JOT WWW.IIJOT.COM SPRING 2013 VOLUME 8 NUMBER 2 The Voices of Influence | iijournals.com Investment and Trade Execution in Emerging Markets: Prospects and Challenges BHARAT KUMAR, N. KANNAN, AND LALATENDU KHANDAGIRI

Transcript

JOTW W W . I I J O T . C O M S P R I N G 2 0 1 3 V O L U M E 8 N U M B E R 2

The Voices of Influence | iijournals.com

Investment and Trade Execution in Emerging Markets: Prospects and ChallengesBHARAT KUMAR, N. KANNAN, AND LALATENDU KHANDAGIRI

THE JOURNAL OF TRADING SPRING 2013

Investment and Trade Execution in Emerging Markets: Prospects and ChallengesBHARAT KUMAR, N. KANNAN, AND LALATENDU KHANDAGIRI

BHARAT KUMAR

is a vice president at Eval-ueserve.com Pvt. Ltd. in Haryana, [email protected]

N. KANNAN

is a group manager at Evalueserve.com Pvt. Ltd. in Haryana, [email protected]

LALATENDU KHANDAGIRI

is a senior research lead at Evalueserve.com Pvt. Ltd. in Haryana, [email protected]

The developed world dominated global economic growth over the past century, with giant leaps in industrialization, agricultural prac-

tices, and services. But this has changed in the last 15 years, as illustrated by the GDP growth rates post-1998 in Exhibit 1, which show that emerging markets (EMs) have outperformed developed markets (DMs). Prior to the year 2000, DMs accounted for more than 60% of global GDP, with EMs accounting for the rest. As per IMF forecasts, the outperformance of EMs is expected to continue through 2017, a trend that will see them starting to dominate global GDP in 2013.

In addition to better economic condi-tions, improved policymaking and a stable political environment in the emerging world have helped attract investments. Exhibit 2 looks at the long-term local currency debt rating of major EMs by Standard and Poor’s in 2005 and 2012. Most of the local debt issued by these countries has been rated investment grade or higher (other agencies, such as Fitch and Moody’s, had similar ratings). The ratings of five emerging countries improved in 2012, while those of two countries remained the same. This presents a rather stable environment in emerging countries, which is in contrast to that of developed countries, particularly the Eurozone, which have been subject to rating downgrades in recent times.

Emerging markets are quite large, as measured by their equity market capitaliza-tion. However, the list of the largest exchanges by market capitalization is dominated by developed countries, as shown in Exhibit 3. EMs such as China and India feature among the top 10, and Brazil, South Korea, South Africa, Russia, Taiwan, and Mexico are among the top 20 countries by equity market capitalization.

Exhibit 4 shows private financial f lows into emerging markets. As a result of the fac-tors mentioned above, and as noted earlier, financial f lows into EMs have been consis-tently high. Private financial f lows into EMs picked up in the last decade, with the year 2007 registering the highest f low of close to $700 billion.

OUR METHODOLOGY FOR ANALYSIS

We performed a comparative analysis of select EMs on the basis of a few param-eters. We studied only equity markets and ranked emerging countries on the basis of their domestic equity market capitalization. The top 10 countries were selected for a detailed analysis. In case data were unavail-able for any selected country, it was replaced by the next ranked country by market capitalization.

JOT-KUMAR.indd 45JOT-KUMAR.indd 45 3/13/13 8:44:09 AM3/13/13 8:44:09 AM

INVESTMENT AND TRADE EXECUTION IN EMERGING MARKETS: PROSPECTS AND CHALLENGES SPRING 2013

REGULATORY FRAMEWORK

Historically, many EMs have had closed and/or restricted economies in order to safeguard their domestic business and trade interests. Their trade and economic leg-islation was not robust and led to a series of crises—the Tequila crisis in Mexico (1994), the currency crisis in Brazil (1998–1999), the balance of payments crisis in India (1991), the Russian debt default (1998), and the Asian financial crisis (1997), to name a few. In reaction to these extreme situations, many emerging countries started opening up their domestic economies and establishing and strength-ening their regulatory frameworks. It is interesting to note that these countries have not had any major financial crises in the last decade, except for the impact of the global credit crisis, which originated in the U.S. and Europe in the last few years. We think this is partly due to better policy-making and more robust regulations and market infrastruc-ture, which have been put in place over the last decade.

