Thirteen Critical Points in Contemporary Economic Theory: An Interpretation Oskar Morgenstern Journal of Economic Literature, Vol. 10, No. 4. (Dec., 1972), pp. 1163-1189. Stable URL: http://links.jstor.org/sici?sici=0022-0515%28197212%2910%3A4%3C1163%3ATCPICE%3E2.0.CO%3B2-8 Journal of Economic Literature is currently published by American Economic Association. Your use of the JSTOR archive indicates your acceptance of JSTOR's Terms and Conditions of Use, available at http://www.jstor.org/about/terms.html. JSTOR's Terms and Conditions of Use provides, in part, that unless you have obtained prior permission, you may not download an entire issue of a journal or multiple copies of articles, and you may use content in the JSTOR archive only for your personal, non-commercial use. Please contact the publisher regarding any further use of this work. Publisher contact information may be obtained at http://www.jstor.org/journals/aea.html. Each copy of any part of a JSTOR transmission must contain the same copyright notice that appears on the screen or printed page of such transmission. The JSTOR Archive is a trusted digital repository providing for long-term preservation and access to leading academic journals and scholarly literature from around the world. The Archive is supported by libraries, scholarly societies, publishers, and foundations. It is an initiative of JSTOR, a not-for-profit organization with a mission to help the scholarly community take advantage of advances in technology. For more information regarding JSTOR, please contact [email protected]. http://www.jstor.org Thu Dec 27 23:06:05 2007

Transcript

Thirteen Critical Points in Contemporary Economic Theory: An Interpretation

Oskar Morgenstern

Journal of Economic Literature, Vol. 10, No. 4. (Dec., 1972), pp. 1163-1189.

Journal of Economic Literature is currently published by American Economic Association.

Your use of the JSTOR archive indicates your acceptance of JSTOR's Terms and Conditions of Use, available athttp://www.jstor.org/about/terms.html. JSTOR's Terms and Conditions of Use provides, in part, that unless you have obtainedprior permission, you may not download an entire issue of a journal or multiple copies of articles, and you may use content inthe JSTOR archive only for your personal, non-commercial use.

Please contact the publisher regarding any further use of this work. Publisher contact information may be obtained athttp://www.jstor.org/journals/aea.html.

Each copy of any part of a JSTOR transmission must contain the same copyright notice that appears on the screen or printedpage of such transmission.

The JSTOR Archive is a trusted digital repository providing for long-term preservation and access to leading academicjournals and scholarly literature from around the world. The Archive is supported by libraries, scholarly societies, publishers,and foundations. It is an initiative of JSTOR, a not-for-profit organization with a mission to help the scholarly community takeadvantage of advances in technology. For more information regarding JSTOR, please contact [email protected].

Thirteen Critical Points in Contemporary Economic Theory:

By OSKARMORGENSTERN New York University

I a m grateful for comments received from William Brock, M . D. God-frey, K. P. Heiss, ]. Ladermun, E. Marchi, C. F. Morgenstern, A. Schotter, G. Schwodiauer, G. L. Thompson, and Kan Young. Special thanks are due to Mark Perlman and an anonymous referee. All are, of course, absolved of any responsibility for any of the contents of this paper. Support of this work in part by the OfFice of Naval Research through a grant to New York University is gratefully acknowledged.

IN 1900, David Hilbert addressed the sec- ond International Congress of Mathe-

maticians in Paris on the future of mathe- matics. His speech [B]became famous; in it he listed 23 unsolved problems in mathe- matics from whose solutions much progress could be expected. Many men have subse- quently gained renown for successfully at- tacking Hilbert's problems. Though Hilbert was a mathematician of the purest water, many of his problems sprang from the con- tact of mathematics with physics-the social sciences unfortunately had not yet come into the purview of the great mathemati- cians. Who can say what would by now have happened to economics if that link had been established as early as 1900.

I am aware that I am no Hilbert and the eventual solution of the problems I shall briefly examine may not guarantee the kind of fame that Hilbert promised, but the problems are crucial, even if some are only generally circumscribed. Other economists may define different problems. No complete listing could ever be made. Each problem solved usually suggests new ones which could not have been stated without a given problem first having been solved.

In describing these issues I shall, without either hesitation or further apology, refer to a fair number of my own writings in the be- lief that a life-long concern with economic theory provides the needed justification.

This paper adddresses itself primarily to the young economists who have been brought up on the current group of popular textbooks. What these books have in com- mon so far as I can see, is that few, if any unsolved theoretical (as distinct from ap- plied) problems in economics are men-tioned (or rather, unsolved problems- simply do not seem to exist).l It is therefore all the more surprising that anyone should want to go on into a science that seems to have no open theoretical problems left-a vastly dif- ferent situation from that of physics or biol- ogy where even the layman knows that those worlds are filled with riddles. No wonder that these sciences attract brilliant minds. In fact, however, the world of social phenomena, including the economic one, holds such a plenitude of difficult, impor- tant and unsolved theoretical problems- never once mentioned in the above kinds

' There are refreshing exceptions, e .g . , the book by Vivian C. Walsh [36, 19701.

1164 Journal of Economic Literature

of introductory books-that they too are worthy of the attention of the best. This is particularly important in view of the fact that present-day economics contributes so little that is new or useful towards solving the practical troubles of the world (though on their solution, in part, the very survival of the human race may depend; simultane- ously the astounding progress of the natural sciences often presents, us-via applications -with new social problems).

A decisive change in the development and orientation of a science comes about when a basic new concept or theory is in- troduced and illuminated (such as gravita- tion, relativity, the quantum in physics). A similar reformulation happens when it be- comes apparent that the traditional way of thinking leads deeper and deeper into a maze of poorly understood, disconnected arguments of varying substance. Of the lat- ter, economics offers a number of instances; the most important example was connected with the earlier labor value theory when the substitution of marginal analysis for the maze of countless exceptions and inner con- tradictions was made. It seemed that a sound basis for economic analysis had been found: a unifying principle of great gener- ality and, more important, of practical ap- plicability. Marginal utility did indeed re- solve many issues of labor value theory, but, as always happens, it also sharpened some that remained unsolved (or even identified new problems). The question of how to distribute the value of a joint prod- uct to its contributing parts is paramount; the problem of "imputation" has plagued economists ever since the 1870s, notably in the basic formulation it received from the Austrian economists. Of course, it is implicit in the whole of marginal analysis, no matter how formulated; it is solved only using dual variables, a method derived from game theory.

Economics, being ultimately an empirical science, has to describe and explore the

given problems. But what is "given" and how do we describe? Einstein has com-mented on the fact that most scientists naively think that it is clear what to observe and how to measure. Might that not also be true in economics? In identifying the eco- nomic phenomena, certain primitive con-cepts and terms have to be used. At first, common sense notions such as "price," "offer," "demand," "money," etc., appear to be adequate, to be replaced gradually by scientific concepts as the science develops. However, because of the freedom with which the mind can move, it happens fre- quently that the relation with reality is lost, and that purely hypothetical notions are in- troduced. In addition, there is often a change in the meaning of words. Consider "competition": the common sense meaning is one of struggle with others, of fight, of attempting to get ahead, or at least to hold one's place. It suffices to consult any diction- ary of any language to find that it de-scribes rivalry, fight, struggle, etc. Why this word should be used in economic theory in a way that contradicts ordinary language is difficult to see. No reasonable case can be made for this absurd usage which may con- fuse and must repel any intelligent novice.

In current equilibrium theory, there is nothing of this true kind of competition: there are only individuals, firms or consum- ers, facing given prices, fixed conditions, each firm or consumer for convenience in-significantly small and having no influence whatsoever upon the existing conditions of the market (rather mysteriously formed by thtonnement (cf .point 4 below) and there- fore solely concerned with maximizing su7.e utility or profit-the latter then being ex-actly zero. The contrast with reality is strik- ing; the time has come for economic theory to turn around and to "face the music."

There is, of course, always the possibility and the temptation of proving all sorts of theorems which have no empirical rele-vance whatsoever. This is what happens in

1165 Morgenstern: Contemporary Economic Theory

current textbooks and many treatises, though it is a forward step when theorems of this type are no longer merely asserted, but actually proved. Yet the ultimate crite- rion is whether what the theorem asserts is what is found in reality. One cannot help but be reminded of Hans Christian Ander- sen's story of the Emperor's clothes. Some of the asserted facts simply do not exist: there is hardly a trace of a single market where large numbers of buyers are directly and unmistakably confronted with large numbers of sellers; 'large" meaning pre-cisely so many that the individual partici- pant loses count of the others. Not even the stock market has this property.

