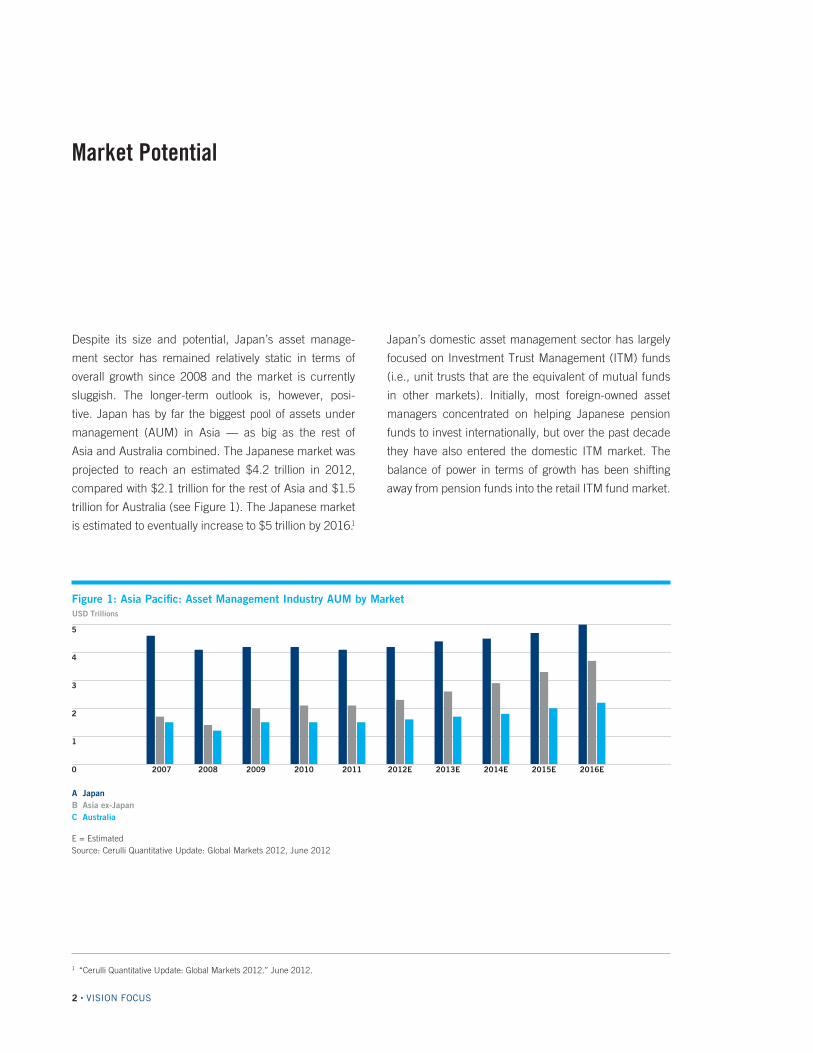

Despite its size and potential, Japan’s asset manage-

ment sector has remained relatively static in terms of

overall growth since 2008 and the market is currently

sluggish. The longer-term outlook is, however, posi-

tive. Japan has by far the biggest pool of assets under

management (AUM) in Asia — as big as the rest of

Asia and Australia combined. The Japanese market was

projected to reach an estimated $4.2 trillion in 2012,

compared with $2.1 trillion for the rest of Asia and $1.5

trillion for Australia (see Figure 1). The Japanese market

is estimated to eventually increase to $5 trillion by 2016.1

Japan’s domestic asset management sector has largely

focused on Investment Trust Management (ITM) funds

(i.e., unit trusts that are the equivalent of mutual funds

in other markets). Initially, most foreign-owned asset

managers concentrated on helping Japanese pension

funds to invest internationally, but over the past decade

they have also entered the domestic ITM market. The

balance of power in terms of growth has been shifting

away from pension funds into the retail ITM fund market.

Market Potential

1 “Cerulli Quantitative Update: Global Markets 2012.” June 2012.

