27

THE WINDS OF CHANGE: MAQUILADORAS BEFORE AND AFTER NAFTA

| Date post: | 25-Dec-2015 |

| Category: |

Documents |

| Upload: | avis-aleesha-robertson |

| View: | 216 times |

| Download: | 0 times |

THE WINDS OF CHANGE: MAQUILADORAS BEFORE AND

AFTER NAFTA

NORTH AMERICAN FREE TRADE AGREEMENT

• TRADE OF COMPLETED PRODUCTS

• MANUFACTURE OF PRODUCTS

THE GENESIS AND EVOLUTION OF THE MAQUILADORA INDUSTRY

• BORDER INDUSTRIALIZATION PROGRAM - 1965

• PRODUCTION SHARING

• MAQUILADORA INDUSTRY DOUBLED IN SIZE IN LATE 1980S -- NOW OVER 2,000 FACTORIES WITH OVER 500,000 WORKERS

• SECOND LARGEST INDUSTRY IN MEXICO

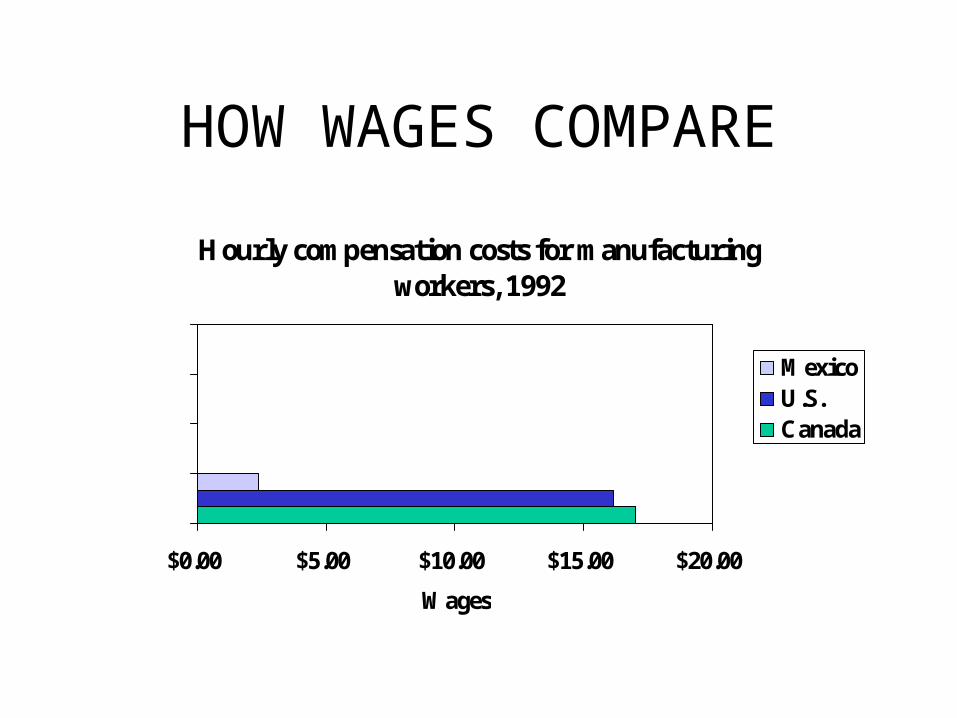

• MEXICO’S COMPETITIVE WEAPON: LOW LABOR COST ==> QUICK DELIVERY

• LOCATION OF MAQUILADORAS: BORDER vs. INTERIOR

THE GENESIS AND EVOLUTION OF THE MAQUILADORA INDUSTRY, continued

• MAQUILADORA WORKERS:– young, mostly female (92% ==>83%)

– pay

– mobility

– generally high turnover rates,averaging 10% per month

• PRODUCTIVITY, QUALITY AND ENVIRONMENTAL ISSUES

• SOME COMPANIES WITHDRAWING FROM MEXICO CITING DECREASED PRODUCTIVITY AND OTHER HIDDEN COSTS

• ADVANCED CONCEPTS SUCH AS JIT, KANBAN, TQM, ISO 9000 AND PRODUCT DESIGN INCREASINGLY FOUND IN MAQUILADORAS

HOW WAGES COMPARE

Hourly compensation costs for manufacturing workers, 1992

$0.00 $5.00 $10.00 $15.00 $20.00

Wages

MexicoU.S.Canada

THE NORTH AMERICAN FREE TRADE AGREEMENT

• MORE TRADE ORIENTED THAN PRODUCTION ORIENTED

• LIMITED FORM OF REGIONAL ECONOMIC INTEGRATION

• DIFFICULTIES OF UNITING TWO MATURE INDUSTRIES WITH A NEWLY INDUSTRIALIZING COUNTRY

• MEXICO IS ALREADY THE US’s THIRD LARGEST TRADING PARTNER

• GOALS AND PURPORTED BENEFITS OF NAFTA:– job creation plus more for all– greater access to Mexican markets– greater freedom in sourcing (removal of tariffs)– opening up of previously protected industries

