Professional Wealth Management Since 1901 Thomson Reuters Corporation (TRI) Shares of Thomson Reuters (“Thomson”) have faced a number of challenges over the last decade that have made the stock a frustrating investment for many Canadian investors. In the early part of this period, the bursting of the tech bubble led to severe employment declines in the financial services industry, which is a key end market for Thomson’s products. During the bull market of early 2003 through late 2007, Thomson’s shares performed well, rising from approximately US$25 to US$47 per share, or generally in line with the S&P 500. Unfortunately for Canadian investors, currency effects muted much of these gains as the Canadian dollar rose from multi-decade lows near US$0.63 to a peak well over par in the fall of 2007. Since that time, Thomson’s shares again came under pressure following the company’s US$16 billion acquisition of Reuters Group PLC, which was purchased at a relatively high valuation. Not long after the close of this transaction in the spring of 2008, the recent credit crisis set in, leading to another sharp decline in financial services employment and renewed challenges for Thomson. Despite these past challenges, Thomson currently offers an attractive investment opportunity considering the outlook for its financial performance in the coming years and its present valuation. Portfolio Advisory Group September 7, 2010 Company Overview Founded in 1934, Thomson has transformed itself over the last two decades from an old economy, print-based business into an electronic information provider serving professionals in the financial services, legal, tax & accounting, and healthcare & science sectors. Thomson was previously built on a group of newspaper holdings around the world, and over the years has held investments in various businesses including North Sea oil and leisure travel. In the 1990s, the company became increasingly focused on information services for professionals and made advances in this area through a series of acquisitions. With the divestiture of its newspapers and other non-core businesses, Thomson has migrated into a digital professional information franchise with approximately 90% of its revenues being electronic-based and 86% recurring through subscription-based customer relationships. In April 2008, Thomson’s acquisition of Reuters significantly increased the company’s exposure to the financial services industry, which now represents over half of the company’s revenues. Woodbridge, the investment holding company of the Thomson family, owns around 55% of Thomson’s shares. Thomson is organized into two divisions: (i) Markets, which consists of financial services and Media, and (ii) Professional, which consists of Legal, Tax & Accounting, and Healthcare & Science segments. Markets accounts for 58% of Thomson’s total revenues and 48% of its operating profit. This unit sells information, supporting technology, and infrastructure to the financial services industry with customers such as investment banks, brokerage houses and fund managers. Primary drivers of this business include: employment in the financial services industry, market volatility which drives 0% 25% 50% 75% 100% 125% 150% 175% 200% Jan-00 Jul-00 Jan-01 Jul-01 Jan-02 Jul-02 Jan-03 Jul-03 Jan-04 Jul-04 Jan-05 Jul-05 Jan-06 Jul-06 Jan-07 Jul-07 Jan-08 Jul-08 Jan-09 Jul-09 Jan-10 Jul-10 Prices rebased to Jan 1, 2000 Thomson (C$) Thomson (US$) S&P 500 TSX Relative Price Performance (2000-2010) Source: Bloomberg

Transcript

Professional Wealth Management Since 1901

Thomson Reuters Corporation (TRI)

