Page 1

Trade Negotiations & U.S.

Agriculture:

Prospects & Issues for the

Future Parr Rosson

Professor & Director

Center for North American Studies

Department of Agricultural Economics

Texas A&M University

CNAS

Page 2

Overview

International Setting & Trade Strategy

Role of Trade Agreements

The World Trade Organization Negotiations in Doha Development Agenda

DS 267, ‘Cotton Case’

Conclusions & Implications

Page 3

International Setting &

Trade Strategy

Page 4

World Population

US Census Bureau

1990 2000 2001 F2005 F2010 F2015 F2020 0

2

4

6

8

0

2

4

6

8

NA WE I. ASIA EE/FSU D. ASIA

ME AFR LA TOTAL

Billions

6,310

7,570

Ind. + 8%, Dev. + 31%

China, India,

Indonesia

Page 5

GDP Growth Projections

Source: International Financial Statistics January 2005 and projections after 2004 are from Global Insight

(formerly DRI-WEFA), FAPRI 2005 U.S. And World Agricultural Outlook.

5.6

4.94.6 4.5 4.4 4.3 4.2 4.1 4 4 3.9

3.2

2.5 2.5 2.5 2.4 2.4 2.4 2.4 2.4 2.3 2.4

2004 2006 2008 2010 2012 2014

0

1

2

3

4

5

6

7

% Change From Previous Year

Developed Countries Developing Countries

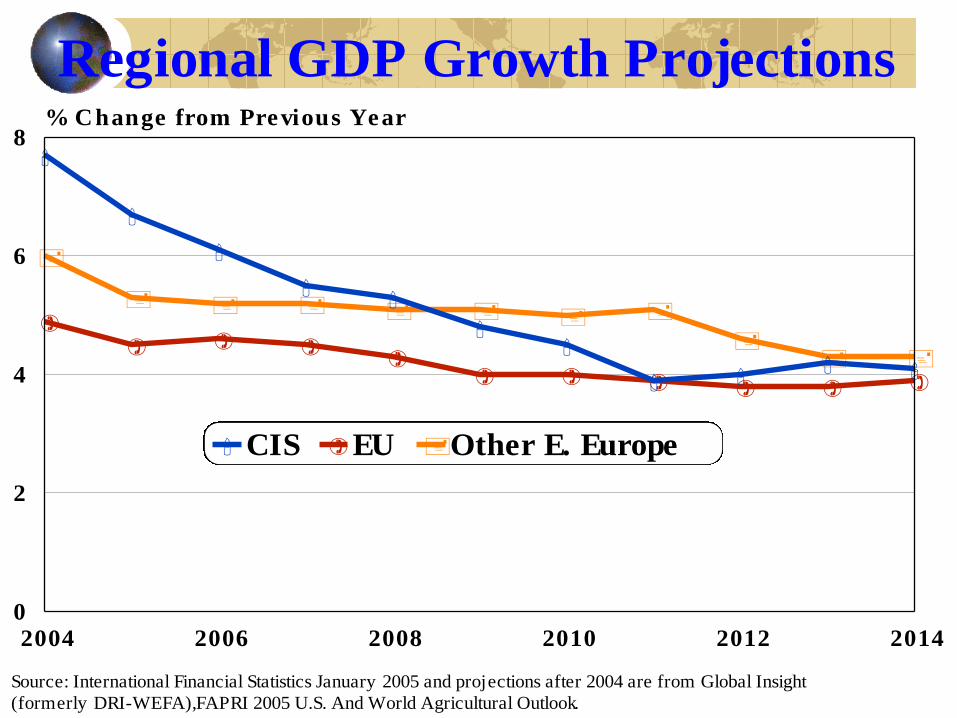

Page 6

Regional GDP Growth Projections

Source: International Financial Statistics January 2005 and projections after 2004 are from Global Insight

(formerly DRI-WEFA), FAPRI 2005 U.S. And World Agricultural Outlook.

2004 2006 2008 2010 2012 20140

1

2

3

4

5

6% Change From Previous Year

Africa Asia Latin America Middle East

China + 6.5%

India + 5.4%

Page 7

Regional GDP Growth Projections

Source: International Financial Statistics January 2005 and projections after 2004 are from Global Insight

(formerly DRI-WEFA), FAPRI 2005 U.S. And World Agricultural Outlook.