THE NORTH AMERICAN FREE TRADE AGREEMENT, continued

• JOB RELATED ISSUES– net gain vs. net loss (differing opinions)

– changing local of jobs, both regionally within the US and between the US and Mexico

– changing demands of jobs

• MANY INDUSTRIES AFFECTED:– chemicals, textiles, telecommunications, equipment, agricultural

• IMPACT ON OTHER COUNTRIES - such as Japan and Latin American countries

• OPPOSITION TO NAFTA– fear of job loss

– environmental and labor concerns

NAFTA: PRODUCTION ISSUES

• IMPLEMENTATION ISSUES -- transition period

• STRATEGIC ISSUES– Larger market (demand) for goods: Hire more cheap labor in

Mexico or return to the US and automate? What is break-even quantity?

– Opening of formerly protected industries: How to expand into new territory -- produce in Mexico or service from existing or other locations?

– Locate closer to the customer? Closer to suppliers? -- In international context, who are suppliers and customers?

– Rationalization of factories, implications for existing facilities in Mexico as well as in the US.

PRODUCTION ISSUES, continued

• Reuniting nearby sister (twin) plants -- most likely on the Mexican side of the border to continue to realize lower labor costs?

• How does the portfolio of plants fit together, with the advent of free trade and more freedom for direct foreign investment? Should any plants be closed or downsized? Should any new ones be built? When? Where?

• And what about distribution and warehousing?

• Supplier issues: Mexican materials used in production by US manufacturers will no longer be subject to US tariffs, but is the quality as good? And are the prospective suppliers reliable?

PRODUCTION ISSUES, continued

• Problems involving infrastructure -- such as roads, electrical grid,and communications -- will have to be resolved.

• Human resource management issues– recruiting native managers

– feasibility of using teams in a production setting in spite of a high turnover rate?

– Can the turnover rate be reduced while maintaining the low labor cost advantage?

CONCLUSIONS

• Under NAFTA, the maquiladoras will essentially be phased out, because then they will be competing on an equal footing with other forms of manufacturing. The more advanced maquiladoras seem to be well prepared for this next stage of development.

• The major US manufacturers will be drawn into this scenario, either voluntarily, if they wish to remain competitive, and will have to totally re-evaluate their production strategies in keeping with this increased global competition. Not only will they have new opportunities in Mexico, but Mexican companies will also have new opportunities in the US.

THE ROLE OF TAXES AND DUTIES ON LOCATION AND

SOURCING DECISIONS

SAMPLE FIRMS

• FIRMS WITH MANUFACTURING FACILITIES IN BOTH LOW AND HIGH TAX COUNTRIES (low tax: Ireland, Singapore, Puerto Rico)

• NINE FIRMS– 3 pharmaceuticals, 3 semiconductor, 1 chemicals, 1 specialty

materials, and 1 software

• SAMPLE BIASED TOWARDS– large size firms (only one less than 100M$ sales)

– significant R&D (exceeded 9% of sales)

SAMPLE FIRMS, continued

• ANALYSIS OF SIXTY EIGHT LOCATION DECISIONS

• RELUSTING FACILITIES SPREAD ALL OVER THE WORLD.

LOCATION OF MANUFACTURING ACTIVITIES

PHARMACEUTICALS

• MAIN INDUSTRY CHARACTERISTICS– High R&D Costs

– Short Harvest Periods (patents expiring)

– Gross Margins High & Operating Risks High

– Relative Costs of Manufacturing Low

• TYPICAL MANUFACTURING STAGES– Production of initial compound

– manufacture active ingredient

– dispense (granulation & mixing) active ingredient

– tablet production

– package finished product

PHARMACEUTICALS, continued

• IMPORTANT LOCATION FACTORS– Product and price approval

• price increases for local manufacturing

• lower prices for access to local markets

• lower prices for shorter approval periods

– Environmental and safety regulations• leads to collocation of production stages

• US approval period the longest– recent legislation allows to export to twenty developed countries if

approval there

• Taxes (or absence of in Puerto Rico & Ireland)

