This article was downloaded by: [McGill University Library] On: 28 September 2012, At: 14:06 Publisher: Routledge Informa Ltd Registered in England and Wales Registered Number: 1072954 Registered office: Mortimer House, 37-41 Mortimer Street, London W1T 3JH, UK Journal of East-West Business Publication details, including instructions for authors and subscription information: http://www.tandfonline.com/loi/wjeb20 The Virtues and Weaknesses of Insider Shareholding Olga Kuznetsova & Andrei Kuznetsov Version of record first published: 12 Oct 2008. To cite this article: Olga Kuznetsova & Andrei Kuznetsov (2001): The Virtues and Weaknesses of Insider Shareholding, Journal of East-West Business, 6:4, 89-106 To link to this article: http://dx.doi.org/10.1300/J097v06n04_06 PLEASE SCROLL DOWN FOR ARTICLE Full terms and conditions of use: http://www.tandfonline.com/page/terms- and-conditions This article may be used for research, teaching, and private study purposes. Any substantial or systematic reproduction, redistribution, reselling, loan, sub-licensing, systematic supply, or distribution in any form to anyone is expressly forbidden. The publisher does not give any warranty express or implied or make any representation that the contents will be complete or accurate or up to date. The accuracy of any instructions, formulae, and drug doses should be independently verified with primary sources. The publisher shall not be liable for any loss, actions, claims, proceedings, demand, or costs or damages whatsoever or howsoever caused arising directly or indirectly in connection with or arising out of the use of this material.

Transcript

This article was downloaded by: [McGill University Library]On: 28 September 2012, At: 14:06Publisher: RoutledgeInforma Ltd Registered in England and Wales Registered Number: 1072954Registered office: Mortimer House, 37-41 Mortimer Street, London W1T 3JH,UK

Journal of East-West BusinessPublication details, including instructions forauthors and subscription information:http://www.tandfonline.com/loi/wjeb20

The Virtues and Weaknesses ofInsider ShareholdingOlga Kuznetsova & Andrei Kuznetsov

Version of record first published: 12 Oct 2008.

To cite this article: Olga Kuznetsova & Andrei Kuznetsov (2001): The Virtues andWeaknesses of Insider Shareholding, Journal of East-West Business, 6:4, 89-106

To link to this article: http://dx.doi.org/10.1300/J097v06n04_06

PLEASE SCROLL DOWN FOR ARTICLE

Full terms and conditions of use: http://www.tandfonline.com/page/terms-and-conditions

This article may be used for research, teaching, and private study purposes.Any substantial or systematic reproduction, redistribution, reselling, loan,sub-licensing, systematic supply, or distribution in any form to anyone isexpressly forbidden.

The publisher does not give any warranty express or implied or make anyrepresentation that the contents will be complete or accurate or up todate. The accuracy of any instructions, formulae, and drug doses should beindependently verified with primary sources. The publisher shall not be liablefor any loss, actions, claims, proceedings, demand, or costs or damageswhatsoever or howsoever caused arising directly or indirectly in connectionwith or arising out of the use of this material.

[Haworth co-indexing entry note]: “The Virtues and Weaknesses of Insider Shareholding.” Kuznetsova,Olga, and Andrei Kuznetsov. Co-published simultaneously in Journal of East-West Business (InternationalBusiness Press, an imprint of The Haworth Press, Inc.) Vol. 6, No. 4, 2001, pp. 89-106; and: Russian Corpora-tions: The Strategies of Survival and Development (ed: Andrei Kuznetsov) International Business Press, animprint of The Haworth Press, Inc., 2001, pp. 89-106. Single or multiple copies of this article are available fora fee from The Haworth Document Delivery Service [1-800-342-9678, 9:00 a.m. - 5:00 p.m. (EST). E-mailaddress: [email protected]].

After years of painful reforms the Russian version of the market remainsdistorted and crippled in comparison to western counterparts. In its presentform it looks quite unconventional and yet it is not uncommon that standardconcepts reflecting the realities of mature markets are heavily relied upon as abasis for the analysis of the Russian economy.1 Sometimes this may lead to themisrepresentation of certain trends. This article seeks to demonstrate that thethreat of shareholders-insiders to the success of restructuring of Russian cor-porations may be easily exaggerated if no proper attention is paid to the pecu-liarities of the Russian business circumstances. The analysis is conducted fromthe prospective of social cost and social benefit within the constraints of a tran-sitional environment.

The article challenges the opinion that insiders necessarily represent a threatto the speed and advancement of reforms and the introduction of an efficientgovernance model in Russian firms. It claims that the weakness of institutionsprevents insider shareholders from imposing their interests and objectives ei-ther as shareholders or as stakeholders. Insider shareholding has not stopped ordelayed restructuring if restructuring is defined as the ability of the businessorganization to adapt to the requirements of the existing business environment.The survival of the thousands of businesses in Russia based on former Sovietstate-owned enterprises is the evidence that cannot be disputed. Further alter-ations in the economic environment will force economic agents to continue toremodel their conduct and organizational arrangements, but not before theyfeel pressure (either external or internal, or both) for changes.

The transitional economic system is immature from the market prospective.It suffers from loose ties between economic players and the poor quality ofeconomic information, which often lacks sufficient transparency even in themost basic business matters. Institutional deficiency makes it puzzling formarket participants to choose priorities and adjust behavior. In turn, the stu-dents of transition meet with difficulties evaluating the full range of the aggre-gate benefits and losses caused by agent’s behavioral preferences. The modernRussian corporate system is contradictory but it is not as damaging to the eco-nomic performance of corporations as is claimed sometimes (see for exampleDesai and Golgberg, 2000). Russian companies have proved their ability tocope with the situation of institutional failure applying the strategy of evasionand calculated avoidance of long-term commitments. The social benefit ofstrategies and behavior responses chosen by the firms outbalance the uninspir-ing pure economic results calculated in terms of the volume of output or GDPgrowth.

