Page 1

Naño, Quiamno 1

CHAPTER 1

INTRODUCTION

RATIONALE

Poverty is one of the problems of our country today. Having a wide range of

population and low income in every household is the primary reason to consider our

country in poverty.

Money is very essential to every individual since it is used as a medium of

exchange. It is considered as one of the most outstanding inventions in the entire

history of mankind. To poor people, money is equal to survival. Everyone needs money

to satisfy their wants and needs. Thus, people are engaged in credit

Credit is the ability of an individual to obtain goods, services, or money at the

present time in exchange of a promise to pay at a definite future time. It enables people

to acquire money that could help them to finance their needs. The poorest of the poor

should be given the opportunity to receive benefits of a credit system. It is this

depressed group which needs credit most. People, who have been granted credit, have

the opportunity to improve their social and economic conditions as long as they use

credit properly.

Many programs have been developed to improve the local community.

Microfinance which has the purpose of lending a sum certain amount of money was

established. It is the provision of financial services to low income clients, including

consumers and the self-employed, who traditionally lack access to banking and related

Page 2

Naño, Quiamno 2

services. More broadly, it is a movement whose object is a world in which as many poor

and near-poor households as possible have permanent access to an appropriate range

of high quality financial services, including not just credit but also savings, insurance

and fund transfers. Those who promote microfinance generally believe that such access

will help poor people out of poverty.

The Microfinance institutions are providing easy access loans for everyone.

Unlike bank loans it is designed to help poor communities by the financial services and

intended to alleviate poverty in many countries. Here, in our country, there have been

many different Microfinance institutions in any forms and shapes. The goal is to reach

out impoverished communities and provide financial assistance.

The Social Action Center (SAC) of the Diocese of Legazpi is one of the service

oriented non-profit, non-government Catholic Organization that implement programs

through people's organization and Christian formation that will generate people’s

participation in the enhancement of the socio-economic and spiritual well-being of the

parishioners for a dynamic, dignified and self-reliant Christian communities.

It was established in 1972 as an offshoot of Vatican 11’s call for the church’s

greater involvement in social issues. As the social actions arm of the Bishop of Legazpi,

Most Rev. Jose C. Sorra, D.D is to coordinate, supervise, and implement community

projects of the Diocese whether initiated by the parish priest or the civic groups.

Social-Economic Development Program (SEDP) Inc. has a vision for a dynamic

and pro-active financial foundation of the Diocese of Legazpi committed to the total

advancement of the poor. Their mission is commits to deliver sustainable financial

Page 3

Naño, Quiamno 3

services with training and foundation to marginalized women towards improved socio-

economic condition, political empowerment and enhance spiritual well-being.

The program components of Social-Economic Development Program (SEDP)

consist of credit services like production loan, housing loan and multi-purpose loan.

They also have savings mobilization which provides a good incentive for the program

participants to develop the saving habit. The Micro-insurance provides for debt

redemption and burial assistance or emergency medical assistance. They also have

formation and training in Spiritual and valued formation such as recollection, retreat,

team building, basic bible orientation, marriage enrichment, session, values clarification

and in skills training which provides the members improve their capability in managing

their organization and their respective projects. They also

offer Medical Mission, Marriage Validation and Counselling, Relief Assistance during

calamities, Scholarship, Advance Entrepreneurial Training, Parish Integration and On-

going Formation and Current Events Updating through their media, such as SAC

operations, DSWBS Special Program for Social-Economic Development Program and

news brief by Social Action Center Operations or so-called Ang Bangraw.

Nowadays, the SEDP Inc. is adopting the Grameen Banking Scheme. Grameen

is a Bengali language which means “village” (barrio or barangay). This program aims to

increase member’s income and improve socio-economic status of their families. A

profound understanding and application of these beliefs have guided micro credit to

reach the poorest with service that are sustainable.

Page 4

Naño, Quiamno 4

Several reasons have prompted the researchers to select this topic and conduct

it among the beneficiaries of the SEDP Inc. The researchers want to find out if these

people who are actively involved in this program are aware of the possible gains and

negative effects brought by it and to know their perception on SEDP Inc.

The researcher has to conduct this study for better understanding of cash

management of any individual and the benefits of the following:

While doing the research the researcher had learned a lot of things from this

topic. It has been an eye-opener for them to finally realize on how poverty affected

millions of lives around the world and financial institution works especially the

Microfinance institution as one of the means they are using for fighting or alleviating

poverty today.

On the part Microfinance Institutions (SEDP of SAC) it may serve as a

helping tool in developing and improving their program and to have suitable goal

regarding the effects of their program to its beneficiaries.

O n the part of the microfinance beneficiaries it may help out in determining

whether availing loans from this microfinance lending institution is an advantage or may

cause to several problems. This will develop their awareness to value money for

personal, economics, social and entrepreneurial development,

On the part of the community, it will be a way to erudite of the possible

effects that microfinance could bring on their lives and how people will be benefited from

it and of course to admonished poverty.

Page 5

Naño, Quiamno 5

On the part of the students/ readers , awareness is great benefit that they

could obtain in this research. They will be more knowledgeable on things that somehow

they are not familiar enough; probably students are aware of the poverty we are all

experiencing .This is not just additional information for them to know and to keep but to

enable them to be more socially responsible, for them to act and do something.

On the part of future researcher, this study will serve as a reference material

for future studies with the same undertaking.

Statement of the Problem

This study aims to determine the perceive gains and negative effects of Social-

Economic Development Program Inc. of SAC to household beneficiaries of Ligao City.

Specifically, it attempted to answer the following problems:

1. What is the profile of the beneficiaries in terms of:

a) Age

b) Educational background

c) Occupation

d) Monthly income

e) Respondents membership status

2. What are the socio-economic factors that motivate households in availing the

microfinance?

3. What are the perceive gains of SEDP Inc. beneficiaries in availing loans and

services of the microfinance?

Page 6

Naño, Quiamno 6

4. What are the negative effects SEDP Inc. beneficiaries in availing loans and

services of the microfinance?

5. What are the ways in reducing the negative effects of Microfinance to its

beneficiaries?

Hypothesis

In this study, the researcher presumes the following as answer to the identified

problems:

That Microfinance institution does not consider age, educational attainment,

occupation and monthly income of its beneficiaries in granting loans but on the

membership status and attitudes of its beneficiaries in repaying.

That social factor that motivates households in availing loan can help them in

assuage in poverty.

In terms of benefits gained by the member from their loans they gained

knowledge in managing business, the developed self-disciplined in apportioning money

and their financial status was elevated from poverty and the problems that are brought

in availing loans.

Background

The name Ligao is derived from the local word "ticao", once an abundant tree

whose poisonous leaves were used to catch fish in rivers or creeks. Most Ligaoeños,

Page 7

Naño, Quiamno 7

however, believe that the name Ligao was originally "licau" which means to take the

long way around or to turn away from the ordinary or usual route. Ligao started as a

small settlement known as Cavasi in the 16th century. It grew in population as it

attracted natives from nearby settlements. Eventually, power struggles among

ambitious and aggressive leaders caused trouble as they created divisions among the

settlement. There arose five divisions led by maginoos (chieftains): Pagkilatan, Maaban,

Sampoñgan, Makabongay and Hokoman. Peace was only restored when Chieftain

Pagkilatan was appointed supreme leader over the entire settlement with the approval

of the other chieftains. The town was founded as a barrio of Polangui in 1606, being

ceded to Oas in 1665, and finally becoming an independent municipality in 1666.

Related Non-Research Works

The Senate Bill No. 1180, section 2, introduced by Senator Ramon B.

Magsaysay which is “An Act Regulating the Establishment and Operation of Lending

Companies in the Philippines and for Other Purposes.” The Declaration of policy

declared that the policy of the State to regulate the establishment and activities of

lending companies, placing their operations on a sound, efficient and stable basis to

derive the optimum advantages from them as an additional source of credit; to prevent

and mitigate, as far as practicable, practices prejudicial to public interest; and to lay

down the minimum requirements and standards under which they may be established

and do business.