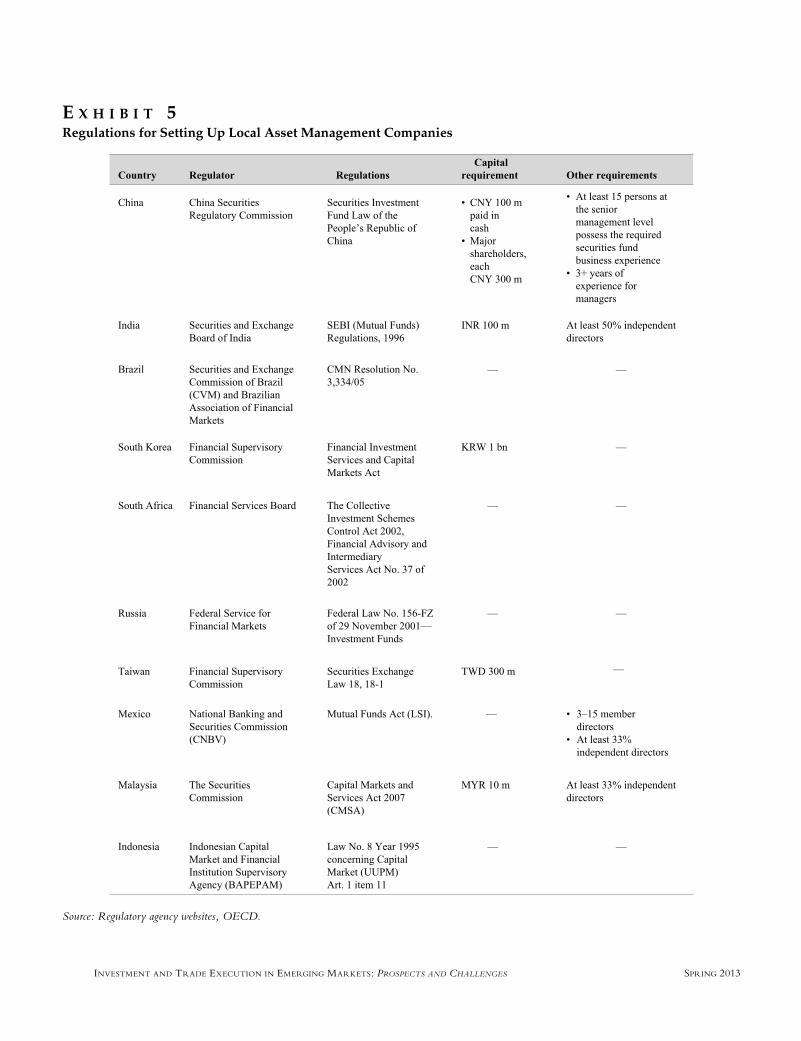

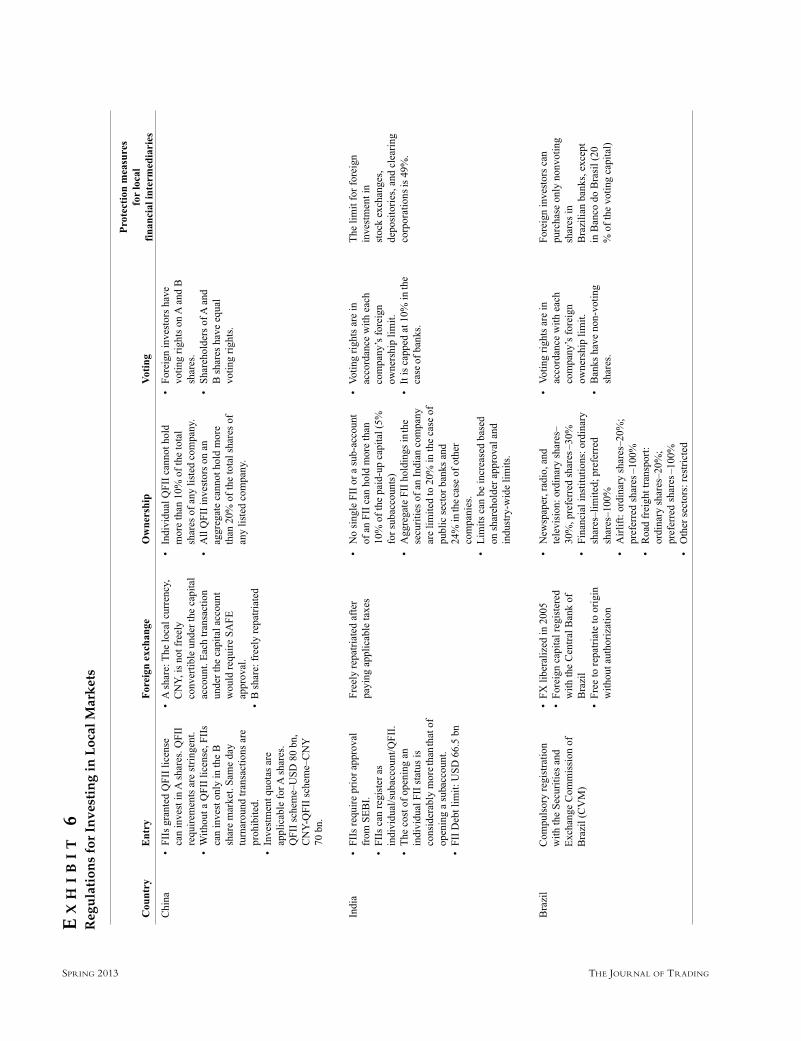

In this section, we address two sets of regulations—those involving setting up local asset management com-panies and those involving investment in local markets for products, such as mutual funds, offered to investors in their own country.

The regulations for establishing a domestic asset management company are illustrated in Exhibit 5, while Exhibit 6 shows the regulations for investing in local mar-kets. Exhibit 7 shows foreign holdings in local equities for 2011.

E X H I B I T 1GDP Growth Rates and Share of EMs and DMs

Source: International Monetary Fund, World Economic Outlook Database, as of October 2012.

Source: Standard and Poor’s, Bloomberg.

E X H I B I T 2Long-Term Local Currency Debt Ratings

JOT-KUMAR.indd 46JOT-KUMAR.indd 46 3/13/13 8:44:09 AM3/13/13 8:44:09 AM

THE JOURNAL OF TRADING SPRING 2013

Across emerging markets, securities market regu-lators are the primary agencies responsible for approval and registration of foreign investors. These regulators play a balancing act by increasing international participa-tion in domestic equity markets but restricting owner-ship in strategic sectors, preventing market disruption, and restricting illegal capital.

Capital controls and foreign exchange transactions are regulated by central banks. Ownership thresholds are generally monitored by securities regulators, but central banks are involved in monitoring ownership in select sectors such as banking.

We identified four factors that would be of primary importance to an institutional investor looking to enter any foreign market.

1. Entry. Relatively easy registration for invest-ment and equal treatment compared with local participants, without limit to the quantum of investment

2. Foreign exchange. Easy entry/exit from markets and transfer of proceeds, absence of capital controls, and well-developed currency markets

