.Docuient of The World Bank.' FOR OFFICIAL USE ONLY 1,1 32V?. 1 Reprt RNo. 8644-iND STAFF, APPRAISAL REPORT ZNDONESIA - SE,COND BRI IMPEDES S4ALL CREDIT PROJECT July 10, 1990 Industryand Energy Operations Division - CotntryDepartment V Asia Region . is do_etl has a esotd dubufte ad may be usd by recienonly in th pdoa of thek ofticW dute. Its contents may not otherw be disdosed without Word Bak authoizon. Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

Transcript

.Docuient of

The World Bank.'

FOR OFFICIAL USE ONLY

1,1 32V?. 1

Reprt RNo. 8644-iND

STAFF, APPRAISAL REPORT

ZNDONESIA

- SE,COND BRI IMPEDES S4ALL CREDIT PROJECT

July 10, 1990

Industry and Energy Operations Division -

Cotntry Department VAsia Region

. is do_etl has a esotd dubufte ad may be usd by recienonly in th pdoa ofthek ofticW dute. Its contents may not otherw be disdosed without Word Bak authoizon.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

-=- CURRENCY EQUIVALENT

Currency unit = Indonesian rupiah(as of May 1, 1990)

US$1.00 Rp 1,830Rp 1.0 billion - US$0.546 million

FISCAL YEAR

Government of Indonesia - April 1 - March 31Bank Rakyat Indonesia - January 1 - December 31

PRINCIPAL ABBREVIATIONS AND ACRONYMS USED

BAPINDO - Bank Pembangunan Indonesia (Development Bank of Indonesia)BI - Bank IndonesiaBKK - Badan Kredit Kecamatan (Rural Credit Institutions)BPKP - Agency for Financial and Development SupervisionBRI - -Bank Rakyat IndonesiaCP&F - Credit Processes and ProceduresDMB - Deposit Money BankGDP - Gross Domestic ProductGNP - Gross National ProductGOI - Government of IndonesiaJSE - Jakarta Stock exchangeIMP - International Monetary Fund --

IPTW - Prompt.Repayment Incentive(KIK - Kredit Investasi Kecil (Small Investment Credit Ptogram)MKPm - Kredit Modal Kerja Permanen (Small Permanent Working Capital

Program)IUPEDES - Kredit Umum Fedesan (General Village Ciredit Program)LPPI - Indonesia Bafiking Development InstituteMOP - Ministry of FinanceNES - Nucleus Estate Smallholder ProjectsPDFCI - Private Development Finance Company of IndonesiaPIP - Performance Improvement ProgramPPAR - Project Performance Audit ReportPT ASKRINDO - PT Asuransi Kredit Indonesia (Credit Insurance Company of

4 . Indonesia)SBI - Sertifikat Bank IndonesiaSBPU - Surat Berharga Pasar UangSCB - State-Owned,Commercial BankSEDP Small Enterprise Development ProjectSIMPEDES - Simpanan Pedesan (Village Sayings Program)TABANAS - Tabungan Nasional (Small Saving Program)UBM - Untt Desa Business ManagerUDO - Unit Desa Qfficer

) USAID - United States Agency for International Development X

FOR OFFICIUL USE ONLV

INDONESIA

SECOND BRIIKUPEDES SMALL CREDIT PROJECT

Loan and Project Summary

Borrowers Republic of Indonesia

Beneficiaryt Bank Rakyat Indonesia (BRI)

Amounts $125 million equivalent

Termss Twenty years, including five years of grace, at the Bank'sstandard variable interest rate,

Onlending Terms: The proceeds of the loan would be onlent to BRI for twentyyears, including a grace period of five years, at avariable interest rate pegged to Bank Indonesia's (BI)three-month domestic money market certificate (SertifikatBank Indonesia--SBI). The rate would be adjusted onJanuary 1 and July 1 of each year, based-on the average ofSBI three-month maturity quotations during the precedingsix months, not to exceed the average of end-of-dayquotations of the five state-owned commercial banks' three-month time deposits during the same period. The Governmentwould bear the foreign exchange risk.: On July 1 of eachyear, at the request of either the Borrower or the Bank,the basis for determining the onlending rate would bereviewed. BRI would also pay commitment fees equal- tothose payable by the GOI to the,Bank under the loan. End-users would borrow these funds at rates reflectingprevailing market conditions; effective annual-interestrates currently range from 22.7 to 31.7 percent, based onloan amount.

ProjectDescription: The primary objective of the7project is to promote BRI's-

ongoing efforts to strengthen and expand its Unit Desasystem as a financially viable subbranch network thatmobilizes resources and provides nonsubsidized credit(KUPEDES loans) nationwide to creditworthy small borrowers.The project will also support continued development ofBRI's institutional capability as related to its Unit Desasystem.

The project comprises three componentss (a) a creditcomponent for general-purpose KUPEDES financing; (b) _qcapital expenditure component for the expansion of BRI'sfive regional Unit Desa training centers, includingcomputer equipment; and tc) technical assistance for long-

This documrent has a restricted distribution and may be used by recipients only in the performanceof their official duties. Its contents may *ot otherwise be disclosed without World Bank authorization.

. l

v---eriM advisory and shortterm counsulting services le-developing and iproving BRI's Unit Desa and rural bankingactivities.

Risks: The project supports a market rate-based scheme designed tomeet the needs of small borrowero and small savers. Underthe project, the Unit Desa system would be expanded andcontinued access to credit by eligible borrowers would beensured. Substantial socioeconomic benefits can beexpected from an expanding KUPEDES program. The majorrisk--portfolio deterioration--is mitigated by BRI'ssatisfactory track record to date. Appropriate staff'training and advisory support services will contributetowards the continued implementation of sound lending andsupervision procedures that are assoclated with themaintenance of high-quality loan portfolio.

I. SECTORAL ASPECTS . .......... ............... I...... 1

A. The Financial Sector ... .. ..... .. *9 * * * * * ........ 1Background .......... ****#**# 1

The Reform Program ........................* * a * *............. 1Future Agenda and Priorities ........................... 3

B. Characteristics of Small and Family Enterprises ........ .... 3C. Financial Services for Small Savers and Borrovers ......... 4D. Bank Objectives, Strategy and Role in the Pinancial

U1. EXPERIENCE UNDER PAST WORLD BANK GROUP FINANCIA SECTORLENDING OPERATIONS ............................... ,.*9* .. 7

III. PRESENT STATUS OF THE BENEFICIARY AND THE KUPEDES PROGRAM .... 8

A. Bank Rakyat Indonesia .. ...................... ... ... 8B. The BRT Unit Desa System and the KUPEDES Program .......... 9

Background ........ ........ 9........*.. 9Project Implementation Under Loan 2800-IND ............. 10Organization ............................... ..*... ....... ... 0...... llScope and Terms of KUPEDES Lending..................... 13IUPEDES Lending Operations ................ ........... 15Characteristics and Impact of KUPEDES Lending .......... 15Unit Desa Administration and Financial Operations ...... 18Funding of the Unit Desas and Resource Mobilization .... 18Financial Position and Performance of the Unit Dsss a... 20

IV. THE PROJECT........ ........................................ 23

A. Project Rationale, Objectives and Content .............. ... 2S3B. The Credit Component - Operational Projections

and Resource Requirements ..............................9 24C. Capital Expenditure and Technical Assistance Components... 26D. Project Cost Estimates and Financing Plan ................. 27

This report is based on the findings of an appraisal mission in March 1990.Mission members were Charles Magnus (AS51E-task manager), Kathlien McCollom(ASTDR) and Victor Agius (AS5RS).

- iv -

Pate No.

IV. THE PROJECT (cont'd)

E. Features of the Loan ...................................... 29Lending Arrangements ...................... 29Loan Administration ............................. 30

F. Project Benefits and Risks ................................ 33

V. AGREEMENTS AND UNDDERITAN1)INGS.. . ...... ........................ 33

TABLES IN TEXT

1.1 Financial Institutions Serving Small Borrowers and Saversin Indonesia ... ..... .*.................... . ..... .4

3.1 Total Resources Available to the Unit Desa System, End-1989... 203.2 Indicators of Unit Desas' Financial Performance, 1984-89 ..... 224.1 Actual and Projected Total Resources Available to the Unit

Desa System, End-1989 and End-1992 ............ ..........*.. 254.2 Sensitivity of Projected Total Resources Available to the

Unit Desa System to Changes in Growth Rates, End-1992 ..... 264.3 Total Project Costs. ...... . ............ .. .... .. 28

4.4 Financing Plan ....................................... 29

1. Documents Available in the Project File2. Bank Rakyat Indonesia - Institutional Aspectsi3. World Bank Group/ADB Funds to BRI, 1972-894. Bank Rakyat Indonesia Unit Desa Policy Statement5. Bank Rakyat Indonesia Unit Desa Strategy Statement6. BRI Unit Desa System

Table l Summary of Actual KUPEDES Lending Operations, 1984-89Table 2s Balance Sheets, 1984-89Table 3: Income Statements, 1984-89Table 4: Analysis of RUPEDES Loan Portfolio, 1984-89Table 5: Projected KIPEDES Lending Operations, 1990-92Table 6: Projected Resource Requirements/Funds Utilization