90 Russian Corporations: The Strategies of Survival and Development

Dow

nloa

ded

by [

McG

ill U

nive

rsity

Lib

rary

] at

14:

06 2

8 Se

ptem

ber

2012

RUSSIAN CORPORATIONS:INDISTINCT ENTITIES

WITH AN UNCERTAIN MISSION

Introducing Corporate Governance

It is widely acknowledged that modern corporations have great influence onmany aspects of the modern society following the scale of their activities, the po-litical influence they have achieved, their contribution to the national welfareand the internationalization of their operations. In countries like Britain and theUSA, for example, the value of listed companies exceeds national GDP. Conse-quently, a better understanding of the rationale which guides corporations isimportant to reconcile the interests of corporations and the society and makeeconomic policies more sensible. There is increasing support in the literatureto the claim that corporations should contribute to economic growth thatmakes possible sustainable, equitable and democratic development (Stiglitz,1998; Nellis, 1999; Fox and Heller, 1999). In other words, there is growing ap-preciation of the social consequences of economic activities.

One of the forces that allegedly influence corporations is the shareholder.From the point of view of the society shareholders are responsible for impos-ing on corporate management the requirements of socially meaningful effi-ciency by demanding a fair return on their assets. This argument was used tojustify mass privatization in Russia. However, shareholders may fulfil their so-cial function only in the presence of a certain institutional infrastructure in-cluding statutory law and regulations. This infrastructure reflects the concernsof the society regarding corporations and allows shareholders to implement asocial function while pursuing their own interests. Such infrastructure wasmissing in Russia when mass privatization was launched and currently, tenyears later, it is still very much not in place. Obviously, this is bound to havevery serious consequences as far as the forces affecting corporate governanceare concerned. Effectively, privatization and newly evolved ownership pat-terns have produced a transitional version of the corporate system, which doesnot require sophisticated market infrastructure and can use expertise devel-oped in the Soviet period.

The weakness of this arrangement is that the Russian society remains de-prived of substantive economic advantages that the corporate system devel-oped in the West has to offer. The most prominent areas of concern forbusiness people and academics alike are the lack of transparency in the oper-ations of joint-stock companies, neglect of shareholders rights, the poorcompatibility of the government economic policy with the needs of the busi-ness community (let alone the population who possess a significant fraction

Olga Kuznetsova and Andrei Kuznetsov 91

Dow

nloa

ded

by [

McG

ill U

nive

rsity

Lib

rary

] at

14:

06 2

8 Se

ptem

ber

2012

of equity). One of the significant consequences of the inadequate develop-ment of the corporate system is growing public mistrust of market institutions(Isaksson, 1999), the factor that can affect the speed of reforms and increasethe cost of transformation.

The efficiency of corporate governance, seen here as a mechanism translat-ing signals from product and input markets into corporate behavior (Berglöfand von Thadden, 1999), depends on the degree of development of relevantformal and informal institutions. Corporate governance provides the structurethrough which the objectives of the company are set and the means of attainingthose objectives and monitoring performance are determined. This allows cor-porations to respond to the expectations of shareholders but not only them. It isnow widely recognized that “the competitiveness and ultimate success of acorporation is the result of teamwork that embodies contributions from a rangeof different resource providers including investors, employees, creditors andsuppliers” (OECD Principles of Corporate Governance, 1999). Consequen-tially, these contributors will be deeply affected by the corporation’s successor failure. This puts good corporate governance outside the concern of share-holders alone and into a wider domain that includes the stakeholders of thecompany as well.

By tuning the mechanism of corporate governance through legislation andother instruments the society can address particular needs of different stake-holders and increase the chance of a socially responsible conduct by corpora-tions as shareholders can find it individually rational to avoid responsibilityassociated with ownership (Charkham and Simpson, 1999). Russia providesmany examples of the indifference of this sort. This may be explained by theabsence of incentives for a long-term commitment, as the diffusion of sharesamong insiders did not create many shareholders with other than marginal in-fluence and involvement.

Conscious shareholding is a phenomenon sequential to the conditions andrules that guide business activities. It is imperative for a responsible equityholding that companies are focused on their objectives, competitive in opera-tions and accountable for their actions. Therefore, we believe that it is ex-tremely important to examine existing incentives and obstacles affectinginsider’s behavior in modern Russia. Currently very little is known about thecost to the society incurred by the passivity of shareholders-insiders.

Can the Past Be Always Blamed?

The literature quite often blames the legacy of the “pervasive failures” ofthe command economy for the deficiencies of the modern Russian economy(Brada, 1996). The commonality of this attitude warrants some comment. We

92 Russian Corporations: The Strategies of Survival and Development

Dow

nloa

ded

by [

McG

ill U

nive

rsity

Lib

rary

] at

14:

06 2

8 Se

ptem

ber

2012

do not think that it is constructive as far as corporate governance is concernedfor the simple reason that at the micro level there were no or little provisionsfor this type of relations in the Soviet system. However, there was another typeof principle-agent relations at what may be called the macro level that some-times may be mistaken for proper corporate governance.

During the Soviet period the combined (united) public property was offi-cially proclaimed to be inseparable from the combined (united) proprietor, thepublic. Consequently, the national economy was conceived and organized as abig household managed from a single center according to a single plan. Henceat the macro level there was room for agency relations, which were never for-mally acknowledged by the way, as the public property operated through themechanism of state regulation and control and thus “management” was sepa-rated from the owner. In terms of corporate governance, the state had acquiredthe functions of the topmost manager who should protect the interests of theowner, the public.2 According to theory, however, the manager (the state) re-quires some special motivations (be it an incentive scheme of any kind or effi-cient monitoring device) to act in the interest of the owner (the public). Undersocialism the “principle” was deprived of the means of control over “execu-tives” as the state and party bureaucracy had succeeded in erecting an insur-mountable barrier between themselves and the people. As a result, social andwelfare goals and other elements of the public utility function were neversought to be maximized. The major consequence was an economic structureproviding little resources for the production of consumer services and goodswhile concentrating them openly or indirectly in heavy industries and militarysectors instead.3

These speculations suggest that it is only with serious reservations that “badinheritance” may be accepted as the source of the malformation of the instituteof corporate governance in modern Russia. The “micro-level” corporate gov-ernance in Russia is to be created from scratch and this is a historical opportu-nity that should not be mishandled.

