12

THE VIEW ON THE GROUND INDONESIA Singapore Mining Club - Coal Seminar 4 June 2015 James Brown Managing Director www.alturamining.com ASX: AJM For personal use only

THE VIEW ON THE GROUND

INDONESIA

Singapore Mining Club - Coal Seminar

4 June 2015

James BrownManaging Director

www.alturamining.comASX: AJM

For

per

sona

l use

onl

y

This presentation has been prepared by Altura Mining Limited (“Altura” or the “Company”). It should not be consideredas an invitation or offer to subscribe for or purchase any securities in the Company or as an inducement to make aninvitation or offer with respect to those securities. No agreement to subscribe for securities in the Company will beentered into on the basis of this presentation.

This presentation is provided on the basis that none of Altura nor its respective officers, shareholders, related bodiescorporate, partners, affiliates, employees, representatives and advisers make any representation or warranty (expressor implied) as to the accuracy, reliability, relevance or completeness of the material contained in the presentation andnothing contained in the presentation is, or may be relied upon as, a promise, representation or warranty, whether as tothe past or the future. The Company hereby excludes all warranties that can be excluded by law.

DISCLAIMER

2

the past or the future. The Company hereby excludes all warranties that can be excluded by law.

The presentation contains forward looking information and prospective financial material which is predictive in natureand may be affected by inaccurate assumptions or by known or unknown risks and uncertainties, and may differmaterially from results ultimately achieved. All references to future production, production targets and resource targetsand infrastructure access are subject to the completion of all necessary feasibility studies, permitting, construction,financing arrangements and infrastructure-related agreements. Where such a reference is made, it should be readsubject to this paragraph and in conjunction with further information about the Mineral Resources and ExplorationResults, as well as the Competent Persons' Statements.

All persons should consider seeking appropriate professional advice in reviewing the presentation and all otherinformation with respect to the Company and evaluating the business, financial performance and operations of theCompany. Neither the provision of the presentation nor any information contained in the presentation or subsequentlycommunicated to any person in connection with the presentation is, or should be taken as, constituting the giving ofinvestment advice to any person.