R.A. 3779 known as the “Savings and Loan Associated Act” as amended:

Page 8

Naño, Quiamno 8

Whereas savings and loans associated have prove to be effective instrument in

encouraging the savings habit of people, especially low and middle income groups and

providing additional credit facilities to household, consumers, small scale entrepreneurs

and home builders.

The R.A. 6938 known as the Cooperative Code of the Philippines it enacted:

This law encourages the growth of cooperatives to promote self-reliance and

harness people towards economic development and social justice. This shall be the

guiding law of existing future cooperative in the country. It provides for the rules and

procedures for the organization, administration, registration, dissolution and auditing of

cooperatives. It also sets out the rights, privileges and responsibilities of cooperative as

well as the members. This act enjoins the private sector to undertake actual

organization of cooperatives. On the other hand, it commands the government to

provide technical guidance, financial assistance and other services for the development

of cooperatives.

Microfinance’s worldwide recognition can also be credited to Muhammad Yunus,

founder of the Grameen Bank in Bangladesh and recipient of the 2006 Nobel Peace

Prize. Although microfinance was not his original idea, Yunus pioneered the

implementation of joint-liability groups as a substitute to tangible collaterals when

borrowing loans, and emphasized the role of women in managing credit and organizing

microenterprises. He founded the Grameen Bank in the 1970s as an effort to ameliorate

the destitute poverty that plagued his country. He believes that the poor possess an

“entrepreneurial drive” and are equipped with “survival skills” that allow them to become

Page 9

Naño, Quiamno 9

successful microentrepreneurs .He also asserts that to develop tools and services that

would greatly benefit the poor, their limitations must be carefully considered by

institutions which fight poverty .As of now his Grameen Bank has more than 1,000

branches and 6 million members, and boasts a 98 percent repayment rate.

On the other hand, Bangko Sentral’s Circular 685 provides the rules for the

recognition of Microfinance Institution Rating Agencies or MIRAs. This should improve

access to financing and capital as ratings have proven effective in enhancing the quality

of microfinance institutions in terms of transparency, discipline, and overall governance.

This should also promote investments in the Philippine microfinance industry. These are

the circulars the Bangko Sentral issued this year to promote the further development of

our microfinance sector. With the support of all stakeholders, we should start seeing

positive results from these initiatives. I also look forward to the participation of more

banks in the microfinance sector. As of December 2009, there were more than 200

banks engaged in microfinance with total loans outstanding of about P6 billion lent out

to about 900,000 borrowers. By any yardstick, these are good numbers. However, with

millions of Filipinos still living in poverty, we should commit to do more together to do

better in spreading the gospel of microfinance and how it can uplift and transform

individuals, families, as well as communities”.

Whether we accept it or not, money is hard to make nowadays; at the same time,

expenses keep on increasing. If our ,money we are making is not enough and we bills

and expenses to pay, most often than not we end up in debt. There are two common

Page 10

Naño, Quiamno 10

reasons why we get into debt: Spending tomorrow’s income today and unwilling to

change lifestyle when circumstances have changed. Getting out of debt is not fun; it is a

painful process but there are ways out of debt. Willingness to pay matters most not the

real amount, dealing with the root of the problem ( the attitudes and bad habits led us to

indebtedness) and lastly tough love, letting your family, friends and or relatives

borrowing habitually is not good not all because they forgot God in their life.

Credit is a very important tool in economic development. If it is sufficient and if it

is properly used, credit benefits all users, individuals, community, or country.

According to Estapa, the confidence in which credit is built in two fold in

characteristics, the lender must be morally certain that borrowers has the ability to pay

debt and to pay debt when due. This ability to pay is evaluated through the

requirements imposed before granting loan. This includes collateral, evaluation of

payment capacity loan and their capacity to pay debt. There are, however, other factors

that should be taken into accounts before credit is finally granted. Those factors are

commonly called the C’s of Credit: character, capacity, capital, collateral and conditions.

Microfinance is a tool designed to uplift the quality of life of people, it provides

additional capital to the business people who are engaged with or it helps them to start

a business. In addition, it is also a tool for community development and capability

building to people who had been engaged in business.

According to the World vision, the term microfinance refers to the practice of

providing financial services to people in impoverished countries who have no collateral,

credit history, or access to traditional lending service." Microfinance institutions manage

Page 11

Naño, Quiamno 11

and administer the loans and credit programs. These institutions are located near the

areas they serve.

According to Asian Development Bank: The Poverty and the Government

Responses

The major causes of poverty in the Philippines fall into several broad categories(1)

weak macroeconomics management(ii)employment issues;(iii)high population growth

rates,(iv)an underperforming agricultural sector and an unfinished land reform agenda;

(v) governance issues including corruption and a weak state; (vi) conflict and security

issues , particularly in Mindanao; and (vii) disability. The 2004-2010 Medium-Term

Philippines Development Plan contains ambitious poverty reduction targets. Successive

governments of the Philippines since 1985 have attached a high priority to poverty

reduction, but have had only moderate success in reducing the overall headcount, and

outright failure in reducing the absolute number of poor Filipinos. Targeting has been a

key problem, as have issues of budget, governance, and LGU capacity (particularly in

the context of decentralization, initiated with the 1991 Local Government Code). The

tendency to derail old programs and to launch new ones with each new President has

resulted in duplication of efforts, wasted resources, and continuous state of transition.

The stated goal is to reduce the poverty incidence of families from 28.4% in 200 to

17'9% in 2010. Similarly, the subsistence incidence of families is intended to drop from

13.10% of 1.93% per year for the period 2005-2010. However, it does not articulate a

clear population policy.

According to the Asia Society: Microfinance: the Seed of Change

Page 12

Naño, Quiamno 12

Microfinance institutions thrive in urban settings; they are also being having the

ability to change life for the better rural areas. They also provide clients with their basic

financial services that they need to grow the money they earn, so that the business can

benefit the villagers who produce the items.

Related Studies

Many studies are conducted regarding credit and microfinance institutions that

are related to this study.

Cañada (2008), on her study on the Effect of Microcredit financing–Socio-

Economic Development Program of Social Action Center in Cabunturan, Malinao,

Albay, that the primary effect of availing micro-credit financing services, gives impact to

be involved in the social activities as well as improved one’s values. The economic

effects of micro credit financing services generate income to sustain the needs of the

family.

Moral (2008) studied and assessed the performance of the Simbag sa

Pagasenso as to its credit services in one Center of the Old Albay Branch. Her findings

showed that majority of the respondents were very satisfied on the credit services

offered by the institution. Majority of the respondents had an improved status of their

business, increased financial management capability and improved socio-economic

condition which had an equivalent rating of very effective as to the extent of

performance of SEDP in supporting the entrepreneurial activities of each member.

Cate (2003) concluded that the perceived socio-economic effects of

Microfinance-HELP were positive. That is, the client beneficiaries evaluated the whole

Page 13

Naño, Quiamno 13

program as good because it helped them among other to improve their well-being,

achieve social aspiration and taught them how to save and appreciate the value of

saving. It also increased their family income and taught them wise budget management.

Neo (2008) conducted a study to analyze a formal microfinance lending

institution named as the UKNOWIT Cooperative. Her findings revealed that a majority of

the respondents believed that they have become more disciplined and more

responsible. All of them used the money borrowed for business. The income derived

from the business supported by the loan proceeds was used by the respondents for

their basic needs as well as the education of their children. The cooperative has exerted

efforts to solve those problems through review of policies and its operational

procedures, particularly in their dealing with the clienteles and the community.

The study entitled, the Effects of Borrowed Capital to the Daraga Public Market

vendors was conducted by Alcazar et al (2004). As to the effects of borrowed capital to

the Daraga market, borrowing capital is their primary option to address unavailability of

funds for their business. It provides opportunity to transact business in exchange for the

goods and also it can provide opportunity for the borrowers to expand another line for

business.

Miraflor studied the effects of the informal lending sector on the profitability of the

Micro-Business establishments in the market site of Daraga, Albay. Her study revealed

that all micro business owners utilized loans to keep their business enterprise going. As

to their economic profitability, almost all agreed that the utilization of amount borrowed

was economically profitable.