Deceitful Present

In Russia, as everywhere, the economic environment imposes rigorous con-straints on the behavior of corporations. What makes the situation unique is theintermediate nature of the economy itself: “most of the Russian economy hasnot been making progress toward the market or even marking time. It is ac-tively moving in the opposite direction” by choosing to protect itself againstthe market contrary to the option of accepting it (Gaddy and Ickes, 1998).

In transitional Russia, corporations emerged out of state-owned enterprises.The majority of the latter were immensely big and enjoyed monopolistic ad-

Olga Kuznetsova and Andrei Kuznetsov 93

Dow

nloa

ded

by [

McG

ill U

nive

rsity

Lib

rary

] at

14:

06 2

8 Se

ptem

ber

2012

vantages. Organizationally and technologically they were tailor-made to fit avery specific economic system. It did not incorporate, like modern capitalisteconomies, highly developed agency relations. There were no stimuli for thedevelopment of certain economic institutions that in western counties alleviatetransaction costs in order to overcome externalities of the agency. These insti-tutions, as pointed out by Stiglitz (1999), need to grow incrementally and re-quire decades to evolve. Obviously, Russian firms cannot postpone theiroperation till after this process is complete. It is no wonder then that in circum-stances of institutional uncertainty, which are more propitious for stealing thenproducing, less complicated relations and organizational forms prove to bemore attractive. In practice this means that in the situation of institutional col-lapse a governance system that requires less advanced institutional support canbe more efficient as a tool of running a firm then more sophisticated arrange-ments. An organization prevailed by insiders who have obtained ownershiprights without incurring any cost or putting in a noticeable effort may well besuch an initial form of corporation. Organizationally, it has not moved faraway from its predecessor, the state-owned enterprise, and therefore could bemanaged with existing expertise.

DISAMBIGUATING TRANSITIONAL CHALLENGES

To set up the point of reference for our further analysis we have to evaluatethe developments in the area of corporate governance from the point of view oftheir contribution to the success of market reforms. It is necessary to decidefirst what should be counted as a positive result and what as negative. We needto identify then whether what has been achieved is in any relation to a particu-lar model of corporate governance or whether the role of corporate governancewas no more then figurative.

However, the success or failure of reforms cannot be evaluated in economicterms alone. Post communist transition is as much about emerging societies asit is about emerging economies. We agree with Birman (1996) and Stiglitz(1999) who emphasize that the creation of a market economy should beviewed as a mean to secure broader objectives. As Stiglitz (1999, p.12) wrote:“It is not just the creation of a market economy that matters, but the improve-ment of living standards and the establishment of the foundations of sustain-able, equitable, and democratic development.” Therefore the development ofsocial norms and institutions, social capital and trust are critically important aswell. The design of economic objectives should reflect socially acceptable val-ues. At the same time the definition of a socially responsible behavior for cor-porations will have different meaning and scope in a mature market economy

94 Russian Corporations: The Strategies of Survival and Development

Dow

nloa

ded

by [

McG

ill U

nive

rsity

Lib

rary

] at

14:

06 2

8 Se

ptem

ber

2012

and a transitional economy. A distinct feature of the latter is that the institutionaldisorder contributes heavily to the complexity of the business environment asthe “rules of engagement” are not clearly set. Under these circumstances, it ismore difficult to formulate and make noticeable social demands for businessas well as allocate responsibility for their fulfillment.

Successful corporate performance is the justification of and the remunera-tion for efficient corporate governance. With regard to economies in transitiona number of important questions have never been answered (and possibly havenever been asked): What is the social criterion (i.e., shared by the society dur-ing a particular historical period) of the efficient corporation in terms ofachievements, responsibility and conduct? If the mass privatization in Russiawas launched with the purpose to create preconditions for democracy, has itled to establishing corporations capable of assuming socially justifiable eco-nomic policies? How can corporate governance help corporations in achievingsocially significant goals?

Russian mass privatization was first and foremost politically motivated.There was talk about “liberating” the market forces and creating “effectiveowners” in the interests of the best employment of assets (Chubais andVishnevskaya, 1993), but these developments were compromised as the re-formers showed little concern for putting together the infrastructure and insti-tutions of the market. As it happened, the “liberation” made rich a very smallgroup of people, while enterprises and their employees were left to struggle forsurvival. The class of “effective owners” has failed to become prominent. AsCharkham and Simpson (1999) put it, the possession of an umbrella is not thesame as the ownership of British Telecom shares. The latter requires matchinginstitutions and mechanisms. In their absence, it is little surprise that newly-created corporations in Russia have offered so far no definitive proof of the su-periority of the market mechanism of resources allocation over central plan-ning: the absolute majority of privatized firms are poor performers or lossmakers. Most “prosperous” companies belong to natural monopolies and canhardly be evidence of the success of the new order.

In Russia, the performance of privatized firms defies theoretical forecasts,prognosticating that the output dynamics in transitional countries would fol-low a U-shaped curve (Blanchard, 1997). Most firms retain excessive laborand invest inefficiently (Kapelyushnikov, 1998; Batyaeva and Aukutsionek,1999). Many are closed joint stock companies, just few hundred are listed onthe stock exchange and only dozens see any trading in their shares. In this con-text the expression “to go public” has acquired certain irony when applied toRussian corporations. They are not particularly keen on any disclosure and id-iosyncratic to the “more transparency” claim, which instead of recalling asso-ciation with external investors, make them think about bankruptcy.

