24

This Time is Different MARK ZANDI, CHIEF ECONOMIST FROM MOODY’S ECONOMY.COM

| Date post: | 24-Dec-2015 |

| Category: |

Documents |

| Upload: | leslie-lee |

| View: | 219 times |

| Download: | 0 times |

This Time is DifferentMARK ZANDI, CHIEF ECONOMIST

FROM MOODY’S ECONOMY.COM

'12q4 '13q1 '13q2 '13q3 '13q4 '14q1 '14q2 '14q3 '14q4-2.0

-1.5

-1.0

-0.5

0.0

Other Tax and SpendingPayroll TaxSequester

Fiscal Headwinds Are Blowing Hard…Real GDP growth impact of fiscal austerity, percentage points

Source: Moody’s Analytics

'05 '06 '07 '08 '09 '10 '11 '12 '13F '14F '15F-6-5-4-3-2-1012345

Private EconomyFederal Fiscal PolicyTotal

…But Will Fade Next Year…

Source: Moody’s Analytics

Contribution to real GDP growth, %

'10 '11 '12 '13 '14 '15 '16 '17 '18 '19 '20 '21 '2250%

55%

60%

65%

70%

75%

80%

85%

90%

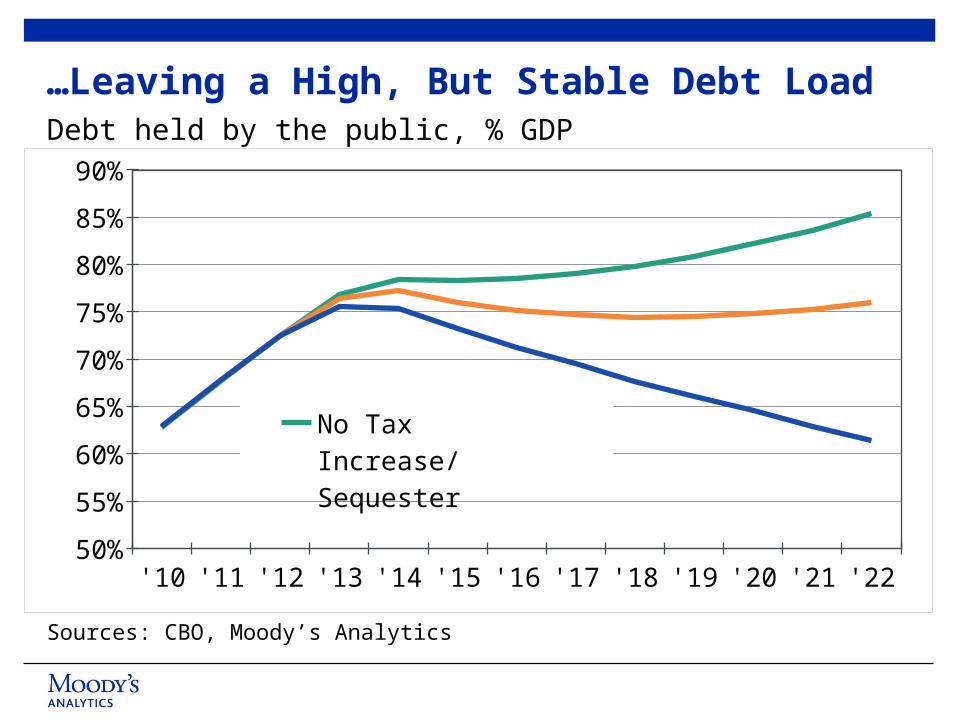

No Tax Increase/SequesterCurrent PolicySimpson-Bowles

…Leaving a High, But Stable Debt LoadDebt held by the public, % GDP

Sources: CBO, Moody’s Analytics

'45

'46

'47

'48

'49

'50

'51

'52

'53

'54

'55

'56

'57

'58

'59

'60

'61

'62

'63

'64

'65

'66

'67

'68

'69

'70

'71

'72

'73

'74

'75

'76

'77

'78

'79

'80

'81

'82

'83

'84

'85

'86

'87

'88

'89

'90

'91

'92

'93

'94

'95

'96

