Page 1

UNIVERSITY OF MISKOLC

FACULTY OF ECONOMICS

THESIS ANNOUNCEMENT

FULL NAME: Heena Kapoor

NEPTUN CODE: YL70T

TYPE OF PROGRAMME: MSc

NAME OF PROGRAMME: Master of Business Administration (English)

NAME OF SPECIALISATION: Economics

RESPONSIBLE DEPARTMENT OR INSTITUTE: Institute of Management Science

TITLE OF THESIS: Comparative Analysis On Budapest Stock Exchange And Bombay Stock

Exchange

ASSIGNMENT:

− Introducing the economy of India and Hungary

− Introducing the Stock exchanges of both countries Analysis of the financial ratio of

the company

− Analyzing the Value at Risk model using company stock prices

BASE ORGANISATION : Richter Gedeon Nyrt, Sun Pharma, OTP Bank, SBI, MOL and ONGC

INTERNAL CONSULTANT : Dr Zsombori Zsolt, Lecturer

EXTERNAL CONSULTANT (name, position):

DATE OF THESIS ANNOUNCEMENT:

Date: …………………

………………………………..

Head of Institute

Page 2

UNIVERSITY OF MISKOLC

FACULTY OF ECONOMICS

CONSULTATION SHEET

FULL NAME: HEENA KAPOOR

NEPTUN CODE: YL970T

TITLE OF THESIS: Comparative Analysis On Budapest Stock Exchange And Bombay Stock

Exchange

BASE ORGANISATION : Richter Gedeon Nyrt, Sun Pharma, OTP Bank, SBI, MOL and ONGC

INTERNAL CONSULTANT : Dr Zsombori Zsolt, Assistant Professor

EXTERNAL CONSULTANT (name, position):

DATES OF CONSULTATIONS:

Consultation date Signature of internal

consultant Consultation date

Signature of external

consultant

The thesis can be accepted:

Date: …………………

………………………………..

Internal Consultant

Date: …………………

………………………………..

External Consultant

Page 3

Declaration Of Originality

FULL NAME: HEENA KAPOOR

NEPTUN CODE: YL970T

TITLE OF THESIS: Comparative Analysis On Budapest Stock Exchange And Bombay Stock

Exchange

I, the undersigned, hereby declare under penalty and perjury that each part of my thesis (text,

figures, tables, etc.) – except the cited ones − is my own work and does not rely on other

documents including my previous theses.

I am aware of the fact that plagiarism consists of:

− direct quoting without indicating the reference;

− indirect quoting without indicating the reference;

− publishing others’ ideas as my own.

I, the undersigned, hereby declare that I am aware of the definition of plagiarism and I

understand that according to connecting regulations my thesis can be rejected and

disciplinary proceedings may be applied if plagiarism is proved.

I declare that the electronic (CD and uploaded) and hard copy of my thesis are identical in

form and content.

Date: …………………

………………………………..

Signature of Student

Page 4

STUDENT’S DECLARATION FORM

Student’s name: HEENA KAPOOR

Neptun code: YL970T

Faculty and programme: Faculty of Economics, Master of business administration

Year of thesis submission: 2019

Title of the thesis: Comparative analysis of Budapest stock exchange and Bombay stock

exchange

I request that my thesis be treated confidentially (requires an application for confidential

treatment). (Please underline as applicable.)

Yes No

I allow the university library to publish my thesis as full text on the Internet. (Please underline as applicable.)

Yes No

In full awareness of my liability I declare that the electronic version of my thesis is identical to the printed thesis I submitted.

Date: …………………….

…………………………………………..

Signature of student

Student’s current address: 2/A kiss Jozsef utca, Budapest, 1081 Hungary

E-mail: [email protected]

Phone number: +36702715667

Page 5

UNIVERSITY OF MISKOLC

FACULTY OF ECONOMICS

Comparative Analysis of Budapest Stock Exchange

and Bombay Stock Exchange

Heena Kapoor

2019

Page 6

Abstract

Stock market is a vital part of every economy. Rise and fall in economy are reflected by the

stock market. Bullish stock market is the sign of developing industrial sector and growing

economy of the country. This thesis involves the analysis of Budapest stock exchange and

Bombay stock exchange, and in order to further understand the associated risk, a comparison

was made between them using two statistical techniques. The Oil, Banking and

Pharmaceutical industries forms the backbone of nation’s economy. Thus, the analysis was

conducted on the prominent companies in Oil, Banking and Pharmaceutical industries of

both the stock exchanges. The VaR analysis was performed on the portfolio to analyse the

risk associated with market. The evaluation of companies operating, and financial

performance was conducted using ratio analysis technique.

Financial results have become an important indicator for business valuation. The Average

Price Return have the significant influence on the Ratios represents the aggregate value of a

company or stock. The purpose of this study is to analyse the relationship between the

Financial Ratio and the Average Price Return of the chosen companies from the two Stock

Exchanges. The price of company’s stock is a significant factor and should be kept in mind

while making investment as it shows the value of a company. We took 3 companies from 3

important sector of economy- Banking, Pharmaceuticals and Oil.

Page 7

Table of Contents

1. Introduction ................................................................................................................... 1

2. Objectives ...................................................................................................................... 5

3. Limitations of the study ................................................................................................. 6

4. Hypotheses .................................................................................................................... 7

5. Methodology .................................................................................................................. 8

1. Value at Risk ....................................................................................................... 8

2. Benchmark model ....................................................................................................... 8

3. Excel ........................................................................................................................... 8

6. Literature Review .......................................................................................................... 9

7. Theoretical Background .............................................................................................. 12

7.1 Hungarian Economy .............................................................................................. 12

7.2 Indian Economy ......................................................................................................... 14

7.3 Stock Exchange ..................................................................................................... 16

7.3.1 Budapest Stock Exchange ...................................................................................... 17

7.3.2 Bombay Stock Exchange ........................................................................................ 20

7.3.3 Listed Domestic Companies ................................................................................... 22

7.4 MOL .......................................................................................................................... 23

7.5 Oil and Natural Gas Corporation Ltd ........................................................................ 24

7.6 OTP BANK ............................................................................................................... 25

7.7 State Bank of India .................................................................................................... 26

7.8 Richter Gedeon Nyrt ............................................................................................. 27

7.9 Sun Pharmaceuticals .................................................................................................. 28

7.10 Investment Risk Management ................................................................................. 29

7.11 VAR MODEL ................................................................................................... 30

7.12 Ratio .................................................................................................................. 33

7.13 T-Test in Ms-Excel............................................................................................ 36

8 Quantitative Analysis ................................................................................................... 37

8.1.1 OTP ......................................................................................................................... 37

Ratio Analysis ............................................................................................................. 37

T-TEST ........................................................................................................................ 37

8.1.2 Richter Gedeon Nyrt ............................................................................................... 39

RATIO ANALYSIS .................................................................................................... 39

T-TEST ........................................................................................................................ 39

Page 8

8.1.3 MOL ....................................................................................................................... 41

RATIO ANALYSIS .................................................................................................... 41

T-TEST ........................................................................................................................ 41

8.1.4 SBI .......................................................................................................................... 43

RATIO ANALYSIS .................................................................................................... 43

T-TEST ........................................................................................................................ 43

8.1.5 Sun Pharma ....................................................................................................... 45

RATIO ANALYSIS .................................................................................................... 45

T-TEST ........................................................................................................................ 45

8.1.6 ONGC ..................................................................................................................... 47

RATIO ANALYSIS .................................................................................................... 47

T-TEST ........................................................................................................................ 47