Figure 1: Asia Pacific: Asset Management Industry AUM by Market

E = Estimated Source: Cerulli Quantitative Update: Global Markets 2012, June 2012

THE TREND TOWARD OUTSOURCING: A CASE STUDY OF JAPAN • 3

2 “Japan’s Asset Management Business 2011–12.” Nomura Research Institute Ltd., December 2011.3 State Street Japan Client Interviews, November 2012.4 “BPO utilization expands amid changes in Western asset managers middle office operations.” Nomura Research Institute, January 2011. 5 State Street Japan Client Interviews, November 2012.

While many of the major international asset managers

have a presence in Japan, the local operations of these

non-Japanese institutions are relatively small compared

to those owned by the four or five major integrated

Japanese financial conglomerates, which dominate the

market. International asset managers tend to have a

global operating model in which Japan is generally an

outlier, while the Japanese managers have traditionally

had limited or no operations outside of Japan.

Growing role for outsourcing

This landscape in the Japanese fund market is now

changing, as international asset managers look to

leverage their commitment to Japan by doing more

with their presence in the market. Japanese institu-

tions are also beginning to explore prospects for growth

internationally, according to a recent Nomura Research

Institute (NRI) report. Many Japanese asset manage-

ment companies that already have overseas units are

planning to expand their overseas staff. For large asset

managers in particular, says NRI, seeking new clients

overseas is an inevitable trend.2 Outsourcing is beginning

to play a more important role in the Japanese market to

support this expansion. “We have seen outsourcing of

investment management associated with quantitative

expansion and diversification of investment in overseas

assets,” noted one market participant.3

A key difference in the Japanese market is that local

asset managers have traditionally taken on the task

of calculating NAVs and have not yet significantly

utilized back-office outsourcing.4 However, international

outsourcing institutions are finding that local asset

managers are increasingly willing to forego in-house

control, providing they can be assured that the quality of

services can be maintained and improved, and that local

regulatory requirements are met.

In addition, previously perceived barriers such as

local language requirements and lack of investment

management experience have been overcome through

technological advances and development of well trained

in-country teams staffed with industry veterans.

Clients interviewed by State Street noted that outsourcing

back-office functions had enabled them to cut relative

costs and ease seasonal business fluctuations. “These

services have fundamentally changed the operating

model of our Japanese subsidiary,” said one client.5

Increased competition is encouraging Japan-based

firms to align with global best practices, reinvigorating

the market for outsourcing.

Japan’s asset management industry faces a number

of challenges that are compelling asset managers

to consider outsourcing as a way of enabling them

to refocus on their core investment business to stay

competitive. Many of these challenges are shared

by asset managers in other Asia Pacific markets and

around the world.

The domestic Japanese economy hovered on the edge

of recession throughout the 1990s and early 2000s

before showing signs of recovery around 2005, then

slipping back into recession mode. Meanwhile, an aging

population is resulting in higher pension payouts that

are eroding pension fund assets. These pressures were

exacerbated by the 2008 global financial crisis and

subsequent global economic turmoil. These challenges

have reinforced the need for asset managers operating in

Japan to attain greater operational efficiencies and have

made them more receptive to outsourcing as a solution.

Many of the current Japanese financial conglomerates

were created through earlier industry consolidation in

the 1990s. As a result, inefficiencies exist in their asset

manager operations, with some institutions having

multiple domestic asset manager affiliates, in some

cases operating independently of each other. They

increasingly recognize outsourcing to a third party as a

potential solution.

Regulatory developments are also impacting outsourcing

in Japan as new reporting and operational requirements

encourage asset managers to consider outsourcing.

The rules around outsourcing are, however, typically

perceived by some observers as vaguely worded and

requiring more clear definition, which has discouraged

some asset managers from outsourcing.