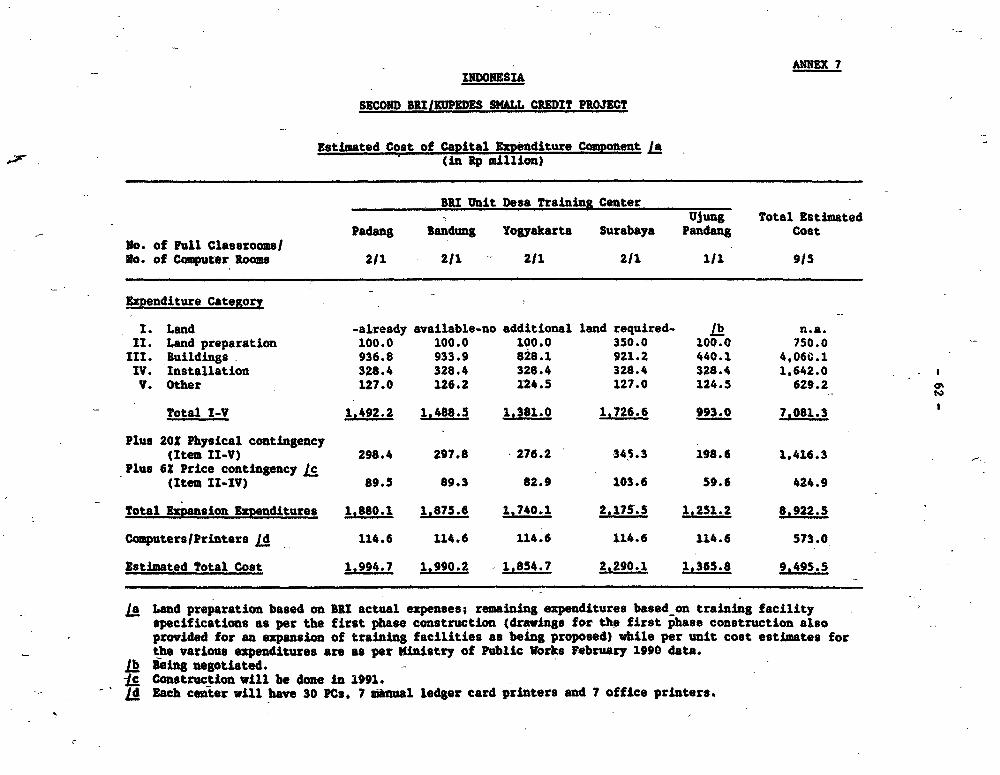

of BRI Unit Desa System, 1990-927. Estimated Cost of Capital Expenditure Component8. Terms of References Long-Term Advisory Positions9. Estimated Disbursement Schedule

CHART

1. BRI Business Unit Desa De,artment

MAP

IBRD 20514R1

INDONESIA

SECOND BRIIKUPEDES SMALL CREDIT PROJECT

l. SECTORAL ASPECTS

A. The Financial Sector

Background

1.1 The financial sector of Indonesia has undergone a major transforma-tion towards a competitive, market-based system since the initiation by theGovernrent of Indonesia (GOI) in 1983 of a comprehensive program of policyreforms. These reforms were introduced in stages, in conjunction with realsector reforms, and within the context of an open capital account and a G0opolicy of refraining from domestic financing of budget deficits. As a result,the reforms contributed to a strong revival of private sector investment, non-oil export growth, improvements in the efficiency of capital use and faster-than-expected economic growth.

1.2 Until the early 19809, the development of the financial sector inIndonesia was constrained by the imposition of interest rate and creditceilings. The Government played a large role in the allocation of resourcesthrough the liquidity credit system, under which low interest loans topriority sectors were automatically eligible for refinancing with BankIndonesia (BI), and often with substantial government guarantee. Thefinancial system compriied mainly the banking sector, which was dominated byBI and the five state-owned commercial banks (SCBs),1/ accounting for about80 percent of the total assets of the deposit money banks. Strict control waskept on the entry of new banks and of the branching of existing institutions.As a result, the growth of financial assets stagnated and the securitiesmarket did not develop.

The Reform Program

1.3 In June 1983, the GO implemented the first in a series of reforms toimprove the efficiency of the financial sector. Interest rates werederegulated and credit ceilings were replaced with a system of reserve moneymanagement. These reforms were followed by the introduction of new moneymarket instruments in 1984 and 1985. Additional financial sector reforms wereundertaken during October-December 1988. The main objectives of these reformswere: (a) to enhance financial sector efficiency by encouraging competitionby eliminating entry barriers; (b) to increase the availability of long-termfinance by promoting the development of capital markets; and (c) to improvethe stability of the financial system by strengthening prudential regulations.

1/ These are Bank Dagang Negara (BDN), Bank Negara Indonesia (BNI), BankRakyat Indonesia (BRI), Bank Ekspor Impor Indonesia (BEII) and BankBumi Daya (BBD). All are participating in the Bank's Second ExportDevelopment Project (Loan 2979-IND) and the Industrial RestructuringProject (Loan 3040-IND). All except BEII are participating in theSmall and Medium Industrial Enterprise Project (Loan 3041-IND).

-2 -;

Specific reform measures includeds (i) permitting the entry of new banks,including joint ventures with foreign banks; (ii) easing restrictions onestablishing new branches; (i1i) allowing banks and nonbank financialinstitutions (NBFIs) to increase their cap. 1. through share issues;(iv) permitting public enterprises to place p to 50 percent of their depositswith private banks; (v) easing the requirements to become a foreign exchangebank and allowing NBFIs to issue certificate of depositsl and (vi) allowingbanks to have subsidiaries that are multiservice financial companies thatprovide leasing, factoring, consumer finance and venture capital facilities.To spur the development of the domestic short-term money markets, restrictionson interbank borrowing were removed and required reserves reduced to 2 percentof all bank third party liabilities. To encourage mobilization of long-termfunds and risk capital, the reformss (a) moved towards equalizing the netreturns to savers holding different financial assets; (b) allowed the privatesector to operate stock exchanges and established an over-the-counter (OTC)markets and Cc) permitted foreign investors to buy up to 49 percent of theshares in each company listed on the stock exchange. In addition, measureswere adopted to enhance prudential regulations by defining loan concentrationratios and by establishing rules to prohibit insider trading on the stockexchanges. These measures were complemented by a program of institutionalstrengthening of BI to strengthen its supervisory capabilities.

1.4 The reform measures yielded substantial positive results as evidencedbys (i) the increase in the number of new banks and other financialInstitutions; (ii) a quadrupling of the gross assets of the finAncial sector,reflected by an increase in the ha:GNP ratio from 21 percent to 33 percent anda more than doubling of private sector financial savings over 1982-89; and(iii) a fifteen-fold increase, albeit from a smaller base, in the issue valueof listings on the stock market. 'While all banks showed strong growth, theprivate banks by far surpassed the SCBs both in relative and absolute terms.The share of the SCBs' total banking sector deposits declined from 67 percentto 59 percent within one year of the reforms. The level of interest ratesremained high, but both deposit and lending rates declined in 1989. There wasalso a substantial lowering of the very high intermediation margin enjoyed bythe banks in the past. Meanwhile, the share of subsidized directed creditsdeclined from over 50 percent to less than 30 percent between 1982 and 1989.However, the directed credit program continued to distort and segment thefinancial market, leading to the misallocation of resources and weakenedfinaneial discipline.

1.5 The GOI announced another round of policy reforms in January 1990 toeliminate distortions created by the subsidized directed credit programs. Thenumber of programs eligible for refinancing was reduced drastically, and theinterest rate moved closer to the market. Insurance, which was compulsoryprior to the reform, was made voluntary and premiums would be market-based.At the same time, banks were required to allocate 20 percent of their loanportfolio to small enterprises, defined as those having fixed asset (excludingland) of up to Rp 600 million (US$330,000 equivalent). In order to fosterfurther the development of capital market, the GOI also announced itsintention to privatize the Jakarta Stock Exchange. The impact of these reformmeasures is expected to be increasingly felt in the near-term, as theefficiency of financial intermediation improves further and the distortionscaused by the liquidity credits are minimized.

Future ARenda and Priorities

1.6 The Indonesian financial sector is now well integrated with theinternational financial markets. The reform measures have led to a rapidincrease In the proportion of private savings intermediated through thefinancial system. However, the sector remains relatively small in relation tothe size of the economy (H2 represents just over 30 percent of GDP compared to60 percent in Malaysia and Thailand). The sector needs to sustain high butstable growth to enable it to support continued expansion in the real sector.The January 1990 reforms have put in place the last main component for thederegulation of the financial sector. The GOI's priority now is to proceedwith a comprehensive program to strengthen financial institutions. To thisend, the GOI is currently preparing new legislation covering the bankingsector, and insurance and pension plans. The GOI also recognizes that afreer, market-based system requires appropriate supervision. Attention hasthus focused on strengthening the prudential control and supervisory apparatusfor both the banking sector and the capital market. With IMF assistance,efforts are underway to strengthen BI's supervisory functions. Similarly.with the assistance of consultants, the regulatory body for the capitalmarkets is being strengthened, and efforts are underway to deepen the moneymarkets and to develop a credit information system. Beyond this, the mainconcern for the healthy development of the sector is to ensure that the SCBs,which, despite their diminished market share, still account for almost60 percent of the deposit banking sector, develop into efficient andfinancially autonomous institutions. This is likely to require both portfoliorestructuring and equity infusions, as well as follow-up on the institution-building programs that each of these institutions has al-eady initiated on itsown. The Bank is discussing with the GOI the possibility of assisting in theareas mentioned above, particularly in restructuring the SCBs, as part of aproposed Financial Sector Restructuring Operation.