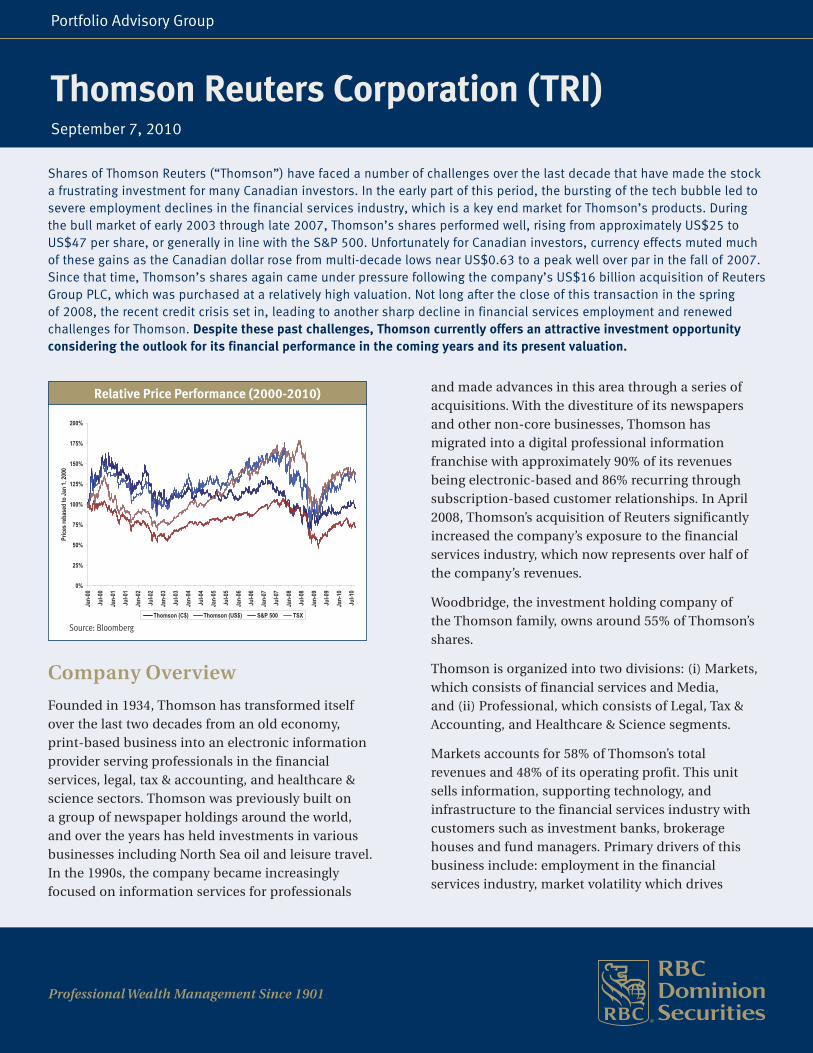

Shares of Thomson Reuters (“Thomson”) have faced a number of challenges over the last decade that have made the stock a frustrating investment for many Canadian investors. In the early part of this period, the bursting of the tech bubble led to severe employment declines in the financial services industry, which is a key end market for Thomson’s products. During the bull market of early 2003 through late 2007, Thomson’s shares performed well, rising from approximately US$25 to US$47 per share, or generally in line with the S&P 500. Unfortunately for Canadian investors, currency effects muted much of these gains as the Canadian dollar rose from multi-decade lows near US$0.63 to a peak well over par in the fall of 2007. Since that time, Thomson’s shares again came under pressure following the company’s US$16 billion acquisition of Reuters Group PLC, which was purchased at a relatively high valuation. Not long after the close of this transaction in the spring of 2008, the recent credit crisis set in, leading to another sharp decline in financial services employment and renewed challenges for Thomson. Despite these past challenges, Thomson currently offers an attractive investment opportunity considering the outlook for its financial performance in the coming years and its present valuation.

Portfolio Advisory Group

September 7, 2010

Company Overview

Founded in 1934, Thomson has transformed itself over the last two decades from an old economy, print-based business into an electronic information provider serving professionals in the financial services, legal, tax & accounting, and healthcare & science sectors. Thomson was previously built on a group of newspaper holdings around the world, and over the years has held investments in various businesses including North Sea oil and leisure travel. In the 1990s, the company became increasingly focused on information services for professionals

and made advances in this area through a series of acquisitions. With the divestiture of its newspapers and other non-core businesses, Thomson has migrated into a digital professional information franchise with approximately 90% of its revenues being electronic-based and 86% recurring through subscription-based customer relationships. In April 2008, Thomson’s acquisition of Reuters significantly increased the company’s exposure to the financial services industry, which now represents over half of the company’s revenues.

Woodbridge, the investment holding company of the Thomson family, owns around 55% of Thomson’s shares.

Thomson is organized into two divisions: (i) Markets, which consists of financial services and Media, and (ii) Professional, which consists of Legal, Tax & Accounting, and Healthcare & Science segments.

Markets accounts for 58% of Thomson’s total revenues and 48% of its operating profit. This unit sells information, supporting technology, and infrastructure to the financial services industry with customers such as investment banks, brokerage houses and fund managers. Primary drivers of this business include: employment in the financial services industry, market volatility which drives

0%

25%

50%

75%

100%

125%

150%

175%

200%

Jan-

00

Jul-0

0

Jan-

01

Jul-0

1

Jan-

02

Jul-0

2

Jan-

03

Jul-0

3

Jan-

04

Jul-0

4

Jan-

05

Jul-0

5

Jan-

06

Jul-0

6

Jan-

07

Jul-0

7

Jan-

08

Jul-0

8

Jan-

09

Jul-0

9

Jan-

10

Jul-1

0

Pric

es re

base

d to

Jan

1, 2

000

Thomson (C$) Thomson (US$) S&P 500 TSX

Relative Price Performance (2000-2010)

Source: Bloomberg

transaction and data volumes, and the long-term trend towards increased automated trading. In 2010, performance of the Markets division continues to suffer. This is in part due to the lag effect of Thomson’s subscription-based model, which is still picking up the cancellation trends of 2009.