One is reminded of J. J. Rousseau: "Nier ce qui est, et expliquer ce qui n'est pas."

TO show that a wrong problem is being solved-wrong in the sense that it is not the empirically given one-is a first ground for rejecting a theory: a matter of irrelevance. A second basis for rejection would be to show that improper, inadequate, or over-simplifying assumptions have been made. Arguments of the second kind are often, but not necessarily, identical with those of the first kind. The third basis, by far the most powerful, is the immanent criticism which accepts the assumptions used and shows that the asserted conclusions do not follow. Some of the subsequent comments employ this method. However, to carry out imman- ent criticism the assumptions have to be stated with clarity and sharpness. In an em- pirical science this is often difficult to do; therefore it is not surprising that even for some well-explored parts of economics it is not easy to find out exactly what was as- sumed; hence, the continual quarrel about the "true" assumptions. In what follows it will also be necessary to state that certain assumptions are implicitly contained in the theory or in other assumptions.

No argument of the latter kind is possible if the theory is formulated axiomatically. I shall not discuss the axiomatic method here

in extenso, but merely state that any theory ultimately will have to be axiomatized. This means that a set of postulates or axioms is formulated to achieve some definite aim: some specific theorem or theorems are to be derivable from the axioms. The axioms must be free of contradictions and be inde- pendent; they may also possess categoricity (completeness), depending on the subject matter. I t is desirable that their number be small and that each axiom be transparent, i.e., intuitively acceptable. To find a good balance between these latter demands is in part a matter of taste. The axiomatic method is the most powerful and demand- ing way of stating a theory. As a rule a field will only be axiomatized fairly late in its development, though not necessarily so.

The first set of axioms in economics was probably presented by R. Frisch in 1926 [6], another one, also dealing with utility theory, by F. Alt in 1936 [ I ] ; in 1936 I dis-cussed the role of the axiomatic method for the social sciences [16a]. The first axiomatic system appears to have been the von Neu- mann-Morgenstern utility theory [35] of 1944 with the proof that the axioms actually imply the existence of an expected utility numerical up to a linear transformation, added in 1947 (games of strategy were also axiomatized in 1944). Since then several ax- iomatic statements have made their appear- ance in economics, a healthy development, though proof is not always given that the axioms fulfill all requirements they have to meet. Without that proof one cannot truly speak of a proper use of the axiomatic method. But at any rate, more of an effort is now made to state assumptions unambigu- ously.

The following 13 Points appear to be among the most interesting to which atten- tion ought to be drawn. They follow no par- ticular order of importance.

1. Control of Economic Variables Present economic theory allegedly deals

1166 Journal of Economic Literature

with maxima e.g., of profit, utility . . . (or minima, e.g., of cost, disutility . . .). The fundamental objection is that these extrema exist and are attainable only if the individ- ual or firm (or whatever other entity) con-trols all variables on which the maximum depends. Some variables may be statisti- cally controllable, such as the behavior of nature. If some variables, on which the out- come depends, are under the conscious con- trol of other entities which wish to maxi- mize their utility or profit and who may ei- ther be opposed to a given economic agent (individual, firm, labor union, government, etc. ) or, as it might be, sometime may wish to cooperate with it, then such complete control is lacking for the individual and it is not a maximum problem which is involved, but a curious mixture of maxima, minima, etc. We are confronted with a conceptually different situation which cannot be treated in the conventional manner of differential calculus. Nor can this situation be de-scribed by maxima subject to side condi- tions (no matter how difficult or complex). Virtually all economic activity involving ex- change of goods and services, direct or indi- rect, is described by the fact that none of the parties completely controls the outcome (not even statistically, as in the case of a- presumably-indiff erent nature). The seem- ing argument that of, say, 100 vari-ables, only one is under someone else's con- trol and could therefore be neglected (i.e., retaining for the individual the maximum property) is conceptually incorrect and hence, inapplicable. Economic theory sim- ply is not, in general, confronted with pure maximum problem^,^ certainly not when the theory deals with the interaction of the individual agents not under centralized control. However, this is how economic the- ory is set up at present and how it is still

'Not even necessarily when considering a dynamic open expanding economy as G. L. Thomp-son and I have shown [22a, 19721.

viewed, e.g.,by Samuelson in his Nobel lec- ture [28a]. But it is necessary to face up to the empirically given problem.

What is stated above summarizes a pre- cise and more elaborate exposition of the fundamental issue spelled out in the first chapter of Theory of games and economic behavior [35].In view of the importance of this point, I quote from what von Neumann and I wrote in 1944: Let us look more closely at the type of economy which is represented by the "Robinson Crusoe" model, that is an economy of an isolated single per- son or otherwise organized under a single will. This economy is confronted with certain quantities of commodities and a numher of wants which they may satisfy. The prohlem is to obtain a maximum satisfac- tion. This is-considering in particular our assump- tion of the numerical character of utility-indeed an ordinary maximum prohlem, its difficulty depend- ing apparently on the numher of variables and on the nature of the function to he maximized; hut this is more of a practical difficulty than a theoretical one.. . .

Thus Crusoe faces an ordinary maximum prohlem, the difficulties of which are of a purely technical- and not conceptual-nature, as pointed out.

Consider now a participant a social exchange economy. His problem has, of course, many elements in common with a maximum prohlem. But it also contains some, very essential, elements of an en-tirely different nature. He too tries to obtain .an optimum result. But in order to achieve this, he must enter into relations of exchange with others. If two or more persons exchange goods with each other, then the result for each one will depend in general not merely upon his own actions but on those of the others as well. Thus each participant at- tempts to maximize a function (his aho;e-men- tioned "result") of which he does not control all variables. This is certainlv no maximum vroblem. but a peculiar and disconcerting mixture of several conflicting maximum problems. Every participant is guided by another principle and neither determines all variables which affect his interest.

This kind of problem is nowhere dealt uith in classical mathematics. W e emphasize at the risk of being pedantic that this is no conditional maximum problem, no problem of the calculus of eariation.9, of functional analysis, etc. It arises in full clarity, ez;en in the most "elementary" situatioi~s, e.g., when all uariabler can a.Tsume only a finite number of

1167 Morgenstern: Contemporary Economic Theory

A particularly striking expression of the popular misunderitanding about this pseudo-maximum prob- lem is the famous statement according to which the purpose of social effort is the "greatest possible good for the greatest possible number." A guiding prin- ciple cannot be formulated by the requirement of maximizing two (o r more) functions a t once.

Such a principle, taken literally, is self-contra- dictory. ( In general one function will have no maxi- mum where the other function has one.) I t is no better than saying, e.g., that a firm should obtain maximum prices at maximum turnover, or a maxi- mum revenue a t minimum outlay. If some order of importance of these principles or some weighted average is meant, this should be stated. However, in the situation of the participants in a social economy nothing of that sort is intended, but all maxima are desired a t once-by various participants.

One would be mistaken to believe that it can be obviated, like the difficulty in the Crusoe case . . . by a mere recourse to the devices of the theory of prob- ability. Every participant can determine the vari- ables which describe his own actions but not those of the others. Nevertheless those "alien" variables can- not, from his point of view, be described by statis- tical assumptions. This is because the others are guided, just as he himself, by rational principles- whatever that may mean-and no modus proce-dendi can be correct which does not attempt to understand those principles and the interactions of the conflicting interests of all participants.

Sometimes some of these interests run more or less parallel-then we are nearer to a simple maximum problem. But they can just as well be opposed. The general theory must cover all these possibilities, all intermediary stages, and all their combinations.

I t is sometimes believed that linear pro- gramming, or some of its variants, provides a method for avoiding the above difficulties. This is then attributed to the duality be- tween a zero-sum two-person game and a linear program. Linear economic models are, of course, most interesting, none more so than von Neumann's which has given rise to a considerable literature and is recog- nized as one of the few truly original contri- butions to mathematical economics.

To put linear programming into the right perspective, I quote:

Linear programming is a conceptually very limited matter: it replaces assumptions of continuous rela-

tionships by discontinuous ones and allows for in- equalities. This makes linear programming more realistic in application, provided the basic condition is met. which is that there must be a central authoritv on whose acts alone the outcome depends. This must be due to the overriding fact that this authority (person, firm, government) has a complete and un- challenged control over all variables. Where there is not complete, central control, i.e., where the out- come depends on several decision makers, as in game theory, linear programming does not give the com- plete answer. I t can, however, provide ceteris paribus answers [22,p. 4461.