'97

'98

'99

'00

'01

'02

'03

'04

'05

'06

'07

'08

'09

'10

'11

'12

6

8

10

12

14

16

18

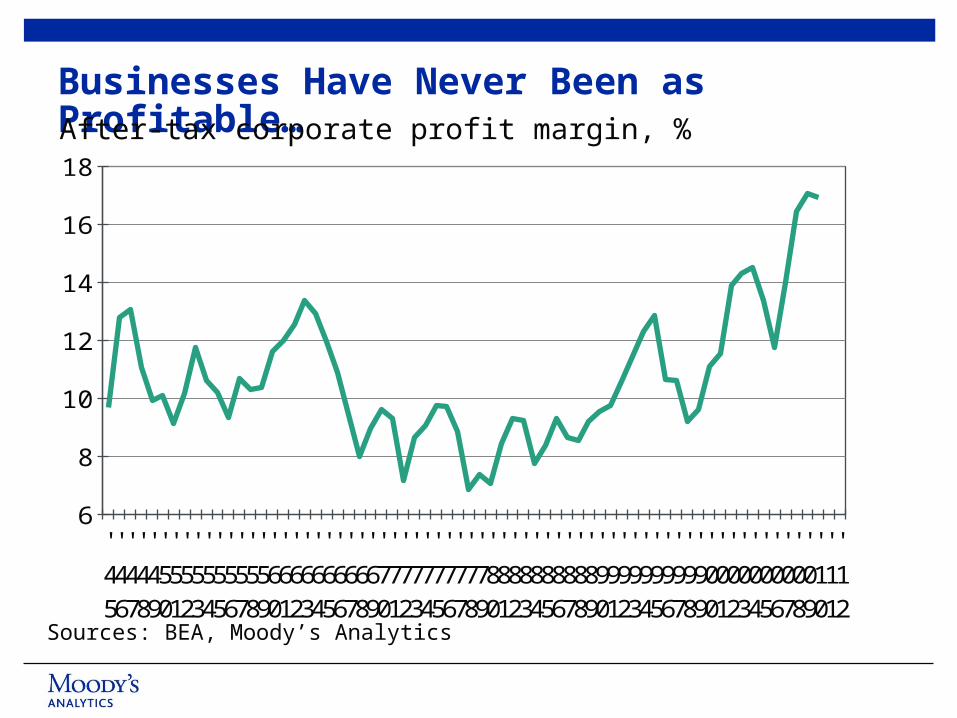

Businesses Have Never Been as Profitable…

Sources: BEA, Moody’s Analytics

After-tax corporate profit margin, %

8080:02:0080:03:0080:04:0081:01:0081:02:0081:03:0081:04:0082:01:0082:02:0082:03:0082:04:0083:01:0083:02:0083:03:0083:04:0084:01:0084:02:0084:03:0084:04:008585:02:0085:03:0085:04:0086:01:0086:02:0086:03:0086:04:0087:01:0087:02:0087:03:0087:04:0088:01:0088:02:0088:03:0088:04:0089:01:0089:02:0089:03:0089:04:009090:02:0090:03:0090:04:0091:01:0091:02:0091:03:0091:04:0092:01:0092:02:0092:03:0092:04:0093:01:0093:02:0093:03:0093:04:0094:01:0094:02:0094:03:0094:04:009595:02:0095:03:0095:04:0096:01:0096:02:0096:03:0096:04:0097:01:0097:02:0097:03:0097:04:0098:01:0098:02:0098:03:0098:04:0099:01:0099:02:0099:03:0099:04:000001020304050607080910'11'120

10

20

30

40

50

60

Interest coverage ratio

Quick ratio

…And Their Balance Sheets Are StrongNonfinancial corporate businesses

Sources: Federal Reserve, Moody’s Analytics

80 82 84 86 88 90 92 94 96 98 00 02 04 06 08 10 1210.0

10.5

11.0

11.5

12.0

12.5

13.0

13.5

14.0

14.5

15.0

15.5

16.0

16.5

17.0

17.5

18.0

18.5

19.0Debt service (L)Financial obligations (R)