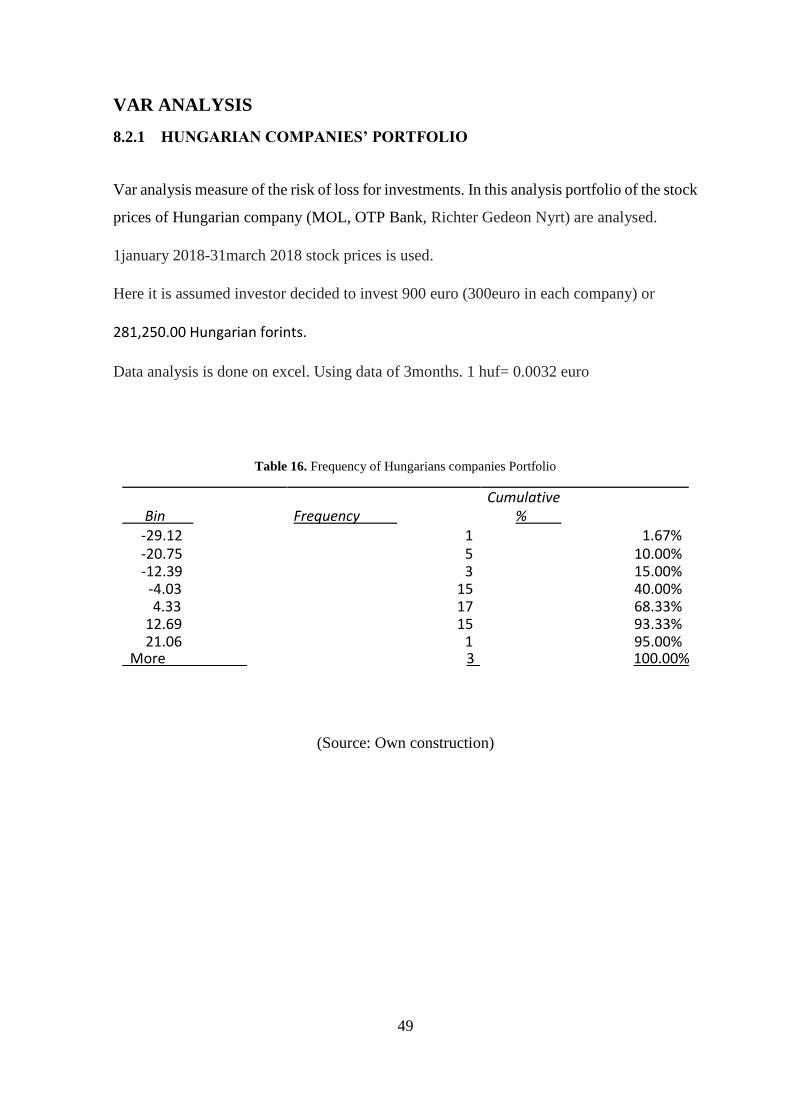

8.2.1 HUNGARIAN COMPANIES’ PORTFOLIO .................................................. 49

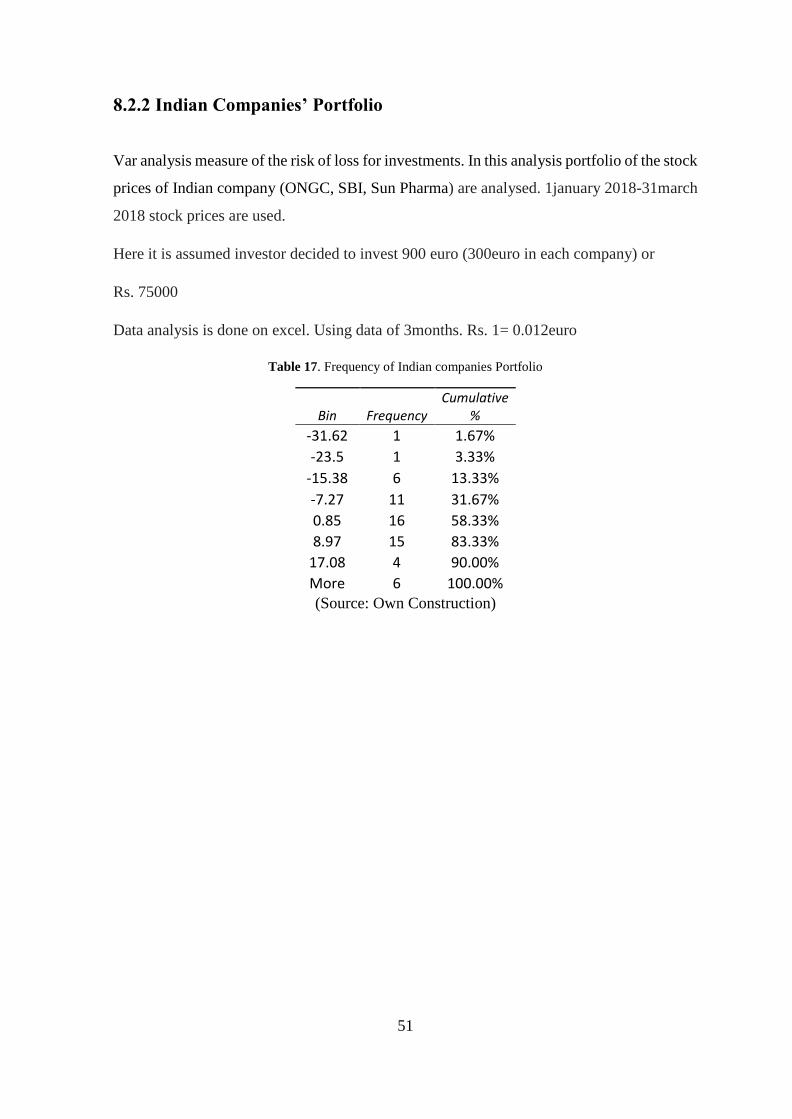

8.2.2 Indian Companies’ Portfolio .................................................................................. 51

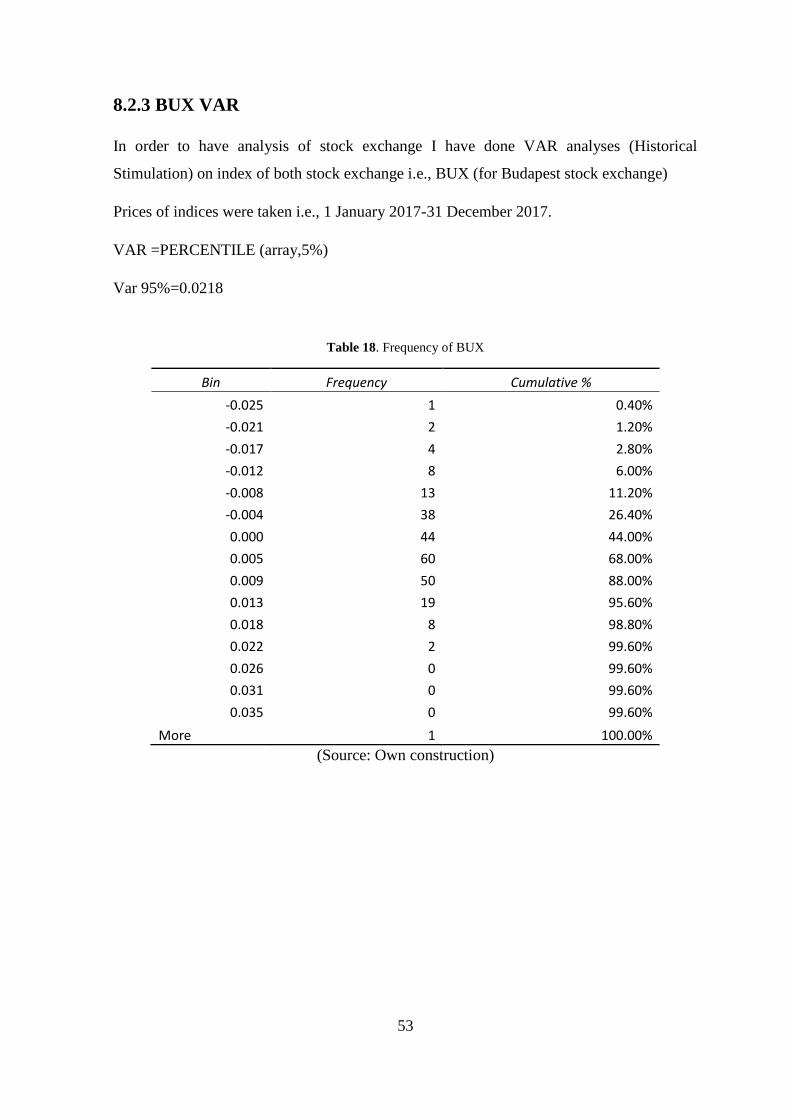

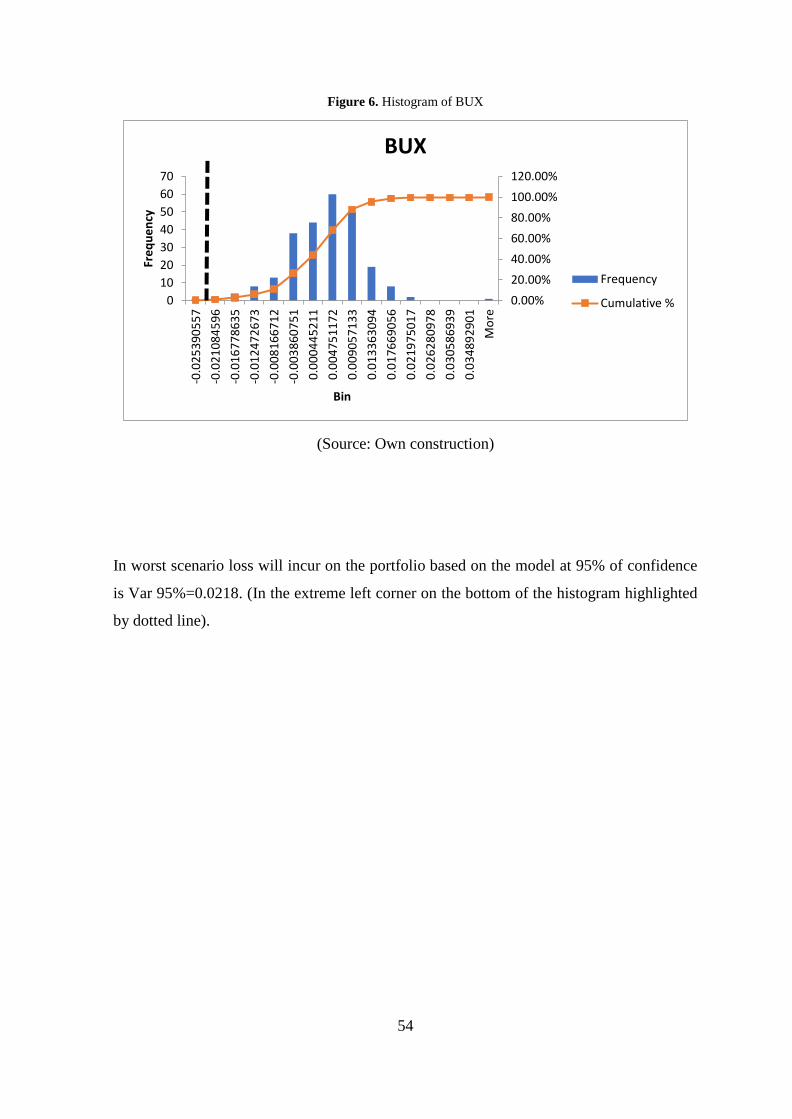

8.2.3 BUX VAR .............................................................................................................. 53

8.2.4 SENSEX VAR ........................................................................................................ 55

9. Conclusion ....................................................................................................................... 57

References ........................................................................................................................... 59

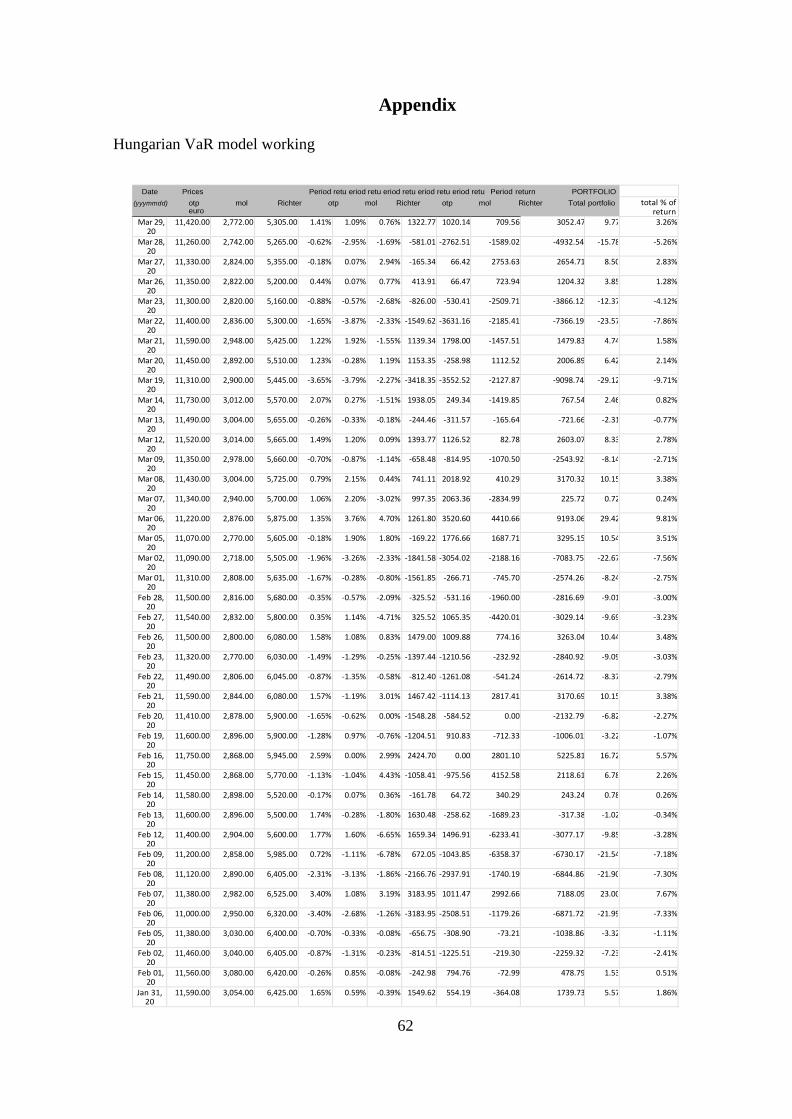

Appendix ............................................................................................................................. 62

Page 9

List of Figures

Figure 1. Listed domestic companies in India .................................................................... 22

Figure 2. Listed domestic companies in Hungary .............................................................. 22

Figure 3. Probability density versus portfolio value with 90% confidence in portfolio ..... 30

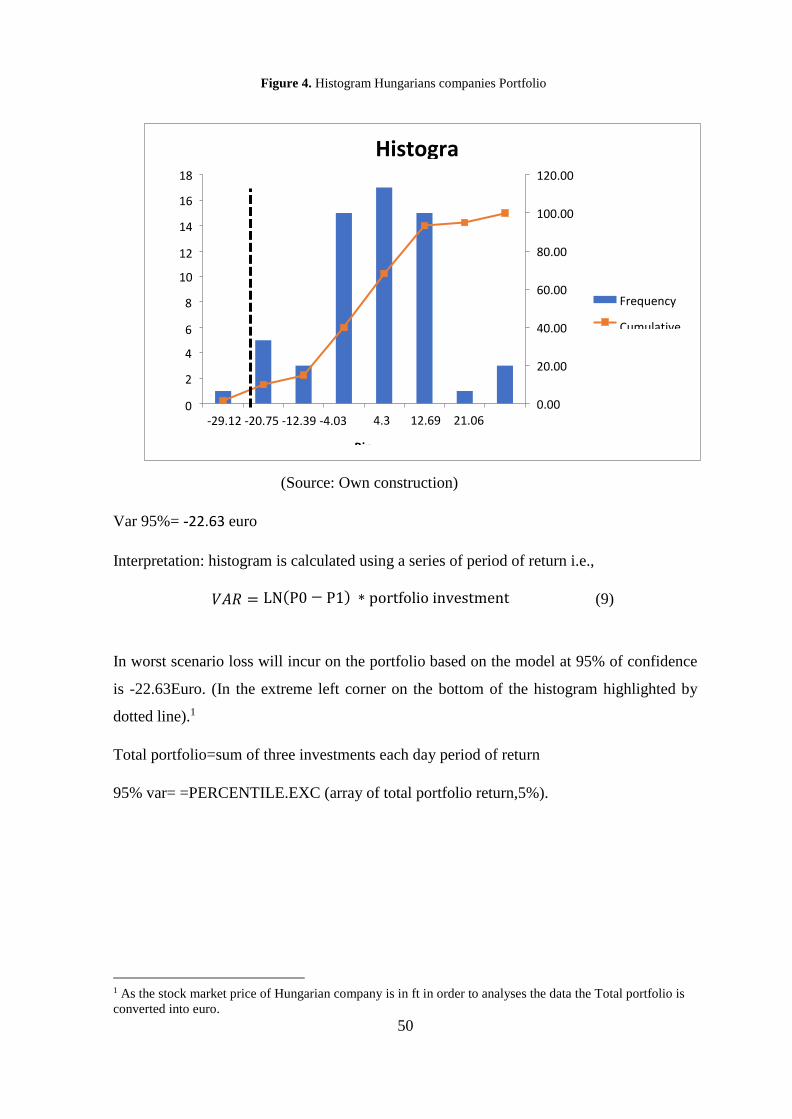

Figure 4. Histogram Hungarians companies Portfolio ...................................................... 50

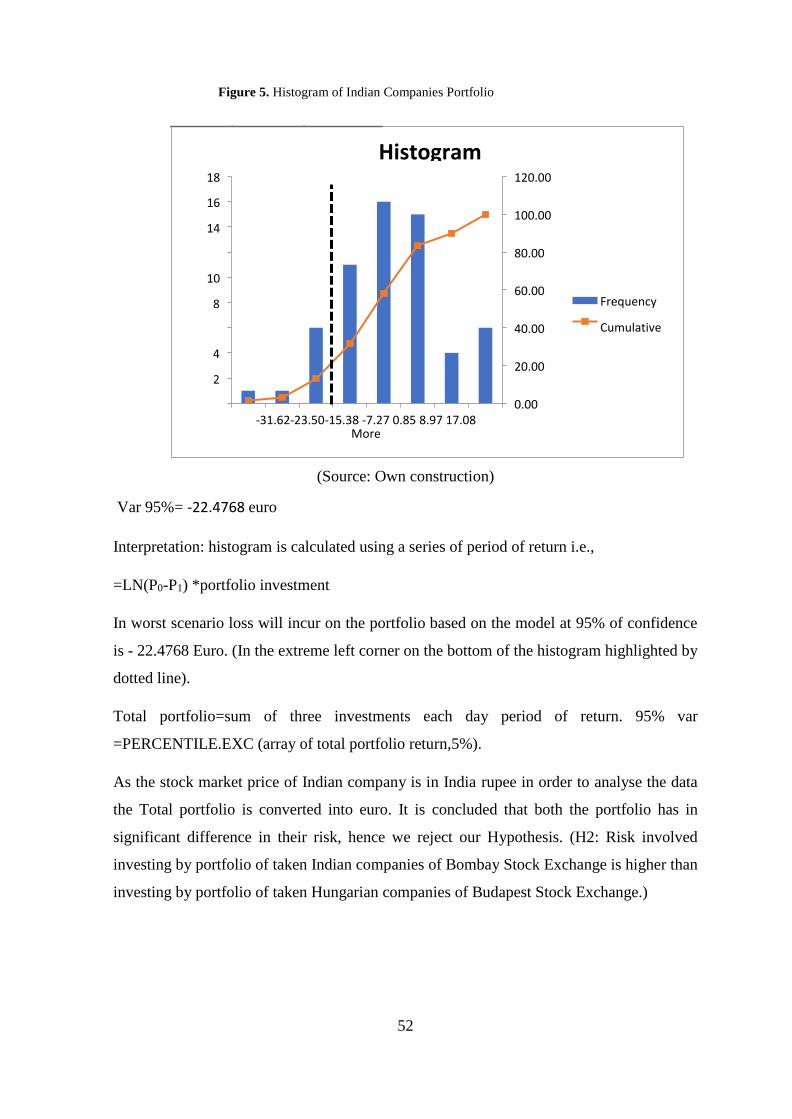

Figure 5. Histogram of Indian Companies Portfolio .......................................................... 52

Figure 6. Histogram of BUX ............................................................................................... 54

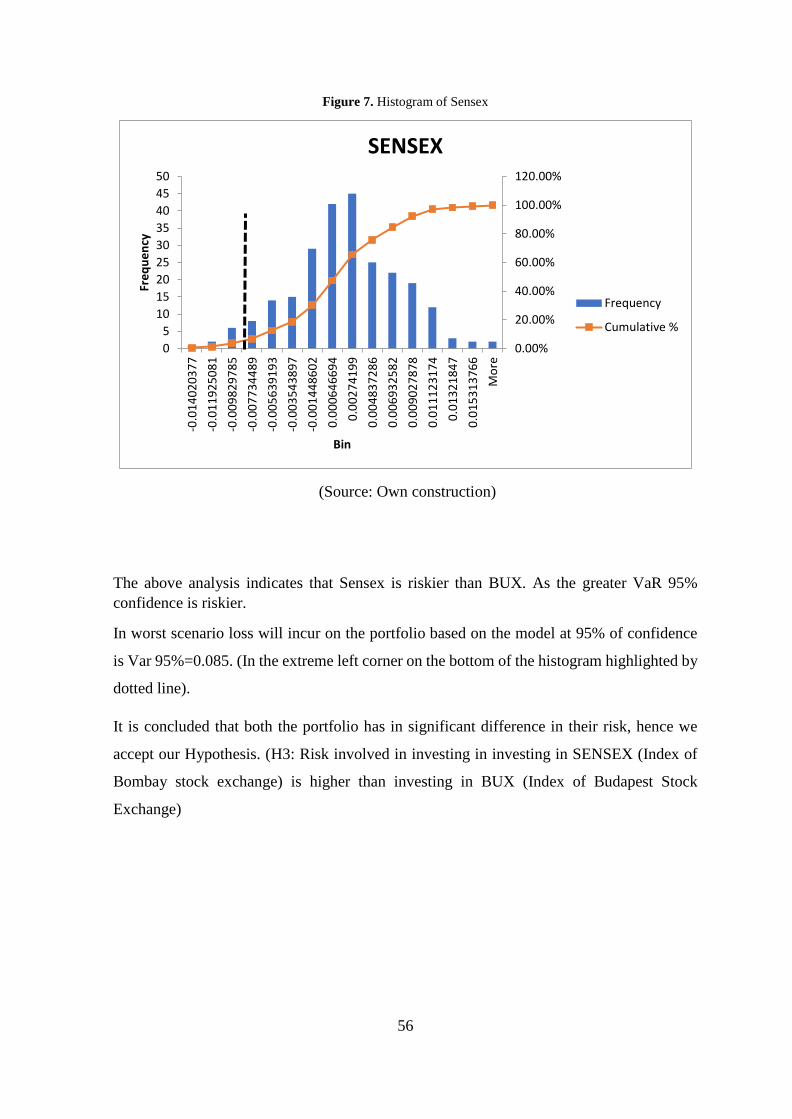

Figure 7. Histogram of Sensex ............................................................................................ 56

