27

The Use of IFRS for Prudential and Regulatory Purposes IFRS 9 - Update REPARIS IFRS Seminar Vienna, Sept 6-7 2010

The Use of IFRS for Prudential and Regulatory Purposes IFRS 9 - Update

REPARIS IFRS Seminar Vienna, Sept 6-7 2010

! Introduction ! IFRS 9 – Classification and Measurement ! IFRS 9 – Impairment ! IFRS 9 – Hedge Accounting ! FASB Exposure Draft Financial

Instruments ! Fair Value Measurement ED ! ED Other Comprehensive Income (OCI)

Agenda

2

! IAS 39 replacement project (IFRS 9: Financial Instruments), conducted in three phases: - Phase 1-Classification and Measurement

(completed in November 2009 for asset side) - Phase 2-Impairment Methodology : ED 2009/12 Amortised Cost

and Impairment, based on expected cash flow model, published in Nov. 2009, comments due June 2010, final standard expected end 2010

- Phase 3-Hedge Accounting (ED in 3rd or 4th quarter of 2010) IASB aims to replace all of the requirements of IAS 39 by the 2nd quarter of 2011

! FASB Exposure Draft (26 May 2010) Accounting for Financial Instruments and Revisions to the Accounting for Derivative Instruments and Hedging Activities

Introduction

3

! Goals of the Financial Instrument Project - Increase transparency by reducing complexity - Ensure that information is relevant so that the accounting

accurately mirrors the business activity - Provide reliable information free from bias - Enable comparability between entities and over time

! Convergence project between IASB and US FASB - Example ED on Improvements to Disclosure Requirements

for Level 3 Fair Value Measurements: jointly issued ED’s by both standard setters

- Example Fair Value Measurement ED: one standard setter in lead, the other is “following”

- Example Financial Instruments Project: different timing, different project approach, different accounting model

Introduction (continued)

4

! IFRS 9 as of November 2009 - For financial assets only - Required application by 2013 - EU hasn’t endorsed IFRS 9 (Phase 1) as had been

planned - EU-endorsement postponed till all phases are completed

! ED FVO for Financial Liabilities (11 May 2010) - IFRS 9 as of 12 November 2009 excluded financial

liabilities from its scope - Main reason was unsolved problem of handling Own Credit

Risk (OCR) - 24 May 2010 – IASB’s Own Credit ED user questionnaire

(deadline 16 July 2010)

IFRS 9

5

IFRS 9

6

Amortised Cost Fair Value

Business model: hold assets to collect the contractual cash flows Contractual cash flows: solely payments of principal and interest on the principal outstanding

derivates equity instruments Fair Value Option financial instruments, missing amortised cost-requirements

Effective Interest Model Impairment

Gains/Losses as per sale

P&L

Fair Value changes interest, dividends

OCI P&L

Reclassification (only as per changing

of business model)

Fair Value Option (only „accounting mismatch“)

Option for equity instruments which are not held for trading

dividends

Classification and Measurement – Assets

! Comments on ED/2010/4 due to 16 July 2010 ! Main features

- IAS 39 requirements for Financial Liabilities mainly retained - twofold mixed measurement model - FVO with IAS 39-requirements: accounting mismatch,

hybrid (combined) instruments with embedded derivatives, portfolio fair valuation for a group of financial instruments

- bifurcation requirement for structured instruments with embedded derivatives

- proposed change: Own Credit Risk (OCR) requirements

IFRS 9

7

Classification and Measurement – Liabilities ED FVO for Financial Liabilities (11 May 2010)

IFRS 9

8

Classification and Measurement – Liabilities ED FVO for Financial Liabilities (11 May 2010)

9

! OCR requirements - OCR = accounting effect of changes in the own credit risk on

fair value of financial liabilities ! counter-intuitive and confusing

- ∆ OCR ∆ FV Liability - OCR ↓ FV Liability ↓ Gain ↑ (et vice versa)

! two-step approach - fair value change of liabilities under the FVO recognised in P&L - portion of fair value change due to OCR would be reversed

out of P&L and recognised in OCI - no recycling of OCR component into P&L; transfer within equity

! P&L volatility will no longer result from changes in OCR while information on OCR will still be available for investors