Olga Kuznetsova and Andrei Kuznetsov 95

Dow

nloa

ded

by [

McG

ill U

nive

rsity

Lib

rary

] at

14:

06 2

8 Se

ptem

ber

2012

The delay in institution building has obviously created additional difficul-ties for the advancement of reforms. Firms reacted by opting for a survivalstrategy based on the calculated avoidance of long-term commitments andstructural adjustments for the sake of a short-term gain. The society dependson corporations but lack of the mechanisms of corporate control interfereswith establishing understanding and trust between the two. More scrupulouseconomic policy and new institutions are required to merge business interestsand the societal interest in sustainable development.

SHARE OF SHARES OR SHARE OF CONTROL?

Changes in the Structure of Shareholding

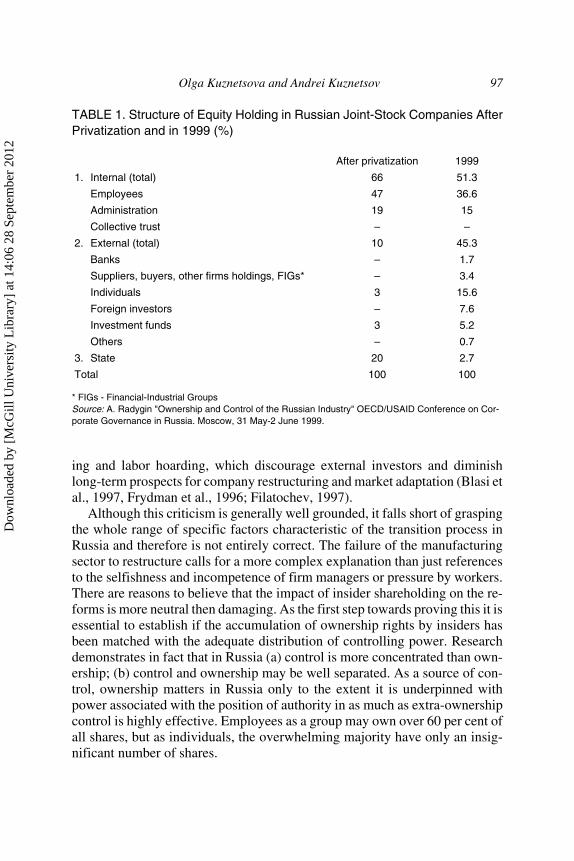

Let us turn to the issue of Russian corporation’s progress in terms of owner-ship structure and performance. The privatization procedures advantaged in-siders. As a result, employees usually hold the largest cut of shares (Table 1).

Since the end of the mass privatization the distribution of shares betweeninsiders has been shifting in favor of managers. The proportion of externalshareholders remains low despite some noticeable growth.4 Institutional in-volvement has not taken off yet. Banks generally show little interest inshareholding although a few of them have become centers of substantial finan-cial-industrial groups. The state remains a prominent shareholder in a consid-erable number of firms.

Firm managers are a particularly prominent group of shareholders. Accord-ing to some sources, initially they acquired about 7% of all equity distributedduring privatization in Russia. In consequent years this share increased to up to10-12% and in some cases incumbent managers reserved for themselves up to50% of the company’s shares (Jones, 1998; Blasi and Shleifer, 1996). Our ownanalysis of the data collected by REB reveals a similar trend: managementstaff as a group own on average 33% of shares.

The implications of the prevalence of insiders are manifold. First, it set up abackdrop for the development of the system of corporate governance in thecountry. Second, it highlighted the conflict of interests between sharehold-ers-insiders and shareholders-outsiders. Third, this created an environment fa-vorable for integrating the interests of different groups of insiders at leastduring the early phase of the evolution of corporate governance in Russia.Forth, privatization legitimized the influence and control acquired by “Red Di-rectors” during the pre-reforms era.

Theorists are generally quite critical about the structure of corporate owner-ship in Russia. It is believed to have led to managerial entrenchment, rent seek-

96 Russian Corporations: The Strategies of Survival and Development

Dow

nloa

ded

by [

McG

ill U

nive

rsity

Lib

rary

] at

14:

06 2

8 Se

ptem

ber

2012

ing and labor hoarding, which discourage external investors and diminishlong-term prospects for company restructuring and market adaptation (Blasi etal., 1997, Frydman et al., 1996; Filatochev, 1997).

Although this criticism is generally well grounded, it falls short of graspingthe whole range of specific factors characteristic of the transition process inRussia and therefore is not entirely correct. The failure of the manufacturingsector to restructure calls for a more complex explanation than just referencesto the selfishness and incompetence of firm managers or pressure by workers.There are reasons to believe that the impact of insider shareholding on the re-forms is more neutral then damaging. As the first step towards proving this it isessential to establish if the accumulation of ownership rights by insiders hasbeen matched with the adequate distribution of controlling power. Researchdemonstrates in fact that in Russia (a) control is more concentrated than own-ership; (b) control and ownership may be well separated. As a source of con-trol, ownership matters in Russia only to the extent it is underpinned withpower associated with the position of authority in as much as extra-ownershipcontrol is highly effective. Employees as a group may own over 60 per cent ofall shares, but as individuals, the overwhelming majority have only an insig-nificant number of shares.

Olga Kuznetsova and Andrei Kuznetsov 97

TABLE 1. Structure of Equity Holding in Russian Joint-Stock Companies AfterPrivatization and in 1999 (%)

After privatization 1999

1. Internal (total) 66 51.3

Employees 47 36.6

Administration 19 15

Collective trust – –

2. External (total) 10 45.3

Banks – 1.7

Suppliers, buyers, other firms holdings, FIGs* – 3.4

Individuals 3 15.6

Foreign investors – 7.6

Investment funds 3 5.2

Others – 0.7

3. State 20 2.7

Total 100 100

* FIGs - Financial-Industrial GroupsSource: A. Radygin "Ownership and Control of the Russian Industry" OECD/USAID Conference on Cor-porate Governance in Russia. Moscow, 31 May-2 June 1999.

Dow

nloa

ded

by [

McG

ill U

nive

rsity

Lib

rary

] at

14:

06 2

8 Se

ptem

ber

2012

What is clear is that small shareholders have little power to influence corpo-rate policy and that they are restricted in their ability to exercise their ownrights in full. It would be naïve, then, to expect shareholders not to be aware ofthis and adjust their behavior accordingly. There are only few examples ofshareholders-employees to take consorted action. Mostly this category ofshareholders is quite inert, possibly because the cost of monitoring managers istoo high for dispersed shareholders in the atmosphere of secrecy prevailing inRussia.