3. Ownership. Unrestricted holdings in sectors with attractive investment potential and on par treat-ment with domestic investors

4. Voting. Unrestricted voting rights proportional to institutional investors shareholding, which will give them a say in major business policies of companies invested in.

Subsequently, we analyzed the selected EMs on these parameters. We summarize the results as follows:

• Most of the EMs do not have a fully developed offshore currency market and have restrictions on onshore markets.

• Foreign ownership in domestic equity is restricted by most EMs, which may have resulted in lower foreign participation (see Exhibit 7). Foreign ownership levels in India are the lowest among EMs. A possible reason could be high government ownership in large corporations. The government should look at divesting its stake in such corporations, which can increase foreign ownership and aid capital reserve.

• A few EMs have put a limitation on the voting rights of foreign investors. Such restrictions could be in several forms—limited voting rights in selected sectors (such as banking), separate classes of shares without voting rights, or suspen-sion of voting rights when ownership exceeds the threshold.

• We expect such restrictions to ease off gradually, with the objective of gaining the confidence of foreign investors who would want their rights to be on par with that of local participants.

Source: IMF, World Economic Outlook Database, as of October 2012.

E X H I B I T 4Private Financial Flows into EMs

E X H I B I T 3Market Cap by Exchange

Source: World Federation of Exchanges.

JOT-KUMAR.indd 47JOT-KUMAR.indd 47 3/13/13 8:44:10 AM3/13/13 8:44:10 AM

INVESTMENT AND TRADE EXECUTION IN EMERGING MARKETS: PROSPECTS AND CHALLENGES SPRING 2013

E X H I B I T 5Regulations for Setting Up Local Asset Management Companies

Source: Regulatory agency websites, OECD.