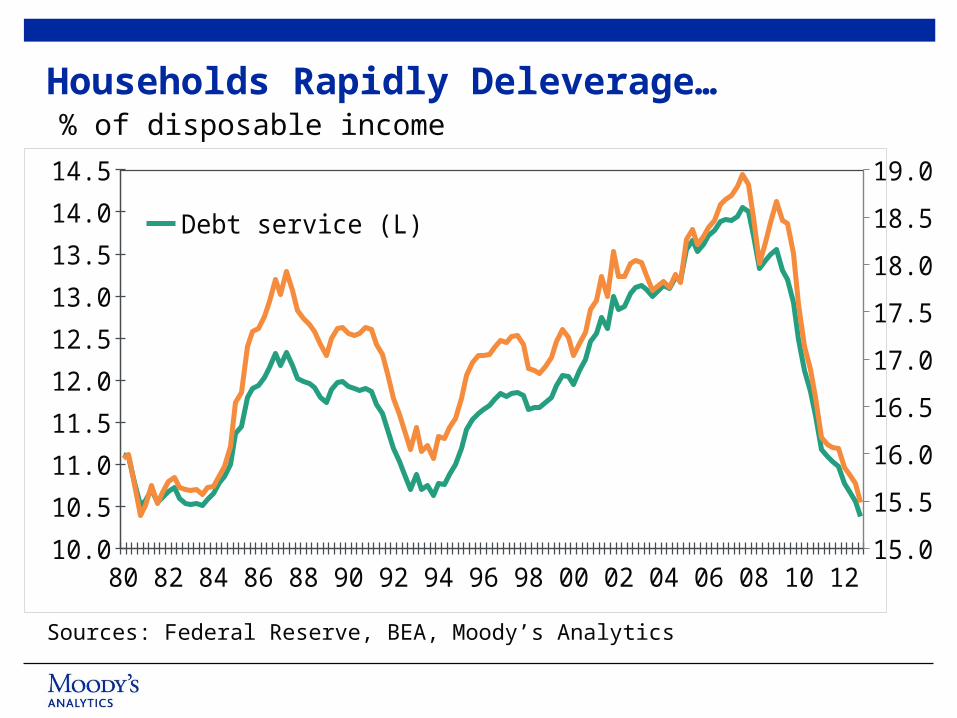

Households Rapidly Deleverage… % of disposable income

Sources: Federal Reserve, BEA, Moody’s Analytics

'06

6-Feb

6-Mar

6-Apr

6-May

6-Jun

6-Jul

6-Aug

6-Sep

6-Oct

6-Nov

6-Dec

077-Feb

7-Mar

7-Apr

7-May

7-Jun

7-Jul

7-Aug

7-Sep

7-Oct

7-Nov

7-Dec

'08

8-Feb

8-Mar

8-Apr

8-May

8-Jun

8-Jul

8-Aug

8-Sep

8-Oct

8-Nov

8-Dec

'09

9-Feb

9-Mar

9-Apr

9-May

9-Jun

9-Jul

9-Aug

9-Sep

9-Oct

9-Nov

9-Dec

'10

10-Feb

10-Mar

10-Apr

10-May

10-Jun

10-Jul

10-Aug

10-Sep

10-Oct

10-Nov

10-Dec

'11

11-Feb

11-Mar

11-Apr

11-May

11-Jun

11-Jul

11-Aug

11-Sep

11-Oct

11-Nov

11-Dec

'12

12-Feb

12-Mar

12-Apr

12-May

12-Jun

12-Jul

12-Aug

12-Sep

12-Oct

12-Nov

12-Dec

'13

13-Feb

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5Non First Mortgage

First Mortgage

30-90 Day Delinquency Rate, % of $, SA

Sources: Equifax, Moody’s Analytics

…And Right the Wrongs

'90

90:02:00

90:03:00

90:04:00

91:01:00

91:02:00

91:03:00

91:04:00

'92

92:02:00

92:03:00

92:04:00

93:01:00

93:02:00

93:03:00

93:04:00

'94

94:02:00

94:03:00

94:04:00

95:01:00

95:02:00

95:03:00

95:04:00

'96

96:02:00

96:03:00

96:04:00

97:01:00

97:02:00

97:03:00

97:04:00

'98

98:02:00

98:03:00

98:04:00

99:01:00

99:02:00

99:03:00

99:04:00

'00

0:02

0:03

0:04

1:01

1:02

1:03

1:04

'02

2:02

2:03

2:04

3:01

3:02

3:03

3:04

'04

4:02

4:03

4:04

5:01

5:02

5:03

5:04

'06

6:02

6:03

6:04

7:01

7:02

7:03

7:04

'08

8:02

8:03

8:04

9:01

9:02

9:03

9:04

'10

'11

'12

6.25

6.75

7.25

7.75

8.25

8.75

9.25

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

Core Capital Ratio (L)

Return on Assets (R )

