The World Nuclear Industry Status Report 2012 An Independent Assessment 15 Months After Fukushima (see www.WorldNuclearReport.org) Mycle Schneider International Consultant on Energy and Nuclear Policy Paris, France Mycle Schneider Consulting (MSC) IAEA-INPRO-Dialogue Forum “Long-term Prospects for Nuclear Energy in the Post-Fukushima Era” Seoul, 29 August 2012 Seoul, 29 August 2012

Transcript

The World Nuclear Industry Status Report 2012

An Independent Assessment 15 Months After Fukushima (see www.WorldNuclearReport.org)

Mycle Schneider International Consultant on Energy and Nuclear Policy

Paris, France

Mycle Schneider Consulting (MSC)

IAEA-INPRO-Dialogue Forum “Long-term Prospects for Nuclear Energy in the Post-Fukushima Era”

Seoul, 29 August 2012

Seoul, 29 August 2012

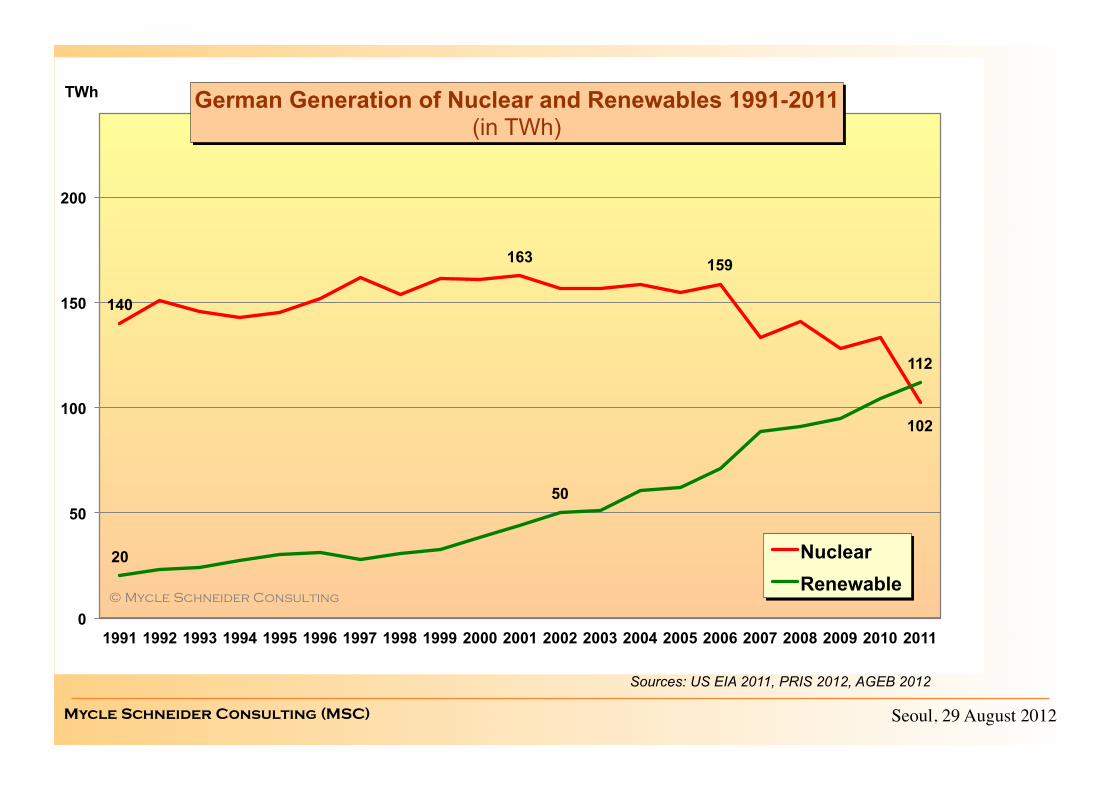

Seoul, 29 August 2012 Mycle Schneider Consulting (MSC)

Source: IAEA-PRIS, MSC, 2012

Seoul, 29 August 2012 Mycle Schneider Consulting (MSC)

Source: IAEA-PRIS, MSC, 2012

Seoul, 29 August 2012 Mycle Schneider Consulting (MSC)

Current Status of the Nuclear Power Plants in Japan(as of August 17, 2012)

: In�operation

(2

unit,�2.36GWe)

:�Outage�for�the�periodic�inspection

(35�units,�30.61GWe)

:�Shutdown�due�to�tsunami�

andand�the�government�request

(13�units,�13.18�GWe)

TOTAL�:�50

units,�46.15

GWe

Abolished

Seoul, 29 August 2012 Mycle Schneider Consulting (MSC)