In addition, in 2012 the industry was hit by the scandal

in which AIJ Investment Advisors Co., a relatively small

asset manager, is alleged to have presented false NAVs

to hide poor investment performance and fraudulently

collect a massive amount of client assets, partly via an

offshore entity. In follow-up investigations, Japanese

regulator the Financial Services Agency (FSA) found that

less than one half of the 265 asset managers it surveyed

had commissioned outside auditors to check their

accounts, leading to calls for tighter controls in some

areas of the industry.6 Tighter rules will place greater

obligations on Japan’s asset managers and outsourcing

providers, thereby making the choice of outsourcing

provider increasingly critical.

Regulatory environment

As noted, one of the most significant factors affecting

the potential use of outsourcing services in Japan is the

domestic regulatory environment. In the early 2000s,

outsourcing by financial institutions was scrutinized

by the FSA and quite often resulted in administrative

action being taken against financial institutions for lack

of written documents, appropriate oversight and/or due

diligence. The general principles and business practice

around outsourcing were established by the mid-2000s,

and in 2007 the FSA incorporated the requirements of

outsourcing for deposit-taking institutions into the FSA

inspection manual for deposit-taking institutions.

4 • VISION FOCUS

Challenges for Japan’s Asset Management Sector

6 “Shades of Madoff in pension fund scandal,” Nikkei Weekly, March 26, 2012; “Law enforcers urged to probe misappropriation of AIJ’s pension funds,” The Mainichi, June 20, 2012.

7 UCITS Notices: “Undertakings for Collective Investment in Transferable Securities authorized under European Communities (Undertakings for Collective Investment in Transferable Securities) Regulations 2011,” December 2011.

8 APRA. “Draft Prudential Practice Guide - SPG 231 – Outsourcing”, December 2012.

However, while it is generally understood that

responsibility for outsourced activities remains with

the outsourcing asset manager, a key concern facing

any manager considering outsourcing is the level of

oversight over outsourced activities and due diligence

that will be required. Because of this, some asset

managers not familiar with outsourcing have considered

the outsourcing of back- and middle-operations to

be impractical. Another factor that may have stalled

acceptance of outsourcing is that, prior to the global

financial crisis of 2008–2009, there was no player in

Japan able to offer full services in the area of back- and

middle-office operations. As a consequence, until the

extended global downturn in the asset management

business over the past few years, asset managers in

Japan had little incentive to challenge the status quo

and proactively initiate outsourcing, even as their global

competitors embraced the concept.

The requirements in the FSA inspection manual are

in principle similar to those in other major financial

markets in the world, where outsourcing is an accepted

and regulated practice, and governed by specific

rules and frameworks. For example, in Europe, there

are strict definitions as to how outsourcing can be

implemented. For collective investment schemes (CIS)

in Ireland, regulations governing Undertakings for

Collective Investment in Transferable Securities (UCITS)

stipulate that the ultimate responsibility for the proper

management of the risks associated with outsourcing

lies with the administration firm’s senior management,

and that outsourcing arrangements can never result in

the delegation of senior management’s responsibility.

The outsourcing of core management functions —

such as setting the risk strategy, the risk policy and,

accordingly, the risk-bearing capacity of the firm —

and the final responsibility toward clients and the Irish

Central Bank must not be outsourced.7

Another example is the Australian Prudential Regulation

Authority (APRA), which that has issued a prudential

standard and a draft prudential practice guide on

outsourcing for superannuation or pension scheme

service providers related to outsourcing. The outsourced

activities include administration, custody arrangements,

investment management functions, business continuity

planning arrangements, marketing and arrangements

with financial planners and fund promoters, and the

internal audit function. The standard requires that,

among other things, consideration be given to the

adequacy of resources of a service provider, business

continuity management arrangements and oversight.8

There has been discussion of possible changes to

Japanese regulations to make it easier to outsource

operations. Some industry participants recommend

clarification of the scope of activities permissible for

outsourcing by asset managers. However, in discussions

at the Investment Trust Management Working Group

(ITMWG) of the Financial System Council, the FSA

made it clear that outsourcing is permissible by ITM

companies under the current regulations.