Banks are Well Capitalized and More Profitable…Commercial banks

Source: FDIC

90Jan-00

Jan-00

Jan-00

Jan-00

91:02:00

91:03:00

91:04:00

9292:02:00

92:03:00

92:04:00

93:01:00

93:02:00

93:03:00

93:04:00

9494:02:00

94:03:00

94:04:00

95:01:00

95:02:00

95:03:00

95:04:00

9696:02:00

96:03:00

96:04:00

97:01:00

97:02:00

97:03:00

97:04:00

9898:02:00

98:03:00

98:04:00

99:01:00

99:02:00

99:03:00

99:04:00

000:02

0:03

0:04

1:01

1:02

1:03

1:04

022:02

2:03

2:04

3:01

3:02

3:03

3:04

044:02

4:03

4:04

5:01

5:02

5:03

5:04

066:02

6:03

6:04

7:01

7:02

7:03

7:04

088:02

8:03

8:04

9:01

9:02

9:03

9:04

1010:02

10:03

10:04

11

12

'13

-50

-40

-30

-20

-10

0

10

20

30

40

50

-80

-60

-40

-20

0

20

40

60

80

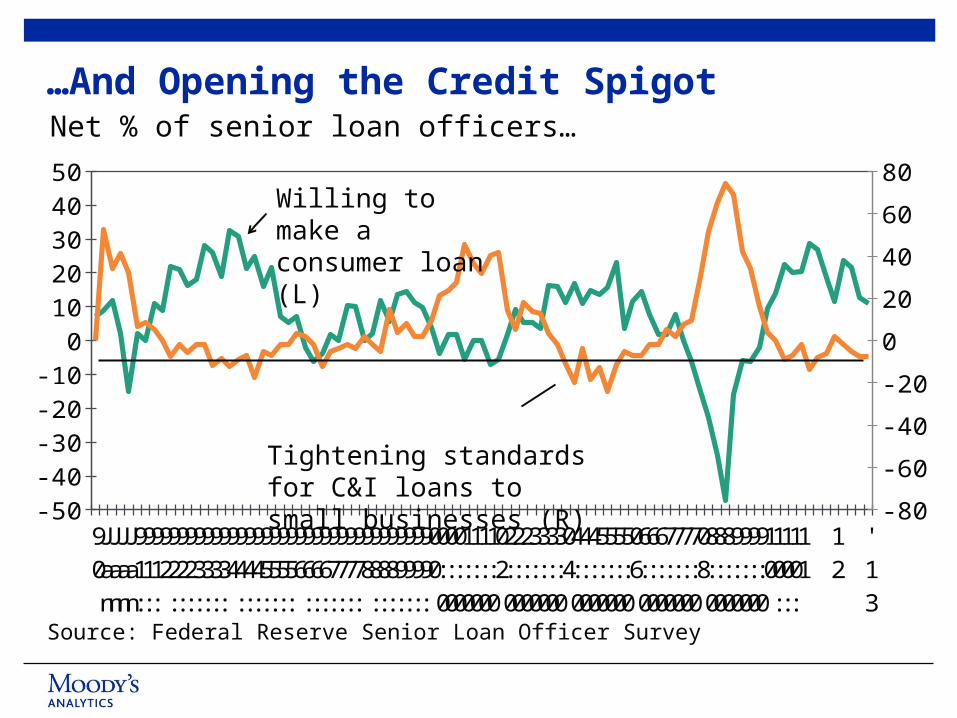

…And Opening the Credit Spigot

Source: Federal Reserve Senior Loan Officer Survey

Net % of senior loan officers…

Willing to make a consumer loan (L)

Tightening standards for C&I loans to small businesses (R)

90

91

92

93

94

95

96

97

98

99

00

01

02

03

04

05

06

07

08

09

10

11

12

-20

-10

0

10

20

30

40

50

60

Fairly valued

Housing Is Fairly Valued…

Sources: PPR, BEA, Census Bureau, Fiserv, Moody’s Analytics

% over- or undervalued

9090909091919191929292929393939394949494959595959696969697979797989898989999999900000000010101010202020203030303040404040505050506060606070707070808080809090909101010101111111112121212

5,500

6,500

7,500

8,500

9,500

10,500

11,500

Trend Vacancy

Sources: Census, Moody’s Analytics

Vacant homes for sale, for rent and held off market, ths

…And Will Soon Be Undersupplied…

Housing Supply 950,000 Single-family 600,000 Multifamily 300,000 Manufactured Housing 50,000

Housing Demand 1,800,000 Household Formations 1,250,000 Obsolescence 350,000 Second Homes 200,000

…Fueling a Big Turn in Housing’s Contribution…

96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15-2.5

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

Housing wealth effectResidential investmentTotal

Source: Moody’s Analytics

Contribution to real GDP growth, %

'05

5-Feb

5-Mar

5-Apr

5-May

5-Jun

5-Jul

5-Aug

5-Sep

5-Oct

5-Nov

5-Dec

'06

6-Feb

6-Mar

6-Apr

6-May

6-Jun

6-Jul

6-Aug

6-Sep

6-Oct

6-Nov

6-Dec

'07

7-Feb

7-Mar

7-Apr

7-May

7-Jun

7-Jul

7-Aug

7-Sep

7-Oct

7-Nov

7-Dec

'08

8-Feb

8-Mar

8-Apr

8-May

8-Jun

8-Jul

8-Aug

8-Sep

8-Oct

8-Nov

8-Dec

'09

9-Feb

9-Mar

9-Apr

9-May

9-Jun

9-Jul

9-Aug

9-Sep

9-Oct

9-Nov

9-Dec

'10

10-Feb

10-Mar

10-Apr

10-May

10-Jun

10-Jul

10-Aug

10-Sep

10-Oct

10-Nov

10-Dec

'11

11-Feb

11-Mar

11-Apr

11-May

11-Jun

11-Jul

11-Aug

11-Sep

11-Oct

11-Nov

11-Dec

'12

12-Feb

12-Mar

12-Apr

12-May

12-Jun

12-Jul

12-Aug

12-Sep

12-Oct

12-Nov

12-Dec

'13

13-Feb

6,000

6,500

7,000

7,500

8,000

8,500

9,000

9,500

122,000

124,000

126,000

128,000

130,000

Housing-Related (L)

Non Housing-Related (R )

…And More Job Growth

Source: Wall Street Journal, Moody’s Analytics

Millions of jobs

'96

'97

'98

'99

'00

'01

'02

'03

'04

'05

'06

'07

'08

'09

'10

'11

'12

8

10

12

14

16

18

20

-6

-4

-2

0

2

4

6

8

10

12

Units (L)Spent-up/pent-up demand (R)