Dispersed shareholding requires more rigorous institutional support to beconsequential. In Russia, however, the mechanism of the legal protection ofshareholder rights is still in infancy and the culture of equity holding is lacking.In any corporate system, the ability of small shareholders to exercise control isnegligible unless they find ways to agree on common goals and act jointly toachieve them (Carberry, 1996). In Russia, small shareholders have even fewerresources and incentives to execute their right of control over corporate assetsand policy (Kuznetsov and Kuznetsova, 1996). Therefore, it is not the insiders’shareholding that represents a real threat to the success of reforms, but the defi-ciency of institutions providing support to scattered shareholding.

Employee Ownership?

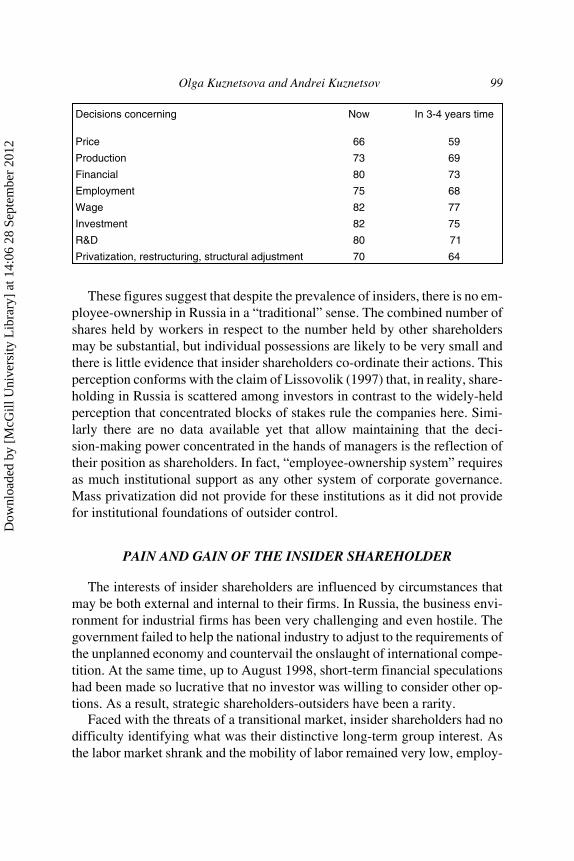

In joint-stock companies, the distribution of ownership rights is not equal tothe distribution of control. Hence, a simple reference to the total share of theequity allocated to insiders does not get one really far in understanding the bal-ance of forces as far as the controlling power of various groups of shareholdersis concerned. Besides, there is evidence in the literature (Carberry, 1996) thatan extensive employee ownership does not usually translate into employee in-volvement in corporate-level decisions; their voting rights are rarely used as ameans to gain influence; even when employees do have a significant role ingovernance, this does not lead to drastic changes in corporate policy. We triedto find evidence in REB surveys that workers abused their shareholder rightsand influenced the firm policy so as to protect their interests as stakeholders(i.e., the firm’s employees). As REB data show, enterprises with labor over-hang mention pressure from workers-shareholders as an obstacle for redun-dancies in no more then five per cent of cases (Kapelyushnikov, 1998). In thefirst half of 1999, with the assistance of REB, we approached 116 firms withthe question, “Who does define the priorities in areas related to the perfor-mance of the firm?” The respondents (enterprise managers) were asked to put100 if the director of the enterprise is solely responsible for the decisions and 0if he is not involved in the process of decision-making at all. The results showthat directors enjoy almost unchecked discretion in decision-making:

98 Russian Corporations: The Strategies of Survival and Development

Dow

nloa

ded

by [

McG

ill U

nive

rsity

Lib

rary

] at

14:

06 2

8 Se

ptem

ber

2012

These figures suggest that despite the prevalence of insiders, there is no em-ployee-ownership in Russia in a “traditional” sense. The combined number ofshares held by workers in respect to the number held by other shareholdersmay be substantial, but individual possessions are likely to be very small andthere is little evidence that insider shareholders co-ordinate their actions. Thisperception conforms with the claim of Lissovolik (1997) that, in reality, share-holding in Russia is scattered among investors in contrast to the widely-heldperception that concentrated blocks of stakes rule the companies here. Simi-larly there are no data available yet that allow maintaining that the deci-sion-making power concentrated in the hands of managers is the reflection oftheir position as shareholders. In fact, “employee-ownership system” requiresas much institutional support as any other system of corporate governance.Mass privatization did not provide for these institutions as it did not providefor institutional foundations of outsider control.

PAIN AND GAIN OF THE INSIDER SHAREHOLDER

The interests of insider shareholders are influenced by circumstances thatmay be both external and internal to their firms. In Russia, the business envi-ronment for industrial firms has been very challenging and even hostile. Thegovernment failed to help the national industry to adjust to the requirements ofthe unplanned economy and countervail the onslaught of international compe-tition. At the same time, up to August 1998, short-term financial speculationshad been made so lucrative that no investor was willing to consider other op-tions. As a result, strategic shareholders-outsiders have been a rarity.

Faced with the threats of a transitional market, insider shareholders had nodifficulty identifying what was their distinctive long-term group interest. Asthe labor market shrank and the mobility of labor remained very low, employ-

ees had a vested interest in keeping their enterprise operational, as they re-garded it as the provider of the means for their livelihood. Noticeably, thesemeans never came as dividends or return on the sale of shares, because as arule, shares are not liquid and dividends have never been either paid or, if paid,significant. Wages, although often delayed, and benefits in kind provided byenterprises determined that the interests of insiders as employees overwhelmedtheir interests as shareholders. This situation was likely to urge them to supportdecisions that would make them better off as stakeholders while probablymaking them worse off as shareholders.