B. Characteristics of Small and Family Enterprises

1.7 Most small-scale economic activities in Indonesia, particularly inrural areas, are carried out by individuals, or within the family, generallywithout the use of hired labor. Families usually have several economlcactivities, and they shift labor and working capital among these to takeadvantage of opportunities available. Rather than continuing to expand oneparticular activity, families often prefer to shift part of their resourcesinto new areas. This reduces the risk of failure. Apart from agriculturalproduction, these activities incluie the processing and marketing ofagricultural products, trade, cottage-level industries, and work in private orpublic construction.

1.8 Ahe most recent data available indicate that the total number ofsmall enterprises, including those engaged in farming, fisheries, forestry andlivestock, exceeds 27 million. Most are small and employ an average of fewerthan three people, often family members. Over a quarter of the labor force isself-employed. Small and family enterprises probably account for about75 percent of total employment in Indonesia, with the majority engaged inagricultural and trading activities (often, of agricultural products). Smallfarms produce the bulk of staple food output and a significant proportion ofexport crops such as rubber, coffee and pepper. In manufacturing, the

-4 _

contribution of small entrepreneurs is greatest in domestic resource-basedindustries, such as rice milling, furniture and bakery products. Much of theroad transport services is carried out by individual private operators. Inconstruction, most projects are also undertaken by small entrepreneurs. Smallwholesale and retail traders are essential intermediaries between producersand consumers, financing and holding stocks of raw materials and finishedproducts. A number of surveys also indicate that small traders have been animportant source of informal credit in rural areas to farmers who have limitedaccess to formal credit.

C. Financial Services for Small Savers and Borrowers

1.9 Despite the rapid expansion of the larger financial institutions'branch networks since the start of the GOl's financial sector reform programin 1983, except for BRI, few have had more than a mint-al presence outside thelarger provincial towns. At this level and below, banking services areprovided by a wide range of numerous formal and informal small financialinstitutions. These are presently estimated to exceed 17,000 in number. Mostoperate at the Kecamatan (subdistrict) or desa (village) level, and are ownedby the national, provincial or local governments. Nevertheless, they aregenerally market-oriented and serve relatively large numbers of clients. Onthe lending side, their focus is usually on short-term trade-related workingcapital loans. Table 1.1 below summarizes the formal institutions operatingat the subdistrict and village level,

TW&Ia1.X:; PMWJAL DVJ1fUM SERV8Wl SML 80R11WOR AM) SA IN DONESA

I,atituticn/Progran Omereip Garaphil Foe A1nal Interest ft." Ha-Min Siz ve r Lau- laturt Col later Svngeon eclining balance) t" )ge ir Sd

Privote 8J"WS: Priveta, Main In*ao., 20 - JO 8 million * n.e. Ipte frl yODI01 Provincial cili S ear title to

end Dietrict le, real sees

IlRSfUnit Oee/ ilRSS _ n t b S - u t.000 a te mEO toal yesKotes district l2) IS llti t title to land

a year or ther t Ibble

Sank Peoa, Private Kecamte 40 - USO u to 780,000 up to full limitedatarpom (abdi.tri.t) I .illIon 1 year aI"na

reetor tvl invntrCopeative.

Prowvicial Prewvnctnl Vil te I - 510 , 000 - 60.000 up to r limitdcredit b dana So"raunt v1 1 -100,000 1 yer rm OX") O"d

Cooperatives OWd b Vii, 8SI ve. by - up o minimal limitedCooptiv Cooper,tiva 2 yer

1.10 By far the most important of these operations is BRI's Unit Desasystem which now accounts for over half of the total loans outstanding of therural financial institutions. The next most important is the more than 200Bank Pasars (market banks) which account for about 30 percent of the themarket. Cooperatives and provincial government-owned institutions eachaccount for about 5 percent. The Bank's Rural Credit Sector Review (ReportNo. 6917), dated April 29, 1988, details the structure and characteristics ofthe sector and the various institutions.

1.11 At the lowest level, by loan amount, are the credit activities of theXoperasi Unit Desas (KUDs), or cooperatives. Their credit programs areusually funded from official sources with little savings mobilization efforts.Loans are to KUD members. Most of the credit programs carried out by the KUDsare conceived at the national level and are imposed on the KUDs. Their pasttrack record has been poor, with arrears of 20 percent and more. Only about14 percent of the KUDs are classified as well-run and self-sufficient. Overthe past four years. the Bank Umum Koperasi Pinjaman (BUKOPIN), withassistance from the Dutch Government and the Rabobank Foundation, has embarkedon a pilot program to improve the credit and savings mobilization efforts ofthe KUDs. Initial results have been encouraging.

1.12 At the next level are the provincial-owned banking networks. Thebest known and most developed is the Badan Kredit Kecamatan (BRK) in CentralJava which was started in 1972. Others include the Kredit Usaha Rakyat Kecil(KURR) in East Java, Lembaga Perkreditan Kecamatan (LPK) in West Java and theLumbung Pitih Negari in West Sumatra.21 Most of these institut$ons arelocally administered and financially autonomous. The main characteristics ofBKK-type credit operations ares little paperwork, no collateral and relianceon local social pressure for repayment; a post system, or mobile service(usually by motorcycle) operating at village markets, which compensates forthe limited mobility of most villagers; and the willingness of borrowers topay the high interest rates necessary to cover the costs of such a program.BKK loans are very small and finance mostly market traders. Theseinstitutions have been successful in keeping arrears low (about 5 percent ofoutstanding loans) and enabling them to operate profitably. The BKKs' fundingcomes from the initial capital provided by the provincial authorities,mandatory savings paid in by borrowers as part of their loan agreement, andfrom annual net revenues. Recently, some of these institutions have startedto provide savings facilities on a pilot basis. The BPD (Bank PembangunanDaerah--Regional Developmzw.,Banka) have at times provided technicalsupervision to sawt-ThTe BKKs, particularly in the areas of bookkeeping,reporting ajwtEi and personnel policies.

1.13 There are now over 200 Bank Pasars (Market Banks), of which more thanhalf are privately owned, mostly by commercial banks. The others belong toeither government or cooperatives. Bank Pasars are generally located in aprovince's main city and conduct business in the city and in the marketsnearby. Bank Pasars tend to specialize in short-term loans to small traders,for which they charge about 3.5 percent per month. Borrowers are normallyrequired to hold compensating balances of at least 5 percent in noninterest-bearing deposit accounts (raising the effective annual interest rate to about44 percent). They also require collateral in the form of inventory, fixedassets or durable goods with a value of 150 percent of the amount of the loan.

1.14 The BRI Unit Desa network is the single most important nationwidebanking system throughout Indonesia. It comprises some 2,850 Unit Desas

21 Central Java has about 500 subdistrict level institutions (the BRKS)with about 3,060 village posts. East Java has about 1,600 KURUs andWest Java about 200 LPKs. Best Sumatra has about 150 active LPNs.Bali has abobt 50 similar institutions.

-6-

(subdistrict or village-based subbranches) and 835 posts. This networtkbridges the gap between the provincial-owned banking institutions and thelarge, usually city-based, private banks and SCB branches. The development ofthe Unit Dess system over the past six years has impressively demonstrated thelarge potential for small savings mobilization and for introducing smallsavers to the formal bankin8 system. Prospects for further growth in thisarea, and for developing other banking services, e.g., cash transfers and newsavings instruments, remain significant. On the lending size, the KUPEDESloan program has developed into the main source of financing for smallborrowers at onlending rates which are not subsidized, permit full costrecovery, and yield BRI a profit. As of end-1989, KUPEDES loans outstandingnumbered 1.6 million and amounted to Rp 845.6 billion (about $460 millionequivalent). Loan collection experience has been very good. A recent impactstudy undertaken by BRI (financed by USAID) shows that KUPEDES has had asignificant impact in poverty alleviation and in facilitating the access ofwomen to credit.

