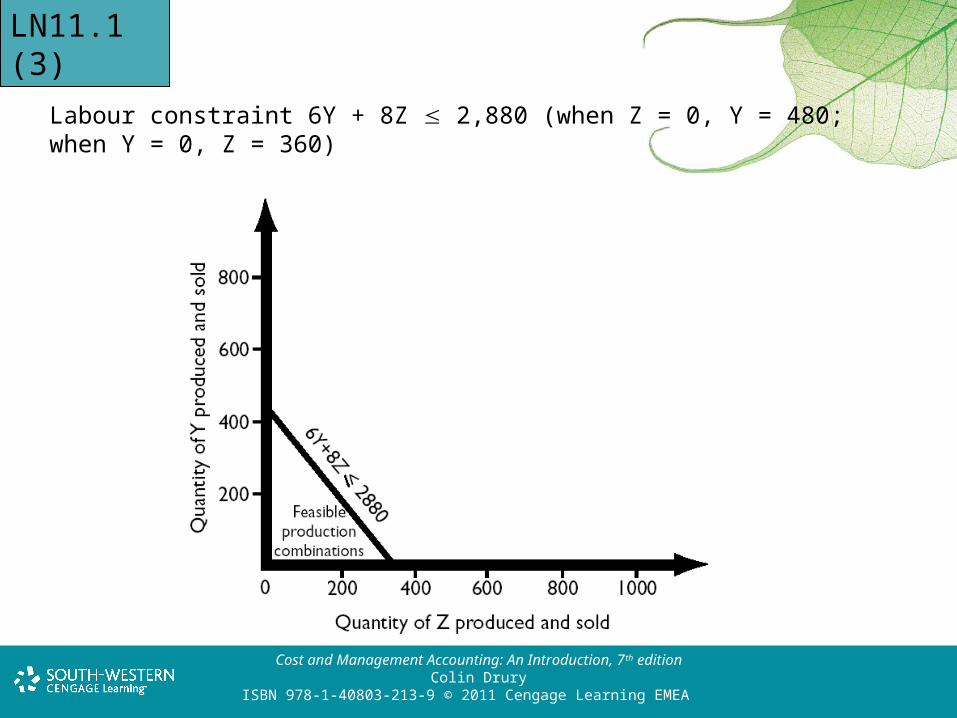

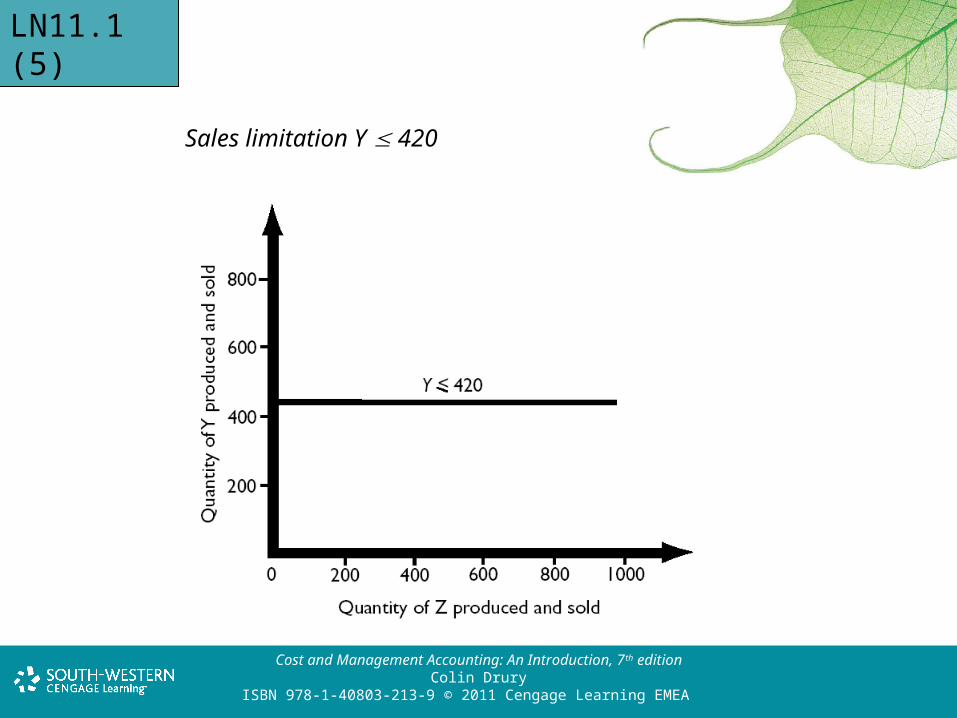

LEARNING NOTE 11.1. The use of linear programming for the allocation of scarce resources. LN11.1 (1a). Linear programming. LN11.1 (1b). Example (cont.). LN11.1 (2). Materials constraint (8Y + 4Z 3,440 (When Y= 0, Z = 860; when Z= 0, Y = 430. LN11.1 (3). - PowerPoint PPT Presentation

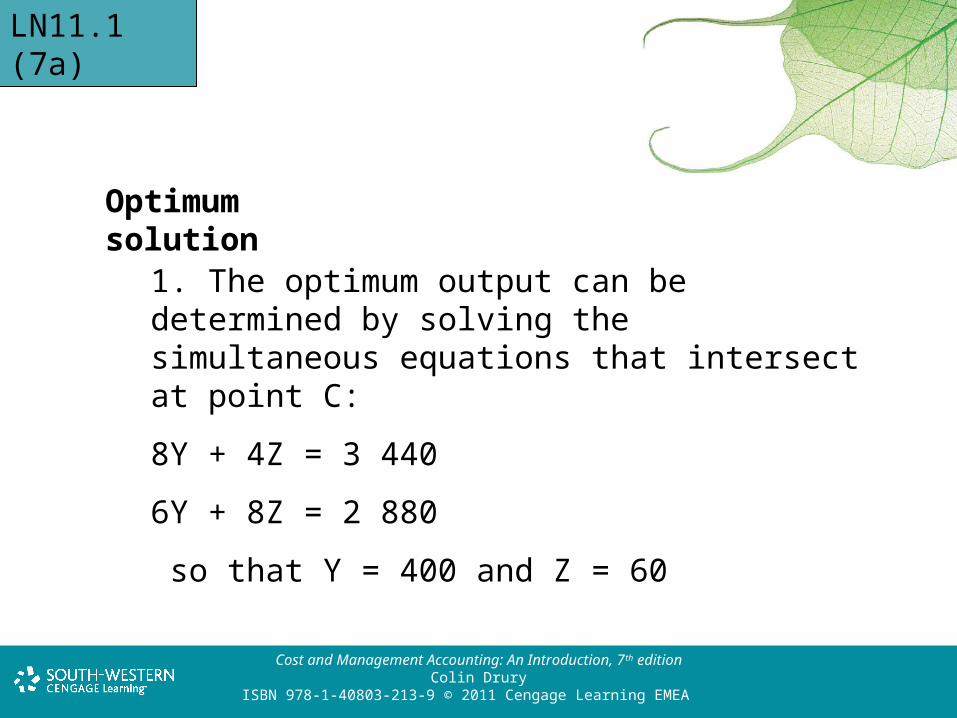

2. The materials and labour constraints are binding and therefore have opportunity costs. The marginal contribution from obtaining one extra unit of materials can be calculated by solving the following equations:

8Y + 4Z = 3 441 (revised materials constraint)

6Y + 8Z = 2 880 (unchanged labour constraint)

Y = 400.2 units, Z = 59.85 units

Therefore the planned output of Y would be increased by 0.2 units and Z reduced by 0.15 units and contribution will increase by £0.40 (the opportunity cost).

LN11.1 (7b)

Cost and Management Accounting: An Introduction, 7 th editionColin Drury