Complete control-allowing only for probability-is given, for example, in the traveling salesmen situation, in scheduling airlines or school buses, in optimizing food mixes, etc. But it is clear than in any eco- nomic transaction, i.e., deal, or in any pol- icy measure, there are at least two separate decision makers. Even when their number increases, their influence never vanishes. Thus, we are then confronted with situa- tions that can only be modeled by suitable games of strategy. This is the challenge that game theory presents. Economic theory will have to accept this fact, painful as it may be. It suffices to consult almost any modern, contemporary textbook on microeconomics, whether introductory or advanced, to see how great the gulf is that has been opened.

To summarize: There is no complete sub- stitution by game theory, but it is evident that maximization, programming, whether linear, non-linear, dynamic, et'c., become subordinate in the theory of general deci- sion processes. This is similar to the restric- tion of the role of Newtonian planetary me- chanics by the wider space-time concept of relativity theory. However, the absorption of a new paradigm awaits, as a rule, a new generation as Planck has so clearly stated in his scientific autobiography (quoted by S. Bochner [la, 1966, p. 1331) .

2. Revealed Preferen.ce Theory

Revealed preference theory asserts that it

1168 Journal of Economic Literature

is possible, by observing the choices of goods of an individual under budget constraints in a market, to determine the order (ranking) of his preferences. Thus, when confronted with the goods x, y, z . . . he chooses first y, then x, then z, this "reveals" his presumably complete ordering y > x > z. How and ~ h y does one conclude from one such observa- tion and without further explicit assump- tions that the ordering is complete? Further, no such disclosure need be involved even when the underlying ordering is complete: if x, y, z are durable goods and the individual is capable (by virtue of his income) of acquiring all three, he can choose x before y, or y before x, or z before x, etc., as he pleases; nothing is "revealed." Or he can choose all at once in which case the inequalities are x 2 y 2 z. The theory clearly has to allow for all these possibilities if it is intended to deal comprehensively with revelation of prefer- ences.

The choice is made, given prices for the commodities. The theory asserts that it is possible to infer his preferences from the individual's behavior when confronted with successively changing prices. The above ar- gument, however, stands, that if he can af- ford x, and y, and z in each of two different price situations, and if these are durable goods, then nothing is "revealed-except the fact that he acquires all three.

Hence, his preference structure can only be "revealed by an analysis that reaches much farther than the observation of his behavior in the above given circumstance. This "farther" reach means either that he has to be questioned directly-or indirectly by carefully designed experiments-and that certain minimal time intervals have to be considered over which the attempted preference extends. The time intervals are partly a function of the expected life span of the durable goods and partly of the na- ture of his income stream. The time factor, of course, adds a great complication to

what appears to be an innocuous arrange- ment.

Only if x,y, z . . . are instantly perishable goods or services with effects which often disappear instantly, can one imagine that preferences are revealed by the chronologi- cal sequence of choices. The theory of re-vealed preference is, however, supposed to apply to any kind of goods, to any mixture of durable or non-durable goods. This is by implication, by virtue of the claim of its general validity.

The theory is usually presented by con- sidering "bundles" of goods instead of indi- vidual goods. But this does not help mat- ters, since bundles are composites, i.e., mix- tures, and must be reducible to simple goods as the most primitive manifestations of a "bundle." This method is therefore only an inconsequential trick. The final choices of an individual are of specific single goods, which can be composites, as e.g., a motor car with radio, air conditioning, etc. A bun- dle must necessarily contain durable goods, since none could be made up solely of a number of instantly perishable goods and services, which, though perishable, require time for their successive consumption dur- ing which time the others are perhaps de- stroyed or become unavailable. There is in that connection no escape from the compli- cations due to the time and expectation fac- tor which has been so little analyzed in eco- nomic theory. ( I have more to say on this in Points 4 and 9 below, and refer, regarding the above, to my 1934 paper [15] published prior to the theory of revealed preference. )

So we conclude that the theory of re-vealed reference, in spite of its sometimes mathematical presentation, whether in "weak" or "strong" form, is found wanting in some of its basic assumptions and is at best restricted to an exceedingly narrow empirical basis. Another theory will have to take its place. Is this ~ e r h a p s also an illus- tration of the falsehood of Fourier's state-

1169 Morgenstern: Contemporary Economic Theory

ment that mathematics has no symbols for confused ideas? It is often easier to mathe- matize a false theory than to confront real- it^.^

3. Pareto Optimum

This central idea is often formulated in the following manner: an optimum of a group or society is reached when, by im- proving the position of one individual (by adding to his possessions) no one else's po- sition is deteriorated. Economic literature is replete with the use of the Pareto optimum thus formulated or in equivalent language. The simplest case is when utilities of differ- ent individuals are independent of each other. The case where they are interdepen- dent has also been touched on but the for- malism derived from it adds nothing to the simpler assumption of independence which has to be resolved first. It shall, therefore, not be further considered in view of the troubles encountered even for indepen-dence. The additional question whether the theory is invariant under a change of sign- i.e., diminishing someone's position rather than improving it-has also not been settled.

A fundamental alleged advantage of the notion of the Pareto optimum is the sup- posed avoidance of interpersonal compari- sons of utility which, as is well known, al- ways seems to involve ethical judgments not belonging in a descriptive theory. But are such comparisons really avoided and if so, at what price?

How does one find out whether there is improvement or diminution? There are only two ways: either the individuals have to be questioned or the outside observer has to make the decision on the basis of the facts.- But, what facts are known to him? How are they established? If questioned, an individ- ual may deny that he is better off, or assert

9 s to the logical and semantic confusion of this the0 cf. the searching study by W. Kroeber-R i e l r i ~ ,19111.

that he is diminished if someone else re- ceives an addition to his possession~.~ Nei-ther of these statements need be true. They may be made to extract larger com- pensatory amounts or to stop the other from obtaining whatever is being offered. Thus, falsehood has to be excluded expressis uer- bis from the assumptions; but this restricts the theory fundamentally and it would be operationally impossible to enforce. Or, else, the observer has to decide what is the case: he has to state whether the total util- ity experienced by the first individual ( to whom an addition of some particular good is made) is greater than before ( i t might be smaller, if he is already satiated!), and whether no other individual has been di- minished in his utility by this operation. But as this is interpersonal comparison of utilities, it is precisely the notion that the Pareto optimum was designed to avoid!

Thus, we have here a basic concept of contemporary theory which has not been sufficiently explored. No doubt the idea has to be rejected, as formulated cla~sically.~ It reappears-termino~ogically-in recent writ- ing on game theory which is unfortunate, but not critical.

There are some further considerations but only two shall be mentioned: ( a ) The current theory of the Pareto optimum does not say anything about the nature of the goods added, nor about their amozlnts. AS-sume the good to be money: the "others" will perhaps be indifferent if the first indi- vidual is given one dollar more, but hardly

'Note that this postulates some kind of inter-dependence of the utilities of different individuals- which is certainly true in many cases-but in conflict with the normal assumption in contempor- ary theory that they are independent of each other.

Note that the theory of the Pareto optimum in this, its classical form, has to be distinguished from the use of the term, as in e.g., the theory of exchange where merely the state is so named when all further trading stops because no one can any longer improve his position. The dif-ference, however, is not always sharp.

1170 Journal of Econornic Literature

if he is given one million dollars. The rea- son need not be envy, but rather the fact that the large amount gives added power, puts the individual in a more favorable strategic position, and thereby diminishes the others, indirectly. Information about all this would again have to be obtained either from the members of the group or from an all-seeing outside observer. If the addition is not in money, there might in addition have to be restrictions on the kind of goods involved: e.g., are weapons, poisons, etc. to be admitted? Are restrictions concerning their possible uses to be imposed? if admit- ted? etc. In short the social framework would have to be firmly delineated. I shall not follow up this line of thought here.

( b ) The individual may not be able to say truthfully whether he is better off or di- minished. Here is a basic problem. The rea- son would be that he may not know his position fully, partly because of the infor- mation pattern of his own activities, partly because of the dimension of his operations, etc., both possibly (but not necessarily! ) of a stochastic origin, or else also because of the dynamic properties of the economy. It may, for example, be impossible to predict the consequences of an addition when a new good, involving technological progress, is involved. The impossibility of prediction may also be due to the nature of the market ( e .g . ,when the market is subject to a ran- dom walk, as the stock market), or, more intricate, because the future state is more specifically dependent on the behavior of others as described by games of strategy, es- pecially when the individual is involved in an integral game [23].