Page 14

Naño, Quiamno 14

Cresencio (2006) concluded that the loan availed have l increased profitability on

some business activities of the borrowers has resulted to a positive outcome as shown

by the increase in the weighted average in terms of assets, sales and ultimately, profit.

The monthly income of the borrowers could hardly sustain the basic needs of the family.

Basic needs is still the main reason for diversion of funds initially intended for business

operation and thus results to unsuccessful operation.

On the study conducted by Ereve (2008), the microfinance program possessed a

good system in the delivery of its program to the society. Wherein, The problems

encountered by the respondents were based on the personal background and

experience being member-borrower of the microfinance program.

Manrique (2008) entitle” analysis Of The Credit Delivery System Of Simbag Sa

Pag-Asenso, Inc. – SEDP Of The Social Action Center (SAC) Of Legazpi City”, some

measure recommend by the SEDP Inc. In Legazpi City to improve credit delivery were

to provide trainings and seminars which could help their clients to expand their business

and provide higher income, provide additional services and benefits to productive

clients. They also implemented rules and regulations on loan to prompt delinquent

clients and recovery of their accounts and consider safety of the worker assigned to

distant places in carrying big amount of money which is perilous for them.

Alaurin et al (2007) on their study, they found out that the great social and

economic benefits after the procurement of loans. Majority of them used the loaned

amount to meet their financial commitments. The loan availed furthermore added to the

income level of the family, thereby increasing their purchasing ability.

Page 15

Naño, Quiamno 15

The Cash Management System of Air Material Wing Savings Loan Association

Incorporated, Albay branch was the study conducted by Caraballo and Danisco ( 2007).

It was mentioned that all business need to control their cash efficiency as possible even

if your company has cash hand, cash need change a companies grow, cash needed for

expansion an expanding company requires cash, additional staff and new assets.

However, it may be taken several months or longer before the benefits of the expansion

generates higher revenue and eventually turned back into cash. Cash management

involves managing of the monies of firms in order to maximize cash availability and

interest on any idle funds. The firm’s effort to get customers to pay their bills at a certain

time fall within accounts receivable management, on the other hand the firms decision

about when to pay bills involves accounts payable and accrual management.

According to Clutario et al ( 2006) in their study entitled “The Social and

Economic Benefits of People’s Alternative Livelihood Foundation of Sorsogon Inc.

(PALFSI)” to its borrowers, the problems that the PALFSI clients have encountered in

the procurement of loans are not quite felt by most, except for some. The very problem

of the majority is the inability of their co-borrowers to pay back the borrowed amount

which in effect burdens the other members in terms of payment.

Synthesis

From the reviewed literature and studies.

The reviewed studies revealed similarities and difference to the present study.

The similarities of the in dealt were the researcher would like to spot the perceived

gains member-borrower or beneficiaries in availing loans in microfinance institution/

Page 16

Naño, Quiamno 16

Socio- Economic Development Program Inc. The difference were the objectives and

focused of each study.

Microfinance programs are increasingly publicized as one of the most successful

tools for development with the ability to positively affect its participant’s economic and

social status

The study of Canada, Moral, Cate, Alcazar and Miraflor studied the effect of

availing micro-financing services, gives impact to be involved in the social activities as

well as improved one’s values and an improved status of their business, increased

financial management capability and improved socio-economic condition.

Cresencio, Ereve, Neo, Manrique, Alaurin et al, Caraballo and Danisco and

Clutario et al concluded when microfinance program possessed a good system in the

delivery of its program to the society. Thus, the microfinance program also reflected its

socio-economic impact to its client, the service its personnel exerted and the extent of

the awareness and benefit its member-borrower derives from the program.

Cañada, Moral, Manrique who have studied the same microfinance institution is

different from the present study but it will focus on the beneficiary’s perceive gains and

negative effects.

Gap Bridged by the Study

From the various studies presented, some focused on microfinance. The other

research dealt with other microfinance institution. There are also some studies

concerning the same institution, however, this research is not a duplicate for it focuses

on a different scope. One of the previous studies has pointed on the delivery system of

Page 17

Naño, Quiamno 17

the institution. The field of consideration of the other is the effect of microcredit financing

on Cabunturan, Malinao, Albay. And the other has made an assessment of performance

in Legazpi City.

This study gap the bridge in a way that this will focus on perception of

beneficiaries in Ligao City with regards to the gains and negative effects of SEDP Inc.

Theoretical Framework

This study is anchored on David Mc Clellands’ Needs – Based Motivational

Theory. This model asserts that every individual is driven by their needs and wants.

These needs are found to be in altered degrees in every person and this mix of

motivational needs characterize a person’s style and behaviour.

The hierarchy of needs of Maslow was also be used in this study, people have

needs they wish to satisfy and that gratified needs are not as strongly motivating as

unmet needs. A fully satisfied need will not be a strong motivator. This model has

shown the human needs in the form of hierarchy that should be satisfied in order, from

the lowest to the highest needs. The needs that are stated in this model include

physiological, security, love and belongingness, self esteem, and self actualization.

Considering the present condition, it is an admitted fact that there is a strong

need to uplift the economic and social life of people. To secure the welfare of every

individual most especially families who have children to be raised, some find out that the

only way to minimize these problem is to resort in borrowing.

Page 18

Uplifted socio-economics status and social life.

People with needs and wants in

RelativeSatisfaction

Maslow’s Hierarchy of Needs Theory

Naño, Quiamno 18

Theoretical Paradigm

Figure 1

David McClelland’s Need Based-

Motivational Theory

Page 19

Naño, Quiamno 19

Conceptual Framework

The researchers will use the following concepts to make the study more

successful. Figure 2 shows the conceptual paradigm of the study. This study will find

out the socio-economic factors that motivate the household to avail microfinance, SEDP

Inc, which the beneficiaries’ profile in terms of age, educational background, occupation,

and monthly income, respondent’s membership status. This will also determine the

perceived gains and negative effects of SEDP to its beneficiaries.

The first box includes the profile of the beneficiaries that availed loan in

microfinance institution.

The second box also includes socio-economic factors and the third box includes

the perceive gains on availing microfinance. And the fourth box includes the negative

effects of availing microfinance services. And lastly the fifth box contains the possible

way of reducing the negative effects in availing loans in microfinance institution that if

not ended may lead to a serious problem.

Page 20

Socio – EconomicFactors

Profile of the beneficiaries in terms of:

a. Ageb.Educational backgroundc. Occupation d.Monthly incomee.Respondents membership status

Negative Effects

Positive Effects

Ways in Reducing Negative Effects

Naño, Quiamno 20

Conceptual Paradigm

Figure 2

Page 21

Naño, Quiamno 21

Definition of terms

Beneficiaries – a person who benefits or is expected to benefit from something.

- in this study it refers to the person who have been benefited of the

programs and practices of Social Economic Development Inc.

Microfinance Institution - is the provision of financial services to low-income clients,

including consumers and the self-employed, who traditionally lack access to banking

and related services.

- In this study it refers to SEDP Inc. that offered help to the women of

Ligao City in developing the socio-economic status.

Perceived gain – defined in this study as the advantages received by the members of

the institution

Negative effect - in this research it refers to the unhelpful results that the beneficiaries

observe as a member of microfinance institution that can cause problem.

SEDP Inc. /Socio Economic Development Program Incorporated- is one of the

institute providing microfinance services in the City of Ligao which in this study is

focused on.

Socio-economic factors- these are the social and economic experiences and realities

that help mould one's personality, attitudes, and lifestyle.

Page 22

Naño, Quiamno 22

- In this study refers to the aspects that motivate household on availing

microfinance services.

Households- In this study, they are the beneficiaries of the microfinance institution.

Page 23

Naño, Quiamno 23

CHAPTER II

METHODOLOGY

This chapter presents methodology engaged in this study, sources of data

population and sample, data gathering, instruments and procedure and the statistical

treatment of data. This part of the research answers the questions on how study was

conducted.

I- Research Design

This study is engaged descriptive design of research in which it employed

survey questionnaires as the main gathering instrument. The records of

Simbag sa Pag-asenso, Inc. was looked over to cope up with necessary

information needed in completing the study.

II- Sampling Design

The population of this study was the members/beneficiaries of the institution.