JOT-KUMAR.indd 48JOT-KUMAR.indd 48 3/13/13 8:44:11 AM3/13/13 8:44:11 AM

THE JOURNAL OF TRADING SPRING 2013

EX

HI

BI

T 6

Reg

ula

tion

s fo

r In

vest

ing

in L

ocal

Mar

ket

s

JOT-KUMAR.indd 49JOT-KUMAR.indd 49 3/13/13 8:44:12 AM3/13/13 8:44:12 AM

INVESTMENT AND TRADE EXECUTION IN EMERGING MARKETS: PROSPECTS AND CHALLENGES SPRING 2013

EX

HI

BI

T 6

(C

onti

nued

)

JOT-KUMAR.indd 50JOT-KUMAR.indd 50 3/13/13 8:44:13 AM3/13/13 8:44:13 AM

THE JOURNAL OF TRADING SPRING 2013

Sour

ce:

Wor

ld F

eder

atio

n of

Exc

hang

es,

regu

lato

ry a

genc

y w

ebsit

es,

ww

w.a

siaet

radi

ng.c

om.

EX

HI

BI

T 6

(C

onti

nued

)

JOT-KUMAR.indd 51JOT-KUMAR.indd 51 3/13/13 8:44:14 AM3/13/13 8:44:14 AM

INVESTMENT AND TRADE EXECUTION IN EMERGING MARKETS: PROSPECTS AND CHALLENGES SPRING 2013

INSTRUMENTS, INFRASTRUCTURE, AND OTHER FEATURES OF TRADING

Product offerings in EMs have increased to include all possible exchange-traded equity and equity derivative instruments such as index and single-stock futures and options. Some of the derivatives in emerging markets feature among the most traded in the world, based on the number of contracts and traded value. Exhibit 8 shows the available market instruments across emerging markets. As seen in the exhibit, China, Indonesia, and Malaysia perhaps should consider introducing more instruments in their equity derivatives markets to cover the entire range of products.

LIQUIDITY

Turnover is an important factor in assessing ease of trading, because it enables investors to enter and exit mar-

kets easily. We analyzed equity turnover across global mar-kets and compared levels observed in DMs against that in EMs. We picked the top 20 exchanges by year-to-date equity turnover (January to October 2012) and segregated them by the type of market (developed and emerging). The U.S. leads the tally with two exchanges (NYSE and NASDAQ) occupying the first and second spots. Japan gets the third place, while China’s exchanges are placed fourth and fifth (Shanghai and Shenzhen). Overall, EMs fill 8 positions among the top 20, with 3 positions in the top 10 (see Exhibit 9). While exchanges in DMs dominate the list, there is a healthy presence of EMs.

Derivative contract volumes also offer a peek into the trading activity taking place across exchanges. We consid-ered the volume of futures and option contracts on single stocks and indices, and selected the top 20 exchanges globally. As seen in Exhibit 10, stock exchanges in EMs, such as KSE in Korea, NSE in India, and BOVESPA in

E X H I B I T 7Foreign Holdings in Local Equities in 2011

Source: Based on international investment position (as provided by central banks) and market capitalization data (World Bank).

E X H I B I T 8Available Market Instruments across Emerging Markets

Source: World Federation of Exchanges, stock exchange websites, www.asiaetrading.com.

JOT-KUMAR.indd 52JOT-KUMAR.indd 52 3/13/13 8:44:15 AM3/13/13 8:44:15 AM

THE JOURNAL OF TRADING SPRING 2013

E X H I B I T 9Equity Turnover by Exchange

Source: World Federation of Exchanges.

E X H I B I T 1 0Total Contracts Traded by Exchange

Source: World Federation of Exchanges.

JOT-KUMAR.indd 53JOT-KUMAR.indd 53 3/13/13 8:44:16 AM3/13/13 8:44:16 AM

INVESTMENT AND TRADE EXECUTION IN EMERGING MARKETS: PROSPECTS AND CHALLENGES SPRING 2013

Brazil, figure in the top five. Although this result is not an indication of traded value, it brings into light the amount of f loor activity witnessed across EMs.

Bid–ask spread can serve as a measure to help assess ease of trading. We listed the top 10 EMs by equity market cap and identified each one’s benchmark equity index with futures contracts on it. The f irst generic contract of the most-liquid future on these indices was identified, and the daily bid and ask prices were collected for the last four years. The spreads were computed in basis points (bps) and annual averages were calculated, as summarized in Exhibit 11.