Current theory does not consider these questions which, however, pose themselves quite naturally. For a fuller treatment, also involving additional problems, I refer to my article of 1964 [20]. Clearly the notion of the Pareto optimum must be used with extreme caution. It is capable of re-interpretation in game theoretical terms which means that it

must be stripped of its restrictive assump- tions of "competition" as this term is cur-rently used.

4. Tdtonnement

This notion still plays a considerable role in past and present formulations of the the- ory of general equilibrium. The assertion is that if initial contracts do not lead to an equilibrium, they are called off and new con- tracts are made. If they are not called off, it follows that a different ultimate price system would result, depending on how "wrong the initial process and transactions were. The question also arises, but is nowhere resolved, whether successive recontracting-when contracts are canceled for want of equilib- rium-is to go on with participants forget- ting the previously planned (non-optimal) positions taken, or negotiating the new pro- posed contracts with total recall. Clearly, different sequences of positions would hap- pen. Also, every participant in the general market is supposed to be both buyer and seller. Irrespective of the latter, tdtonnement is patently impossible if among the items traded there are services or instantly perisha- ble goods. Their supply is irreversible: once made they are gone. Services can, therefore, not even be part of tdtonnement unless this is taken to be a purely hypothetical pro- cedure and not a description of a possible physical sequence of events.

In the Walrasian-Paretian theory an as- sumption of perfect foresight is made or im- plied (see the discussion, for example, by F. H. Knight on this point as discussed in my ar- ticle [16] ) . Now clearly, if perfect foresight exists, there will be no tdtonnement since ev-eryone would go directly to the final equilib- rium price. On the other hand, I have shown (and I believe conclusively) that the notion of "perfect" foresight, taken literally, as it must be taken, leads to logical contradic- tions such that it can never form a basis of a theory of economic equilibrium. If this idea is dropped, then it is necessary to make

1171 Morgenstern: Contemporary Economic Theory

other specific asumptions about the distribu- tion of different degrees of foresight, or lack of it, among the participants in the market, and to examine how an equilibrium is at- tained. I know of no such investigations in the literature concerned with general equi- librium. "Perfect foresight" must, of course, not be confused with perfect and complete information since these concepts are used in a specific manner in game theory and with- out contradiction. In game theory the differ- ent states of information and their develop- ment during the course of a play are thor- oughly taken into account, especially in the extensive form of a game tree.

It is clear that the idea of the tdtonnement in contemporary theory is only a method- ological device and not a description of any historical, actual process even as it is de- scribed in game theory. The postulate that by this device one could or would converge to, or arrive at, the set of equilibrium prices is characterized by the fact that no excess demand or supply is supposed to exist at equilibrium. How many steps are permitted? Is their number finite (recall Zeno's para- dox!)? How many commodities and buyers and sellers are involved? Since it is conceiva- ble that a state of equilibrium may never be reached in any finite time, the existence of equilibrium has to be proved independently of the use of tdtonnement and it is doubtful whether this superficially intriguing notion is at all required. What possibilities there are would require the use of methods of conver- gence of non-linear programming.

An additional remark is that this theory necessarily makes the restrictive, though not explicit, assumption that it is forbidden for participants to cooperate while tdtonnement is going on, since cooperation would trans- form a "free competition" market of many participants into one of fewer effective par- ticipants, i.e., into one essentially of oligo- polistic-oligopsonistic nature. Nor does tdtonnement allow for "price leaders," ad- ministered prices, etc., situations with which

we certainly are familiar and for which we certainly have to account in general equilib- rium theory. With such markets entirely dif- ferent conditions obtain which cannot be derived from those presumably existing un- der "free" competition allegedly arrived at by tdtonnement, and it is not certain that, given cooperation, tdtonnement would ever converge toward any kind of the postulated type of equilibrium. Note, also, that "per- fect foresight" and cooperative bargaining are logically incompatible (the other diffi- culties of "perfect foresight" quite apart).

5. The Walras-Pareto Fixation

As already stated, it is a complete misno- mer to call the conditions under which the general economic equilibrium is discussed "free" or "perfect competition." Competition means struggle, fight, maneuvering, bluff hiding of information-and precisely that word is used to describe a situation in which no one has any influence on anything, where there is ni gain, ni perte, where everyone faces fixed conditions, given prices, and has only to adapt himself to them so as to attain an individual maximum which may even be zero as in the case of profits. Yet this is what most economic theorists and their textbooks are primarily concerned with! My quarrel is, however, not primarily with the word "competition," but rather with the concen- tration on that largely irrelevant subject mat- ter, whatever name is given to it. It is hard to explain the persistence of this fixation; perhaps it is the silent recognition that fac- ing the real world, the empirically given problem, means the overthrow of much of established, cherished doctrine, and in its wake the abandonment of certain mathemat- ical tools which have become dear to so many. Quoting Marx-mutatis mutandis-I say that "a spectre has arisenv-game the-ory-which, as in their heart they know, rightly challenges the classical outlook, a theory which is so uncomfortable to em-brace. However, there will be no escape. The

1172 Journal of Economic Literature

Walras-Pareto Fixation will have to give way, first slowly, then with increasing mo- mentum. "Free competition," now the center and starting point of economic theorizing, will be recognized as what it is: a pathological, limiting case of possible eco- nomic organization, millions of miles from any reality we have ever known through the ages. Curiously, Pareto himself has stated the matter concisely: "Free competition pro- duces the maximum of ophelimitk; free com- petition is the rule in our societies; these are two different propositions. The first is most likely true; the second is certainly false" [25, 11, p. 130, my translation]. I would say that the first is also false or at least unproven or unprovable.

In addition, just as utility theory-i.e., the textbook variant of indifference curve analy- sis-is completely deterministic, so is gen- eral equilibrium theory, although Arrow, Borch, and Debreu have made important dents into that structure. Let no one think that matters could be improved funda-mentally, i.e., made more realistic, merely by introducing stochastic considerations into the latter, interesting as the effort would b& Clearly, there is uncertainty about prices, about quantities produced, about demand, about stocks, etc. But this is not enough: apart from the random fluctuations that have to be considered for virtually any model (and hence, for any description of re- ality), it is the question of the acceptability of the model itself. Randomness of the above kind does not resolve the basic-game theo-retic-problem of how the interlocking ac- tions of the economic agents should be described and explored. To make the dis- tinction between the mere introduction of statistical uncertainties into the current Walrasian type general equilibrium theory and a proper treatment of uncertainties in man's behavior vis-ci-vis man by means of game theory completely, almost brutally clear, one cannot treat one's adversary in chess or poker statistically if one wishes to

prevail. Instead one must determine one's optimal strategy; and that is not a problem of finding maxima.

The fact that the theory of non-coopera- tive games with infinitely many players pro- duces results that correspond closely to the usual analysis of general economic equilib- rium is, of course, interesting and important -though, clearly, in reality there are never infinitely many players, this being strictly a mathematical hypothesis. In that there emerges a basic characteristic of Walrasian theory: it is forbidden-tacitly by Walras and his follower^!^-that consumers and pro- ducers cooperate with each other to in-crease their advantages. Such games are properly called "inessential." The truly in- teresting cases are those where cooperation takes place, whether with or without side- payments flowing among the participants. The strictly mathematical aspects of the re- lation of the two theories are of high inter- est, but this neither contributes to, nor de- tracts from, the overriding consideration that a model ultimately must conform to re- ality. A game of infinitely many non-cooper- ating players is an interesting mathematical construct; a Walrasian system of "perfect competition" is an economic aberration.

One principal reason for rejecting the study of more and more aspects of the "free competition" is that it cannot take care of the phenomenon of bargaining which per- vades all of economic life. Wherever bar- gaining occurs there is no "free competi- tion" in the sense of contemporary theory. Bargaining always takes place where the object to be sold or bought involves a sig- nificant part of one's patrimony or income. At a given level we do not bother to bar- gain, e.g., for a loaf of bread; but we d~ bargain when buying a car or a house. At

'But not by C. Menger who in 1871 specifically introduced the likelihood of cooperation and collusion! Unfortunately he did not pursue this matter any further.

1173 Morgenstern: Contemporary Economic Theory

other income levels other relationships pre- vail. The idea that the poor eastern trader "loves to bargain" is false: his bargaining even for "small" values is merely an expres- sion of his poverty.