The total population or member was 928 record as July 12, 2010. The

researcher used the Slovin’s formula to determine the sample. Hence:

n= N

1+ Ne2

Where: n= sample size

N= Population size

e= desired margin of error

Page 24

Naño, Quiamno 24

The margin of error used was five percent (5%), which resulted to a sample of

284 beneficiaries.

After determining the sample size the researcher will use the random

sampling to determine the respondents who of will be the respondents of the

study.

III- Research Strategies

This study used the descriptive survey method. The survey method was a

form of questionnaires. The questionnaires have guide and provided the

respondents with questions that will help the researcher picture out how

SEDP Inc, Ligao Branch helps it beneficiaries in their socio- economic

conditions.

IV- Instrumentation

`The instrument used in this research was divided into five parts. The first part

answers the profile of the beneficiaries regarding name, age, educational

attainment, civil status, number of children, monthly income and most

importantly the membership status.

On the other hand, the second part of the instrument answered the

second question in the problem, the socio- economic factors that motivate the

beneficiaries in availing loans. It is a checklist that can be answered by more

than once.

The next part was determining the perceived gains of the beneficiaries,

which is divided into three categories: as a businesswoman, attitudes and

Page 25

Naño, Quiamno 25

family. The fourth part of the questionnaire answers the negative effects of

microfinance.

Lastly, is the ways on how to reduce the negative effects in availing loans

in microfinance institution may brought in its beneficiaries

V- Data Collection Procedure

In gathering data, the researchers took the following steps:

1. The researchers made a letter to the Branch Manager of SEDP Inc. to

ask permission to conduct the study undersigned by their professor,

department chairperson and assistant dean.

2. The researchers request the needed information in conducting of the

study such as the number of beneficiaries.

3. To look for related literatures and studies the researchers went to

different libraries and surf to the internet for additional information.

4. The researchers combined all information gathered.

5. The researchers went to the different places wherein the Socio

Economic Development Program Inc. have its centers.

6. The researcher personally distributed the instrument to their

respondents during weekends.

Page 26

Naño, Quiamno 26

VI- Analytical Tool

In analyzing the data the researcher used following statistical tools to

quantify the response and for proper interpretation:

Frequency Count - for tallying the actual number of response to an item or

question.

Percentage - which refers to the ratio of the observable frequency over the

total population.

P= f/n ×100

Where P- percentage

f- Frequency

n- Total of number respondents

100-constant

Frequency ranking- to denote importance of an item or response discussed to

strengthen the interpretation of percentage.

Page 27

Naño, Quiamno 27

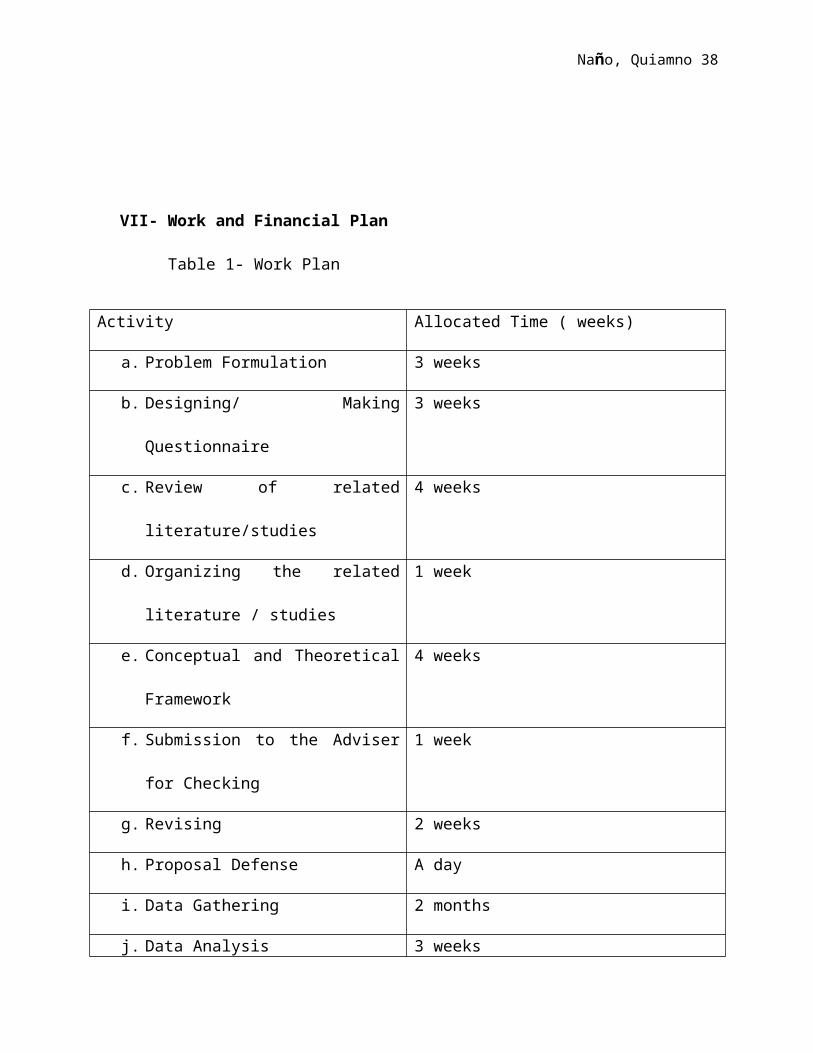

VII- Work and Financial Plan

Table 1- Work Plan

Activity Allocated Time ( weeks)

a. Problem Formulation 3 weeks

b. Designing/ Making Questionnaire 3 weeks

c. Review of related literature/studies 4 weeks

d. Organizing the related literature /

studies

1 week

e. Conceptual and Theoretical

Framework

4 weeks

f. Submission to the Adviser for

Checking

1 week

g. Revising 2 weeks

h. Proposal Defense A day

i. Data Gathering 2 months

j. Data Analysis 3 weeks

k. Making Conclusion and

Recommendation

2 weeks

Page 28

Naño, Quiamno 28

Table 2- Financial Plan

Expenditures Amount

a. Transportation Php. 1500.00

b. Foods 750.00

c. Printing 1700.00

d. Encoding 500.00

e. Bookbinding 450.00

f. Snacks for panel list 1000.00

g. Editor’s Fee 250.00

h. Other expenses 800.00

Total Php. 5, 950.00

Page 29

Naño, Quiamno 29

Work Cited

Alaurin, Raquel P., Armena, Ma. Kristina B., Azucena, Ann E., Frayna, Mayflor

A., Lopez, Kathrina Denesse L. “The Lending Operations of Social Welfare (SOWEL)

Fund of Department of Social Welfare and Development (DSWD)ROV” (Unpublished

Undergraduate Thesis), 2007 (College of Business Administration, Aquinas University,

Legazpi City).

Alcazar, Roy M., Astor, Marian Pauline E., Deza, Rhaian B., Helis, Ervin L.,

Frayna, Ivy S., “The effects of Borrowed Capital to the Daraga Public Market Vendors”

(Unpublished Undergraduate Thesis), 2004 (College of Business Administration,

Aquinas University, Legazpi City).

Cañada, Shiela Mae. “The Effect of Micro credit Financing –Socio Economic

Development Program of Social Action in Cabunturan, Malinao, Albay: An Assessment”

(Unpublished Undergraduate Thesis), 2008 (Bicol University College of Business,

Economics and Management, Daraga, Albay).

Chinkee Tan, Till Debt Do Us Apart ( Practical steps on Financial Problem)

Cate, Jerry Raffalo. “Microfinance and Empowering through Livelihood Program

(HELP) of the Bango Santiago de Libon: an Anlysis” (Unpublished Undergraduate

Thesis), 2003 (Bicol University College of Business, Economics and Management,

Daraga, Albay).

Page 30

Naño, Quiamno 30

Caraballo, M. R., Dansico, Johan D. “The Cash Management System of Air

Material Wing Savings and Loan Association Incorporrated, Albay Branch”

(Unpublished Undergraduate Thesis), 2007 (Divine Words College of Legazpi, Legazpi

City).