Privatization did not change organizational routines much, except that theperspectives of managerial employment became conditional to a slightly dif-ferent set of regulations and arrangements. Experience and authority gained byincumbents under central planning has not lost its relevance completely, inas-much as old skills are better than none, but more importantly, because sluggishreforms failed to make these skills obsolete. According to our data, the averagenumber of years current directors were in charge in the surveyed enterpriseswas nine and their average age was 50. Understandably, in the absence of aproper job market for this category of specialists, the opportunity for horizon-tal or vertical job mobility is extremely restricted. Our survey indicates onlyvery limited turnover among management staff, the only significant reasonsfor dismissal revealed being retirement age and voluntary withdrawal. Underthese circumstances, the protection of their own status has become a strongmotivation of managerial behavior and, often, opportunism. This implies thechoice between two possible types of conduct. One, the “survival” type of re-sponse, will aim at keeping the company afloat at any cost, gaining support ofthe work collective and important stakeholders. The other will seek to exploitshort-term opportunities supplied by the infant market and prioritize assetsstripping and rent-seeking, usually with deadly consequences for the firm con-cerned.

Interestingly, managers who started their jobs in the 1990’s demonstratesimilarity to the pre-reform generation of directors in values, behavioral normsand even priorities. Moreover, the share of managers with revealed pro-marketorientation, although small overall, is higher in those enterprises in which oldmanagement was retained (Aukutsionek, 1997). This is a strong piece of evi-dence in favor of the claim that social and economic constraints determinemanagerial attitudes in the first place. At the same time, there is little manifes-tation that either managers or workers who gained a major share of equity capi-tal during privatization have acquired awareness characteristic of shareholdersin the West (Blasi et al., 1997). Managers and workers of privatized firms ap-pear to share interests more as stakeholders rather than shareholders as for themajority of employees equity ownership is little more than a formality which,

100 Russian Corporations: The Strategies of Survival and Development

Dow

nloa

ded

by [

McG

ill U

nive

rsity

Lib

rary

] at

14:

06 2

8 Se

ptem

ber

2012

at least at present, has hardly any impact on their life. In Russia, the rights tovote do not necessarily secure economic benefits associated with shareholding,as a shareholder retains proportional voting rights, which do not necessarilycorrespond to the company’s value. Even large investors owning a blockingminority stake in a company find it difficult to enforce proportional economicinterest (Corporate Governance in Russia, 1999).

In fact, post-communist privatization caught the employees and managersof state-owned enterprises as unprepared as the rest of the population. In theWest, the decision to buy out is taken by interested parties voluntarily, either tofacilitate the restructuring of troubled firms, or to release efficiencies which re-quire the full commitment of insiders (Thompson and Wright, 1995). By con-trast, in transition economies, to name just a few differences, “buy outs” wereimposed by governments on sound and ailing firms alike, on political grounds,mainly. For the insiders, becoming owners of their enterprises was not somuch the issue of increasing efficiency and returns as preserving their verylivelihood in a hostile and uncertain environment. In a short run, financial in-centives appear to be of less interest for Russian managers than the consider-ations of securing their own position in the hierarchy of the newly privatizedfirm.

FROM CONTINGENCY TOWARDS PROBABILITY

It is common that the efficiency of firms controlled by insiders is put inquestion in the literature on the grounds that they lack mechanisms to checkthe possible abuse of power by managers. This argument loses some of its poi-gnancy in countries like Russia, in which such mechanisms are equally absentin firms under outsider control as well, following the general paralysis of thelaw enforcement system. The impact of legal regulation depends not so muchon what is regulated but on what can be enforced: if the enforcement instru-ments are missing, legal protection is of little help to those entitled. The po-tency of the legal system is just one example of forces external to the firm thatare instrumental in shaping the pattern of control allocation within the firm. Ifthese forces fail to make their impact noticeable, the internal structures of thefirm must assume functions that would allow it to adapt to such failure. Theymay also be forces to assume some faculties, which are plethoric for them andwould be placed elsewhere in other situations. This enhances the role of insid-ers while making them less receptive to signals from outside their organiza-tion. With this, the scope of the social responsibility of corporations getsnarrower and reflects the interests of those internal to the corporations or

Olga Kuznetsova and Andrei Kuznetsov 101

Dow

nloa

ded

by [

McG

ill U

nive

rsity

Lib

rary

] at

14:

06 2

8 Se

ptem

ber

2012

strongly associated with them. In other words, the situation favors stake-holders.

That stakeholders appear to have a stronger grip over firms than sharehold-ers is often regarded as a serious weakness of the system of corporate gover-nance in Russia. The domination of top managers in particular is seen as amajor setback for reforms. But as soon as one accepts that a survival strategyhas been a prime option for Russian firms as determined by the economic envi-ronment, the evaluation of managerial performance shifts its emphasis. Thedrive of top managers towards concentrating economic power emerges as a ra-tional choice motivated by the weakness or absence of some important marketinstitutions and operational systems, in particular, that shareholders as formalowners are not able to take a lead as a strategic force. By contrast, the interestof stakeholders is more emphatic. Under these circumstances, what may ap-pear as “the abuse of power” in terms of standard organizational theory comesout as a rational response to existing constraints. These constraints include,apart from the weakness of market institutions mentioned earlier, the conser-vation of many features of the pre-reform economic mechanism. The paradoxof the Russian corporate system is that, due to inconsistent reforms, the mecha-nisms of the market are still too inadequate to subdue firms to their disciplinethus leaving them to rely on now obsolete practices, as well as the intuition andthe experience of managers. Actually, dependence on networks and kin ties,avoidance to rise capital from outside the company is not a Russian-specificfeature but a common type of behavior brought about by the inoperative forcommercial purposes environment (Miwa and Ramseyer, 1999). It is not im-possible that concentration of shares in the hands of insiders and managers inparticular will have a positive impact in a long run. Shareholding encouragesthe development of a long-term commitment to the firm and may interfere withthe impulses pushing towards funneling resources and assets stripping. Whatwill tip the balance is the success in putting together institutions that will pro-vide the shareholders with the mechanisms of monitoring and intervention,thus facilitating owner’s control, whatever the ownership structure.