Page 10

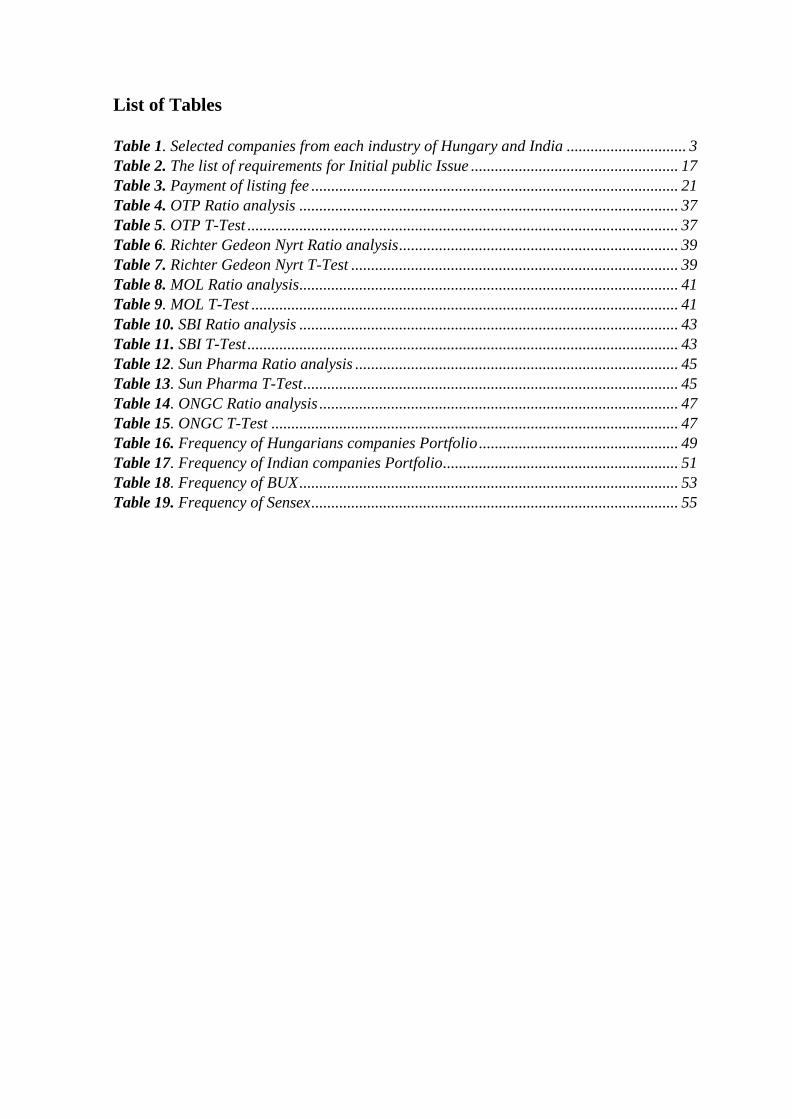

List of Tables

Table 1. Selected companies from each industry of Hungary and India .............................. 3

Table 2. The list of requirements for Initial public Issue .................................................... 17

Table 3. Payment of listing fee ............................................................................................ 21

Table 4. OTP Ratio analysis ............................................................................................... 37

Table 5. OTP T-Test ............................................................................................................ 37

Table 6. Richter Gedeon Nyrt Ratio analysis ...................................................................... 39

Table 7. Richter Gedeon Nyrt T-Test .................................................................................. 39

Table 8. MOL Ratio analysis ............................................................................................... 41

Table 9. MOL T-Test ........................................................................................................... 41

Table 10. SBI Ratio analysis ............................................................................................... 43

Table 11. SBI T-Test ............................................................................................................ 43

Table 12. Sun Pharma Ratio analysis ................................................................................. 45

Table 13. Sun Pharma T-Test .............................................................................................. 45

Table 14. ONGC Ratio analysis .......................................................................................... 47

Table 15. ONGC T-Test ...................................................................................................... 47

Table 16. Frequency of Hungarians companies Portfolio .................................................. 49

Table 17. Frequency of Indian companies Portfolio ........................................................... 51

Table 18. Frequency of BUX ............................................................................................... 53

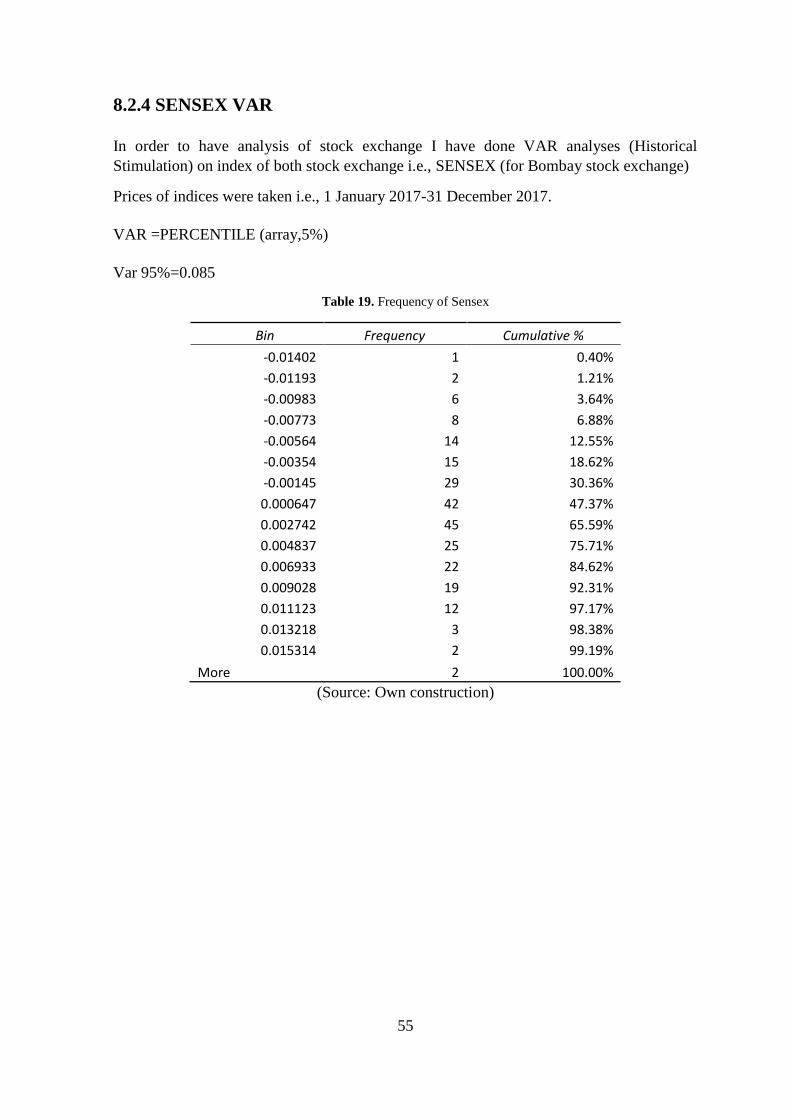

Table 19. Frequency of Sensex ............................................................................................ 55

Page 11

1

1. Introduction

Stock Market is a key indicator of the financial strength of the country’s economy. It is a

marketplace where different types of securities are being freely traded between the traders

or investors. Stock Exchange provides a great platform for purchasing and selling

securities, debt and derivatives with easy liquidity option. Nowadays, the stock market

has become very intense and is increasingly gaining importance in the economic growth

of a country.

It is not only important for the country’s economic growth but also the main sources of

finance for all the companies and allows them to publicly trade their shares or raise capital

or additional capital in case of expansion by selling shares of the company in an open

market. For some companies (especially the large companies) it is a more flexible way to

raise capital than borrowing from Banks. Stock Market is a reflector of the economic

condition of a country’s economy, if an economy is growing then the production of

outputs are increasing which increase the sale and profit of the companies which in turn

increases the tax paid by them to the government and also shoots up the GDP percentage.

Higher profit will also attract new investors in the market as investors are getting a high

interest in the shares. But it can also work in reversing way also, loss or less profit may

affect the share prices and can cause create disturbance in the stock market which can

create disturbance in the economic condition of the company. It helps in mobilizing the

resources in the economy.

Companies have to get listed on the stock market and sell their shares. This enables them

to gain finance to invest. In a free-market economy, stock market plays an important role

because it provides an easy access to the capital in exchange of giving up a certain

percentage of ownership. It acts as a bridge between the person who needs money and

have a new idea (Company) and those who have surplus money and want to invest and

earn interest (investors). It provides a platform for investors to grow their small amount

of money into large, without taking the risk of starting a business by themselves or leaving

their career to earn some extra money. Stock market gives a good interest on investment

if we compare with the returns given by the banks but the investment involves a certain

level of risk associated with it. Most of the countries have more than one major stock

exchanges. Example New York Stock Exchange (NYSE), National Association of

Securities Dealers Automated Quotations NASDAQ of America. National Stock

Page 12

2

Exchange of India and Bombay stock exchange of India. The stock market is an example

of perfect competition market as it provides all the information is readily available to the

investor and prospective investor as most countries promote transparency when it comes

to the stock market as it is the one the main component for an economy the stock exchange

of countries is free from control of the government. But have to work according to rules

and regulations of that countries. Each country has its own set of laws that help in smooth

functioning of the stock exchange and provide protection to the investors. Due to an

increase e of a number of scams in the stock market, it is important to have some

regulatory bodies in order to stabilize the confidence of the investors. In order to avoid

scams and attract investors Government of each country came up with their rules and law

which help in governing the stock market easily. These laws are made to have a more

transparent view of stock exchange.

With the globalization, accessing the international market became easier. Now not only

local investors have their investment in the market but also the international traders are

involved. International traders are mostly interested in investing the developing Economy

as it provides a great return on their investments. Globalization affected all spheres- stock

market was also one among them. It gave rise to the integration of financial market.

Globalization had made foreign investment in stock market much easier. Because of

transparency in this business, the investment in stocks are not limited to the local market,

many investors are investing in different countries stock by Global depository receipt etc.

In the market there are numerous of company listed on exchanges. In order to determine

the size of the company analysing the share prices are not enough, Market Capitalization

is the one of the common techniques to determine the size. In recent years Market

capitalization have become an important indicator in order to evaluate the companies in

the stock market. Market capitalization is the total dollar value of all outstanding shares

of a company. It is calculated by multiplying the current share price by the number of

outstanding shares. Outstanding Shares are all the shares which are currently owned by

stockholders, company officials, and investors in the public domain. Usually analyst use

the figure to determine the size and the position of the company. Since it is calculated

with the help of share price which is not stable so, the market capitalization can also

fluctuate on daily basis.

Page 13

3

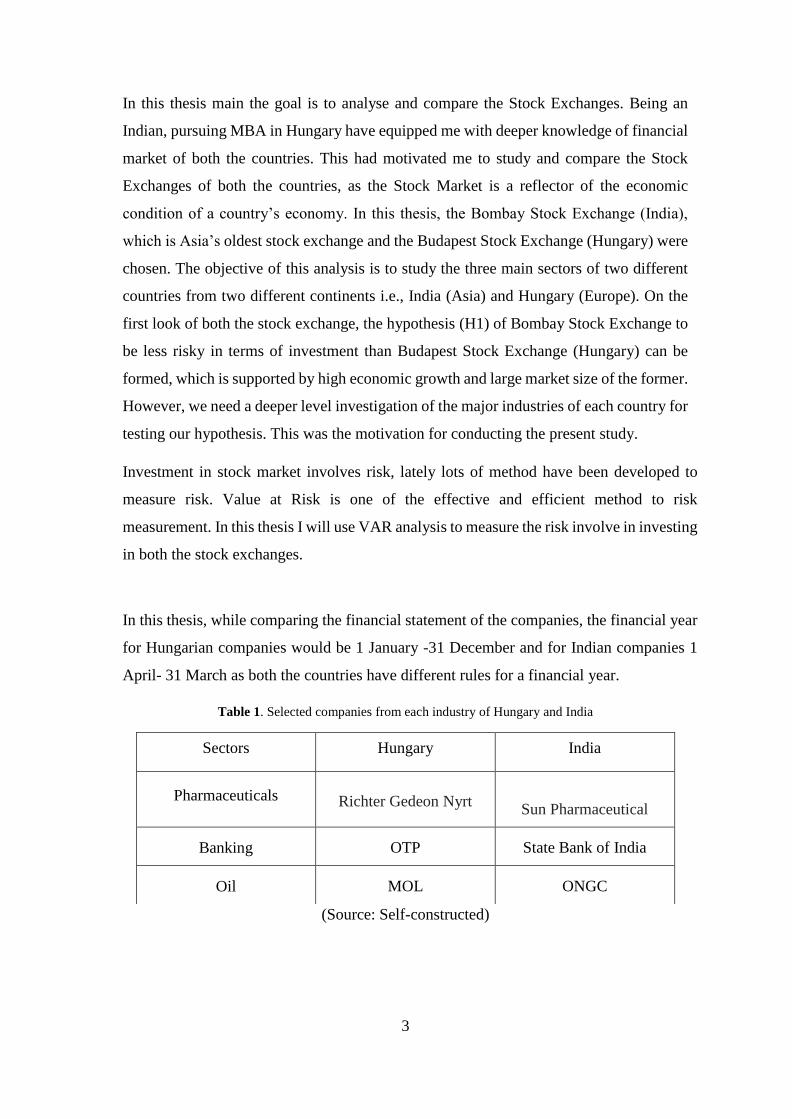

In this thesis main the goal is to analyse and compare the Stock Exchanges. Being an

Indian, pursuing MBA in Hungary have equipped me with deeper knowledge of financial

market of both the countries. This had motivated me to study and compare the Stock

Exchanges of both the countries, as the Stock Market is a reflector of the economic

condition of a country’s economy. In this thesis, the Bombay Stock Exchange (India),

which is Asia’s oldest stock exchange and the Budapest Stock Exchange (Hungary) were

chosen. The objective of this analysis is to study the three main sectors of two different

countries from two different continents i.e., India (Asia) and Hungary (Europe). On the

first look of both the stock exchange, the hypothesis (H1) of Bombay Stock Exchange to

be less risky in terms of investment than Budapest Stock Exchange (Hungary) can be

formed, which is supported by high economic growth and large market size of the former.

However, we need a deeper level investigation of the major industries of each country for

testing our hypothesis. This was the motivation for conducting the present study.

Investment in stock market involves risk, lately lots of method have been developed to

measure risk. Value at Risk is one of the effective and efficient method to risk

measurement. In this thesis I will use VAR analysis to measure the risk involve in investing

in both the stock exchanges.

In this thesis, while comparing the financial statement of the companies, the financial year

for Hungarian companies would be 1 January -31 December and for Indian companies 1

April- 31 March as both the countries have different rules for a financial year.

Table 1. Selected companies from each industry of Hungary and India

(Source: Self-constructed)

Sectors Hungary India

Pharmaceuticals Richter Gedeon Nyrt

Sun Pharmaceutical

Banking OTP State Bank of India

Oil MOL ONGC

Page 14

4

Pharmaceuticals, Banking and Oil Company are the main sectors of both the countries. The

choose companies are one of the leading players in the economy and have a good financial

position which is been proved by bench mark analysis.

In this thesis I will try to formulate the relationship between chosen firm’s financial

performance, market price and risk involved in investing. Due to globalization accessing to

worldwide market became easy, now investors have lots of option to invest not in local

market but also in different countries. To make correct decision in-depth analysis is

important. In this thesis I took two developing countries situated in different continents (Asia

and Europe). I will analyse the historical price movement of the selected companies and

stock exchange with their financial performance.

Page 15

5

2. Objectives

• To have a comparative analysis of both stock exchanges

• To study the fluctuations in share prices of selected companies

• Effect of the stock exchange on the economy of both Countries.

• Analysis of financial position of the company using ratio analysis and the risk involves

the stocks of taken companies with the help of a model.

• To understand the correlation between the stock prices and financial performances.

• To find out investing in which country is more risker and profitable by using historical

data and analysing it.

Page 16

6

3. Limitations of the study

• The topic has a broad nature which is a limitation.

• The study is based only on secondary data.

• Time is a major constraint for a detailed study.

• Two countries follow different financial years.

Page 17

7

4. Hypotheses

➢ H1: There is significant relationship between taken companies financial ratios and

their stock market price.

➢ H2: Risk involved investing by portfolio of taken Indian companies of Bombay

Stock Exchange is higher than investing by portfolio of taken Hungarian companies

of Budapest Stock Exchange.

➢ H3: Risk involved in investing in investing in SENSEX (Index of Bombay stock

exchange) is higher than investing in BUX (Index of Budapest Stock Exchange).

Page 18

8

5. Methodology

To have an in-depth study of both the countries, I have chosen 3 companies from each

country. In this thesis two methods are being used:

1. Value at Risk - As share market is uncertain and VAR model is one of the models

which help in calculating the risk. In this thesis, I have compared the risk involved

in the shares of the chosen company.