Clutario, Evan Albert C., Logronio, Micheal John H., Perez, Ronald Jason H.,

“The Social and Economic Benefits of People’s Alternative Livelihood Foundation of

Sorsogon, Inc. (PALFSI)” (Unpublished Undergraduate Thesis), 2006 (College of

Business Administration, Aquinas University, Legazpi City).

Consuelo B. Estapa, Ph. D Mercedes M. Leuterio, Ph. D. Economics of Money

and Banking ( Manila Phil: UST Publishing House, 2001), p. 92

Cresencio, Leslie Gaye A., “The Microfinancing program of Bicol Friendly

Savings Bank: A Case study” (unpublished Thesis), 2006 (Divine Words College of

Legazpi, Legazpi City).

Ereve, Archie E.”Effectiveness of the Gubat St. Anthony Cooperatives

Microfinance Program as Perceived by its Member-Borrowers in Barangay Gabigaan,

Gubat, Sorsogon” (Unpublished Undergraduate Thesis), 2008 (Bicol University College

of Business, Economics and Management, Daraga, Albay).

Espartinez, Junalyn B., Monreal, Jolibee L., “Credit Management Practices of

Selected Financing Institutions in Legazpi City” (Unpublished Undergraduate

Thesis), 2007 (Divine Words College of Legazpi, Legazpi City).

Page 31

Naño, Quiamno 31

Fajardo, Feliciano, Economics Development, (National Bookstore Inc., 1985), p.

96

http://en.wikipedia.org/wiki/Microfinance

http://www.eHow.com/Microfinance

http://en.wikipedia.org/wiki/Ligao City

http://ifrm,acin/cmf/20060401/evaluatimh-microfinance-randomize/

yahoo.com,Microfinance

http://www.businessballs.com/davidmcclelland.htm

International year of micro- credit- http//www.yahoo.com Copyright 2007, May 7. 2004

Manrique, Dennis. “An Analysis of the Credit Delivery System of Simbag sa Pag-

Asenso, Inc.-SEDP, Legazpi City” (Unpublished Undergraduate Thesis), 2008 (Bicol

University College of Business, Economics and Management, Daraga, Albay).

Michelle V. Remo, Philippine Daily Inquirer- November 11, 2009

Miraflor, J.P. “The Effects of Informal Lending Sectors on the Profitability of

Microbusiness Establishment in the Market Site of Daraga, Albay” (Unpublished

Undergraduate Thesis), 2002 (Bicol University, Daraga, Albay).

Miranda, Gregorio S., Essentials of Money, Credit and Banking (Philippines: Land G

Business House 1998), p. 107

Page 32

Naño, Quiamno 32

Moderno, Kathryn, “Microfinance: Path to Poverty alleviation” ,The first Annual

Undergraduate Applied Social Justice Essay , April 10 ,2010

Moral, C.C. “An assessment of the Performance of SEDP, Inc. in Legazpi City”

(Unpublished Undergraduate Thesis), 2008 (Bicol University, Daraga, Albay).

Neo, Maria Cristina. “A Case Analysis of a Formal Microfinance Lending

Institution.” (Unpublished Undergraduate Thesis), 2008 (Bicol University College of

Business, Economics and Management, Daraga, Albay).

Organizational Behavior( Human Behavior at Work) john w. Newstorm Ph. D. university

of Minnesota Duluthmc graw. Hill interbational edition, 12th edition p. 106

Philippines Microfinance Sector high on innovation :BSP Governor, Mr. Amando M

Tetangco Jr, congratulated the microfinance sector for its robust growth(an excerpt),

Microfinance Focus, May 27, 2010

Schelzig, Karen " Poverty in the Philippines: Income, Assets and Access" Copyright 2005 Asian

Development Bank, Microfinance in the Philippines

Webster’s Dictionary for students.(Federal Street Press), 2007

Vat II, Gaudium et Spes No. 1

Page 33

Naño, Quiamno 33

CHAPTER III

PRESENTATION, ANALYSIS AND INTERPRETATION OF DATA

This chapter discusses the interpretation of the data gathered by the researchers

regarding the perceptions of beneficiaries on Socio-Economic Development Program

Inc. in Ligao City. The data are presented, analyzed and interpreted according to the

statement of the research problem.

1. PROFILE OF THE BENEFICIARIES

The first objective of the study is to know the profile of each beneficiary of the

SEDP. Inc. for it helped the researchers to determine the perceived gains and negative

effects of the microfinance to its beneficiaries. The profile of the respondents consist of

their age, educational attainment, civil status, occupation, number of children living with

them, monthly income and membership status.

The following tables show the data and information concerning the profile of the

respondents of the study.

a. AGE

Based from the results, the ages of the respondents are ranging from 26 to 61

and above.

Page 34

Naño, Quiamno 34

Table 1.1

Age of the respondents

Age Frequency Percent26-30 15 5.231-35 39 13.536-40 59 20.441-45 39 13.546-50 48 16.651-55 34 11.856-60 34 11.861 & Above 21 7.3Total 289 100.0

Table 1.1 shows that there are only 15 of the total respondents who have the age

of 26 to 30 and 39 of them were 31 to 35. There are also 59 has the age of 36 to 40 and

39 are 41 to 45. The number of respondents with 46 to 50 years old was 48 and 34

among them were at the age of 51 to 56. 34 respondents are at the age of 56 to 60 and

only 21 of the total respondents have the age of 61 and above. It was shown that the

most prominent among the ages was respondents having the age of 36 to 40.

The aforementioned ages by the respondents were important to this study to

analyze which age has the least capability to repay a loan.

b. EDUCATIONAL ATTAINMENT

According to the gathered data, the highest education of the beneficiaries which

they completed is stated in the table. This helped the researchers to determine whether

the beneficiaries were knowledgeable enough and has the ability to understand how the

microfinance could help them especially to their socio economic development.

Page 35

Naño, Quiamno 35

Table 1.2

Educational attainment

Table 1.2

illustrated that

majority of the

beneficiaries attained high school graduate with 34.9 percent (101 out of 289). It was

followed by 61 of respondents who only graduated elementary. Only 2 of the total

respondents were elementary undergraduate and 60 of them were high school

undergraduate. There are also 39 of the total respondents who were college

undergraduate, 22 have graduated college and 4 who took vocational.

Since majority of the beneficiaries were only elementary graduates, there is a

tendency that most of them have less knowledge in handling the money that the

institution had provided.

c. CIVIL STATUS

Table 1.3

Frequency and percentage of the civil status of the beneficiaries

Educational Attainment Frequency PercentElementary Undergraduate 2 .7Elementary Graduate 61 21.1High School Undergraduate 60 20.8High School Graduate 101 34.9College Undergraduate 39 13.5College Graduate 22 7.6Vocational 4 1.4Total 289 100.0

Page 36

Naño, Quiamno 36

It was shown in table 1.3 that there are

only 1.4 percent (4 out of 289) of respondents

were single and 98.6 percent of them were married. It only shows that the majority of

the respondents were in need of supporting their own family that’s why they are being

encouraged to engage in microfinance institution.

Table 1.4 Occupations

Government employee and Self-Employed

d. OCCUPATION

Civil Status

Frequency Percent

Single 4 1.4Married 285 98.6Total 289 100

Government Employee

Frequency Percent

Teacher 5 23.8

Office Clerk 2 9.5

Others 14 66.7

Total 21 100

Self-Employed

Frequency

Percent

Store Owner 73 27

Buy and Sell 93 34

Farm Owner 57 21

Others 49 18

Total 268 100

Page 37

Naño, Quiamno 37

The occupation of the beneficiaries is divided into two groups. First is

government employee wherein they can be a teacher, office clerks and others. Second

is self employed which can be a store owner, buy and sell, farm owner and others.

Table 1.4 shows that majority of the beneficiaries were self employed. Only 7

percent of the total respondents were government employee. There are 5 of them who

were teachers, 2 were office clerks and 14 have other jobs in the government. Majority

of the self- employed respondents were buying and selling different types of products.

There are also 73 of the beneficiaries who are able to have their own stores. 57 of them

were farm owners only 49 were having other types of business where they were

working.