Sources: BEA, Moody’s Analytics

Light vehicle sales, milPent-Up Demand Mounts

Trend sales

08394513945639461394643946939472394773948239485394903949339498395033950639511395143951939524395273953239535395403954539548395533955639561395663956939574395773958239587395903959539598396033960839611396163961939624396293963239637396403964539650396533965839661396663967139674396793968239687396923969539700397033970839713397163972139724397293973439737397423974539750397553975839763397663977139776397793978439787397923979739800398053980839813398183982139826398293983439839398423984739850398553986039863398683987139876398813988439889398923989739902399053991039913399183992339926399313993439939399443994739952399553996039965399683997339976399813998639989399943999740002400074001040015400184002340028400314003640039400444004940052400574006040065400704007340078400814008640091400944009940102401074011240115401204012340128401334013640141401444014940154401574016240165401704017540178401834018640191401964019940204402074021240217402204022540228402334023840241402464024940254402594026240267402704027540280402834028840291402964030140304403094031240317403224032540330403334033840343403464035140354403594036440367403724037540380403854038840393403964040140406404094041440417404224042740430404354043840443404484045140456404594046440469404724047740480404854049040493404984050140506405114051440519405224052740532405354054040543405481140556405614056440569405744057740582405854059040595405984060340606406114061640619406244062740632406374064040645406484065340658406614066640669406744067940682406874069040695407004070340708407114071640721407247/5/20117/8/20117/13/20117/18/20117/21/20117/26/20117/29/20118/3/20118/8/20118/11/20118/16/20118/19/20118/24/20118/29/20119/1/20119/6/20119/9/20119/14/20119/19/20119/22/20119/27/20119/30/201110/5/201110/10/201110/13/201110/18/201110/21/201110/26/201110/31/201111/3/201111/8/201111/11/201111/16/201111/21/201111/24/201111/29/201112/2/201112/7/201112/12/201112/15/201112/20/201112/23/2011121212121212121/26/20121/31/20122/3/20122/8/20122/13/20122/16/20122/21/20122/24/20122/29/20123/5/20123/8/20123/13/20123/16/20123/21/20123/26/20123/29/20124/3/20124/6/20124/11/20124/16/20124/19/20124/24/20124/27/20125/2/20125/7/20125/10/20125/15/20125/18/20125/23/20125/28/20125/31/20126/5/20126/8/20126/13/20126/18/20126/21/20126/26/20126/29/20127/4/20127/9/20127/12/20127/17/20127/20/20127/25/20127/30/20128/2/20128/7/20128/10/20128/15/20128/20/20128/23/20128/28/20128/31/20129/5/20129/10/20123.0

3.5

4.0

4.5

5.0

5.5

6.0

6.5

7.0

7.5

8.0

LTRO

LTRO

SMP

OTM

Sources: Bloomberg, Moody’s Analytics

Spanish 10-yr sovereign yields

Euro Zone Struggles To Hang Together

ECB Extraordinary Actions:

SMP = Securities market programLTRO = Long-term refinancing operationOTM = Outright monetary transaction

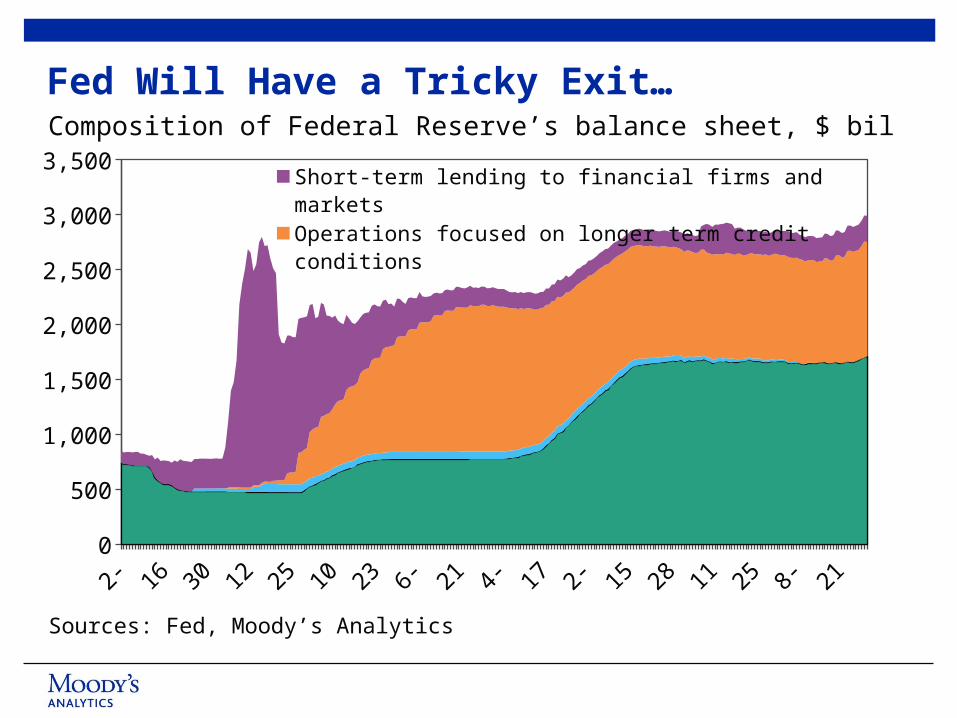

Fed Will Have a Tricky Exit…Composition of Federal Reserve’s balance sheet, $ bil

Sources: Fed, Moody’s Analytics

Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-130

500

1,000

1,500

2,000

2,500

3,000

3,500Short-term lending to financial firms and marketsOperations focused on longer term credit conditionsRescue operationsTraditional portfolio

