Thomas Berry- Stölzle Hendrik Kläver Shen Qiu Terry College of Business University of Georgia Should Life Insurance Companies Invest in Hedge Funds? Financial support from the AXA Colonia-Studienstiftung im Stifterverband für die Deutsche Wissenschaft is gratefully acknowledged.

Transcript

Thomas Berry-Stölzle

Hendrik Kläver

Shen Qiu

Terry College of Business

University of Georgia

Should Life Insurance CompaniesInvest in Hedge Funds?

Financial support from the AXA Colonia-Studienstiftung im Stifterverband für die Deutsche Wissenschaft is gratefully

acknowledged.

T. Berry-Stölzle University of Georgia

1. Introduction

Agenda

2. Model

3. Simulation Results

4. Implications for Asset Management

5. Summary

T. Berry-Stölzle University of Georgia

The assets under management in the hedge fund industry rose from approximately $50 billion in 1990 to approximately $1 trillion by the end of 2004.

Hedge funds provide actively managed portfolios in publicly traded assets.

Hedge funds are free from the regulatory controls stipulated by the Investmant Company Act of 1940.

Free choice in the type of securities for investment as well as the type of positions. e.g., investment in derivatives, sell short or take on leveraged positions.

Potential to generate risk return profiles different from traditional asset classes.

1. Introduction

T. Berry-Stölzle University of Georgia

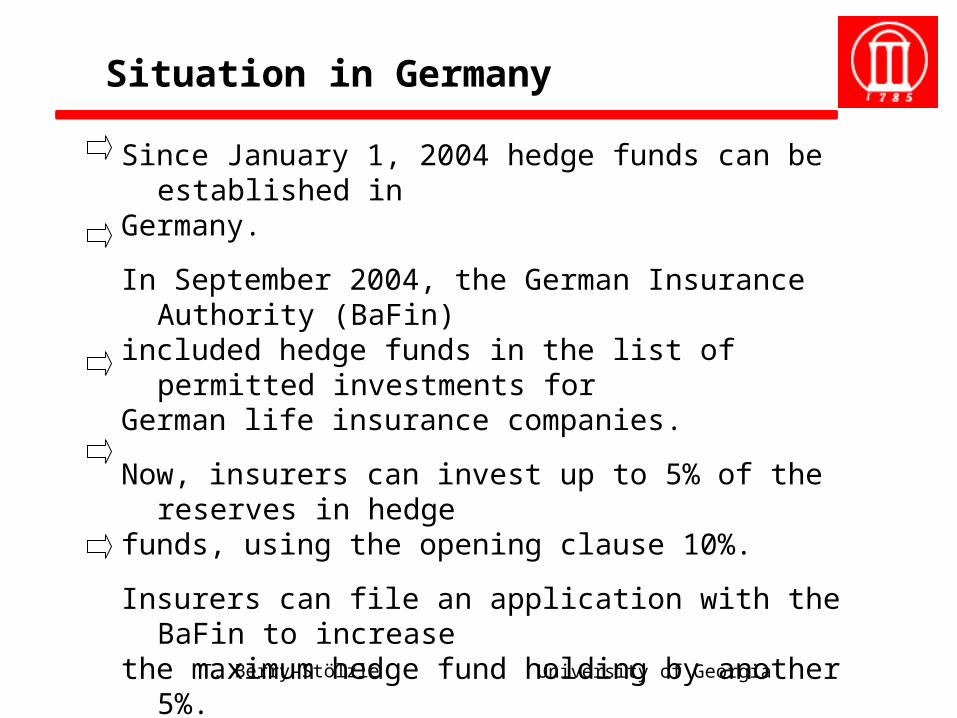

Since January 1, 2004 hedge funds can be established in Germany.

In September 2004, the German Insurance Authority (BaFin) included hedge funds in the list of permitted investments for German life insurance companies.

Now, insurers can invest up to 5% of the reserves in hedge funds, using the opening clause 10%.

Insurers can file an application with the BaFin to increase the maximum hedge fund holding by another 5%.

Insurers are not allowed to invest more than 35% of the reserves in „risky“ assets.

Situation in Germany

T. Berry-Stölzle University of Georgia

Should life insurers invest in hedge funds?