For

per

sona

l use

onl

y

• Altura’s coal interests

• Thermal coal price

• Thermal coal forecast

• Cost reduction targets

PRESENTATIONSUMMARY

3

• Cost reduction targets

• Other opportunities

• Moving forward

• Managing expectations

For

per

sona

l use

onl

y

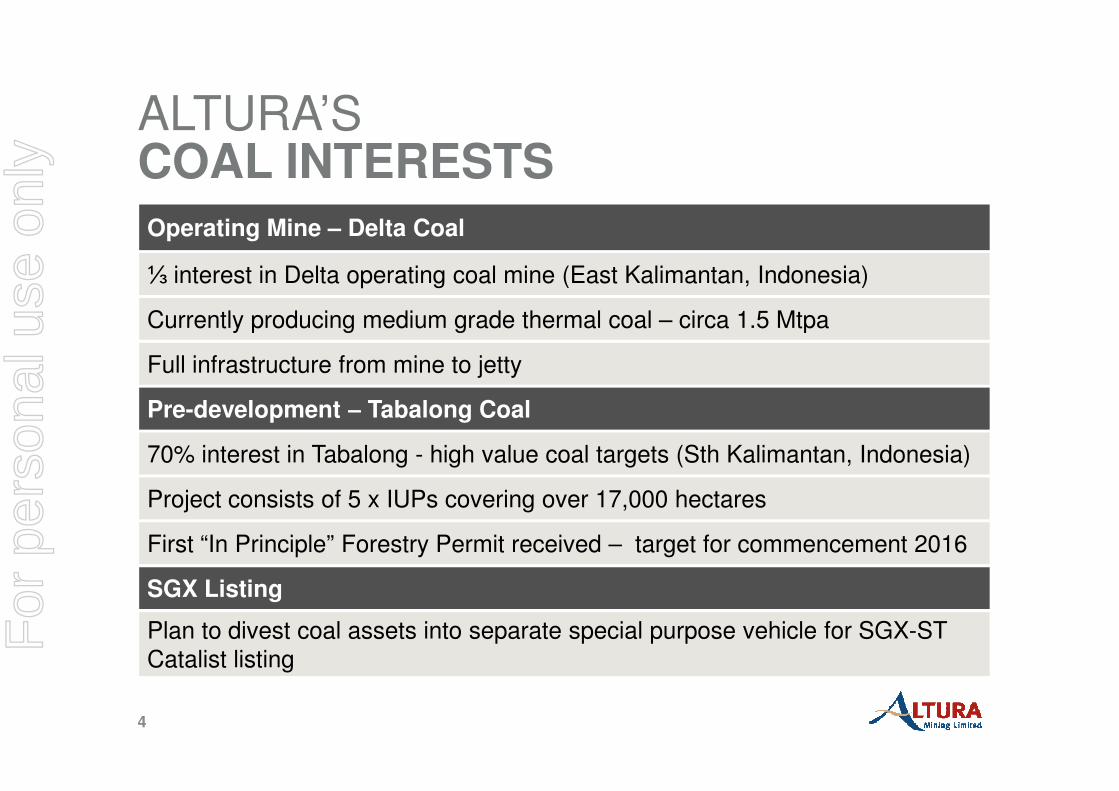

ALTURA’S COAL INTERESTS

Operating Mine – Delta Coal

⅓ interest in Delta operating coal mine (East Kalimantan, Indonesia)

Currently producing medium grade thermal coal – circa 1.5 Mtpa

Full infrastructure from mine to jetty

Pre-development – Tabalong Coal

4

Pre-development – Tabalong Coal

70% interest in Tabalong - high value coal targets (Sth Kalimantan, Indonesia)

Project consists of 5 x IUPs covering over 17,000 hectares

First “In Principle” Forestry Permit received – target for commencement 2016

SGX Listing

Plan to divest coal assets into separate special purpose vehicle for SGX-ST Catalist listing

For

per

sona

l use

onl

y

• Coal price has been in decline since early 2011

� Production has increased from 350MT to 430MT during same period

� Indonesia maintains position of world’s largest thermal coal exporter

� Coal producers face challenges to reduce costs to combat reduced revenue

� Producers increasing production in order to lower unit costs – delays price recovery with more coal in the market for sale