D. Bank Obiectives, Strategy sand Role in the Financial Sector

1.15 The Bank fully supports the GOI's objectives and its priotiti%Žs inthe further development and efficient growth of the financial cector. Overthe last several years, the Bank has been involved in policy dialogue with theGOI through sector and economic reports, informal policy notes and discussionon specific issues. The Bank has also supported the 6OT's reform initiativesthrough adjustment loans. In the past, the Bank's involvement in thefinancial sector focused primarily on supporting the development ofinstitutions and the provision of lines of credit to redress market failureseither in the availability of long-term credit or in the access to such creditfor "targeted, groups of borrowers. In light of the mott recent developmentsin Indonesia's financial sector (paras. 1.3-1.5), priority will now beaccorded to: (i) reducing further and/or eliminating the residue 104n marketsegmentations (ii) remedying infrastructural inadequacies for formal finance;(iii) strengthening the SCBs in order for them to compete in the new financialenvironments and (iv) fostering the further development of capital markets.The Bank is currently discussing with the GOI how it may support mosteffectively its strategy for addressing the above issues within the context ofa proposed Financial Sector Restructuring Operation. It is expected that thetargeted approach reflected in the Bank's financial sector lending operationsto date will be phased out as the policy environment for resource allocationimproves and the financial system becomes increasingly competitive andsophisticated. As a transitional measure, however, the Bank would continue tosupport efforts, on the basis of demonstrated financial viability andsustainability, to expand and to improve the efficient delivery of credit togroups of borrowers whose access to nonsubsidized credit has been constrainedin the past. BRI's Unit Desa system represents such an effort that-warrantscontinued Bank support. The proposed Second BRI/UPEDES Small Credit Projectsupports the further development of a nationwide, market-based banking systemthat not only provides financial servi^es to small borrowers and-savers, butalso has achieved substantial socioeconomic benefits (para. 3.19-3.26).

II. EXPERIENCE UNDER PAST WORLD BANK GROUP FINANCIAL SECTORLENDING OPERATIONS

2.1 To date, the Bank Group has approved a total of $1,488.1 million in16 operations for financing investment through financial intermediaries. Thegeneral focus of loans made prior to the onset of the GOI's financial reformprogram in 1983 reflected the Bank's traditional DFC lending focus on singlefinancial intermediaries with emphasis on institution-building. Theseprojects comprised one credit and five loans to BAPINDO ($367.4 million) andtwo to the Private Development Finance Company of Indonesia (PDFCI--$25.Omillion). The Bank Group's participation in the three Small EnterpriseDevelopment Projects (SEDPs--$350.7 million) aimed at supporting thedevelopment of Indonesia's small-scale enterprises through BI. Success inmeeting the project objectives of these operations was mixed.

2.2 The most recent Proiect Performance Audit Report (PPAR) No. 6403,covering the Bank Group's relationship with BAPINDO (Loans 1054-IND, 1437-INDand 1703-IND) over 1979-83, noted that, while BAPINDO had made some progressin terms of institutional development, its achievements fell short of mutualexpectations and BAPINDO continued to face substantial problems. The PPARmade a number of recommendations for improvements. Subsequently, duringimplementation of Loan 2277-IND (BAPINDO V), BAPINDO undertook a comprehensiveportfolio review, carried out a reorganization, and strengthened its capitalbase through an Infusion of equity from the GOI. PPAR No. 3862 on the secondPDFCI project (Loan 1363-IND) found that, although Bank loan proceeds weretransferred to sound industrial projects, performance towards institutionaland policy goals was disappointing, primarily because of the restrictivemacro-policy environment prior to the 1983 reforms.

2.3 The three SEDPe (Credit 785-IND, Loan 2011-IND and Loan 2430-IND)were In support of BIIs XIK/JMKP program.31 This program was funded throughliquidity credits and provided subsidized loans to end-users. As highlightedin the two Prolect Completion Reports on these lending operations, the SEDPsmet their objectives of generating jobs and training bank staff; however, ascredit operations they failed to achieve their policy and Institutionaldevelopment objectives due to several factorss poor borrower selectioncriteria; subsidized interest rates; insufficient spreads to intermediaries;and overly generous credit insurance. This combination resulted in poorcollection rates and high arrears. The major design flaws that wereidentified as having contributed to the failure of the SEDPs were avoided insetting up BRI's small credit (KUPEDES) scheme.

2.4 Following the 1983 reforms and in light of its previous experience,the Bank made two significant shifts in the mid-1980s in its approach tofinancial sector lending operations. One, it moved away from subsidizedlending; and two, it limited significantly single beneficiary lending, thusenabling end-users to have greater access to the Bank's term resources througha larger number of competing financial intermediaries. Recent projects (i.e.,the Export Development Projects--Loans 2702-tID and 2979-IMN for $229.5

31 Iredit Investasi Recil (KIK - small investment credit) and Kredit ModalKerja Permanen (RhIP - small working capital credit).

million, the Industrial Restructuring Project--Loan 3040-IND for $284 million,and the Small and Medium Industrial Enterprise Project--Loan 3041-INM for $100million) have incorporated an increasing number of participating financialinstitutions (from three under Loan 2702-IND to 13 under Loan 3041-IND).While specific subsector/entrepreneurial groups continued to benefit from theBank's lending activities to redress market failures either in theavailability of long-term credit or in the access zo such credit for targetedgroups of borrowers, all loan proceeds are passed on to the financialintermediaries at variable, market-determined interest rates; these funds, inturn, are onlent to qualifying enterprises at competitive and prevailingmarket rates as determined by the individual intermediaries. Increasingemphasis on environmental concern have also been incorporated in recentfinancial intermediation operations. Under Loans 2979-IND, 3040-IND and3041-IND, the assessment of environmental impact and the identification ofappropriate environmental safeguards are included in the subproject reviewprocesses provided under these loans. These projects are ongoing andimplementation has proceeded satisfactorily. The BRI/KUPEDES Small CreditProject (Loan 2800-IND) had the objective of helping promote the developmentof a market-based, financially viable, nationwide rural banking network(paras. 3.6 and 3.7).

2.5 To summarize, both the very substantial reforms of the financialsystem, which will lead increasingly to the allocation of credit according tocompetitive market signals, and the lessons from past operations, which havedemonstrated the ineffectiveness of supporting subsidized, directed creditprograms, will guide the Bank's further inv%i'vement in credit operations.Targeted credit and single beneficiary operations will be phased outappropriately, and replaced by the sectoral and system-wide approach nowevident in the proposed Financial Sector Restructuring Operation underpreparation (paras. 1.6 and 1.15).

III. PRESENT STATUS OF TEE BENEFICIARY AND THE KUPEDES PROGRAM

A. Bank Rakyat Indonesia

3.1 Bank Rakyat Indonesia (BRI) was founded in 1896 as a small savingsbank in central Java. It was later established as a fully state-owned bankunder Law No. 21 of December 18, 1968. The statutory mandate established forBRI under the 1968 law required it to: (a) assist the Government inimplementing national agricultural policies and rural development programs;(b) undertake commercial banking activities, primarily short- and medium-termlending to farmers, fishermen, small-scale industries and traders; and(c) supervise secondary rural banks in accordance with BI directives. Priorto the financial sector reforms of June 1983, BRI functioned largely as anagent of the Government charged with nationwide administration of a number ofliquidity credit programs for the rural and small-scale sectors. For severalof these programs, BRI had little or no say in client selection and verylimited, if any, credit risk as many program loans were insured or otherwiseguaranteed by the Government. Even so, the narrow spreads allowed to BRIunder most of the directed programs did not adequately cover its costs and, incombination with repayment guarantees, provided BRI with little incentive toemphasize loan collections, leading to a portfolio characterized by relativelyhigh arrears. As a result of these policies, BRI developed into a large,

-9-

relatively bureaucratic institution reliant on BI funding, operating at highcosts and realizing little profit.

3.2 Impact of the June 1983 Reforms. The introduction of the June 1983reforms (para. 1.3) coincided with the appointment of a new (and current)President-Director for BRI, who quickly recognized that BRI would no longer beable to survive solely as an administrative agent of the government and wouldneed to develop into a profitable and effective financial intermediary. Thus,BRlI's management put priority on defining a strategy for developing into abroad-based, sound and commercially viable bank. The strategy called for:(a) diversification of income generating activities to ensure BRI's short-termfinancial viability; (b) a comprehensive review of its organization andprocedures to improve internal efficiency and productivity; and (c) a productprofitability analysis to determine which activities to pursue, modify or dropso as to maximize profitability. To achieve the needed transformation, BRIsought outside technical assistance. In consultation with the Bank and withfunding initially provided under Loan 2430-IND and continued under Loan2800-IND, BRI in 1986 engaged a management consulting firm to provide anexperienced banking team to assist it in focusing on the main institutionalissues facing it and in recommending appropriate institutional, operationaland marketing changes (including an action program for implementing theserecommendations). This program was planned and implemented under the directsupervision of BRI's President and Board of Managing Directors.

3.3 BRI's institutional strengthening efforts have been encouraging. Itsmanagement has taken the initiative to proceed with a number of far-reachingactions designed to improve its financial position and performance in anincreasingly competitive financial sector. Annex 2 provides a more detaileddiscussion of these institutional efforts as well as an overview of BRI'sCi) organizational structure, (ii) loan portfolio, and (iii) financialcondition and performance.