If we look at any economy we see bar- gaining on all levels, whether it be wages, price contracts, private or government, and so on. Wages, in particular, are set by pro- longed negotiations and often involve mil- lions of persons. But a look at some leading textbooks on economic theory discloses that for example, hardly more than 1page (lit- erally!) out of 400 is devoted to bargaining and the word "wage" does not even occur in the index. What a change in the interest of economists! A few decades ago the prob- lems were price formation, income crea-tion, and distribution. There is more about this below in Point 9 where indifference curve analysis is discussed, where we find that there simply "exists" a price line. Indif- ference curves do not contribute anything to answering the question where these prices come from. Not one word about the extensive game-theoretic literature on bar- gaining, about the many, subsequent so-phisticated experiments, but merely the statement that it is a complex phenomenon, which is indeed true and which is a reason why it should excite the interest of theo- rists. The presentation of the contract curve helps, but does not exhaust the matter; that analysis, by Edgeworth in 1881, was how- ever already contained in Menger's work of 1871. Do we stop at this point? Frequently also the impression is given that the "inde- terminacy" of the price is an inadequacy of the theory while in fact it is a fundamental feature of social and economic organization.

I do not intend to give here an exhaustive list of objections to the current general equilibrium theory. I shall only mention two: first there is the fact that the forma- tion of prices is not explained, as mentioned above. Explanation of price formation is surely a task for economic theory. In cur-

rent theory prices simply exist-some are equilibrium prices, others are not. If not, the adjustments are supposed to occur which will certainly lead to equilibrium ei- ther by tdtonnement or in time. Tdtonne- ment has been discussed above. So a few words about the treatment of time, the sec- ond comment on general equilibrium the- ory is appropriate.

In the standard treatment of general equilibrium there is nothing explicit about the speed with which processes run their course. The topic is clearly a vast one. Some economists have worried about it, e.g., a long time ago, the much neglected H. L. Moore; but there still is no deliberate, ex- plicit, and comprehensive incorporation of time intervals into the body of contempo- rary theory, excepting, of course, where in- terest appears. But time is a factor in util- ity, in value, in savings, in expectations, in storage, in the very notion of a durable good. Time is an element in the adjustment of demand to changing prices (4.Point 8 below). It seems doubtful whether an eco- nomic theory can be fashioned which does not either consider time explicitly with all its complications due to its pervasiveness, or which openly abstracts from the time factor, e.g., by accepting the fiction of infi- nitely fast adjustments to all variations. The latter may be an acceptable methodological procedure provided one is interested in de- termining whether such a model is at all logically possible, and its empirical rele- vance is a subsidiary consideration. This is a sound sequence of model buildup.

What is not satisfactory is to have a mix- ture of phenomena for which time is con- sidered explicitly and with varying assump- tions, and of phenomena where time is ne- glected though clearly and powerfully pres- ent. This is the present state. Viewed as transitory, little harm may be done, but there ought to be evidence of effort to pro- ceed to the study of the effects of the time factor in those areas where it so far has

1174 Journal of Economic Literature

been neglected, e.g., demand theory, (c f . Point 8) .

In summa, the presentation of the econ- omy as one in which there is "free competi- tion" of the kind discussed above, no coop- eration, no antagonism-where all this is relegated to oligopoly as an anomalous situ- ation-is like giving a theory of the solar system without gravitation. I t is Hamlet without Hamlet. No wonder this kind of theory is helpless in the face of reality. How can students, who often have a good sense of reality, be attracted to this science? I t would be a different matter if theory were presented as a hypothetical first approach, in which one tries to determine whether such a model is at all possible, and were to go on from there rapidly to situations and models which better correspond to reality. However, this sequence does not work. In- stead one will have to start the other way around: begin with 2, 3 . . . agents in the market and arriving at arbitrarily large numbers only as a limiting case. Using se- vere, additional assumptions, one might reach the extreme, hypothetical situation which is now the center of theory rather than a remote possibility, as well as of less intellectual interest, and perhaps difficulty, than the cases of smaller numbers of agents.

Finally, these systems are supposed to be in stable equilibrium. One can only marvel at the audacity and confidence with which statements about the stability of all sorts of economic systems are made. Is it not inter- esting to recall that we cannot yet prove that the orbit of the moon around the earth is stable-a much simpler system than that of, say, the American economy?

6. Allocation of Resources

I t is the tenet of current theory that the market, and the market alone, allocates re- sources optimally, presumably under "free competition." If this is to be a description of reality it overlooks the existence of monop-

oly, duopoly, and oligopoly; I fail to see proofs of the existence of general equilibria incorporating these market forms in various arbitrary admixtures. Furthermore, there exist what Italian economists have called "prezzi politici," i.e., prices formed by polit- ical processes. Consider these briefly re-garding allocation. Economic theory as-sumes that allocation of resources is only through markets and that this assumption holds (implicitly) even if there were the above mentioned mixtures of market forms. This view completely overlooks the exis- tence of governments, national and local, where allocations are made not through the medium of markets but by means of voting as recently stressed in the generally splen- did paper by Martin Shubik [32, 19701. Congress, parliaments, governments vote Izow much is to be invested in capital goods, when and where the investment should take place. They vote the income of millions of persons, (government employ- ees, the military personnel, welfare recipi- ents, etc.). Clearly the movement of these funds-a respectable percentage of national income-sets forth flows of money, deter- mines demand, influences prices and thus affects the "free economy sector" of the whole economy with its prices, incomes, al- locations.

Now it is obviously necessary to expand and deepen the theory of voting just as we try to form a theory of pricing and income formation in the classical sense. Hence, at- tention should be paid to voting procedures which also are of importance for explaining the operation of boards of directors of com- panies-not only in government.

We thus need studies starting with Con- dorcet and leading to the theory of a multi- tude of majority games where votes may even be bought, etc. I t is clear that the goals and methods in these games differ substantially from those describing com-petitive pricing. I t will be very difficult to

Morgenstern: Contemplorary Economic Theory

combine these two worlds into one. The sci- ence of public finance continues to lead a kind of solitary existence of its own. Many novel ideas there, developed over the last few decades, ought to be incorporated into the general economic theory.

There are also allocations-again affect-ing income formation-by chance (e.g., stock market, inheritance, gifts, etc.); or by technological-scientific progress (when certain processes become obsolete and en- tirely new ones become possible). Some of these are compatible with static theory, others have a dynamic element.

Optimal allocation is a conceptually sim- ple matter for the consumer or the firm when they think that they have completely fixed conditions, both present and future. All they have to do then is to equate mar- ginal costs and marginal benefits because these concepts are applicable then, but only then. This may be computationally of phe- nomenal difficulty, but logically there is no problem of any complication. However, this is not the world we live in. Rather, alloca- tions are made in the face of "others" who are also trying to allocate optimally, all in- teracting with each other in various ways. Once this fact is realized, a different struc- ture emerges and optimal allocation poses new intriguing problems. It may suffice here to indicate that they exist [23, 19731.

In brief, there is good reason to return to the older notion of political economy as a more adequate discipline for our world than mere economics.

7. Substitution

A universal principle in economic theory is that goods that are substitutable for each other (either different units of the same good, or different goods in suitably differ- ent quantities) must have the same value.

In evaluating this basic generally ac-cepted principle it suffices to show one counter-example where this principle does

not hold. For each case where it is being applied, it will then be necessary to prove that the unique assignments of values to substitutable units are possible.

The following is one of several counter examples: (i.e., one of several black swans to disprove the universal statement that all swans are white): A simple majority game of six players 1, 2, . . . 6 exists which has the symbol [W, W, W, 1, 1, 11, 1 < W < 3 (which means that the weight W given to each of the first three players, is insufficient to override an overall majority, the last three players having each a weight of 1 ) . Various productive combinations are formed (i.e., of "players," who are simply the owners or rep- resentatives of services or goods) and these are called "winning."

The following three sets S,, S,, S, of pro- ductive combinations result:

s,: (1 ,2 ,3) S,: (a, b, h ) where a, b are any two of

1, 2, 3; h = 4 or 5 or 6 S,: (a, 4, 5, 6 ) where a = 1or 2 or 3.

It has been proved that games of this type have a "main simple solution," which states that the payoff of the winners is equal to the total number of players, in this case = 6.

We thus have three equations:

El: XI + XP + ~3 = 6 E z :X, + xi, + ~ h = 6 \a, 6, h E 3 : x , + x 4 + x j + x 6 = 6 {asabove.

These equations have no solution. S, shows that 4, 5, 6 can be substituted for each other which gives them the same value. S3 shows that 1,2, 3 can be substituted for each other which gives them the same value.

But: S, and S, show that one of 1,2, 3 can be substituted for one of 4, 5, 6.

S, and S, show that one of 1, 2, 3 can be substituted for two of 4,5,6.