The ITMWG notes that both the Financial Instruments

and Exchange Act (FIEA) and the Act on Investment

Trusts and Investment Corporations (ITM Act) prescribe

the scope of investment management that ITM

companies can delegate to third parties. But it also

recognizes that there is no regulation under FIEA with

respect to the outsourcing of other activities by ITM

companies to third parties, and therefore, some industry

participants still argue that it is unclear whether or not

ITM companies can outsource such activities. According

to the FSA, the fact that there is no specific regulation

under the FIEA or ITM Act means that ITM companies

can outsource such activities. The working group asked

that it be made clear that outsourcing activities other

than investment management was permissible.

Notwithstanding this, Japanese and foreign-owned

investment managers have been outsourcing limited

administrative functions for a decade or more, NAV

calculation being one example, and more recently there

has been quite extensive outsourcing, particularly by

foreign-owned asset managers in Japan.

THE TREND TOWARD OUTSOURCING: A CASE STUDY OF JAPAN • 5

Outsourcing services firms have had to address a

number of challenges in the Japanese market, including

an established tradition of keeping back- and middle-

office operations under in-house control, stemming from

fears that outsourcing will result in a lack of end-to-end

control that may cause reputational damage.

But there is now clear evidence of a changing mindset on

the part of Japan’s asset managers. As the market responds

to the impact of the recent global economic challenges,

domestic asset managers have become more receptive

to outsourcing. Some asset managers are proactively

looking ahead at a continuing tough environment and

are investigating outsourcing as a way to support their

business in the event of a prolonged downturn. They are

seeking alternatives to devoting significant staff and costly

technology investment to upgrading and integrating back-

and middle-office services.

Big domestic asset managers that are looking to

respond to current market pressures through further

consolidation and scaling up of operations are beginning

to realize the difficulties and costs involved in trying

to integrate their multiple back and middle offices. In

addition, many stand-alone domestic asset managers

also recognize the need to invest significantly in systems

and staff to remain competitive, and are questioning if

these investments are the best value for money in the

current environment. As noted earlier, Japanese asset

managers are now pursuing opportunities overseas,

and can benefit from the scale and local knowledge of

outsourcing providers to support these ambitions.

While outsourcing does not necessarily represent an

overnight reduction in costs, it can deliver significant

long-term benefits by removing the need for ongoing

investment in technology and staff over the long term.

International firms helping drive change

The drivers toward outsourcing and the pressures to

consider outsourcing are the same among all managers,

whether they are affiliated with major Japanese or

international institutions. However, growth in the use

of outsourcing has initially come from investment

management firms with affiliations both inside and

outside Japan. During difficult economic conditions,

these organizations have been the first to feel the

pressure to achieve greater economies of scale when

operating in Japan.

They have also experienced in other markets the

operational efficiencies that outsourcing can offer.

In turn, their experience is helping fuel a changed

approach on the part of domestic asset managers.

One example of how the environment is responding is

the inroads made by outsourcing companies in meeting

back-office needs such as NAV pricing. These needs

have traditionally been met in-house, by Japanese

trust banks or by a small group of local research/IT

players that have provided this service in a data entry

capacity. International outsourcing providers initially

offered trustee services to Japanese pension funds, but

have evolved into such areas as providing ITM fund

valuation services, and a variety of operational and

reporting outsourcing services.

Service providers are now providing specialized reporting

and governance packages, and intraday, daily, monthly

and quarterly critical management reporting. In some

6 • VISION FOCUS

Changing Mindset

9 State Street Japan Client Interviews, November 2012.10 “Japan’s Asset Management Business 2011–12.” Nomura Research Institute Ltd., December 2011.11 State Street Japan Client Interviews, November 2012.12 “Japan’s Asset Management Business 2011–12.” Nomura Research Institute Ltd., December 2011.

areas they can offer an improvement on the services

that have traditionally been available in the market. The

major Japanese domestic asset managers are aware that

the market has been transformed over the past five years

and are conscious that some competitor international

companies operating in Japan are outsourcing their

back- and middle-office operations.