Source: IAEA-PRIS, MSC, 2012

Seoul, 29 August 2012 Mycle Schneider Consulting (MSC)

Source: IAEA-PRIS, 2012

0

100

200

300

400

500

600

700

800

900 U

nite

d St

ates

Fran

ce

Rus

sia

Japa

n

Sout

h K

orea

Ger

man

y

Can

ada

Ukr

aine

Chi

na

Uni

ted

Kin

gdom

Swed

en

Spai

n

Bel

gium

Taiw

an

Indi

a

Cze

ch R

epub

lic

Switz

erla

nd

Finl

and

Bul

garia

Bra

zil

Hun

gary

Slov

akia

Sout

h A

fric

a

Rom

ania

Mex

ico

Slov

enia

Arg

entin

a

Net

herla

nds

Paki

stan

Arm

enia

Nuclear Electricity Generation in the World in 2011 (per country) (net TWh)

Seoul, 29 August 2012 Mycle Schneider Consulting (MSC)

Source: WNISR 2012

Evolution of EPR Cost Estimates 2003-2012

Seoul, 29 August 2012 Mycle Schneider Consulting (MSC)

• ”Most nuclear projects are financed either by Governments or by very large utilities.”

• ”They are at high risk of being completed late and significantly over budget.”

• ”Nuclear projects face heightened political risk relative to other energy assets.”

• ”Public acceptance is not assured and this brings reputational risk.”

• ”No clear idea about the economics.”

French BNP-Paribas Bank Conclusions on Nuclear New Build

Source: BNP-Paribas 2012, “How will financing be secured in the future?”, Mark Muldowney, Presented at the European Nuclear Forum, Brussels, 19 March 2012

Seoul, 29 August 2012 Mycle Schneider Consulting (MSC)

Source: WNISR 2012

Seoul, 29 August 2012 Mycle Schneider Consulting (MSC)

Source: WNISR 2012

Long Term Credit Ratings of Nuclear Related Companies

Seoul, 29 August 2012 Mycle Schneider Consulting (MSC)

Rating Agency Moody’s and Nuclear Power “…a nuclear project could be the thing that pushes [the utility] over the edge—it's just another negative factor.” Decisions considered “credit positive”:

• German utilities E.ON and RWE pullout of UK new-build market is considered positive because they “can instead focus on investment in less risky projects”. • German electronics company Siemens announcement to entirely withdraw from nuclear power “frees up funds that Siemens can redeploy in businesses with better visibility”.

Sources: see WNISR 2012

Seoul, 29 August 2012 Mycle Schneider Consulting (MSC)

Sources: BNEF 2012; WNISR 2012

0

50

100

150

200

250

300

2004 2005 2006 2007 2008 2009 2010 2011

Global Investment Decisions in New Renewables and Nuclear Power 2004-2011

Seoul, 29 August 2012 Mycle Schneider Consulting (MSC)

Post-Fukushima Reactions in China

• No construction initiation in 2011. • Limiting units per site?

• Startup of 2 new commercial reactors in 2011 (1,600 MW).

• Abandoning of CPR1000 series? Waiting for Gen III reactors?

• Acceleration of renewable energy programs in 2011:

+18,000 MW wind (11 x nuclear) à 63,000 MW installed (= French nuclear) +3,000 MW solar (2 x nuclear, 5 x addition 2010) à Target quadrupled to 20 GW by 2015

Seoul, 29 August 2012 Mycle Schneider Consulting (MSC)

1

12

26

42

63

0,1 0,9 3,8

2 5

10 12

2000 2002 2004 2006 2008 2010 0

10

20

30

40

50

60

70 Installed Nuclear, Wind and Solar Capacity in China 2000-2011 (in GWe)

Seoul, 29 August 2012 Mycle Schneider Consulting (MSC)

Source: IPSOS, June 2011

South-Korean Public Most Influenced by 3/11

One Less Nuclear Power Plant through energy saving and new & renewable energy generation

Conclusions • Nuclear power plays a limited role in the international energy sector: ≈11% of electricity, <5% of primary energy, <2% of final energy in the world. • Most of the indicators are on the decline (installed capacity, power generation, share in global power generation, units under construction…). • Fukushima increases costs (safety, insurance, financing…) and problems (public opinion, political parties, competence…). Many nuclear companies are in deep financial trouble. • Post-Fukushima policy decisions, especially in two of the four major economies in the world—Germany, Japan—will likely have a strong pull effect on non-nuclear policies. • Globally, nuclear’s main competitors are natural gas and renewables with very fast, steady and large growth rates. • Renewables penetration will accelerate with storage and grid developments.

Seoul, 29 August 2012 Mycle Schneider Consulting (MSC)

Seoul, 29 August 2012 Mycle Schneider Consulting (MSC)