• Local Content Requirements– filling/finishing stage in the country of approval

LOCATION OF MANUFACTURING FACILITIES

SEMICONDUCTORS• MAIN INDUSTRY CHARACTERISTICS

• Products– high volume commodity chip (production cost)

– microprocessors (product innovation)

– short harvest periods (product obsolescence)

– lower gross margins (than pharmaceuticals)• more low margin products

• higher cost of goods sold

– steep manufacturing - learning curve

– transfer of learning from high-volume to proprietary products

– more extreme fluctuations in demand

SEMICONDUCTORS, continued

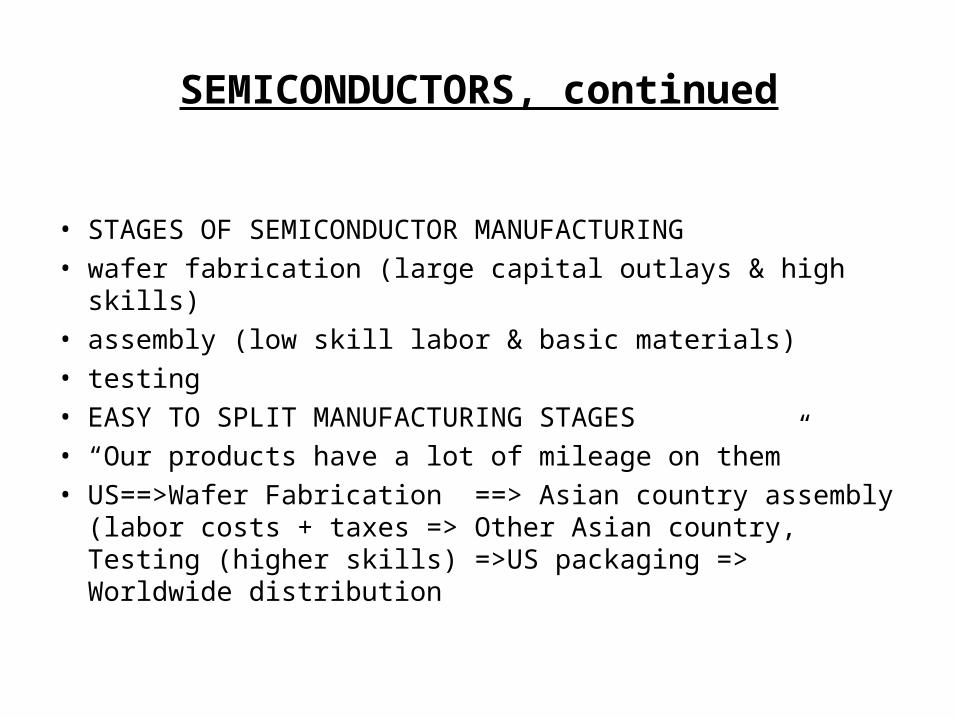

• STAGES OF SEMICONDUCTOR MANUFACTURING

• wafer fabrication (large capital outlays & high skills)

• assembly (low skill labor & basic materials)

• testing

• EASY TO SPLIT MANUFACTURING STAGES

• “Our products have a lot of mileage on them”

• US==>Wafer Fabrication ==> Asian country assembly (labor costs + taxes => Other Asian country, Testing (higher skills) =>US packaging => Worldwide distribution