! no new measurement method introduced ! ED/2010/4.A2: cumulative change in OCR will be disclosed IFRS 7.10(a) ! to determine OCR reference to IFRS 7.10(a) and B4:

amount of change that is not attributable to changes in market conditions that give rise to market risk

Classification and Measurement – Liabilities ED FVO for Financial Liabilities (11 May 2010)

IFRS 9

10

Classification and Measurement – Liabilities ED FVO for Financial Liabilities (11 May 2010)

! ED 2009/12 Amortised Cost and Impairment, based on expected cash flow model, published in November 2009, comments due 30 June 2010, final standard expected end 2010

! Ongoing discussions within the Board ! 9 July 2010 – Summary of the discussions by the Expert Advisory

Panel (EAP) ! BCBS sent a Comment Letter with its own proposal on an expected

loss based impairment model main features

! EBF with separate proposal ! No final decision taken yet

IFRS - Impairment

11

! 3rd phase of IAS 39 replacement project ! Ongoing discussion about an ED at the IASB ! Fair Value Hedge Accounting (FVH)

- At an early stage IASB tentatively decided to replace the FVH mechanics with those for cash flow hedge accounting (CFH)

• Effective portion of fair value change of hedging instrument would have been recognised in OCI

• Introduces volatility in equity - Outreach activities of the IASB on that proposal changed thinking

• FVH might retained but developed • IASB sees problem of ‘leverage volatility’ as accounting treatment other

than CFH results in the recognition and change of additional amounts for both the hedge item and the hedging instrument

IFRS 9 - Hedgeaccounting

12

- Current discussions of IASB about FVH • Changed its tentative decision for FVH • Discussed approach

o Present cumulative gains and losses on hedged item attributable to hedged risk as a separate line item in balance sheet

o Fair value changes of hedging instrument and hedged item attributable to hedged risk are taken to OCI

o Any ineffectiveness is transferred immediately to P&L - Idea of linked presentation of hedge item and hedging instrument

! Eligible hedged items: groups and net positions - IASB is still discussing whether a net position of a group/portfolio of

financial instruments could be a hedged item - IASB is still discussing whether a portion of an existing item could be a

hedged item - Both may require a clear and robust link to risk management

IFRS 9 – Hedgeaccounting (continued)

13

! Hedge Effectiveness - IASB is still discussing how effectiveness of a hedgeaccounting

relationship should be measured - Board emphasised to build hedge accounting around the notion of

‘offset’, as offsetting must be characteristic for a hedging relationship

- As such IASB-staff proposed • to eliminate accidental offsetting from the scope of hedge

accounting • to link effectiveness testing to the entity’s risk management

- Link to risk management shall connect hedge effectiveness testing in accounting to the risk strategy of a bank, rather than using a separate merely accounting related effectiveness target as IAS 39, which is often an artificial exercise and apart from the risk management approach of the bank

- Shall also reflect that there is not a meaningful single target level for all types of hedging relationships and entities (no ‘one size fits all’ threshold)

IFRS 9 – Hedgeaccounting (continued)

14

Hedge Effectiveness

IFRS 9 – Hedgeaccounting (continued)

15

Hedge Effectiveness – discussed approaches

IFRS 9 – Hedgeaccounting (continued)

16

! “4th phase“ of IAS 39 replacement project ! In response to stakeholders’ concerns, IASB and FASB decided

to jointly issue a separate exposure draft proposing changes to address differences in their standards on balance sheet netting of derivative contracts and other financial instruments that can result in material differences in financial reporting by financial institutions. The boards understand the importance of this issue, which is one of the more significant financial instrument presentation differences between IFRS and US GAAP.

! Question of netting is highly relevant for banking supervisors - Comparison of volume and risk position of banks using different

accounting standards - With regard to the Leverage Ratio

IFRS 9 – Asset and liability Offsetting

17

! Asset and liability offsetting questionnaire (submission deadline 20 August 2010)

! As part of its deliberations the IASB would like to better understand whether and how investors and analysts use the gross and net information related to financial instruments, and in particular, derivatives. If you are not an investor or analyst, please do not complete the survey.