The Professional division is less cyclical than Markets and has offered a buffer for company-wide results during periods of economic weakness. The Professional division is segmented into three units: Legal (28% of company-wide 2009 revenues), Tax & Accounting (8%), and Healthcare & Science (6%). The Legal unit has focused on the U.S. market because of the lower margins in international markets due to multiple jurisdictions and related inefficiencies. Key drivers for this division are employment in the

legal profession and increased litigation activity. Law firms represent 60% of the Legal unit’s revenues, government 19%, academic 13% and corporate 8%. Over the longer term, growth has been in the mid-single digits. Tax & Accounting and Heathcare & Science are smaller contributors but nonetheless represent nearly $2 billion in revenues. These units have been pillars of strength in the recent recession with 2009 revenues up 8.6% and 5.7%, respectively, year over year.

Investment Highlights

Attractive Business ModelThomson’s business model exhibits a number of attractive characteristics. The company is well diversified by geography with access to important

Markets Division58%

ProfessionalDivision

42%

Revenues By Division (2009)

Print / CD10%

Electronic,Software

& Services90%

Revenues By Media (2009)

Europe, Middle East &Africa30%

Asia11%

Americas59%

Revenues By Region (2009)

Recurring86%

Non-recurring

14%

Revenues By Type (2009)

Source: Company Reports

growth markets in Asia and the Middle East. The subscription-based model means repeat business from most customers each year enhancing the predictability of revenues. Thomson has #1 or #2 industry positions in most sectors, and its Markets and Legal units essentially compete against only one large competitor each, resulting in near duopolies. Finally, it requires substantial infrastructure to establish a business like Thomson’s, making it difficult for new competitors to enter the industry with products of similar quality.

Strong Financial Track Record The resilience of Thomson’s business model is reflected in its strong financial results. The company has consistently delivered positive net profits even through the slowdown of the early 2000s and the recession of 2008/09.

Reuters Acquisition Set To Realize Significant Cost SavingsCost savings from the consolidation of data centers, networks and product suites has led Thomson to target synergies of $1.2 billion from Reuters and total cost savings from all initiatives of $1.6 billion from 2008 to year-end 2011. To achieve these savings, Thomson has had to incur upfront one-time charges that have been around $500 million per year for each of 2008 through 2010. These one-time charges are expected to drop to $125 million in 2011. As they fade away and the full impact of recurring costs savings come to fruition, significant earnings power should be unleashed, as reflected by the consensus outlook below.

Conservative LeverageThomson has maintained a conservative approach to debt levels over the years and currently has a manageable level of leverage as reflected by investment grade credit ratings of A- (Stable) by Standard & Poor’s and Baa1 (Stable) by Moody’s. This conservative level of leverage has allowed Thomson to advance its acquisition strategy even in the tough environment of 2009, when it completed 31 acquisitions.

History of Growing DividendsThomson has been a consistent dividend grower and targets a conservative payout ratio of 40% of free cash flow. Looking forward, RBC Capital Markets expects mid to high single-digit dividend increases in 2011 and 2012. The current dividend yield is 3.2%.

Valuation A common measure for assessing the value of media companies is to look at the company’s “Enterprise Value” (sum of equity market cap and net debt) as

Source: Capital IQ; 2010 based on latest quarter annualized

Source: RBC CM

compared to operating profit before depreciation and amortization (“EBITDA”). This is known as EV/EBITDA.

For Thomson, the historical range of EV/EBITDA is 9.5-12.5x post the tech bubble burst and prior to the financial crisis of late 2008 / early 2009. The business today trades at 9.5x, which is an attractive level as compared to the historical range. Every 0.5x increase in the multiple translates to approximately $3 of value per share.

Risks

Foreign ExchangeThomson reports in U.S. dollars and generates approximately two thirds of its revenues from U.S. dollar sources. Other major currency exposures include the Euro and the British pound. Therefore, despite its Canadian roots and inclusion in the S&P/TSX Composite Index, Thomson can also be thought of as a U.S. stock. For Canadian investors, translation of the U.S. dollar stock price back into Canadian dollars is an important consideration.

Revenue Trends Challenging in 2010Thomson’s subscription-based model improves the predictability of its earnings; however, the 1-3 year duration of contracts makes 2010 a tough year because revenue trends are still facing headwinds from 2009 cancellations.

A key area of investor focus in recent quarters has been the return to positive revenue growth. Management currently expects this to occur in Q3/10 versus some time in H2/10 as previously indicated. In Professional, net sales were up double digits in Q2/10. In Markets, net sales remained negative in Q2/10. Regardless, net sales in Markets were the strongest since Q3/08 and were positive and accelerating in May and June.