This means that there are no substitution rates of the asserted, conventional kind. What values can be assigned to each player

1176 Journal of Economic Literature

are due to the relations of players to each other, not to substitution. It might be possi- ble to define some "unprofitable uses" but this goes beyond the argument under dis- cussion. At any rate it is obvious that pro- ductive combinations of factors of this type can be envisaged which is all that is neces- sary to destroy the universality claim of what the substitution principle asserts. In fact, other combinations have also been studied which yield similar results [19, 1950 and 35, 19471 and the field is still wide open. What kind of substitutions of factors and services actually take place in eco-nomic processes is a quaestio facti. We have shown that a general assertion does not hold. From now on it is necessary to have far more specific assumptions in each case. The economist must examine concrete empirical cases which the theory is sup- posed to explain. This is as it should be. It follows that the notion of substitution is far more complicated and difficult, especially when discrete objects are involved, than contemporary economic theory asserts. Complementarity of value, having proved particularly intractable until a resolution was found in the form of the super-additive characteristic function of cooperative n-person games, is now joined by another equally important basic phenomenon that requires a new treatment.

8. Demand and Supply

This is a large field and I shall touch only briefly on a few items, demand having been examined in considerable detail in my pa- per, "Demand Theory Reconsidered [18, 1948 reprinted in 4a, Ekelund, et al., 19721 where the excellent detailed introductory paper by Ekelund-Furobotn-Gram should be consulted to see demand theory in its historical perspective [cf. also 30, Shubik, 1959 and 32, Shubik, 1970; 24, Nyblkn, 1951, and 27, Reichardt, 19621.

I shall start with the aggregate demand curve. One recalls Sraffa's [34] efforts in the

1920s to construct a non-additive supply curve, i.e., one where the individual supply curves of different producers of the same product are interdependent. He did not suc- ceed and I have yet to see anyone construct such a curve from individual supply curves as it should be done. A constructive device or procedure is necessary to be able to use aggregate supply and demand functions freely. Yet in all textbooks aggregate curves abound which either are (constructively) additive, or are merely postulated when they are not additive. A serious gap!

Assume aggregate demand curves to be additive-the textbook case. Now it ought to be clear that the same aggregate demand curve could be the sum of 2, or 3, or 4, or 1000 prospective buyers. No one will be able to deny that the markets which this ag- gregate demand curve supposedly describes have quite different properties depending on the number of buyers from which the aggregate curves are obtained by simple addition (which may be entirely unwar-ranted). Thus the elasticity of demand would differ even on these simple grounds (there are deeper reasons too: clearly, if there are only two buyers, we have a duop- sony; three, a triopsony, etc.). And how many sellers hide behind the aggregate supply curve? Which "intersects" the aggre- gate demand curve? Some buyers may only be in the market for one unit, others for several, some may have "elastic" and others inelastic demand functions, some markets may only be composed of buyers each buy- ing only one discrete unit per time unit (e.g., refrigerators, newspapers, etc.), while in other cases each buyer would buy alter- natively different quantities at different prices, etc, All this is submerged and unan- alyzed when only the aggregative demand curve is exhibited. Even the idea that there always must exist a market or aggregate de- mand curve of the ordinary kind is ques- tionable as the analysis of stockmarket transactions shows (cf . the 1964 article by

1177 Morgenstern: Contempo lrary Economic Theory

Godfrey, Granger, and Morgenstern [7, 19641 and the book by Granger and Mor- gensten [8, 19701,especially Chapter XI11 ) .

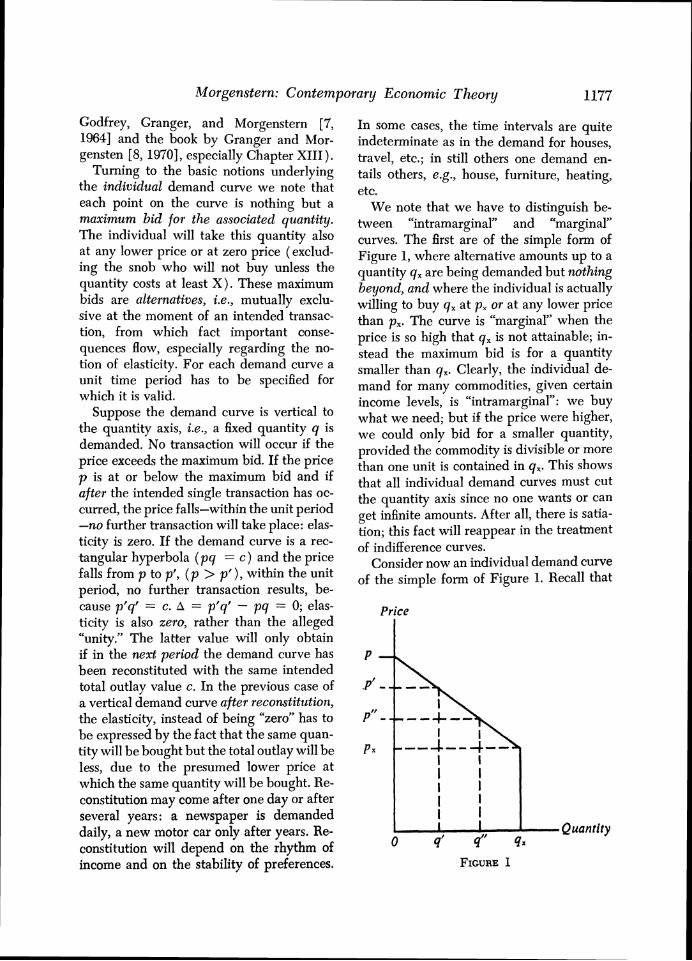

Turning to the basic notions underlying the individual demand curve we note that each point on the curve is nothing but a maximum bid for the associated quantity. The individual will take this quantity also at any lower price or at zero price (exclud- ing the snob who will not buy unless the quantity costs at least X) . These maximum bids are alternatives, i.e., nlutually exclu- sive at the moment of an intended transac- tion, from which fact important conse-quences flow, especially regarding the no- tion of elasticity. For each demand curve a unit time period has to be specified for which it is valid.

Suppose the demand curve is vertical to the quantity axis, i.e., a fixed quantity q is demanded. No transaction will occur if the price exceeds the maximum bid. If the price p is at or below the maximum bid and if after the intended single transaction has oc- curred, the price falls-within the unit period -no further transaction will take place: elas- ticity is zero. If the demand curve is a rec- tangular hyperbola ( p q = c ) and the price falls from p to p', ( p > p'), within the unit period, no further transaction results, be- cause p'q' = c. 4 = p'q' - pq = 0; elas-ticity is also zero, rather than the alleged "unity." The latter value will only obtain if in the next period the demand curve has been reconstituted with the same intended total outlay value c. In the previous case of a vertical demand curve after reconstitution, the elasticity, instead of being "zero" has to be expressed by the fact that the same quan- tity will be bought but the total outlay will be less, due to the presumed lower price at which the same quantity will be bought. Re- constitution may come after one day or after several years: a newspaper is demanded daily, a new motor car only after years. Re- constitution will depend on the rhythm of income and on the stability of preferences.

In some cases, the time intervals are quite indeterminate as in the demand for houses, travel, etc.; in still others one demand en- tails others, e.g., house, furniture, heating, etc.

We note that we have to distinguish be- tween "intramarginal" and "marginal" curves. The first are of the simple form of Figure 1,where alternative amounts up to a quantity q, are being demanded but nothing beyond, and where the individual is actually willing to buy q, at p, or at any lower price than p,. The curve is "marginal" when the price is so high that q, is not attainable; in- stead the maximum bid is for a quantity smaller than q,. Clearly, the individual de- mand for many commodities, given certain income levels, is "intramarginal": we buy what we need; but if the price were higher, we could only bid for a smaller quantity, provided the commodity is divisible or more than one unit is contained in q,. This shows that all individual demand curves must cut the quantity axis since no one wants or can get infinite amounts. After all, there is satia- tion; this fact will reappear in the treatment of indifference curves.

Consider now an individual demand curve of the simple form of Figure 1. Recall that

Price

Quantity

1178 Journal of Economic Literature

all points are alternative maximum bids valid within a given unit of time for the respective quantities. Assume the price p' to fall to p". The standard interpretation is that "now" the larger quantity q", associated with p", will be demanded. This is not so since in the quantity q" there is also contained q' < q" which has just been bought at price p' > p". If A = p"q" - p'q' > 0, then at price p" < p' not the quantity q" but another smaller quantity 0 i q * < q will be demanded. This is the true elasticity of demand in the case of an individual demand curve. The full amount q" associated with p" will only be demanded at the price p" if the demand curve has been reconstituted in the subse- quent time period. A reconstitution of indi- vidual demand will only happen if a need for more units of the commodity under con- sideration is combined with the availability of funds which may, for example, depend on the rhythm of income. Only after reconsti- tution does the conventional measure of elas- ticity apply.