2004 2006 2008 2010 2012 2014

0

2

4

6

8% Change from Previous Year

CIS EU Other E. Europe

Page 8

U.S. Agricultural Trade, 1970 - 2005E

Source: U.S. Trade Internet System, www.fas.usda.gov/ustrade

1970 1975 1980 1985 1990 1995 2000 2005E

$0.0

$20.0

$40.0

$60.0

$80.0

-$20.0

-$40.0

-$60.0

Billion Dollars

Exports Imports Balance

Page 9

U.S. Tariffs, 1789-2004

Statistical Abstract of the United States

1789 1816 1820 1840 1860 1880 1900 1920 1940 1960 1980 2000 0

10

20

30

40

50

60

70 Percent

0

10

20

30

40

50

60

70

Tariff of Abominations, 1828

Morrill Act, 1861

Smoot-Hawley Tariff, 1930

Generalized System

of Preferences, 1968

Fordney-McCumber

Tariff, 1922

GATT, 1947

WTO,

1995

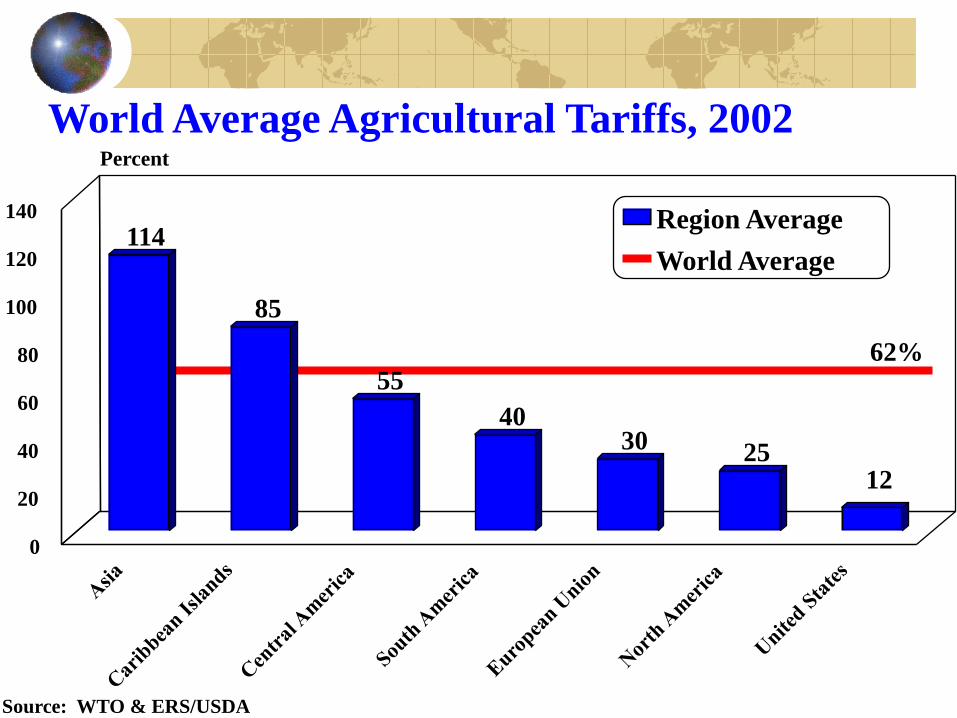

Page 10

World Average Agricultural Tariffs, 2002

Source: WTO & ERS/USDA

114

85

55

40 30 25

12

0

20

40

60

80

100

120

140

Percent

Region Average

World Average

62%

Page 11

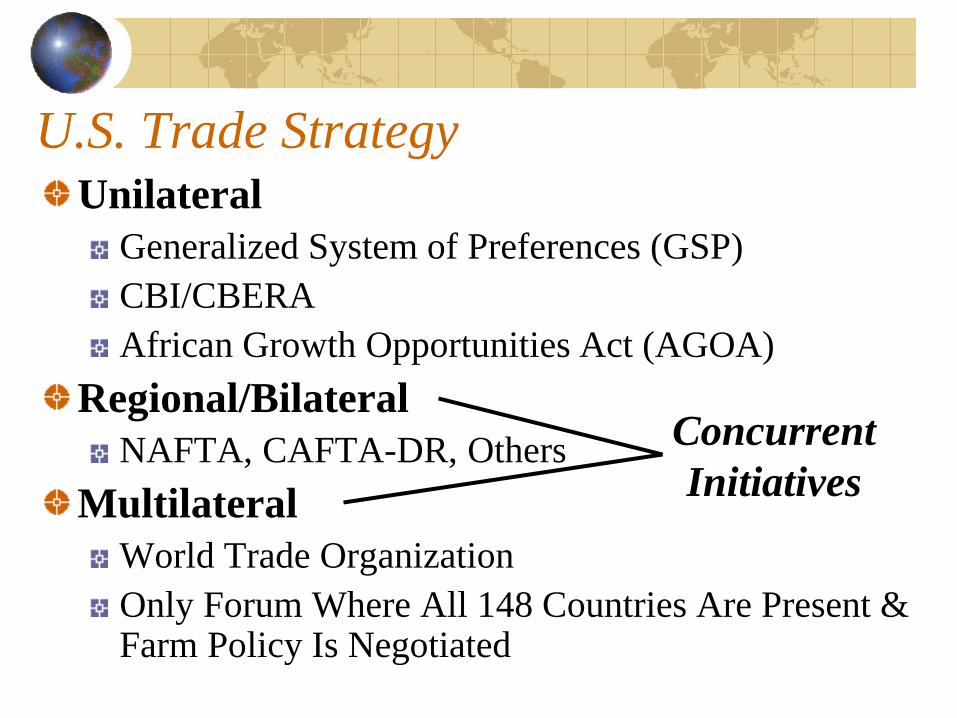

U.S. Trade Strategy

Unilateral

Generalized System of Preferences (GSP)

CBI/CBERA

African Growth Opportunities Act (AGOA)

Regional/Bilateral

NAFTA, CAFTA-DR, Others

Multilateral

World Trade Organization

Only Forum Where All 148 Countries Are Present & Farm Policy Is Negotiated

Concurrent

Initiatives

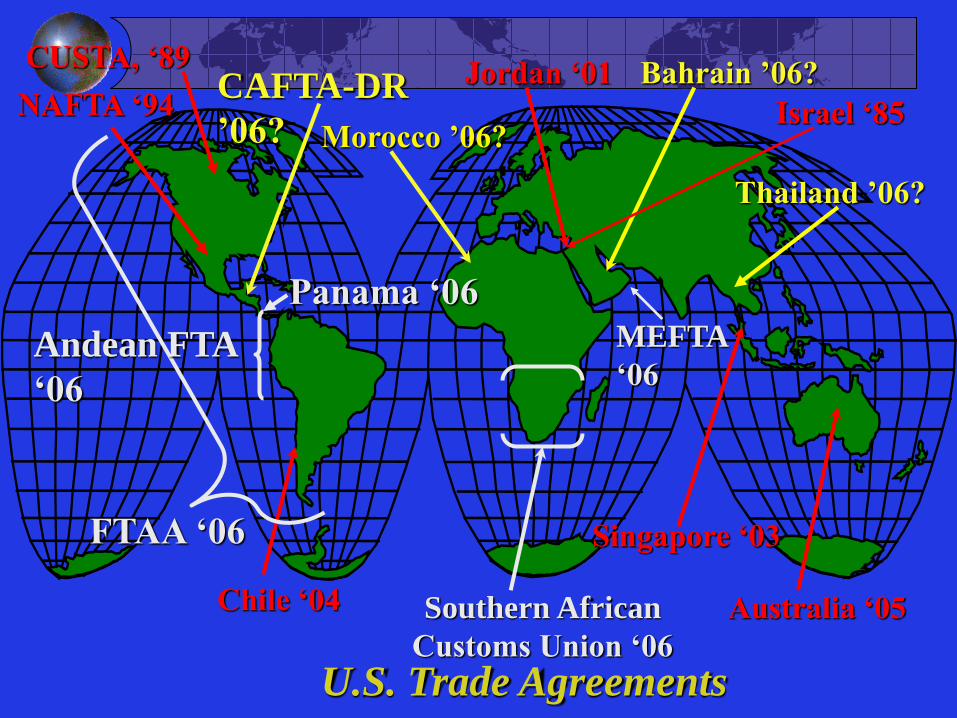

Page 13

Australia ‘05

Bahrain ’06? CAFTA-DR

’06?