2. Benchmark model - Financial position of the company has a strong influence on

the stock prices of the company. In order to have some pictures of the company’s

financial statements in this thesis I have done ratio analysis and compare the ratios

with the benchmark ratios.

3. Excel - (Software) Data is analyse using statistical formulas and processed to get

the results.

Page 19

9

6. Literature Review

The stock exchange has become a major source of earning and it is a market which is

difficult to predict. Many studies are done on the stock market. With the globalization of

capital markets, stock exchanges around the world have faced their most challenging era

since 2005. While the traditional role of the stock exchange should evolve by enforcing

competitive advantage, as the heart of modern capital markets, stock exchanges give rise

to both capital demand outflows and capital supply inflows, and both must be taken into

consideration. Since 2005, the competition among the world's stock exchanges has rapidly

increased. To secure their competitive positions, the traditional role of the stock exchange

needs to change quickly through the enforcement of competitive advantage. (Lo, 2013)

According to a researcher, there is a link between economic variables with growth are

extremely significant. These indicators are either quantitative or qualitative. The active-

features are stock market size in terms of market capitalisation ratio, having positive

significance correlated with real per capita GDP, market liquidity and activity in terms of

value traded, turnover, and further having a positive sign with growth, namely that market

volatility has negatively and insignificantly correlated with real per capita GDP growth.

(Masoud, 2003) Stock market volatility modelling and estimation have established certain

issues of great interest not only for investors, financial practitioners and academics,

especially in terms of modern finance perspectives. Moreover, one of the main aims of the

investment process is to reduce the high exposure to risk considering the fact that

international portfolio diversification provides superior risk-adjusted returns. (Ramona

Birăua, 2015).

The study of (Prasad, 2015) focused on the effect of profitability and market value ratios

on market. In this study 23 listed infrastructural companies of CNX infrastructure Index

has been taken for analysis. The main finding is market capitalization and firm performance

that the influence of various variables such as return on equity (ROE), P/E ratio, return on

asset (ROA), profitability etc. over market capitalization has been undertaking

independently.

This study of (Dr. Mohammad Abdelkarim Yousef Almumani, April 2018) aims to

investigate the effect of profitability ratios and market value ratios on the market

capitalization for Jordanian listed commercial banks. In this study data of 2010-2016 was

used from the Amman stock exchange archives. Thus, the study draws out a relationship

Page 20

10

of market capitalization with five other variables namely ROE, ROA, EPS, PER and DPR.

The finding of study is that return on equity and dividend pay-out ratio are the major

determinants of market capitalization of the listed commercial banks in Jordan.

The study of (MacKenzie, 2015)focus on the risk indices are used to communicate risks to

the public, understand how risk is changing over time, compare among different risks, and

support decision making. This paper focus on the importance of describing risk with a

probability distribution, developing a numerical risk measure that summarizes the

probability distribution, and finally translating the risk measure to an index.

The study of (Li*, 2015) focus on VaR model is mainly suitable for measuring market risk,

and not a measure of credit risk. It is because of existing financial risk measure is not perfect,

it is worth our financial institutions to learn it and study it. The study emphasis on studied

theories, methods and technical standards of China's financial risk management, in order to

enhance the competitiveness level of our financial institutions.

The study (Vinay Kaura) focused on historical prices to create future scenarios one can

determine the “Value-At Risk” of a specified portfolio using back testing, this report

demonstrates how the developed model would have, hypothetically, been able to make

profits of up to 40% over the course of the past year while the FTSE 100 benchmark rose by

only 27%.

According to Mussalam earnings yield ratio, and dividend yield ratio enhance market stock

returns while other ratios do not effect on market stock returns in Qatar. (MUSALLAM,

2018)

In study market-to-book ratio, dividend yield and firm size have significant positive

relationship with stock returns, while price-to-sales ratio and earnings per share are

insignificant and negative relationship with the stock returns. (LAI Ping-fu (Brian), 2016)

According the study there are relationships between the financial ratios which is valuable

information to the stock investors. (Meri, Kamışlı', & Temizel, November 2017)

The article emphasizes that the market fluctuations relations to the prices, due to price

movements it is difficult to observe the pattern, it is observed that the financial position and

performance of the firms are in correlation with present market prices. (GAUTAMI &

KALYAN, 2018)

Page 21

11

The researcher did an analysis on a sample of 46 firms to show the value relevance of the

financial ratios and their usefulness in security valuation in Egypt. They used three models

to test for linear and non-linear relationships and Concluded that ROE seems to play a

significant role in investment decisions in the Egyptian market (Omran & Ragab, 2004)

Page 22

12

7. Theoretical Background

7.1 Hungarian Economy

Hungary is one of the Central and Eastern European countries. The total land area is 90,530

Km2 with approx. 10 million population. Despite being in European Union Hungarian

government have retained its own Currency which Hungarian forint (HUF). Average market

value of 1 Euro=310 ft

Hungary became member of European Union in since 1 May 2004.

Hungary is the democratic country. From 2016 Hungary becomes an attractive country for

tourism and employment. Hungarian Government decided to adopt Privatization policy in

1990 because of Hungarian foreign debt got so much increased that the government decide

to sell some part of state property instead of being in debt. During the early nineties, century

lot of government decided to take this step. External Debt in Hungary increased to 105322.07

EUR Million in the second quarter of 2018 from 103657.39 EUR Million in the first quarter

of 2018 (Economics .T, 2019)

In 20th century The Hungarian economy have been open to the world for trade. Hungarian

economy went through a deep transformational and structural crisis during the transition,

and it resulted in a modern national economy, ready for the

Integration into the European Union. This came together with mainly necessary sacrifices

that the society, the majority of the people had to suffer, but in the same time these sacrifices

created the long-run conditions for catching up. Among others the catching up.

The volume of gross domestic product was 4.2% higher in Hungary in the 1st quarter of

2017 than in the corresponding period of the previous year. The primary contributors to the

growth were market-based services and industry. (ksh, 2019)

After privatization lot of new companies came into the market which gave a boost to the

economy and increases competition. In 1994 government decided to enter join European

Union. European Union main motto is to ensure free movement of people and trade. It helps

the Hungarian market to import goods and technology from other EU member countries

easily, moreover, the union also provide economic support to Hungarian

In 2004 Hungary became the tenth country to join the union.

Hungary was one of those countries which was affected by the 2008 global crises -6.4% was

the recession which affected the economy and it took a lot of time to recover from this loss.

Page 23

13

The monetary policy decision of the country is taken by Hungarian National Bank

(Hungarian: Magyar Nemzeti Bank, MNB) which is the central bank in Hungary whose

prime objective is price stability.

“According to IMF Gross domestic product, current prices of Hungary in 2017 was USD

125.297 Billion And for 2018 USD130.376 Billions. According to recent data, Hungary’s

real GDP growth in the first quarter was 4.2% higher than the previous year GDP. The main

driver of this growth is due to service and industrial contribution to the economy. This year

the economic performance was also improved by 3.8% if we compare data with the previous

year. The value added of agriculture decreased by 6.3%.” (ksh, 2019)

Page 24

14

7.2 Indian Economy

Indian economy is the developing mixed Economy. India is situated in Asia Continent. It is

the world's sixth- largest economy by nominal GDP and the third-largest by purchasing

power parity (PPP) Seven largest Country by area. The Indian currency is Indian Rupee

(INR) ₹. 1 Euro is equal 80 INR. According to IMF India is one of the fastest growing

countries in the world.

The main sectors of Indian economy are agriculture, handicrafts, industries, and services.

With the technological and economic growth service sector became the important part of the

economy especially the Information and technology. India is considered as the main service

provider for information and technology many companies have outsourced their IT services

from India and Banking and Financial services have 37% of GDP share. Services are the

main source of economic growth in India today, though two-thirds of Indian people earn

their living directly or indirectly through agriculture. Industry accounts for 26% of GDP and

Agriculture accounted for 23% of GDP (BENCHMARKING, 2017)

India was always an agriculturally based country because of its climate and land fertility.

India exported $256B, making it the 18th largest exporter in the world. Major exported good

are Crude oil, Gold, Jute. India imported $344B, making it the 14th largest importer in the

world which is increased by 33.9% since 2009. (OEC, 2017) In 1991 Indian government

decided to adopt Liberalization and privatization policy. As India was dealing a huge

financial crisis mainly due to Balance of payment deficit in order to cover deficit government

applied for a loan from IMF who asked India to adopt liberalization policy. Before 1991 for

most of the business acquired, the license was mandatory. But after 1991 licensing policy

was removed from most of the business. This economic change proved beneficial for the

economy as it helps in economic growth and technological growth of the country.

India is a democratic country where the government have very less influence on the market.

Reserve Bank of India (RBI) is the central bank who is responsible for making monetary

policy. RBI is free from any governmental interference. According to UNCTAD’s World

Investment Report 2015, India ranks third among most prospective host economy for 2015-

17 (after China and the US) in the world. Foreign direct investment (FDI) is one of the major

sources of non-debt financial resource for the Indian economy. Foreign companies are

attracted to invest because of relatively lower wages and availability of human resources

(both skilled and unskilled), tax exemptions, for the new companies and investment etc. FDI

Page 25

15

not only increases capital flow in the country but also help in technological growth and give

rise to the level of employment in the country. In 2017 India has 7.2% GDP rate According

to IMF the GDP will rise further to 7.8% in 2019.

In 2016, the Indian government decided to demonetize its 500- and 1000- rupee notes, which

is the two biggest currency notes in India. The government replaced the 500rupee notes with

a new note and removed 1000 rupee note from the economy and issued a new 2000rupee

note. This change was made in overnight and time period of exchanging the currency was

very short. The government took this step-in order to remove fake currency and black money

(untaxed amount) in circulation. This was an unexpected move by the government which

impacted the stock market as a number of investors left the market and some left due to lack

of funds and other withdraw as they were expecting fall in the market. It took some time for

the exchange to come back to normal place. The government tax collection was also

increased to the demonetization.

In 2017 Indian economy faced another major change in the form of new tax reform the

government introduces new indirect tax i.e., Goods and service tax and replaced some of its

old indirect tax which also created some disturbance in the economic system of the country.

This increases the government revenue from taxation. The major reform done by the new

government had increased the personal tax collection to 2.3% of GDP

Page 26

16

7.3 Stock Exchange

Stock exchanges are indispensable for the smooth and orderly functioning of the corporate

sector in a free market economy. The main function of the stock market is to provide a ready

market for sale and purchase of securities. The presence of stock exchange market gives

assurance to investors that their investment can be converted into cash whenever they want.

The investors can invest in long-term investment projects without any hesitation, as because

of stock exchange they can convert a long-term investment into short term and medium term.

The stock market offers attractive opportunities for investment in various securities. These

attractive opportunities encourage people to save more and invest in securities of the

corporate sector rather than investing in unproductive assets such as gold, silver

Stock Exchange requires companies to follow some minimum standards operational or

capital structure for listing. It helps to maintain the quality of market and efficiency of the

market. Listing means an admission of securities to dealings on a recognized stock exchange.

Page 27

17

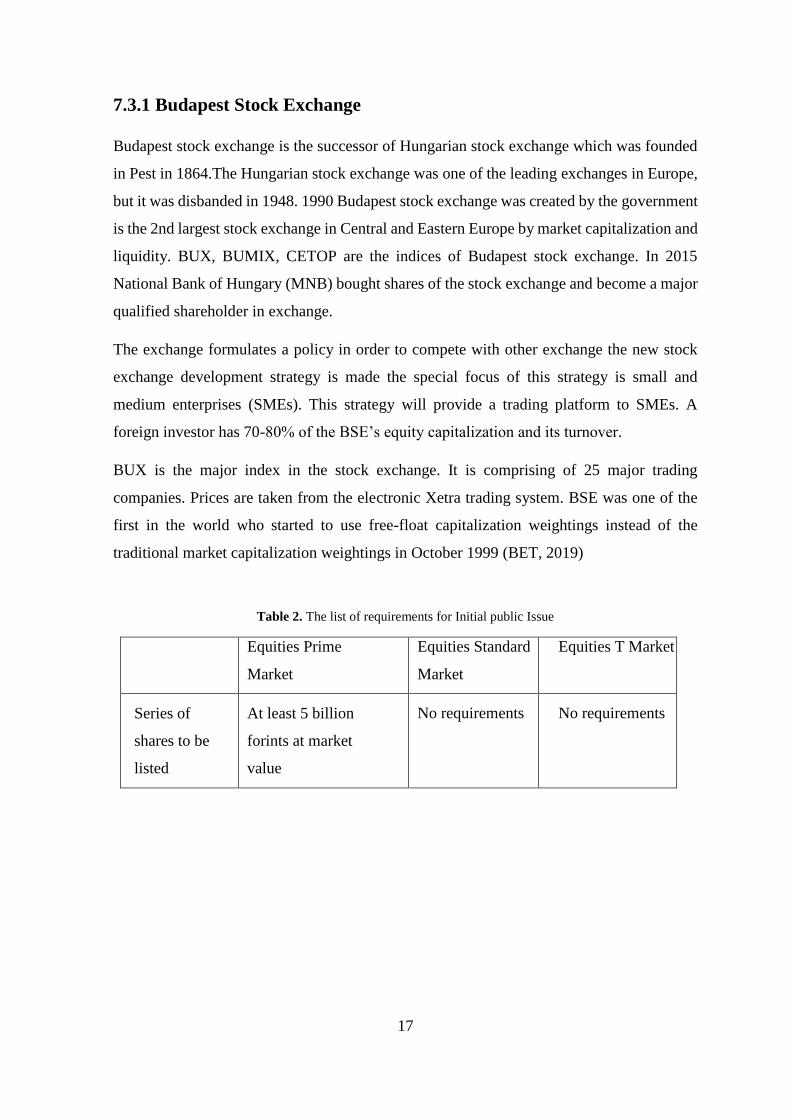

7.3.1 Budapest Stock Exchange

Budapest stock exchange is the successor of Hungarian stock exchange which was founded

in Pest in 1864.The Hungarian stock exchange was one of the leading exchanges in Europe,

but it was disbanded in 1948. 1990 Budapest stock exchange was created by the government

is the 2nd largest stock exchange in Central and Eastern Europe by market capitalization and

liquidity. BUX, BUMIX, CETOP are the indices of Budapest stock exchange. In 2015

National Bank of Hungary (MNB) bought shares of the stock exchange and become a major

qualified shareholder in exchange.

The exchange formulates a policy in order to compete with other exchange the new stock

exchange development strategy is made the special focus of this strategy is small and

medium enterprises (SMEs). This strategy will provide a trading platform to SMEs. A

foreign investor has 70-80% of the BSE’s equity capitalization and its turnover.