CONCLUSIONS

A more balanced approach to the impact on transition of insider share-holding is necessary if the full account is taken of the fact that Russia lacks abasic market infrastructure and regulatory framework. Market institutions andmarket relations, such as the contract, for example, often bear only superficialresemblance to their counterparts in mature market conditions.

102 Russian Corporations: The Strategies of Survival and Development

Dow

nloa

ded

by [

McG

ill U

nive

rsity

Lib

rary

] at

14:

06 2

8 Se

ptem

ber

2012

Privatization made self-defense the motor of managerial behavior. To sup-port the continuation of their tenure managers had no choice but to seize theleadership by concentrating efforts on enterprise survival, reaching the internalconsensus and consolidating power through personal shareholding. In ad-vanced capitalist countries the allocation of shares to managers is used nor-mally to set additional incentives for managerial performance. By contrast forRussian managers owning stocks is neither incentive, nor compensation.

Furthermore, they have to respond to a very specific economic environmentcharacterized inter alia with the following features:

• the collapse of the national economy has turned Russia to a great extentinto a “moneyless society” as over 50 per cent of all transactions betweenfirms take place in a form of barter;

• employees are either not paid wages for months or urged to take the prod-ucts of their firms as payment;

• the stock market is not an instrument that helps capital to flow to the mostattractive sectors of the economy from the least attractive. A World Bankpublication (Lieberman, and Kirkness, 1998) points at poor implementa-tion of even basic rules on trading, little or no protection for shareholderrights. With little or no activity in most shares, stock quotations and pricesoften do not reflect the prices at which transactions would take place;

• a new type of ownership was created through the process of voucher dis-tribution. Individuals obtained ownership rights without injecting anycapital of their own, hence, the majority are not investors in the propersense of the word;

• the culture of committed shareholding is missing.

Clearly, these conditions could not but affect the nature of responsibilities ofcorporate executives to their shareholders and the allocation of priorities byfirms with regard to the corporate performance. The distinction between theshareholder and the stakeholder is blurred, as the major group of shareholders isidentical to the major group of stakeholders. At the same time, standard financialindicators like revenue, debt, dividends, the price of shares, due to market ineffi-ciency, become too arbitrary to carry any constructive information. As a result,the role of external shareholders is insignificant as they find it equally difficulteither to make up their mind about company performance or to make their willknown to corporate executives. Meanwhile, with the feeble stock market capa-ble of generating only weak signals, executives are more likely to bow to pres-sures from inside the firm (Kuznetsov and Kuznetsova, 1996).

The following circumstances make managers particularly receptive to in-ternal influences:

Olga Kuznetsova and Andrei Kuznetsov 103

Dow

nloa

ded

by [

McG

ill U

nive

rsity

Lib

rary

] at

14:

06 2

8 Se

ptem

ber

2012

• the paternalistic role traditionally played by Russian managers towardstheir workforce (Clarke, 1995);

• dependence on important local informal networks (Kuznetsova andKuznetsov, 1996);

• susceptibility to coercion on the part of regional government as a resultof the political weakness of the center and inadequate legal protection;

• the questionable legality of ownership rights (Glazyev, 2000);• the realization that the government would be more prepared to bail out

ailing firms if the latter play an important role as providers of social ser-vices to local communities.

With the informational function of the stock market in disarray, control bystakeholders is the only way to keep corporations socially responsive and man-agers accountable. Increasing shareholder’s wealth may be a legitimate crite-rion of efficiency in performing market systems. In the midst of a deepeconomic crisis, Russian firms are preoccupied with survival. Revealed stake-holder’s interests provide managers with a set of socially significant referencemarks within which they are able to maximize the short-term performance oftheir firms but also pursue some social goals, which might not be intrinsically apart of a business enterprise. Paternalism of the Russian managers inheritedfrom the Soviet system has brought about positive results by having smoothedsocial tension and offering shelter to socially exposed citizens. It also substitutesfor otherwise absent informal (like in the USA) or formal (like in Germany) in-ternal structures that allow employees to influence corporate decision-makingfrom the shop floor. REB surveys helped to establish paternalistic attitudes asone of the main factors of labor hoarding at Russian enterprises (Kapelyush-nikov, 1998). The last factor seems to be particularly important having beenmentioned by 51 per cent of respondents.

While the literature on Russian transition routinely criticizes managers forcalculated avoidance of long-term adjustments, the approach taken by this papersuggests that environmental constraints should take their part of blame too. Asfor Russia, existing constraints require that a whole set of definitions must be re-vised if and when they are applied to this country. The very criterion of the effi-cient corporation needs some updating. For example, the one inherent in theAnglo-Saxon paradigm, on the growth of the wealth of shareholders, loses itslure in the Russian context. Managers cannot be expected to fulfil the impossiblemission of pursuing meaningless goals. Further more, the strain of a transitionalprocess places a bias on the issue of social responsibility of corporations, theirability to contribute to the shaping of a new society rather than simply behave“properly” in a new type of economy. Insider shareholding cannot stop or delayrestructuring more than the business environment can stop or delay it.

104 Russian Corporations: The Strategies of Survival and Development

Dow

nloa

ded

by [

McG

ill U

nive

rsity

Lib

rary

] at

14:

06 2

8 Se

ptem

ber

2012

NOTES

1. Thus, Gaddy and Ickes (1998), who found an innovative analytical approach, weremore successful in explaining some unconventional outcomes of the Russian transitionthan many of their colleagues.

2. Such an approach provides another interesting angle for analysis: post-communisttransition as a transformation of a Russian economy as a bankrupt corporation. See:J. Stiglitz and D. Ellerman “New Bridges Across the Chasm: Macro- and Micro-Strat-egies for Russia.” Paper presented at the ECR panel on the Russian economy, January8, 2000, Boston, USA.