Chile ‘04

FTAA ‘06

Morocco ’06?

Southern African

Customs Union ‘06

Singapore ‘03

Jordan ‘01

U.S. Trade Agreements

NAFTA ‘94 Israel ‘85

CUSTA, ‘89

Andean FTA

‘06

Panama ‘06

Thailand ’06?

MEFTA

‘06

Page 14

Trade Agreements In-Place (7)

Israel-1985-1994

Canada-US

(CUSTA)-1989-1998

North America

(NAFTA)-1994-2008

US-Mexico

US-Canada

Canada-Mexico

Jordan-December

17, 2001-2010

Chile-January 1,

2004-2015

Singapore-May 6

2003-2012

Australia-January 1,

2005-2022

Page 15

Trade Agreements-Pending (9)

Morocco-President Signed 8/17/04, Pending Signature, King of Morocco

CAFTA-DR-Signed by President, Passed El Salvador, Guatemala, Honduras (20 Years)

Bahrain-Pending Submission to Congress

Panama-Nine

Negotiating Sessions

Held, Panama Delays

Colombia, Ecuador,

Peru (ANDEAN)-

Nine Rounds,

Negotiations Continue

Thailand-Three

Rounds Held

Page 16

Trade Agreements-Pending (9)

Southern African Customs Union (SACU): Botswana, Namibia, Lesotho, Swaziland, South Africa-Six Rounds Held

Oman-Two Rounds of Negotiations Held, Part of Middle East Free Trade Area (MEFTA)

United Arab Emirates-Two Rounds Held, part of MEFTA

Page 17

Why Regional Agreements?

2d Best After MTN WTO Has Been Slower than Desired

Outcome is Uncertain

Economic Incentives Open Markets

Increase Business Efficiency

Keep Pressure on MTN to Perform

Any One Agreement-Small Impact, Taken Together-Large Impact

Page 18

Strategic Considerations

Secure Key Strategic Materials

Oil, Fertilizer, Natural Gas

Stem Illegal Immigration by Creating

Economic Opportunity in Other Countries

Create ‘Buffer Zone’ Against Terrorism

(Thomas Barnett & 9/11 Commission

Report)

Page 19

Doha Development Agenda in the

World Trade Organization (2001-?

Preparing for the Hong

Kong Ministerial

December 8-13, 2005

Page 20

Three Pillars of Trade Reform

(Agreed in Concept August 1, 2004)

Market Access: Reductions in

Tariffs

Export Competition: Elimination

of Export Subsidies

Trade Distorting Domestic

Support: Reductions Over Time

Page 21

Market Access Highest Tariffs Cut the Most

U.S. Pushing for Deep Tariff Cuts by

Developing Countries (60-75%)

Issue: Many Developing Countries

Want ‘Special’ Treatment & Some

Reluctant to Agree to Large Cuts

Much Left ‘To Be Negotiated’ &

A Potential ‘Deal Breaker’

Page 22

Export Competition

Reduce & Eliminate Export Subsidies by Date Certain (Agreed)

EU Export Subsidies, $2+ Billion/Year

U.S. Export Credit Guarantees > 180 Days

Food Aid to Be Disciplined

Strong Support for Export Competition Reforms

Page 23

Trade Distorting Domestic Support Programs that Cause Production to Be Different

than Would Be Without Programs

Year 1 Cut of 20%

Subsequent Phased Reductions • 40-50% Range

Reductions from Allowable Support

Issue: Developing Countries Wanted Cuts Now, Tariff Reductions Later

If Big 3 Don’t Make Substantial Cuts, A ‘Deal Breaker’

Page 24

Agricultural Producer Support By Country 1986-88 and 2001-03

-Percent of Total Farm Receipts from Government-

Source: OECD's database (see www.oecd.org)

12%

33%

26%

40%

62%

71%

2%

20% 20%

39%

60% 65%

New Zealand Canada United States EU Japan Korea 0%

20%

40%

60%

80% 1986-1988

2001-2003

Page 25

Total Allowable Trade Distorting Domestic

Support, 'The Big 3,‘ 2002

WTO, Trade Policy Review and calculations.