! Questions 1. Do you require both gross and net values of financial asset and liability

positions, and in particular derivatives, when analysing financial statements?

2. Assuming you need both gross and net information, which information would you prefer to see on the face of the balance sheet and which should be disclosed in the footnotes to the financial statements?

3. If net information is presented either on the face of the balance sheet or in the footnotes, should the netting be allowed based on an unconditional right to offset, or on a conditional right to offset (ie only in bankruptcy or default)?

4. If offsetting (netting) is based on risk exposure, should it be allowed for different types of risks?

IFRS 9 – Asset and liability Offsetting

18

FASB / IASB Offsetting Users Survey

FASB

19

! ED issued 26 May 2010 ! Comments due to 30 September 2010 ! IASB is inviting constituents to comment on FASB’s ED ! May influence the IASB regards its IAS 39 Replacement Project/IFRS 9 ! Comparison between IAS 39 Replacement Project and FASB ED

Exposure Draft Financial Instruments

IASB FASB

Measurement Approach • Fair Value • Amortised Cost

• Fair Value • Amortised Cost

Categories of Financial Instruments

• FV through P&L • Amortised Cost • FV through OCI (limited option for some equity investments)

• FV through NI • FV through OCI for qualifying instruments only • Amortised Cost (limited use)

Reclassifications • Required for financial assets if entity’s business model changes • Prohibited for financial liabilities

• Not permitted

FASB

20

IASB FASB

FV-OCI Classification Criteria

• Option for investments in equity instruments at inception

• Option for dept instruments • Entity’s business strategy for the instrument is to collect or pay contractual cash flows • Not a hybrid instrument

Amortised Cost Criteria • Financial asset must be at AC if: 1. Business model is to

hold the asset and collect contractual cash flows

2. Contractual cash flows are solely payments on principal and interest

• Financial liabilities are at AC if they are not held for trading or under the FVO

• Option for financial liabilities (only) that 1. Meet the criteria for FV-

OCI measurement 2. Measurement at FV would

create or exacerbate a measurement mismatch between assets and liabilities

Exposure Draft Financial Instruments

FASB

21

FASB IASB

Fair value through net

income

Fair value through OCI

Fair value through net

income

Amortized cost

Fair value through OCI Amortized cost

Exposure Draft Financial Instruments

FASB

IASB FASB

Fair Value Option • Financial assets: to reduce accounting measurement mismatch • Financial liabilities:

• reduce accounting measurement mismatch • group of financial instruments is managed on a fair value basis • liability contains separable embedded derivatives

• Not applicable

Impairment • Expected loss model starting when the financial asset is first recognised

• Contractual interest revenue, less the initial expected credit loss

• Expected credit losses would be reassessed each period and the effects ...

• For financial instruments at FV-OCI

• Entity is required to determine if impairment exists for financial asset(s) in considering all available information relating to past events an existing economic conditions

Exposure Draft Financial Instruments

FASB

IASB FASB

Impairment (continued)

• ... of any changes in expectations would be recognised in net income immediately

• No forecasts of possible future conditions • Recognise in net income a loss related to the amount of credit impairment for all contractual amounts that an entity does not expect to collect