3.4 Project Aid to BRI. Since 1972, BRI has participated extensively innumerous projects funded by bilateral and multilateral agencies. As shown inAnnex 3, IDA (five credits) and IBRD (eight loans) credit lines, includingtechnical assistance, totaling $284.3 million equivalent have been madeavailable directly to BRI since 1972. ADB (through nine loans) has extendedanother $122.5 million equivalent of such funding. As of December 31, 1989,the outstanding balances of IDAIIBRD and ADB funds were Rp 304.9 billion andRp 55.4 billion, respectively. BRI was also a participating bank in the SEDPs(KIKIKMKP programs), and is an executing bank for the Bank's Nucleus Estatesand Smallholders and tree-crop projects. BRI's performance as an implementingagency in ongoing Bank projects is satisfactory.

B. The BRI Unit Desa System and the KUPEDES Program

Background

3.5 Following the June 1983 liberalization measures, BRI was encouragedby the GOI to develop its Kredit Umum Pedesan (KUPEDES) scheme. Today, thisprogram makes available to creditworthy small borrowers, primarily in ruralareas, loans for directly productive activities (e.g., agriculture, trading

- 10 -

and cottage industry) at market-determined interest rates. It operatesexclusively through a subdistrict-based Unit Desa (village subbranch) system,which was established by the GOI in 1970 and originally administered by SRI toprovide credit related to the GOI's rice crop intensification (BIMAS) program.41BIGOI bore up to 75 percent of the credit risk on these BINAS loans andprovided an administrative subsidy to BRI to cover Unit Desa operatingexpenses. In 1983, the 001 recognized thst the BIMAS program had outlived itsusefulness and it was discontinued. BRI then faced the choice of eithers(i) abandoning the Unit Desa system (comprising some 3,500 offices and 14,000employees), since the operations would no longer be subsidized by the GOI5 or(ii) changing its role and functions in an effort to make it profitable.Based on the fact that ongoing Kredit Mini and Kredit Midi operations 5/ hadshown that there was a large loan demand for all kinds of village-basedentrepreneurial activities, and that Unit Desa staff had already learned howto administer smill credit programs, BRI opted for the second alternative. Asa result, BRI organized the Unit Desa system as an autonomous financial entitywithin the bank that would be operated as a separate profit center and wouldno longer participate in administered credit programs. While financialservices outside the large urban centers, especially those for small-sizedborrowers and savers, are provided by a variety of formal and informalfinancial intermediaries (paras. 1.10-1.13), BRI's Unit Desa system has becomethe most important nationwide scheme for both mobilizing savings and servingthe credit needs of the rural population.

Proiect Implementation Under Loan 2800-IND

3.6 In April 1987, the Bank approved a loan of $101.5 million for theBRIIKUPEDES Small Credit Project (Loan 2800-IND). This first KUPEDES Projectallowed the Bank to support an approach, which it had long advocated, thatneither promoted nor extended subsidized funds. Major design flaws that wereidentified as having contributed to the failure of the Bank's SEDPs(para. 2.3) were avoided in setting up the RUPEDES scheme. This project hadthe specific objectives of% (a) supporting BRI's efforts to develop the UnitDesa system into a financially viable network that would be able to providecredit on a nonsubsidized basis to all creditworthy small borrowers, tomobilize savings and to provide other banking services; (b) encouraging BRI toimprove its resource mobilization efforts so that it could eventually fundKUPEDES loans with deposits raised through the Unit Desa system; (c) reducingBRI's reliance on DI liquidity credits, which had been initially provided forthe start-up of the KUPEDES program; and (d) improving the overallinstitutional capability of BRI as well as that of the KUPEDES program. This

4/ The BIMAS program aimed at improving agricultural production andpractices through the provision of physical inputs, technicalassistance and short-term credit through the Unit Desas at a subsidizedinterest rate of 12 percent per annum.

5/ Established in 1973 and 1979, respectively, these programs made creditavailable to small borrowers outside of the BIMAS program, primarilyfor off-farm economic activities. Under Kredit Mini, the loan ceilingwas Rp 200,000; under Rredit Midi, it was Rp 500,000.

- 11 -

first KUPEDES Project comprised a credit component of $96.7 million and atechnical assistance (TA) component of $4.8 million, which was complementedwith a TA grant of $10.0 million provided by USAID.

3.7 Implementation of the first KUPEDES project has proceeded verysatisfactorily. The project's credit component was fully disbursed within the27-month period estimated at the time of appraisal; Bank loan proceedsaccounted for 9.4 percent of total KUPEDES disbursements and 46 percent of theincremental growth in the KUPEDES portfolio during this period. Of the TAcomponent, $3.5 million has been disbursed and BRI recently submitted to theBank its proposal for utilizing over the next two years the remaining $1.3million for research and training activities as outlined under the project.BRI's efforts and success in achieving project objectives have not onlygenerally met original appraisal expectations, but often exceeded them.Implementation of the USAID project has also proceeded satisfactorily and thegrant is expected to be fully disbursed in early 1991. With the USAID grantproceeds, (i) a team of long-term consultants was recruited to advise BRIsenior management on rural banking policy and training matters, (ii) a team oflong-term consultants developed and implemented a computerized accountingprogram for the Unit Desas, (iii) 600 Unit Desas were equipped with computers,(iv) the first-phase construction of five regional Unit Desa training centerswas undertaken, and (v) approximately $2.0 million of Unit Desa trainingexpenses were funded. A formal evaluation of this coma?onent will be done byUSAID in July 1990.

Organization

3.8 The Read Office. BRI's Board of Managing Directors is the mainauthority for establishing policy regarding Unit Desa activities. Policydirectives (in the form of operational circulars) art communicated from theBoard through the regional offices and branches to their respective UnitDesas. BRI's Unit Desa Policy and Unit Desa Strategy Statements (Annexes 4and 5, respectively) outline the overall goals and operational objectives ofthe Unit Desa system. These statements were reviewed and agreed with the Bankduring appraisal, and the adoption of these statements by BRI's Board ofManaging Directors was a condition of loan negotiations. During loannegotiations, it was agreed that neither statement would be amended in amaterial way without the prior agreement of the Bank. In late 1988, inrecognition of the growing importance of the Unit Desas as a major service andprofit center within BRI, the Village Unit Development Division, originallycreated for overall responsibility of Unit Desa operations within the thenexisting Cooperatives, Farmers and Fishermen Credit Department, wasreorganized and upgraded to a full Department known as Business Unit Desa(Chart 1). BRI senior management is assisted on Unit Desa and rural banking-related matters by a team of advisors who report directly to the PresidentDirector and coordinate on a day-to-day basis with the Business Unit DesaDepartment. Funding for the retention of this advisory team, currentlyfinanced with USAID grant assistance, is provided under the proposed project(para. 4.5).

3.9 Regional and Branch Offices. While the regional offices oversee theoperations of the branches, branches have primary responsibility for the day-to-day supervision of Unit Desa activities. Each branch has at least one Unit

- 12 -

Desa Business Manager (UBM--one for every four Unit Desas), who routinelyvisits and monitors Unit Desa operations, cash balances and financialcontrols; in those branches where there are more than ten Unit Desas, a UnitDesa Officer (UDO) is assigned to oversee the UBMs. As of December 31, 1989,there were 839 UBMs and 127 UDOs. Although the Unit Desa itself collects dataand compiles standardized monthly reports, Unit Desa operational and financialdata are consolidated and analysis is undertaken at the branch level.Overall, the present information system for Unit Desa operations is adequate.

3.10 The Unit Desa. The standard Unit Desa comprises a manager, a loanofficer, a bookkeeper and a cashier. Standardized workload coefficients(based on number of loans, number of savings accounts and average daily cashtransactions) have been developed that determine the number of additional loanofficers, bookkeepers and cashiers needed in order to operate efficiently aUnit Desa. Once the volume of Unit Desa operations requires 11 staff members,a Unit Desa is split into two. 'Posts", comprising two-person teams, areattached to those Unit Desas where there is significant business activity inoutlying areas but insufficient transactions to justify the creation of afully-staffed Unit Desa. As of end-1989, BRI's Unit Desa system constituted2,843 Unit Desas and 835 Posts;6/ total employees numbered 13,666: 2,805managers. 3,323 loan officers, 4,109 bookkeepers and 3,429 cashiers. Due tothe tremendous growth in operations during 1989, the Unit Desa system iscurrently understaffed, with vacancies estimated at around 900; this situationcould jeopardize both the continued growth and the quality of Unit Desaoperations. To rectify the problem, BRI recently implemented a new systemthat should ensure, in future, that Unit Desa staff vacancies are promptlyfilled by qualified staff. Each region identifies its total annual Unit Desapersonnel requirements on the basis of 'projected* needs (taking intoconsideration lending and savings growth prospects, internal promotions andnatural attrition, as well as establishing a 5 percent reserve at the branchlevel to fill temporary vacancies resulting from regular Unit Desa staff beingsick, on leave or in training), rather than on current vacancies only.Second, for entry-level cashier and bookkeeping positions, psychologicaltesting will no longer be required; this should produce a larger pool ofcandidates available for final placement. (A recent survey of traineecandidates showed that 40 percent of those applicants who passed the oralinterview and the security clearance test then proceeded to fail the finalmajor recruitment hurdle, the psychological test.)