I shall not carry out here the complicated analysis of elasticity for the case of general aggregate and additive, let alone non-addi- tive, demand curves [18, 19481. It is, how- ever, evident that the above derivation has to be carried out for each of the constituent individual demand curves to arrive at the true elasticity of the aggregate curve. Dif- ferent individuals will require varying time periods for reconstitution. The elasticity will be quite different from the standard elasticity which is measured without paying any attention to whether one deals with in- dividual or an aggregative demand curves nor of how many individuals the latter is made up, nor whether it was additively ar- rived at or consisted of interdependent, non-additive individual demand curves, etc.

Important consequences apply to the measurement of "consumers' surplus" which notion is obviously greatly affected by the above. Mutatis mutandis a similar argu-ment applies to cost and supply curves.

There additivity is an even less plausible assumption than for demand. This shall not be followed up here any further.

Apart from the question of additivity, or sub- or superadditivity, the fundamental factor that emerges is time. What are the time periods involved in current theories? Are the "unit time periods" to which refer- ence is sometimes made in demand analysis all equal for the various individuals or even for each individual for different commodi- ties and services? Where is there clarity and explicit recognition of time, information, and of expectations?

What was said in this section can be pre- sented rigorously in mathematical language. Involved is a complicated problem of com- binatorics7 which has been thoroughly ex-amined by G. L. Thompson [34a, 19671.

9. Indifference curve analysis

Indifference curve theory is entirely de- terministic-a severe drawback even if there were no other objections. The theory can- not be made non-deterministic and retain its merely ordinal character. This was proved in the Appendix of Theory of games and economic behavior [35]. The resulting

'Karl Menger, in his important contribution [14] to the Menger Symposium at the University of Vienna, June-July 1971 (dedicated to his father's memory) stressed in particular the instability of the demand functions shown above as one of the more complicating elements in mathematical econo- mies.

I recall, with sadness, a comment made to me by the author of a well-known textbook. Upon being asked whether he accepted my analysis of demand theory as presented first in 1948, the reply was positive. He added that it would not be included in his advanced textbook because "it would upset too many things and be too disturbing, i.e., Dicta non movere." So much for the acceptance of new scientific results and for a truly scientific attitude.

Compare this with the attitude of von Neumann, who while teaching in 1931 a course on mathemat- ical logic and on the foundations of mathematics, read Kurt Godel's just ublished paper containing his famous undecidabiety theorem, walked into his class, and said: "Forget what I taught you. It was all wrong. I shall only teach you what Cadel has just published."

1179 Morgenstern: Contemporary Economic T h e o r y

ordering, though still complete, loses the Archimedean property, which means that utility differences would be infinite and that consequently no indifference curves can ex- ist at all. Of course, it is not clear why one should want to retain the clumsy indiffer- ence curve analysis when, in fact, one has derived a numerical utility-up to a positive linear transformation-precisely taking the all-pervading element of uncertainty into account.

The follou~ing, however, is immanent criticism and refers to the deterministic sit- uation.

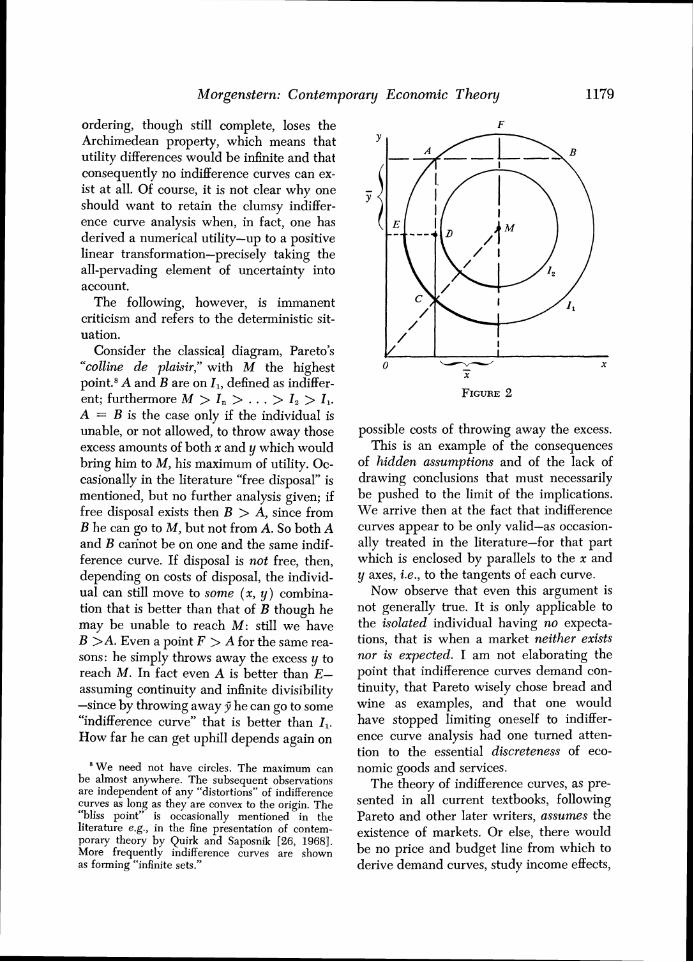

Consider the classical diagram, Pareto's "colline de plaisir," with M the highest point.8A and B are on I,, defined as indiffer- ent; furthermore M > I, > . . . > I , > I,. A = B is the case only if the individual is unable, or not allowed, to throw away those excess amounts of both x and y which would bring him to M, his maximum of utility. Oc- casionally in the literature "free disposal" is mentioned, but no further analysis given; if free disposal exists then B > A, since from B he can go to M, but not from A. So both A and B cannot be on one and the same indif- ference curve. If disposal is not free, then, depending on costs of disposal, the individ- ual can still move to some ( x , y ) combina-tion that is better than that of B though he may be unable to reach M: still we have B >A. Even a point F > A for the same rea- sons: he simply throws away the excess y to reach M. In fact even A is better than E-assuming continuity and infinite divisibility -since by throwing away 9 he can go to some "indifference curve" that is better than I,. How far he can get uphill depends again on

W e need not have circles. The maximum can be almost anywhere. The subsequent observations are independent of any "distortions" of indifference curves as long as they are convex to the origin. The "bliss point" is occasionally mentioned in the literature e.g., in the fine presentation of contem- porary theory by Quirk and Saposnik [26, 19681. More frequently indifference curves are shown as forming "infinite sets."

possible costs of throwing away the excess. This is an example of the consequences

of hidden assumptions and of the lack of drawing conclusions that must necessarily be pushed to the limit of the implications. We arrive then at the fact that indifference curves appear to be only valid-as occasion-ally treated in the literature-for that part which is enclosed by parallels to the x and y axes, i.e., to the tangents of each curve.

Now observe that even this argument is not generally true. It is only applicable to the isolated individual having no expecta-tions, that is when a market neither exists nor is expected. I am not elaborating the point that indifference curves demand con- tinuity, that Pareto wisely chose bread and wine as examples, and that one would have stopped limiting oneself to indiffer- ence curve analysis had one turned atten- tion to the essential discreteness of eco-nomic goods and services.

The theory of indifference curves, as pre- sented in all current textbooks, following Pareto and other later writers, assumes the existence of markets. Or else, there would be no price and budget line from which to derive demand curves, study income effects,

1180 Journal of E conornic Literature

and the like. These lines are simply given. There is no explanation of the formation of prices which remains mysterious. However, there is an implicit argument: the consumers buy or exchange according to their income position, as an (x, , yo) combination in their indifference map, using an existing price sys- tem. However, this price system depends on the choices of precisely these same con- sumers. Such implict theorizing is possible, as is shown in von Neumann's model of a uniformly expanding economy. But the mathematical difficulties then are formida- ble and exceed the tools used in discussing prices and incomes found in current text- books; neither do the textbooks give a hint where the student reader can acquire that knowledge.