THERMAL COALPRICE

5

recovery with more coal in the market for sale

Source: Coalspot

For

per

sona

l use

onl

y

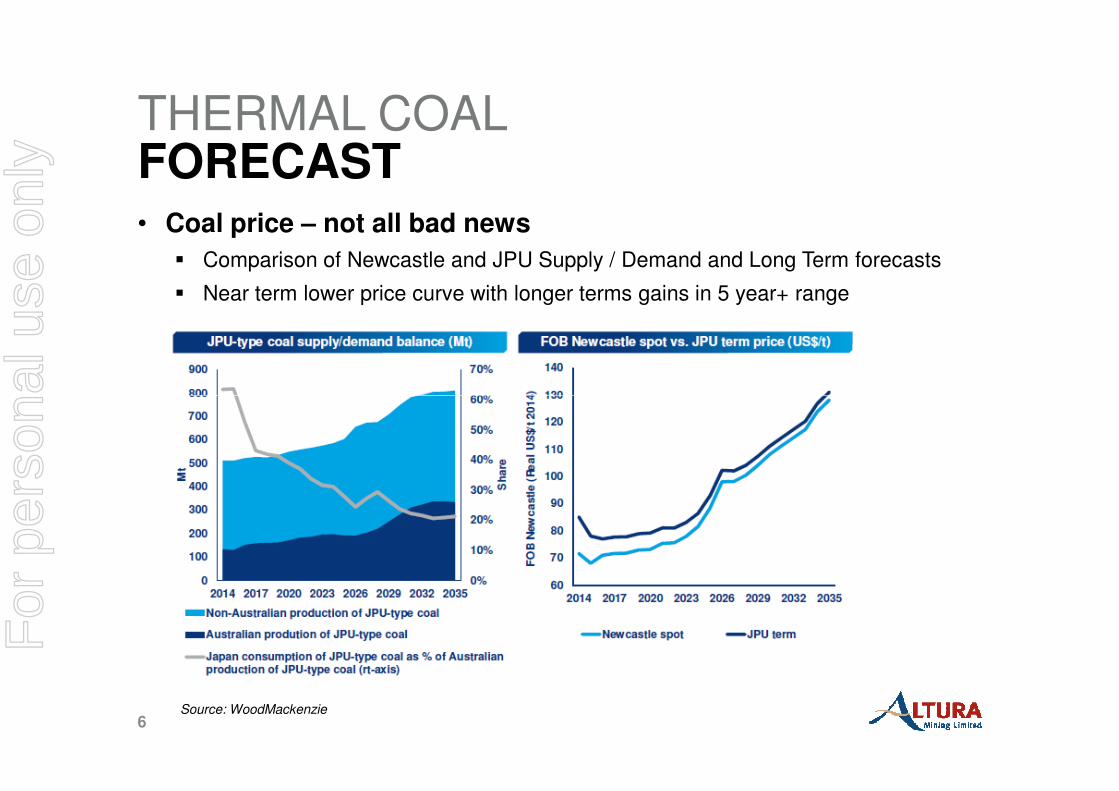

• Coal price – not all bad news

� Comparison of Newcastle and JPU Supply / Demand and Long Term forecasts

� Near term lower price curve with longer terms gains in 5 year+ range

THERMAL COALFORECAST

6Source: WoodMackenzie

For

per

sona

l use

onl

y

• Starting with the Big Ticket items

� In cyclical industry such as coal mining there is a natural tendency to become complacent when it comes to opportunities to reduce costs

� Many Indonesian Coal mines have quite small “hands on” management teams so cost saving initiatives need to be fostered at the coal face itself

� Generally the largest single cost item for miners is contracting costs and therefore provides greatest opportunity for savings

COST REDUCTIONTARGETS

7

provides greatest opportunity for savings

� Cost reduction via lowering of stripping ratio – the key is balancing maximum coal resource recovery to avoid “glory holing”

� Reduction in rates themselves – may not be palatable to the contractors but sustainability of the mine and the contractors is key to long term partnerships

� Experience has shown that “transparency” will assist with negotiations

� Mutual Fairness – rates could be “coal index linked” so each party can share the benefits in a better market

� The “weak link” in the chain is failure to adhere precisely to the production plan –coal inventory “what you want and when you need it”

For

per

sona

l use

onl

y

• Mine Optimisation

� Revisit mine planning – sometimes a fresh set of eyes can provide opportunities

� Indonesia has a large range of competent and experienced consultants

� $$$ spent in the planning stage can provide substantial multiples in the mine

� Maximise coal quality blending for maximum price yield

COST REDUCTIONTARGETS

8

• Continuous Improvement

� Safety is paramount – safe mines are the most productive mines

� Vigilance in the mine – reduce coal losses and regular reconciliations

� Working with contractors to reduce downtime to allow more “effective” operating hours