3.11 Training. Recognizing that its existing training facilities werephysically incapable of accommodating the type of training program that wasneeded for its Unit Desa system, BRI decided in 1986 to establish fivetraining centers exclusively for Unit Desa personnel at Bandung, Padang,Yogyakarta, Surabaya and Ujung Padang. With USAID technical assistance, twoof these centers are now operational, another two will become operationalaround mid-1990 and the remaining one is expected to be finished in early1991. To date, 52 trainers have been locally recruited and trained by BRI and

61 As of end-December 1989, approximately 7 percent of BRI's Unit Desasare located in urban centers (defined as those cities, includingJakarta, in which BRI's regional headquarters are located) and accountfor about 9 percent of total Unit Desa savings deposits and 5 percentof the outstanding KUPEDES portfolio.

- 13 -

its advisory team (another group of 30 trainers will be ready for assignmentin aid-1990). Courses, based on vell-prepared curricula, range from fourweeks for bookkeepers and cashiers, to 12 weeks for the Unit Desa manager.Shorter courses (two weeks) have also been developed for the UDOs and UBMs.Formal training began in 1988, with priority given to the Unit Desa managersand loan officers. Total staff trained in 1988 were slightly less than 3,000;another 5,200 were trained in 1989. BRI plans to train 7,950 staff in 1990,8,750 in 1991 and 11,850 in 1992. This program is ambitious, but attainable.

Scope and Terms of KUPEDES Lending

3.12 Eligibility. The main criterion for loan approval is thecreditworthiness of the borrower. KUPEDES loans are generally intended fordirectly productive activities, although fixed-income earners can also qualify(less than 5 percent of total loan volume is currently extended to thisgroup). Borrowers are required to provide proof of income sources and/or acertification of their business activities. All loan applications require acosigner, who is normally the applicant's spouse.

3.13 Collateral. All borrowers must provide collateral sufficient tocover the value of their loans. While land, buildings or any other propertymay be accepted, most borrowers use land (including house plots). A borroweris classified on the basis of his repayment record, and this establishes theperson's limit for subsequent loans. Since the legal system for realizingcollateral in the case of loan default is time-consuming and complicated, thedocumentation of collateral for each loan is more for the purpose ofestablishing the borrower's ability and serious intent to repay than it is toprovide a basis for legal action or an alternative source of loan repayment.

3.14 Repayment Schedule. Repayment schedules for working capital loansrange from three to 24 months, with or without grace periods of three to ninemonths. Single balloon payments for three- to 12-month maturities are alsoavailable. Repayment schedules for loans for investment purposes range up toa maximum term of 36 months, including grace periods.

3.15 Loan Size. The minimum size KUPEDES loan is Rp 25,000 ($14equivalent). In practice, few loans of less than Rp 100,000 ($55 equivalent)have been made. The maximum KUPEDES loan amount was initially set at Rp 1million. This was raised in April 1986 to Rp 2 million and to Rp 3 million inmid-1988. (On a pilot basis begun in late 1988, it was raised toRp 5 million--$2,730 equivalent.) This upper limit is generally availableonly to repeat customers who have promptly and fully repaid previous loans.

3.16 Interest Rates. Unlike the approach reflected in previous officialcredit programs to support small borrowers, the market-based approach tosetting interest rates for KUPEDES loans focuses on establishing rates thatwill ensure (a) prompt delivery of credit and (b) adequate profitability forthe financial intermediary. The underlying assumption is that for smallborrowers, access to credit is more important than the interest ratesinvolved. The decision to base KUPEDES interest rates on prevailing marketconditions meant that BRI had to: (a) set deposit rates sufficiently high toattract savings; and (b) set lending rates sufficiently high to cover itsfunding and operating costs, including adequate provisions for loan losses,

- 14 -

and to permit it to earn a reasonable profit. As a result, BR? set onlendingrates of 1.5 percent per month for working capital loans, calculated on theoriginal loan amounts, and 1 percent per month for investment loans, similarlycalculated. [At the time, this differential was considered necessary toencourage investment activity. Recent changes in KUPEDES lending parameters,however, recognized the need to rationalize this aspect of KUPEDES interestrates (para. 3.17).] Since onlending rates are stated in terms of interest onthe original amount borrowed rather than on the declining balance, theeffective annual interest rates were 31.7 percent for working capital loansand 21.5 percent for investment loans.71 While these rates are higher thaneffective market rates for larger loans (which currently range from 17 to22 percent), they compare favorably to rates charged by other lenders tosmaller borrowers (Table 1.1). In addition to the basic interest rate, there4s a sprompt repayment incentive (IPTW)" fee of 0.5 percent per month (alsocalculated on original loan amounts) collected monthly. This is effectivelyan upfront penalty for failure to pay loan installments on time. It isreturned, in full, at the time of final loan payment to borrowers who havepaid all installments on time.

3.17 Revised KUPEDES Londinf Parameters. BBl's experience to dateindicates that there is room for increasing its XUPEDES op)rations byprudently expanlkng the scope of its coverage, specifically, by more activelysoliciting urban borrowers as well as *larger* small borrowers (both rural andurban). During appraisal, the following new loan parameters were agreed withBRI and they became operationally effective on May 1, 1990t

(a) an increase in the maximum loan size to Rp 25 million (approximately$13,700 equivalent);

(b) a revision of the interest rate structures

Ci) on loans of Rp 3 million or less--l.5 percent per month,calculated on a flat rate basis on the original loan principal;and

(ii) on loans of more than Rp 3 millioa--l.5 percent per month,calculated on a flat rate basis on the first Rp 3 million of tneoriginal loan principal and 1.0 percent per month, calculated ona flat rate basis on the amount of the original loan principalexceeding Rp 3 million.

Working capital and investment loans would carry the same rate. Theeffective annual interest rate would be 31.7 percent for loans ofRp 3 million and less; for loans of more than Rp 3 million, theeffective annual interest rate would range from slightly less than31.7 percent to 22.7 percent for a maximum loan of Rp 25 million;

(c) the IPTW (prompt repayment incentive) fee of 0.5 percent per month,still calculated on a flat rate basis on the original loan principal,

71 For loans (shorter as well as longer than one year) with grace periods,the effective interest rate is kept basically the same as for thestandard one-year loan vith no grace period.

- 15 -

would be refunded to the borrower (on a pro-rata basis) on asemiannual basis if all repayments are made on time as per theoriginal amortization schedule for each respective six-month periodsand

(d) in instances where the borrower decides to repay his loan before itbecomes due, he/she would not be required (as previously) to pay allinterest due on the prepaid amount as computed at the time the loanwas extended.

These changes achieve several objectives. They allow the Unit Desas to seeklarger clients while providing competitive rates (economies of scale result inlower processing costs for larger loans, thus permitting lower onlending ratesto the end-users). They also enable the Unit Desas to provide financialincentives to their good clients [i.e., items (c) and (d)] withoutjeopardizing their lending margins. In addition, the revised interest ratestructure corrects the previous situation in which not only were investmentloans being effectively cross-subsidized, but also Unit Desa staff weredeclining to extend investment loans because they realized that they werelosing income on these loans.

IMPEDES Lending Ooerations

3.18 During its six years of operations, the Unit Desas have disbursedabout Rp 3.4 trillion in KUPEDES loans (almost $1.9 billion equivalent usingthe end-1989 official exchange rate); the total number of loans made duringthis time was 6.4 million (Annex 6, Table 1). Average loan size has increasedalmost threefold since 1984--from Rp 287,000 to Rp 777,000 in 1989. Thenumber of annual loans made during this same period has increased twofold--from 0.64 million to 1.38 million. After stabilizing at around 1.1 millionloans annually over 1986-88, the number of loans in 1989 increased by21 percent. Based on annual disbursement and repayment data, the average loanmaturity remains around 12 months. Sector-wise, trading continues to account(by Rupiah) for about 60 percent of KUPEDES loans (compared to around70 percent in 1987 and earlier years). Agriculture accounts for another26 percent. industrial activities account for only 2 percent andtransportationliervices for another 8 percent. General consumption loans,extended to fixed-income (salaried) borrowers only, account for the remaining4 percent. Geographically, 70 percent of the KUPEDES loan portfolio isconcentrated in Java (a decline from 75 percent in 1986). However, this isnot unusual' considering that more than 60 percent of Indonesia's populationlives on Java and that the level of economic activity there is relativelyhigher than in the other islands.

Characteristics and Impact of KUPEDES Lending

3.19 In mid-1989, BRI undertook a general survey of KUPEDES borrowers tomeasure the socioeconomic benefits derived from the lending program. Whilethe results of KUPEDES lending have been generally assessed as posit1v,i this

16 _

survey demdnstrates quantitatively the dramatic success of a relatively youngprogram. The major survey findings are summarized in paras. 3.20-3.26 below.8/

3.20 Profile of KUPEDES Borrowers. The survey results confirm thatKUPEDES mainly serves nonagricultural sectors of the rural economy. Loans forsmall traders, cottage industries and service occupations accounted for78 percent of total lending in the areas sampled. These activities arecharacterized by a very rapid turnover of working capital (an average of onceevery 23 days). Traders often turn over their entire working capital daily.Every time capital is turned over, a profit ranging from 5 percent to25 percent is earned. For this reason, borrowers who take out working capitalloans for nonagricultural activities are relatively unconcerned about theinterest rate charged. With regard to agricultural lending activities,KUPEDES loans are used mainly for livestock rather than rice growing due tothe existence of the government-sponsored KUT program which supports riceproduction. The working capital turnover on agricultural loans averages 153days, but borrowers often opt for monthly repayments, which are paid fromincome earned on their other economic activities.