BUX is the major index in the stock exchange. It is comprising of 25 major trading

companies. Prices are taken from the electronic Xetra trading system. BSE was one of the

first in the world who started to use free-float capitalization weightings instead of the

traditional market capitalization weightings in October 1999 (BET, 2019)

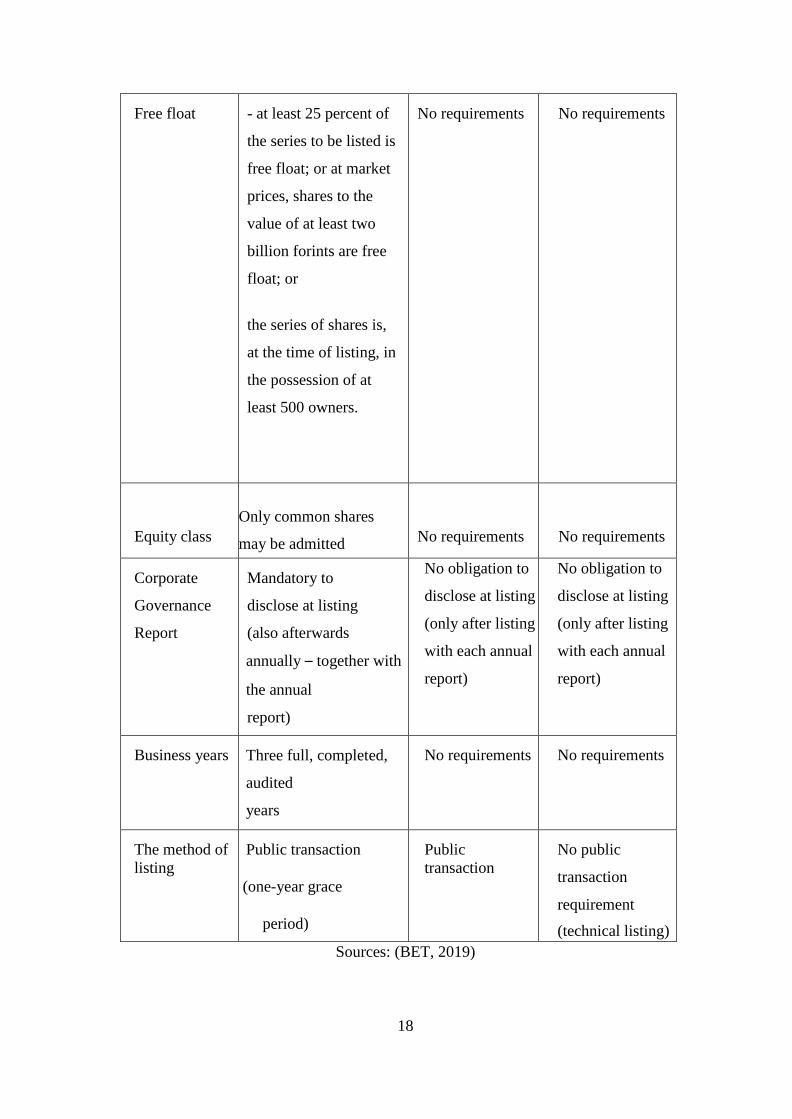

Table 2. The list of requirements for Initial public Issue

Equities Prime

Market

Equities Standard

Market

Equities T Market

Series of

shares to be

listed

At least 5 billion

forints at market

value

No requirements No requirements

Page 28

18

Free float - at least 25 percent of

the series to be listed is

free float; or at market

prices, shares to the

value of at least two

billion forints are free

float; or

the series of shares is,

at the time of listing, in

the possession of at

least 500 owners.

No requirements No requirements

Equity class

Only common shares

may be admitted

No requirements

No requirements

Corporate

Governance

Report

Mandatory to

disclose at listing

(also afterwards

annually – together with

the annual

report)

No obligation to

disclose at listing

(only after listing

with each annual

report)

No obligation to

disclose at listing

(only after listing

with each annual

report)

Business years Three full, completed,

audited

years

No requirements No requirements

The method of

listing

Public transaction

(one-year grace

period)

Public

transaction

No public

transaction

requirement

(technical listing)

Sources: (BET, 2019)

Page 29

19

The listing fee payable Issuers are not obliged to pay a fee for listing Equities and Other

Securities Issued. The Amount of the annual listing maintenance fee is based on

https://www.bse.hu/Issuers/Listing-on-the-BSE/Terms-of-Listing capitalization.

The Budapest Stock Exchange's Market Capitalization is $23.2 Billion, Market

Capitalization to GDP ratio, which when compared to the historic ratio is an indicator that a

market is over or undervalued, is 17.77% (BET, 2019)

Page 30

20

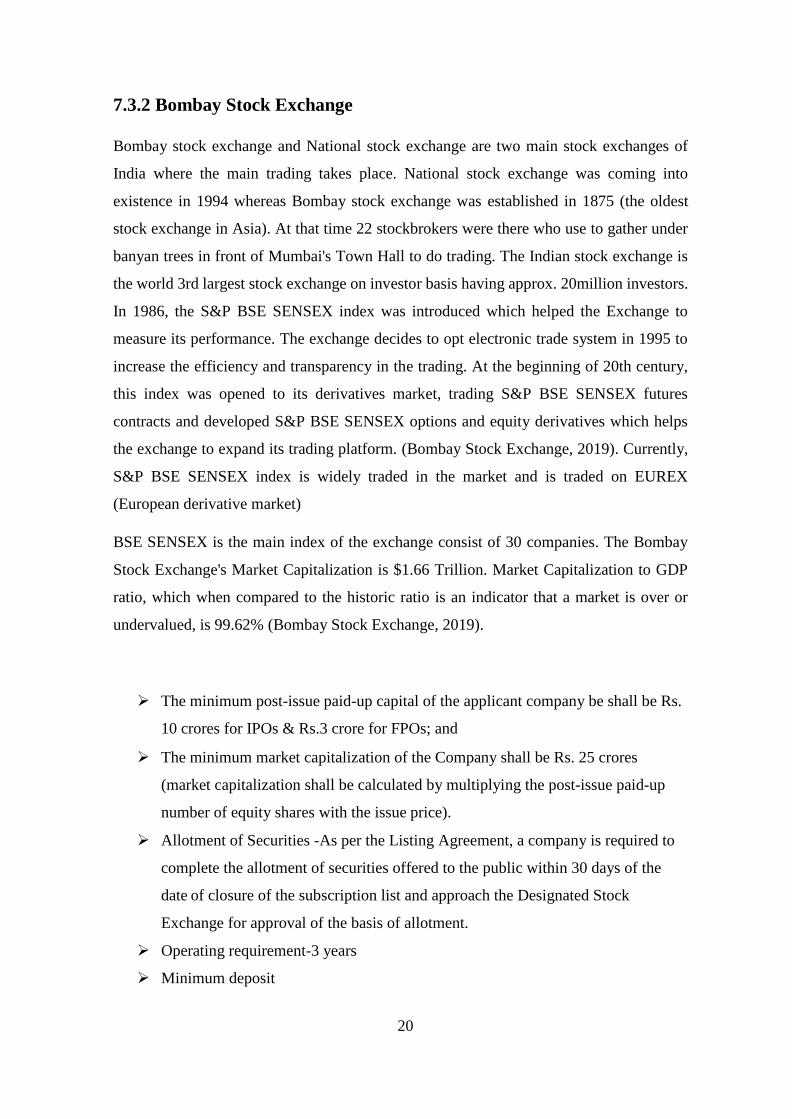

7.3.2 Bombay Stock Exchange

Bombay stock exchange and National stock exchange are two main stock exchanges of

India where the main trading takes place. National stock exchange was coming into

existence in 1994 whereas Bombay stock exchange was established in 1875 (the oldest

stock exchange in Asia). At that time 22 stockbrokers were there who use to gather under

banyan trees in front of Mumbai's Town Hall to do trading. The Indian stock exchange is

the world 3rd largest stock exchange on investor basis having approx. 20million investors.

In 1986, the S&P BSE SENSEX index was introduced which helped the Exchange to

measure its performance. The exchange decides to opt electronic trade system in 1995 to

increase the efficiency and transparency in the trading. At the beginning of 20th century,

this index was opened to its derivatives market, trading S&P BSE SENSEX futures

contracts and developed S&P BSE SENSEX options and equity derivatives which helps

the exchange to expand its trading platform. (Bombay Stock Exchange, 2019). Currently,

S&P BSE SENSEX index is widely traded in the market and is traded on EUREX

(European derivative market)

BSE SENSEX is the main index of the exchange consist of 30 companies. The Bombay

Stock Exchange's Market Capitalization is $1.66 Trillion. Market Capitalization to GDP

ratio, which when compared to the historic ratio is an indicator that a market is over or

undervalued, is 99.62% (Bombay Stock Exchange, 2019).

➢ The minimum post-issue paid-up capital of the applicant company be shall be Rs.

10 crores for IPOs & Rs.3 crore for FPOs; and

➢ The minimum market capitalization of the Company shall be Rs. 25 crores

(market capitalization shall be calculated by multiplying the post-issue paid-up

number of equity shares with the issue price).

➢ Allotment of Securities -As per the Listing Agreement, a company is required to

complete the allotment of securities offered to the public within 30 days of the

date of closure of the subscription list and approach the Designated Stock

Exchange for approval of the basis of allotment.

➢ Operating requirement-3 years

➢ Minimum deposit

Page 31

21

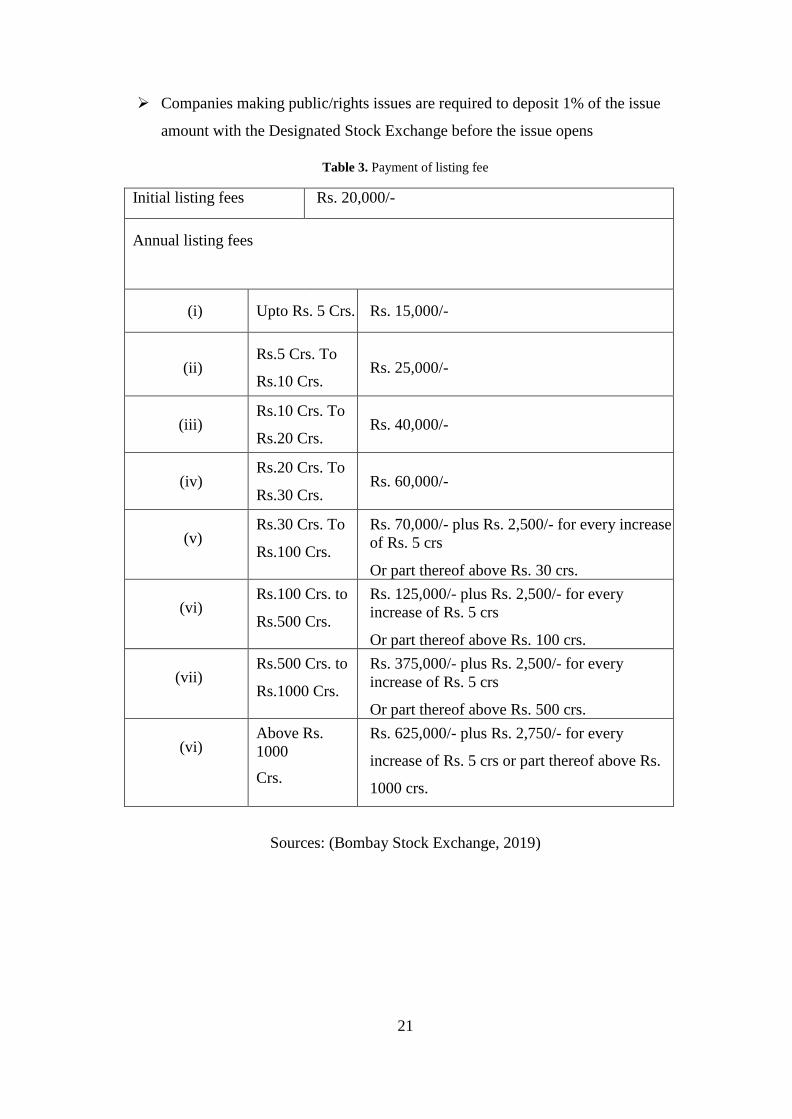

➢ Companies making public/rights issues are required to deposit 1% of the issue

amount with the Designated Stock Exchange before the issue opens

Table 3. Payment of listing fee

Initial listing fees Rs. 20,000/-

Annual listing fees

(i) Upto Rs. 5 Crs. Rs. 15,000/-

(ii)

Rs.5 Crs. To

Rs.10 Crs.

Rs. 25,000/-

(iii) Rs.10 Crs. To

Rs.20 Crs.

Rs. 40,000/-

(iv) Rs.20 Crs. To

Rs.30 Crs.

Rs. 60,000/-

(v) Rs.30 Crs. To

Rs.100 Crs.

Rs. 70,000/- plus Rs. 2,500/- for every increase

of Rs. 5 crs

Or part thereof above Rs. 30 crs.

(vi) Rs.100 Crs. to

Rs.500 Crs.

Rs. 125,000/- plus Rs. 2,500/- for every

increase of Rs. 5 crs

Or part thereof above Rs. 100 crs.

(vii) Rs.500 Crs. to

Rs.1000 Crs.

Rs. 375,000/- plus Rs. 2,500/- for every

increase of Rs. 5 crs

Or part thereof above Rs. 500 crs.

(vi) Above Rs.

1000

Crs.

Rs. 625,000/- plus Rs. 2,750/- for every

increase of Rs. 5 crs or part thereof above Rs.

1000 crs.

Sources: (Bombay Stock Exchange, 2019)

Page 32

22

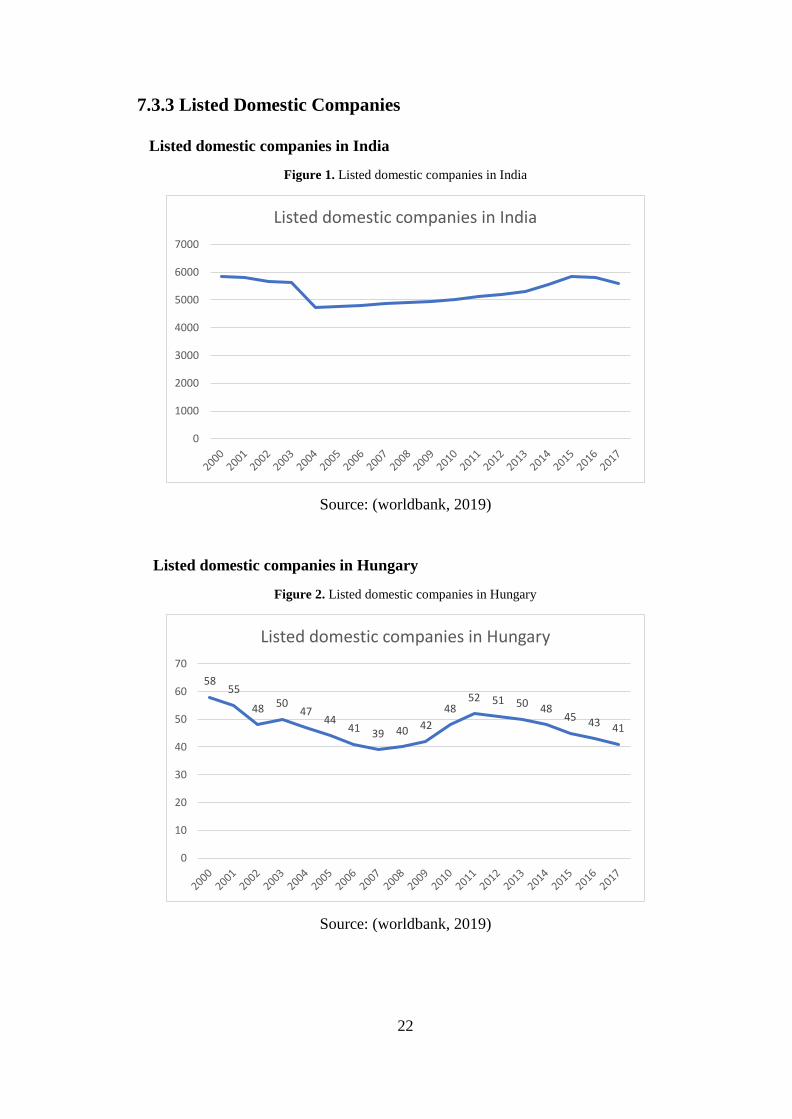

7.3.3 Listed Domestic Companies

Listed domestic companies in India

Figure 1. Listed domestic companies in India

Source: (worldbank, 2019)