'6060:02:0060:03:0060:04:0061:01:0061:02:0061:03:0061:04:0062:01:0062:02:0062:03:0062:04:0063:01:0063:02:0063:03:0063:04:0064:01:0064:02:0064:03:0064:04:00'6565:02:0065:03:0065:04:0066:01:0066:02:0066:03:0066:04:0067:01:0067:02:0067:03:0067:04:0068:01:0068:02:0068:03:0068:04:0069:01:0069:02:0069:03:0069:04:00'7070:02:0070:03:0070:04:0071:01:0071:02:0071:03:0071:04:0072:01:0072:02:0072:03:0072:04:0073:01:0073:02:0073:03:0073:04:0074:01:0074:02:0074:03:0074:04:00'7575:02:0075:03:0075:04:0076:01:0076:02:0076:03:0076:04:0077:01:0077:02:0077:03:0077:04:0078:01:0078:02:0078:03:0078:04:0079:01:0079:02:0079:03:0079:04:00'8080:02:0080:03:0080:04:0081:01:0081:02:0081:03:0081:04:0082:01:0082:02:0082:03:0082:04:0083:01:0083:02:0083:03:0083:04:0084:01:0084:02:0084:03:0084:04:00'8585:02:0085:03:0085:04:0086:01:0086:02:0086:03:0086:04:0087:01:0087:02:0087:03:0087:04:0088:01:0088:02:0088:03:0088:04:0089:01:0089:02:0089:03:0089:04:00'9090:02:0090:03:0090:04:0091:01:0091:02:0091:03:0091:04:0092:01:0092:02:0092:03:0092:04:0093:01:0093:02:0093:03:0093:04:0094:01:0094:02:0094:03:0094:04:00'9595:02:0095:03:0095:04:0096:01:0096:02:0096:03:0096:04:0097:01:0097:02:0097:03:0097:04:0098:01:0098:02:0098:03:0098:04:0099:01:0099:02:0099:03:0099:04:00'000:020:030:041:011:021:031:042:012:022:032:043:013:023:033:044:014:024:034:04'055:025:035:046:016:026:036:047:017:027:037:048:018:028:038:049:019:029:039:04'1010:0210:0310:0411:0111:0211:0311:0412:0112:0212:03-3

-2

-1

0

1

2

3

4

…Given the Overvalued Bond Market…

Source: Treasury, BEA, Moody’s Analytics

Difference between 10-yr Treasury yield and potential GDP growth

Undervalued

Overvalued

'8585:02:0085:03:0085:04:0086:01:0086:02:0086:03:0086:04:0087:01:0087:02:0087:03:0087:04:0088:01:0088:02:0088:03:0088:04:0089:01:0089:02:0089:03:0089:04:00'9090:02:0090:03:0090:04:0091:01:0091:02:0091:03:0091:04:0092:01:0092:02:0092:03:0092:04:0093:01:0093:02:0093:03:0093:04:0094:01:0094:02:0094:03:0094:04:00'9595:02:0095:03:0095:04:0096:01:0096:02:0096:03:0096:04:0097:01:0097:02:0097:03:0097:04:0098:01:0098:02:0098:03:0098:04:0099:01:0099:02:0099:03:0099:04:00'000:02:000:03:000:04:001:01:001:02:001:03:001:04:002:01:002:02:002:03:002:04:003:01:003:02:003:03:003:04:004:01:004:02:004:03:004:04:00'055:02:005:03:005:04:006:01:006:02:006:03:006:04:007:01:007:02:007:03:007:04:008:01:008:02:008:03:008:04:009:01:009:02:009:03:009:04:00'1010:02:0010:03:0010:04:0011:01:0011:02:0011:03:0011:04:0012:01:0012:02:0012:03:0012:04:000