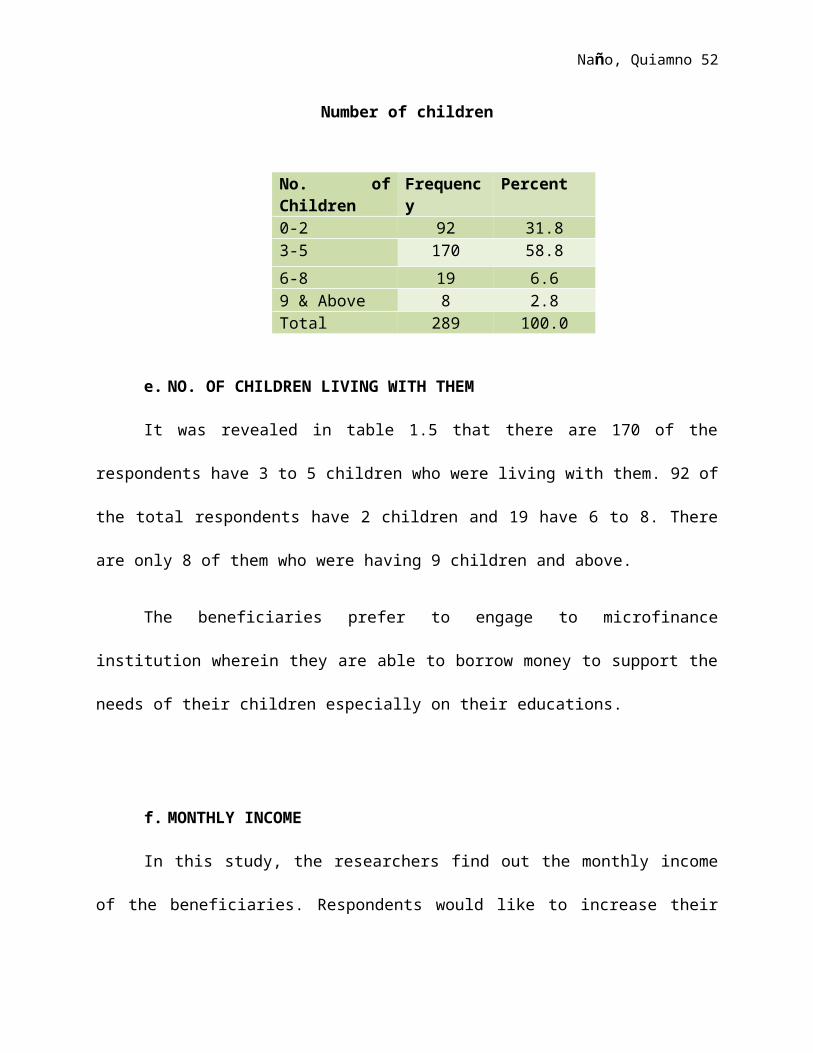

Table 1.5

Number of children

e. NO. OF CHILDREN LIVING WITH THEM

It was revealed in table 1.5 that there are 170 of the respondents have 3 to 5

children who were living with them. 92 of the total respondents have 2 children and 19

have 6 to 8. There are only 8 of them who were having 9 children and above.

No. of Children

Frequency Percent

0-2 92 31.83-5 170 58.8

6-8 19 6.69 & Above 8 2.8Total 289 100.0

Page 38

Naño, Quiamno 38

The beneficiaries prefer to engage to microfinance institution wherein they are

able to borrow money to support the needs of their children especially on their

educations.

f. MONTHLY INCOME

In this study, the researchers find out the monthly income of the beneficiaries.

Respondents would like to increase their incomes. They believe that engaging in a

microfinance institution can solve their problem regarding their monthly income.

Table 1.6

Monthly Income

Table 1.6 illustrated the monthly income of the beneficiaries. It was revealed that

there are only 2 of the total respondents have the income of P 16, 000 and above. Many

of them have only P 4, 000 to P 6, 999 with the number of 100 respondents. There are

Monthly Income

Frequency

Percent

P 1, 000- 3, 999

74 25.6

4, 000- 6999 100 34.67, 000- 9, 999 68 23.510, 000- 12, 999

31 10.7

13, 000- 15, 999

14 4.8

16, 000 & Above

2 .7

Total 289 100.0

Page 39

Naño, Quiamno 39

74 respondents who have only P 1, 000 to P 3, 999 monthly incomes. 68 of the

respondents have the income of P 7, 000 to P 9, 999, 31 respondents with P 10, 000 to

P 12, 999 and 14 respondents who have P 13, 000 to P 15, 999 monthly incomes.

g. MEMBERSHIP STATUS

This includes the number of years beneficiaries were availing the program of the

institution, their latest loans, and if they are still availing other microfinance other than

Socio- Economic Development Program Inc.

Number of Years in SEDP Inc.

This states the number of years the beneficiaries are being part of the

institution.

Table 1.7

No. Of Years in SEDP Inc.

Table 1.7 illustrated that there are 63 of the total respondents were already 1 to 3

years as part of the institution. Majority of the respondents were 4 to 6 years in SEDP

Inc. as a member of the institution. 56 of the respondents spent 7 to 9 years and only 36

of them are 10 years and above in the institution.

Latest Loan

No. of years in SEDP Inc.

Frequency

Percent

1-3 63 21.84-6 132 45.77-9 58 20.110 or more 36 8.0Total 289 100.0

Page 40

Naño, Quiamno 40

Based from the responses of the beneficiaries, their latest loans are ranging from P 3,

000 as their initial loan to P 35, 000 as the highest loans which they acquired from the

institution. P 3, 000 as the smallest amount is the loan that a newly member can only

obtain and can be increased depending on cycle which they can continuously obtain a

loan. They can acquire loans every after their final payment of their current loan. P35,

000 as a loan can be attained if a member is already 12-15 years in SEDP Inc.

Table 1.8

Latest Loans

As shown on Table 1.8, there are 30 of the total respondents who have a latest

loan of P 3, 000 to P 5, 999 and only two respondents having a loan of P 6, 000 to

P 8, 999. There are also 42 of the respondents having their latest loan of P 12, 000 to

Latest Loan Frequency PercentP 3, 000- 5, 999

30 10.4

6, 000- 8, 999

2 .7

9, 000- 11, 999

127 44

12, 000- 14, 999

42 14.5

15000 38 13.120000.00 11 3.822000.00 6 2.122500.00 2 .725000.00 27 9.335000.00 6 2.1Total 289 100.0

Page 41

Naño, Quiamno 41

P 14, 999 and 38 respondents with P 15, 000. 6 of them have their latest loan of

P 22, 000, 2 respondents with P 22, 500, 27 respondents with P 25, 000, and only 6 of

the total respondents having the latest loan of P 35, 000.

Received other help from other microfinance rather than SEPD Inc.

Table 1.9.1

Frequency and percentage of beneficiaries who receives other help from other

microfinance

Table 1.9 illustrated that majority of the total respondents does not receive any

other help from other microfinance institution rather than Socio- Economic Development

Program Inc. only 60 of them availed from other institutions such as Tulong sa Pag-

Unlad, Inc. (TSPI) Center for Agriculture and Rural Development (CARD), Happy

Lending Institution, Intertrade, Agricultural and Rural Development for Catanduanes,

Inc. (ARDCI), and others.

Table 1.9.2

Other Microfinance Institutions

Frequency PercentNo 229 79.2Yes 60 20.8Total 289 100.0

Page 42

Naño, Quiamno 42

Table 1.9.2 shows the various other microfinance wherein some other

beneficiaries of SEDP, Inc. availed loans. There are 23 of the respondents who

borrowed money from TSPI, 21 respondents loaned from CARD Inc., only 4 of them

availed on HLIP, 6 respondents borrowed money from INTERTRADE and 3 of them

availed loans from ARDCI. There are also 7 of the total respondents borrowed from

other microfinance not stated above.

II. SOCIO- ECONOMIC FACTORS THAT MOTIVATED BENEFICIARIES IN AVAILING

MICROFINANCE

This includes the socio- economic factors that could be the reason to motivate

the beneficiaries who obtained loan from microfinance.