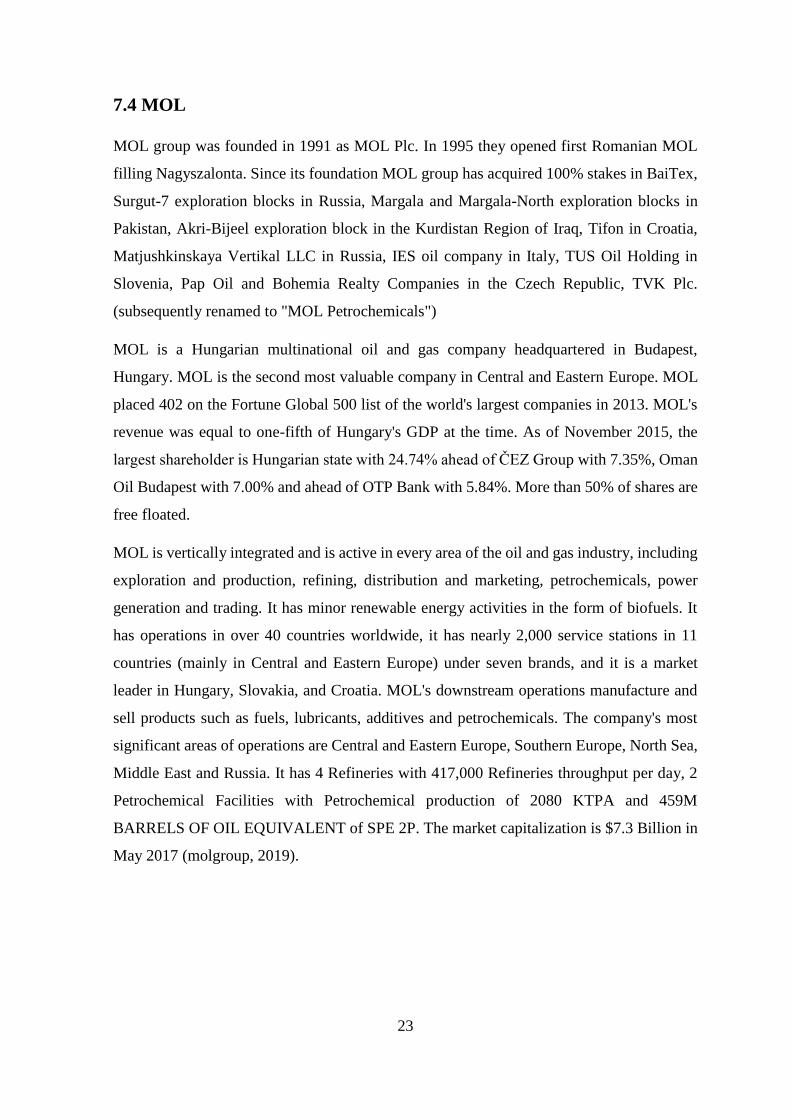

Listed domestic companies in Hungary

Figure 2. Listed domestic companies in Hungary

Source: (worldbank, 2019)

0

1000

2000

3000

4000

5000

6000

7000

Listed domestic companies in India

5855

48 5047

4441 39 40 42

4852 51 50 48

45 43 41

0

10

20

30

40

50

60

70

Listed domestic companies in Hungary

Page 33

23

7.4 MOL

MOL group was founded in 1991 as MOL Plc. In 1995 they opened first Romanian MOL

filling Nagyszalonta. Since its foundation MOL group has acquired 100% stakes in BaiTex,

Surgut-7 exploration blocks in Russia, Margala and Margala-North exploration blocks in

Pakistan, Akri-Bijeel exploration block in the Kurdistan Region of Iraq, Tifon in Croatia,

Matjushkinskaya Vertikal LLC in Russia, IES oil company in Italy, TUS Oil Holding in

Slovenia, Pap Oil and Bohemia Realty Companies in the Czech Republic, TVK Plc.

(subsequently renamed to "MOL Petrochemicals")

MOL is a Hungarian multinational oil and gas company headquartered in Budapest,

Hungary. MOL is the second most valuable company in Central and Eastern Europe. MOL

placed 402 on the Fortune Global 500 list of the world's largest companies in 2013. MOL's

revenue was equal to one-fifth of Hungary's GDP at the time. As of November 2015, the

largest shareholder is Hungarian state with 24.74% ahead of ČEZ Group with 7.35%, Oman

Oil Budapest with 7.00% and ahead of OTP Bank with 5.84%. More than 50% of shares are

free floated.

MOL is vertically integrated and is active in every area of the oil and gas industry, including

exploration and production, refining, distribution and marketing, petrochemicals, power

generation and trading. It has minor renewable energy activities in the form of biofuels. It

has operations in over 40 countries worldwide, it has nearly 2,000 service stations in 11

countries (mainly in Central and Eastern Europe) under seven brands, and it is a market

leader in Hungary, Slovakia, and Croatia. MOL's downstream operations manufacture and

sell products such as fuels, lubricants, additives and petrochemicals. The company's most

significant areas of operations are Central and Eastern Europe, Southern Europe, North Sea,

Middle East and Russia. It has 4 Refineries with 417,000 Refineries throughput per day, 2

Petrochemical Facilities with Petrochemical production of 2080 KTPA and 459M

BARRELS OF OIL EQUIVALENT of SPE 2P. The market capitalization is $7.3 Billion in

May 2017 (molgroup, 2019).

Page 34

24

7.5 Oil and Natural Gas Corporation Ltd

Oil and Natural Gas Corporation Ltd. (ONGC) is an India oil company a Navaratna public

sector enterprise engaged in the exploration of hydrocarbons is one of the leading companies

with significant contribution in its industrial and economic growth over the years ONGC has

been fairly successful in building up a vibrant oil industry in the country. The Oil and Natural

directorate were formed in the year 1952 as part of Department of Geological Survey of

India (GSI) to undertake the task of exploration of crude oil in the country. The directorate

was transformed into commission in the year 1956 thenceforth it was known as Oil and

Natural Gas Commission till recently in the year 1993 when it converted into a public limited

company and is known as Oil and Natural Gas Corporation Limited. The various products

of ONGC are Crude Oil, NGL (Natural Gasoline), LPG (Liquefied Petroleum Gas), Ethane-

Propane, Natural Gas.

Maharatna ONGC is the largest producer of crude oil and natural gas in India, contributing

around 70 percent of Indian domestic production.

It is one of the most valued public enterprises in India, and one of the highest profit-making

and dividend-paying. ONGC has a unique distinction of being a company with in-house

service capabilities in all areas of Exploration and Production of oil & gas and related oilfield

services. Winner of the Best Employer award, a dedicated team of over 33,927 professionals’

toils round the clock in challenging locations.

Its wholly-owned subsidiary ONGC Videsh Limited (OVL) is the biggest Indian

multinational in the energy space, participating in 36 oil and gas properties in 17 countries.

ONGC subsidiary Mangalore Refinery and Petrochemicals Limited.

ONGC is one of the most valuable corporations trading on Indian stock exchanges. With a

current approximate share price of around INR 250 per share and 8555.60 million equity

share base, the market valuation of ONGC is INR 2,138,900 million. Its market

capitalization is 231,960.73 (Oil and Natural Gas Corporation Limited, 2019).

Page 35

25

7.6 OTP BANK

OTP Bank Group is one of the largest independent financial services providers in Central

and Eastern Europe with a full range of banking services for private individuals and

corporate clients. OTP Group comprises large subsidiaries, granting services in the field of

insurance, real estate, factoring, leasing and asset management, investment and pension

funds. The bank is serving clients in 9 countries, namely Hungary, Slovakia, Bulgaria,

Serbia, Romania, Croatia, Ukraine, Montenegro and Russia.

OTP Group provides its universal financial services through several subsidiaries. In

Hungary, traditional banking operations are performed by the Bank while specialized

services, including car leasing, investment funds are developed and offered by the Bank's

subsidiaries. Insurance claims of OTP Group clients are supplied by sales of insurance

products with strategic collaboration with French insurance company, Groupama, after its

OTP Garancia aqutision. The predecessor of OTP Bank called the National Savings Bank

(OTP Bank) was established in 1949 as a nationwide, state-owned, banking entity providing

retail deposits and loans. In the ensuing years, its activities and the scope of its authority

gradually widened.

Nowadays OTP Groups' more than 38,000 employees are serving 13 million clients in over

1,500 branches and through electronic channels on all the markets of the bank. OTP is still

the largest commercial bank in Hungary with over 25% market share. OTP Group started its

activity in 1949 when OTP Bank was founded as state savings and commercial bank. OTP

stands for Országos Takarék Pénztár (National Savings Bank) which indicates the original

purpose of establishment of the bank. The bank went public in 1995, and the share of the

state in the bank capital decreased to one preferential gold share, which also eliminated

shortly thereafter. Currently, most of the banks' shares are owned by private and institutional

investors.OTP has a high free float shareholder structure; the free float ratio reaches the

68.61%. The rest is held by one of the Forbes billionaire Megdet Rahimkulov in 8.88%,

Hungarian MOL Group in 8.57%, French Groupama in 8.30% and American Lazard in

5.64%. The market cap of otp as on May 2017 was $7.9 Billion (OTP, 2019).

Page 36

26

7.7 State Bank of India

State Bank of India (SBI) is an Indian multinational, public sector banking and financial

services company. It is a government-owned corporation with its headquarters in Mumbai,

Maharashtra. State Bank of India (SBI), with a 200-year history, is the largest commercial

bank in India in terms of assets, deposits, profits, branches, customers and employees. The

Government of India is the single largest shareholder of this Fortune 500 entity with 61.58%

ownership. SBI is ranked 60th in the list of Top 1000 Banks in the world by "The Banker"

in July 2012.

The SBI group consists of SBI and five associate banks. The group has an extensive network,

with over 20000 plus branches in India and another 173 offices in 34 countries across the

world.

As of 31st March 2012, the group had assets worth USD 359 billion, deposits of USD 278

billion and capital & reserves in excess of USD 20.88 billion. The group commands over

22% share of the domestic Indian banking market. SBI’s non- banking subsidiaries/joint

ventures are market leaders in their respective areas and provide wide-ranging services,

which include life insurance, merchant banking, mutual funds, credit cards, factoring

services, security trading and primary dealership, making the SBI Group a truly large

financial supermarket and India’s financial icon. SBI has arrangements with over 1500

various international/local banks to exchange financial messages through SWIFT in all

business centres of the world to facilitate trade related banking business, reinforced by

dedicated and highly skilled teams of professionals. (Linda, 2019)

In April market cap of SBI Rs 2,35,307.51 crore. On April 1, 2017, the State Bank of India,

India's largest bank, merged with five of its associate banks (State Bank of Bikaner & Jaipur,

State Bank of Hyderabad, State Bank of Mysore, State Bank of Patiala and State Bank of

Travancore), and with the Bhartiya Mahila Bank. This merger was the first largest

consolidation in the Indian banking industry.

Page 37

27

7.8 Richter Gedeon Nyrt

Richter Group is active in two major business segments, primarily Pharmaceuticals

comprising the research and development, manufacturing, sales and marketing of

pharmaceutical products, and it is also engaged in the Wholesale and Retail of these

products. In addition, there is a third group (’Other’) of companies comprising those

members of the Group that provide auxiliary services to the former segments. Research,

development, manufacturing and marketing of pharmaceutical products are the core

activities of Richter and in this endeavour, the Group is supported by a number of

subsidiaries, joint ventures and associated companies. Manufacturing subsidiaries of the

Group which operate in traditional markets together with a broad network of trading

affiliates that ensure a strong market presence have together created the foundation for

regional leadership and a global presence in the area of Women’s Healthcare (Richter, 2019).

Richter Gedeon Nyrt is a Hungarian company registered under Budapest stock exchange.

The total number of shares in issue at 186,374,860 as of 31 December 2016 which is as same

as in last year. The Company is following corporate governance Corporate Governance

according to guidelines set by the Budapest Stock Exchange and the directives of the capital

market.

Gedeon Richter’s key principles of Corporate Governance are to create and maintain

satisfactory shareholders so as to enhance shareholder value, to differentiate the roles and

responsibilities of the Board of Directors, the Executive Board and the Supervisory Board,

and to operate the Group’s business in compliance with legal and regulatory requirements

and to maintain the highest ethical standards (Richter, 2019).

Page 38

28

7.9 Sun Pharmaceuticals

Sun Pharmaceuticals was established by Mr Dilip Shanghvi in 1983 in Vapi, India with five

products to treat psychiatry ailments. Today, it is the largest chronic prescription company

in India and a market leader in psychiatry, neurology, cardiology, orthopedics,

ophthalmology, gastroenterology and nephrology. Sun Pharma was listed on the stock

exchange in 1994 in an issue oversubscribed 55 times. The founding family continues to

hold a majority stake in the company. Today Sun Pharma is the second largest and the most

profitable pharmaceutical company in India, as well as the largest pharmaceutical company

by market capitalization on the Indian exchanges. They have over 40 (API & finished dose)

state-of-the-art manufacturing sites spanning 6 continents. These manufacturing units are

located in India, the US, Brazil, Canada, Egypt, Hungary, Israel, Bangladesh, Mexico,

Romania, Ireland, Morocco, Nigeria, South Africa and Malaysia. These units provide best-

in-class products to patients across 150 countries worldwide.

In Hungary, they engaged in manufacturing and sale of APIs, intermediates and finished

products which are supplied in the domestic and foreign markets.Some of their key APIs

include Codeine Phosphate Hemihydrate, Dihydrocodeine Bitartrate, and Pholcodine,

Ethylmorphine HCl, Oxycodone HCl, Morphine Sulfate, Phenobarbital Acid and Sodium.

Their diverse product portfolio covers cardiology, substances for the central nervous system,

antidepressants, antispasmodics and other products for coughing.

Their operations in Hungary are supported by global R&D and manufacturing with an

unwavering commitment to quality. Their medicines are trusted by healthcare professionals

and patients in over 150 countries of the world. Their global presence is supported by over

41 manufacturing facilities across 5 continents. They have a multi-cultural workforce

comprising more than 30,000 employees of over 50 nationalities.

In 2007, Sun Pharma demerged its innovative R&D arm and listed it separately on the stock

market as the Sun Pharma Advanced Research Company Ltd. (NSE: SPARC, BSE: 532872).

In 2013, SPARC declared revenue of Rs. 873 million. SPARC focuses on new chemical

entities (NCE) research. Market Cap in May 2017 was $24.9 Billion (sunpharma, 2019)

Page 39

29

7.10 Investment Risk Management

Risk means uncertainty in the investment. In the stock market, there is a risk that the investor

will not get the same amount which he had expected. Generally, return on investment is

related to the risk. High returns mean high risk associated with that investment. High return

is the reward for the risk taken for an investment. It can be caused by a various event like

fluctuation in prices, changes in governmental policy, some disturbance in the world market,

Risk can’t be removed from an investment but can be minimized with the risk management.

Risk management is the process of identifying, analysing the uncertain event that will affect

the investment. In order to make investment less risky, there is some model. With help of

models and analysis, the investor can have a rough idea about the risk involves in the

investments. Risk management is not only beneficial for the investor but also to the

organization. It is the ongoing process it needs to be applied and make changes with the time.

The risk can be reduced either by transferring the risk or sharing the risk. Transferring risk

is diversifying the investment or making a diversified portfolio with this the risk got

transferred to financial investments or hedging.

Financial risk modelling is done determine the risk it includes lots of model Value at Risk is

the most common and efficient model to identify the risk. Basel II also proposed the risk

modelling.