2

4

6

8

10

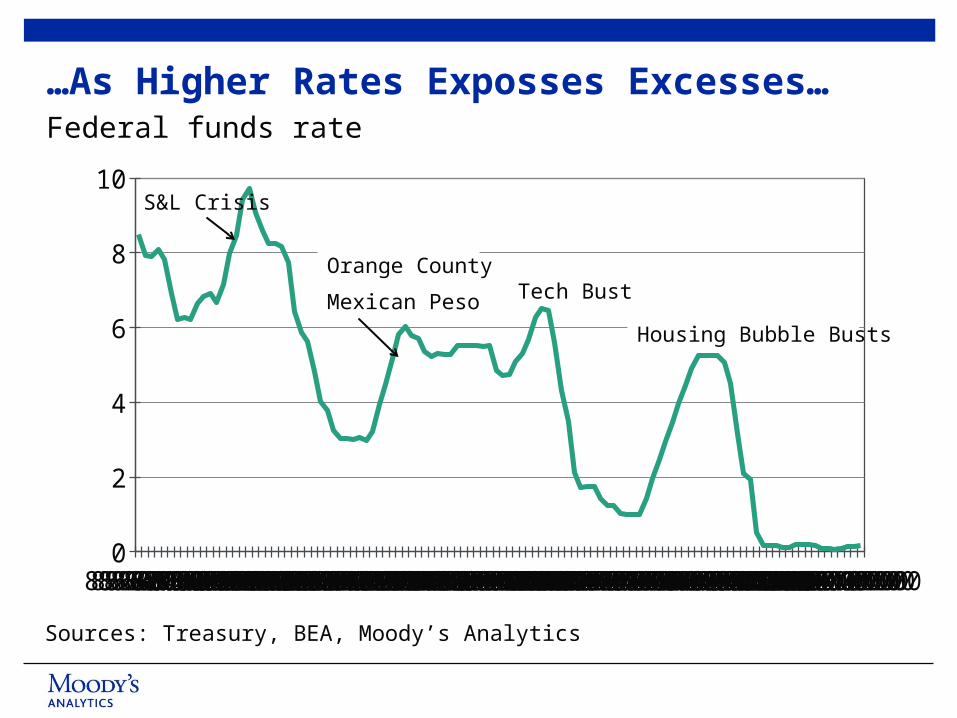

…As Higher Rates Exposses Excesses…

Sources: Treasury, BEA, Moody’s Analytics

Federal funds rate

S&L Crisis

Orange County

Mexican Peso Tech Bust

Housing Bubble Busts

'85 '87 '89 '91 '93 '95 '97 '99 '01 '03 '05 '07 '09 '1115

20

25

30

35

40

45

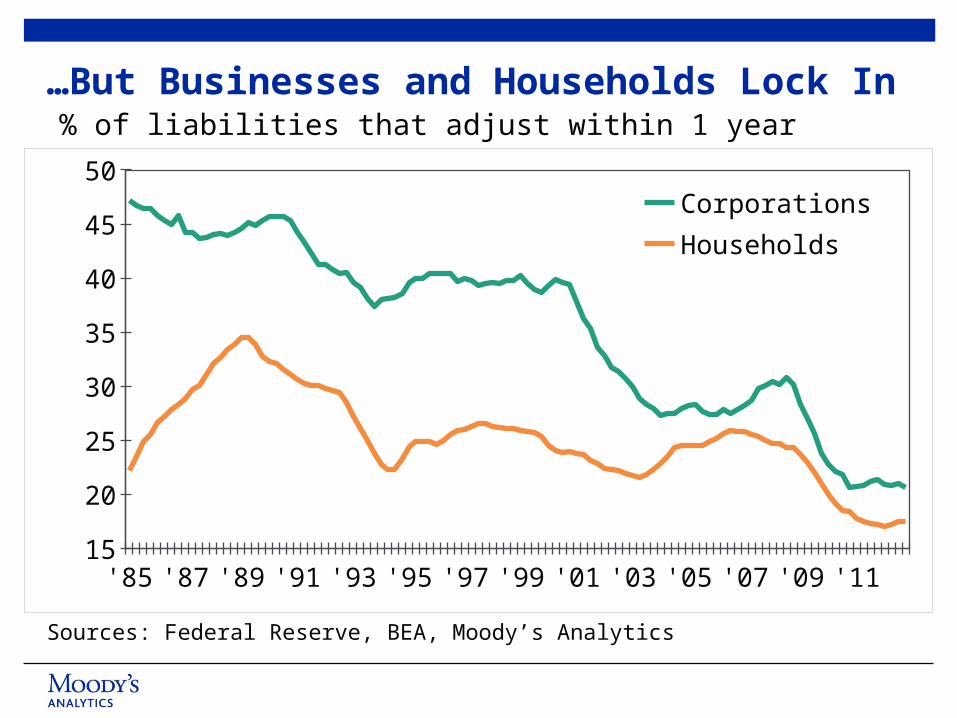

50Corporations

Households

…But Businesses and Households Lock In % of liabilities that adjust within 1 year

Sources: Federal Reserve, BEA, Moody’s Analytics

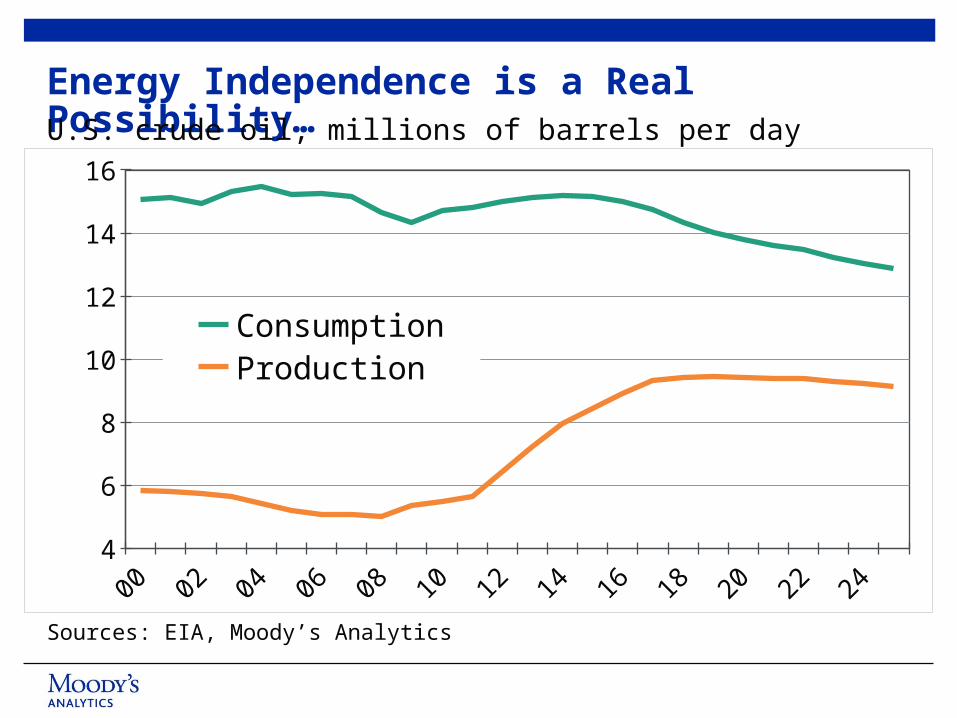

00010203040506070809101112131415161718192021222324254

6

8

10

12

14

16

ConsumptionProduction

Sources: EIA, Moody’s Analytics

Energy Independence is a Real Possibility…U.S. crude oil, millions of barrels per day