Other Microfinance Institutions

Frequency Percent

None 225 77.9TSPI 23 8.0CARD 21 7.3HLIP 4 1.4INTERTRADE 6 2.1ARDCI 3 1.0Others 7 2.4Total 289 100.0

Page 43

Naño, Quiamno 43

Table 2

Frequency, percent and ranking distribution of respondents by the Socio-

Economic Factors which motivated beneficiaries from availing microfinance

Table

2 shows

the

frequency, percent and ranking distribution of respondents by the socio-economic

factors that motivated them to avail microfinance. It reveals that most of the

respondents who engage in availing of microfinance loan utilized the amount loaned for

their additional capital. They acquire loan in order to increase their income through

loans from lending institutions and adjoin the money to their capital on business. It also

shows that the amount loaned was used for capital for their new business. According to

them, they can build a new business through their loans from the institution. It also

revealed that they are encouraged to engage in microfinance so that they can be able to

renovate their house and construct their houses. One of the reasons on availing a

lending institution is that its loan is a long term and has a low interest loan. They also

Socio-Economic Factors Frequency Percent Rank

Additional Capital 201 69.6 1

Education of children 182 63 2

Long-term loan 131 45.33 3

Low percent interest loan 128 44.29 4

Capital for a new business

92 31.83 5

Renovation of House 87 30.1 6

Medical and Emergencies

40 13.8 7

No job 23 8 8

Construction of new house

13 4.5 9

Others 10 3.46 10

Page 44

Naño, Quiamno 44

utilized the amount loaned for the medical and emergencies on their family and other

said that they are not able to find a job. Through microfinance, they can earn money by

investing it in a proper way.

III. PERCEIVED GAINS OF THE BENEFICIARIES ON MICROFINANCE

Table 3.1

Perceived gains as a businesswoman of the beneficiaries on microfinance

a. AS A BUSINESSWOMAN

As shown in table 3.1, the perceived gains of the beneficiaries on microfinance

are the following: there are 92 of the respondents believed that they were able to build

their own business through their loaned money from microfinance, 22 respondents said

Perceived Gains as a businesswoman

Frequency

Percent

Capital for a new business

92 31.8

Business Expansion 22 7.6

Additional capital 197 68.2

Total 289 100.0Business Type Frequen

cyPercent

Buy and Sell 56 62

Handicraft 3 3Food Production 5 5Services 4 4Others 24 26Total 92 100

Page 45

Naño, Quiamno 45

that they were able to expand their business, and 197 believed that the amount loaned

from microfinance had helped them to increase their capital on their business.

Having a capital for their new business, beneficiaries were engage to businesses

such as buy and sell, handicraft, food production, services and others. Majority of them

used the borrowed money in buying and selling various types of products. There are

only 3 of the respondents who used loaned money for handicraft. Some of them used

the loaned money for food production, services and others.

Table 3.2

Perceived gains on attitudes

b.

ATTITUDES

Perceived gains on attitude

Frequency Percent Rank

Became more disciplined 204 70.6 1

Leaned to save 153 52.9 4Developed self and group awareness

59 20.4 6

Became more diligent 167 57.8 3Became more responsible 200 69.2 2

Developed leadership skill 17 5.9 7Learned to communicate with others

98 33.9 5

Page 46

Naño, Quiamno 46

Table 3.2 shows that 70.6 percent of the beneficiaries developed their discipline.

With their loans, they learned how to spend their money properly and wisely. 153 of the

total respondents also believed that they learned to save. By the amount they loaned,

they became aware on how to allocate their money so that they can repay their loans on

time. 59 of them said that they developed their self and group awareness. Through

weekly meetings, they were able to know each other better. 167 respondents became

more diligent. They became more industrious to be able to repay loans weekly. 200 of

them also became more responsible because of their obligation to pay amount loaned

and 17 of them said that they were able to develop their leadership skill. Every center

has center chief who is responsible for manage all group members and checking if

which member could not repay on the weekly meeting. There are also 98 who believed

that they learned to communicate with others. In some instances, some of the group

members could not repay weekly, by proper communication they were able to provide

money from their group mates and can pay for the weekly collection of loans.

c. IN THE FAMILY

There are also benefits in the family by availing of lending institution loan. These

are determined through the responses of the respondents.

Table 3.3

Perceived gains in the family

Page 47

Naño, Quiamno 47

The table illustrated the perceived gains in the family of the beneficiaries’ of

the microfinance. It revealed that many of them have increased their family income. By

investing the amount loaned, they were able to raise their family income. Others were

able to send their children to school. They utilized the money loaned for buying of

school materials, for allowances and most importantly for settling the tuition fees. Some

of them are able to renovate their houses. The institution also offered trainings and

seminars which enabled them to gain new ideas concerning business enhancement.

Other respondents were able to construct their houses and some has used for

medicines and emergency cases on their family.

IV. NEGATIVE EFFECTS OF MICROFINANCE TO BENEFICIARIES

There are some problems faced by the beneficiaries that lead to negative effects

of microfinance to the beneficiaries. Based from the data gathered, the negative effects

are consisted with the following: non- cooperation of group members, being dependent

on the SEDP, Inc., difficulty in repaying the loan and slow processing of loans.

Perceived gains in the family Frequency

Percent

Rank

Increased family income 227 78.5 1

Used for education of children 206 71.3 2

Used for renovation of house 116 40.1 4

Offered trainings 119 41.2 3Used for construction of new

house28 9.7 6

Used for medicines and emergencies

57 19.7 5

Others 13 4.5 7

Page 48

Naño, Quiamno 48

Table 4

Negative effects of the microfinance to the beneficiaries

As shown in table 4, majority of the beneficiaries have affected by the non-

cooperation of group members and difficulty of repaying their loans. There are also 11

of them who revealed that they became dependent to SEDP, Inc.. they did not find other

source of capital or money rather than microfinance. There are only 7 respondents who

said that the institution was slow in processing of loans and 3 of them share other

negative effects.

CHAPTER IV

Negative effects Frequency Percent Rank

Non- cooperation of group member 136 47.1 1.5

Difficulty in repaying loans 136 47.1 1.5

Being dependent to microfinance 11 3.8 3

Slow processing of loans 7 2.4 4

Others 3 1.0 5

Page 49

Naño, Quiamno 49

SUMMARY OF FINDINGS, CONCLUSIONS AND RECOMMENDATIONS

This chapter presents the summary, findings and conclusions from which the

recommendations were drawn to give value to the result of the study.

Summary

This study was conducted to determine the perceived gains and negative effects

of programs and practices of socio- economic Development program, Inc. in Ligao City.

Specifically, the study sought answers to the following questions:

1. What is the profile of the beneficiaries in terms of:

f) Age

g) Educational background

h) Civil status

i) Occupation

j) Number of children

k) Monthly income

l) Respondents membership status

2. What are the socio-economic factors that motivate households on availing the

microfinance?

Page 50

Naño, Quiamno 50

3. What are the perceived gains of the beneficiaries on availing the

microfinance?

4. What are the negative effects of the beneficiaries on availing the

microfinance?

5. What are the ways to reduce the effect of microfinance?

This study used descriptive method in determining the perception of the

beneficiaries towards the effects of the programs and practices of Socio-Economic

Development Program, Inc. in Ligao City. The researchers used questionnaires in

gathering data. Two hundred eighty nine (289) were the key informants of this study.

The data gathered were analyzed using frequency count, percentage rating ad ranking

as statistical tools.

Findings

Based on the results of the study, the following findings were revealed.

1. a. Age- The age of the respondents is ranging from twenty six (26) to sixty (60)

and above. Based from the responses, there are beneficiaries with the age of seventy

two (72). There are only fifteen of them were at the age of twenty six (26) to thirty (30)

and thirty nine (39) respondents were thirty one (31) to thirty five (35). Fifty nine (59) of

the respondents were thirty six (36) to forty ( 40) years of age and thirty nine (39) of

them with forty one (41) to forty five (45) ages. There are also forty eight (48)

Page 51

Naño, Quiamno 51

respondents who were at the age of forty six (46) to fifty (50) and thirty four (34) among

them were fifty one (51) to fifty six (56) years of age.

b. Educational attainment- majority of the respondents (101) were high school

graduate. There are sixty one (61) of the respondents who only graduated elementary

and two (2) respondents were elementary undergraduate. Thirty nine (39) of them were

college undergraduate and twenty two (22) respondents who completely attained their

college degree. There are also 4 respondents who took vocational.

c. Civil status- mostly, the respondents were married two hundred eighty five

(285). Only few of them which are four (4) respondents were single.

d. Occupation- majority of the respondents were self employed with the number

of 268. The remaining twenty one (21) of them were working in the government. Five (5)

of the respondents were teachers and two (2) of them wee office clerks. Fourteen (14)

of the government employed were barangay health worker and DSWD foster parent.