Page 40

30

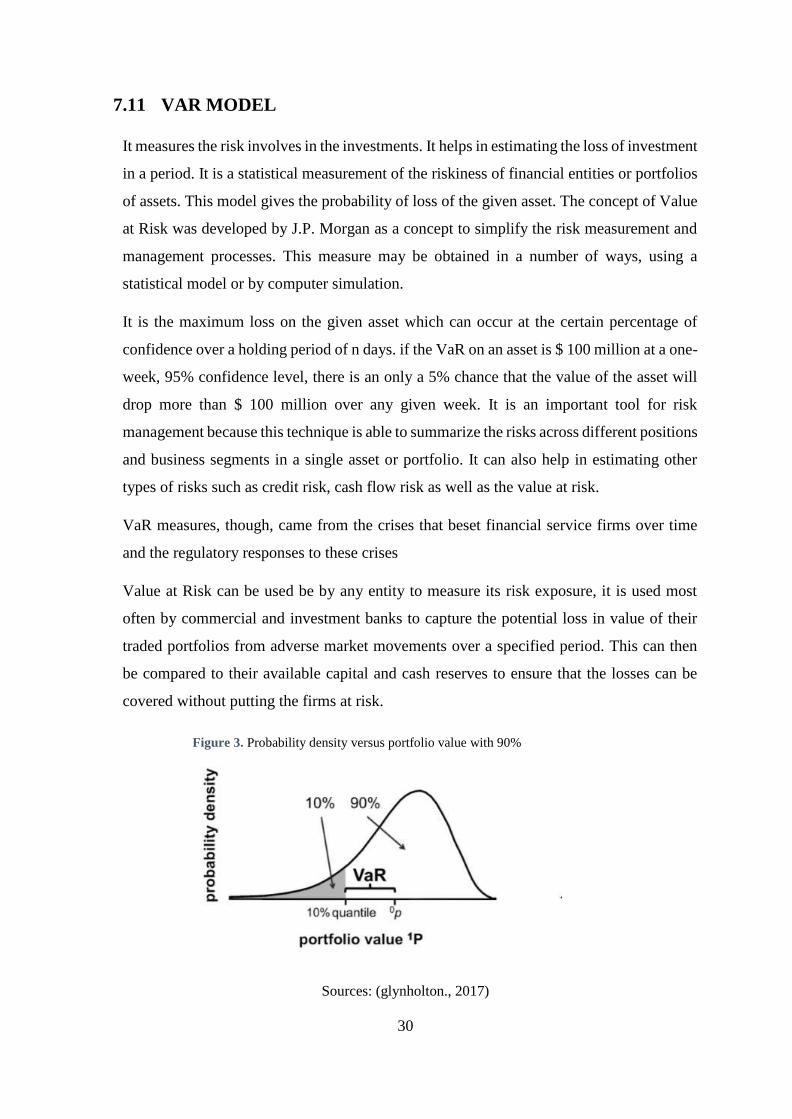

7.11 VAR MODEL

It measures the risk involves in the investments. It helps in estimating the loss of investment

in a period. It is a statistical measurement of the riskiness of financial entities or portfolios

of assets. This model gives the probability of loss of the given asset. The concept of Value

at Risk was developed by J.P. Morgan as a concept to simplify the risk measurement and

management processes. This measure may be obtained in a number of ways, using a

statistical model or by computer simulation.

It is the maximum loss on the given asset which can occur at the certain percentage of

confidence over a holding period of n days. if the VaR on an asset is $ 100 million at a one-

week, 95% confidence level, there is an only a 5% chance that the value of the asset will

drop more than $ 100 million over any given week. It is an important tool for risk

management because this technique is able to summarize the risks across different positions

and business segments in a single asset or portfolio. It can also help in estimating other

types of risks such as credit risk, cash flow risk as well as the value at risk.

VaR measures, though, came from the crises that beset financial service firms over time

and the regulatory responses to these crises

Value at Risk can be used be by any entity to measure its risk exposure, it is used most

often by commercial and investment banks to capture the potential loss in value of their

traded portfolios from adverse market movements over a specified period. This can then

be compared to their available capital and cash reserves to ensure that the losses can be

covered without putting the firms at risk.

Sources: (glynholton., 2017)

Figure 3. Probability density versus portfolio value with 90%

confidence in portfolio

Page 41

31

The Fig.3 shows that in case 90% VaR i.e., 90% confidence in the portfolio.

VAR have two main parameters

1. Horizon

2. Confidence Level

There are three main approaches of calculating VaR

• Variance-Covariance approach,

• Historical simulation

• Monte Carlo simulation

Variance approach- In this method, it is assumed that the returns on risk factors are normally

distributed, the correlations between risk factors are constant. The daily Value at Risk is a

function of the standard deviation and the desired confidence level. To measure the standard

deviation of each risk factor is the historical data is used.

Historical Stimulation- This model calculates potential losses using actual returns in the risk

factors from historical data. The rare events and crashes can be included

In the results. As the risk factor returns used for revaluing the portfolio are actual past

movements, the correlations in the calculation are also actual past correlations. They capture

the dynamic nature of correlation as well as scenarios when the usual correlation

relationships break down.

Monte Carlo simulation method- It is similar to historical stimulation but instead of using

historical changes, a distribution that adequately describes price changes are used. After

simulating price changes or changes in risk factors, hypothetical profits and losses are

calculated. Finally, VaR is calculated as a percentile corresponding to the chosen confidence

level. This method is capable of finding the behaviour in the complex products.

Page 42

32

Limitation

• VaR is dependent on the underlying assumptions used by the model, such as normality

and liquid markets.

• Using historical data sometime doesn’t help in predicting future risk.

Page 43

33

7.12 Ratio

Financial ratios are the comparison of the financial statement of the company. It is easier

to understand and give a brief idea about company’s performance. It can be also used to

compare the two companies as it is a simple mathematical formula. It doesn’t take in

consideration of the size of the firm. Ratio analysis allows us to compare the two

companies which are in different counties doing business in different currencies. It is just

computing data from the financial statement of the company and having a deep analysis

of the results. The financial ratio is divided into several categories: liquidity, solvency,

efficiency, profitability, market prospect, investment leverage. The ratio analysis will

help in analysing the financial performance of the company with market capitalization.

I) Liquidity ratio: It analyses the company’s ability to pay it debt. It shows that if in any

unseen event the company have to its debt how much it can pay off its liabilities and other

a) Quick Ratio/ Acid test Ratio: shows how easily a company can convert its asset into

cash in order to pay off its current liabilities.

Formula:

Quick Ratio =

Total Current Assets − Inventory − Prepaid Expenses

Current Liabilities

(1)

II) Financial leverage ratio/ equity debt ratio: it measures the overall debt of the company

in comparison of the assets or equity. It indicates the assets of the company which actually

belongs to the shareholder and the capital structure of the company. If the leverage is high it

means the creditors have major share in the asset. In case of solvency, the shareholder will

be in loss.

a) Debt to equity ratio: It shows the percentage of finance come from creditors and

shareholders. This ratio helps the investor or stakeholders to know the overall burden in

future indicates how much debt a company is using to finance its assets relative to the value

of shareholders’ equity

Page 44

34

Formula:

Debt − Equity Ratio =

Total Liabilities

Shareholder′s Equity

(2)

Lower ratio is better for the company. Lower debt to equity implies the company is more

financially stable.

III) Profitability Ratio:

Profitable ratio shows the profit generated by the company from its core business. It helps

the investor to have an idea of the return on investment

a) Profit margin/ Return on sale/ Gross profit:

It measures the amount of net income earned with each dollar of sales generated by

comparing the net income and net sales of a company It shows the stakeholders to about the

efficiency of company. Low margin shows that company’s expenses are high which is not

good for the company. It shows how much profit is been generated in relation with the sales.

Formula:

Profit margin =

Net Income

Net Sales

(3)

b) Return on equity Ratio

It shows the profit generated from the investment done by the shareholders. This ratio is

beneficial for potential investor as it indicates how their money will be utilized by the

company. Higher Ratio is better. A return on € 1 means that every euro of common

stockholders' equity generates 1 euro of net income

Formula:

Return on equity Ratio =

Net Income

Shareholder’s equity

(4)

Page 45

35

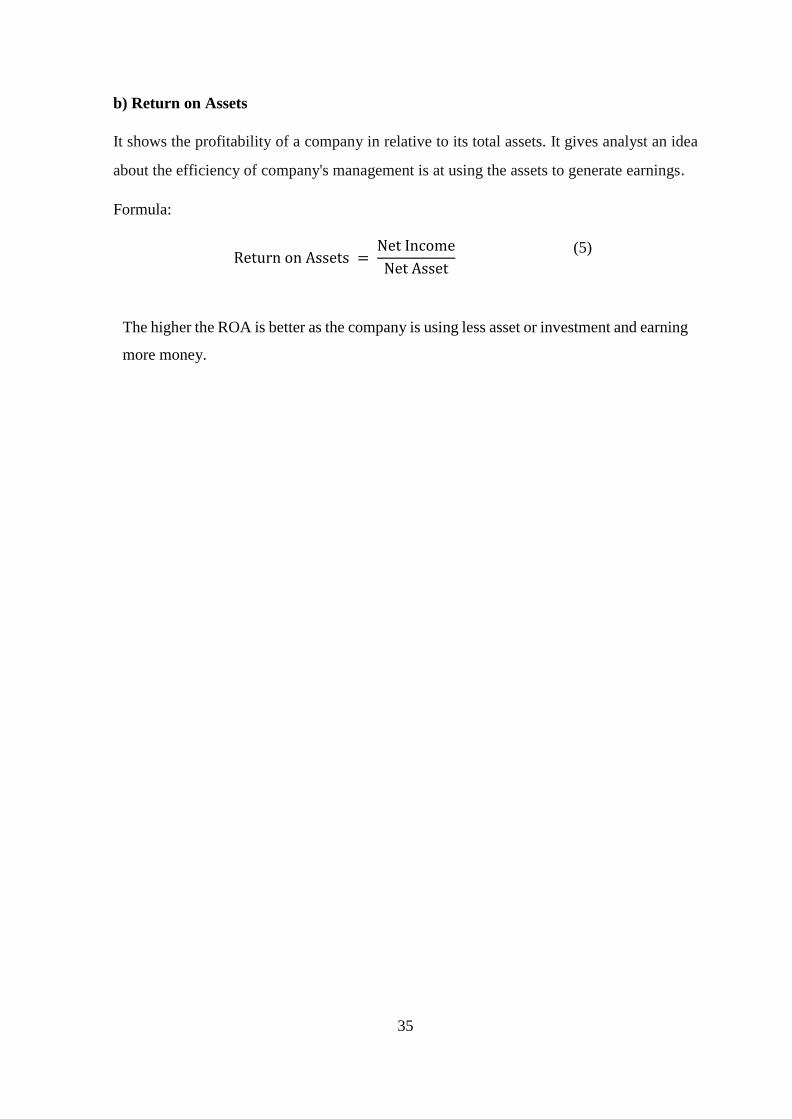

b) Return on Assets

It shows the profitability of a company in relative to its total assets. It gives analyst an idea

about the efficiency of company's management is at using the assets to generate earnings.

Formula:

Return on Assets =

Net Income

Net Asset

(5)

The higher the ROA is better as the company is using less asset or investment and earning

more money.

Page 46

36

7.13 T-Test in Ms-Excel

It is a standardized value which is calculated from sample data during a hypothesis test. T-

tests are the test results are all based on t-values. It is a procedure which helps in calculating

the statistical test that compares data to what is expected under the null hypothesis, Null

hypothesis is a hypothesis of no difference.

If data set have multiple random samples of the same size from the same population and

performed the same t-test, we will have number of t-values. A specific t-distribution is

known by its degrees of freedom (DF), a value closely related to sample size. Therefore,

different t-distributions exist for every sample size. For t-tests, if we take a t-value and place

it in the context of the correct t-distribution, we can calculate the probabilities associated

with that t-value.A probability allows us to find how common or rare our t-value is under

the assumption that the null hypothesis is true. If the probability is low enough, we can

conclude that the effect observed in our sample is inconsistent with the null hypothesis. The

evidence in the sample data is strong enough to reject the null hypothesis for the entire

population. (Minitab Blog Editor, 2016)

Page 47

37

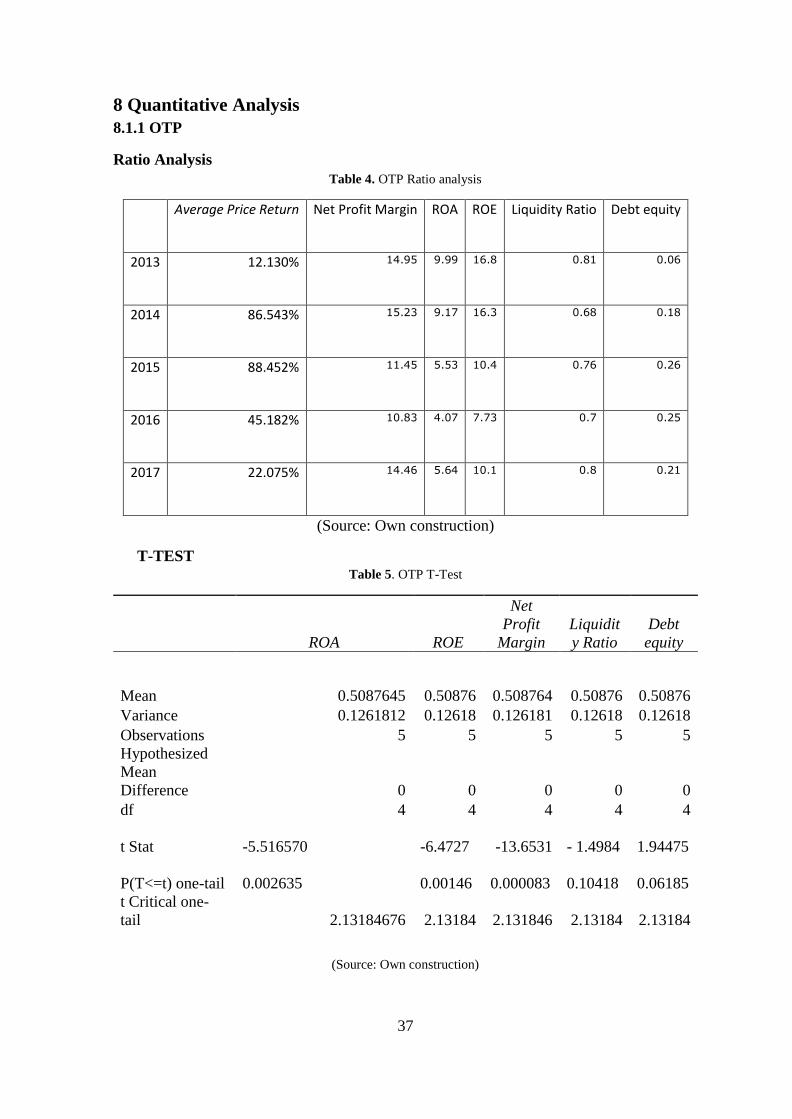

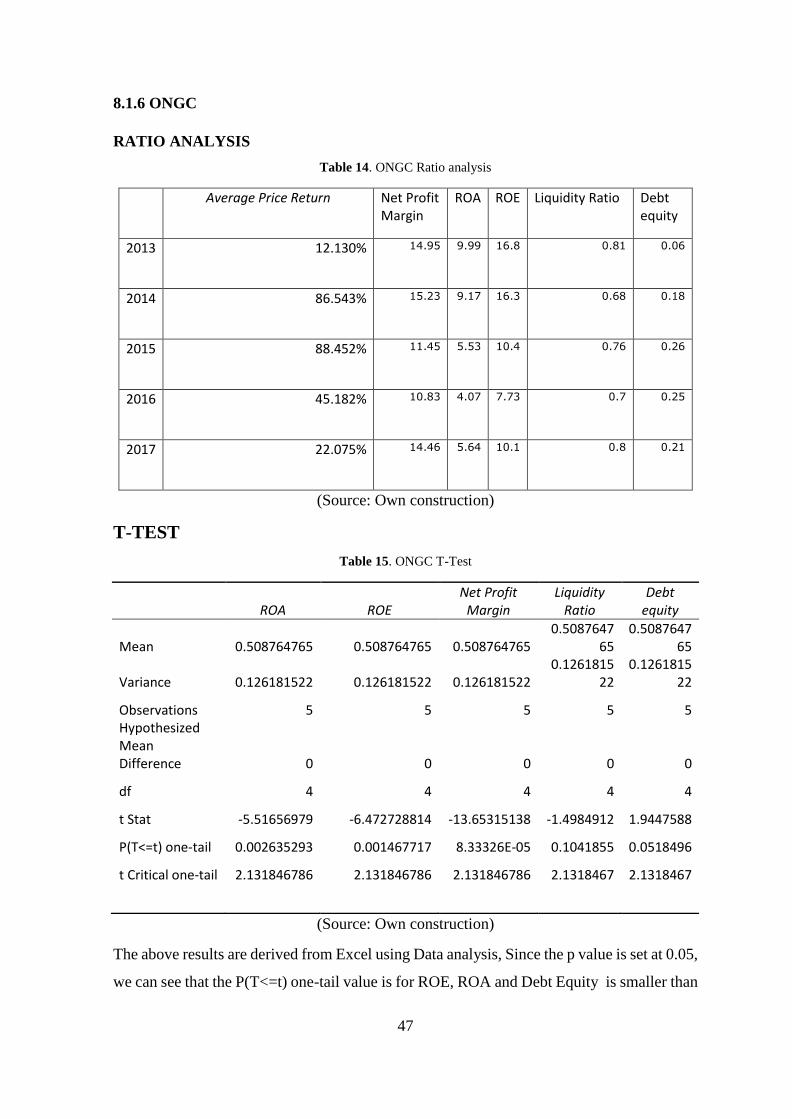

8 Quantitative Analysis

8.1.1 OTP

Ratio Analysis

Table 4. OTP Ratio analysis

Average Price Return Net Profit Margin ROA ROE Liquidity Ratio Debt equity

2013 12.130% 14.95 9.99 16.8 0.81 0.06

2014 86.543% 15.23 9.17 16.3 0.68 0.18

2015 88.452% 11.45 5.53 10.4 0.76 0.26

2016 45.182% 10.83 4.07 7.73 0.7 0.25

2017 22.075% 14.46 5.64 10.1 0.8 0.21

(Source: Own construction)