Exposure to The Cyclicality of Financial MarketsAs with most media companies, Thomson’s costs are largely fixed (approximately 70%), which means that a modest decline in revenues can have a meaningful impact on profits. The potential for a double-dip recession, its impact on equity markets and hence financial services employment could have a meaningful impact on the Markets division.

Professional Division HeadwindsWhile typically less cyclical, the Legal unit faced a small revenue decline in 2009 as law firms struggled with a

protracted recession that led to a significant decline in legal billings and layoffs. In Q1/10 headcount declines were still being observed at U.S. law firms. However, the industry is stabilizing with Thomson’s recent “Law Firm Leaders” survey showing 60% of participants expecting current year billings to be up from last year. Net sales in Legal were trending positively in Q2/10 providing an encouraging sign that mitigates this risk.

Product Launch Execution RiskThomson has a variety of new product launches in 2010, which presents some execution risk in the near term. While the launch of WestlawNext (Legal) is progressing well, Eikon (Markets) is a second half of 2010 roll out and could become a 2012 story rather than a 2011 driver of performance depending on clients’ IT adoption cycle.

European Union ExaminationIn November 2009, the European Union launched a formal anti-trust proceeding against Thomson to investigate the company’s practices in the area of real-time datafeeds. The primary issue of concern is whether Thomson’s customers or competitors are prevented from translating certain codes used with Reuters and hence impair competition. There is no deadline for completing the investigation. The datafeeds component of Thomson’s business represents about 5% of total company revenues.

Scenario Analysis

The Thomson story hinges on two broad themes. The first is the cost savings to be achieved in the year or so ahead stemming from the Reuters acquisition. The second is the impact of market volatility and risk regarding financial sector employment, which threatens to delay the realization of the long-term story.

While Thomson’s business model is resilient, a decline in equity markets and hence employment in the financial services industry could have a significant impact on the performance of the stock. To help frame the range of outcomes, below are three scenarios:

1. Nodoubledip:A modest but sustainable global economic recovery with modest employment growth unfolds and earnings from operations see double digit growth from 2009 to 2012. Under this scenario, RBC Capital Markets would expect the stock to exit 2010 in the low US$40s, approaching US$50 over the next 18-24 months.

2. U.S.economicslowdown:The U.S. falls back into a mild recession with tactical layoffs, while the global economy holds a path towards a sustainable but sluggish recovery. Under this scenario, RBC Capital Markets would expect the stock to trade in the mid-US$30s pending improved macro visibility.

3. Globalrecession:The global economy falls back into recession leading to a widespread contraction in the financial services industry. Under this scenario, RBC Capital Markets would expect the stock to trade in the high US$20s / low US$30s pending improved macro visibility.

Summary

Thomson offers investors a strong business model with end market diversification and high customer renewal rates that have delivered consistently profitable results over the cycles. The duopoly structure of the Markets and Legal segments delivers pricing power that was apparent even in the challenging market conditions of the last two years. Management’s conservative approach to leverage has ensured that Thomson can manage through weak economic conditions and still invest for the future as seen with continued spending to drive new product launches in 2010. Earnings are expected to show significant growth next year as the full effect of Reuters synergies are realized and one-time integration costs fade away. The key market catalyst for Thomson is a return to positive revenue growth which management expects in the third quarter of 2010. In addition to the potential for capital appreciation based on earnings growth and potentially higher valuation multiples, investors are paid to wait with a dividend yield of 3.2%.

An analyst’s “sector” is the universe of companies for which the analyst provides research coverage. Accordingly, the rating assigned to a particular stock represents solely the analyst’s view of how that stock will perform over the next 12 months relative to the analyst’s sector.

Ratings:

Top Pick (TP): Represents best in Outperform category; analyst’s best ideas; expected to significantly outperform the sector over 12 months; provides best risk-reward ratio; approximately 10% of analyst’s recommendations.

Outperform (O): Expected to materially outperform sector average over 12 months.

Sector Perform (SP): Returns expected to be in line with sector average over 12 months.

Underperform (U): Returns expected to be materially below sector average over 12 months.

Risk Qualifiers (any of the following criteria may be present):

Average Risk (Avg): Volatility and risk expected to be comparable to sector; average revenue and earnings predictability; no significant cash flow/financing concerns over coming 12-24 months; fairly liquid.

Above Average Risk (AA): Volatility and risk expected to be above sector; below average revenue and earnings predictability; may not be suitable for a significant class of individual equity investors; may have negative cash flow; low market cap or float.