3.21 The majority of KUPEDES borrowers come from landless and nearlandless families. About 48 percent of the borrowing families surveyed own norice land at all, while 25 percent own micro plots of 2,000 square meters orless. Although many borrowers own no cropland, they usually do own a smallhouse plot which provides the security for the loan; the percentage of loansguaranteed by house plots is 66 percent. Only 3 percent of borrowers sampledhave ever had a loan from a private bank and less than 9 percent havepreviously had a loan from a private bank or government bank/agency. For themajority of borrowers, the BRI Unit Desa office is their first-ever contactwith a formal sector credit institution.

3.22 The participation rate of women in the RUPEDES program is high.About 25 percent of borrowers are women. The size of loans given to femaleborrowers does not vary significantly from the size of loans given to maleborrowers. Moreover, about 32 percent of loan funds are utilized byenterprises that are owned and operated by women, reflecting the fact thatloans taken out in the husband's name are often shared with the wife.

3.23 Development Impact. It appears that KUPEDES lending has directlycontributed to poverty alleviation at the village level. Survey resultsindicate that RUPEDES lending has both increased employment for hired workersin borrower enterprises and increased the incomes for borrower families whowere below the poverty line. Using Bank guidelines, 15 percent of first-timeRUPEDES borrowers in 1986 fell below the poverty line; this roughlycorresponds to the overall incidence of rural poverty which was established at16 percent of the rural population in 1987. After an average three years ofprogram participation, however, only 4 percent of KUPEDES borrowers were stillbelow the poverty line. on a national scale, this means that an estimated186,000 families have moved out of the seriously poor category.

8/ A more detailed discussion of this survey (Briefing Booklet--KUPEDESDevelopment Impact Survey) is available in the Project File.

- 17 -

3.24 KUPEDES has had a major impact on profits earned by borrowerenterprises. Prior to taking out their first XUPEDES loan, borrowerenterprises earned an average of Rp 141,098 (about $75) per month. After anaverage three years of program participation, this monthly income had grown toRp 327,595 (about $180); after adjusting for inflation, that is a realincrease of 94 percent. The four major reasons why enterprise incomes haveincreased so substantially aret

(a) borrowers with trade enterprises often double or triple the amount ofgoods bought and sold after getting their KUPEDES loans;

(b) borrowers with small industry enterprises often double or triple theamount of goods produced after getting their KUPEDES loans;

(c) borrowers who previously obtained trade goods or raw materials oncredit from suppliers and paid high interest rates (an average of5.7 percent per month) can now pay cash; and

(d) borrowers who previously experienzed work stoppages du to a lack ofworking capital can now work continuously year-round.

3.25 KUPEDES lending has also contributed to employment growth. Theaverage borrower surveyed has participated in the program for three years andhas had three or more loans. In this time, employment, measured in terms ofnumber of workers per enterprise, has increased an average of 65 percent; ifemployment is measured by annual labor hours per enterprise, the averageincrease is 84 percent. In absolute terms, employment has increased for bothunpaid family workers and hired workers. Proportionally, however, the shareof labor contributed by unpaid family workers has declined by about 7 percent,if measured in terms of number of workers, and by 18 percent, if measured inlabor hours. The most dramatic increase in employment has been for piece-ratevorkers, many of whom are women who work in their own homes. These workersallow borrowers to enlarge their labor force without building new work places.

3.26 The standard of living of many KUPEDES borrowers has subsequentlyimproved. Personal consumption has increased with many borrowers reportingthat they are now able to purchase new clothing, radios, furniture andmotorcycles. Many have made housing repairs, added rooms to their houses oreven built new houses. Borrowers who formerly relied on a traditional medicalspecialist when ill now visit the local health worker or a doctor in town.Women who formerly relied on traditional midwives are now going to maternityclinics. Many families report an increased frequency in the consumption ofprotein foods such as meat and fish. Many families who had no savings threeyears ago now have savings in the form of gold jewelry or savings accounts.The average annual amount spent on school fees and related educationalexpenses by families who have received KUPEDES loans has increased fromRp 171,272 to Rp 338 791 per household, for a real increase of 65 percent.

- 18 -

Unit Desa Administration and Financial Operations

3.27 In 1984, BRI developed accounting and monitoring systems thatpermitted the Unit Doses to fund their respective operations and to identifytheir respective costs and profits. This entailed: (a) reconstruction ofeach Unit Desa's financial statements; (b) establishment of a mechanism toenable each Unit Desa to fund its loan operations, irrespective of the amountof deposits it could raise; (c) creation of a mechanism to allow the Unit Desato invest (without incurring a loss) deposits it had mobilized in excess ofloan demand; and (d) allocation of overhead costs associated with the branch'ssupervision of the Unit Desa. To ensure that the system's sustainability isnot based on subsidized funds, BRI adopted an internal transfer pricingmechanism so that funds loaned to the Unit Desas are at an interest rate thatis no less than the rate paid by the Unit Desas on three-month time deposits;at the same time, Unit Desas with surplus savings can deposit these funds withtheir branches and receive this same rate (currently 16 percent). Thismechanism promotes savings mobilization (deposits are cheaper than borrowedfunds), while those Unit Desas whose savings exceed loan demand are notpenalized for having successfully mobilized resources. Another distinguishingfeature of the Unit Desa system is its incorporation of an annual "bonus"incentive. The staff of each Unit Desa are paid a bonus of up to one month'ssalary that is based directly on the financial performance of the unit. AUnit Desa Development Fund was also set up under the first KUPEDES Project towhich was allocated at least 50 percent of the margin between the cost of Bankloan proceeds to BRI and the onlending rate to the Unit Desas. These fundsare used for expenditures in support of the Untt Desas.

Funding of the Unit-Desas and Resource Mobilization

3.28 Funds available to the Unit Desas for extending RUPEDES loans comefrom several sources:

(a) Equity. This consists of the proceeds of the Government's grant ofRp 66.7 billion to BRI for the Kredit Mini program which, in 1984,were reallocated for funding KUPEDES loans. BRI distributes thisgrant among the Unit Desas as 'an equity contribution' of Rp 19million each;

(b) Liquidity Credit from DI. This consists ofs (i) the conversion ofRp 43 billion in liquidity credit originally provided by BI for thepurpose of funding the Rredit Midi program; and (ii) an initialRp 100 billion of liquidiiy credit made available to BRI for KNUPEDESlending. Undor the first KUPEDES Project, it was agreed that BRIwould pay a single consolidated rate of 12 percent per annum on theseliquidity funds,9/ and that they would be repaid on a quarterly basis

9/ Originally, the interest rate to BRI on the BI liquidity credit was15 percent, excepting amounts utilized for investment purposes on whichthe rate would be A percent. Since a working capital/investment blendof 75s25 was assun*d at the time, BI charged BRI an interest rate of12 percent for the sake of administrative convenience, with anunderstanding that this rate would be adjusted at a later date.

- 19 -

over seven years, beginning in the first quarter of 1989. (BRI iscurrent in making the agreed repayments.) This arrangement wasreconfirmed at negotiations:

(c) Official Loans. Under Loan 2800-IND, World Bank funds of Rp 165.7billion have been disbursed (to be repaid semi-annually over 15years, exclusive of a five-year grace period, beginning in January1993). In 1989, BRI received from the Exim Bank of Japan Rp 50.7billion for local cost financing associated with the first KUPEDESProject (to be repaid semi-annually over 15 years beginning inSeptember 1991); and

(d) Savings Mobilization by the Unit Desas. The Unit Desas provide twomajor savings instruments: TABANAS and SIMPEDES. Tabungan Nasional(Small Savings Program--TABANAS) is a national savings schemesponsored by BI and available to depositors in all banks, both stateand private. The interest rate is currently 16 percent on theminimum monthly balance (zero percent on balances of less thanRp 250,000). Under TABANAS, withdrawals are restricted to two permonth. Simpanan Pedesan (Village Savings Program--SIMPEDES) wasintroduced by BRI as a Unit Desa savings instrument in 1985.SIMPEDES interest rates, calculated on the basis of minimum monthlybalances, are zero percent on balances of less than Rp 25,000,9 percent on balances from Rp 25,000 to Rp 200,000, and 13.5 percenton balances above Rp 200,000. The saver is permitted unlimitedwithdrawals; this is considered the key factor behind the success oftbe program. SIMPEDES accounted for 75 percent of total Unit Desadeposits as of end-1989. In addition to the TABANAS and SIMPEDESaccounts,10/ Unit Desas offer time deposits with maturities rangingfrom three months to one year and checking (Giro) accounts, which areheld primarily by local government agencies.11/

As of December 31, 1989, total resources available to the Unit Desa systemamounted to Rp 1.4 trillion (approximately $765 million equivalent) as shownin Table 3.1 below.