ExplorationGeological

Modeling

Mine

Planning

Production

Scheduling

For

per

sona

l use

onl

y

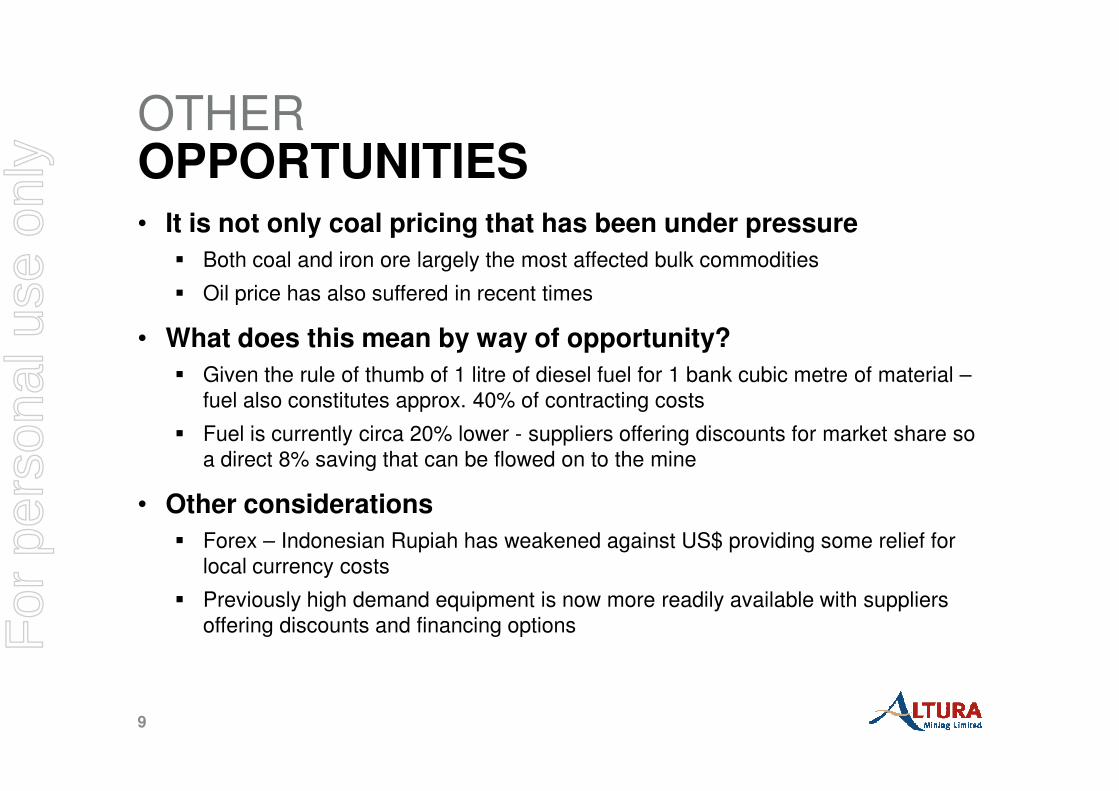

• It is not only coal pricing that has been under pressure

� Both coal and iron ore largely the most affected bulk commodities

� Oil price has also suffered in recent times

• What does this mean by way of opportunity?

� Given the rule of thumb of 1 litre of diesel fuel for 1 bank cubic metre of material –fuel also constitutes approx. 40% of contracting costs

OTHER OPPORTUNITIES

9

fuel also constitutes approx. 40% of contracting costs

� Fuel is currently circa 20% lower - suppliers offering discounts for market share so a direct 8% saving that can be flowed on to the mine

• Other considerations

� Forex – Indonesian Rupiah has weakened against US$ providing some relief for local currency costs

� Previously high demand equipment is now more readily available with suppliers offering discounts and financing optionsF

or p

erso

nal u

se o

nly

• Regulators and producers better understand the market

� Potential increases in levies and taxes will add further pressure to producers

� Indonesian regulators have often modified regulations to match circumstance –industry bodies lobbying for deferment of any new taxes or levies

� New permits such as Registered Exporter (ET) licencing in order to reduce incidence of illegal coal entering the market

MOVING FORWARD SUSTAINABILITY

10

• Who is best suited to thrive

� Indonesia has several key advantages over other coal producing countries -location to market, efficient and cost effective river transport system, skilled and ample labour force and lower capital and operating costs over key competitors

� Established miners with in-place infrastructure that can maintain current cost structures are best suited to thrive in the current market

� High calorie coal producers will be at a distinct advantage as Indonesia’s predicted overall coal energy is reduced over the medium to long term

� Miners that continue to reduce debt during lower interest rate periods

For

per

sona

l use

onl

y

• The new millennium has provided extreme contrasts

� Record coal prices ushered in a new level of mine development

� Shareholders expecting a greater return on investment – are we expecting too much in regards to dollars per tonne margin?

� Increased focus from environmental groups to curb development of coal fired power stations

MANAGING EXPECTATIONS

11

� The communities we work in expect us to deliver better outcomes for them

• The positives

� The industry has seen highs and lows in the market previously – record production levels shows it can adapt and expand

� Demand is there and will remain for some time – growth forecasts are positive

� More sustained view for mining operations – innovative miners looking towards maximising coal resource recovery

� Industry focus on delivering coals with reduced emissions and lower environmental impact – clean coal technology development

For

per

sona

l use

onl

y

THANK YOU.QUESTIONS?

12

For

per

sona

l use

onl

y