Speculative (Spec): Risk consistent with venture capital; low public float; potential balance sheet concerns; risk of being delisted.

Distribution of Ratings, Firmwide

For purposes of disclosing ratings distributions, regulatory rules require member firms to assign all rated stocks to one of three rating categories−Buy, Hold/Neutral, or Sell−regardless of a firm’s own rating categories. Although RBC Capital Markets’ stock ratings of Top Pick/Outperform, Sector Perform and Underperform most closely correspond to Buy, Hold/Neutral and Sell, respectively, the meanings are not the same because our ratings are determined on a relative basis (as described above).

In the event that this is a compendium report (covers six or more subject companies), RBC Dominion Securities may choose to provide specific disclosures for the subject companies by reference. To access current disclosures, clients should refer to: http://www7.rbccm.com/GLDisclosure/PublicWeb/DisclosureLookup.aspx?EntityID=1 or send a request to RBC Dominion Securities, Attention: Manager, Portfolio Advisory Group, 155 Wellington Street West, 17th floor, Toronto (Ontario) M5V 3K7.

Dissemination of Research

RBC Capital Markets endeavours to make all reasonable efforts to provide research simultaneously to all eligible clients. RBC Capital Markets’ equity research is posted to our proprietary websites to ensure eligible clients receive coverage initiations and changes in rating, targets and opinions in a timely manner. Additional distribution may be done by the sales personnel via email, fax or regular mail. Clients may also receive our research via third party vendors. Please contact your investment advisor or institutional salesperson for more information regarding RBC Capital Markets research.

Important DisclosuresA member company of RBC Capital Markets or one of its affiliates managed or co-managed a public offering of securities for Thomson Reuters Corporation in the past 12 months. A member company of RBC Capital Markets or one of its affiliates received compensation for investment banking services from Thomson Reuters Corporation in the past 12 months.

RBC Dominion Securities Inc. makes a market in the securities of Thomson Reuters Corporation and may act as principal with regard to sales or purchases of this security. Royal Bank of Canada, together with its affiliates, beneficially owns 1 percent or more of a class of common equity securities of Thomson Reuters Corporation. A member company of RBC Capital Markets or one of its affiliates received compensation for products or services other than investment banking services from Thomson Reuters Corporation during the past 12 months. During this time, a member company of RBC Capital Markets or one of its affiliates provided non-securities services to Thomson Reuters Corporation.

RBC Capital Markets is currently providing Thomson Reuters Corporation with non-securities services. RBC Capital Markets has provided Thomson Reuters Corporation with investment banking services in the past 12 months. RBC Capital Markets has provided Thomson Reuters Corporation with non-securities services in the past 12 months.

A member of the Board of Directors of the Royal Bank of Canada is a member of the Board of Directors or is an officer of Thomson Reuters Corporation.

The author(s) of this report are employed by RBC Dominion Securities Inc., a securities broker-dealer with principal offices located in Toronto, Canada.

Distribution of ratings, firmwideRBC Capital Markets

The information contained in this report has been compiled by RBC Dominion Securities Inc. (“RBCDS-Canada”) from sources believed by it to be reliable, but no representations or warranty, express or implied, is made by RBCDS-Canada or any other person as to it accuracy, completeness or correctness. All opinions and estimates contained in this report constitute RBCDS-Canada’s judgment as of the date of this report, are subject to change without notice and are provided in good faith but without legal responsibility. This report is not an offer to sell or a solicitation of an offer to buy any securities. RBCDS-Canada and its affiliates may have an investment banking or other relationship with some of all of the issuers

mentioned herein and may trade in any of the securities mentioned herein either for their own account or the accounts of their customers. RBCDS-Canada and its affiliates also may issue options on securities mentioned herein and may trade in options issued by others. Accordingly, RBC-DS Canada or its affiliates may at any time have a long or short position in any such security or option thereon. The securities discussed in this report may not be eligible for sale in some states or in some countries. Neither RBCDS-Canada or any of its affiliates, nor any other person, accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or the information contained herein. Any U.S. recipient of this report that is not a registered broker-dealer or a bank acting in a broker or dealer capacity and that wishes further information regarding, or to effect any transaction in, any of the securities discussed in this report, should contact and place orders with RBC Capital Markets Corporation, a U. S. registered broker-dealer affiliate of RBC-DS Canada, at (212) 361-2619, which without in any way limiting the foregoing, accepts responsibility (within the meaning, and for the purposes, of Rule 15a-6, under the U. S. Securities Exchange Act of 1934), for this report and its dissemination in the United States. This report may not be reproduced, distributed or published by any recipient hereof for any purpose.