10/ At the end-1989, the Unit Desas held 3.5 million TABANAS accounts(averaging Rp 32,700, or about $18 equivalent) and 2.65 millionSIMPEDES accounts (averaging Rp 261,100, or about $143 equivalent).

111 BRI introduced a new savings instrument in December 1989 calledSIHASKOT available at both Unit Desas (initially in urban locationsonly) and branch offices. It is similar to SINPEDES, but provides aninterest rate of 14.5 percent on accounts larger than Rp 5.0 million.

- 20 -

Table 3.1t TOTAL RESOURCES AVAILABLE TO THE UNIT DESA SYSTEK, END-1989

Resource Rp (billion) Z of total

Kredit Mini (equity) grant 66.7 4.8Converted Kredit Midi }BI liquidity credit } 165.4 11.8IBRD Loan 2800-IND 165.7 11.8Exim Bank of Japan 50.7 3.6TABANAS (Unit Desas only) 113.7 8.1SIMPEDES 694.7 49.6Deposits and Giro 145.1 10.3

Total 1,402.0 100.0

3.29 Auditing and Internal Control. Due to the sheer number of A.*nit Desasand the staffing constraints currently faced by BRI's Internal AuditDepartment (para. 11 of Annex 2), BRI has not audited annually each t1 itsUnit Desas. In 1989, only 542;(or 19 percent) of BR1's 2,850 Unit Dotas wereindividually audited. Inasmuch as Unit Desa operations are reflected in thefinancial position of the branches, however, all Unit Desas are audited,albeit in a very limited fashion. SRI relies primarily on the financialreview and supervision of the Unit Desas as performed by the branches andoverseen by the regional and headquarters offices (para. 3.9). Thii does notmean that this supervision capability is intended or expected to replace theinternal audit function. With the expansion and strengthening of BRI'sInternal Audit Department, it is expected that 700 Unit Desas will be auditedin 1990, with all Unit Desas being audited beginning in 1992. Externalauditing at BRI is performed by the Government's Agency for Financial andDevelopment Supervision (BPXP). BPXP's audit teams visit all BRI,regional andbranch offices, but they only audit Unit Desas on a sample basis.'

Financial Position and Performance of the Unit Desas

3.30 Financial Position. The Unit Desas' financial position since 1984 ispresented in Annex 6, Table 2. During'the past six years, the Unit pesasystem has registered impressive growth. Between end-1984 and end-1989, totalassets increased sevenfold, from Rp 0.18 trillion to Rp 1.29 trillion ($700million equivalent). The outstanding KUPEDES portfolio has increased fromRp 110.7 million' to Rp 845.6 million ($465 million equivalent), althoughannual growth rates have fluctuated greatly, e.g., from 25 percent in 1987 and -~

1988, to 57 percent in 1989, to'78 percent in 1985. During 1984-87, RUPEDESloans accounted for 62 percent to 84 percent of total assets. As of end-1988and end-1989, however, as a result of the Unit Desas''very quccessfut resourcemobilization efforts that produced large net surpluses of loanable funds,these respective ligures declined to 60 percent and 65 percent, respectively.Savings deposits (in particular, SIMPEDES5 have also increased dramatically,from Rp 40.2 billion at end-X984 to Rp 920.6 billion ($509 million equivalent)at end-1989. [At the end-1989, these savings represented 14 percent of BRU's

,- - l .~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~'

- 21 -

total deposits.] Like the KUPEDES portfolio, annual growth rates havefluctuated widely, varying from about 75 percent in 1985 and 1988, to132 percent :n 1986, to 94 percent in 1989. As of December 31, 1989, thoseUnit Desas with surplus liquidity showed a total cash position of Rp 452.5billion, while those with negative liquidity positions showed net "branchborrowings' amounting to Rp 198.4 billion. In aggregate, adjusting forvarious reserve requirements and working cash margins, the Unit Desas' netliquidity position was Rp 545.5 billion (about $300 million equivalent).

3.31 Financial Performance. After incurring initial start-up losses(wbich were expected) in 1984 and 1985, the Unit Desa system has generatedsteadily increasing annual net profits (before taxes), totaling Rp 9.8 billionin 1986 and increasing to Rp 36.9 billion ($20.3 million equivalent) in 1989(Annex 6, Table 3). As shown in Table 3.2 below, these annual profits reflecta reasonable and fair return on the Unit Desas average total assets. TheGait Desas' profitability performauce also demonstrates the system'sincreasingly important role in contributing to BRI's overall profitability--in1988 and 1989, the Unit Desas accounted for 30 percent of BRI's total netincome (before taxes). The key factors, as reflected in the other financialindicators shown in Table 3.2, that have enabled the Unit Desas to performprofitably includes (i) an adequate lending spread; (ii) the maintenance of ahigh-quality KUPEDES portfolio (para. 3.32); and (iii) firm control ofpersonnel and administrative expenses. It should be noted that, in 1989, twopolicy changes resulted in a significant increase (in absolute Rupiah terms)in personnel and administrative expenses: one, all Unit Desa staff wereupgraded to full BRI employee status (resulting in higher salary and employeebenefits); and two, all training costs for Unit Desa personnel are nowexpensed directly against the Unit Desa system. Despite these changes, theUnit Desas' profitability remained very satisfactory and the upgradingexercise had the additional benefit of improving staff morale.

3.32 Quality of Portfolio. The quality of the KUPEDES loan portfo.iocontinues to be good. As of December 31, 1989, only Rp 45.7 billion (or lessthan 5.5 percent of the outstanding portfolio) were in arrears, with arrearsvery conservatively defined as any payment of principal overdue by one day ormore (Annex 6, Table 4). Total arrears of more than one day beyond finalinstallment due dates totaled Rp 20.7 billion, or 2.5 percent of theoutstanding portfolio. Much of the Unit Desas' succes,' in keeping KUPEDESloan arrears low can be attributed to prudent lending and accountingprocedures, intensive follow-up by Unit Desa staff of their borrowers, andclose supervision and monitoring by the branches (as well as by theheadquarter office). Recent steps taken by BRI to ensure adequate and timelyrecruitment of personnel will help ensure that this quality can be maintainedin future (para. 3.10). The Unit Desas have also proved successful incollecting loans previously written off--about 25 percent of them as of end-December 1989. BkI's comprehensive and ongoing training program for the UnitDesa personnel also plays a positive role (para. 3.11). BRI has clearlydemonstrated its commitment to ensuring that the experience of high arrearagesunder previous credit programs for small borrowers is not repeated. However,as under the first KUPEDES Project, to enable the Bank to provide timelyguidance in case of unforeseen rapid portfolio deterioration, BRI agreed atnegotiations to consult with the Bank and to draw up within three months atime-bound action program, acceptable to the Bank, for dealing with arrearsonce they reached a level of 8 percent over a continuous six-month period. BRI

- 22 _

Table 3.2: INDICATORS OF UNIT DESAS' FINANCIAL PERFORMANCE, 1984-89

1984 1985 1986 1987 1988 1989

Average Total Assets(Rp billion) 89.4 239.6 364.2 469.9 624.1 1,013.7

Average Borrowings(Rp billion) 62.5 176.2 289.5 382.1 516.1 885.8

As a I of Average Assets(a) Income from lending lb 20.2 20.8 23.6 24.6 23.2 19.3(b) IPTW forfeited n.a. n-a. n.a. 2.0 2.4 1.9(c) Other income 5.1j, 3.7Lc 4.1k 3.0 3.4 4.8(d) Gross income 25.3 24.5 27.7 29.6 29.0 26.0(e) Financial expenses 4.9 8.2 9.6 10.2 9.8 9.5(f) Gross spread (d-e) 20.4 16.3 19.1 19.4 19.2 16.5(g) Salary and personnel

expenses id 34.0 13.8 9.3 8.4 7.0 6.0(h) Administrative and

other expenses 5.0 1.9 2.8 2.6 3.0 4.5Mi) Provision for bad debt 9.4 1.0 3.3 3.6 4.3 2.4(j) Profitiloss le (28.0) (0.4) 2.7 4.8 4.9 3.6

Lendint Margin(k) Income from lending as Z

of average loan portfolio 26.2 25.9 29.0 29.8 29.8 28.3(1) Financial expenses as 2

of average borrowings 7.0 11.2 12.1 12.6 11.9 10.9(m) Spread on lending (k-i) 19.2 19.7 16.9 17.2 17.9 17.4

Provision for Bad Debt as Iof Outstanding Loan Portfolio 6.6 4.3 5.9 4.9 6.3 4.7

Salary and PersonnelExpenses 1d as S of Aver-age Loan Portfolio 44.1 17.3 11.4 10.2 9.0 8.7

/a Before provisions.Ib Income from lending excludes IPTW collected; likewise, IPTW collected (and

which is set aside in a reserve) is excluded as an expense in the expensecomputations below.

/c Includes IPTW forfeited./d Excludes bonuses, which are included in administrative and other expenses.le Before taxes. Unit Desa annual profits (losses) are appropriated by BRI.

- 23 -