Hedgeaccounting • IASB ED on Hedgeaccounting has to be published

• FV and CF Hedge • For FV Hedges changes

in hedge fair value recognized in net income

• Effectiveness threshold modified from highly to reasonable effective

• Elimination of shortcut method in assessing hedgeeffectiveness

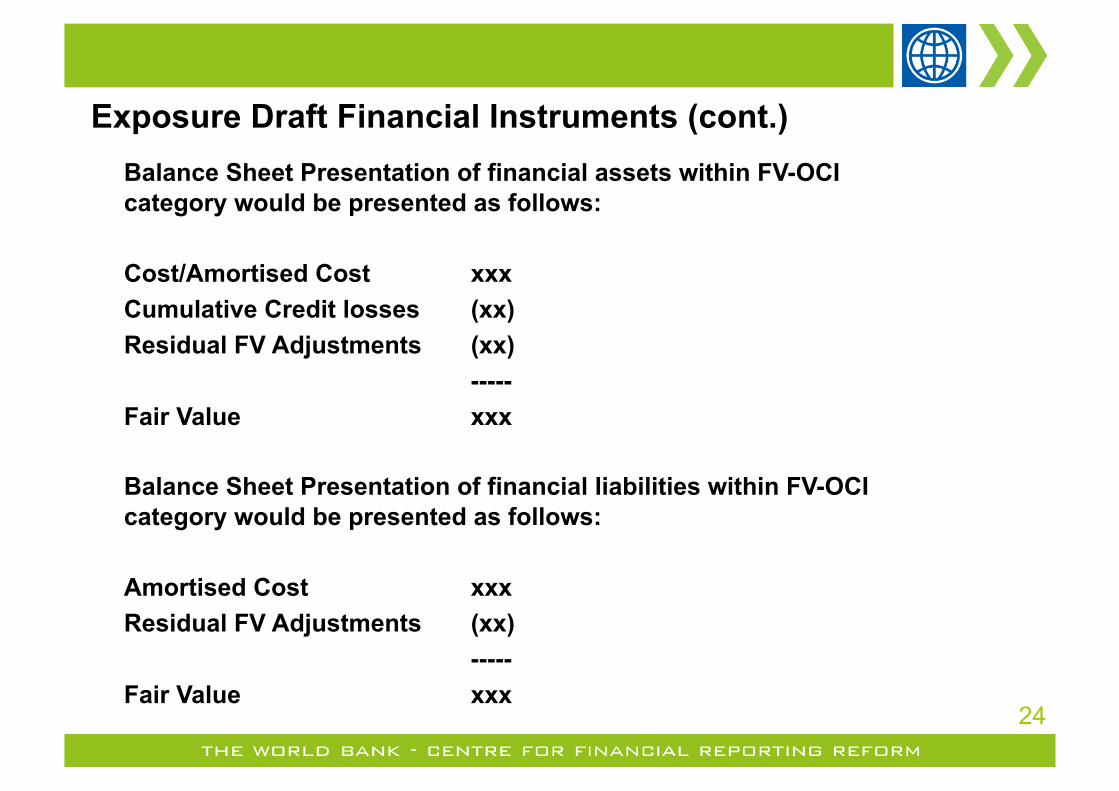

Exposure Draft Financial Instruments (cont.)

Balance Sheet Presentation of financial assets within FV-OCI category would be presented as follows:

Cost/Amortised Cost xxx Cumulative Credit losses (xx) Residual FV Adjustments (xx)

----- Fair Value xxx

24

Exposure Draft Financial Instruments (cont.)

Balance Sheet Presentation of financial liabilities within FV-OCI category would be presented as follows:

Amortised Cost xxx Residual FV Adjustments (xx)

----- Fair Value xxx

! ED comment deadline is 7 September 2010 ! Valuation uncertainty is a matter of level 3-values ! Question of valuation adjustments and/or disclosures about valuation

risk ! ED is about appropriate disclosure in the case of level 3-valuation ! IASB is proposing to enhance the required measurement uncertainty

analysis disclosure to reflect the interdependencies (correlation) between unobservable inputs used to measure fair value in Level 3

! This information shall allow users to asses the effect that the use of different unobservable inputs would have had on the fair value measurement

! Banking Supervisors Bodies argue for a valuation adjustment in case of valuation uncertainty (Level 3) rather than having additional disclosure requirements only

IASB - Fair Value Measurement

25

Measurement Uncertainty Analysis Disclosure for Fair value Measurement Limited re-exposure of proposed disclosure

! ED 26 May 2010; comment deadline 30 September 2010 ! Relates to Financial Statement Presentation DP (IAS 1) ! What is the IASB proposal about? - Require P&L and OCI shown as separate components of a new

combined statement of comprehensive income - Require separate presentation of OCI items that will and will not

be reclassified/recycled ! Why is the IASB proposing a change? - Lack of clarity regarding the nature of OCI - Confusion over reclassification - Continued and increasing use of OCI (IFRS 9 – equity assets,

hedgeaccounting, OCR of financial liabilities; IAS 19 Employee Benefits)

IASB – ED OCI

26

ED Presentation of Items of Other Comprehensive Income - OCI

IASB – ED OCI

27

ED Presentation of Items of Other Comprehensive Income – OCI (continued)