3. Igor Birman and Alec Nove contributed immensely to this disclosure.4. There are speculations supported mainly with anecdotal evidence, though, that the

increase of the outsider holdings was the result of cross-holdings with significant man-agerial involvement.

REFERENCES

Aukutsionek, S. (1997). Measuring Progress towards a Market Economy. CommunistEconomies & Economic Transformation, 9 (2), 161-162.

Batyaeva, A. and Aukutsionek S. (1999). Investment and Non-Investment in the Rus-sian Industry. The Russian Economic Barometer, VIII (4), 3-23.

Berglöf, E. and von Thadden E.-L. (1999). “The Changing Corporate Governance Para-digm: Implications for Transition and developing Countries.” Paper presented at theAnnual Bank Conference on Developmemt Economies-Europe (ABCDE) “Gover-nance, Equity and Global Markets,” June 21-23, 1999, Paris.

Birman, I. (1996). Gloomy Prospects for the Russian Economy. Europe-Asia Studies,48 (5), 735-750.

Blanchard, O. (1997). The Economics of Post-Communist Transition. Oxford: Claren-don Press.

Blasi, J.R., Kroumova, M., and Kruse, D. (1997). Kremlin Capitalism. London: Cor-nell University Press.

Brada, J.C. (1996). Corporate Governance in Transition Economies: Lesson from Re-cent Developments in OECD Member Countries. OECD, Paris.

Carberry, E. J. (1996). Corporate Governance In Employee-Ownership Companies.The Corporate Board, September/October, 15-20.

Charkham, J. and Simpson, A. (1999). Fair Shares. The Future of Shareholder Powerand Responsibility. New York: Oxford University Press Inc., 275 pp.

Chubais, A., and Vishnevskaya M. (1993). Main Issues of Privatization in Russia. Re-printed in Åslund A. (ed.) Russia’s Economic Transformation in the 1990’s. Lon-don and Washington: Pinter, 1997.

Clarke, S. (ed.) (1995) Management and Industry in Russia. London: Edward Elgar.Corporate Governance in Russia: Cleaning up the Mess (1999). Troika Dialog Re-

search, May. Moscow, 119 pp.Desai, R.M. and Golgberg, I. (2000). The Vicious Circles of Control. Regional Gov-

ernments and Insiders in Privatized Russian Enterprises. Policy Research WorkingPaper (2247). The World Bank. Europe and Central Asia Region. Private and Fi-nancial Sectors Development Union. Washington, DC, USA, 23 pp.

Filatochev, I. (1997). “Privatization and Corporate Governance” Review Article.World Economy, 20(4), 497-510.

Olga Kuznetsova and Andrei Kuznetsov 105

Dow

nloa

ded

by [

McG

ill U

nive

rsity

Lib

rary

] at

14:

06 2

8 Se

ptem

ber

2012

Fox, M.B. and Heller, M.A.(1999). Lessons From Fiascos in Russian Corporate Gov-ernance (Paper #99-012). University of Michigan Law School, William DavidsonInstitute.

Frydman, R., Gray, C. and Rapaczynski, A. (eds.) (1996). Corporate Governance inCentral Europe and Russia. Vol. 1 and 2–Budapest: CEU Press.

Gaddy, C. and Ickes, B. (1998). Russia’s Virtual Economy. Foreign Affairs. 77(5),53-67.

Glazyev, S. (2000). Interview with Sergei Glazyev, Chairman of the Duma Committeeon Economic Policies and Entrepreneurship. Vek, No. 5 (370), February.

Isaksson, M. (1999). Investment, Financing and Corporate Governance: The Role andStructure of Corporate Governance Arrangements in OECD Countries. OECD,USAID and World Bank Conference. Moscow, 31 May-2 June 1999.

Kapelyushnikov, R. (1998). “Chto skryvaets’a za ”skritoy bezrabotitsey"?" in T.Maleeva (Ed.): State and Corporate Employment Policy. Moscow, Carnegie En-dowment for International Peace, pp. 75-111.

Kuznetsov, A. and Kuznetsova, O. (1996). Privatization, Shareholding and the Effi-ciency Argument: Russian Experience. Europe-Asia Studies, 48(7), 1173-85.

Kuznetsova, O. and Kuznetsov, A. (1996). From a Socialist Enterprise to a CapitalistFirm: The Hazards of the Managerial Learning Curve. Communist Economies &Economic Transformation, 8(4), 517-528.

Kuznetsova, O. and Kuznetsov, A. (1999). The State as a Shareholder: Responsibilitiesand Objectives. Europe-Asia Studies, 51(3), 433-446.

Lieberman, I.W. and Kirkness C.D. (1998). Privatization and Emerging Equity Mar-kets. Washington: World Bank.

Miwa, Y. and Ramseyer, J.M. (1999). The Value of Prominent Directors: Lessons inCorporate Governance from Transitional Japan. Paper presented at the WilliamDavidson Institute, The University of Michigan Law School, September 1999.

Nellis, J. (1999). Time to Rethink Privatization in Transition Economies? Transition,10(1), 4-6.

OECD General Principles of Company Law for Transition Economies (1999). TheJournal of Corporation Law, 24(2) (Winter), 190-293.

OECD Principles of Corporate Governance (1999). OECD, Directorate for Financial, Fis-cal and Enterprise Affairs. Paris. http://www.oecd.org/daf/governance/principles.htm

Thompson, S. and Wright, M. (1995). Corporate Governance–The Role of Restruc-turing Transactions. Economic Journal, 105(430), 690-703.

Stiglitz, J. (1998) More Instruments and Broader Goals: Moving towards the Post-Washington Consensus. WIDER Annual Lecture, The United Nations University,Helsinki.

Stiglitz, J. (1999). Wither Reforms? Ten Years of the Transition. Keynote address atthe Annual Conference of the World Bank on Development Economics, April28-30, Washington.

SUBMITTED: January 2000FIRST REVISION: June 2000

SECOND REVISION: August 2000ACCEPTED: August 2000

106 Russian Corporations: The Strategies of Survival and Development