$128

$49 $48

European Union United States Japan $0

$20

$40

$60

$80

$100

$120

$140

Billion $

Includes Amber + Blue Boxes, Product Specific

+ Non-product Specific De Minimis, Each Based

on 5% of Total Value of Agricultural Production

Page 26

Total Trade Distorting Domestic Support Remaining

After Year 1 Down Payment (calculated)

$100.2

$39.2 $38.4

European Union United States Japan $0.0

$20.0

$40.0

$60.0

$80.0

$100.0

$120.0

Billion $

Page 27

Total Trade Distorting Domestic Support

Assuming 50 Percent Reduction

Calculated

$50.1

$19.6 $19.2

European Union United States Japan $0.0

$10.0

$20.0

$30.0

$40.0

$50.0

$60.0 -Billion Dollars-

Page 28

Real Income Effects of Liberalization of Global Merchandise Trade, by Country, 2015

-Impacts in 2015 Relative to the Baseline (2001 dollars)-

Source: Anderson, Martin and van der Mensbrugghe (2005a, Table 12.3)

$60.4

$12.3

$52.2 $44.2

$10.9 $12.9

$190.9

$142.1

$277.9

EU 25

United States

Japan Korea and

Taiwan

Brazil

Middle East High-income

Countries Developing

Countries

World Total

$0.0

$50.0

$100.0

$150.0

$200.0

$250.0

$300.0

$350.0 -Billion Dollars-

Page 29

Impacts of Doha on Agricultural Output and

Employment Growth, by Country, 2005-2015

-Annual Average Growth Rate (Percent)-

Source: Anderson, Martin and van Mensbrugghe (2005a, Tables 12.12 and 12.13)

4.3%

1.7%

-0.4%

-1.4%

1.6%

4.4% 4.4%

1%

-1.4%

-2.8%

-4.1%

-2.1%

2.2%

1.1%

Canada

United States

EU 25

Japan

Korea and Taiwan

Brazil

New Zealand

0%

2%

4%

6%

-2%

-4%

-6%

Output

Employment

Page 30

Trade Liberalization Impacts on Factor Prices, 2015

Anderson, Martin, and van der Mensbrugghe (2005a, Table 12.7).

Skilled WagesUnskilled

Wages

Land Owner

RentInflation

EU 25 1.3 -0.1 -71 -1.2

United States 0.2 0 -24 -0.3

Japan 2.4 1.5 -67.2 -0.2

Korea and Taiwan 7.8 7.3 -45.8 -1.3

Brazil 1.4 2.8 35.9 2.8

Sub-Saharan Africa 5.7 8.4 6.4 -4.3

Thailand 6.3 13.4 12.5 -0.2

Vietnam 15.1 23.3 5.8 -0.2

New Zealand 1.1 3.5 20.9 1.5

Percent Change

Large

Gains

Page 31

Conclusions and Implications

Page 32

Conclusions & Implications

U.S. Market Is Open, Rest of World Is Not

U.S. Export Growth Lags Import Growth

Agricultural Trade Distorted by Tariffs, Export Subsidies, Trade Distorting Domestic Support

U.S. Pushing for Deep Tariff Cuts by Developing Countries To Open More Markets for U.S. Exports

Little Agreement on How Much Tariffs Might Be Cut

Page 33

Conclusions & Implications Reductions in Trade Distorting Domestic Support Likely Substantial

Some Adjustment for U.S. Producers

Absent WTO Progress, World Trade & Economic Growth Stifled, Especially in Agriculture-Not Good for U.S. Agriculture

Cotton Case Could Figure in Outcome U.S. Response

Other Cases (Rice, Soybeans??)

Trade Reform is at a Crossroads: Protection or Progress?

If Export Markets Are Important, Trade Agreements & WTO Progress Are Necessary

Page 34

Thank You!

Questions?

Parr Rosson

Department of Agricultural Economics

Texas A&M University

College Station, TX 77843-2124

E-mail: [email protected]

Telephone: 979-845-3070

CNASCNAS