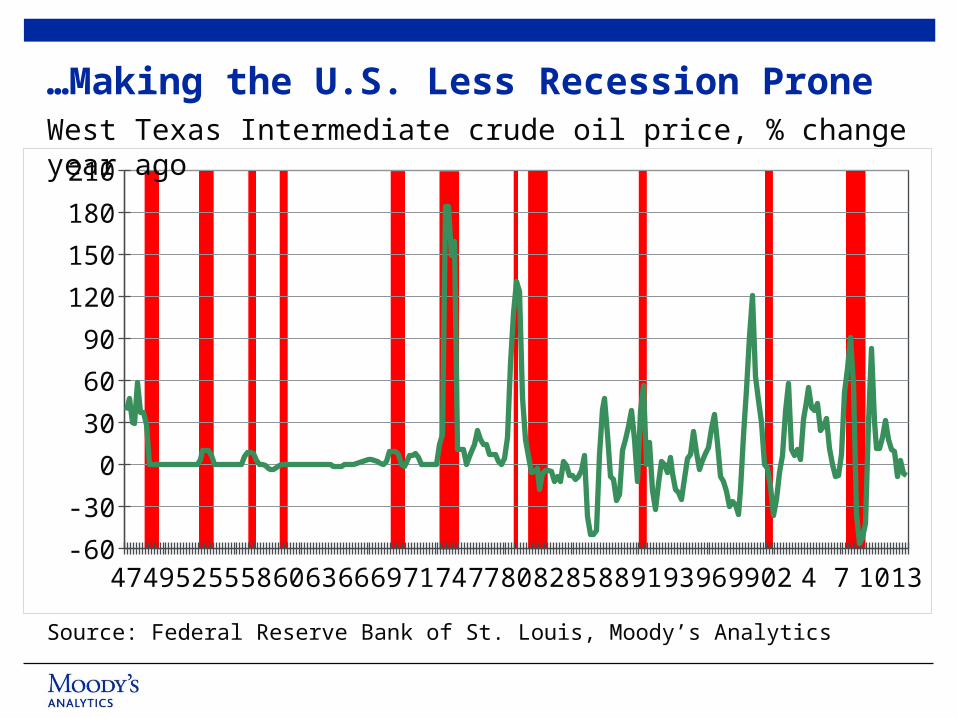

474952555860636669717477808285889193969902 4 7 1013-60

-30

0

30

60

90

120

150

180

210

…Making the U.S. Less Recession ProneWest Texas Intermediate crude oil price, % change year ago

Source: Federal Reserve Bank of St. Louis, Moody’s Analytics

www.economy.com121 North Walnut StreetSuite 500West Chester, PA 19380610.235.5299

2424

© 2012, Moody's Analytics, Inc. and/or its licensors and affiliates (together, "Moody's"). All rights reserved. ALL INFORMATION CONTAINED HEREIN IS PROTECTED BY COPYRIGHT LAW AND NONE OF SUCH INFORMATION MAY BE COPIED OR OTHERWISE REPRODUCED, REPACKAGED, FURTHER

TRANSMITTED, TRANSFERRED, DISSEMINATED, REDISTRIBUTED OR RESOLD, OR STORED FOR SUBSEQUENT USE FOR ANY PURPOSE, IN WHOLE OR IN PART, IN ANY FORM OR MANNER OR BY ANY MEANS WHATSOEVER, BY ANY PERSON WITHOUT MOODY'S PRIOR WRITTEN CONSENT. All

information contained herein is obtained by Moody's from sources believed by it to be accurate and reliable. Because of the possibility of human and mechanical error as well as other factors, however, all information contained herein is provided "AS IS" without warranty of any kind. Under no circumstances shall Moody's have any liability to any person or entity for (a) any loss or damage in whole or in part caused by, resulting from, or relating to, any error (negligent or otherwise)

or other circumstance or contingency within or outside the control of Moody's or any of its directors, officers, employees or agents in connection with the procurement, collection, compilation, analysis, interpretation, communication, publication or delivery of any such information, or (b) any direct, indirect, special,

consequential, compensatory or incidental damages whatsoever (including without limitation, lost profits), even if Moody's is advised in advance of the possibility of such damages, resulting from the use of or inability to use, any such information. The financial reporting, analysis, projections, observations, and other

information contained herein are, and must be construed solely as, statements of opinion and not statements of fact or recommendations to purchase, sell, or hold any securities. NO WARRANTY, EXPRESS OR IMPLIED, AS TO THE ACCURACY, TIMELINESS, COMPLETENESS, MERCHANTABILITY OR FITNESS

FOR ANY PARTICULAR PURPOSE OF ANY SUCH OPINION OR INFORMATION IS GIVEN OR MADE BY MOODY'S IN ANY FORM OR MANNER WHATSOEVER. Each opinion must be weighed solely as one factor in any investment decision made by or on behalf of any user of the information contained

herein, and each such user must accordingly make its own study and evaluation prior to investing.