SEMICONDUCTORS, continued

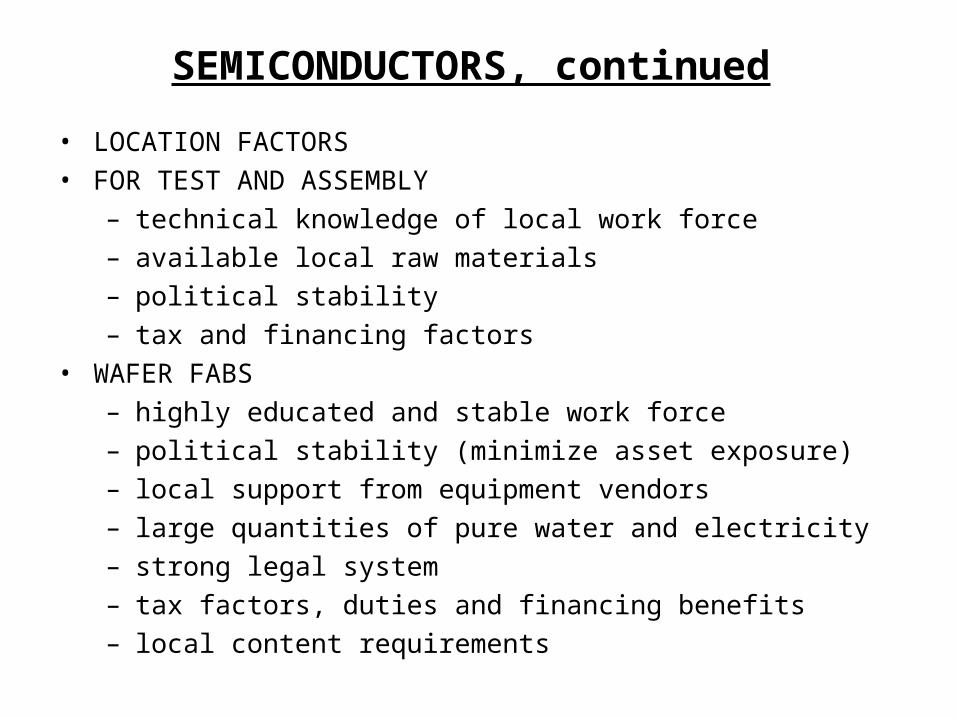

• LOCATION FACTORS

• FOR TEST AND ASSEMBLY

– technical knowledge of local work force

– available local raw materials

– political stability

– tax and financing factors

• WAFER FABS

– highly educated and stable work force

– political stability (minimize asset exposure)

– local support from equipment vendors

– large quantities of pure water and electricity

– strong legal system

– tax factors, duties and financing benefits

– local content requirements

SEMICONDUCTORS, continued

• IN SUMMARY

– taxes and labor costs are tie breaker for test and assembly

– taxes and duties are tie breaker for wafer fabs

• RECENT TRENDS

– local content requirements ==> customer proximity

– automation of test and assembly == > collocation with wafer fab

LOCATION OF MANUFACTURING FACILITIESCHEMICALS

• SAMPLE FIRMS– lower gross margins

– large centralized factories

– competitive priorities

– mostly low cost production

– more emphasis on advanced chemicals (require smaller plants)

– transportation costs high

• CHEMICAL FACILITIES LESS ATTRACTIVE TO HOST COUNTRIES– demand large quantities of water and electricity

– represent an environmental risk

– employ small medium-skilled workforce

CHEMICALS, continued

• AND CHEMICAL COMPANIES RECEIVE LESS TAX BENEFITS

• TAX FACTORS LESS IMPORTANT FOR CHEMICAL COMPANIES, BUT ALWAYS ENTERS THE PICTURE

LOCATION OF MANUFACTURING ACTIVITIES: SOFTWARE

• SAMPLE SOFTWARE COMPANY

– recent start up

– high R&D and marketing costs

– low manufacturing costs

– transcribe code to floppy disks

– package disks for sale

• TAXES PRIMARY DIRVER IN LOCATION DECISIONS

– location decision process: list of low tax countries

• COMPANY CURRENTLY IN PUERTO RICO

• POTENTIAL PROBLEM

– US Treasury argues that software operations do not constitute legitimate manufacturing

– transfer price: cost - plus

LOCATION OF MANUFACTURING ACTIVITIES: MATERIALS

• SAMPLE FIRM

– specializes in niche markets

– close linkage to its customers

– many product changes

• TAX FACTOR A SMALL ROLE

• WENT TO SINGAPORE IN ORDER TO SERVE MALAYSIA AND SINGAPORE

LOCATION OF MARKETING & DISTRIBUTION CENTERS: AN EXAMPLE

• NEW STRUCTURE MOTIVATED BY DUTY CONSIDERATIONS– before: duty on transfer price from AP to Italy

– now: duty on transfer price from AP to AP-International

AP(American Parent)

ITALYNB

(Netherlands’ branch)

AP-International (located in the US)

New Invoicing

New Invoicing

OldInvoicing

SOURCING AND TRANSFER PRICING

• TAX BENEFITS DUE TO SOURCING DERIVE FROM

– Setting tax transfer prices

– Setting quantities to be sourced from various locations

• FIRMS THAT BENEFIT THE MSOT– High gross margins (few comparable products)

– decouple business activities

• FLEXIBILITY IN TRANSFER PRICING REDUCED BY– Aggressive auditing

– Price approval (cost plus)

(prices vs. duties)

SOURCING AND TRANSFER PRICING

• TRANSFER PRICES MAY BE USED FOR NON-TAX PURPOSES (FOR MANAGER MOTIVATION)

– Risky to use two sets of transfer prices (tax authorities)

– Use performance measures not affected by transfer prices