T-TEST Table 5. OTP T-Test

ROA ROE

Net

Profit

Margin

Liquidit

y Ratio

Debt

equity

Mean 0.5087645 0.50876 0.508764 0.50876 0.50876

Variance 0.1261812 0.12618 0.126181 0.12618 0.12618

Observations 5 5 5 5 5

Hypothesized

Mean

Difference 0 0 0 0 0

df 4 4 4 4 4

t Stat

-5.516570 -6.4727 -13.6531 - 1.4984

1.94475

P(T<=t) one-tail

0.002635

0.00146

0.000083

0.10418

0.06185

t Critical one-

tail 2.13184676 2.13184 2.131846 2.13184 2.13184

(Source: Own construction)

Page 48

38

The above results are derived from Excel using Data analysis, Since the p value is set at 0.05,

we can see that the P(T<=t) one-tail value is for the ROE (0.002), ROA (0.0014),

Net Profit Margin ratio (0.000083) is smaller than the p-value(0.05) to reject the null

hypothesis, Moreover, the t-value is smaller than the t-critical value, for ROE , ROA, Net

Profit Margin ratio reject the null hypothesis

Page 49

39

8.1.2 Richter Gedeon Nyrt

RATIO ANALYSIS

Table 6. Richter Gedeon Nyrt Ratio analysis

Average Price Return Net

Profit Margin

ROA ROE Liquidity Ratio Debt equity

2013 -0.047% 12.17 6.16 8.03 2.9 0.1

2014 0.103% 7.05 3.47 4.51 2.37 0.08

2015 -0.168% 14.86 7.39 9.23 3.26 0.06

2016 -0.041% 16.99 8.47 10.2 2.45 0.04

2017 -0.015% 2 1.13 1.33 2.54 0

(Source: Own construction)

T-TEST Table 7. Richter Gedeon Nyrt T-Test

Net Profit

Margin Debt

equity Liquidity

Ratio ROA ROE

Mean -0.00033777 -0.00033 -

0.000337779 -0.000337 -

0.0003377

Variance 9.31827 9.31827 9.31827 9.31827 9.31827

Observations 5 5 5 5 5 Hypothesized Mean Difference 0 0 0 0 0

df 4 4 4 4 4

t Stat -3.90182744 -3.273535 -16.3000115 -3.974658 -4.048802

P(T<=t) one-tail 0.008757189 0.015343

0.00004145 0.008171 0.007571

t Critical one-tail 2.131846786 2.131846 2.131846786 2.131786 2.131786

(Source: Own construction)

Page 50

40

The above results are derived from Excel using Data analysis, Since the p value is set at 0.05,

we can see that the P(T<=t) one-tail value is for all the ratio is smaller than the p-value to

reject the null hypothesis,

ROE (0.0075), Net profit (0.008), ROA (0.0081), Liquidity (0.00004), Debt Equity (0.01)

Moreover, the t-value is smaller than the t-critical value, for all the ratio reject the null

hypothesis

Page 51

41

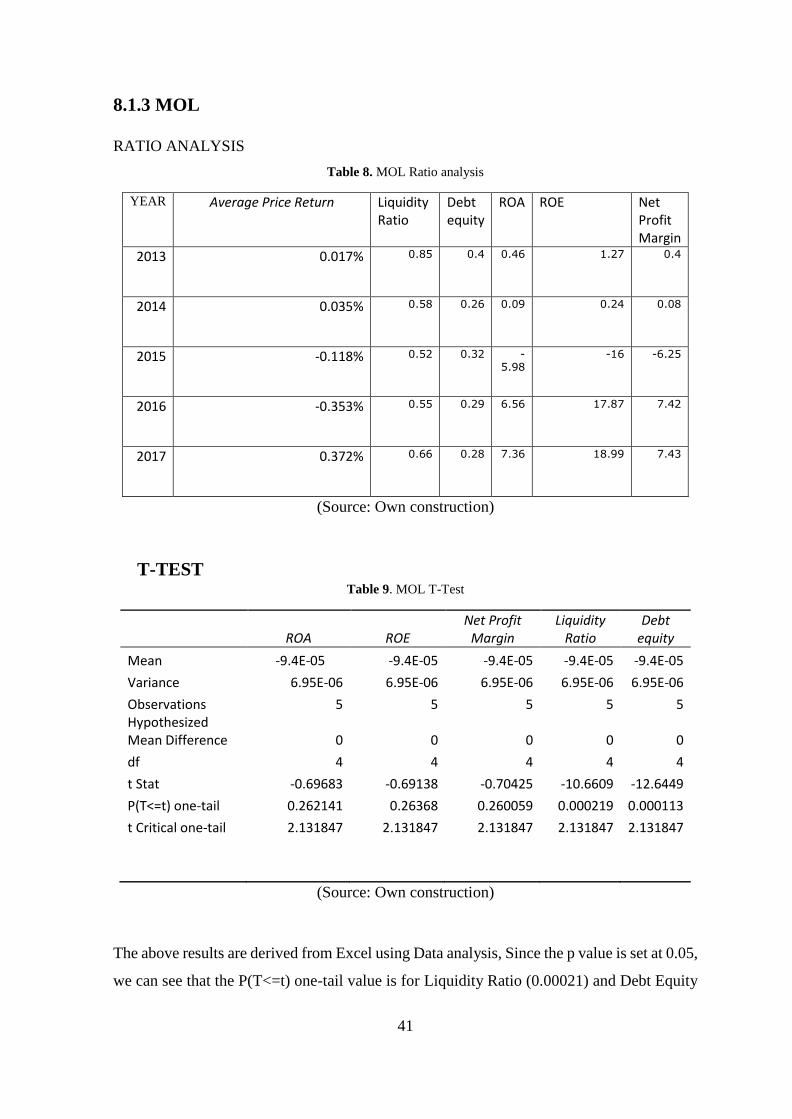

8.1.3 MOL

RATIO ANALYSIS

Table 8. MOL Ratio analysis

YEAR Average Price Return Liquidity Ratio

Debt equity

ROA ROE Net Profit Margin

2013 0.017% 0.85 0.4 0.46 1.27 0.4

2014 0.035% 0.58 0.26 0.09 0.24 0.08

2015 -0.118% 0.52 0.32 -5.98

-16 -6.25

2016 -0.353% 0.55 0.29 6.56 17.87 7.42

2017 0.372% 0.66 0.28 7.36 18.99 7.43

(Source: Own construction)

T-TEST Table 9. MOL T-Test

ROA ROE Net Profit

Margin Liquidity

Ratio Debt

equity

Mean -9.4E-05 -9.4E-05 -9.4E-05 -9.4E-05 -9.4E-05

Variance 6.95E-06 6.95E-06 6.95E-06 6.95E-06 6.95E-06

Observations 5 5 5 5 5 Hypothesized Mean Difference 0 0 0 0 0

df 4 4 4 4 4

t Stat -0.69683 -0.69138 -0.70425 -10.6609 -12.6449

P(T<=t) one-tail 0.262141 0.26368 0.260059 0.000219 0.000113

t Critical one-tail 2.131847 2.131847 2.131847 2.131847 2.131847

(Source: Own construction)

The above results are derived from Excel using Data analysis, Since the p value is set at 0.05,

we can see that the P(T<=t) one-tail value is for Liquidity Ratio (0.00021) and Debt Equity

Page 52

42

Ratio (0.00011) is smaller than the p-value to reject the null hypothesis for them, Moreover,

the t-value is smaller than the t-critical value, for Liquidity Ratio and Debt Equity Ratio

reject the null hypothesis

Page 53

43

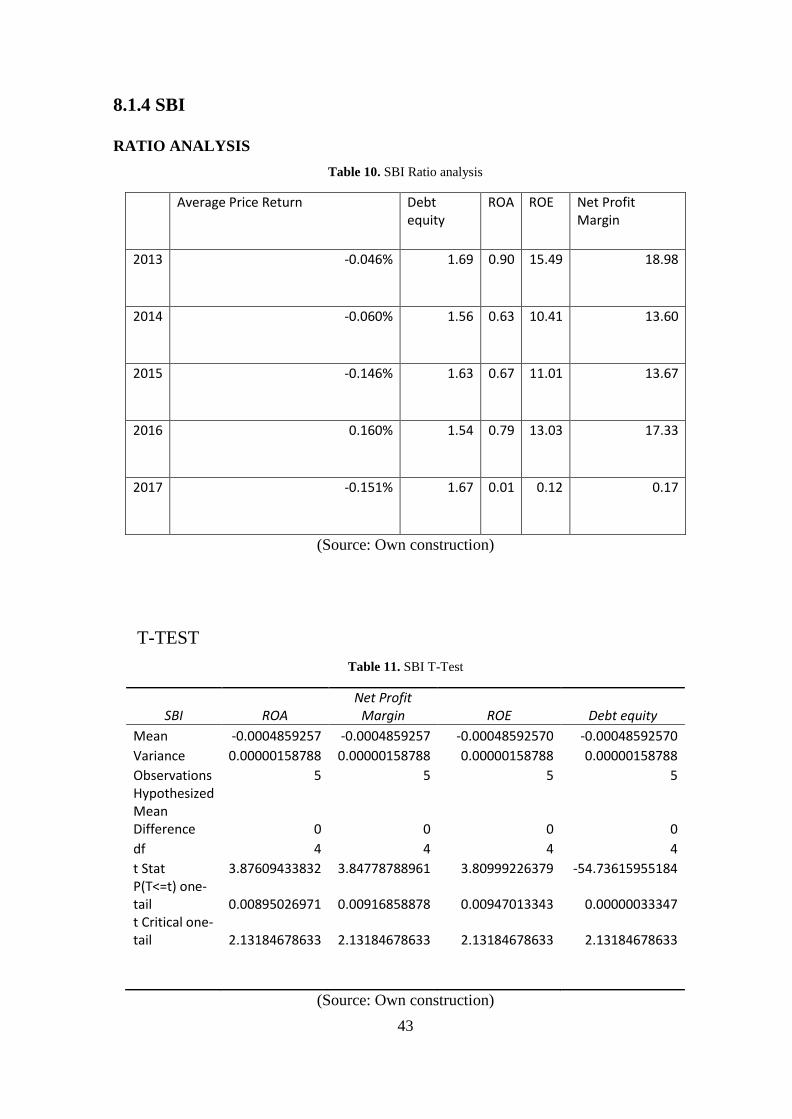

8.1.4 SBI

RATIO ANALYSIS

Table 10. SBI Ratio analysis

Average Price Return Debt

equity ROA ROE Net Profit

Margin

2013 -0.046% 1.69 0.90 15.49 18.98

2014 -0.060% 1.56 0.63 10.41 13.60

2015 -0.146% 1.63 0.67 11.01 13.67

2016 0.160% 1.54 0.79 13.03 17.33

2017 -0.151% 1.67 0.01 0.12 0.17

(Source: Own construction)

T-TEST

Table 11. SBI T-Test

SBI ROA Net Profit

Margin ROE Debt equity

Mean -0.0004859257 -0.0004859257 -0.00048592570 -0.00048592570

Variance 0.00000158788 0.00000158788 0.00000158788 0.00000158788

Observations 5 5 5 5 Hypothesized Mean Difference 0 0 0 0

df 4 4 4 4

t Stat 3.87609433832 3.84778788961 3.80999226379 -54.73615955184 P(T<=t) one-tail 0.00895026971 0.00916858878 0.00947013343 0.00000033347 t Critical one-tail 2.13184678633 2.13184678633 2.13184678633 2.13184678633

(Source: Own construction)

Page 54

44

The above results are derived from Excel using Data analysis, Since the p value is set at 0.05,

we can see that the P(T<=t) one-tail value is for all the ratio is smaller than the p-value to

reject the null hypothesis,

ROA (0.0089), Net profit (0.009), ROE (0.0094) Liquidity (0.00004), Debt Equity

(0.0000003334)

Moreover, the t-value is smaller than the t-critical value, for all the ratio reject the null

hypothesis.

Page 55

45

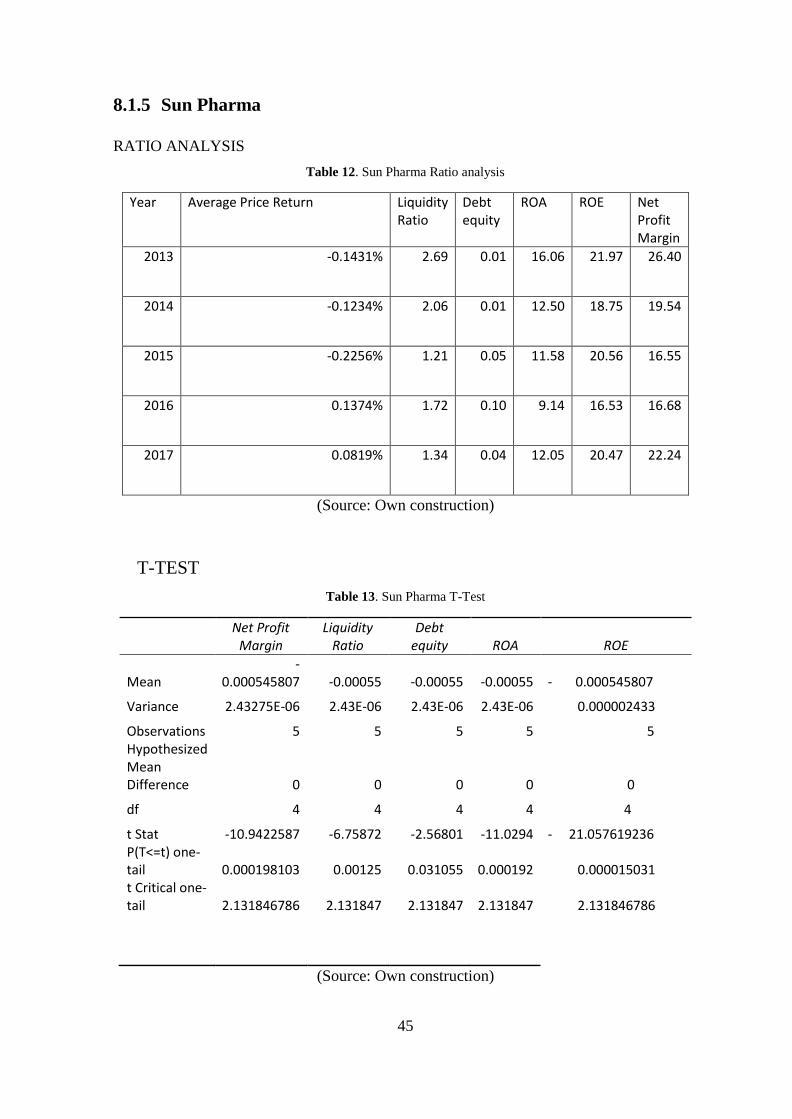

8.1.5 Sun Pharma

RATIO ANALYSIS

Table 12. Sun Pharma Ratio analysis

Year Average Price Return Liquidity Ratio

Debt equity

ROA ROE Net Profit Margin