Bid–ask spreads were found to be less than 5 bps for six countries, which is closer to the levels observed

in DMs. A lower bid–ask spread also keeps trading costs in check and acts as a positive measure of liquidity. His-torically, spreads have gone down in most markets, indicating enhanced liquidity, thereby improving overall trade quality.

It is interesting to observe that many of the EMs have spreads compa-rable to those in DMs. Russia, Mexico, and Malaysia should look at improving liquidity in their equity markets, as the futures spreads on their frontline benchmark indices are higher than the average spread across emerging countries.

TECHNOLOGY—DIRECT MARKET ACCESS (DMA)

Over the years, technology has transformed trading from open outcry to an electronic platform. DMA takes this a step further by providing direct access to the order book of an exchange. This aids faster trade execution, lower transaction costs, and better trade pricing. The DMA facility provides an option for anon-ymous trade execution, as multiple investors can use the same broker ID. Exchanges in EMs have enabled this service, and currently DMA is being offered by large brokers to their clients in addition to their regular trading facilities.

Source: Bloomberg.

E X H I B I T 1 1Spreads on Frontline Equity Index Futures

E X H I B I T 1 2DMA Availability across Emerging Markets

Source: Stock exchange websites.

JOT-KUMAR.indd 54JOT-KUMAR.indd 54 3/13/13 8:44:18 AM3/13/13 8:44:18 AM

THE JOURNAL OF TRADING SPRING 2013

Exhibit 12 shows the DMA availability across emerging markets; on the basis of this information, one might recommend that Taiwan should adopt DMA and move away from the current market access system, which requires orders to be routed through a broker.

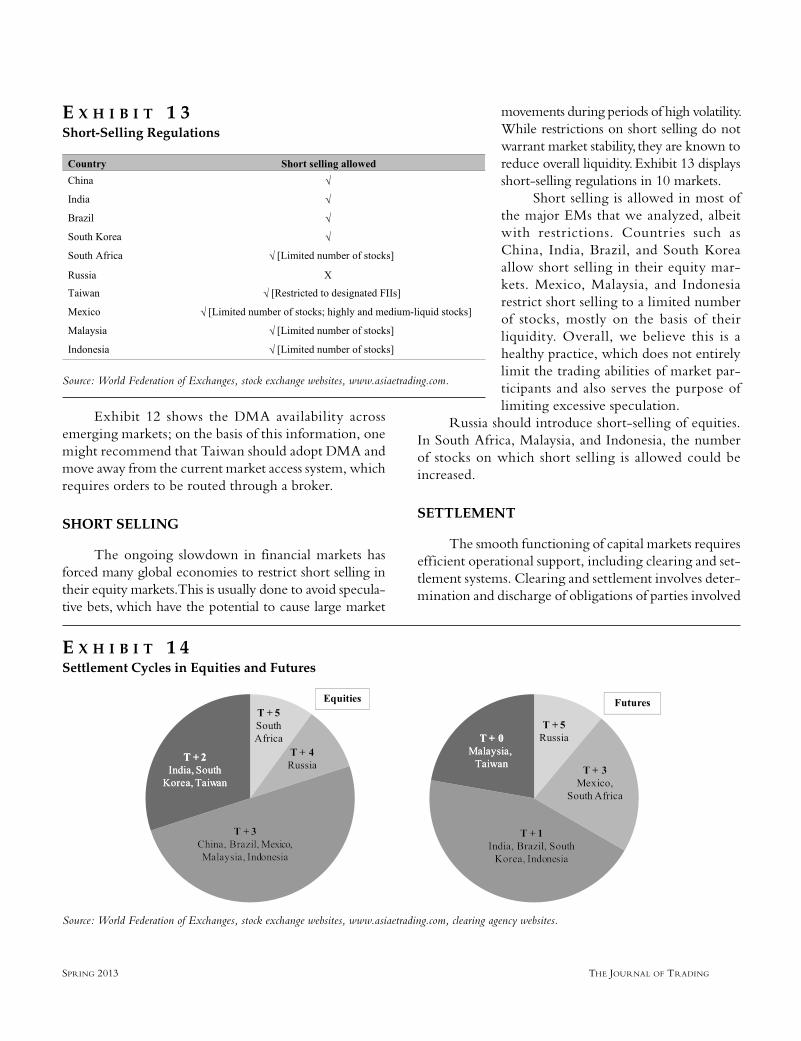

SHORT SELLING

The ongoing slowdown in financial markets has forced many global economies to restrict short selling in their equity markets. This is usually done to avoid specula-tive bets, which have the potential to cause large market

movements during periods of high volatility. While restrictions on short selling do not warrant market stability, they are known to reduce overall liquidity. Exhibit 13 displays short-selling regulations in 10 markets.