Turning now to the expectation vs. t he existence of a market: in Figure 2, A will be preferred to E though both are on the same indifference curve I , because the disposal of some y will bring the individual to a higher indifference curve, say to D on I* > I,.But if a market is expected to emerge (within a "reasonable" time limit! ) this disposal will not take place, since-depending on the ex- pected prices-the individual will expect to be able, by trading y for x, to move to a still higher I"" > I*, possibly even to M. Hence A will be preferred to whatever point can be reached even by free disposal! Suppose the individual is at F or B (Figure 2 ) . Then it appears that any emerging price x : y is ir- relevant since he can at any rate go directly to M by throwing away appropriate amounts of y. However, even this does not exhaust the possibilities: each of these points may have a different value for him if he expects (or there exists) a market for whatever excess of x and y, that he can trade for commodities other than x or y which he also desires. This then links the satisfaction he gets from ( x , y ) combinations to those also involving u, v, w, . . . ,not demonstrable in this two-dimen- sional set-up.

Note that when, given a market and a

budget line, a decrease of the price of x is expected, the individual win not move au- tomatically along the given budget line, as is asserted, but rather wait (how long?) un- til he can exploit the new opportunities.

Thus it suffices to introduce expectations to reach conditions which differ from the case of the isolated individual having no expectations; but how could an individual not have expectations of his future states? If he has expectations of obtaining additional quantities of x or y he is not indifferent among the points of any given curve, de- pending on which other point he may be able to reach, from whatever point he is at. We have seen that, when there are no expec- tations, point A (Fig. 2 ) is better than C, i.e., A > C, because from A point D, which is on a higher indifference curve than either A or C or E, can be reached. If there are gx-pectations of obtaining some specific quan- tity F (marked on Fig. 2 ) then clearly from D the individual reaches M, his desired max- imum. Given this expectation of Zthe points between the tangents of I, (which are par- allel to the x and y axes) are then no longer indifferent: Indeed, E > C since, with the expected addition of x to the respective amounts of x associated with positions E and C, new indifference curves will be reached. This would bring the individual from E to a higher new indifference curve than from C.9 Hence, given this expectation, E is pre- ferred to C which contradicts the statement that points on the same indifference curve between the above mentioned tangents are equal to each other, i.e., that the individual does not care where he is between those tan- gents along the "indifference" curve I,. (When the expectation is for obtaining y, instead of x, the converse of the above argu- ment applies.)

Complete complementarity is shown by

Clearly, when the supposed indifference map is not of the classical Pareto shape of Fig. 2 but de- formed, somewhat different observations follow without, however, invalidating the main argument.

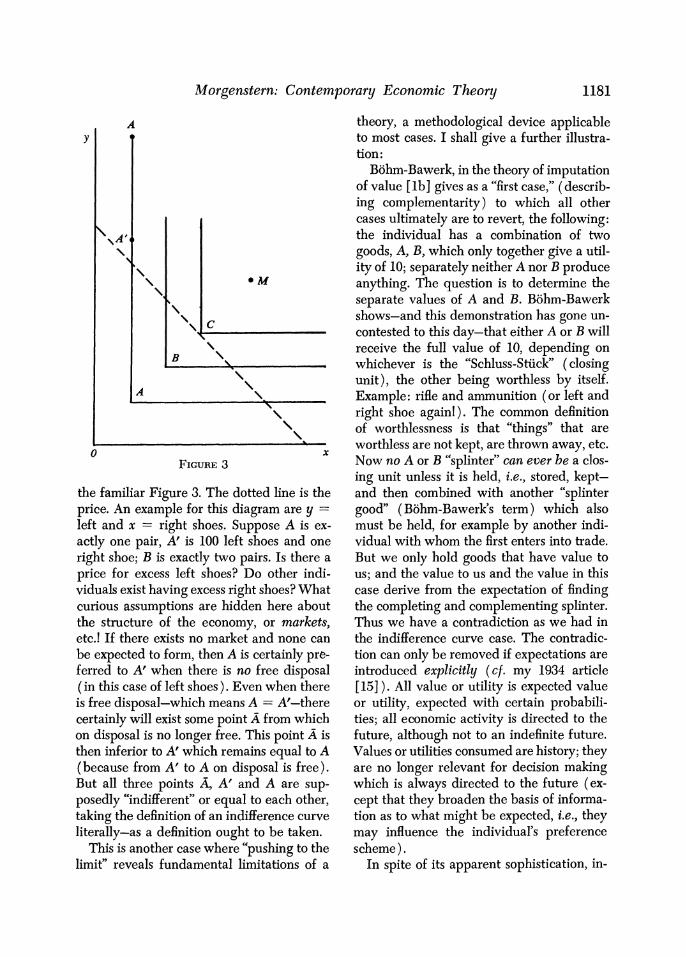

1181 Morgenstern: Contemporary Economic Theory

the familiar Figure 3. The dotted line is the price. An example for this diagram are y = left and x = right shoes. Suppose A is ex- actly one pair, A' is 100 left shoes and one right shoe; B is exactly two pairs. Is there a price for excess left shoes? Do other indi- viduals exist having excess right shoes? What curious assumptions are hidden here about the structure of the economy, or markets, etc.! If there exists no market and none can be expected to form, then A is certainly pre- ferred to A' when there is no free disposal (in this case of left shoes). Even when there is free disposal-which means A = A'-there certainly will exist some point A from which on disposal is no longer free. This point A is then inferior to A' which remains equal to A (because from A' to A on disposal is free). But all three points A, A' and A are sup- posedly "indifferent" or equal to each other, taking the definition of an indifference curve literally-as a definition ought to be taken.

This is another case where "pushing to the limit" reveals fundamental limitations of a

theory, a methodological device applicable to most cases. I shall give a further illustra- tion :

Bohm-Bawerk, in the theory of imputation of value [ lb ] gives as a "first case," (describ- ing complementarity) to which all other cases ultimately are to revert, the following: the individual has a combination of two goods, A, B, which only together give a util- ity of 10; separately neither A nor B produce anything. The question is to determine the separate values of A and B. Bohm-Bawerk shows-and this demonstration has gone un- contested to this day-that either A or B will receive the full value of 10, depending on whichever is the "Schluss-Stiick" (closing unit), the other being worthless by itself. Example: rifle and ammunition (or left and right shoe again! ) . The common definition of worthlessness is that "things" that are worthless are not kept, are thrown away, etc. Now no A or B "splinter" can ever be a clos- ing unit unless it is held, i.e., stored, kept- and then combined with another "splinter good" (Bohm-Bawerk's term) which also must be held, for example by another indi- vidual with whom the first enters into trade. But we only hold goods that have value to us; and the value to us and the value in this case derive from the expectation of finding the completing and con~plementing splinter. Thus we have a contradiction as we had in the indifference curve case. The contradic- tion can only be removed if expectations are introduced explicitly ( c f . my 1934 article [15] ). All value or utility is expected value or utility, expected with certain probabili- ties; all economic activity is directed to the future, although not to an indefinite future. Values or utilities consumed are history; they are no longer relevant for decision making which is always directed to the future (ex- cept that they broaden the basis of informa- tion as to what might be expected, i.e., they may influence the individual's preference scheme ) .

In spite of its apparent sophistication, in-

1182 Journal of Economic Literature

difference curve analysis is exceedingly primitive and vague in its assumptions and scope. Naturally it was a great step for Edgeworth and Irving Fisher to take, and I am the last to want to diminish their stat- ure,1° but since the 1880s a deeper insight into utility has developed; yet it is not re- flected in the development of that theory nor in "revealed preference."

The theory of expected utility, leading to a numerical concept, represents a new step from which many consequences derive. As the vast recent literature demonstrates, "utility" and "preference" are far more com- plicated phenomena than has so far been realized. It is difficult to see why indiffer- ence curve analysis should still fill our text- books when we can have a utility function allowing for uncertainty and when it fur- thermore has been proved, as mentioned above, that a non-numerical utility with al- lowance for uncertainty would lack the Ar- chimedean property, which then means that indifference curves do not exist [35, App.]. The textbooks, to save this old-fash- ioned tool, simply ignore uncertainty and expectation-as if there were no uncertainty in life, in planning, in setting prices, in profits, in behavior, etc!

The true complication of preference and utility would probably only be taken care of if preferences were viewed as forming (a t best) a partially ordered set (not as now assumed by virtually every economist, a completely ordered one), that has subsets, some with orderings which also possess the Archimedean property of continuity, others without it, some lexicographic, all, of course, allowing for the future, hence con- cerned with uncertain. prospects. This ap- pears to be a much finer representation of reality than what has so far been the object of study.ll It is evident that, given the

''Indeed, I believe Edgeworth in particular to have been one of the greatest economists and Fisher the most eminent of all past American ones.

"To get an idea of how complicated the whole field of preference analysis and utility theory is I