Clients interviewed by State Street in Japan referred

to the “huge impact” that the entry of foreign

outsourcing suppliers has had on the market.

According to one Japan-based asset manager, their

services and products have “significantly lowered

the hurdle of using outsourcing service providers for

Japanese financial institutions, and especially asset

management companies.”

Asset managers are recognizing that outsourcing firms

are making it easier for them to realize significant

operational efficiencies. In addition, clients noted that

Japan’s outsourcing industry was becoming more

competitive, with some domestic firms seeking to

expand the scope of their services. One respondent

noted that foreign service providers were more solutions-

oriented than domestic outsourcing firms, which in turn

was having an impact on the market.9

Incentives to outsource

Japan’s asset managers realize they face three options

in addressing their current challenges:

• Continue to fight for share in a domestic market that

shows no signs of immediate improvement or growth

• Look for ways of increasing operational efficiencies

and reinvigorate their focus on their core business of

investment management

• Diversify into other markets and asset classes

Each of these options provides an incentive to examine

the benefits of outsourcing. Addressing the overall cost

base is a major driver. Staffing costs are a key element

for Japan’s asset managers, especially in a market that

traditionally followed a policy of lifetime employment,

resulting in large headcounts. Personnel costs are

the biggest expense for Japan’s asset managers and

personnel cost containment has become a major theme

for Japanese management.10

Outsourcing offers the potential to redeploy staff more

effectively by concentrating personnel on the investment

side of the business, while back- and middle-office

functions are increasingly outsourced. “Outsourcing these

functions enables us to cut relative costs and to achieve

partial conversion of fixed costs to variable costs, as well

as remove an impact on the quality maintenance due

to the change of staff and systems,” observed one asset

manager.11 In a recent survey, Japan’s asset managers

predicted headcount decreases across all organizational

functions, with the exception of overseas operations.12

Thus, as a result of the recent market challenges,

Japan’s asset managers are increasingly beginning to

reach out to outsourcing providers, to provide both back-

and middle-office services for Japanese operations.

However, subsidiaries of international asset managers

are not the only ones leading the way; some Japanese

companies have also been early adopters. For example,

Nikko Asset Management, a large domestic player

previously controlled by Citigroup and now owned by

Sumitomo Mitsui Trust Group, was one of the first major

Japanese companies to opt for significant outsourcing.

Significantly, some asset managers are now looking

for service providers that can manage their back- and

middle-office functions, and free up resources that

can be focused on their core business of investment

management. And, as Japanese asset managers

increasingly look abroad for new opportunities, they

need service providers with a combination of global

scale and knowledge and expertise in local markets

to help them seize these opportunities and make

inroads internationally.

THE TREND TOWARD OUTSOURCING: A CASE STUDY OF JAPAN • 7

13 State Street Japan Client Interviews, November 2012.14 “BPO utilization expands amid changes in Western asset managers middle office operations.” Nomura Research Institute, 2011.

8 • VISION FOCUS

Japan’s asset managers cite a number of recent drivers

of change in the industry, including increasingly fierce

competition for customized operations due to diverse

client needs and operational schemes. They also

note the need for more flexible structures to provide

services because reporting and disclosure have become

increasingly important.13

The flipside is that it is not enough for outsourcing

providers to offer breadth of capability, flexibility and

global best practices in Japan. This approach must be

offered in the context of a service that meets local market

standards around accuracy, timeliness and quality. For

example, State Street operates its outsourcing services

through a local trust bank structure in Japan that enables

it to provide appropriate accountability for the firm and

confidence for the client in this market.

Japan’s asset managers who have begun to use

outsourcing services report a number of advantages,

including the ability to cut internal fixed costs, improve

This material provides information of a general nature. Any comments or observations we have made have been drawn from information, sources of which we believe reliable and we make no representation or warranty as to its accuracy.

The products and services may not be available in all jurisdictions. Please contact your sales representative for further information.

For questions or comments about our Vision series,