How much should they invest in hedge funds?

How does an insurance company’s liability structure affect investments in hedge funds?

Research Questions

T. Berry-Stölzle University of Georgia

Idea: Kling, Richter, and Ruß (2007) model the standard German life insurance product with all its guarantees. We extend their model on the asset side with 3 correlated AR(1) GARCH(1,1) processes.

Calibrate model to DAX, REXP, and hedge funds indices

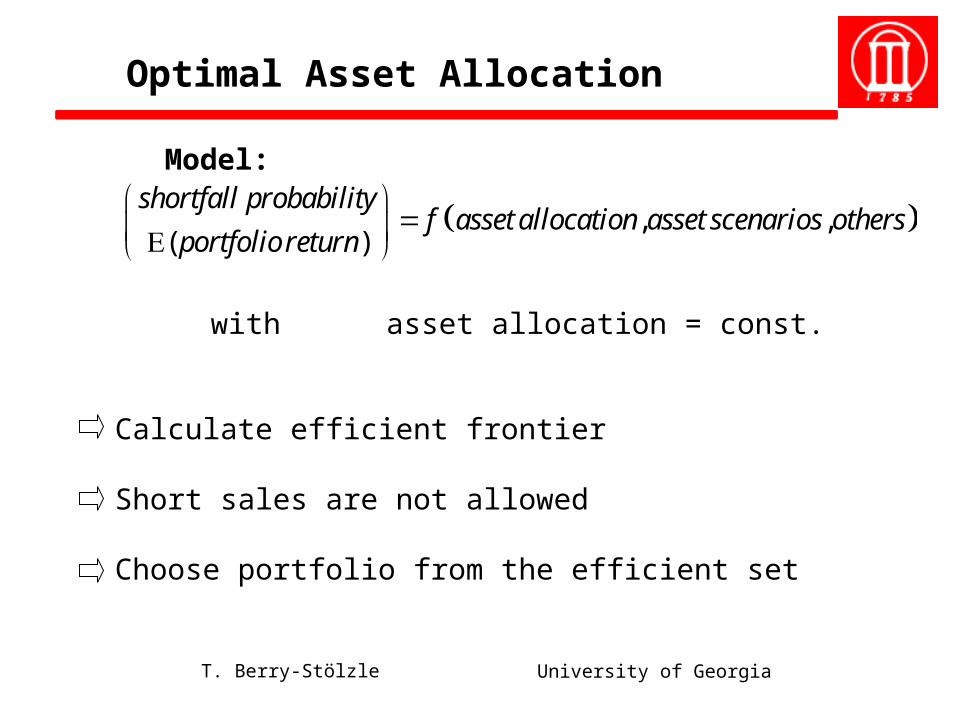

Analyze optimal asset allocation under various parameter settings applying Monte Carlo Simulations.

Method

T. Berry-Stölzle University of Georgia

2. Model

Balance Sheet Perspective:

Assets Liabilities

With: market value of assets

policy reserve / book value of liabilities

hidden reserves (+capital)

tA tL

tR

tAtA

tA

tL

tR

T. Berry-Stölzle University of Georgia

Three Assets: Stock, Bond, Hedge Fund

Each follows an AR(1) GARCH(1,1) process

Processes are correlated

Special case of Engle and Kroner (1995)

Limitation: Only one set of GARCH parameters for all three processes.

Assets

T. Berry-Stölzle University of Georgia

Insurance Contract:

Single-premium term-fix insurance (no charges)

Premium P is payed at t=0, benefit is payed at t=T

No mortality effects

Regulatory and Legal Requirements:

Minimum interest rate guarantee for whole policy period

Cliquet-style guarantee!

At least = 90% of asset returns have to be credited to the policyholders’ accounts (based on book values !)

Liabilities

T. Berry-Stölzle University of Georgia

Asset Valuation:

Hidden reserves: market value of assets exceeds book value

Insurers can reduce reserves immediately.

Increase of reserves subject to constraints (parameter y = 50%)

Profit Participation:

Usually German insurers credit a smoothed rate of interest to policyholders‘ accounts.

Management decision rule:

Credit target rate of interest z>g to policyholders, as long as the reserve quota stays within [a,b].