Short selling is allowed in most of the major EMs that we analyzed, albeit with restrictions. Countries such as China, India, Brazil, and South Korea allow short selling in their equity mar-kets. Mexico, Malaysia, and Indonesia restrict short selling to a limited number of stocks, mostly on the basis of their liquidity. Overall, we believe this is a healthy practice, which does not entirely limit the trading abilities of market par-ticipants and also serves the purpose of limiting excessive speculation.

Russia should introduce short-selling of equities. In South Africa, Malaysia, and Indonesia, the number of stocks on which short selling is allowed could be increased.

SETTLEMENT

The smooth functioning of capital markets requires efficient operational support, including clearing and set-tlement systems. Clearing and settlement involves deter-mination and discharge of obligations of parties involved

E X H I B I T 1 3Short-Selling Regulations

Source: World Federation of Exchanges, stock exchange websites, www.asiaetrading.com.

E X H I B I T 1 4Settlement Cycles in Equities and Futures

Source: World Federation of Exchanges, stock exchange websites, www.asiaetrading.com, clearing agency websites.

JOT-KUMAR.indd 55JOT-KUMAR.indd 55 3/13/13 8:44:19 AM3/13/13 8:44:19 AM

INVESTMENT AND TRADE EXECUTION IN EMERGING MARKETS: PROSPECTS AND CHALLENGES SPRING 2013

in the trade. Two important participants in the clearing framework are the clearing agency and the depository. All the EMs analyzed have a central clearing agency, which acts as the central counterparty. India, Indonesia, Malaysia, Russia, and Mexico have separate organiza-tions acting as clearing agencies and depositories, while China, Korea, Taiwan, Brazil, and South Africa have a single organization that performs both these functions.

Major developed market economies—the U.S., Germany, and the U.K.—have a T+3 settlement cycle in equities. The majority of EMs analyzed have T+3 or shorter cycles. Shorter settlement cycles are advanta-geous, as they result in lower operating costs, reduced trading capital requirements, and minimized risks.

As illustrated in Exhibit 14, South Africa and Russia have large settlement cycles (T+5 and T+4), which can be advanced to be in line with the most common cycle—T+3.

THE WAY AHEAD

Overall, emerging countries have shown signs of improvement over the past decade. Over the years, debt ratings have improved, traded volumes have increased, and bid–ask spreads have declined across major emerging countries. The settlement cycles and available instru-ments are also comparable to those in developed mar-kets. Despite these improvements, there is still room for progress for most of the countries we studied, as sum-marized in the following:

• Improvement in market liquidity—Russia, Mexico, and Malaysia

• Introduction of derivative instruments—China, Indonesia, and Malaysia

• Increase in foreign ownership—India• Increase in voting rights and development of off-

shore currency markets—across EMs• Adoption of DMA—Taiwan• Reduction in settlement cycles—South Africa and

Russia

Although emerging countries have acknowledged the benefits of liberalizing their economies, the pace of liberalization has been cautious. Traditionally, the f low of capital from the developed world into EMs has been guided by higher returns on investment resulting from greater economic growth. To continue attracting capital inf lows, however, policymakers will need to improve existing regulatory frameworks and market infrastruc-ture. We are optimistic that the process of increasing the openness of domestic markets and enhancing regulations will continue in the coming years.

To order reprints of this article, please contact Dewey Palmieri at [email protected] or 212-224-3675.

DisclaimerAlthough the information contained in this publication has been obtained from sources believed to be reliable, the authors and Evalueserve disclaim all warranties as to the accuracy, completeness, or adequacy of such informa-tion. Evalueserve shall have no liability for errors, omissions, or inadequacies in the information contained herein or for interpretations thereof.

JOT-KUMAR.indd 56JOT-KUMAR.indd 56 3/13/13 8:44:20 AM3/13/13 8:44:20 AM