Ninety three (93) of the total number of respondents was buying and selling of various

types of products, seventy three (73) respondents having their stores and fifty seven

(57) respondents were farm owners (rice, corn, vegetables, etc.). The rest of the

respondents (49) were having employed to other types of business like direct selling,

ladies accessories, piggery, franchise dealer, food vending and vegetable vending.

e. Number of children living with you. One hundred seventy (170) of the

respondents have 3 to 5 children. Ninety two (92) of the total respondents have 2

children and below and 19 of them have 6 to 8 children. There are only eight (8) of them

who have 9 children and above.

Page 52

Naño, Quiamno 52

f. Monthly income- only two of the total respondents have a monthly income of P

16, 000 and above. Majority of the respondents (100) have only P 4, 000 to 6, 999

monthly income. There are 74 respondents revealed that they have P 1, 000 to 3, 999

monthly incomes. 68 respondents have P 7, 000 to 9, 999 monthly income, 31

respondents with P 10, 000 to P 12, 999 and 14 respondents who have P 13, 000 to 15,

999 monthly incomes.

g. Membership status- in terms of number of years they were availing of the

microfinance, majority of the respondents were 4 to 6 years as a member of the

institution. 56 of the respondents were 7 to 9 years and 36 of them are 10 years and

above in the institution. As to latest loan, there are 30 respondents who have a latest

loan of P 3, 000 to 5, 999 and 2 respondents having P 6, 000 to P 8, 999 loan. 42 of

them have P 12, 000 to 14, 999 latest loan and 38 respondents with P 15, 000. 6 of

them have P 22, 000, 2 respondents with P 22, 500, 27 respondents with P 25, 000,

and 6 of them having the latest loan of P 35, 000. Majority(78 %) of the respondents did

not avail other loans from other institutions. Only 22 % of them availed.

2. As to socio economic factors that motivated beneficiaries on availing of microfinance,

it revealed that most of the respondents need to increase their capital with 201

respondents and 182 of them revealed that they need money for the education of their

children. 131 said that it ia a long term loan and 128 revealed that the interest rate of

the institution is low.92 of them said that they used the loan for capital in a new

business and 87 said that they need to renovate their houses. 40 said that it would be in

medicines and emergencies, 23 are unemployed and 13 for the construction of their

house. Only 10 of them were having other motivators in availing loan.

Page 53

Naño, Quiamno 53

3. Perceived gains- as a business woman, majority revealed that they have used the

amount loaned for additional capital of their existing business. 22 of the respondents

have used the money for business expansion and 92 of them said that they used it for

additional capital for their businesses such as buy and sell (62 %), handicraft (3%), food

production (5%), services (4%) and others (26 %). In terms o perceived gains to

attitude, 204 of them became more disciplined, 153 have learned to save, fifty nine (59)

respondents developed self and group awareness and 167 became more diligent.

There is also a lot of respondents who became more responsible, only seventeen (17)

developed their leadership skill and 98 of the respondents learned to communicate with

others. In the family, majority have increase their income, 206 used the loaned money in

education of children, one hundred sixteen (116) have renovated their house, one

hundred nineteen (119) said that institutions have offered trainings, twenty eight (28) of

them were able to built their new house, fifty seven (57) respondents have used amount

loaned for medicines and emergencies and 13 respondents used money borrowed in

other matters.

4. As to negative effects of microfinance to its beneficiaries, same number of

respondents revealed that their group members did not cooperate. Eleven (11) of them

became independent on microfinance, there are also 7 who said that their processing

was slow and 3 other effects were revealed.

5. There are a number of suggestions given by the respondents to reduce the effect of

microfinance of microfinance to their lives. 143 of the total respondents which are 49

percent gave their suggestions regarding the reduction of the effects of engaging in the

institution.

Page 54

Naño, Quiamno 54

Conclusions

Based on the significant findings of the study, the following conclusions are

deduced:

1. Majority of the beneficiaries are at the age of 36 to 40. These ages are in need of

source of income because they were not able to find a job especially in rural

areas. They prefer to engage in this institution to be able to have fund for

whatever they are planning for.

Many of the respondents are only high school graduate. They are less

knowledgeable on how to handle their money borrowed and less aware of the

possible effect of lending institutions to their lives. Majority of the beneficiaries

are married. They need to have a source of income in order to help and support

their families. 170 of the respondents have 3 to 5 children. By availing of

microfinance, they believe that they can support the needs of their children.

Mostly, the monthly income of the respondents is ranging P 4, 000 to 6, 999. This

is very small amount and not enough to support the needs of the family and one

of the reasons why beneficiaries availed the program. Most of the beneficiaries

were 4 to 6 years availing the loan. They preferred to stay as a member of

microfinance to continuously finance their businesses. Majority of respondents

have the latest loan of 9, 000 to 11, 999. It shows that it also increases the needs

of the respondents for financial of their activities or businesses. There are 60 of

the respondents who are still availing other microfinance. This shows that other

beneficiaries are not contented with the program that SEDP Inc. has provided for

them.

Page 55

Naño, Quiamno 55

2. Most of the respondents stated that they need to have an additional capital. They

believe that availing of lending institution loan like Socio- Economic Development

Program Inc. is the easiest way to increase their capital in their existing business.

3. Mostly, additional capital is the primary gains that beneficiaries have perceived.

They have their own business, however, they still avail microfinance to increase

their capital. In their attitude, most of them have developed their discipline.

Because of the obligation they accepted, they now have to repay their loans.

Majority of the respondents have increased their income. By investing their

amount loans practically, they can increase their loans.

4. The same number of respondents have affected by the non cooperation of group

members and difficulty in repaying of loans.

5. Many of the respondents suggested different ways to reduce the negative effect

of microfinance to their lives. By suggesting such ways, they believed that this

can help them to lessen the effects.

Recommendations

1. The Socio- Economic Development Program should improve their recruitment

process and add some qualifications for their incoming members so that it would

help to lessen the problems faced by the current members. They should improve

their program and services so that their beneficiaries will be contented on the

institution and will not avail from other microfinance.

2. By the suggestions given, the institution should not recruit those who are not

capable of repaying a loan. They should make sure that the person to be

recruited is recognized by the current member from a certain center. And current

Page 56

Naño, Quiamno 56

members should select their members that they really know that she is capable

of repaying loans.

3. Members should allocate their money properly and invest in profitable way to be

able to repay their loaned money.

4. Problems from a various centers should be given attention by the office and

concerned persons and immediately make actions to resolve the problem.

5. Beneficiaries should be responsible enough to carry their obligations and always

prepare for weekly payments.

6. The institution must plan more seminars and trainings on how to improve the

livelihood of its beneficiaries and lecture them some tips on how to handle money

rightly and how to invest their amount loaned properly.

7. Force resignation or offset for those who are not repaying their loans regularly or

inactive members. They can cause problems and may affect active members

who always pay on time.

8. In case of difficulty, members should not make another loan from other

microfinance institution.

9. Before the loan should be released in a newly members, make sure that they

have a planned project to earned money from the borrowed amount and will be

able to repay loans regularly.

10.Make the processing of loans faster because persons who are availing of it is

really in need of money.

![THESIS TITLE A THESIS SUBMITTED TO THE MIDDLE EAST ...ii.metu.edu.tr/system/files/documents/thesis... · [SAMPLE 1] Approval of the thesis: THESIS TITLE Submitted by STUDENT NAME](https://static.documents.pub/doc/80x56/6019035f39977162fc4f0b03/thesis-title-a-thesis-submitted-to-the-middle-east-iimetuedutrsystemfilesdocumentsthesis.jpg)